Sample Category Title

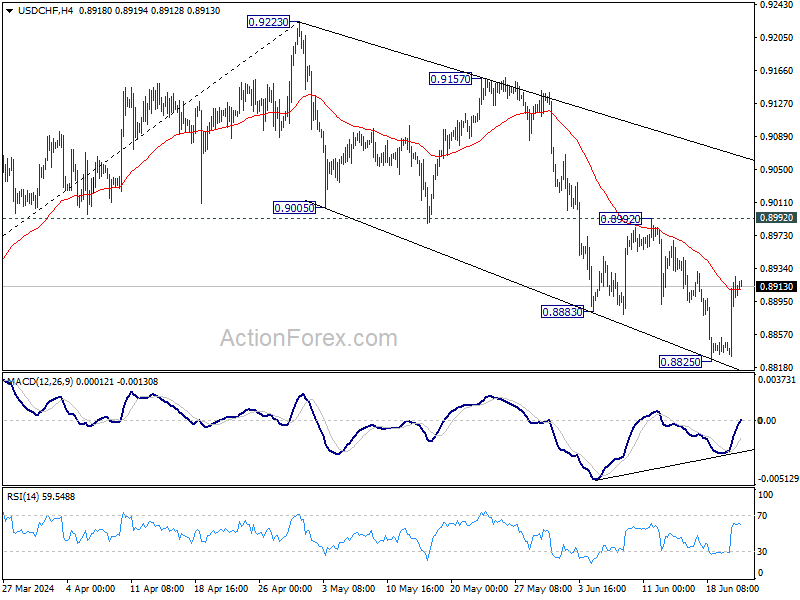

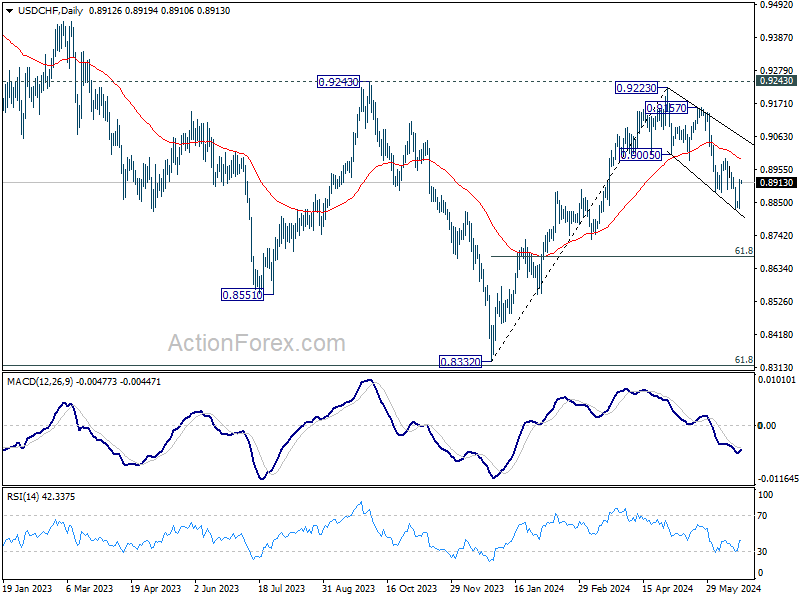

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8855; (P) 0.8891; (R1) 0.8949; More….

USD/CHF is staying in consolidation above 0.8825 and intraday bias remains neutral for the moment. Outlook will stay bearish as long as 0.8992 resistance holds. On the downside, break of 0.8825 will resume the fall from 0.9223. Next target is 61.8% retracement of 0.8332 to 0.9223 at 0.8672.

In the bigger picture, price actions from 0.8332 medium term bottom are seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance affirms this case, and maintains medium term bearishness. While more range trading could be seen between 0.8332/0.9243 first, downside break out is mildly in favor at a later stage.

