Sample Category Title

Swiss Franc Rallies Amid Falling Yields and Political Risks

Swiss Franc breaks higher in early US session as benchmark treasury yields in both the US and Europe plummeted. This rise was partly triggered by US retail sales data coming in much weaker than anticipated. Additionally, investor sentiment in Europe remains fragile due to ongoing political risks in France.

On the geopolitical front, Russian President Vladimir Putin pledged to deepen trade and security ties with North Korea and support it against the US. This visit marks Putin's first to North Korea in 24 years. Simultaneously, Beijing has initiated an anti-dumping investigation targeting certain pork products from the European Union, following Brussels' recent move to raise tariffs on Chinese vehicles.

Australian Dollar is also performing strongly today, following RBA's decision to keep interest rates unchanged and leave door open for future rate hikes. Governor Michele Bullock indicated that the board did not discuss rate cuts today but did consider the rising risks of inflation. The consumer price inflation data for the June quarter will be critical, as it will provide a comprehensive view of inflationary pressures and guide the next monetary policy decisions.

In contrast, New Zealand Dollar is the weakest performer, further pressured by selloff against Australian Dollar. British Pound is the second weakest, followed by Canadian Dollar. Dollar, Euro, and Japanese Yen are trading in the middle of the pack.

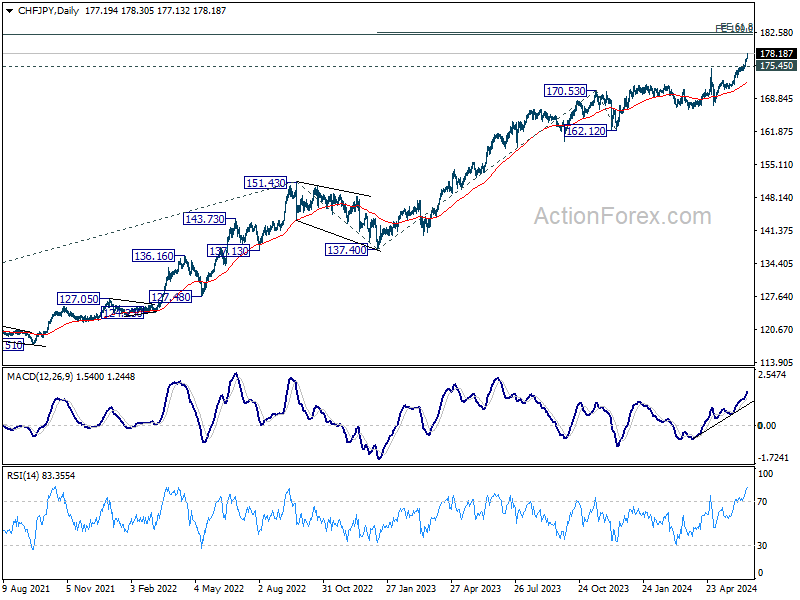

Technically, CHF/JPY is continuing its record run. Near term outlook will stay bullish as long as 175.45 support holds. Next target is 61.8% projection of 137.40 to 170.53 from 162.12 at 182.59.

In Europe, at the time of writing, FTSE is up 0.52%. DAX is up 0.27%. CAC is up 0.61%. UK 10-year yield is down -0.038 at 4.082. Germany 10-year yield is down -0.006 at 2.409. Earlier in Asia, Nikkei rose 1.00%. Hong Kong HSI fell -0.11%. China Shanghai SSE rose 0.48%. Singapore Strait Times rose 0.13%. Japan 10-year JGB yield rose 0.0158 at 0.947.

US retail sales rise 0.1% mom in May, ex-auto sales down -0.1% mom.

US retail sales rose 0.1% mom to USD 703.1B in May, below expectation of 0.3% mom. Ex-auto sales fell -0.1% mom to 569.0B, worse than expectation of 0.2% mom growth. Ex-gasoline sales rose 0.3% mom to USD 649.5B. Ex-auto and gasoline sales rose 0.1% mom to USD 515.5B.

Total sales for the March through May period were up 2.9% from the same period a year ago.

ECB's de Guindos emphasizes importance of economic projections in rate decisions

ECB Vice President Luis de Guindos highlighted the critical role of updated macroeconomic projections in shaping interest rate decisions. During an interview with Spanish state broadcaster TVE, Guindos noted, "The projections are updated every three months, so we'll soon have new ones in September"

"Those are the most significant and interesting moments from the point of view of monetary policy, because our projections are a very important indicator when it comes to deciding the evolution of interest rates," he added.

