Sample Category Title

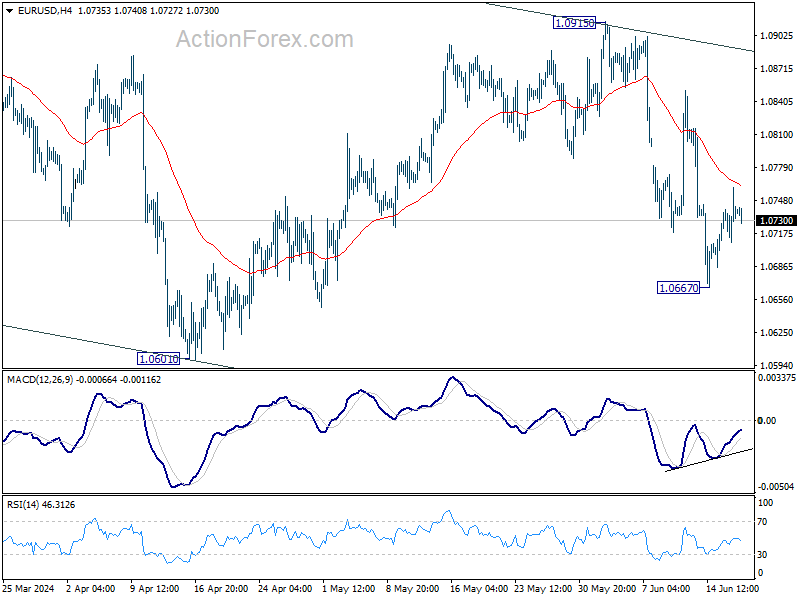

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0713; (P) 1.0737; (R1) 1.0765; More....

Intraday bias in EUR/USD remains neutral and outlook is unchanged. More consolidations could be seen but further fall is expected as long as 55 4H EMA (now at 1.0763) holds. Fall from 1.0915 is seen as another leg in the larger corrective pattern. Below 1.0677 will target 1.0601 low first. Firm break there will target channel support at 1.0500 next.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's still in progress. Break of 1.0601 will target 1.0447 support and possibly further to 100% projection of 1.1274 to 1.0447 from 1.1138 at 1.0311. For now, this will remain the favored case as long as 1.0915 resistance holds, in case of rebound.

BoE Still Has Work to Do to Bring Inflation Back Under Control

Markets

Market focus shifted back to the US yesterday. After last week’s softer than expected price data, US retail sales for the second consecutive month suggested that consumer demand might be slowing. It could point to a better supply-demand balance that might help inflation to slow further. May headline sales only rose a meagre 0.1% M/M coming on the back of a (downwardly) revised 0.2% decline in April. Control group sales, seen as a proxy for private consumption in GDP calculations, rebounded 0.4% (vs 0.5% consensus), but this wasn’t enough to reverse last months -0.5% decline. After a limited rebound on Monday, US yields again ceded between 6 bps (5-y) and 5 bps (30-y). US yields across the curve are again closing in on the lows touched end last week (2-y 4.71%, 10-y 4.22%, 30-y 4.35%). Money markets discount two 25 bps rate cuts by the end of the year. A long line up of Fed governors (with individual nuances) reiterated they need more than one month of better inflation data to be confident to start an easing cycle. European/German bond yields early in the session tried to regain some ground after the recent safe have decline, but this was also reversed after the US data. German yields eased between 0.9 bps (5-y) and 2.3 bps (30-y). Some (temporary) calm also returned to intra-EMU bond markets The French 10-y yield spread (vs Germany) narrowed 2 bps (to 77 bps). A similar easing was seen for the likes of Greece (-4 bps), Italy (-3 bps), Spain and Portugal (-2 bps). European equities also tried to move away from last week’s lows (EuroStoxx 50 + 0.72%). The S&P 500 and the Nasdaq again finished at (marginally higher) closing record levels. The dollar after the US retail sales data reversed earlier intraday gains, but in the end any losses were limited (DXY close 105.26, EUR/USD 1.0740). USD/JPY even closed slightly stronger at 157.86.

US markets are closed today for the Junetheenth holiday and there are few data in EMU. Except for important news from the political scene in France, trading in European markets probably will be technical in nature. The EU commission is expected to open an excessive debt procedure against seven member states, including France. This comes as no surprise but won’t help to restore calm on intra-EMU (bonds) markets.

