Sample Category Title

(SNB) Swiss National Bank Eases Monetary Policy and Lowers SNB Policy Rate to 1.25%

The Swiss National Bank is lowering the SNB policy rate by 0.25 percentage points to 1.25%. The change applies from tomorrow, 21 June 2024. Banks' sight deposits held at the SNB will be remunerated at the SNB policy rate up to a certain threshold, and at 0.75% above this threshold. The SNB is also willing to be active in the foreign exchange market as necessary.

The underlying inflationary pressure has decreased again compared to the previous quarter. With today's lowering of the SNB policy rate, the SNB is able to maintain appropriate monetary conditions. The SNB will continue to monitor the development of inflation closely, and will adjust its monetary policy if necessary to ensure inflation remains within the range consistent with price stability over the medium term.

Inflation has risen slightly since the last monetary policy assessment, and stood at 1.4% in May. Higher inflation in rents, tourism services and oil products has contributed in particular to this increase. Overall, inflation in Switzerland is currently being driven above all by higher prices for domestic services.

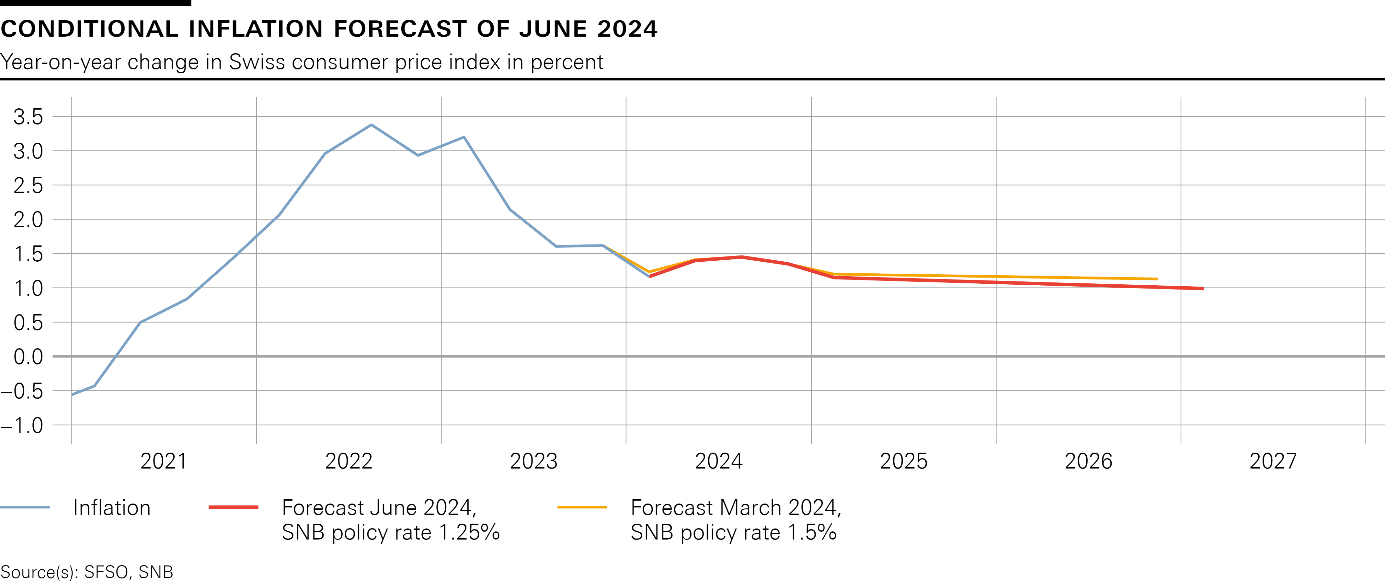

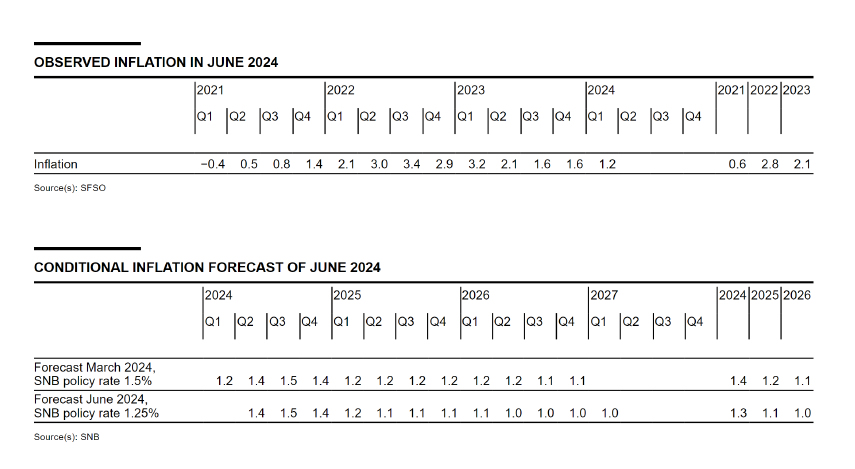

Taking into account today's policy rate cut, the new conditional inflation forecast is similar to that of March. Over the longer term, it is slightly below the previous forecast. This reflects somewhat lower second-round effects. Over the entire forecast horizon, the conditional inflation forecast is within the range of price stability (cf. chart). The forecast puts average annual inflation at 1.3% for 2024, 1.1% for 2025 and 1.0% for 2026 (cf. table). The forecast is based on the assumption that the SNB policy rate is 1.25% over the entire forecast horizon. Without today's rate cut, the forecast would have been lower.

