Sample Category Title

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2678; (P) 1.2700; (R1) 1.2730; More...

GBP/USD is still in weak recovery today and intraday bias remains neutral. Risk will stay on the downside as long as 1.2859 resistance holds. Firm break of 1.2633 resistance turned support will argue that whole rise from 1.2298 has completed, and target 1.2445 and below.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2445 support will extend the corrective pattern with another decline instead.

Sterling and Aussie Show Strength in Quiet Trading

Trading as been relatively quiet in European session today. Sterling strengthened slightly despite CPI data showing inflation returning to BoE's target for the first time in three years. Notably, services inflation remains elevated at 5.7%, which could limit the BoE's ability to aggressively ease policy, although the first rate cut is still expected in August. Market participants will closely watch tomorrow's BoE rate decision, with traders scrutinizing the statement and voting details.

Currently, Australian Dollar is the second strongest currency of the day, although it lacks strong follow through buying momentum. Euro follows as the third strongest. In contrast, New Zealand Dollar is the weakest, with traders awaiting New Zealand's GDP data in the upcoming Asian session. Yen is the second weakest, followed by Dollar, while Swiss Franc and Canadian Dollar are positioned in the middle.

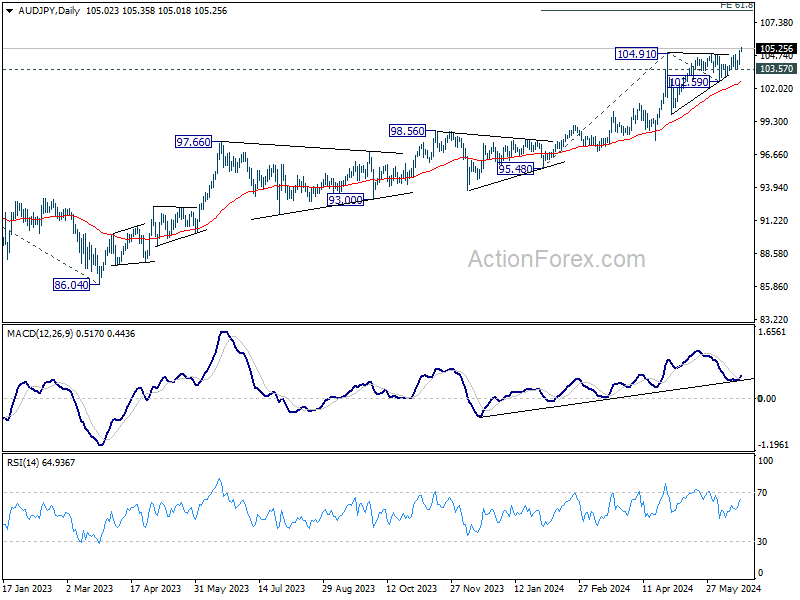

Technically, AUD/JPY is currently the top mover for the week, up more than 1%. The break of 104.91 resistance confirms long term up trend resumption. Near term outlook will stay bullish as long as 102.59 support holds. Next target is 61.8% projection of 95.48 to 104.91 from 102.59 at 108.41.

In Europe, at the time of writing, FTSE is up 0.21%. DAX is down -0.19%. CAC is down -0.51%. UK 10-year yield is up 0.0295 at 4.083. Germany 10-year yield is u 0.027 at 2.422. Earlier in Asia, Nikkei rose 0.23%. Hong Kong HSI rose 2.87%. China Shanghai SSE fell -0.40%. Singapore Strait Times rose 0.07%. Japan 10-year JGB yield fell -0.0114 to 0.936.

UK CPI slows to 2.0% in May, core CPI down to 3.5%

UK CPI slowed from 2.3% yoy to 2.0% yoy in May, lowest since July 2021. Core CPI (excluding energy, food, alcohol and tobacco) slowed from 3.9% yoy to 3.5% yoy. Both matched expectations.

CPI goods annual rate fell from - 0.8% yoy to -1.3% yoy, while CPI services annual rate eased slightly from 5.9% yoy to 5.7% yoy.

On a monthly basis, CPI rose by 0.3%, below expectation of 0.4% mom.

BoJ Minutes highlight concerns over weak Yen's impact on inflation

Minutes from BoJ's April 25-26 meeting revealed that board members are closely monitoring the ongoing risks posed by the weak Yen and its effect on inflation, which could force a monetary policy response.

"Some members" emphasized that exchange rates are crucial factors influencing economic activity and prices, suggesting that "monetary policy responses would be necessary" if there were significant changes in the economic outlook or associated risks.

One of these board members noted the "trilemma of international finance," arguing that monetary policy should not be used solely to stabilize foreign exchange rates. However, they acknowledged that if exchange rate movements impacted firms' medium- to long-term inflation expectations and corporate behavior, this could "raise the risk of prices being affected," making monetary policy adjustments "necessary."