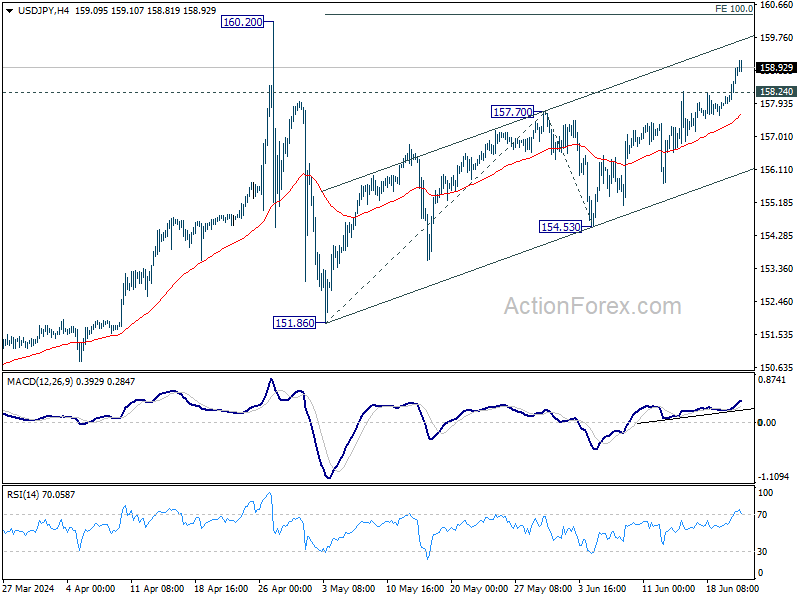

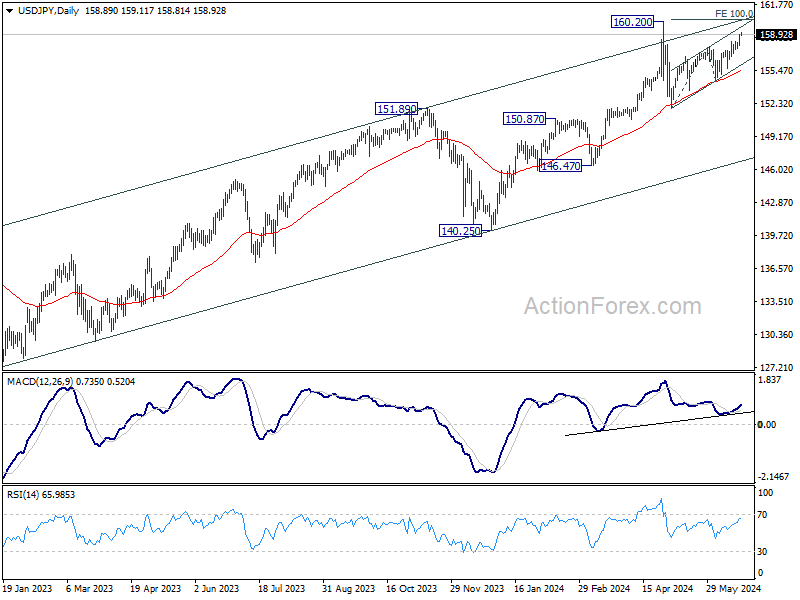

USD/JPY Daily Outlook

Daily Pivots: (S1) 158.25; (P) 158.59; (R1) 159.28; More...

USD/JPY's rise from 151.85 is still in progress and intraday bias stays on the upside. Further rally could be seen to 160.20 high, or possibly to 100% projection of 151.86 to 157.70 from 154.53 at 160.37. But upside should be limited there, at least on first attempt. On the downside, below 158.24 minor support will turn intraday bias neutral first.

In the bigger picture, price actions from 160.20 medium term top are seen as a corrective pattern to rise from 150.25 only. Another rally is still expected at a later stage through 160.02 to resume the larger up trend. However, decisive break of 150.87 will argue that larger correction is possibly underway, and target 146.47 support next.

Yen Approaches 160 Against Dollar, Will Japan Tolerate a Move to 165 or 170?

Yen is under intense scrutiny today as it continues a six-day losing streak, approaching the key psychological level of 160 against Dollar. This move comes despite Japan's core inflation reaccelerating in May, but failed to meet market expected pace. Additionally, core-core CPI, which excludes both food and energy, and services inflation both continued to decline. These mixed signals undermine the case for BoJ to consider raising interest rates again in July. Furthermore, BoJ has yet to clarify its stance on the tapering of bond purchases, adding to the market's uncertainty.

As the Yen edges closer to 160 per Dollar, a level often associated with intervention by Japanese authorities, comments from Japanese officials suggest a more hands-off approach. Masato Kanda, Japan's top currency diplomat, reiterated that the authorities are prepared to counter speculative and highly volatile moves in the currency markets. But more importantly, he emphasized that intervention is "not intended to change the market's trend." He added that as long as currency rates move stably in line with economic fundamentals, there is no need for intervention.

Kanda's comments could be interpreted by some that the authorities might tolerate further Yen depreciation, provided the movement is orderly and reflective of underlying economic conditions. So, Japan's reaction to USD/JPY at 160 in the next few days would be crucial to decide whether the intervention threshold has already moved up, say to 165 or 170.

In the broader currency markets, Australian Dollar is currently the strongest performer of the week, supported by RBA's indication that a rate hike remains on the table. Canadian Dollar is the second strongest, followed by Euro. Conversely, New Zealand Dollar is the second weakest, next to Yen. Sterling is the third worst, following BoE's suggestion that an August rate cut is back on the table. Swiss Franc, despite the pullback after SNB's rate cut, is positioned in the middle, maintaining most of the gains due to political instability in the EU. Dollar is also trading in the middle of the performance chart.

