Sample Category Title

GBP/USD Lower as BoE Holds Rates

The British pound is lower on Thursday. GBP/USD is trading at 1.2683 in the North American session at the time of writing, down 0.29% on the day. The Bank of England held rates at today’s meeting, as expected. There are no releases out of the US today.

Bank of England stays pat

There were no surprises as the Bank of England maintained interest rates at today’s meeting. The BoE kept the benchmark rate unchanged at 5.25% for a eighth straight time. Ahead of the meeting, the money markets had priced the likelihood of a hold at 95%.

The Monetary Policy Committee voted 7-2 in favor of a hold, with two members voting for a quarter-point cut. This result was expected by the markets and was a repeat of the vote at the previous meeting in May. This is a 16-year high but the central bank remains reluctant to cut rates due to concerns over inflation.

The good news was that the inflation rate fell to 2% in May, the first time that the BoE has met its 2% target in almost three years. However, the BoE was less happy about services inflation, which remained extremely high at 5.7% in May. This was down slightly from 5.9% in the previous report but above the market forecast of 5.5%. The rate statement noted that services inflation remained high.

Political considerations likely played a role in the BoE’s decision. The UK is in the midst of an election campaign and is keen not to be seen as interfering in the election. A rate cut at this sensitive time might have been viewed as helping Prime Minister Sunak, whose Conservative Party is trailing badly in opinion polls. Had the BoE trimmed rates, Sunak would have been quick to take credit for the cut and saying it proved that the government’s economic policy was working. Unfortunately for Sunak, the next BoE meeting isn’t till after the election in August.

GBP/USD Technical

- GBP/USD pushed below support at 1.2717 and 1.2695 earlier and is putting pressure on support at 1.2670

- There is resistance at 1.2742 and 1.2764

Euro on Firmer Footing ahead of Flash PMIs as French Risks Subside

- Euro rebounds as French election fears ease

- June PMIs to come into the spotlight amid more cautious ECB

- Flash estimates are due on Friday at 08:00 GMT

Calmer week for the euro after French turmoil

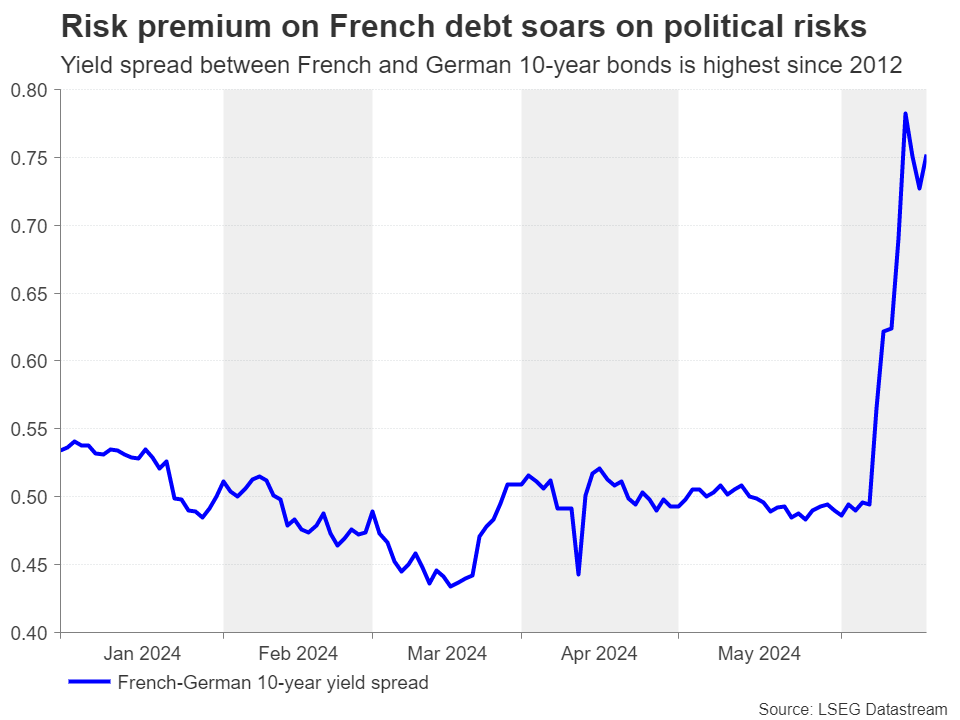

European assets are having a better week following the market panic sparked by the rise of the far right across the continent in the European Parliament elections on June 9. But the biggest shockwave came from French President Emmanuelle Macron’s decision to call a snap legislative election the following day, raising fears that Marine Le Pen’s far-right National Rally party would repeat its success on a national level.

The threat of a far-right government in the Eurozone’s second largest economy raised fears of another debt crisis in the bloc, or at the very least, some kind of a market fallout on the scale seen in the UK from Liz Truss’s mini-budget. Investors’ biggest worries from a Le Pen government are the party’s protectionist policies and its calls for increased public spending.