The minutes also reflected a shared understanding among members that if underlying inflation increases in line with forecasts, BoJ would adjust its degree of monetary accommodation. Additionally, any changes in the outlook for economic activity and prices, or shifts in related risks, would warrant adjustments to the policy interest rate.

RBNZ's Conway: Inflation sticky near-term, could fall more quickly medium term

In a speech today, RBNZ Chief Economist Paul Conway discussed the complexities of bringing inflation sustainably back to target, noting "remaining challenges" and various risks and uncertainties.

Conway pointed out that in the "near term", inflation might be "more persistent" than current projections suggest. He highlighted that domestic or non-tradables inflation and services sector inflation have remained higher than expected, indicating a "sticky" inflationary environment.

Conversely, Conway also sees potential for inflation to "fall more quickly" than anticipated over the "medium term". Factors such as increasing spare capacity in product and labor markets and shifting business and household inflation expectations could accelerate the decline in inflation.

He explained that RBNZ's current policy strategy is "balancing these opposing factors." The bank will closely monitor indicators of core inflation, non-tradables inflation, services inflation, and inflation expectations to assess how these risks unfold. The labor market will also be a critical signal of capacity pressure.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2678; (P) 1.2700; (R1) 1.2730; More...

GBP/USD is still in weak recovery today and intraday bias remains neutral. Risk will stay on the downside as long as 1.2859 resistance holds. Firm break of 1.2633 resistance turned support will argue that whole rise from 1.2298 has completed, and target 1.2445 and below.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2445 support will extend the corrective pattern with another decline instead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Current Account (NZD) Q1 | -4.36B | -4.65B | -7.84B | -7.98B |

| 23:50 | JPY | Trade Balance (JPY) May | -0.62T | -0.63T | -0.56T | |

| 23:50 | JPY | BoJ Minutes | ||||

| 06:00 | GBP | CPI M/M May | 0.30% | 0.40% | 0.30% | |

| 06:00 | GBP | CPI Y/Y May | 2.00% | 2.00% | 2.30% | |

| 06:00 | GBP | Core CPI Y/Y May | 3.50% | 3.50% | 3.90% | |

| 06:00 | GBP | RPI M/M May | 0.40% | 0.50% | 0.50% | |

| 06:00 | GBP | RPI Y/Y May | 3.00% | 3.10% | 3.30% | |

| 06:00 | GBP | PPI Input M/M May | 0% | -0.20% | 0.60% | 0.80% |

| 06:00 | GBP | PPI Input Y/Y May | -0.10% | -1.60% | -1.40% | |

| 06:00 | GBP | PPI Output M/M May | -0.10% | 0.10% | 0.20% | 0.30% |

| 06:00 | GBP | PPI Output Y/Y May | 1.70% | 1.10% | ||

| 06:00 | GBP | PPI Core Output M/M May | 0.20% | 0.00% | 0.20% | |

| 06:00 | GBP | PPI Core Output Y/Y May | 1.00% | 0.20% | 0.30% | |

| 08:00 | EUR | Eurozone Current Account (EUR) Apr | 38.6B | 35.2B | 35.8B | |

| 14:00 | USD | NAHB Housing Index Jun | 46 | 45 | ||

| 17:30 | CAD | BoC Summary of Deliberations |

New Zealand Dollar Faces Growth Challenges

The NZD/USD pair declined to 0.6135 on Wednesday, despite the New Zealand dollar performing much better in the previous session. It rose in response to the fall of the US dollar, which was triggered by weaker-than-expected US retail sales data. These results increased bets on an imminent reduction in the cost of lending by the Federal Reserve System. This caused the USD to retreat, allowing other currencies to rise.

Today, Paul Conway, the chief economist of the Reserve Bank of New Zealand, announced that the process of returning inflation to the target is progressing well. The ongoing softening of the employment sector is releasing spare capacity in the economy, likely leading to a further reduction in inflationary pressure in the economic system.

At the same time, Conway noted that the inflation reduction process may not follow the predicted timeline. An extended period of maintaining a restrictive monetary policy is necessary to achieve a lasting result, a crucial step to ensure the goal is met. The market's attention will now shift to the upcoming Q1 GDP statistics. The data may reflect a fairly modest increase, which could hurt the NZD.