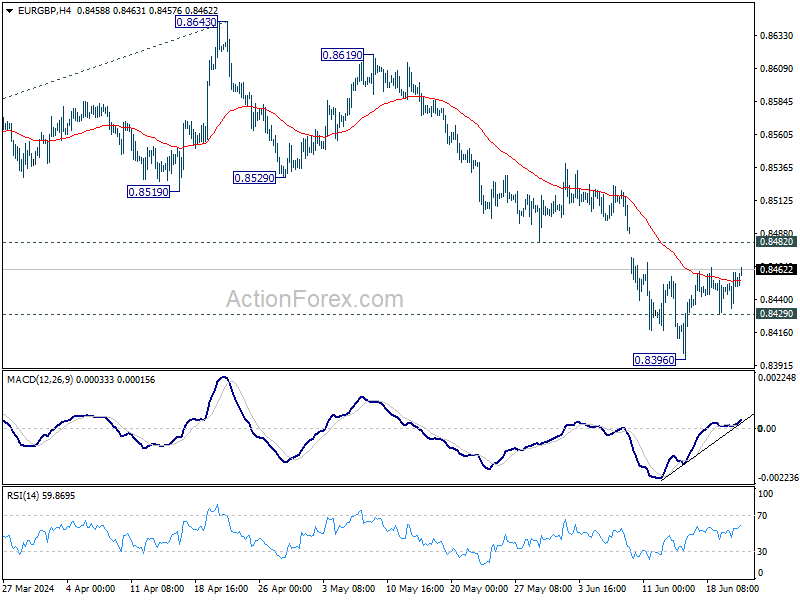

Technically, EUR/GBP is worth some attention today. While recovery from 0.8396 might extend higher, upside could be capped by 0.8482 support turned resistance. Break of 0.8429 minor support will argue that larger down trend is ready to resume through 0.8396. Nevertheless, decisive break of 0.8482 will confirm short term bottoming and bring stronger rebound. Reactions to today's UK retail sales and PMIs, as well as Eurozone PMIs could decide the next move.

In Asia, at the time of writing, Nikkei is down -0.02%. Hong Kong HSI is down -1.71%. China Shanghai SSE is down -0.36%. Singapore Strait Times is up 0.30%. Japan 10-year JGB yield is up 0.0303 at 0.986. Overnight, DOW rose 0.77%. S&P 500 fell -0.25%. NASDSAQ fell -0.79%. 10-year yield rose 0.037 to 4.254.

Japan's CPI core accelerates to 2.5%, but core-core slows to 2.1%

Japan's CPI core (ex-food) accelerated from 2.2% yoy to 2.5% yoy in May, slightly below the expected 2.6%. This marks the 26th consecutive month that core inflation has remained above BoJ's 2% target. However, the increase was primarily driven by a significant 14.7% yoy rise in electricity prices.

In contrast, CPI core-core (ex-food and energy) slowed from 2.4% yoy to 2.1% yoy. Additionally, services inflation eased from 2.5% yoy to 2.2% yoy. Headline CPI also rose from 2.5% to 2.8% yoy, marking its ninth consecutive month of deceleration and the lowest reading since September 2022.

BoJ Governor Kazuo Ueda has repeatedly suggested that a July rate hike is a possibility. However, today's report indicates that the inflation uptick is mainly due to cost-push factors, such as higher electricity prices, rather than increased demand. This might not provide a strong enough basis yet for BoJ to proceed with a rate hike at this time.

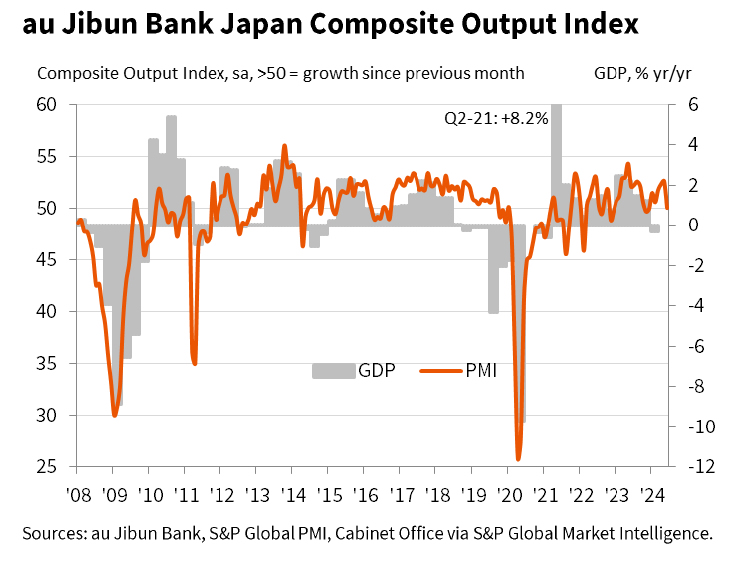

Japan's PMI composite falls to 50, mixed economic signals with rising costs

Japan's latest PMI data for June presents a mixed economic outlook. Manufacturing PMI slipped slightly from 50.4 to 50.1, falling short of expectations of 50.6. However, manufacturing output showed a positive shift, rising from 49.9 to 50.5, marking the first expansion in over a year. Conversely, Services PMI dropped sharply from 53.8 to 49.8, indicating fractional contraction for the first time since August 2022. As a result, Composite PMI fell from 52.6 to 50.0.

