Sample Category Title

AUD/USD Daily Report

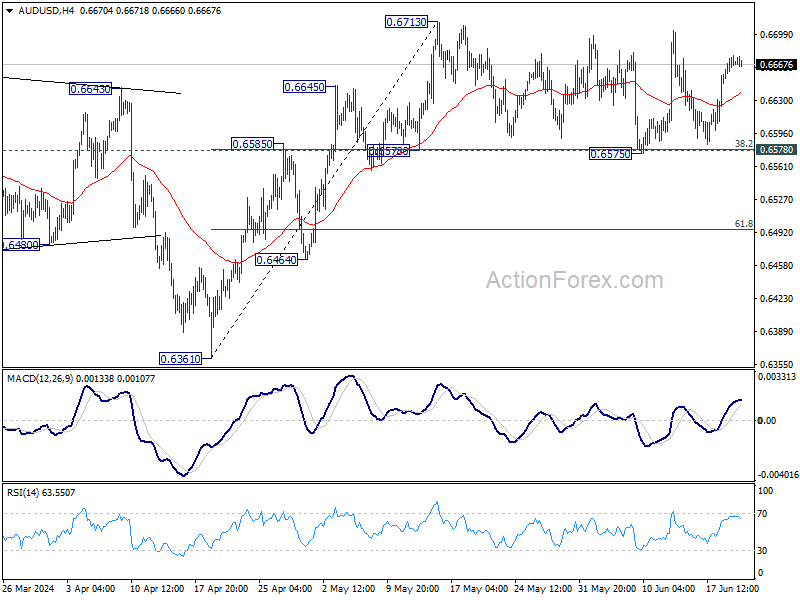

Daily Pivots: (S1) 0.6655; (P) 0.6666; (R1) 0.6684; More...

Intraday bias in AUD/USD remains neutral as range trading continues. Further rally remains in favor with 0.6578 cluster support (38.2% retracement of 0.6361 to 0.6713 at 0.6579) intact. On the upside, firm break of 0.6713 will resume whole rise from 0.6361 to 0.6870 resistance next. However, sustained break of 0.6578 will dampen this bullish view, and bring deeper fall to 61.8% retracement at 0.6495.

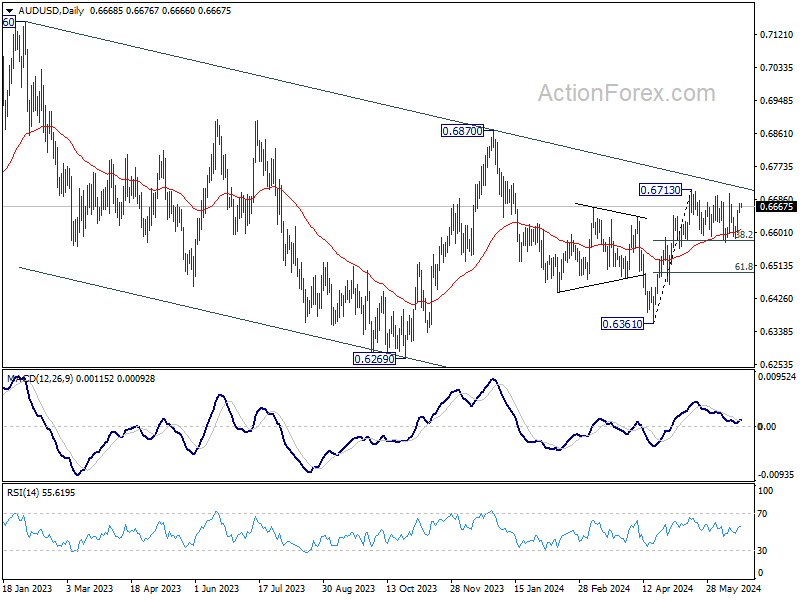

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could have completed at 0.6269 already. Rise from there is seen as the third leg which is now trying to resume through 0.6870 resistance.