Technical analysis of NZD/USD

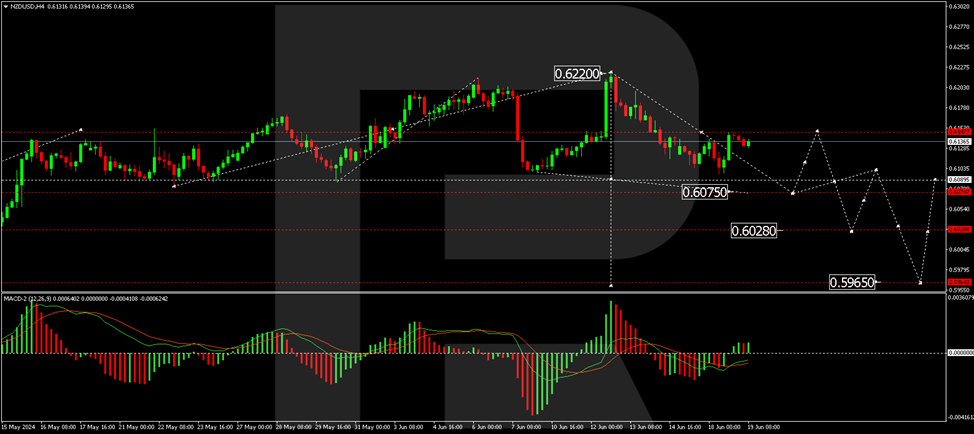

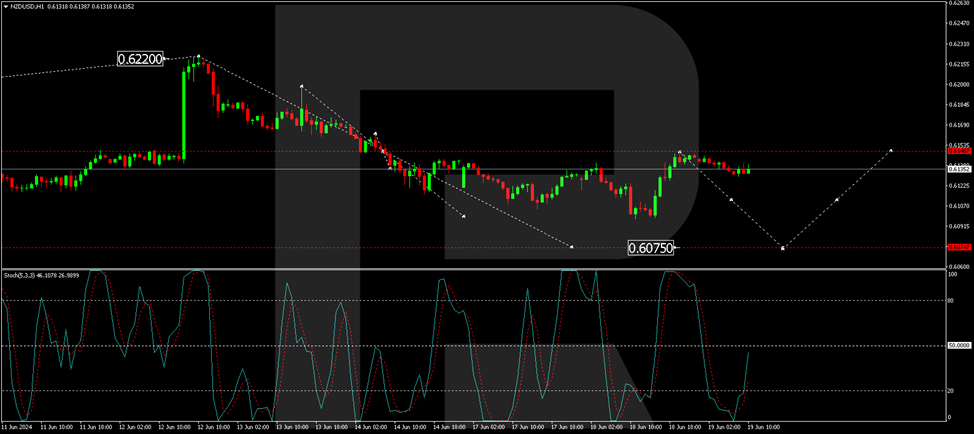

On the H4 NZD/USD chart, the market executed a wave of decline to the level of 0.6097 and a correction to the level of 0.6148. Today, we expect another downward trend to 0.6075, the first goal. After reaching this level, a correction to 0.6140 is possible (testing from below). Next, we will consider a new wave of decline to 0.6028, the local target. This scenario is technically confirmed by the MACD indicator, as its signal line is below the zero mark. An update of the lows is expected.

On the H1 NZD/USD chart, a correction has formed to 0.6148 (testing from below). Today, we expect a decrease to 0.6111. The breakdown of this level will open the potential for a downward trend to 0.6075. Technically, this scenario is also confirmed by the Stochastic oscillator. Its signal line is below the 50 mark, and another decline to the level of 20 is expected.

NZ Dollar Eyes First-Quarter GDP

The New Zealand dollar is steady on Tuesday. NZD/USD is trading at 0.6138, down 0.10% in the European session at the time of writing. US markets are closed for a holiday. New Zealand will release first-quarter GDP early on Thursday.

Is New Zealand still in recession?

There is some uncertainty over what to expect from Tuesday’s GDP report. The markets are expecting the New Zealand economy to have flatlined in the first quarter. The major New Zealand banks are divided, with some projecting a 0.1% gain while others have forecast a -0.1% decline. There is no argument, however, that the economy is in the deep doldrums, having contracted in four of the past five quarters, including the past two quarters. Another decline from Q1 GDP would extend the technical recession.

For the Reserve Bank of New Zealand, a GDP of zero or close to it points to a weak economy, which will support a rate cut sooner rather than later. The RBNZ has been hawkish, insisting that it won’t cut rates before inflation is reined in. Policy makers are willing to consider trimming rates if inflation is within the target band of 1% to 3%, even if it is above the 2% midpoint. Currently, the inflation rate is at 4.0% and that’s simply too high for the central bank to start cutting rates.

The RBNZ has held rates at 5.5% at seven consecutive meetings and another hold is likely at the next meeting on July 10th. At the May meeting, members discussed the possibility of hiking rates, but like the Reserve Bank of Australia, decided against it.