Separately, according to the latest Reuters poll conducted from June 12-18, a substantial majority of economists (nearly 80%, or 64 out of 81) anticipate that ECB will implement two more rate cuts this year, specifically in September and December. This would lower the deposit rate to 3.25%.

Additionally, almost 90% of those surveyed (36 out of 41) believe the risks are tilted towards ECB making fewer cuts than more.

German ZEW ticks up to 47.5, sentiment and situation stagnate

German ZEW Economic Sentiment ticked up from 47.1 to 47.5 in June, below expectation of 50.0. Current Situation Index fell from -72.3 to -73.8, below expectation of -69.0.

Eurozone ZEW Economic Sentiment rose from 47.0 to 51.3, above expectation of 47.2. Current Situation Index was unchanged at -38.6.

ZEW President Professor Achim Wambach said: "Both the sentiment and the situation indicators stagnate. These developments must be interpreted in the context of a constant situation indicator for the eurozone as a whole. In contrast, the inflation expectations of the respondents increase, which is likely related to the inflation rate in May, which turned out higher than what was expected."

Eurozone CPI finalized at 2.6% in May, core at 2.9%

Eurozone CPI was finalized at 2.6% yoy in May, up from April's 2.4% yoy. CPI core (ex energy, food, alcohol & tobacco) was finalized at 2.9% yoy, up from prior month's 2.7% yoy. The highest contribution to the annual inflation rate came from services (+1.83 percentage points, pp), followed by food, alcohol & tobacco (+0.51 pp), non-energy industrial goods (+0.18 pp) and energy (+0.04 pp).

EU CPI was finalized at 2.7% yoy, up from April's 2.6% yoy. The lowest annual rates were registered in Latvia (0.0%), Finland (0.4%) and Italy (0.8%). The highest annual rates were recorded in Romania (5.8%), Belgium (4.9%) and Croatia (4.3%). Compared with April, annual inflation fell in eleven Member States, remained stable in two and rose in fourteen.

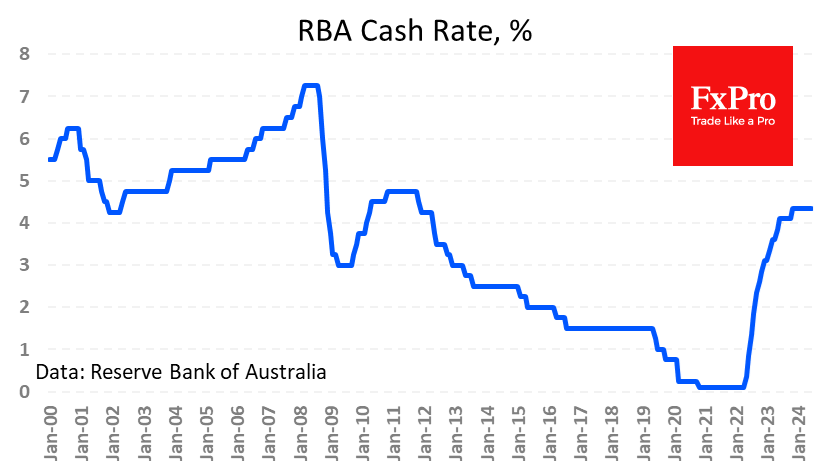

RBA stands pat, still not ruling anything in or out

RBA left its cash rate target unchanged at 4.35%, as widely anticipated. It maintained its stance of "not ruling anything in or out," indicating a cautious approach and open stance amid ongoing economic uncertainties.

While inflation is easing, RBA noted that it is doing so "more slowly than previously expected," and inflation "remains high." The central bank acknowledged that it will be "some time yet" before inflation is sustainably within the target range.

RBA added that recent economic data have been "mixed," reinforcing the need to remain "vigilant to upside risks to inflation." Consequently, the path of interest rates "remains uncertain".

BoJ's Ueda reiterates possibility of July rate hike

BoJ Governor Kazuo Ueda reiterated today that the central bank could raise interest rates again in July, stressing that this decision would be independent of the plan to taper bond purchases.