Global economic growth was solid in the first quarter of 2024. Inflation largely moved sideways over the past months, and remained above central banks' targets in many countries. However, the underlying inflationary pressure continued to decrease slightly. Against this background, some central banks eased their monetary policy for the first time following the tightening cycle of the past two years. However, monetary policy remains restrictive in many countries.

Inflationary pressure abroad is likely to continue to ease gradually over the next quarters. At the same time, the global economy is likely to pick up somewhat. However, for the coming quarters the SNB expects only moderate growth in global economic activity by longer-term comparison.

This scenario for the global economy is still subject to significant risks. Inflation could remain elevated for longer in some countries, necessitating a tighter monetary policy there than expected in the baseline scenario. Equally, a renewed increase in geopolitical tensions could result in weaker development of global economic activity.

Swiss GDP growth was moderate in the first quarter of 2024. The services sector continued to expand, while value added in manufacturing stagnated. There was a further slight increase in unemployment. The utilisation of overall production capacity was normal.

Growth is likely to remain moderate in Switzerland in the coming quarters. The SNB anticipates GDP growth of around 1% this year. In this environment, unemployment is likely to continue to rise slightly, and the utilisation of production capacity is set to decline slightly. Over the medium term, economic activity should improve gradually, supported by somewhat stronger demand from abroad. The SNB currently expects growth of around 1.5% for 2025.

The forecast for Switzerland, as for the global economy, is subject to significant uncertainty. Developments abroad represent the main risk.

Momentum on the mortgage and real estate markets in recent quarters has been weaker than in previous years. However, the vulnerabilities in these markets remain.

More detailed information on the monetary policy decision can be found in the introductory remarks of the Governing Board.

Swiss National Bank, Norges Bank and Bank of England Will Decide on Monetary Policy

Markets

EMU and UK markets yesterday had to develop their own dynamics with no guidance from the US (markets closed for the Juneteenth holiday). The European Commission activated the ‘excessive deficit procedure’ for 7 member states to rectify persistent budgetary slippage. In a separate study on its website, the ECB also published an in extenso article on the huge fiscal pressures EU/EMU countries are facing to cope with the challenges of an ageing population, higher defense spending and climate change and closing the digitalization gap, which are coming on top of current debt burden (cf infra). In calm session, (10-y) intra-EMU spreads (vs Germany) still widened a few bps for peripheral markets (Italy +3 bps, Spain & Portugal +1 bp). France also widened 2 bps. German yields gained less than 1 bp across the curve. The euro showed no clear directional trend with EUR/USD closing marginally higher at 1.0745. UK Gilts underperformed Bunds rising between 4.1 bps (2-y) and 1.7 bps (5-y). UK headline CPI in May returned to BoE‘s 2.0% target but core (0.5% M/M and 3.5% Y/Y) and services inflation (+0.6% M/M and 5.7% Y/Y) indicated that it’s much too early for the BoE already to declare victory. Sterling temporarily gained post the release, but gains could not be sustained. EUR/GBP close the session little changed at 0.8447.

Asian equity markets this morning mostly show modest losses with China tentatively underperforming (CSI 300 -0.55%). The PBOC set the yuan’s fixing at the weakest levels since November, suggesting an further cautious stimulative approach. The on-shore yuan weakens to USD/CNY 7.26. At the restart in Asia, US yields add 2-3 bps across the curve. The dollar also gains a few ticks (EUR/USD 1.0740, DXY 105.3, USD/JPY 158.15).

Later today, the US calendar contains jobless claims, housing starts and permits and the Philly Fed business outlook. After a recent jump higher, especially jobless claims might have some intraday impact. The Swiss National Bank, the Norges Bank and the Bank of England will decide on monetary policy. Markets are divided whether the SNB should follow-up on the March 25 bps cut. The Norges Bank and the BoE probably have no room yet to give concrete guidance on the start of an easing cycle. EUR/GBP for now found a new ST equilibrium between 0.84 and 0.85.

News & Views

New Zealand’s economy escaped from a recession in Q1 of this year. GDP expanded at a modest 0.2% q/q, bringing the yearly figure to 0.3%. The numbers were slightly better than expected though in line with the central bank’s (RBNZ) forecast. Household consumption picked up from 0.6% to 1.6% q/q while government expenditures declined by -0.3%. Rising inventories supported growth while capital investments were a strong drag (-1.3%). Net exports also weighed heavily on the 2024Q1 figure due to a sharp increase in imports (+6.1%). The growth numbers don’t bring a lot of cheer but they won’t entice the RBNZ to cut rates anytime soon. Its chief economist Conway on Tuesday repeated the need to keep the policy rate restrictive for a long enough period, citing still-widespread inflation pressures. Additionally, underlying gauges including services/non-tradeable CPI prove sticky while the economy is expected to gradually gain traction in coming quarters. The central bank last month flagged no cuts before 2025H2. Money markets bet on a first move in November this year. New Zealand swap yields jumped between 5.3 and 7.3 bps after the release but the kiwi dollar barely budged. NZD/USD hovers near 0.613.