EUR/USD Daily Outlook

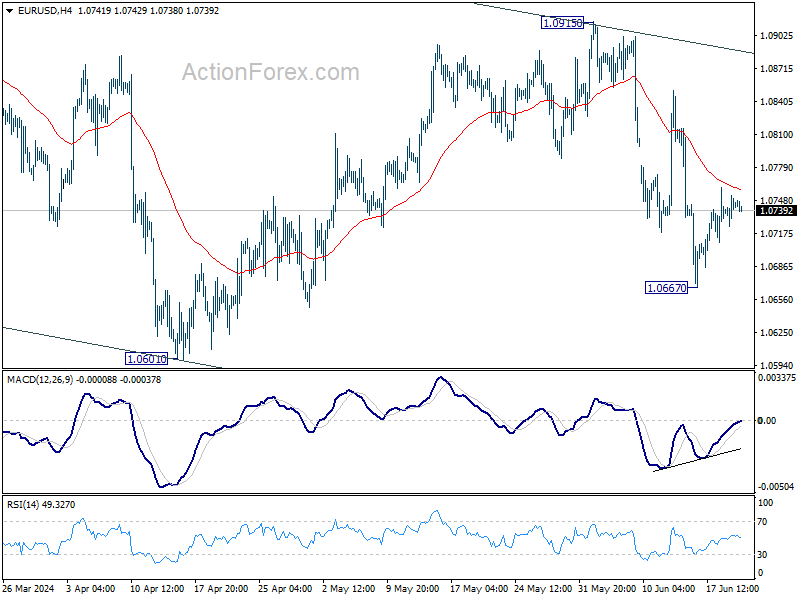

Daily Pivots: (S1) 1.0728; (P) 1.0741; (R1) 1.0756; More....

Intraday bias in EUR/USD remains neutral for the moment. Further decline is expected as long as 55 4H EMA (now at 1.0758) holds. Fall from 1.0915 is seen as another leg in the larger corrective pattern. Below 1.0677 will target 1.0601 low first. Firm break there will target channel support at 1.0500 next. Nevertheless, sustained break of 55 4H EMA will turn bias to the upside for stronger rebound instead.

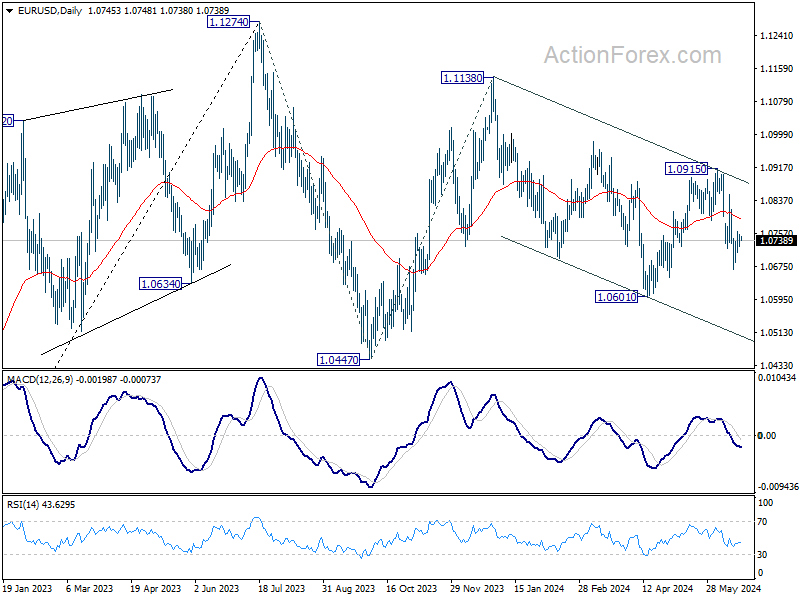

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's still in progress. Break of 1.0601 will target 1.0447 support and possibly further to 100% projection of 1.1274 to 1.0447 from 1.1138 at 1.0311. For now, this will remain the favored case as long as 1.0915 resistance holds, in case of rebound.

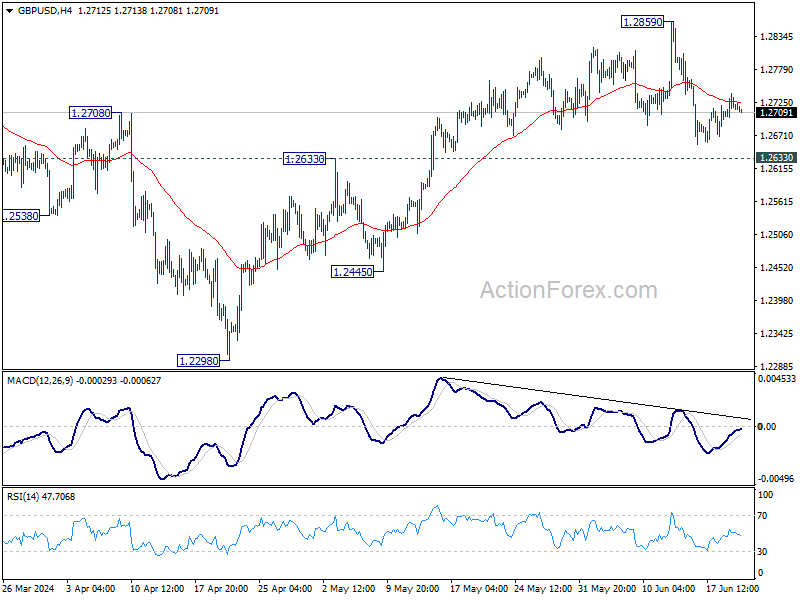

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2695; (P) 1.2717; (R1) 1.2742; More...