NZD/USD Technical

- NZD/USD is tested support at 0.6130. Below, there is support at 0.6111

- 0.6163 and 0.6182 are the next lines of resistance

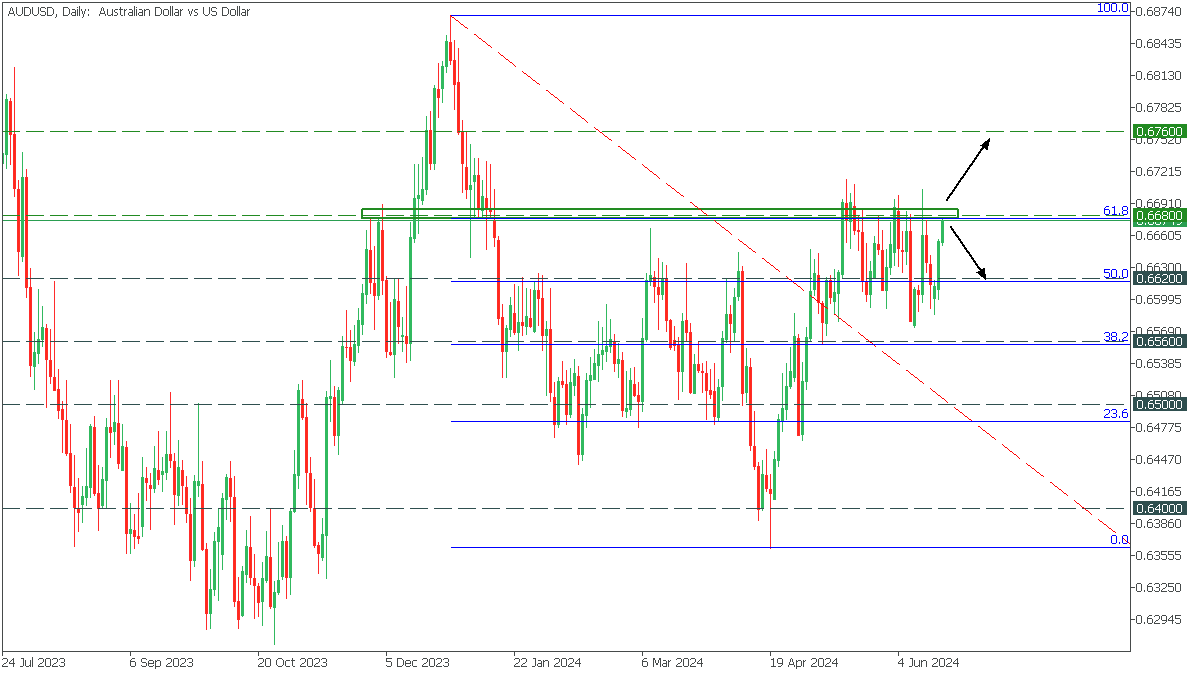

AUDUSD: Strong Zone

In the Daily Timeframe, AUDUSD started a short-term bullish trend after a long-term decline. The price has reached the critical 61.8 Fibonacci resistance area, and despite the growing bullish sentiment, two scenarios should be considered.

- If the bulls push the price above 0.6680, the upside target will be 0.6760;

- A rebound from the resistance will start the correction to the support at 0.6620;