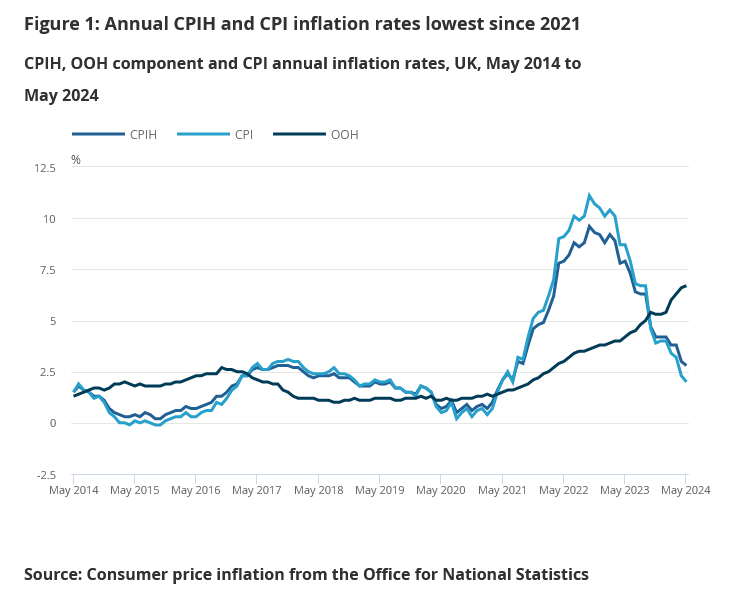

UK May CPI data were close to expectations this morning. Headline CPI eased to 0.3% M/M bringing the Y/Y measure exactly at the 2% BoE target. Core inflation also, as expected, eased to 3.5% from 3.9%. Still the decline in services inflation (5.7% from 5.9%) was less than hoped for. Even as the inflation target for the headline figure has been reached, underlying data suggested that the BoE still has work to do to bring inflation back under control in a sustainable way. This suggests balanced communication at tomorrow’s BoE policy meeting. In a first reaction, sterling tentatively gains a few ticks (EUR/GBP 0.8446).

News & Views

The US’ Congressional Budget Office jacked up its deficit forecast for the running fiscal year (through September) by about 27% to a whopping $1.92tn, or 6.7% of GDP. Doing so the nonpartisan budget watchdog no longer expects the deficit to shrink compared to last FY ($1.69tn, 6.3% of GDP). The new estimate is some $400 bn higher than February’s and reflects additional spending for Ukraine, the Biden administration student-loan relief plans as well as an increase in estimated Medicaid spending. In the updated 10 year outlook, the CBO is projecting deficits equal or in excess of 5.5%. “Since at least 1930, deficits have not remained that large for more than five years in a row.”, the CBO said in an umpteenth warning to the unsustainable fiscal situation. The new economic forecasts assume faster growth (2%) and inflation (2.7% vs 2.1% in the February forecast), leading the CBO to be more cautious on Fed rate cuts. They now expect a first move to happen in 2025Q1 vs mid-2024 previously.

Japan’s Ministry of Finance is considering a shift towards issuing bonds with shorter maturities, Bloomberg reported this morning based on draft proposal. It would mean a major policy shift from the past where the ministry tended to extend the maturity of debt, locking in the extremely low (and negative) rates for as long as possible. The proposal comes after the BoJ recently abandoned its yield curve programme, raised its policy rate out of negative territory and is planning to cut bond purchases from the current JPY 6tn per month. Yields across the spectrum have risen, especially at the long end of the curve as a result.

Graphs

GE 10y yield

The ECB cut its key policy rates by 25 bps at the June policy meeting. A more bumpy inflation path in H2 2024, the EMU economy gradually regaining traction and the Fed’s higher for longer US strategy make follow-up moves difficult. Markets are coming to terms with that. For the time being, though, the political narrative dominates. After hitting a new YtD top at 2.7%, the German 10-yr yield corrected lower on safe haven bids.

US 10y yield

The Fed is seeking more evidence than just one slower-than-expected (May) CPI is providing. Upgraded inflation forecasts and a higher neutral rate complicate the exact timing of a first cut further. June dots suggest one move in 2024 followed by four more next year. Markets are positioned more aggressively, turning the recent low in yields into a technical support zone. The US 10-y yield is testing the downside of the 4.2/4.7% trading range.