Speaking to parliament, Ueda clarified, "Our decision on bond-buying taper and interest rate hikes are two different things." He emphasized that a rate hike at the next policy meeting will depend on the economic, price, and financial data available at the time.

A recent Reuters poll on Monday revealed that 31% of economists surveyed expect BoJ to raise interest rates at its next policy meeting on July 30-31. Another 41% predict the next hike will occur in October, while slightly more than 20% anticipate a September increase. The remaining economists do not foresee a rate hike until 2025. This diversity of expectations underscores the uncertainty in forecasting BoJ's policy move.

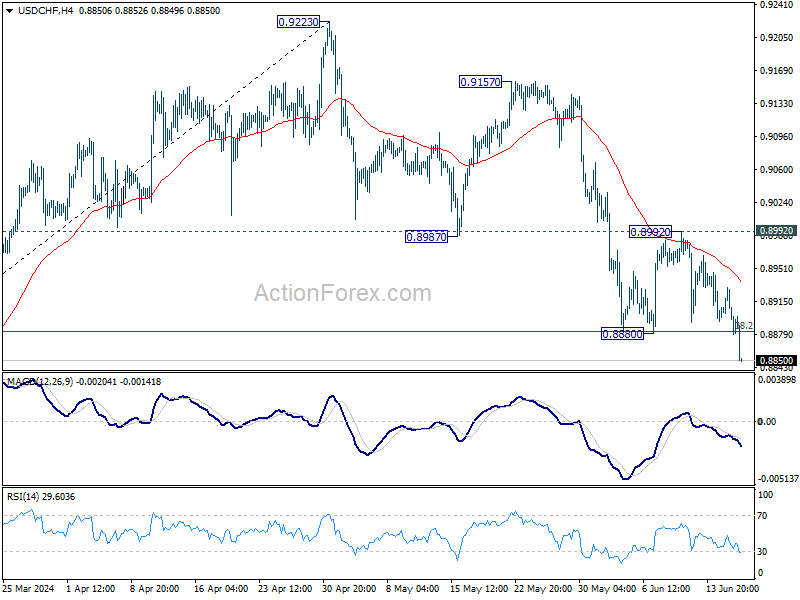

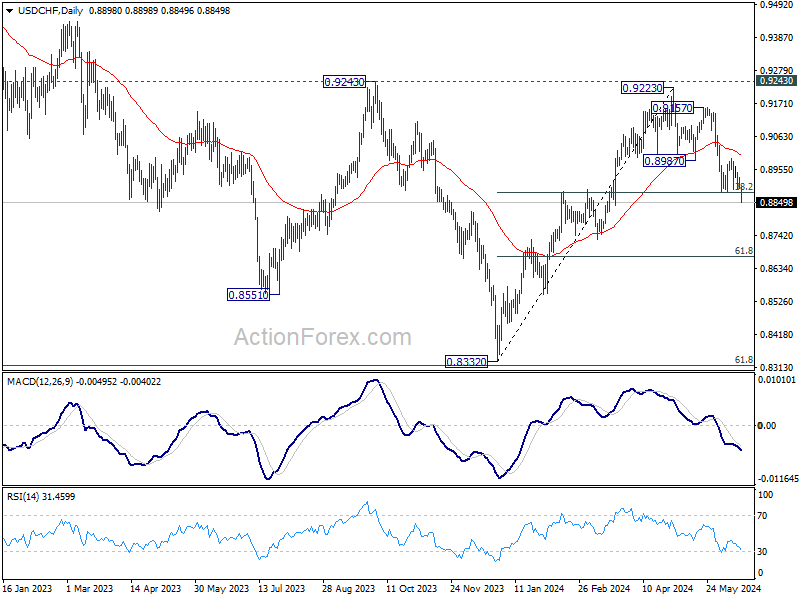

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8883; (P) 0.8908; (R1) 0.8921; More….