Jingyi Pan, Economics Associate Director at S&P Global Market Intelligence, commented that the private sector expansion has stalled midway through the year. The return of manufacturing output growth was overshadowed by a decline in services activity, partially due to labor constraints.

A notable concern is the "pressure on margins," with average input costs rising at the fastest pace in over a year while output price inflation softened, particularly in the service sector. Anecdotal evidence pointed to the weak yen and increasing labor costs as significant factors driving up cost inflation.

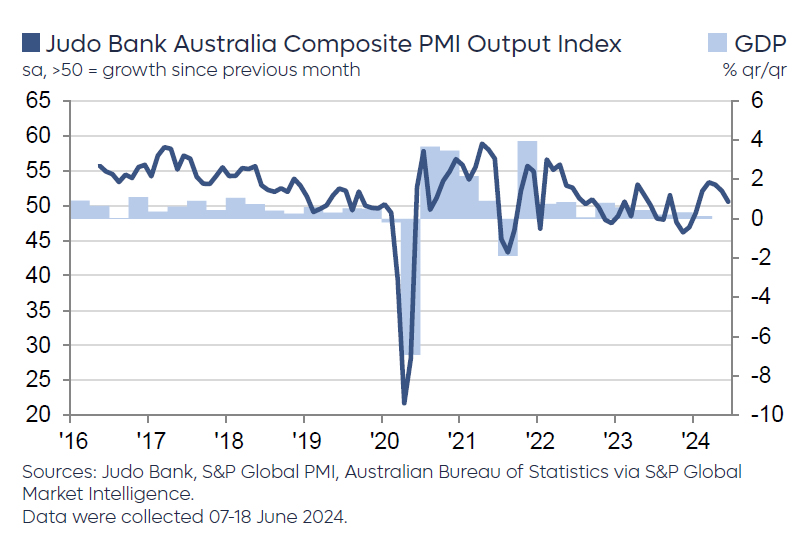

Australia's PMI composite falls to 50.6, slowing business expansion, manufacturing weakness

Australia's PMI data for June indicates a slowdown in business expansion, with Manufacturing PMI falling from 49.7 to 47.5, Services PMI dropping from 52.5 to 51.0, and Composite PMI decreasing from 52.1 to 50.6, hitting a five-month low.

Warren Hogan, Chief Economic Advisor at Judo Bank, noted that while business activity continues to grow, the pace of expansion has slowed compared to the strong performance in the first half of 2024.

The manufacturing sector showed significant weakness, with PMI, output, and new orders declining towards the cyclical lows of 2023, all falling below the 50 threshold that separates expansion from contraction. In contrast, the services sector experienced a slight pullback but remained in expansionary territory.

The composite input price index dropped below 60 for the first time since January 2021, suggesting that business cost growth is easing. Final prices also decreased but still indicate above-target inflation. Service sector price indicators retreated in June, aligning with the view that inflation is gradually easing in 2024, yet they remain above RBA's target range of 2-3%.

Looking ahead

UK will release retail sales and PMIs in European session. Eurozone PMIs will also be featured. Later in the day, Canada will publish retail sales, and IPPI and RMPI. US will release PMIs and existing home sales.

USD/JPY Daily Outlook

Daily Pivots: (S1) 158.25; (P) 158.59; (R1) 159.28; More...

USD/JPY's rise from 151.85 is still in progress and intraday bias stays on the upside. Further rally could be seen to 160.20 high, or possibly to 100% projection of 151.86 to 157.70 from 154.53 at 160.37. But upside should be limited there, at least on first attempt. On the downside, below 158.24 minor support will turn intraday bias neutral first.

In the bigger picture, price actions from 160.20 medium term top are seen as a corrective pattern to rise from 150.25 only. Another rally is still expected at a later stage through 160.02 to resume the larger up trend. However, decisive break of 150.87 will argue that larger correction is possibly underway, and target 146.47 support next.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:00 | AUD | Manufacturing PMI Jun P | 47.5 | 49.7 | ||

| 23:00 | AUD | Services PMI Jun P | 51 | 52.5 | ||

| 23:01 | GBP | GfK Consumer Confidence Jun | -14 | -16 | -17 | |

| 23:30 | JPY | National CPI Y/Y May | 2.80% | 2.50% | ||

| 23:30 | JPY | National CPI ex Fresh Food Y/Y May | 2.50% | 2.60% | 2.20% | |

| 23:30 | JPY | National CPI ex Food Energy Y/Y May | 2.10% | 2.40% | ||

| 00:30 | JPY | Manufacturing PMI Jun P | 50.1 | 50.6 | 50.4 | |

| 00:30 | JPY | Services PMI Jun P | 49.8 | 53.8 | ||

| 06:00 | GBP | Retail Sales M/M May | 1.50% | -2.30% | ||

| 06:00 | GBP | Public Sector Net Borrowing (GBP) May | 14.8B | 19.6B | ||

| 07:15 | EUR | France Manufacturing PMI Jun P | 46.8 | 46.4 | ||

| 07:15 | EUR | France Services PMI Jun P | 50 | 49.3 | ||

| 07:30 | EUR | Germany Manufacturing PMI Jun P | 46.4 | 45.4 | ||

| 07:30 | EUR | Germany Services PMI Jun P | 54.4 | 54.2 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Jun P | 48 | 47.3 | ||