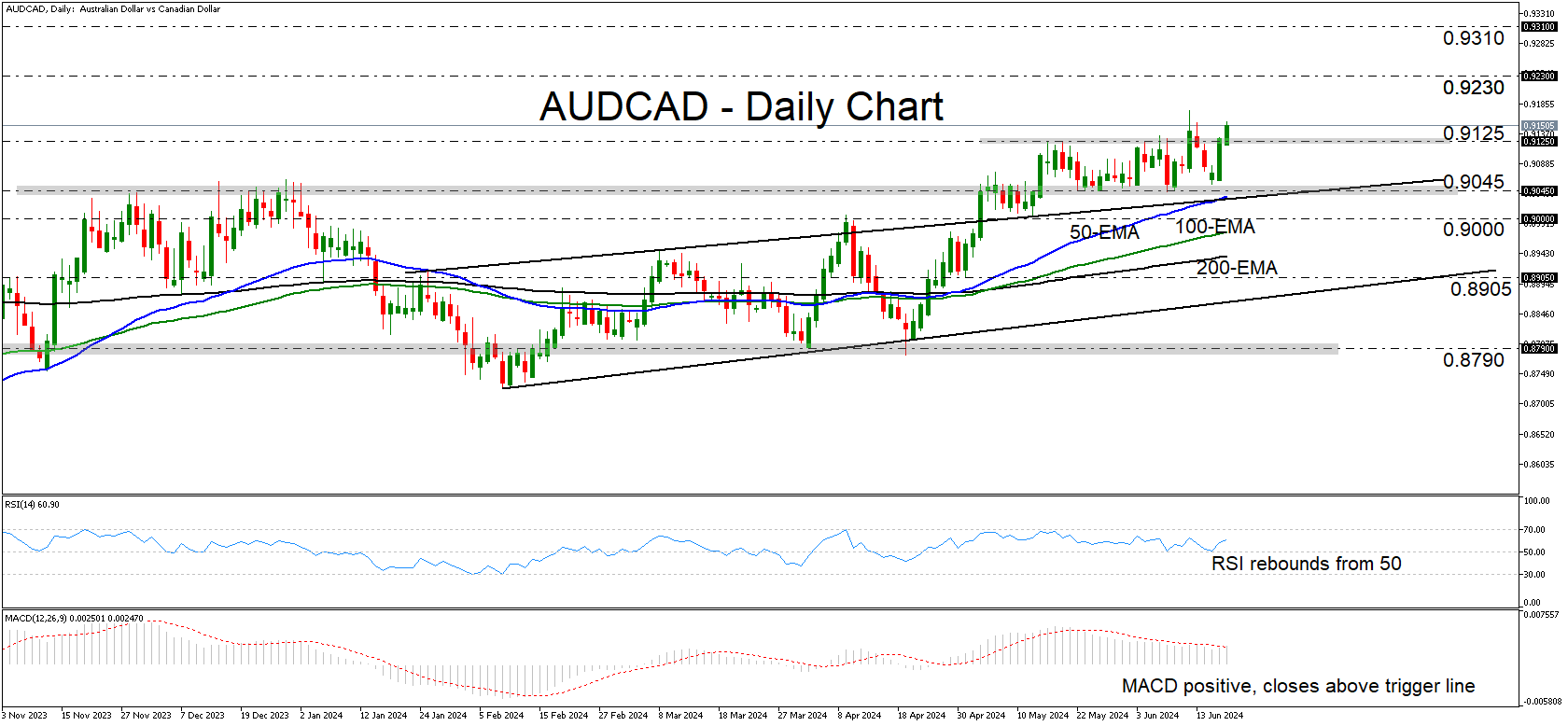

AUDCAD Bulls Stay in the Driver’s Seat

- AUDCAD rebounds and breaks above 0.9125

- Overall, it remains above a prior upside channel

- The advance may continue towards the 0.9230 zone

- A dip below 0.9000 could signal a bearish correction

AUDCAD rebounded strongly on Tuesday, extending its recovery above the key resistance zone of 0.9125. Overall, the pair is trading above the upper bound of a prior upward sloping channel and above all three of the plotted exponential moving averages (EMA). This paints a positive picture.

The daily momentum indicators corroborate the bullish outlook. The RSI rebounded from near its 50 line and it is pointing up, while the MACD, already positive, has just poked its nose above its trigger line.

On June 12, the pair broke above the 0.9125 zone, but the bulls were unable to maintain momentum, resulting in a false breakout. If they are stronger this time around and decide to stay in charge, they may push the action up to the 0.9230 zone, marked by the highs of March 22 and 23, 2023. A break higher could pave the way towards the 0.9310 zone, defined as resistance by the highs of February 20 and 21, 2023.

On the downside, a dip back below the round figure of 0.9000 may confirm the pair’s return within the aforementioned channel and thereby allow a larger bearish correction. However, for the bigger picture to turn negative, a dip below 0.8905 may be needed.

To recap, AUDCAD rebounded strongly yesterday, with the rebound extending above 0.9125, which suggests that further advances may be on the cards.

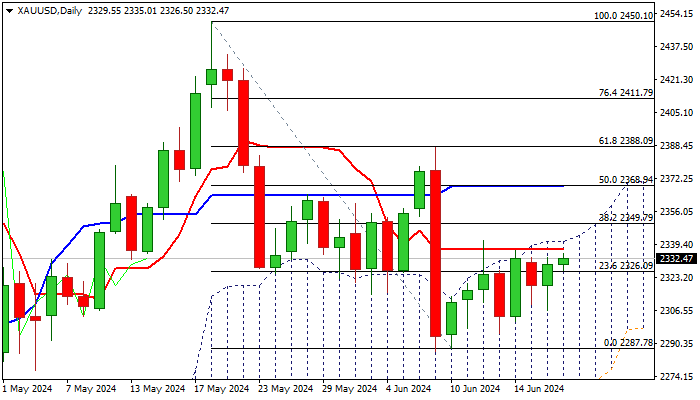

XAU/USD: Gold Price Edges Higher But Still Capped Under Key Barrier

Gold price edged higher in early Wednesday’s trading after softer than expected US retail sales numbers improved the sentiment on fresh expectations for Fed rate cut this year.

The price is holding near pivotal barrier at $2341 (recent range ceiling /top of ascending daily Ichimoku cloud), which caps for the eighth consecutive day.

Technical studies on daily chart remain bearishly aligned (14-d momentum in negative territory /daily Tenkan/Kijun-sen in bearish setup) and the downside is expected to remain vulnerable as long as price action stays below cloud top.

In such scenario, we can expect prolonged sideways near-term mode, with renewed attack at range floor ($2287) not ruled out, if fundamentals weaken.

Loss of $2287 pivot would spark stronger acceleration lower, as this will complete a failure swing pattern, as well as asymmetric Head and Shoulders pattern ($2287 also marks the neckline).

Conversely, sustained break above cloud top would generate bullish signal which will require confirmation on break of $2349 (Fibo 38.2% of $2450/$2287) to open way towards targets at $2368 and $2388 (Fibo 50% and 61.8% respectively).

Res: 2337; 2341; 2349; 2368.

Sup: 2326; 2300; 2287; 2272.

UK Inflation Back at 2% But Services Inflation Remains a Concern, GBP/USD Rises

UK Inflation Rate:

- UK Inflation Rate YoY reaches 2% yet services inflation poses a challenge.

- UK Core Inflation Rate YoY 3.5% down from a previous print of 3.9%.