French jitters ebb, for now

But after the panic-induced selloff in French stocks and bonds, as well as the euro, the National Rally appears to be backtracking on some of the party’s more controversial policies. Moreover, Le Pen has vowed to work with Macron rather than force his resignation.

Subsequently, market jitters have calmed somewhat and the risk premium on French debt has also fallen slightly. The spread between French and German 10-year government bond yields spiked to the highest since 2012 as the French political drama unfolded, but for now, a major crisis appears to have been averted and the focus is once again on ECB rate cut expectations.

ECB rate cut expectations pared back

On its part, the European Central Bank steered clear of getting caught up in France’s domestic politics, but there were subtle warnings that neither would it stand idle should widening yield spreads become problematic.

Meanwhile, ECB policymakers have been out and about since the June 6 policy decision when rates were slashed, casting doubt on the prospect of back-to-back rate cuts. Most seem to be in favour of one cut per quarter, with the markets pricing in somewhere between one and two additional 25-bps cuts for the remainder of the year.

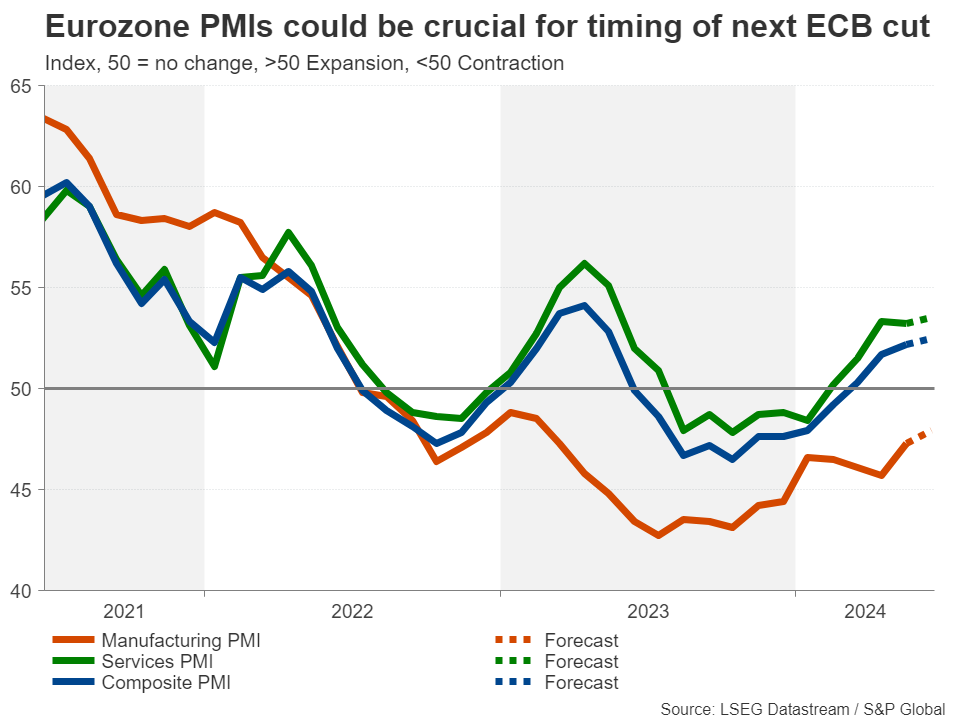

Eurozone economy on the mend

How the economy performs over the coming months will be crucial as to how rate-cut expectations shape out. The Eurozone economy picked up some momentum in the first quarter of 2024 and the composite PMI climbed to the highest in a year in May.

Forecasts point to a further improvement in June’s flash estimates. The services PMI is expected at 53.5 versus 53.2 in May, and the manufacturing PMI is projected to come in at 47.9 from the prior 47.3. The composite PMI is expected to tick up to 52.5 in June.

Investors will also likely be scrutinizing the details of the PMI surveys, particularly on employment, amid still elevated wage growth, and on price pressures. With a follow-up rate cut in September only 60% priced in, a soft set of PMI numbers, or signs of a cooling off in inflation, would boost those odds, weighing on the euro.

Can the euro restore its uptrend?

The single currency recently slipped below its short-term ascending trendline against the US dollar, falling below its 50- and 200-day moving averages (MA) too. Further losses could lead to a re-test of the April low of $1.0599.

However, if the PMIs show a strengthening recovery or an unfavourable trend in inflation, the euro could extend its latest rebound by climbing back above the 200-day MA, bringing into scope the June top of $1.0915.

In the event that the PMI data fails to shed some light on the ECB policy path, investors will turn their attention to the flash CPI readings due on July 2.

Gold & Silver Test Two-Week Highs on Geopolitical Concerns and Rate Cut Optimism

Key Points:

- Geopolitics return to the fore as concerns mount around the Middle East and Asia..

- Safe haven demand sees gold (xau/usd) rise toward 2350 resistance.