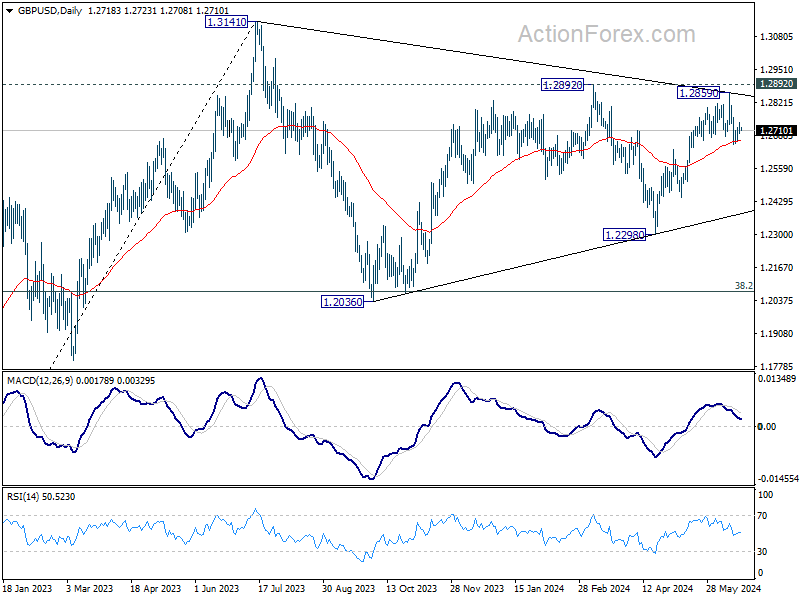

Intraday bias in GBP/USD remains neutral and more consolidations could be seen. Risk will stay on the downside as long as 1.2859 resistance holds. Firm break of 1.2633 resistance turned support will argue that whole rise from 1.2298 has completed, and target 1.2445 and below.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2445 support will extend the corrective pattern with another decline instead.

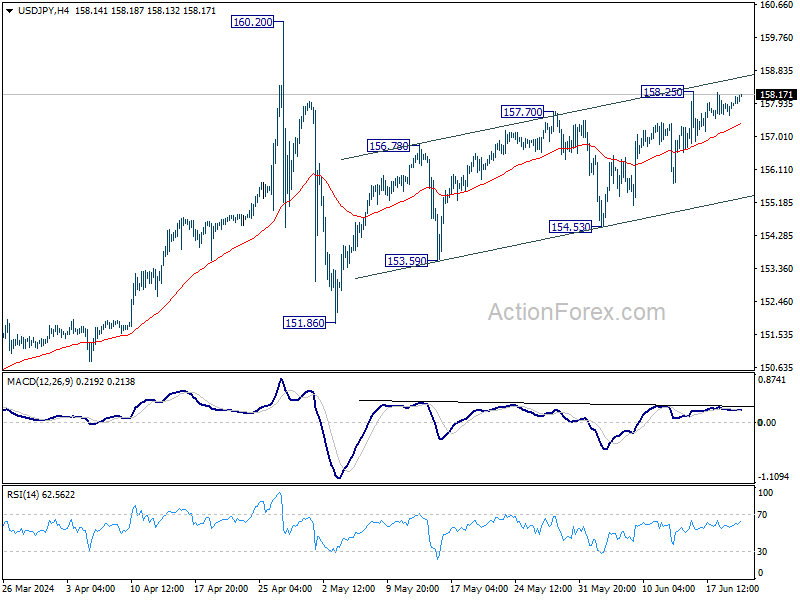

USD/JPY Daily Outlook

Daily Pivots: (S1) 157.76; (P) 157.94; (R1) 158.27; More...

No change in USD/JPY's outlook and intraday bias stays neutral. Further rally would be in favor as long as 154.53 support holds. Break of 158.25 will resume the choppy rise from 151.86 towards 160.20 high. But upside should be limited there, at least on first attempt.

In the bigger picture, price actions from 160.20 medium term top are seen as a corrective pattern to rise from 150.25 only. Another rally is still expected at a later stage through 160.02 to resume the larger up trend. However, decisive break of 150.87 will argue that larger correction is possibly underway, and target 146.47 support next.