The ECB in a publication yesterday outlined and calculated the brutal reality of the fiscal challenges the European bloc is facing in the decades ahead. It calculated that for the euro area to reduce government debt levels towards the 60% level by 2070, an immediate and permanent effort of 2% of GDP is needed annually. This comprises a 1.4% adjustment just to maintain debt levels at the 2023 levels, complemented by a 0.6% effort in order to actually reduce debt levels. Additional costs complicate the picture. The central bank singled out three trends that await member states: demographic ageing (leading to increased costs in pensions, health & long-term care and education), filling the defence gap and climate change. These are estimated to increase the efforts needed by another 3% in coming decades (1.2%, 0,5% and 1.1% respectively). For some individual countries, the situation is much worse. Belgium’s fiscal challenge is guesstimated at more than 7%. Slovakia tops the board with a more than 9% effort needed.

Graphs

GE 10y yield

The ECB cut its key policy rates by 25 bps at the June policy meeting. A more bumpy inflation path in H2 2024, the EMU economy gradually regaining traction and the Fed’s higher for longer US strategy make follow-up moves difficult. Markets are coming to terms with that. For the time being, though, the political narrative dominates. After hitting a new YtD top at 2.7%, the German 10-yr yield corrected lower on safe haven bids.

US 10y yield

The Fed is seeking more evidence than just one slower-than-expected (May) CPI is providing. Upgraded inflation forecasts and a higher neutral rate complicate the exact timing of a first cut further. June dots suggest one move in 2024 followed by four more next year. Markets are positioned more aggressively, turning the recent low in yields into a technical support zone. The US 10-y yield is testing the downside of the 4.2/4.7% trading range.

EUR/USD

EUR/USD is trapped in the 1.06-1.09 range. The desynchronized rate cut cycle with the ECB exceptionally taking the lead, strong US May payrolls and a swing to the right in European elections pulled the pair away from 1.09 resistance. The Fed meeting balanced the weaker than expected US CPI outcome. Euro fragility makes a return to the 1.06 downside more likely than not.

EUR/GBP

Debate at the BOE is focused at the timing of rate cuts. May headline inflation returned to 2%, but core measures suggest it’s too early for the BoE to signal easing anytime soon. General elections (July 4) already made a June cut in line with the ECB unlikely. Money markets are discounting a Fed-like scenario. Sterling benefited. EUR/GBP tested the 2023 & 2024 lows near 0.85. Euro weakness eventually pulled the trick after French president Macron called snap elections following a weak showing in EU elections.

Elliott Wave Analysis on Nasdaq (NQ) Looking for Further Rally

Short Term Elliott Wave in Nasdaq Futures (NQ) suggests that cycle from 4.19.2024 low is in progress as an impulse. Up from 4.19.2024 low, wave 1 ended at 19023.25 and pullback in wave 2 ended at 18241.25. Wave 3 higher is currently in progress with subdivision of an impulse in lesser degree. Up from wave 2, wave (i) ended at 18755.50 and pullback in wave (ii) ended at 18435.75. The Index rallied higher in wave (iii) towards 19124.5 and dips in wave (iv) ended at 18940. Final leg wave (v) ended at 19155 which completed wave ((i)).

Pullback in wave ((ii)) ended at 18971.93 with internal subdivision as a zigzag structure. Down from wave ((i)), wave (a) ended at 18997 and wave (b) ended at 19067.75. Wave (c) lower ended at 18971.93 which completed wave ((ii)) in higher degree. The Index rallied higher in wave ((iii)) as an impulse. Up from wave ((ii)), wave (i) ended at 19671.75 and wave (ii) pullback ended at 19500. Near term, as far as pivot at 18971.9 low stays intact, expect pullback to find support in 3, 7, or 11 swing for further upside.

Nasdaq 60 Minutes Elliott Wave Chart

Nasdaq (NQ) Elliott Wave Video

https://www.youtube.com/watch?v=pJzmipFuf6w

Decision Day Will Bring Three Important Policy Announcements on Top of China’s

Appetite in Europe was weak yesterday in the absence of American markets. The French CAC40 remained firmly offered near its 200-DMA and fell 0.77%, the European Stoxx 600 index retreated 0.17%, and the Swiss SMI consolidated above the 12’000 mark while the FTSE 100 took out the 50-DMA and closed slightly higher at yesterday’s trading session. The French political risks remain on the headlines and many investors are reluctant to go back to the French and European stock indices ahead of the upcoming legislative elections as they fear that a victory for Marine Le Pen’s National Rally could further hit valuations. But the European stock valuations remain attractive as they are way cheaper than the US peers, and some investors make a parallel between France and Italy – which also saw its assets hit by Meloni’s rise to power as Draghi resigned, and point that, in fine, Meloni has successfully kept investors in check and Italy ended up being fine.