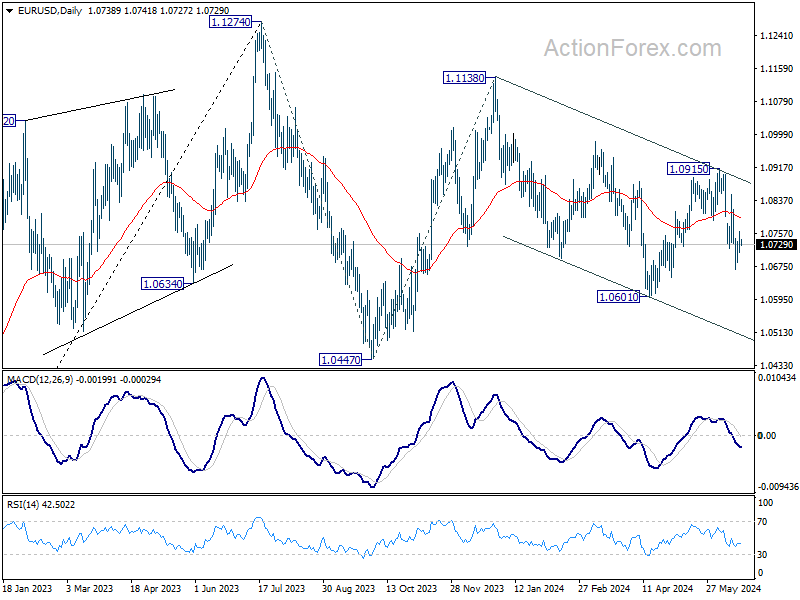

EUR/USD

EUR/USD is trapped in the 1.06-1.09 range. The desynchronized rate cut cycle with the ECB exceptionally taking the lead, strong US May payrolls and a swing to the right in European elections pulled the pair away from 1.09 resistance. The Fed meeting balanced the weaker than expected US CPI outcome. Euro fragility makes a return to the 1.06 downside more likely than not.

EUR/GBP

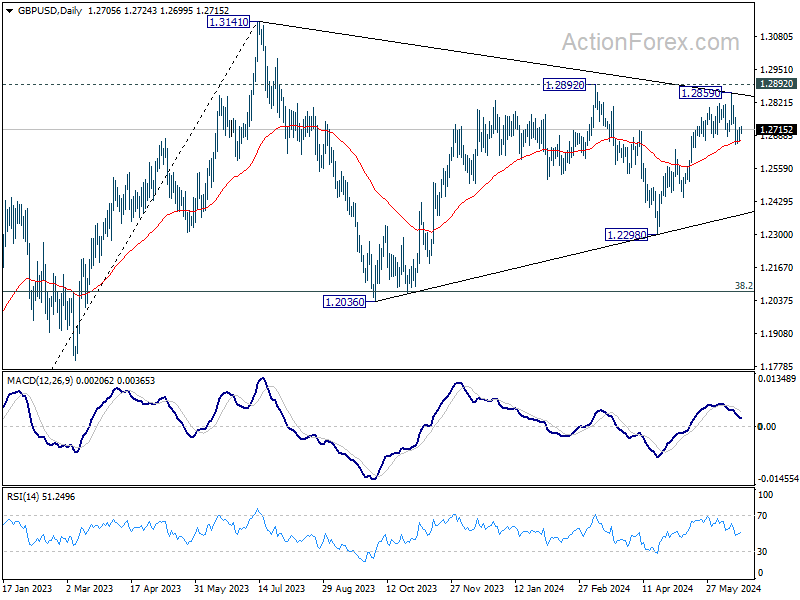

Debate at the Bank of England is focused at the timing of rate cuts. Slower than expected April disinflation and a surprise general election on July 4 suggest that a June cut in line with the ECB looks improbable. Sterling gained momentum with money markets now discounting a Fed-like scenario. EUR/GBP tested the 2023 & 2024 lows near 0.85. Euro weakness eventually pulled the trick after French president Macron called snap elections following a weak showing in EU elections.

Inflation in UK Hit BoE 2% Inflation Goal

Nvidia finally stole the title of the world’s most valuable company from Microsoft and Apple yesterday following a beautiful 3.5% rally that propelled the share price past $135 a share. The catalyst was just a bullish call from an analyst at Rosenblatt Securities who revised his PT up to $200 from $140 and said that its market cap will reach $5 trillion in the coming year - probably the Wall Street version of Roaring Kitty…

Beyond tech

According to Bloomberg, the Magnificent Seven have contributed to more than 60% of the S&P500’s return so far this year. The rest is not doing as well. The S&P500’s equal weight index is stagnating, the reflation trade is weakening along with cautious Federal Reserve (Fed) talk and mixed economic data, there is still a chance that we see a sharp economic slowdown in the US as a result of a painful tightening cycle.