- Silver technicals hint at the potential for further upside.

Commodity markets have returned to positive territory this morning, driven by gains in both silver (XAG/USD) and gold (XAU/USD). Growing concerns about the Middle East and a potential escalation seem to have renewed safe-haven demand following the U.S. holiday yesterday.

Safe haven demand appeared to have waned toward the back end of last week but news of a potential escalation on the northern border between Lebanon and Israel has market participants on edge. The idea of a wider conflict could significantly impact global growth and have an impact on the ongoing fight against inflation.

Furthermore, Russian President Vladimir Putin is in Asia and held meetings with both North Korean and Vietnamese leadership. This is seen as a further escalation in Asia as the G7 looks to reign in China’s influence and support allies in the region. All of these factors over the past few days definitely seem to be having an impact on the risk outlook and thus leading to a renewed demand in haven assets.

Another reason that may be contributing to a rise in both gold and silver prices could be the renewed optimism for rate cuts from the Federal Reserve. The stark decline in retail sales data earlier in the week continued a trend of softening data with the exception of the NFP print earlier in June. We are seeing some signs of strength from the US dollar in the early part of the European session and it will be interesting to gauge whether this continues. If the US dollar continues to appreciate throughout the day will it be able to halt the rally in both gold and silver? This question will be key to the movement of gold prices today and potentially tomorrow as well.

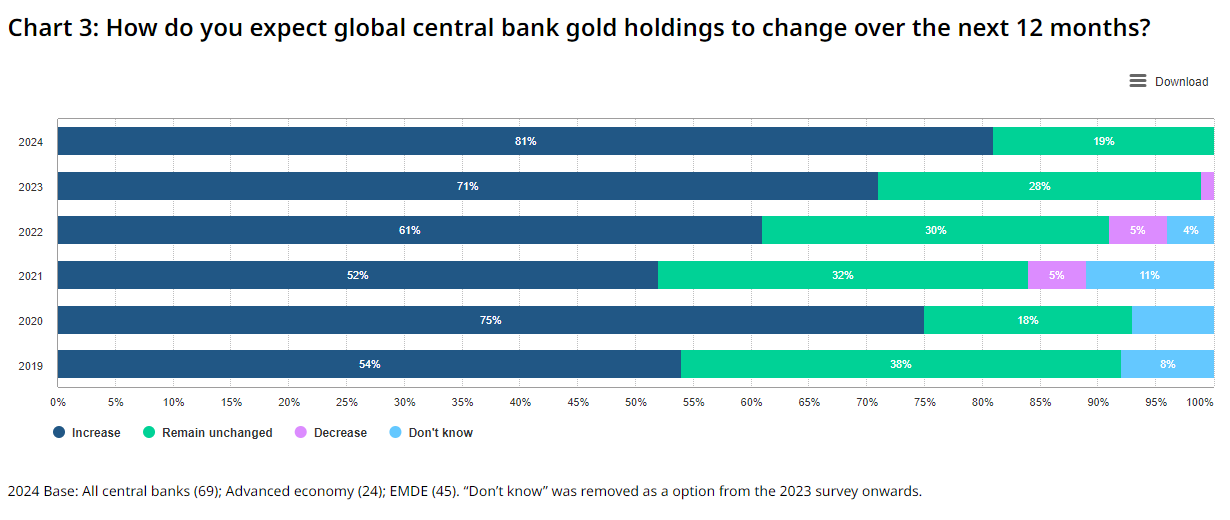

Looking at other reasons that continue to keep buyers interested in the precious metal is the ongoing purchases of the gold by various central banks. According to a World Gold Council report dated June 18, 2024, an increasingly complex geopolitical outlook is making gold the go to for central banks. According to a 2024 Central Bank Gold Reserves (CBGR) survey, conducted among 70 central banks between February 19, 2024 and April 30, 2024, 29% of the central banks intend to increase their gold reserves in the next 12 months. This provides central banks to hedge against geopolitical uncertainty and in the case of some, sanctions as well.

A view of the responses of central banks on gold holdings over the next 12 months

Source: World Gold Council (click to enlarge)