Crude’s rise

Crude oil consolidated gains above the $80pb and remains supported by positive trend vibes since it stepped into the medium bullish consolidation zone after it cleared the major 38.2% Fibonacci resistance on April to June rally. The geopolitical tensions, tight OPEC supply, the rising summer demand and reflation appetite are among factors that support the rally, while a high US and non-OPEC production and a potential weakness in reflation inflows are the major risks to the actual positive formation. The next crucial support stands at $82pb, the major 61.8% Fibonacci retracement, that will either call the end of the latest positive push, or confirm the strength of the rally. I believe there is more chance we see the first scenario unfold rather than the second.

A decision day

The day will bring three important policy announcements on top of China’s. China maintained its rates unchanged today at record lows, as expected, and the People’s Bank of China (PBoC) signaled a new toolkit that could allow the Chinese central bank to start buying government bonds – which would be a new way of injecting liquidity into the markets. But alas, the Chinese CSI index continues to be offered into its 200-DMA as the PBoC refrained from cutting the rates this week and Hang Seng index gave back a part of yesterday’s strong gains.

Closer to home, the Norges Bank, the Swiss National Bank (SNB) and the Bank of England (BoE) will announce their latest policy verdicts today.

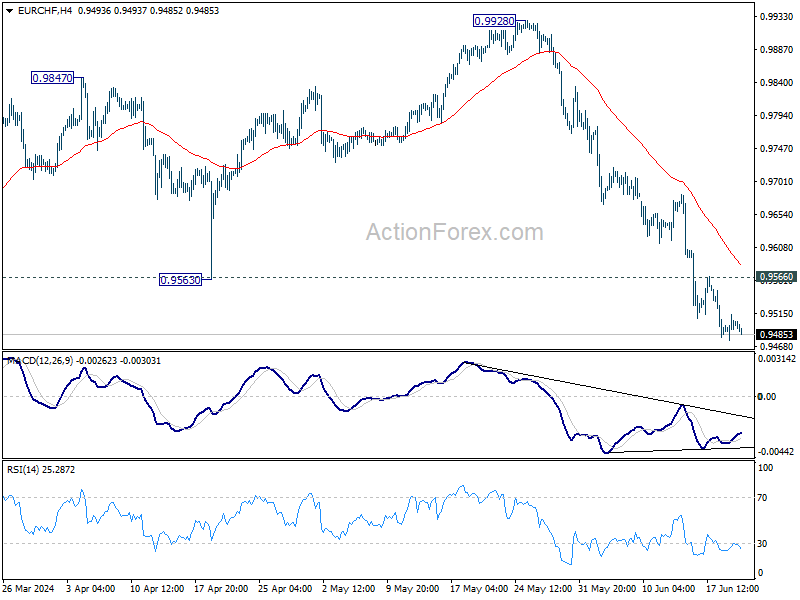

SNB expectations differ from poll to poll. The consensus on a Bloomberg survey hints at no change in rates today in Switzerland while a poll from Reuters suggest a 25bp cut to 1.25% following a 25bp cut from the European Central Bank (ECB) earlier this month. The USDCHF cleared the all-important 200-DMA and major Fibonacci support this week and slipped into the bearish consolidation zone. The euro-franc fell to the lowest levels since February – the fall is amplified by the French political jitters. A potential rate cut from the SNB could eventually slow and stop the franc’s appreciation – especially against the greenback - and send the USDCHF back to a bullish path and I think a 25bp cut would make sense as the SNB has margin on the inflation front to make this move and support the economy.

For the BoE, things are more complicated. Yesterday’s CPI release showed that headline inflation in the UK fell to the BoE’s 2% policy target and the UK ended up being – against all odds at this time last year – the first nation among comparable peers to make this achievement. Yet two things worry the BoE doves and slow down rate cut expectations. First, services inflation remains high – perhaps too high near 6% - to let the BoE cut rates with a peace of mind as services make up around 80% of the British economy. And second, consumer prices could rapidly rebound if natural gas market tightens as traders rush to replenish their stockpiles before winter. As such, if the BoE doesn’t announce a rate cut today, it’s not because they don’t want to put their nose into the country’s political affairs with the upcoming general election, but it’s mostly because the underlying inflationary factors are not yet convincing enough to allow them to do so.

No Rate Cuts Expected from SNB, BoE, or NB today

In focus today

We have three central bank policy decisions today, from Norges Bank (NB), the Swiss National Bank (SNB), and the Bank of England (BoE)

We expect the SNB to keep the policy rate unchanged at 1.50% today after delivering its first cut at the March meeting. The recent strengthening of the CHF poses the biggest risk to our call.

We expect the BoE to keep the Bank Rate unchanged at 5.25% today with 7 members voting for unchanged and 2 members for a cut. We expect little change in communication and expect the first 25bp cut to be delivered in August. See more in Bank of England Preview, 14 June.