Data yesterday showed that retail sales in the US barely increased in May, last two month figures were revised to the downside and core retail sales even fell 0.1% from the month earlier. Industrial production on the other hand jumped more than expected. The data was supportive of the Fed doves and sent the US 2-year yield down below the 4.70% shortly, the 10-year yield fell to 4.20%. A strong sale of US 20-year paper also boosted appetite before US markets went on a short one-day break.

European and the British stocks rebounded yesterday on the back of encouraging data from the US and a jump in oil prices for the FTSE 100. Crude oil jumped past its 50, 100 and 200-DMA since Monday and is consolidating gains above the $81pb level on the back of geopolitical tensions in the Middle East, increased fuel demand in summer and tight supply policy from OPEC. Interestingly, the 2.3-mio barrel rise in US oil inventories last week (according to the latest API data) didn’t discourage oil bulls from carrying the rally above the $80pb psychological level.

On the data front, inflation in the Eurozone ticked slightly higher in May, as expected, while sentiment in Germany remained quite weak. The EURUSD recovered a part of last week’s losses but the main catalyzer of the gains was a broadly softer US dollar. The euro remains subject to political risks.

Goal

Inflation in the UK hit the Bank of England’s (BoE) 2% inflation goal and fueled speculation that the BoE could announce a surprise rate cut when it meets tomorrow. Sterling’s kneejerk reaction was surprisingly positive, however. There is little chance that tomorrow will bring a rate cut in the UK (as inflation is expected to head back to 2.5% in H2) but the thought of it could keep sterling bulls under control until tomorrow’s MPC decision.

Investors’ Focus Will be on Europe

In focus today

In the euro area, the EU commission will reveal against which countries it recommends opening an excessive deficit procedure (EDF) due to breaches of the EU fiscal rules. The Commission will most likely recommend opening an EDP against France, which is to be expected due to France's public finances.

In the UK, inflation figures for May are released, with headline inflation expected to edge down to 2% y/y. Overall, we do not expect the inflation print to affect the immediate policy decision on tomorrow's monetary policy meeting, but it will prove important in terms of guidance for the future rate path.

The Swedish LFS labour market data is scheduled for release at 08:00 CET. In April the unemployment rate stood at 8.5%. However, it must be noted that these data are volatile on a monthly basis and should be taken with a pinch of salt. Moreover, NIER presents its new macroeconomic forecasts at 09:15 CET.

Economic and market news

What happened overnight

In Japan, the minutes from the BoJ's April monetary policy meeting was released. Some officials noted the weak yen's contribution to inflation, emphasizing that the BoJ must respond with monetary policy if exchange rate movements alter its view on the outlook and risks. The market reaction was muted, with USD/JPY trading somewhat higher.

What happened yesterday

In the US, May's retail sales were weaker than expected at 0.1% m/m SA (cons: 0.3%). The weak print could partly stem from the volatile seasonal adjustment factor, which was more negative in May compared to recent years. The core measure of retail sales, namely control group sales, was as expected at 0.4% m/m SA, but April figures were revised lower. While the negative print aligns with weaker data seen lately, we believe this does not signal a sharp weakening in US growth prospects.

Several Fed speakers shared their views after last week's FOMC meeting. NY Fed President Williams (hawk and voting member) mentioned that interest rates will come lower over the next couple of years as inflation approaches the 2% target, but refrained from hinting when the Fed could initiate its cutting cycle. Williams emphasized that policy path depends on incoming data.

St. Louis President Musalem (hawk and non-voting member) stated that the Fed needs sustained lower inflation, moderating demand, and expanding supply before considering rate cuts, which could take several months or even quarters. In a similar vein, Richmond Fed's Barkin (hawk and voting member) stressed the necessity of inflation moving sustainably down to 2% before contemplating policy rate changes, while Boston Fed President Collins (hawk and non-voting member) cautioned that the Fed must remain patient when considering its monetary policy.

Governor Kugler (dove and voting member) suggested that it might be appropriate to cut rates later this year if economic conditions, including smaller price markups, stable inflation expectations, softening demand and more balanced labour markets, continue to move in the right direction.

In Germany, the ZEW index for June revealed that investor confidence rose less than anticipated, with the economic sentiment index increasing to 47.5 (cons: 49.8). The assessment of the current economic situation worsened slightly, recording -73.8 (cons:-65.0).

In Hungary, the central bank cut its policy rate to 7.0% - fully in line with the 25bp we and consensus had expected.