USD/CHF's fall from 0.9223 resumed by breaking through 0.8880 support today. The break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 argues that whole rise from 0.8332 might be completed after missing 0.9243. Intraday bias is back on the downside for 61.8% retracement at 0.8672 next. For now, risk will stay on the downside as long as 0.8992 resistance holds, in case of recovery.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance affirms this case, and maintain medium term bearishness. While more range trading could be seen between 0.8332/0.9243 first, downside break out is mildly in favor at a later stage.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 04:30 | AUD | RBA Interest Rate Decision | 4.35% | 4.35% | 4.35% | |

| 09:00 | EUR | Eurozone CPI Y/Y May F | 2.60% | 2.60% | 2.60% | |

| 09:00 | EUR | Eurozone CPI Core Y/Y May F | 2.90% | 2.90% | 2.90% | |

| 09:00 | EUR | Germany ZEW Economic Sentiment Jun | 47.5 | 50 | 47.1 | |

| 09:00 | EUR | Germany ZEW Current Situation Jun | -73.8 | -69 | -72.3 | |

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Jun | 51.3 | 47.2 | 47 | |

| 12:30 | USD | Retail Sales M/M May | 0.10% | 0.30% | 0.00% | -0.20% |

| 12:30 | USD | Retail Sales ex Autos M/M May | -0.10% | 0.20% | 0.20% | -0.10% |

| 13:15 | USD | Industrial Production M/M May | 0.90% | 0.40% | 0.00% | |

| 13:15 | USD | Capacity Utilization May | 78.70% | 78.60% | 78.40% | 78.20% |

| 14:00 | USD | Business Inventories Apr | 0.30% | -0.10% |

US retail sales rise 0.1% mom in May, ex-auto sales down -0.1% mom

US retail sales rose 0.1% mom to USD 703.1B in May, below expectation of 0.3% mom. Ex-auto sales fell -0.1% mom to 569.0B, worse than expectation of 0.2% mom growth. Ex-gasoline sales rose 0.3% mom to USD 649.5B. Ex-auto and gasoline sales rose 0.1% mom to USD 515.5B.

Total sales for the March through May period were up 2.9% from the same period a year ago.