- GBP/USD rises as 1.2750 resistance area beckons.

The Bank of England (BoE) will likely have mixed feelings this morning following the release of the May inflation report. Inflation has hit the Central Bank’s 2% target for the first time in nearly 3 years but the gap between goods and services inflation is a concern.

As always though one has to look at the entire picture and delve deeper into the data. Underlying price pressures in the service sector remains a particular sticking point coming in at 5.7%. The BoE believes that this figure gives a better picture of the medium term inflation risks and could be the reason we are seeing a rise in the GBP this morning as well as mixed reactions regarding the timing of a first rate cut from the BoE.

If we take a look at the different sectors, the drop in inflation was led by a slowdown in food, with prices falling this year but rising a year ago; the largest upward contribution came from motor fuels, with prices rising slightly this year but falling a year ago. Core CPI (excluding energy, food, alcohol and tobacco) rose by 3.5% in the 12 months to May 2024, down from 3.9% in April. The CPI goods annual rate fell from negative 0.8% to negative 1.3%, while the CPI services annual rate eased from 5.9% to 5.7%.

Bank of England Conundrum

The Bank of England (BoE) is well aware that the fight against inflation is far from over. The data released today is unlikely to result in a rate cut at tomorrow’s BoE monetary policy committee meeting. The BoE has in the past stated a return of inflation to its target is not enough on its own for rate cuts to begin. The uncomfortably high services inflation prints continues to be the major stumbling block as the gap between services and goods inflation is the widest on record all the way back to 1990.

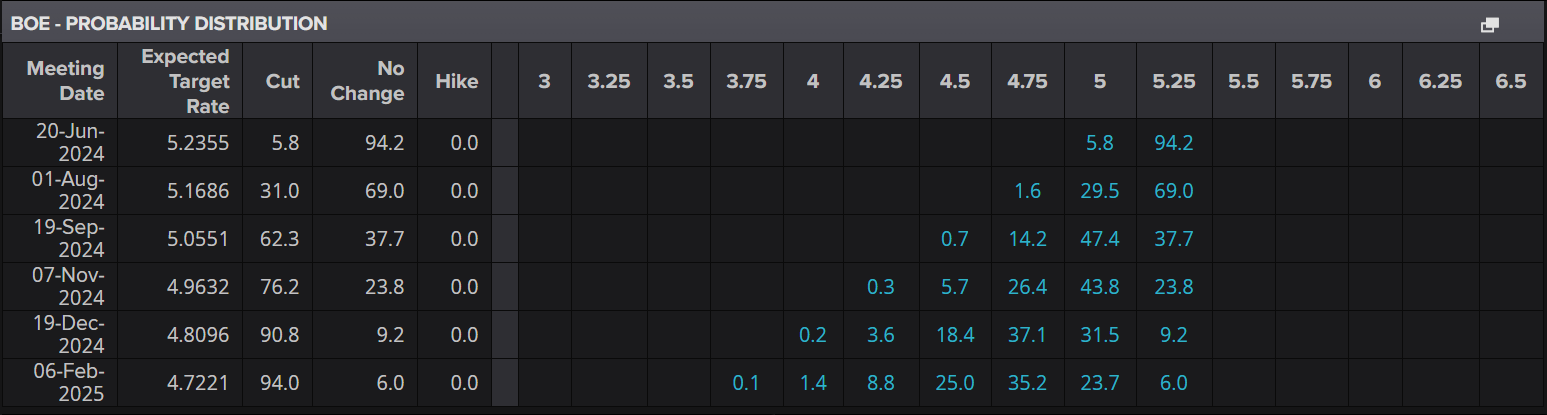

Interest Rate Probabilities for the Bank of England (BoE)

Source: LSEG Eikon (click to enlarge)

The likelihood of a rate cut tomorrow is 5.9%, while a rate cut in August is not guaranteed, currently standing at 31.2%. September appears the most probable for a rate adjustment at this stage. Since Covid-19, central banks have struggled with accurate predictions due to conflicting data releases. This uncertainty leaves market participants puzzled, so I would advise against making bold predictions and suggest instead basing assessments on upcoming data releases.

Market Reaction

The immediate reaction to the data release has been a positive one for the GBP. Cable pushed away from the 1.2700 handle rising to a high of 1.2732 before taking a pause as market participants eye the potential for further gains with the US bank holiday today. Looking at the H4 chart below and immediate resistance rests at the 1.2750 handle with a break beyond that opening up a retest of the 1.2800 or the most recent highs around 1.2850.

Alternatively, a rejection at resistance or a push lower from current price will see cable needing to navigate its way below the 1.2680 support area before eyeing the recent lows at 1.2650. A break of these lows could open cable up to a much deeper retracement with the next significant support area around the 1.2560 handle.