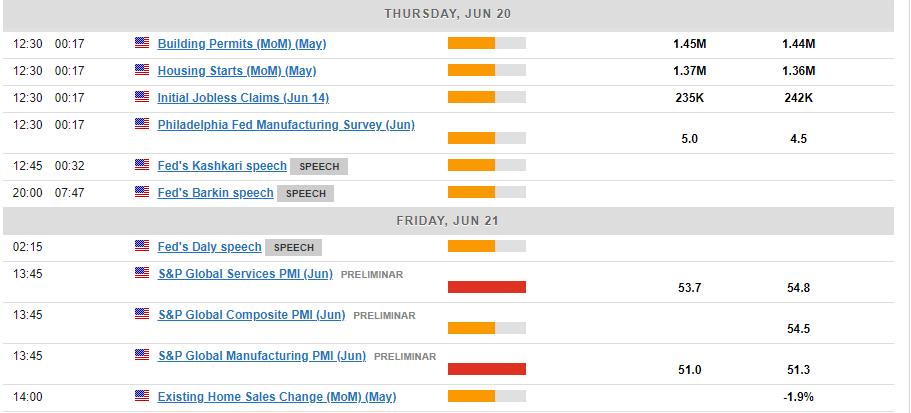

The Look Ahead

Later in the day we have a swathe of low impact US data with the main attractions coming in the form of comments from Federal Reserve policymakers Kashkari and Barkin. The comments by Fed policymakers could stoke some short-term volatility in the US dollar and by extension gold and silver as well. To wrap up the week we have US PMI data to be released tomorrow which could give us further insight into the service sector as well as the US manufacturing sector moving forward.

Technical Outlook

Gold Technical Outlook

Gold prices continue to experience whipsaw price action as the 2300 level continues to provide stern support. This is evidenced by the lack of follow through after the precious metal recorded a daily candle close beneath the 2300 support level on June 7.

Gold has since been on a steady march higher printing higher highs and higher lows on its way to the 2350 resistance level. Looking at the H4 chart below, this morning’s bullish run failed to recapture the 2350 handle, facing selling pressure in the 2344-2345 region.

Source: TradingView.com (click to enlarge)

Key Areas to Pay Attention to:

Support

- 2331 (weekly open)

- 2320

- 2300

Resistance

- 2345

- 2358

- 2370

Silver Technical Outlook

Silver on the other hand provided a very clean technical trade idea yesterday after 4 successive days of sideways price action. The bounce of the ascending trendline (which added a further confluence) has seen silver prices approach a two-week high.

There is a descending trendline ahead which could hold the keys to silver’s next move. A break above the trendline could set silver on course for a retest of the previous highs. Alternatively, a rejection of the trendline could lead to a return toward support around the 28.87 handle.

Silver daily chart, June 20, 2024

Source: TradingView.com (click to enlarge)

Sunset Market Commentary

Markets

The Bank of England was one of the three central bank highlights today. The Norges Bank and the Swiss National Bank outcomes are in the section down below. Threadneedle Street kept the policy rate unchanged at 5.25% in a 7-2 vote with two members voting for a cut (Dhingra and Ramsden). The policy statement contained little added value with a lot of “yes, but’s”. Following on the opening paragraph, the BoE noted inflation on a headline level falling to 2% in May. Services CPI eased less than expected (5.7%) but this was in part technical and due to volatile items. Key indicators of inflation persistence, while still elevated, have continued to moderate. Q1 GDP turned out stronger than expected and growth will probably top expectations for the first half of this year. But the BoE sees business surveys pointing at a slower pace of underlying growth. The central bank concluded with a statement similar to May that it “will consider all of the information available and how this affects the assessment that the risks from inflation persistence are receding. On that basis, the Committee will keep under review for how long Bank Rate should be maintained at its current level.” With the next August (1) meeting one being with new forecasts, the stakes are probably higher this time around. To that end it’s worth noting how the 7-2 vote actually hides a three-way internal divide. Back in May, the meeting minutes described the risk assessment made by the seven policymakers in one paragraph, treating them as one group supporting the status quo for shared reasons. Today, however, the pack of seven was split up in a more hawkish team that wants more evidence of diminishing inflation persistence and a neutral team for whom the status quo was a “finely balanced” decision. Risks are that barring a material upside inflation or economic activity surprise, one or more members may soon join Dhingra and Ramsden’s camp. This was probably the reason for the kneejerk drop in UK gilt yields and sterling. Both recovered afterwards though. Yields currently change less than 2 bps across the curve. EUR/GBP ekes out some gains to trade around 0.8455 currently.

US yields trade 3.4 and 5.4 bps higher in their reopening after yesterday’s Juneteenth holiday. Economic data would have suggested otherwise though with weekly jobless claims (238k), housing data and the Philly Fed business outlook indicator all coming in to the downside of expectations. The jury’s out whether to call it a bottoming out. German yields follow in lockstep with similar-sized gains in a news poor session. EUR/USD loses ground towards 1.072 despite a constructive risk environment.

News & Views

After an inaugural 25 bps cut in March, the Swiss National Bank (SNB) today further reduced its policy rate from 1.50% to 1.25%. Markets were highly divided between a cut or an unchanged decision. Inflation has risen slightly since the March meeting (to 1.4% Y/Y in May), but the SNB sees underlying inflation easing owing to somewhat lower second-round effects. The SNB even after today’s rate cut marginally downwardly revised its inflation forecasts (1.3% 2024, 1.1% 2025 and 1.0% 2026), keeping it firmly within the 0%-2.0% price stability target range. The SNB expects Swiss growth to stay moderate in coming quarters (1.0% 2024), but medium term activity should improve gradually, supported by somewhat stronger demand from abroad (1.5% in 2025). The SNB noted that, after a decline earlier this year, the franc increased substantially mainly due to political uncertainty in Europe. This is causing uncertainty about inflation staying elevated. Monetary policy is taking that into account. The SNB remains prepared to be active in the FX market as necessary to keep monetary conditions appropriate. Comments suggest that potential unwarranted currency strength was a factor tilting the balance to a rate cut. The franc declined modestly post the SNB decision. EUR/CHF rebounded from 0.949 to 0.9545 currently.