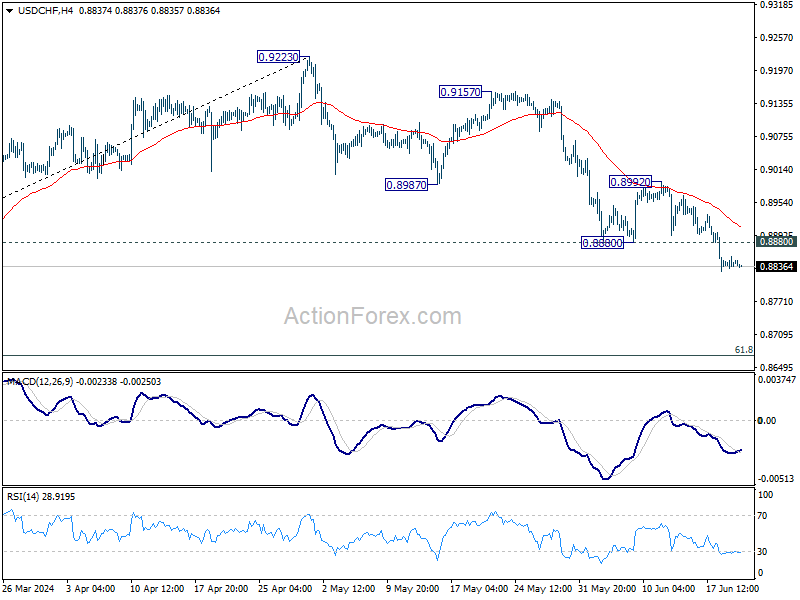

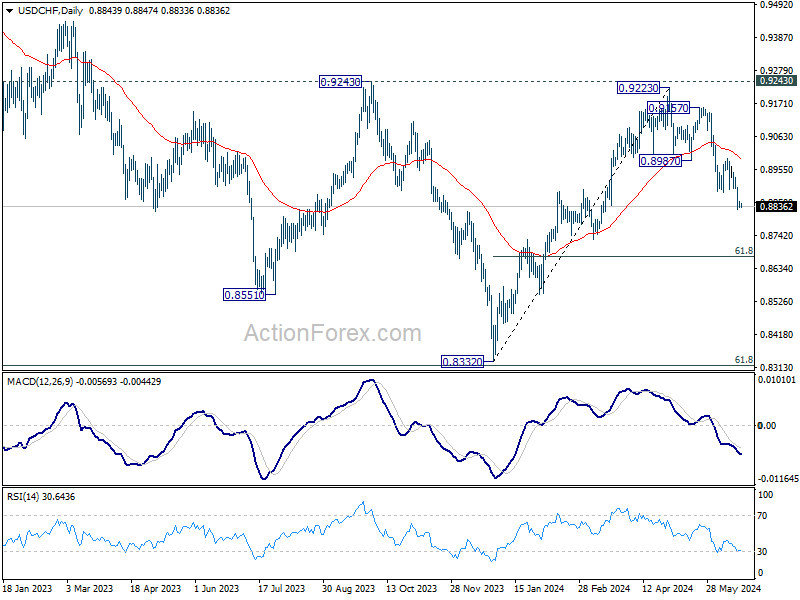

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8835; (P) 0.8845; (R1) 0.8856; More….

Intraday bias in USD/CHF remains on the downside for the moment. Fall from 0.9223 should target 61.8% retracement of 0.8332 to 0.9223 at 0.8672 next. On the upside, above 0.8880 support turned resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 0.8992 resistance holds, in case of recovery.

In the bigger picture, price actions from 0.8332 medium term bottom are seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance affirms this case, and maintains medium term bearishness. While more range trading could be seen between 0.8332/0.9243 first, downside break out is mildly in favor at a later stage.

Markets Await SNB and BoE Decisions, Gold Bounces Higher

As markets await rate decisions from SNB and then BoE today, both Swiss Franc and Sterling are trading largely within established ranges. SNB's decision is particularly uncertain, with a close call on whether they will implement a second consecutive rate cut. If SNB opts to hold rates steady, Swiss Franc could see notable gains, especially against Euro. Meanwhile, BoE is expected to keep interest rates steady today, but the details in the voting and accompanying statement could provide insights into how close the central bank is to monetary easing.