We expect NB to keep the policy rate unchanged at 4.50%. Since the bank first signalled a 25bp September cut back in March, economic growth has picked up compared to what was expected while global rate expectations have adjusted upwards, reducing the room for manoeuvre for Norges Bank. We therefore expect hawkish signals from NB and a reduced probability of a September cut.

In the euro area, we follow the June consumer confidence data in the euro area. Private consumption has been muted despite record-low unemployment, rising real incomes and strong savings. Weak consumer confidence is likely one of the reasons why we have seen this. Hence, it will be important to follow if confidence starts rising significantly.

Overnight, we get May CPI inflation from Japan. Price pressures have faded in the spring and started to look "Japanese" again, rhyming with less than 1% annual inflation. Regional data from Tokyo indicates more of the same in May. We are still waiting for the spring wage increases to kick in and boost consumers' purchasing power and companies' price setting.

Economic and market news

What happened yesterday

UK services inflation was slightly higher than expected in May at 5.7% y/y (cons.: 5.5), and monthly pressures remained elevated, which should continue to worry the MPC on the scale of easing we can expect this year. Headline and core were in line with consensus. Markets initially drove EUR/GBP lower but the cross ended yesterday's session virtually unchanged. We continue to see the first 25bp cut in August followed up by November.

The EU opened excessive deficit procedures against 7 countries yesterday, with major economies such as France, Italy, and Poland in the mix. The countries now have several months to come up with proposals to improve public finances. No big market reaction was seen as this was largely expected given the data on public finances from these countries.

In the Middle East, fears grew of an escalation of the conflict between Israel and Hesbollah in Lebanon after news that the IDF have approved a plan for an offensive into the country. The fears of further escalation in the region kept oil prices elevated during the day despite a US report of rising inventory levels, with the Brent at around 85.33 USD/bbl.

Market movements

Equities: Global equities rose yesterday, lifted by the Far East, although Europe was lower, and the US market was closed for a holiday. Looking at sector rotation in Europe, we continue to see some recovery after last week's significant drop in several European banking stocks. Material stocks also outperformed yesterday, buoyed by positive momentum in China. While we argue that the French and UK elections should lead to cautious risk-taking in Europe in the coming weeks, we also believe that the economic backdrop will dominate post-elections. Therefore, we recommend maintaining a cyclical tilt in portfolios. Asian markets are mixed this morning, as are European futures, while US indices are higher, led by the tech sector.

FI: Yesterday’s trading session was largely without significant market news. The early trading saw European yields lower (mirroring the late US trading session the day before). However, while France and Italy being put in the first step towards an EDP was widely expected, it seemed to be the trigger for a reversal of the gradual sell-off. As a result, 10y Bunds were virtually unchanged on the day, while France reversed some of the benign market dynamics from earlier this week as spreads widened 2bp.

FX: It was a fairly quiet day yesterday due to holiday in the US. EUR/GBP ended the day close to unchanged after service inflation came in higher than expected. Today, focus turns to the monetary policy decision from Norges Bank, the BoE and the SNB, where we expect"“unchange"” decisions across the broad.

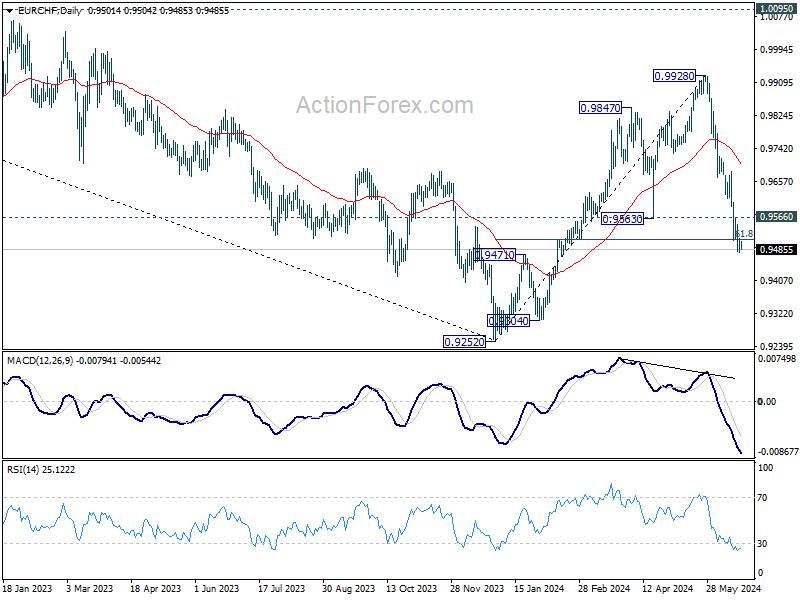

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9483; (P) 0.9499; (R1) 0.9520; More....

Intraday bias in EUR/CHF stays on the downside as fall from 0.9928 is in progress. Sustained trading below 61.8% retracement of 0.9252 to 0.9928 at 0.9510 will raise the chance of long term down trend resumption, and target 0.9252 low next. On the upside, above 0.9566 minor resistance will turn intraday bias neutral again first.