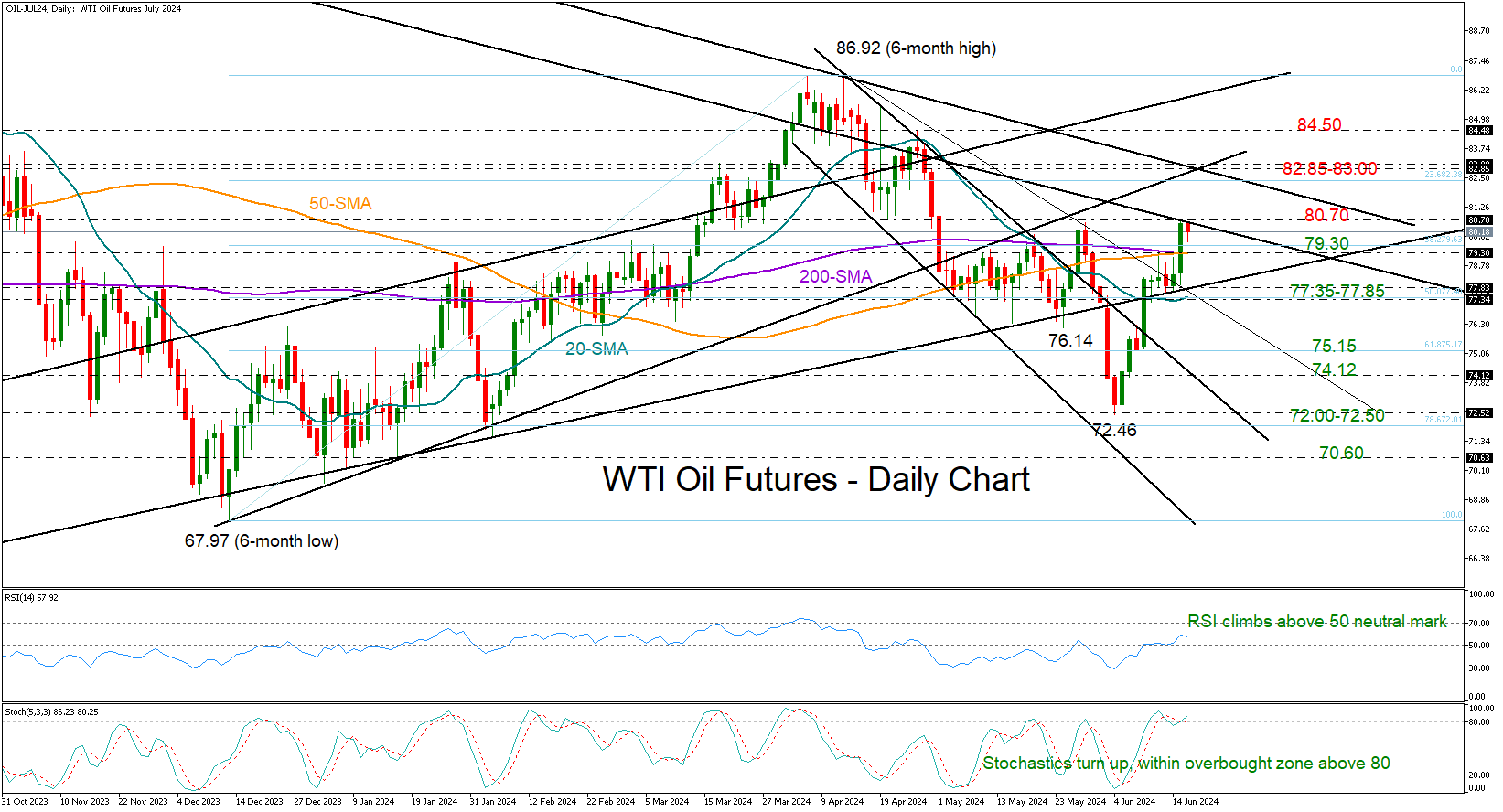

WTI Oil Futures Surge Back to 80

- WTI oil futures swiftly recoup June’s lost ground to trade again above 80

- Technical signals return to positive area, but there is another barrier nearby

Hopes of increased demand in the next quarter caused WTI oil futures to surge back to 80.60, erasing earlier losses that led the price to a four-month low of 72.46 two weeks ago.

The bullish action lifted the price back above its 50- and 200-day simple moving averages (SMAs), pushing the RSI index above its 50 neutral mark as well. The odds for a bullish continuation are technically high, but the bulls need to close above the resistance line at 80.70 to encourage more buying towards the next trendline zone of 82.85-83.00. A successful penetration higher could bring April’s bar of 84.85 under the spotlight.

Should the bullish enthusiasm quickly diminish, the 50- and 200-day SMAs might offer some initial support around 79.30. If not, the price could slip into the 77.35-77.85 region, a break of which could cause a sharper decline towards the 75.17 number. If the 74.12 area gives way too, the sell-off could next pause near the recent low of 72.50 or perhaps around the 72.00 psychological mark.

In summary, WTI oil futures have entered a new bullish phase, and there is a possibility of a further increase if the bulls can surpass the 80.70 level.

ECB’s de Guindos emphasizes importance of economic projections in rate decisions

ECB Vice President Luis de Guindos highlighted the critical role of updated macroeconomic projections in shaping interest rate decisions. During an interview with Spanish state broadcaster TVE, Guindos noted, "The projections are updated every three months, so we'll soon have new ones in September"

"Those are the most significant and interesting moments from the point of view of monetary policy, because our projections are a very important indicator when it comes to deciding the evolution of interest rates," he added.

Separately, according to the latest Reuters poll conducted from June 12-18, a substantial majority of economists (nearly 80%, or 64 out of 81) anticipate that ECB will implement two more rate cuts this year, specifically in September and December. This would lower the deposit rate to 3.25%.

Additionally, almost 90% of those surveyed (36 out of 41) believe the risks are tilted towards ECB making fewer cuts than more.

GBP/USD Eyes UK Inflation

The British pound has edged lower on Tuesday. GBP/USD is trading at 1.2683 in the European session at the time of writing, down 0.16% on the day. There are no UK events on Tuesday, while the US releases retail sales. On Wednesday, we’ll get a look at UK inflation for May.

US retail sales expected to post small gain

US retail sales were flat in April but are expected to improve to 0.2% m/m in May. Yearly, retail sales are projected to dip to 2.8%, compared to 3.0% in April.

The Federal Reserve will be keeping a close eye on today’s retail sales data, hoping that any improvement in May retail sales is mild, as a weakening economy will support cutting interest rates.

The Fed has done a good job slashing inflation, although the final sprint to achieving the 2% target is proving to be a tough challenge. Fed policy makers are likely to go ahead with an initial rate cut even if inflation remains above target, so long as they are confident that inflation will continue to fall.

The markets have priced in a quarter-point cut in September at 60%, according to the CME’s FedWatch tool. That is up from 53% a week ago, but indicates that there is a strong chance that the Fed won’t change its “higher for longer” stance until November or December.