Across the forex markets, Australian Dollar remains the strongest performer of the week, although it has yet to sustain significant buying momentum. Swiss Franc is the second strongest and stands a chance to outperform Aussie, depending on SNB's decision. Euro follows as the third strongest currency. Conversely, Japanese Yen is currently the weakest, though it is holding onto near-term support against Dollar. The New Zealand Dollar is the second weakest, just ahead of Dollar. Sterling and the Canadian Dollar are positioned in the middle of the pack.

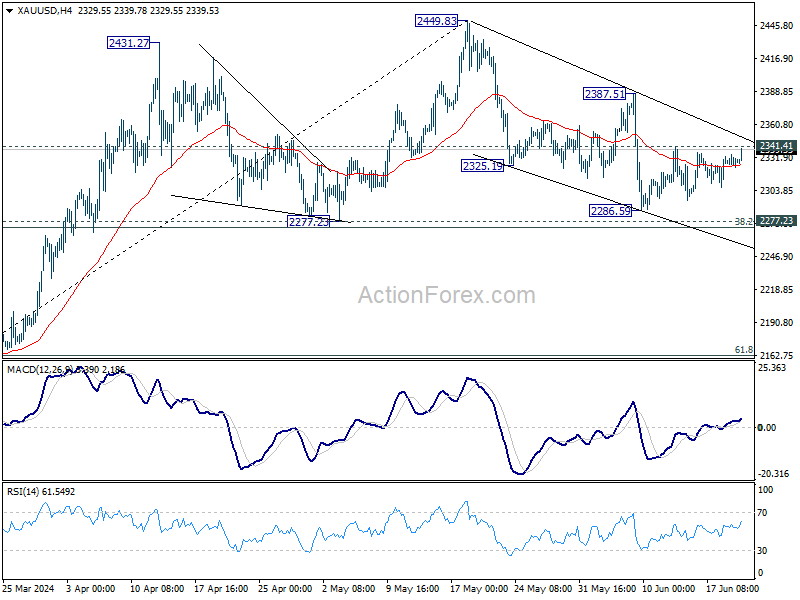

Technically, Gold is worth some attention in additional to the Pound and Franc. Gold bounces after drawing support from 55 4H EMA. Immediate focus is now on 2341.41 minor resistance. Firm break there will resume the rebound from 2286.59. More importantly, that would strengthen the case that correction from 2449.83 has completed ahead of 2277.23 cluster support. Stronger rally would then be seen to 2387.51 resistance for confirmation.

In Asia, at the time of writing, Nikkei is down -0.13%. Hong Kong HSI is down -0.48%. China Shanghai SSE is down -0.27%. Singapore Strait Times is down -0.28%. Japan 10-year JGB yield is up 0.0124 at 0.948. Overnight, the US markets were on holiday.

SNB to cut again or not? A close call

SNB is in the spotlight today as it prepares to announce rate decision which is seen as a close call. Market participants divided on whether another rate cut will be delivered, marking the second consecutive quarterly reduction.

A recent Reuters poll conducted between June 12-17 highlights the uncertainty: 22 out of 33 economists expect SNB to lower its main interest rate by 25 basis points to 1.25%, while 11 predict that SNB will hold rates steady.

The case for a rate cut is supported by the fact that inflation is currently within SNB's target range. Additionally, the central bank views its current policy stance as restrictive. However, Chair Thomas Jordan has flagged a "small upward risk" to the inflation outlook. Should this risk materialize, it would imply that the monetary policy stance might become more accommodative than SNB intends.

Adding another layer of complexity is the recent strength of Swiss Franc, which has surged due to political instability in France. A stronger Franc can help mitigate import-driven inflation, easing some of the inflationary pressures that concern SNB. On the flip side, the central bank might opt for a rate cut to weaken the Franc, thereby providing additional support to the Swiss economy.