| 08:00 | EUR | Eurozone Services PMI Jun P | 53.5 | 53.2 | ||

| 08:30 | GBP | Manufacturing PMI Jun P | 51 | 51.2 | ||

| 08:30 | GBP | Services PMI Jun P | 53.2 | 52.9 | ||

| 12:30 | CAD | Industrial Product Price M/M May | 0.40% | 1.50% | ||

| 12:30 | CAD | Raw Material Price Index May | -0.60% | 5.50% | ||

| 12:30 | CAD | Retail Sales M/M Apr | 0.90% | -0.20% | ||

| 12:30 | CAD | Retail Sales ex Autos M/M Apr | 0.50% | -0.60% | ||

| 13:45 | USD | Manufacturing PMI Jun P | 51 | 51.3 | ||

| 13:45 | USD | Services PMI Jun P | 53.5 | 54.8 | ||

| 14:00 | USD | Existing Home Sales May | 4.10M | 4.14M | ||

| 14:30 | USD | Natural Gas Storage | 69B | 74B |

Cliff Notes: Deliberating on Evolving Risks

Key insights from the week that was.

In Australia, the RBA Board once again left the cash rate unchanged at 4.35%. The Board’s statement emphasised that there remains considerable uncertainty around the economic outlook, particularly as it relates to policy lags, the path for consumption, and consequently inflation’s path back to target. Strong population growth has provided considerable support for aggregate demand, GDP up 1.1%yr in the March quarter despite per capita activity declining 1.3%yr, but capacity is constrained. This context puts the Board in a challenging position on the narrow path back to target inflation, requiring it “to remain vigilant to upside risks to inflation” and “not rule anything in or out” with respect to policy.

Critical to the RBA outlook for the remainder of the year will be forthcoming updates on inflation. As detailed earlier this week, there is likely to be greater-than-usual volatility in headline inflation over the coming twelve months, as various cost-of-living policy initiatives from both federal and state governments lower measured inflation. The RBA Board are likely to ‘look through’ this volatility in headline inflation and focus on developments in core inflation. Supporting our view for a further deceleration in trimmed mean inflation, to 3.5%yr by Dec-24 and 3.0%yr by Jun-25, is a constructive outlook for many of the risks the RBA Board is currently focused on. That includes the more modest decision on minimum and award wages from the Fair Work Commission, the significant moderation in unit labour costs growth to date, and the ongoing improvement in labour productivity.

Overall, we view the Board’s language as striking a delicate balance. Rate cuts are unlikely to be delivered until late in the year, November being our forecast for the first move, with policy relief ensuing at a measured pace thereafter – 25bp per quarter, taking the cash rate to 3.10% by Q4 2025. Should stickiness in price pressures persist, the risk that policy relief will be pushed back will grow.

Offshore, the Bank of England kept rates steady at 5.25% in a 7-2 vote, but gave their first hint of a near-term rate cut. On the whole, economic conditions were viewed as consistent with progress being made, with a number of those who voted for no change noting that their decisions were “finely balanced”. The decision came a day after the release of the May CPI which, on a headline basis, came in at target -- 2%yr. However, core inflation rose 3.5%yr while services remained sticky at 5.7%yr. Helpfully, inflation’s breadth is narrowing -- 59% of the basket was running above the 2% target in May compared to 64% in April. The BoE's analysis also suggests price setting behaviour in the services sector should continue to ease, albeit from a still elevated level.

The UK labour market has been hard to gauge given data quality issues, but the Decision Maker Panel survey implies wage and inflation expectations are decelerating, helping to balance risks to the inflation outlook. Inflation is expected to print just above 2%yr through the second half of 2024 as energy subsidies cycle out. For the BoE to feel confident CPI will sustainably return to target thereafter, further progress on underlying services inflation is required along with easing wage pressures. It is important to recognise that one cut will not take policy from contractionary to neutral, and so we are most likely to see cutting commence before the 2.0%yr target is sustainably attained. The August meeting is best considered live, particularly as revised forecasts will be received by the MPC at that meeting. As in other key jurisdictions, the coming rate cutting cycle for the UK will be measured in timing and scale, with each step determined by incoming data.

Last Friday, the Bank of Japan left policy rates unchanged, but noted they would reduce bond purchases with a detailed plan to be outlined at their July meeting. Commentary around the outlook for the economy remains unchanged -- real wage growth is expected to sustainably support demand and prices, leading to at-target inflation into the medium term. Remaining upbeat but patient will improve the chances of this expectation becoming reality. Also supportive is the weak Yen, as discussed in our note. However, meaningful and persistent increases in real wages and investment are necessary to justify policy normalisation.