In the bigger picture, the break of 0.9563 support, as well as 55 W EMA (now at 0.9672) argues that rebound from 0.9252 has completed at 0.9928. Medium term bearish is maintained with both 1.0095 resistance intact. Firm break of 0.9252 will resume the down trend from 1.2004 (2018 high).

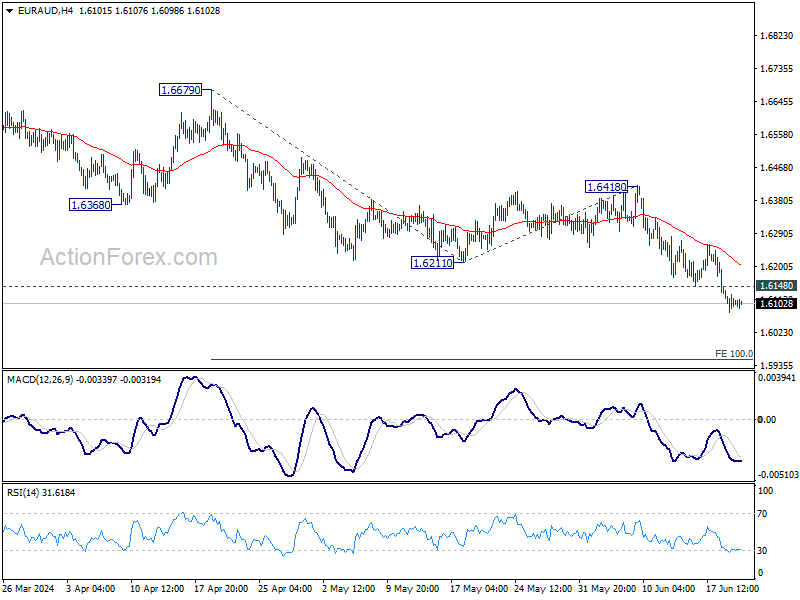

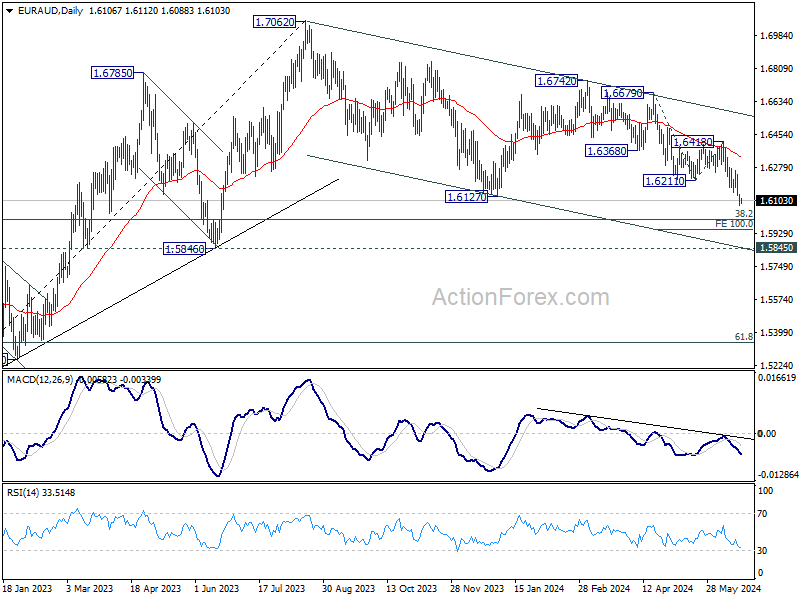

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6072; (P) 1.6109; (R1) 1.6137; More...

Intraday bias in EUR/AUD stays on the downside for the moment. Current down trend should target 100% projection of 1.6679 to 1.6211 from 1.6418 at 1.5950. On the upside, above 1.6148 minor resistance will turn intraday bias neutral and bring consolidations again, before staging another decline.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). In case of deeper fall, strong support is expected around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound. Break of 1.7062 is in favor as a later stage.