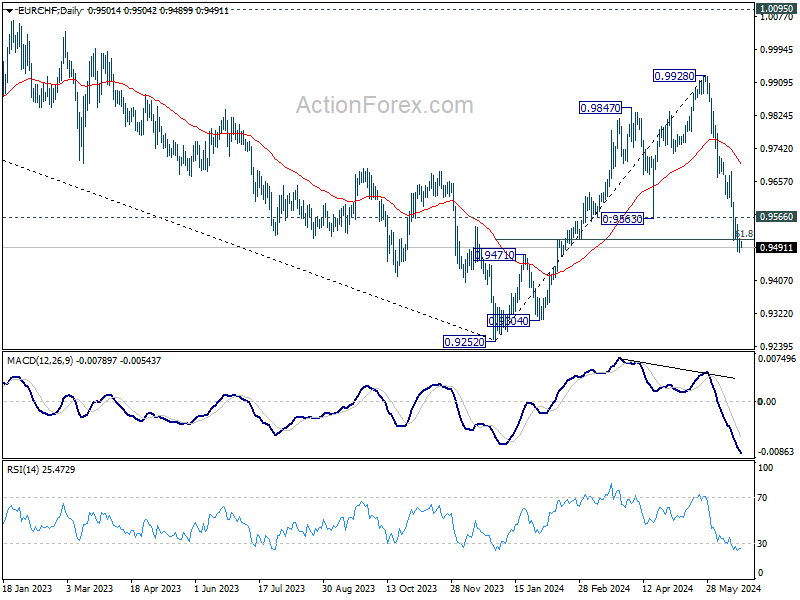

There is no sign of bottoming for EUR/CHF yet after the steep decline since late May. Further break from 61.8% retracement of 0.9252 to 0.9928 at 0.9510, as prompted by less dovish than expected SNB, could trigger more downside acceleration to retest 0.9252 low. Nevertheless, a bounce from current level, with break of 0.9566 minor resistance, would suggest that selling climax is past and bring consolidations first.

BoE to hold rates steady ahead of UK elections

BoE is widely expected to maintain interest rate at 5.25%, to avoid any perception of political interference ahead of the general election in the UK on July 4. Prime Minister Rishi Sunak's unexpected call for an early election are seen by some as indirectly giving BoE additional time to monitor inflation trends and reassess the economic outlook. A more comprehensive decision is anticipated in August, when updated economic forecasts will be available.

Inflation data for May reinforces the case for a cautious, wait-and-see approach. Headline inflation has finally returned to BoE's 2% target for the first time in almost three years, a positive development. However, services inflation remains stubbornly high at 5.7%, indicating underlying inflationary pressures that still need to be addressed.

Reflecting this development, money markets have adjusted their expectations, now pricing in only a 30% chance of a rate cut in August, down from 45% earlier in the week. There is still one quarter-point cut fully priced in for this year, likely by November, with a 60% chance of a second reduction, down from 80% earlier in the week.

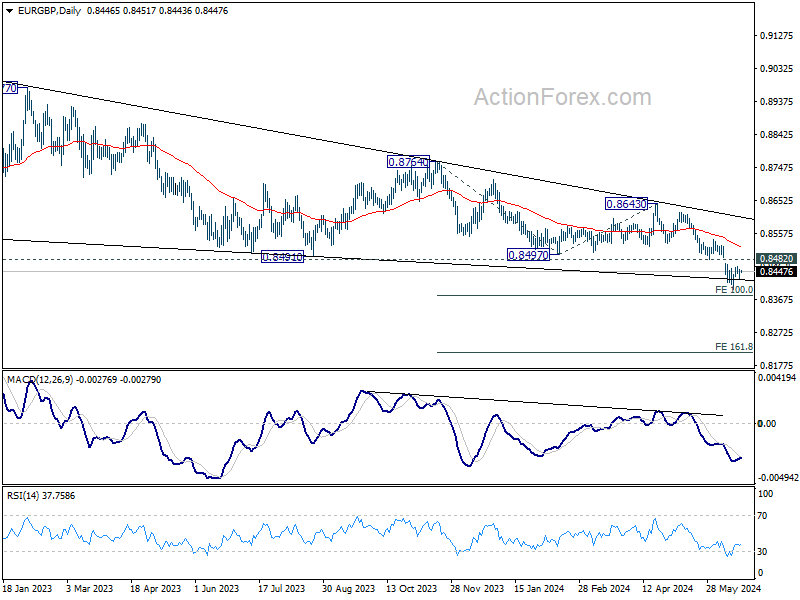

In the currency markets, EUR/GBP's declined stalled after hitting 0.8396 last week. But near term outlook will stay bearish as long as 0.8482 support turned resistance holds. Any hawkish hints from BoE today could resume the down trend through 100% projection of 0.8764 to 0.8497 from 0.8643 at 0.8376.

BoC Minutes: Sufficient progress justifies start of gradual easing

Summary of deliberations from BoC's June meeting revealed consensus among Governing Council members, who noted "four consecutive months" of easing in core inflation and indicators suggesting continued downward momentum. They concluded that there had been "sufficient progress" to warrant the initial rate cut.

BoC decided to reduce its policy rate by 25bps to 4.75% during the meeting, becoming the first G7 central bank to start monetary easing.

Council members also agreed that if inflation continues to ease and remains on a sustainable track to 2% target, it would be "reasonable to expect further cuts to the policy interest rate."