Elsewhere in Asia, Chinese partial data remained mixed in May. Authorities belief that downside risks are being neutralised by policy was challenged by the data, the price of new and used homes declining by 0.7% and 1.0% respectively in May. Investment in the sector also remained 10% lower year-to-date. Consumer spending is best considered resilient (but certainly not strong or strengthening), retail sales up 4.1% year-to-date in May, the same as April. Fixed asset investment continued at a circa 4% pace year-to-date as growth in property investment remained deeply negative and high-tech manufacturing investment growth slowed to a robust but sustainable pace after the rapid gains of recent years. Highlighting the benefit to China from trade, particularly with Asia, industrial production continued to grow around 6% year-to-date.

Finally to the US. FOMC speakers this week again emphasised the prudence of waiting for further progress with respect to inflation’s return to target. That said, it was evident in their remarks that this view was predicated on US growth remaining above trend and no further slippage in the labour market. Data out this week instead highlighted the downside risks for activity. Retail sales again surprised to the downside in May, +0.1%, and April was revised down from flat to -0.2%. Both headline and control group sales point to goods spending being essentially unchanged year-to-date. Despite still robust momentum in services spending, total consumption growth looks to have slipped to a below-trend pace in Q2. Forward looking housing data was also very week in May, with starts now 20% lower than a year ago and permits down 9%yr. Initial claims meanwhile continues to indicate little-to-no job shedding, but all measures of labour demand indicate it is softening, to varying degrees. As we continue to highlight, the FOMC need to be mindful of the evolution of risks that the US faces. This will be as true a year from now as it is today.

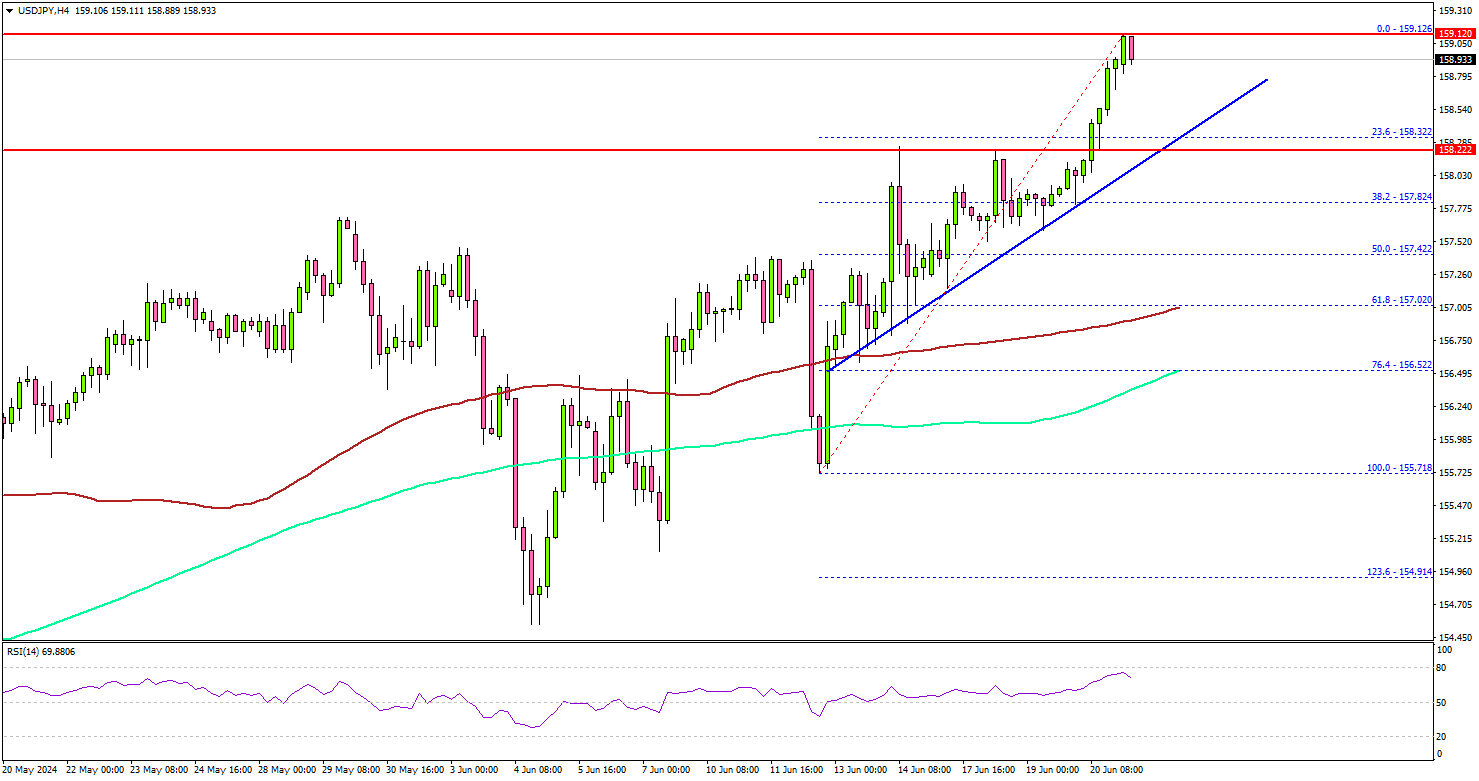

USD/JPY on the Rise: Surges To Aim For New Highs

Key Highlights

- USD/JPY gained pace and cleared the 158.20 resistance.