The Norges Bank today as expected left its policy rate unchanged at 4.5%. Since March, inflation has been a little lower than projected, while unemployment increased as expected. On the other hand, enterprises report improved prospects and it wage growth will be higher than envisaged. This could mean that inflation will be higher than projected. The NB judges that the policy rate is sufficiently high to bring inflation to target within a reasonable time horizon, but that there will be a need to maintain a tight monetary policy stance for somewhat longer than previously projected. The NB now projects to policy rate to stay at current level till the end of the year. The Norwegian krone post the NB decision extended recent gains. EUR/NOK declines from 11.36 this morning to 11.29.

Graphs

EUR/NOK: krone appreciates after Norges Bank extends policy rate status quo to at least the end of the year

EUR/CHF: Swiss National Bank cuts rates to 1.25% with recent CHF strenghtening (probably) having tilted the balance

EUR/GBP: sterling shrugs at today’s Bank of England “yes, but” status quo decision

Nasdaq: opens with new record high with the likes of Nvidia extending its meteoric rise

Bank of England Review – August Rate Cut in Play

- At today's monetary policy meeting the BoE left the Bank Rate unchanged at 5.25% as widely expected.

- As we expected, the BoE retained much of its previous guidance but delivered a slight dovish twist, laying the groundwork for an August cut.

- Gilt yields tracked lower and EUR/GBP moved higher on the dovish twist, but overall the market reaction has been fairly muted.

As expected, the Bank of England (BoE) decided to keep the Bank Rate unchanged at 5.25%. The vote split was unchanged since the May meeting with 7 members voting for an unchanged decision and Dhingra and Ramsden voting for a cut.

The BoE stuck to its previous guidance in its statement noting that "monetary policy could remain restrictive even if Bank Rate were to be reduced, given that it was starting from an already restrictive level" and "the Committee will keep under review for how long Bank Rate should be maintained at its current level". The BoE downplayed the recent topside surprise to service inflation noting that it was partly due to annual price adjustments and volatile components. Likewise, the division in the "unchanged" camp has become more evident. The hawkish members noted that "more evidence of diminishing inflation persistence was needed before reducing the degree of monetary policy restrictiveness" whereas the other members noted that "the policy decision at this meeting was finely balanced". We think this opens the door for a shift towards a majority voting for a cut at the August meeting.

Before the next meeting on 1 August, we get a limited amount of data. Namely one jobs report for May/June and the inflation report for June. We expect the data releases to show further signs easing inflationary pressures and wage growth to level off, leaving the BoE comfortable enough to opt for a rate cut at the August meeting. Risks are however to a later start to the cutting cycle if we get a topside surprise to especially service inflation.

Rates. 2Y Gilt yields moved lower on the statement but overall, the reaction in rates markets was fairly muted. Markets shifted towards a front-loading of cuts with 16bp now priced for the August meeting.

FX. Following the release of the statement, EUR/GBP moved higher on the dovish twist from the statement. Overall, we see relative rates as a negative for GBP but note with risks to both growth and inflation tilted to the topside, this leaves a more challenging backdrop for an impending BoE cutting cycle. By extension and combined with the political uncertainty in France, this also acts as a downside risk to our EUR/GBP forecast of 0.88 in 6-12 months.

Our call. We continue to expect the BoE to deliver the first cut of 25bp in August with risks skewed towards a later start to a cutting cycle. We subsequently expect a 25bp cut in November, totalling 50bp of cuts for 2024. Markets are pricing 50bp for the remainder of the year with the first 25bp cut fully priced by September.