They emphasized that monetary policy easing would likely be "gradual," given the forecast that inflation will ease toward the target gradually. The timing of any further reductions in the policy rate will depend on incoming data and its implications for the future path of inflation.

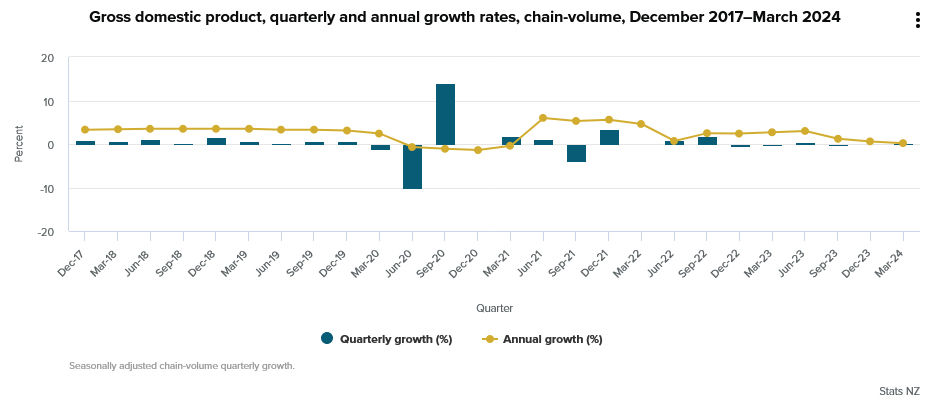

New Zealand GDP grows 0.2% qoq, pulls out of recession despite per capita decline

New Zealand's GDP grew by 0.2% qoq in Q1, surpassing the expected 0.1% growth and pulling the economy out of a technical recession following consecutive declines in the last half of 2023. On an annual basis, GDP growth was also 0.2% yoy. The primary industries experienced a modest growth of 0.2% qoq, while goods-producing industries contracted by -1.3% qoq, and services industries saw a slight decline of -0.1% qoq.

Despite the overall GDP growth, GDP per capita fell by -0.3% qoq, marking the sixth consecutive quarterly decline, with an annual decrease of -2.4% yoy. This indicates that while the economy as a whole is recovering, the average economic output per person continues to decline.

"There were a range of results at industry level, with 8 of the 16 industries rising this quarter," noted Ruvani Ratnayake, senior manager of national accounts industry and production. This mixed performance across different sectors highlights the uneven nature of the economic recovery.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8835; (P) 0.8845; (R1) 0.8856; More….

Intraday bias in USD/CHF remains on the downside for the moment. Fall from 0.9223 should target 61.8% retracement of 0.8332 to 0.9223 at 0.8672 next. On the upside, above 0.8880 support turned resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 0.8992 resistance holds, in case of recovery.

In the bigger picture, price actions from 0.8332 medium term bottom are seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance affirms this case, and maintains medium term bearishness. While more range trading could be seen between 0.8332/0.9243 first, downside break out is mildly in favor at a later stage.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | GDP Q/Q Q1 | 0.20% | 0.10% | -0.10% | |

| 01:15 | CNY | 1-y Loan Prime Rate | 3.45% | 3.45% | 3.45% | |

| 01:15 | CNY | 5-y Loan Prime Rate | 3.95% | 3.95% | 3.95% | |

| 06:00 | CHF | Trade Balance (CHF) May | 3.84B | 4.32B | ||

| 06:00 | EUR | Germany PPI M/M May | 0.10% | 0.20% | ||

| 06:00 | EUR | Germany PPI Y/Y May | -2.00% | -3.30% | ||

| 07:30 | CHF | SNB Interest Rate Decision | 1.50% | 1.50% | ||

| 08:00 | CHF | SNB Press Conference | ||||

| 08:00 | EUR | ECB Economic Bulletin | ||||

| 11:00 | GBP | BoE Interest Rate Decision | 5.25% | 5.25% | ||

| 11:00 | GBP | MPC Official Bank Rate Votes | 0--2--7 | 0--2--7 | ||

| 12:30 | CAD | New Housing Price Index M/M May | 0.20% | 0.20% | ||

| 12:30 | USD | Building Permits May | 1.46M | 1.44M | ||

| 12:30 | USD | Housing Starts May | 1.38M | 1.36M | ||

| 12:30 | USD | Current Account (USD) Q1 | -206B | -195B | ||

| 12:30 | USD | Initial Jobless Claims (Jun 14) | 240K | 242K | ||

| 12:30 | USD | Philadelphia Fed Survey Jun | 4.5 | 4.5 | ||

| 14:00 | EUR | Eurozone Consumer Confidence Jun P | -14 | -14 | ||

| 15:00 | USD | Crude Oil Inventories | -2.8M | 3.7M |

BoE to hold rates steady ahead of UK elections

BoE is widely expected to maintain interest rate at 5.25%, to avoid any perception of political interference ahead of the general election in the UK on July 4. Prime Minister Rishi Sunak's unexpected call for an early election are seen by some as indirectly giving BoE additional time to monitor inflation trends and reassess the economic outlook. A more comprehensive decision is anticipated in August, when updated economic forecasts will be available.