In the equity space, Nvidia has surpassed Microsoft to become the world's most valuable company. The milestone is driven by the imperative role that its chips play in the competitive landscape of artificial intelligence. The company's market value is now more than USD 3tn.

Market movements

Equities: Global equities were higher yesterday, with many headlines around the string of new all-time highs in the US. However, more interestingly, Europe was positive and outperformed the US. Secondly, this was not just a tech rally despite Nvidia becoming the most valuable company. We saw more broad-based gains with banks, energy, and insurance outperforming while tech marginally underperformed. In the US yesterday, the Dow was up 0.2%, the S&P 500 was up 0.3%, the Nasdaq was up 0.03%, and the Russell 2000 was up 0.16%. Asian markets are mostly higher this morning, lifted by Chinese stocks. Futures in Europe and the US are around yesterday's closing levels.

FI: Fading political risks from France led to the intra-euro area spread tightening continuing yesterday. This week, the French-German yield spread has tightening 5bp with a 2bp performance yesterday relative to German bunds. It still trades 25bp wider than ahead of the EU election/election announcement. The IG Metal announcement on asking 7% in pay rise over 12m in 2025 did not seem to catch market attention, neither did the final inflation release that pointed to rising inflation dynamics in most underlying measures. ECB's Knot cautioned yesterday that inflation may start rising again,'‘for example due to continued strong wage growth".

FX: The oil price has risen again to around USD 84-85/bbl which has also contributed to lifting the Norwegian currency in recent sessions. Weaker than expected US retail sales provided support for EUR/USD during yesterdday's session although political risks from France remain in focus. CHF continues to be among the top performs ahead of the SNB meeting tomorrow. For GBP FX, inflation figures released this morning are in focus ahead of the BoE monetary policy meeting tomorrow.

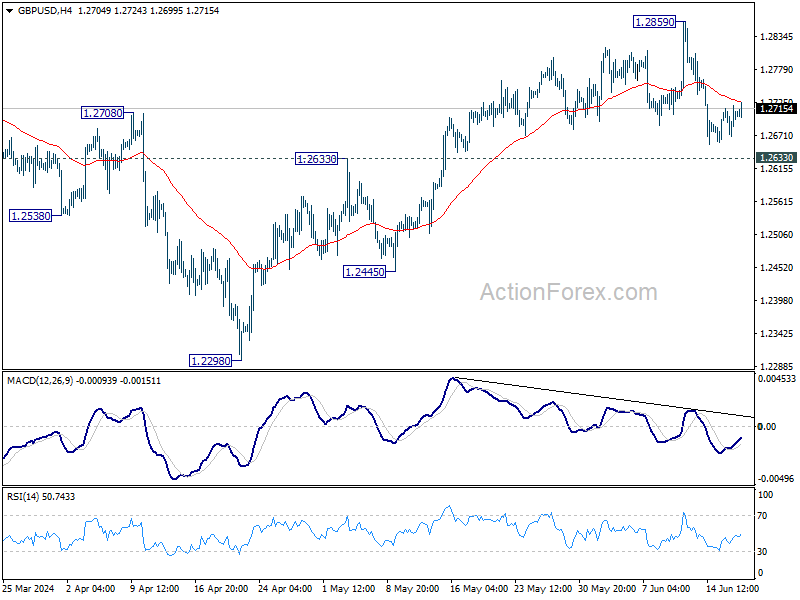

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2678; (P) 1.2700; (R1) 1.2730; More...

GBP/USD is staying in consolidations in tight range and intraday bias remains neutral. Risk will stay on the downside as long as 1.2859 resistance holds. Firm break of 1.2633 resistance turned support will argue that whole rise from 1.2298 has completed, and target 1.2445 and below.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2445 support will extend the corrective pattern with another decline instead.

Sterling Steady as UK Inflation Eases; Australian Dollar Strengthens

British Pound held steady following release of UK data showing decrease in both headline and core consumer inflation for May. This development is unlikely to influence BoE decision tomorrow, where a rate hold is widely anticipated. Although BoE is expected to begin cutting interest rates soon, this plan has been delayed due to the unexpected call for general elections on July 4. Market consensus now points to August as the likely time for the start of monetary policy easing. Traders will be looking for clues from tomorrow's statement and possibly the voting results to solidify this expectation.

Meanwhile, Australian Dollar is currently the strongest currency, buoyed by RBA recent communications. RBA has expressed uncertainty about the disinflation process staying on track and voiced concerns over persistent price pressures. This has led the market to speculate on the possibility of another rate hike, even though this is not the baseline expectation among most economists. The situation, however, could change significantly with the Q2 CPI data due in July, which will clarify the outlook for RBA's decision in August.