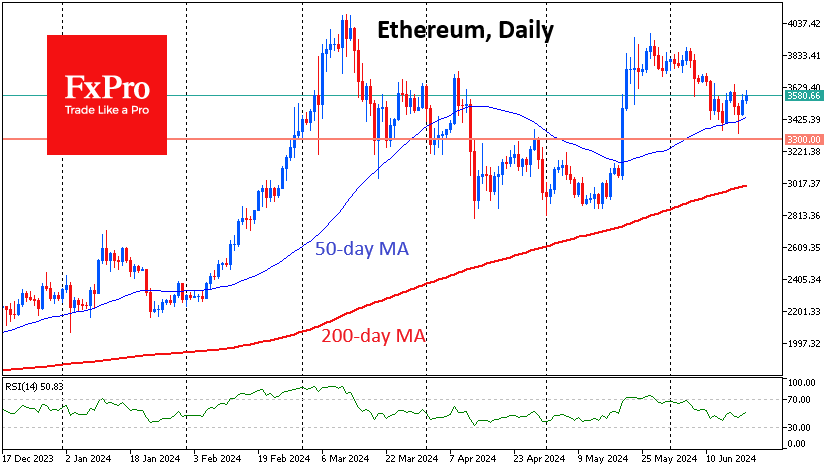

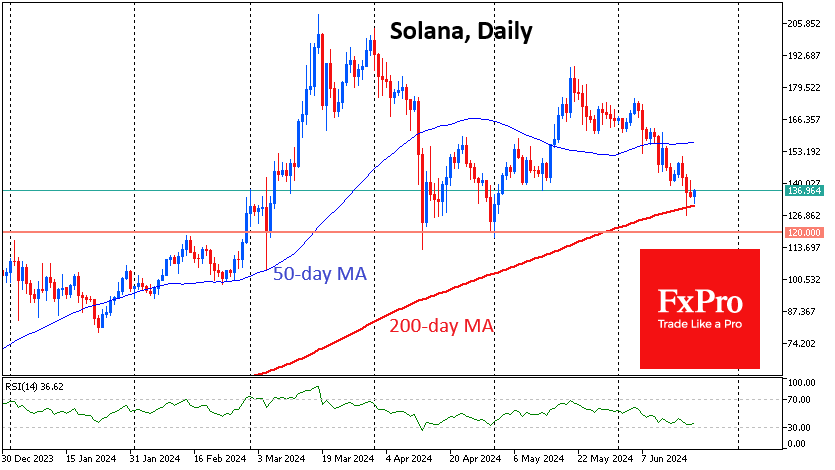

Ethereum and Solana Get Support

Market picture

The crypto market added 1% in 24 hours to $2.4 trillion, supported by positive momentum in Bitcoin (+0.9%) and interest in Ethereum (+2%). Top altcoins are mostly adding to the levels of the day before except for falling Solana (-1.6%), but it too has been rising over the last hours. Toncoin is adding 4.9% over a day and 14% in 30 days, second only to Ethereum (+16%) in the top 20.

Technically, Ethereum has already received its second support this month on the brief dip to the 50-day moving average. This looks like the market’s commitment to the bullish trend that started last month. The news trigger for the rise was speculation about the likely start of trading in spot ETFs on the coin from July 2nd.

Solana is probing support at the 200-day moving average. It managed to push back from this level to nearly $130. The focus now is on whether this rise will continue. This is the fourth time since March that the bulls have defended this area. But the very fact of constant returns to it speaks about the bears’ persistence.

News background

According to ETC Group, cryptocurrency hedge funds are reducing the share of bitcoin in their investment portfolios. Hedge fund investment in BTC has fallen to its lowest level since October 2020.

CryptoQuant noted that traders are in no hurry to replenish their BTC holdings, whale demand remains weak, and the volume of stablecoins is growing at the slowest pace since November 2023. Bitcoin has fallen below the aggregate breakeven level of speculators (~$65,800), which could trigger a continued decline to $60,000.

Santiment estimates that almost all major cryptocurrencies have entered the “undervalued” zone.

The US SEC has dropped its investigation into ConsenSys for recognising Ethereum sales as securities transactions. The SEC took the step after ConsenSys sent a letter asking for clarification of the asset class in approving spot ETH-ETFs.

Arkham pointed out that a German government-affiliated wallet transferred 6,500 BTC (~$425 million) to a new address, some of which ended up on exchanges. The move has raised fears in the community of negative consequences for the exchange rate of the first cryptocurrency.