Inflation data for May reinforces the case for a cautious, wait-and-see approach. Headline inflation has finally returned to BoE's 2% target for the first time in almost three years, a positive development. However, services inflation remains stubbornly high at 5.7%, indicating underlying inflationary pressures that still need to be addressed.

Reflecting this development, money markets have adjusted their expectations, now pricing in only a 30% chance of a rate cut in August, down from 45% earlier in the week. There is still one quarter-point cut fully priced in for this year, likely by November, with a 60% chance of a second reduction, down from 80% earlier in the week.

In the currency markets, EUR/GBP's declined stalled after hitting 0.8396 last week. But near term outlook will stay bearish as long as 0.8482 support turned resistance holds. Any hawkish hints from BoE today could resume the down trend through 100% projection of 0.8764 to 0.8497 from 0.8643 at 0.8376.

SNB to cut again or not? A close call

SNB is in the spotlight today as it prepares to announce rate decision which is seen as a close call. Market participants divided on whether another rate cut will be delivered, marking the second consecutive quarterly reduction.

A recent Reuters poll conducted between June 12-17 highlights the uncertainty: 22 out of 33 economists expect SNB to lower its main interest rate by 25 basis points to 1.25%, while 11 predict that SNB will hold rates steady.

The case for a rate cut is supported by the fact that inflation is currently within SNB's target range. Additionally, the central bank views its current policy stance as restrictive. However, Chair Thomas Jordan has flagged a "small upward risk" to the inflation outlook. Should this risk materialize, it would imply that the monetary policy stance might become more accommodative than SNB intends.

Adding another layer of complexity is the recent strength of Swiss Franc, which has surged due to political instability in France. A stronger Franc can help mitigate import-driven inflation, easing some of the inflationary pressures that concern SNB. On the flip side, the central bank might opt for a rate cut to weaken the Franc, thereby providing additional support to the Swiss economy.

There is no sign of bottoming for EUR/CHF yet after the steep decline since late May. Further break from 61.8% retracement of 0.9252 to 0.9928 at 0.9510, as prompted by less dovish than expected SNB, could trigger more downside acceleration to retest 0.9252 low. Nevertheless, a bounce from current level, with break of 0.9566 minor resistance, would suggest that selling climax is past and bring consolidations first.

New Zealand GDP grows 0.2% qoq, pulls out of recession despite per capita decline

New Zealand's GDP grew by 0.2% qoq in Q1, surpassing the expected 0.1% growth and pulling the economy out of a technical recession following consecutive declines in the last half of 2023. On an annual basis, GDP growth was also 0.2% yoy. The primary industries experienced a modest growth of 0.2% qoq, while goods-producing industries contracted by -1.3% qoq, and services industries saw a slight decline of -0.1% qoq.

Despite the overall GDP growth, GDP per capita fell by -0.3% qoq, marking the sixth consecutive quarterly decline, with an annual decrease of -2.4% yoy. This indicates that while the economy as a whole is recovering, the average economic output per person continues to decline.

"There were a range of results at industry level, with 8 of the 16 industries rising this quarter," noted Ruvani Ratnayake, senior manager of national accounts industry and production. This mixed performance across different sectors highlights the uneven nature of the economic recovery.

.

BoC Minutes: Sufficient progress justifies start of gradual easing

Summary of deliberations from BoC's June meeting revealed consensus among Governing Council members, who noted "four consecutive months" of easing in core inflation and indicators suggesting continued downward momentum. They concluded that there had been "sufficient progress" to warrant the initial rate cut.

BoC decided to reduce its policy rate by 25bps to 4.75% during the meeting, becoming the first G7 central bank to start monetary easing.

Council members also agreed that if inflation continues to ease and remains on a sustainable track to 2% target, it would be "reasonable to expect further cuts to the policy interest rate."

They emphasized that monetary policy easing would likely be "gradual," given the forecast that inflation will ease toward the target gradually. The timing of any further reductions in the policy rate will depend on incoming data and its implications for the future path of inflation.