In the broader currency market, Japanese Yen is the weakest performer this week, followed by New Zealand Dollar and US Dollar. Australian Dollar has overtaken Swiss Franc as the strongest, with Euro in third place. British Pound and Canadian Dollar are trading in the middle of the pack.

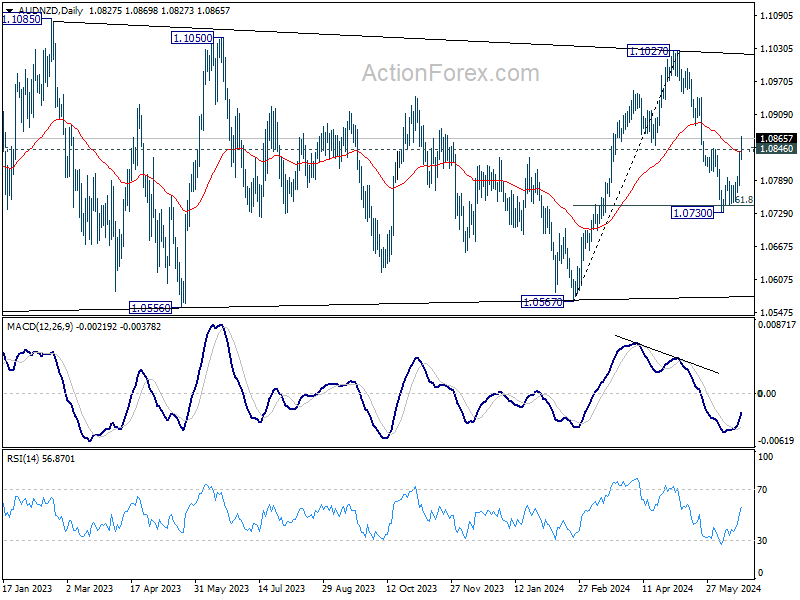

Technically, AUD/NZD' strong break of 1.0846 resistance as well as 55 D EMA suggest that correction from 1.1027 has completed at 1.0730, after drawing support from 61.8% retracement of 1.0567 to 1.1027. At this point, it's still a bit early to determine is the cross is ready to resume the rise from 1.0567 through 1.1027. That would very much depends on the next move of RBA.

In Asia, Nikkei rose 0.10%. Hong Kong HSI is up 2.71%. China Shanghai SSE is down -0.14%. Singapore Strait Times is up 0.42%. Japan 10-year JGB yield fell -0.0081 to 0.939. Overnight, DOW rose 0.15%. S&P 500 rose 0.25%. NASDAQ rose 0.03%. 10-year yield fell -0.062 to 4.217.

UK CPI slows to 2.0% in May, core CPI down to 3.5%

UK CPI slowed from 2.3% yoy to 2.0% yoy in May, lowest since July 2021. Core CPI (excluding energy, food, alcohol and tobacco) slowed from 3.9% yoy to 3.5% yoy. Both matched expectations.

CPI goods annual rate fell from - 0.8% yoy to -1.3% yoy, while CPI services annual rate eased slightly from 5.9% yoy to 5.7% yoy.

On a monthly basis, CPI rose by 0.3%, below expectation of 0.4% mom.

BoJ Minutes highlight concerns over weak Yen's impact on inflation

Minutes from BoJ's April 25-26 meeting revealed that board members are closely monitoring the ongoing risks posed by the weak Yen and its effect on inflation, which could force a monetary policy response.

"Some members" emphasized that exchange rates are crucial factors influencing economic activity and prices, suggesting that "monetary policy responses would be necessary" if there were significant changes in the economic outlook or associated risks.

One of these board members noted the "trilemma of international finance," arguing that monetary policy should not be used solely to stabilize foreign exchange rates. However, they acknowledged that if exchange rate movements impacted firms' medium- to long-term inflation expectations and corporate behavior, this could "raise the risk of prices being affected," making monetary policy adjustments "necessary."

The minutes also reflected a shared understanding among members that if underlying inflation increases in line with forecasts, BoJ would adjust its degree of monetary accommodation. Additionally, any changes in the outlook for economic activity and prices, or shifts in related risks, would warrant adjustments to the policy interest rate.

RBNZ's Conway: Inflation sticky near-term, could fall more quickly medium term

In a speech today, RBNZ Chief Economist Paul Conway discussed the complexities of bringing inflation sustainably back to target, noting "remaining challenges" and various risks and uncertainties.