GBP/USD Daily Chart, June 19, 2024

Source: Tradingview.com (click to enlarge)

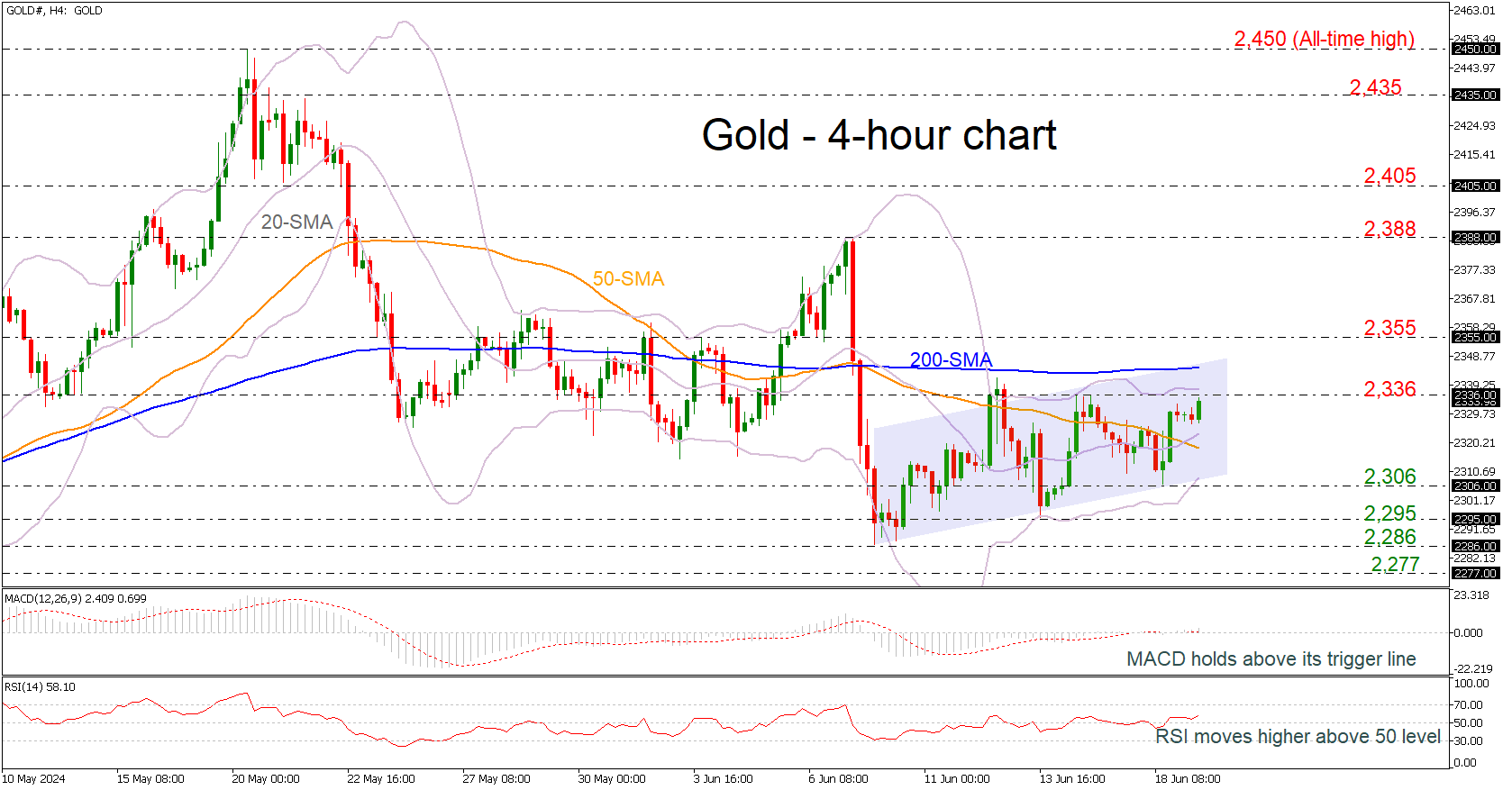

Gold Flirts With Upper Bollinger Band

- Gold consolidates within ascending channel

- 20- and 50-period SMA post bullish cross

- MACD and RSI head higher

Gold prices have been developing within an upward sloping channel in the short-term view with strong resistance at 2,336 and the 200-period simple moving average (SMA) at 2,345.

The mid-level of the Bollinger band (20-period SMA) and the 50-period SMA posted a bullish crossover, and the technical oscillators are heading north. The MACD is standing slightly above its trigger line above the zero level, while the RSI is ticking up beyond the 50 level.

Immediate resistance comes from 2,336 and the 200-period SMA at 2,345, where also the upper Bollinger band lies. Even higher, a climb above the 2,355 bar could endorse the bullish retracement.

On the other hand, a drop below the SMAs could open the way for a retest of the lower Bollinger band around the 2,306 support. Lower, the support levels of 2,295 and 2,286 may halt bearish actions.

To summarize, the precious metal has lost its strong bullish momentum and any declines below 2,286 could endorse the scenario for further decreases.