- A major bullish trend line is forming with support at 158.20 on the 4-hour chart.

- EUR/USD is struggling to clear the 1.0765 resistance zone.

- The US Manufacturing PMI could decline from 51.3 to 51.0 in July 2024 (Preliminary).

USD/JPY Technical Analysis

The US Dollar remained well-bid above the 156.50 support against the Japanese Yen. USD/JPY formed a base and started a fresh increase above the 157.80 resistance.

Looking at the 4-hour chart, the pair settled above the 158.00 level, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). More importantly, there was a clear move above the 158.20 resistance.

The pair is now rising toward the 159.20 resistance zone. The first major resistance is near the 159.50 level. A clear move above the 159.50 resistance might send it toward the 160.00 level. Any more gains might call for a move toward the 161.20 level in the near term.

If not, the pair might dip again. Immediate support is near the 158.20 level. There is also a major bullish trend line forming with support at 158.20 on the same chart.

The next major support is near the 157.80 zone. A downside break and close below the 157.80 support zone could open the doors for a larger decline. In the stated case, the pair could decline toward the 157.20 level.

Looking at EUR/USD, the pair corrected losses, but the bulls are still struggling for a move above the 1.0765 resistance zone.

Economic Releases

- Germany’s Manufacturing PMI for July 2024 (Preliminary) - Forecast 46.4, versus 45.4 previous.

- Germany’s Services PMI for July 2024 (Preliminary) - Forecast 54.4, versus 54.2 previous.

- Euro Zone Manufacturing PMI for July 2024 (Preliminary) – Forecast 47.9, versus 47.3 previous.

- Euro Zone Services PMI for July 2024 (Preliminary) – Forecast 53.5, versus 53.2 previous.

- UK Manufacturing PMI for July 2024 (Preliminary) – Forecast 51.3, versus 51.2 previous.

- UK Services PMI for July 2024 (Preliminary) – Forecast 53.0, versus 52.9 previous.

- US Manufacturing PMI for July 2024 (Preliminary) – Forecast 51.0, versus 51.3 previous.

- US Services PMI for July 2024 (Preliminary) – Forecast 53.7, versus 54.8 previous.

Japan’s CPI core accelerates to 2.5%, but core-core slows to 2.1%

Japan's CPI core (ex-food) accelerated from 2.2% yoy to 2.5% yoy in May, slightly below the expected 2.6%. This marks the 26th consecutive month that core inflation has remained above BoJ's 2% target. However, the increase was primarily driven by a significant 14.7% yoy rise in electricity prices.

In contrast, CPI core-core (ex-food and energy) slowed from 2.4% yoy to 2.1% yoy. Additionally, services inflation eased from 2.5% yoy to 2.2% yoy. Headline CPI also rose from 2.5% to 2.8% yoy, marking its ninth consecutive month of deceleration and the lowest reading since September 2022.

BoJ Governor Kazuo Ueda has repeatedly suggested that a July rate hike is a possibility. However, today's report indicates that the inflation uptick is mainly due to cost-push factors, such as higher electricity prices, rather than increased demand. This might not provide a strong enough basis yet for BoJ to proceed with a rate hike at this time.

Japan’s PMI composite falls to 50, mixed economic signals with rising costs

Japan's latest PMI data for June presents a mixed economic outlook. Manufacturing PMI slipped slightly from 50.4 to 50.1, falling short of expectations of 50.6. However, manufacturing output showed a positive shift, rising from 49.9 to 50.5, marking the first expansion in over a year. Conversely, Services PMI dropped sharply from 53.8 to 49.8, indicating fractional contraction for the first time since August 2022. As a result, Composite PMI fell from 52.6 to 50.0.

Jingyi Pan, Economics Associate Director at S&P Global Market Intelligence, commented that the private sector expansion has stalled midway through the year. The return of manufacturing output growth was overshadowed by a decline in services activity, partially due to labor constraints.

A notable concern is the "pressure on margins," with average input costs rising at the fastest pace in over a year while output price inflation softened, particularly in the service sector. Anecdotal evidence pointed to the weak yen and increasing labor costs as significant factors driving up cost inflation.

Australia’s PMI composite falls to 50.6, slowing business expansion, manufacturing weakness

Australia's PMI data for June indicates a slowdown in business expansion, with Manufacturing PMI falling from 49.7 to 47.5, Services PMI dropping from 52.5 to 51.0, and Composite PMI decreasing from 52.1 to 50.6, hitting a five-month low.