In the UK, inflation is expected to fall to 2% in May, down from 2.3% in April. This would mean inflation has dropped to the Bank of England’s 2% target for the first time since April 2021. Unfortunately for the government, a positive inflation report will not translate into a rate cut at Thursday’s meeting, since there is an election on July 4th and the BoE does not want to be viewed as meddling in the election campaign. As well, services inflation came in at 6% in April, and that has to drop before the BoE will press the rate-cut trigger. The markets have priced in an initial rate cut in August.

GBP/USD Technical

- GBP/USD faces resistance at 1.2734 and 1.2811

- 1.2608 and 1.2531 are the next support lines

RBA Readiness to Hike Positive for AUD

The Reserve Bank of Australia kept its key rate at a 12-year high of 4.35%. The market widely expected the decision, so it did not cause a spike in volatility. However, we note that the RBA warned that it was ready to raise the rate.

In its commentary on the rate decision, the Australian central bank emphasised that inflation is roughly at the same level as in December, at 3.6% y/y overall and 4.1% y/y with the exclusion of volatile goods.

Despite the normalising trend, the economy remains in excess demand; employment is above sustainable full employment; wage growth is above productivity gains.

A “wait-and-see” approach is reasonable in this situation. However, the RBA still notes a shift in risks towards pro-inflationary risks and indicates a willingness to change the rate in either direction — an important shift from the dovish rhetoric of the second half of last year.

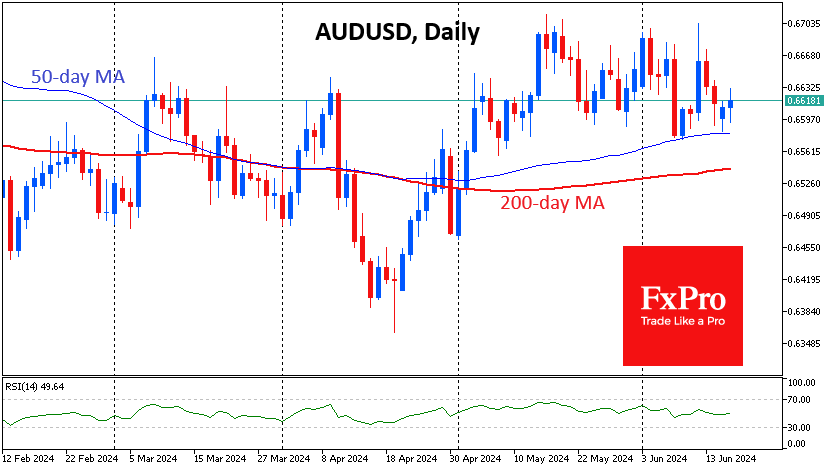

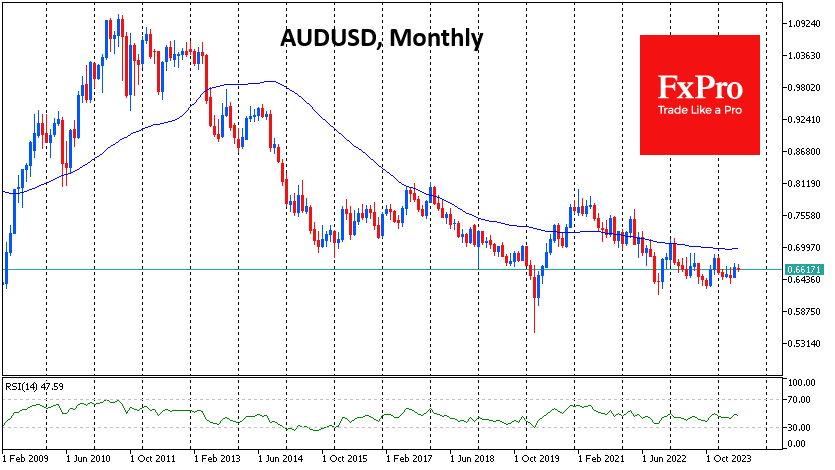

While we haven’t seen a meaningful reaction from AUDUSD, it is performing better than its major peers. It is losing 0.5% this month against the dollar index, which is strengthening over 1%.