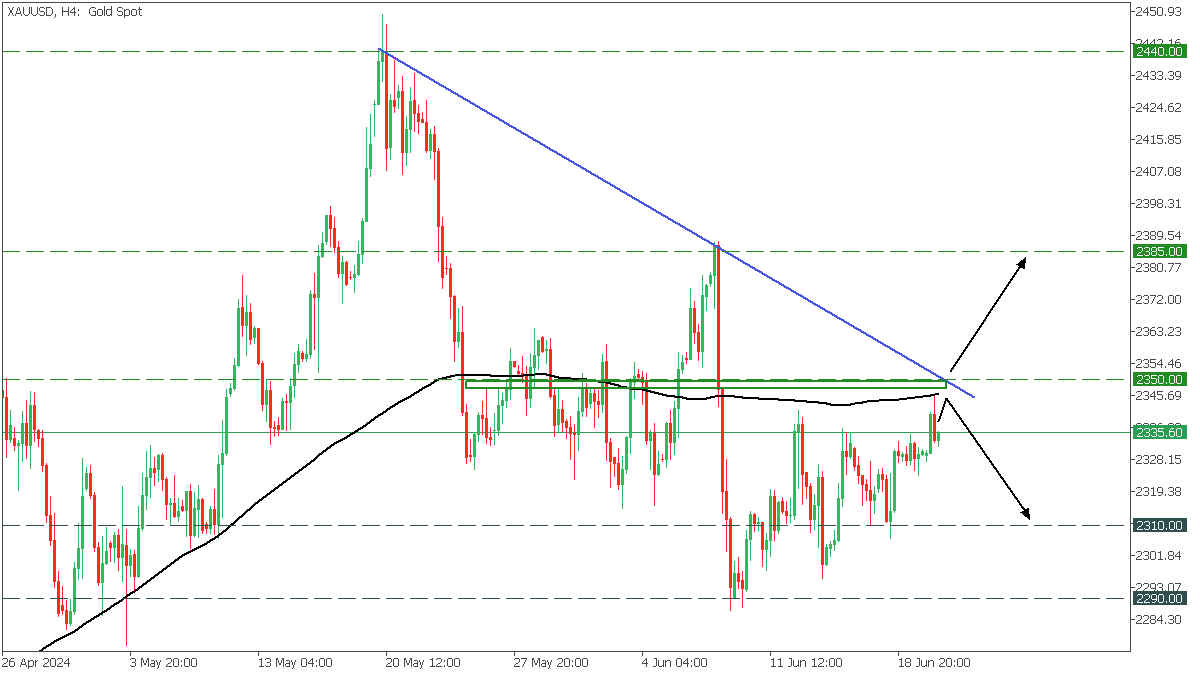

XAUUSD: Trend Breaking?

On the H4, XAUUSD reached a downtrend line after a short-term rise. The price is approaching the critical resistance area and MA200, which also acts as resistance. In this case, two scenarios are possible.

- If Gold breaks the resistance of 2350, the trend line and MA200, a bullish trend will start up to 2385;

- Otherwise, a rebound will drop XAUUSD back to 2310 support;

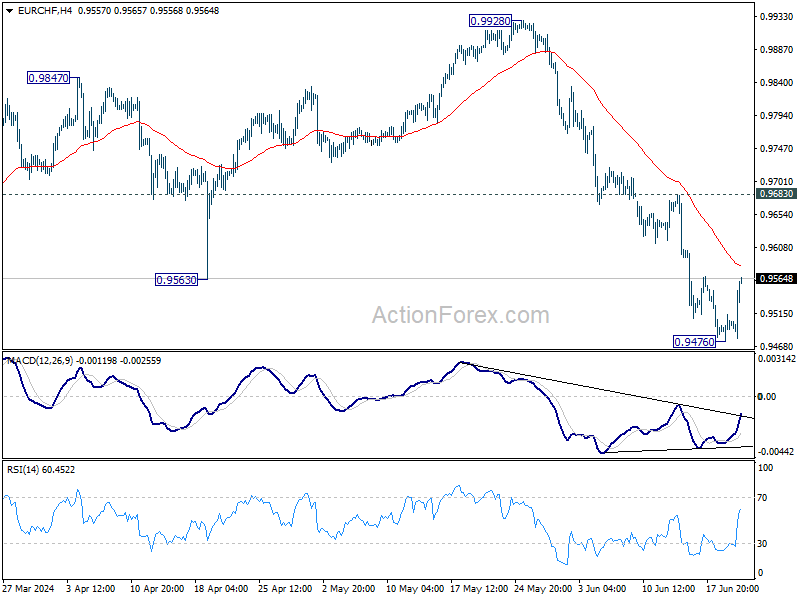

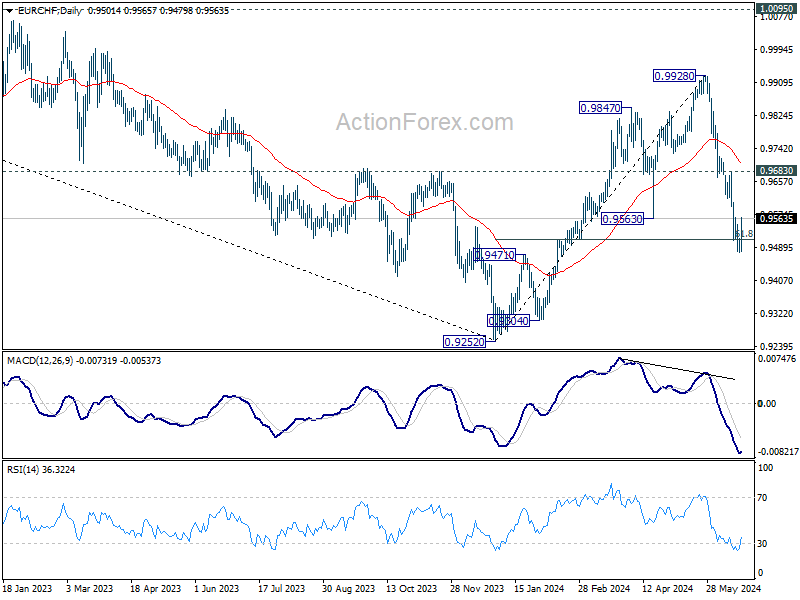

EUR/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9483; (P) 0.9499; (R1) 0.9520; More....