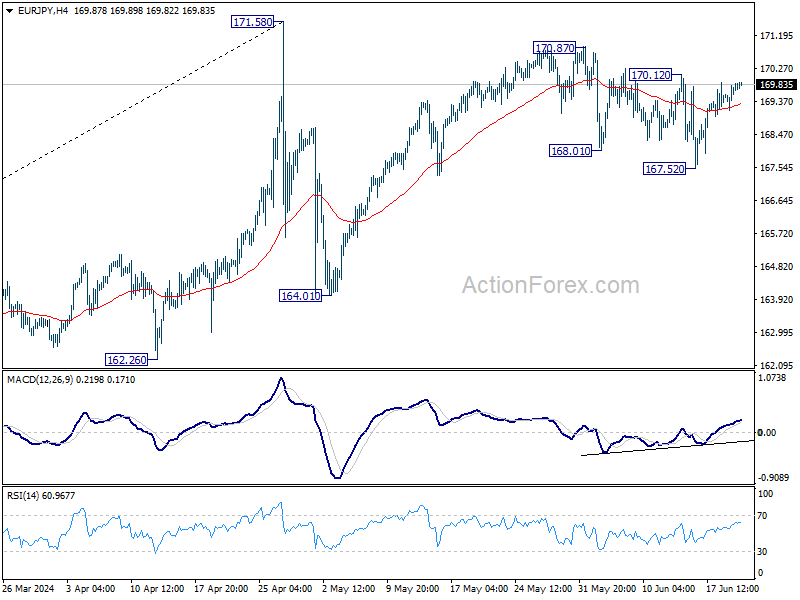

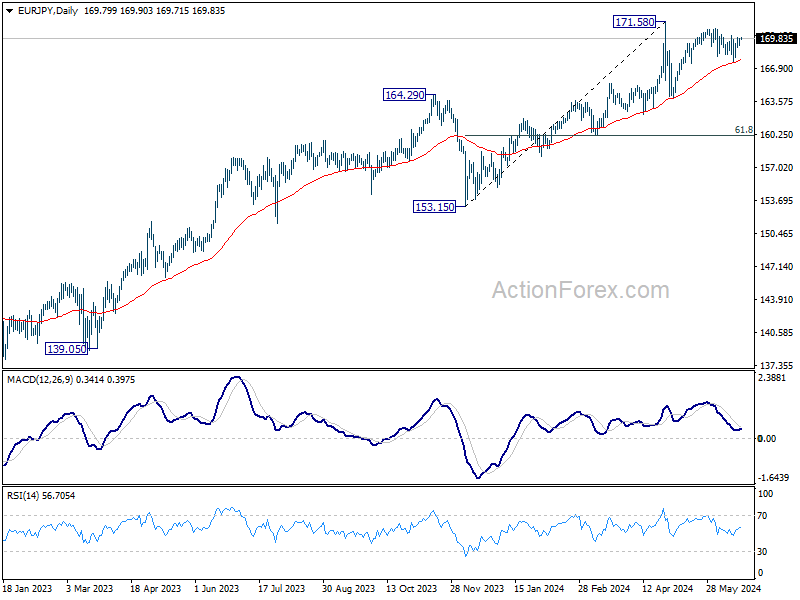

EUR/JPY Daily Outlook

Daily Pivots: (S1) 169.36; (P) 169.63; (R1) 170.12; More...

Intraday bias in EUR/JPY remains neutral for the moment. On the upside break of 170.12 resistance will argue that pull back from 170.87 has completed at167.52, after drawing support from 55 D EMA. Intraday bias will be back on the upside for 170.87 and then 171.58 high.

In the bigger picture, as long as 55 W EMA (now at 159.83) holds, price actions from 171.58 medium term top are seen as as correcting the rise from 153.15 only. That is, larger up trend remains in favor to continue as a later stage. However, sustained break of 55 W EMA will argue that larger scale correction is underway and target 153.15 support.