The Aussie has not dipped below 0.66 for long since early May, making the 50-day moving average an active support line, and is steady above the 200-day average. Both curves are pointing upwards, emphasising the positive trend.

AUDUSD has been recording higher yearly lows for the past two years, marking increased buying interest on downturns.

The strength of the US Dollar this month is making it harder for the AUD to rise, hindered both by strengthening the denominator and by impacting the price of commodities and metals that Australia exports.

Potential buyers are probably better off waiting for AUDUSD to break above 0.67, where we saw a reversal last month. It would also break the sequence of lower local highs seen over the past three years and at an even higher level since 2011.

A reversal in the tone of monetary policy has the potential to feed AUDUSD buying, adding to the local positive picture. The ability to break the long-term downtrend could attract even more buyers, launching a rally.

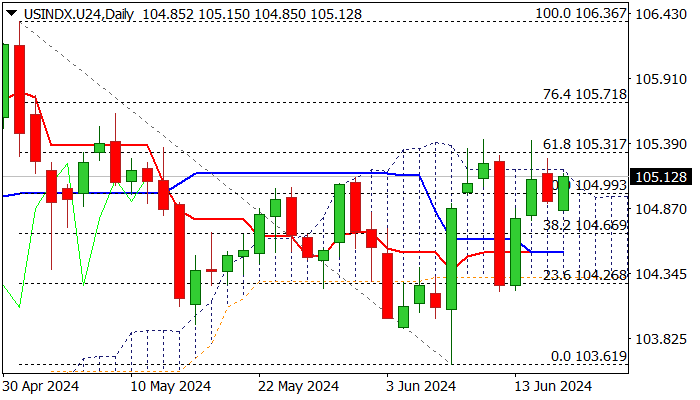

US Dollar Index Outlook: Remains Constructive Ahead of Key Economic Data

The dollar index rose on Tuesday, keeping overall positive sentiment, driven by expectations for Fed rate cut in November and recent political turmoil in the Europe, which deflated Euro.

Traders look for fresh signals about the central bank’s rate cut path, with today’s release of US May retail sales to provide more details about the overall condition of the economy and speeches from several Fed officials, which would give hints about the rate cut timing.

Daily technical studies remain bullish overall, however, near term price action continues to face strong headwinds from the top of daily cloud (15.18) which repeatedly capped attacks and marks solid barrier.

Sustained break here and above recent spikes (105.42) is required to signal bullish continuation and expose targets at 105.71/106.00 (Fibo 76.4% of 106.36/103.61 / round-figure).

Near-term bias to remain with bulls while the price holds above ascending 10DMA (104.77), which guards lower pivots at 104.39/26 (100/200DMA’s / daily cloud base).

Res: 105.18; 105.42; 105.71; 106.00.

Sup: 105.00; 104.77; 104.26; 104.04.