Intraday bias in EUR/CHF is turned neutral with current recovery, and some consolidations would be seen first. But outlook will stay bearish as long as 0.9683 resistance holds, and fall from 0.9928 is expected to resume later. Below 0.8476 will target 61.8% retracement of 0.9252 to 0.9928 at 0.9510. Sustained trading below there will raise the chance of long term down trend resumption, and target 0.9252 low next.

In the bigger picture, the break of 0.9563 support, as well as 55 W EMA (now at 0.9672) argues that rebound from 0.9252 has completed at 0.9928. Medium term bearish is maintained with both 1.0095 resistance intact. Firm break of 0.9252 will resume the down trend from 1.2004 (2018 high).

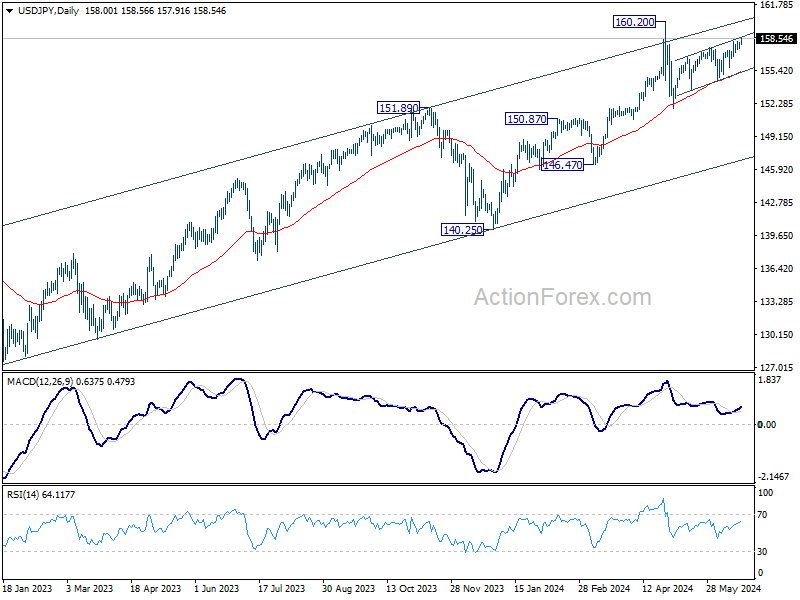

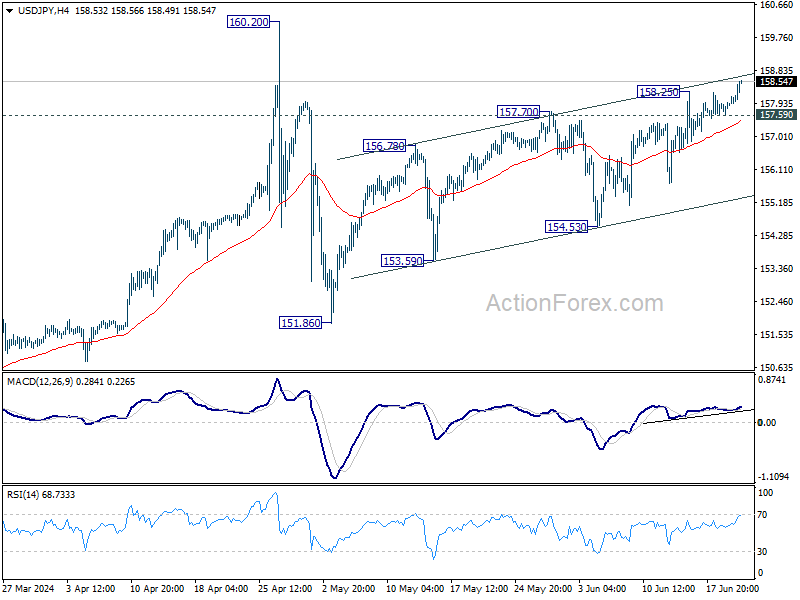

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 157.76; (P) 157.94; (R1) 158.27; More...

Intraday bias in USD/JPY is back on the upside with break of 158.25 temporary top. Choppy rise from 151.86 has resumed and is now targeting a retest on 160.20 high. But upside should be limited there, at least on first attempt. On the downside, below 157.59 minor support will turn intraday bias neutral first.

In the bigger picture, price actions from 160.20 medium term top are seen as a corrective pattern to rise from 150.25 only. Another rally is still expected at a later stage through 160.02 to resume the larger up trend. However, decisive break of 150.87 will argue that larger correction is possibly underway, and target 146.47 support next.