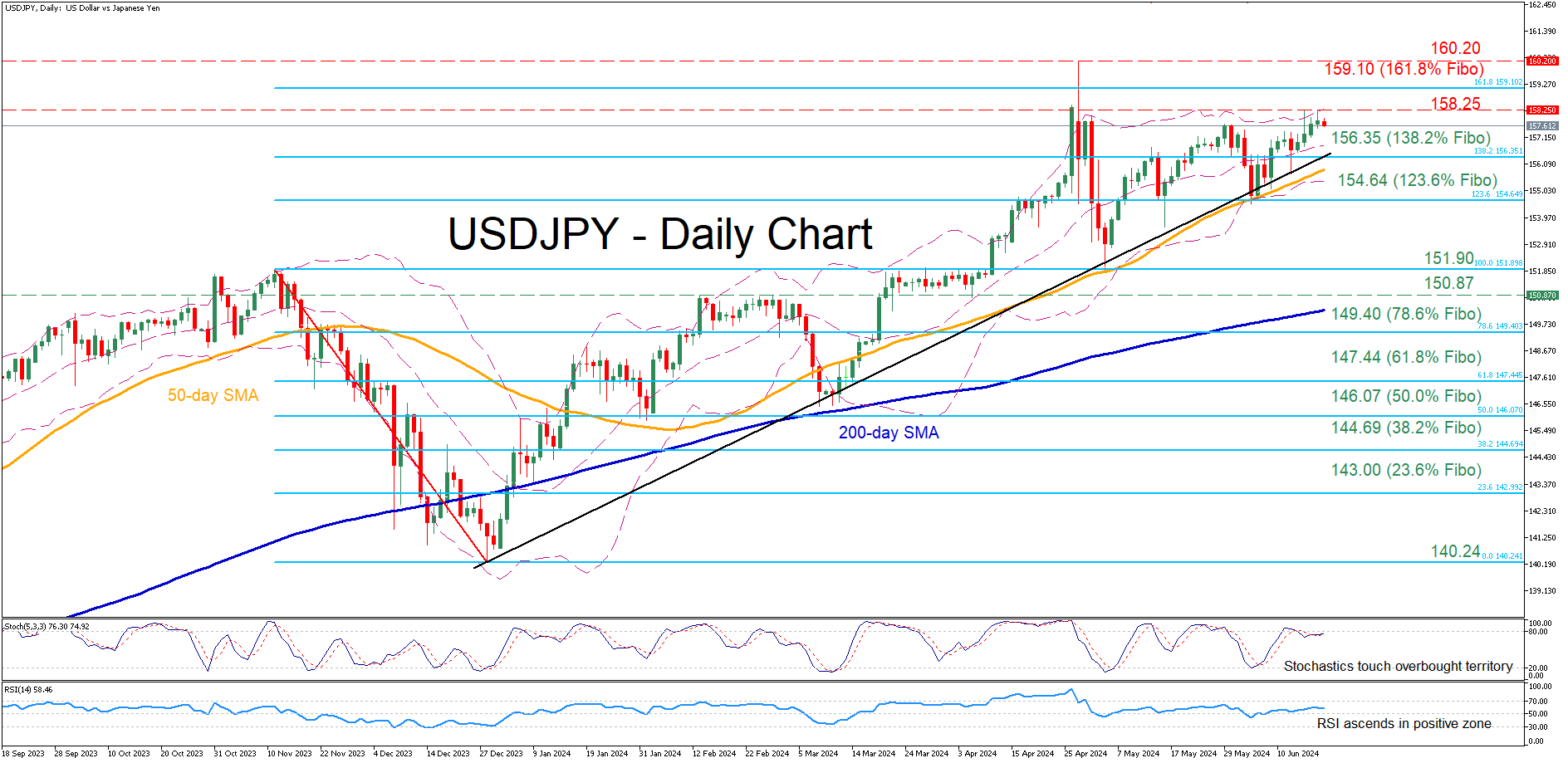

USDJPY Reapproaches Multi-Year Highs

- USDJPY in a steady advance after pullback halts at 50-day SMA

- Momentum indicators are strengthening in their positive zones

USDJPY experienced a strong setback from its 34-year high of 160.20 following an intervention by Japanese authorities in late April. However, the pair has been in a steady uptrend since then, attempting to revisit its recent multi-year highs.

Should bullish pressures persist, the price could initially test the recent resistance of 158.25. Further upside attempts could then cease at 159.10, which is the 161.8% Fibonacci extension of the 151.90-140.24 downleg. A violation of that territory could pave the way for the 34-year peak of 160.20.

Alternatively, if the pair comes under selling pressure, immediate support could be found at the 138.2% Fibo of 156.35. Failing to halt there, the price could descend towards the 123.6% Fibo of 154.64. In case the bears push the pair even lower, the May deflection point of 151.90 may provide downside protection.

In brief, despite the strong selloff in the aftermath of a fresh 34-year peak, USDJPY has been steadily regaining lost ground. Therefore, we could see some heightened volatility moving forward as the price is approaching levels that the Japanese side was willing to defend in the recent past.