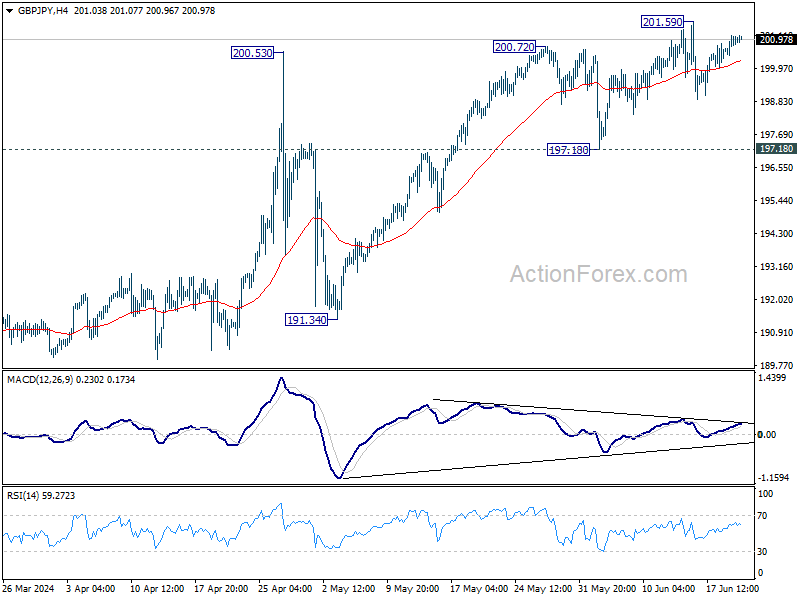

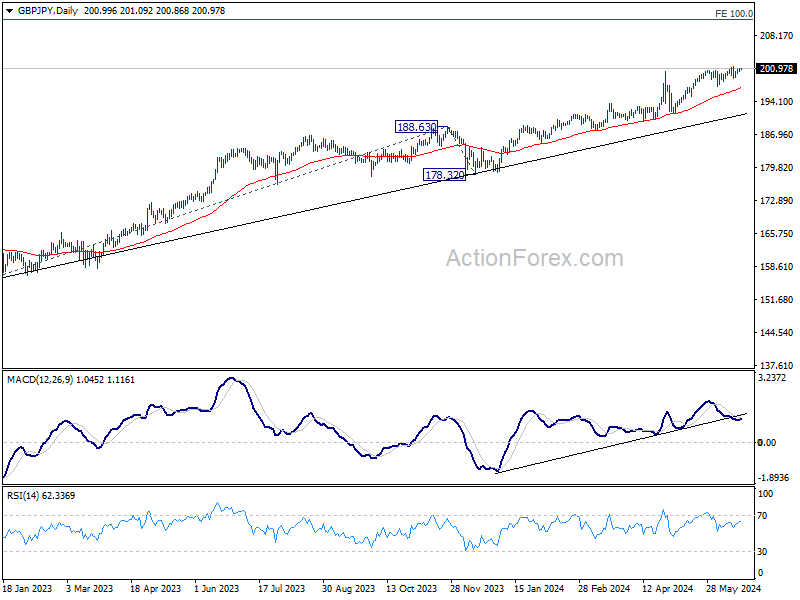

GBP/JPY Daily Outlook

Daily Pivots: (S1) 200.64; (P) 200.88; (R1) 201.35; More...

Intraday bias in GBP/JPY remains neutral as consolidations continues below 201.59. Further rally is expected as long as 197.18 support holds. However, considering bearish divergence condition in 4H MACD, firm break of 197.18 will confirm short term topping, and turn bias back to the downside for 191.34 support instead.

In the bigger picture, as long as 188.63 resistance turned support holds, long term up trend is expected to continue. Next target is 100% projection of 155.33 to 188.63 from 178.32 at 211.62.

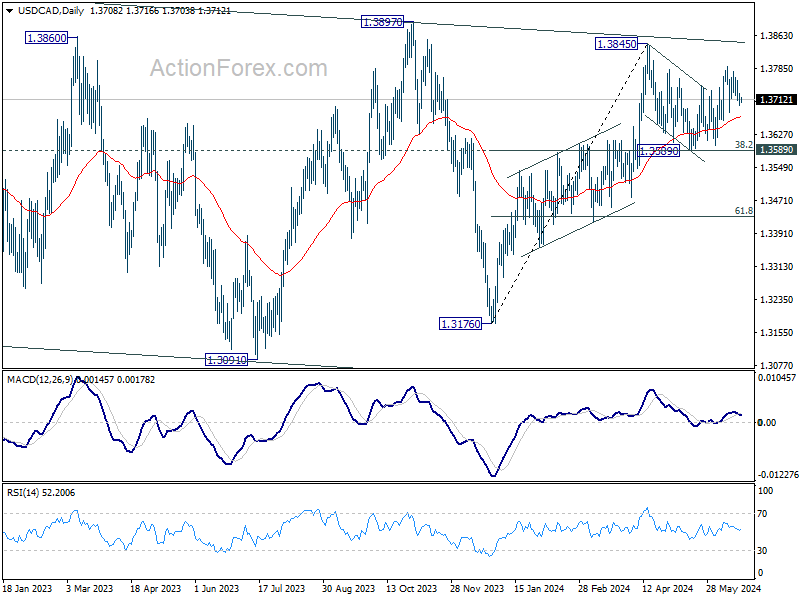

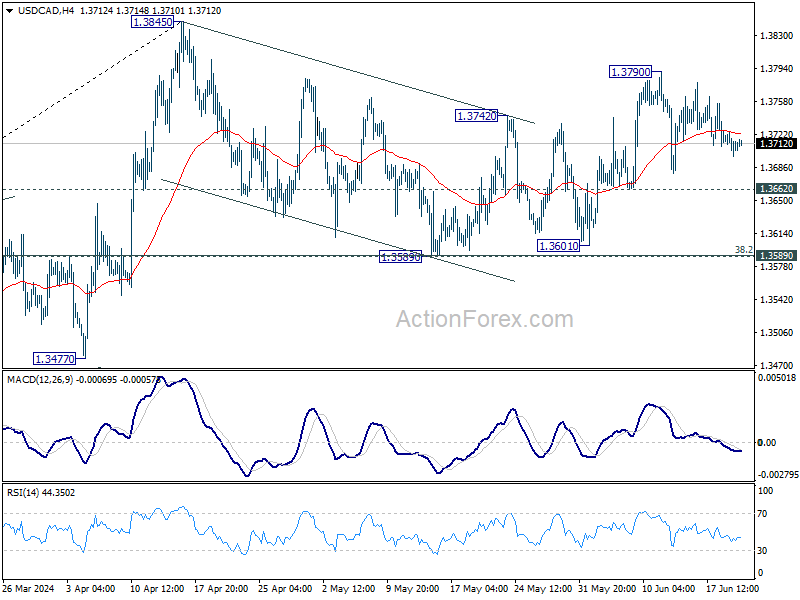

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3695; (P) 1.3710; (R1) 1.3723; More...

USD/CAD is still bounded in sideway trading and intraday bias stays neutral at this point. Corrective fall from 1.3845 should have completed already. Further rally is expected as long as 1.3662 support holds. Break of 1.3790 will target a retest on 1.3845 first. Nevertheless, break of 1.3662 will turn bias to the downside to extend the corrective pattern from 1.3845 with another falling leg.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.