Conway pointed out that in the "near term", inflation might be "more persistent" than current projections suggest. He highlighted that domestic or non-tradables inflation and services sector inflation have remained higher than expected, indicating a "sticky" inflationary environment.

Conversely, Conway also sees potential for inflation to "fall more quickly" than anticipated over the "medium term". Factors such as increasing spare capacity in product and labor markets and shifting business and household inflation expectations could accelerate the decline in inflation.

He explained that RBNZ's current policy strategy is "balancing these opposing factors." The bank will closely monitor indicators of core inflation, non-tradables inflation, services inflation, and inflation expectations to assess how these risks unfold. The labor market will also be a critical signal of capacity pressure.

Fed's Kugler encouraged by renewed progress on inflation

In a speech, Fed Governor Adriana Kugler acknowledged that while inflation remains too high, she is "encouraged" by the overall progress and outlook. Kugler expressed "cautious optimism" based on recent economic and inflation data, suggesting that Fed is on track towards its 2% inflation target.

She noted that progress may have stalled in the first quarter of the year, but subsequent information on economic activity, the labor market, and inflation indicates "renewed progress."

Kugler indicated that, "If the economy evolves as I am expecting, it will likely become appropriate to begin easing policy sometime later this year."

Fed's Musalem calls for sustained favorable conditions before rate cuts

In his debut speech, St. Louis Federal Reserve President Alberto Musalem emphasized the need for sustained favorable conditions before considering a reduction in interest rate. He stated that he needs to see a period of favorable inflation, moderating demand, and expanding supply, which could take "months, and more likely quarters" to materialize.

He also did not rule out additional rate hikes if inflation remains significantly above 2% or if it reaccelerates, although he noted this was not his base case scenario.

Musalem also expressed uncertainty about whether the current monetary policy stance is sufficiently restrictive, pointing out that financial conditions "feel accommodative for some parts of the economy while restrictive for others."

Fed's Logan: Neutral rate may be higher post-pandemic, inflation risks persist

In a moderated Q&A session overnight, Dallas Fed President Lorie Logan stated, "From a monetary policy perspective, we're in a good position, we're in a flexible position to watch the data and be patient." She highlighted the need for "several months" of favorable data to gain confidence that inflation is on track to the 2% target.

Despite signs that the economy is balancing better, Logan expressed concerns about persistent upside risks to inflation. She also suggested that the neutral rate setting may now be higher than pre-pandemic levels.

"We've just been surprised by how well the economy has performed at these higher levels of rates," she noted. Logan attributed this to structural changes in the economy, implying that the neutral rate might be higher than it was in the decade before the pandemic.

Fed's Collins warns against overreacting to short-term inflation data

In a speech, Boston Fed President Susan Collins cautioned against overreacting to "a month or two" of improvements in inflation data. She emphasized, "It is too soon to determine whether inflation is durably on a path back to the 2% target." Collins urged patience in the approach to monetary policy, reflecting the need for a cautious stance.

"In my view, the data suggest an economy with demand and supply coming into better balance, as required to restore price stability," Collins said. "However, this process may just take more time than previously thought."

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2678; (P) 1.2700; (R1) 1.2730; More...

GBP/USD is staying in consolidations in tight range and intraday bias remains neutral. Risk will stay on the downside as long as 1.2859 resistance holds. Firm break of 1.2633 resistance turned support will argue that whole rise from 1.2298 has completed, and target 1.2445 and below.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2445 support will extend the corrective pattern with another decline instead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Current Account (NZD) Q1 | -4.36B | -4.65B | -7.84B | -7.98B |