Warren Hogan, Chief Economic Advisor at Judo Bank, noted that while business activity continues to grow, the pace of expansion has slowed compared to the strong performance in the first half of 2024.

The manufacturing sector showed significant weakness, with PMI, output, and new orders declining towards the cyclical lows of 2023, all falling below the 50 threshold that separates expansion from contraction. In contrast, the services sector experienced a slight pullback but remained in expansionary territory.

The composite input price index dropped below 60 for the first time since January 2021, suggesting that business cost growth is easing. Final prices also decreased but still indicate above-target inflation. Service sector price indicators retreated in June, aligning with the view that inflation is gradually easing in 2024, yet they remain above RBA's target range of 2-3%.

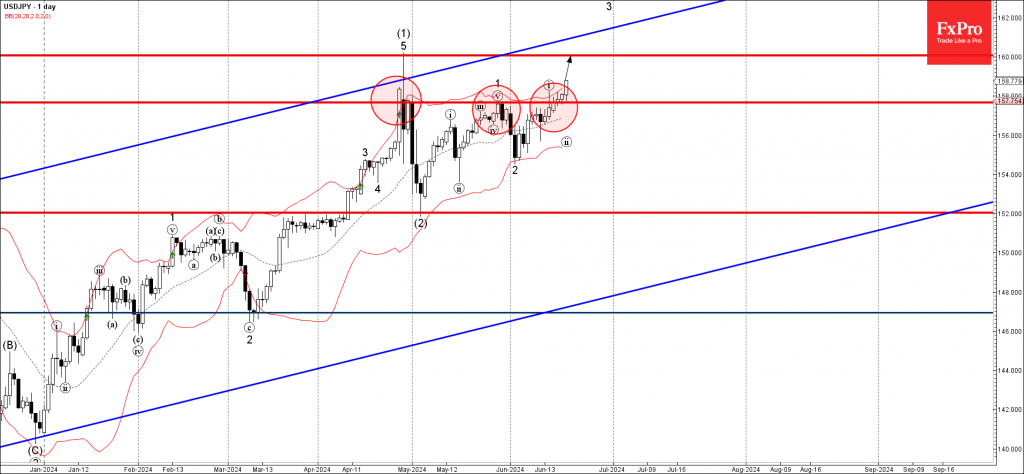

USDJPY Wave Analysis

- USDJPY broke strong resistance level 157.65

- Likely to rise to resistance level 160.00

USDJPY currency pair recently broke above the strong resistance level 157.65 (which has been steadily reversing the price from the end of April, as you can see below).

The breakout of the resistance level 157.65 continues the clear uptrend that can be seen on the daily and the weekly USDJPY charts.

USDJPY currency pair can be expected to rise further to the next resistance level 160.00, which stopped the previous impulse wave (1) at the end of April.

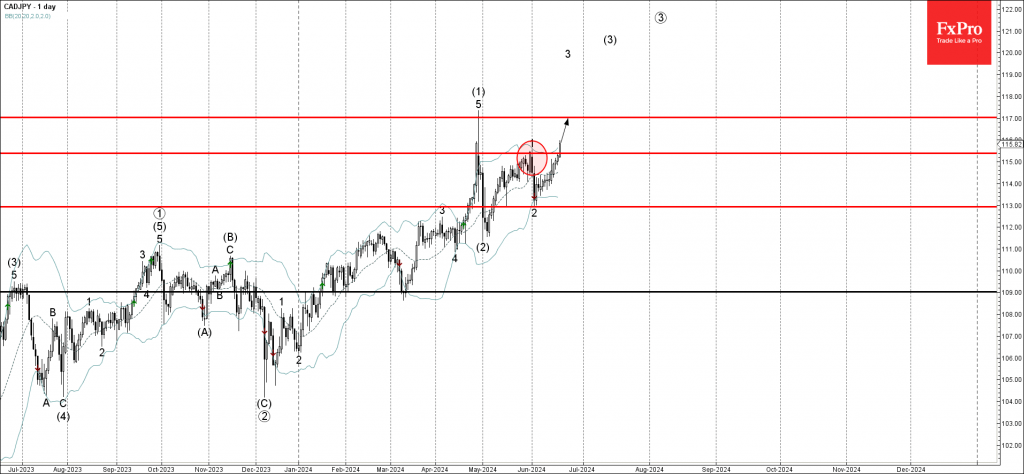

CADJPY Wave Analysis

- CADJPY under bullish pressure

- Likely to rise to resistance 117.00

CADJPY currency pair under the bullish pressure after the price broke above the key resistance level 115.40 (which stopped the previous impulse wave 1 at end of May).

The breakout of the resistance level 115.40 accelerated the active impulse waves 3 and (3).

Given the clear multi-month uptrend and the continuation of the bearish yen sentiment, CADJPY currency pair can be expected to rise further to the next resistance level 117.00.