| 23:50 | JPY | Trade Balance (JPY) May | -0.62T | -0.63T | -0.56T | |

| 23:50 | JPY | BoJ Minutes | ||||

| 06:00 | GBP | CPI M/M May | 0.30% | 0.40% | 0.30% | |

| 06:00 | GBP | CPI Y/Y May | 2.00% | 2.00% | 2.30% | |

| 06:00 | GBP | Core CPI Y/Y May | 3.50% | 3.50% | 3.90% | |

| 06:00 | GBP | RPI M/M May | 0.40% | 0.50% | 0.50% | |

| 06:00 | GBP | RPI Y/Y May | 3.00% | 3.10% | 3.30% | |

| 06:00 | GBP | PPI Input M/M May | 0% | -0.20% | 0.60% | 0.80% |

| 06:00 | GBP | PPI Input Y/Y May | -0.10% | -1.60% | -1.40% | |

| 06:00 | GBP | PPI Output M/M May | -0.10% | 0.10% | 0.20% | 0.30% |

| 06:00 | GBP | PPI Output Y/Y May | 1.70% | 1.10% | ||

| 06:00 | GBP | PPI Core Output M/M May | 0.20% | 0.00% | 0.20% | |

| 06:00 | GBP | PPI Core Output Y/Y May | 1.00% | 0.20% | 0.30% | |

| 08:00 | EUR | Eurozone Current Account (EUR) Apr | 35.2B | 35.8B | ||

| 14:00 | USD | NAHB Housing Index Jun | 46 | 45 | ||

| 17:30 | CAD | BoC Summary of Deliberations |

UK CPI slows to 2.0% in May, core CPI down to 3.5%

UK CPI slowed from 2.3% yoy to 2.0% yoy in May, lowest since July 2021. Core CPI (excluding energy, food, alcohol and tobacco) slowed from 3.9% yoy to 3.5% yoy. Both matched expectations.

CPI goods annual rate fell from - 0.8% yoy to -1.3% yoy, while CPI services annual rate eased slightly from 5.9% yoy to 5.7% yoy.

On a monthly basis, CPI rose by 0.3%, below expectation of 0.4% mom.

Elliott Wave Analysis on Copper (HG) Expects the Metal Turning Higher

Short Term Elliott Wave in Copper (HG) suggests the metal has ended wave (4) correction at 4.375. Wave (3) rally ended at 5.2 on 5.20.2024 which is all-time high price for Copper. Wave (4) pullback unfolded as a double three Elliott Wave structure. Down from wave (3), wave W ended at 4.7435 and wave X ended at 4.903. Wave Y lower subdivided into a zigzag structure where wave ((a)) ended at 4.571 and wave ((b)) ended at 4.696. The 45 minutes chart below shows wave ((b) on the left side of the chart.

Down from there, wave (i) ended at 4.518 and wave (ii) ended at 4.687. Wave (iii) lower ended at 4.431 and rally in wave (iv) ended at 4.612. Final leg wave (v) ended at 4.375. This completed wave ((c)) of Y of (4) in higher degree. The metal has turned higher and the rally looks impulsive. Up from 4.37, expect wave (i) to end soon, then it should pullback in wave (ii) to correct the short term rally from wave (4) before it resumes higher again. Near term, as far as pivot at 4.375 low stays intact, expect dips to find support in 3, 7, 11 swing for more upside.

Copper 45 Minutes Elliott Wave Chart

Copper (HG) Elliott Wave Video

https://www.youtube.com/watch?v=9y8S7HH9xDE

BoJ Minutes highlight concerns over weak Yen’s impact on inflation

Minutes from BoJ's April 25-26 meeting revealed that board members are closely monitoring the ongoing risks posed by the weak Yen and its effect on inflation, which could force a monetary policy response.

"Some members" emphasized that exchange rates are crucial factors influencing economic activity and prices, suggesting that "monetary policy responses would be necessary" if there were significant changes in the economic outlook or associated risks.

One of these board members noted the "trilemma of international finance," arguing that monetary policy should not be used solely to stabilize foreign exchange rates. However, they acknowledged that if exchange rate movements impacted firms' medium- to long-term inflation expectations and corporate behavior, this could "raise the risk of prices being affected," making monetary policy adjustments "necessary."

The minutes also reflected a shared understanding among members that if underlying inflation increases in line with forecasts, BoJ would adjust its degree of monetary accommodation. Additionally, any changes in the outlook for economic activity and prices, or shifts in related risks, would warrant adjustments to the policy interest rate.

RBNZ’s Conway: Inflation sticky near-term, could fall more quickly medium term

In a speech today, RBNZ Chief Economist Paul Conway discussed the complexities of bringing inflation sustainably back to target, noting "remaining challenges" and various risks and uncertainties.

Conway pointed out that in the "near term", inflation might be "more persistent" than current projections suggest. He highlighted that domestic or non-tradables inflation and services sector inflation have remained higher than expected, indicating a "sticky" inflationary environment.

Conversely, Conway also sees potential for inflation to "fall more quickly" than anticipated over the "medium term". Factors such as increasing spare capacity in product and labor markets and shifting business and household inflation expectations could accelerate the decline in inflation.

He explained that RBNZ's current policy strategy is "balancing these opposing factors." The bank will closely monitor indicators of core inflation, non-tradables inflation, services inflation, and inflation expectations to assess how these risks unfold. The labor market will also be a critical signal of capacity pressure.