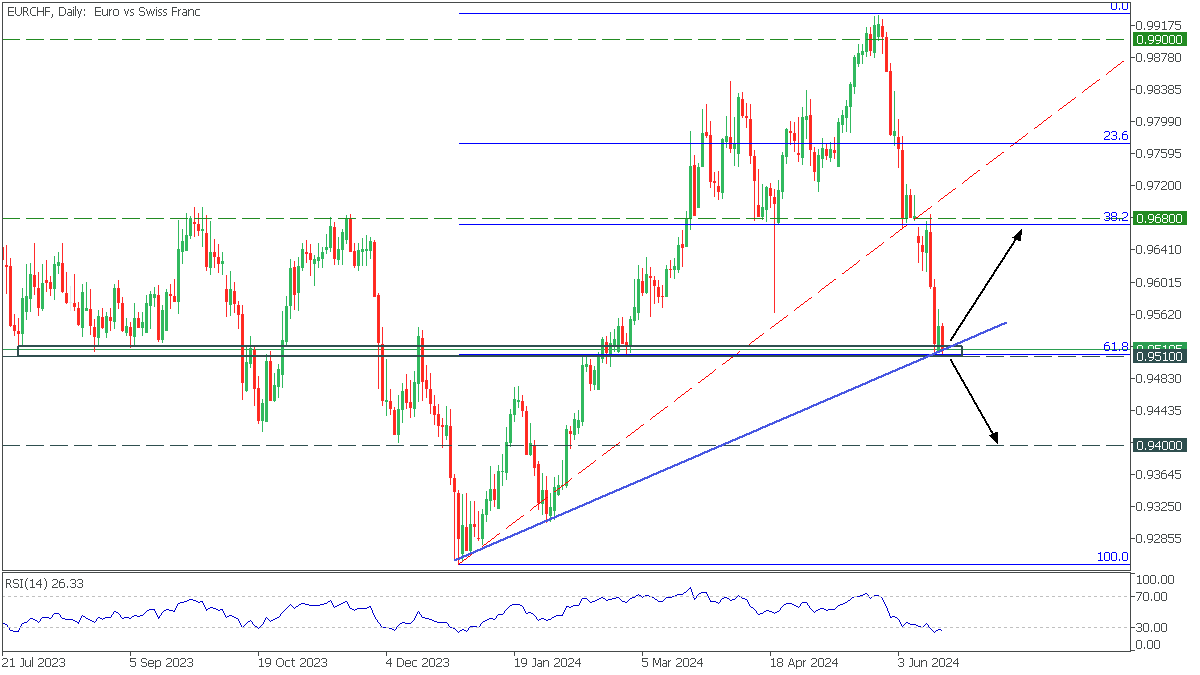

EURCHF: Key Support

In the Daily Timeframe, EURCHF started to decline after a bullish trend and reached 61.8 Fibonacci and the trend line. Despite the strong bearish sentiment, the RSI indicates oversold.

- If the price breaks the trend line and falls below 0.9510, the downside target will be 0.9400;

- A bounce from the trendline will bring EURCHF back to 0.9680 resistance, corresponding to 38.2 Fibonacci;

Brent Oil Has Risen in Price: Reliance on Stock Market Demand Has Worked

The commodity market was adjusted moderately on Tuesday morning after the price of Brent crude oil rose by 2% the day before. A barrel of the North Sea variety is at about 84 USD.

The main support factor currently is the improving prospects for global demand. Additionally, there are expectations that global oil producers will restrain supply.

The latest oil market reports from OPEC+, the International Energy Agency and the US Department of Energy suggest a steady increase in energy demand in the second half of 2024.

Yesterday's surge in Brent's price was also supported by an increase in the value of the entire range of risky assets. This is due to reduced inflationary pressures in the world's largest economies. Such signals strengthen the bet on lowering the cost of lending in the coming months.

The proposal is underpinned by the collaborative efforts of key OPEC+ member countries, including Russia and Iraq, which have confirmed their intentions to adhere to the agreed production quotas. Saudi Arabia has also expressed its readiness to adjust production volumes to fully account for market conditions.

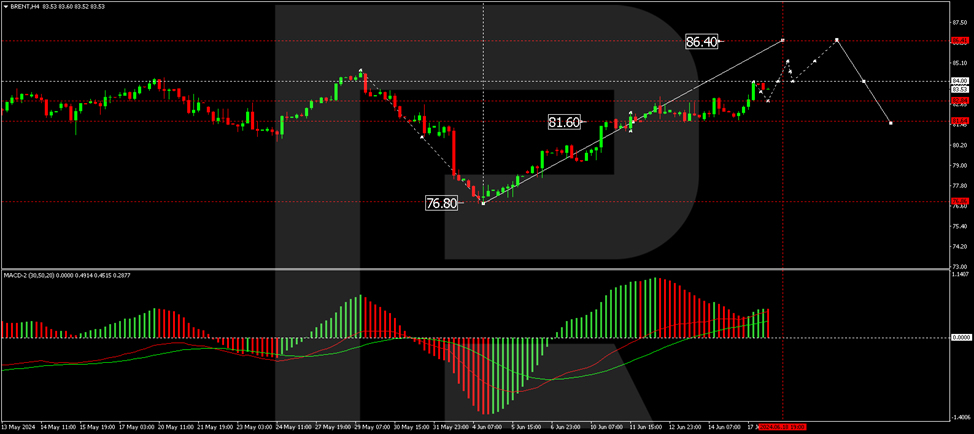

Technical analysis of Brent

On the H4 Brent chart, the market has formed a consolidation range above the 81.60 level. Today, the price has moved up from this range, continuing to develop a wave of growth to the level of 86.40. After achieving this level, we anticipate a correction to 81.60. Next, we expect the trend to continue to the level of 89.00. This scenario is technically confirmed by the MACD indicator, with its signal line above the zero mark and directed strictly upwards.

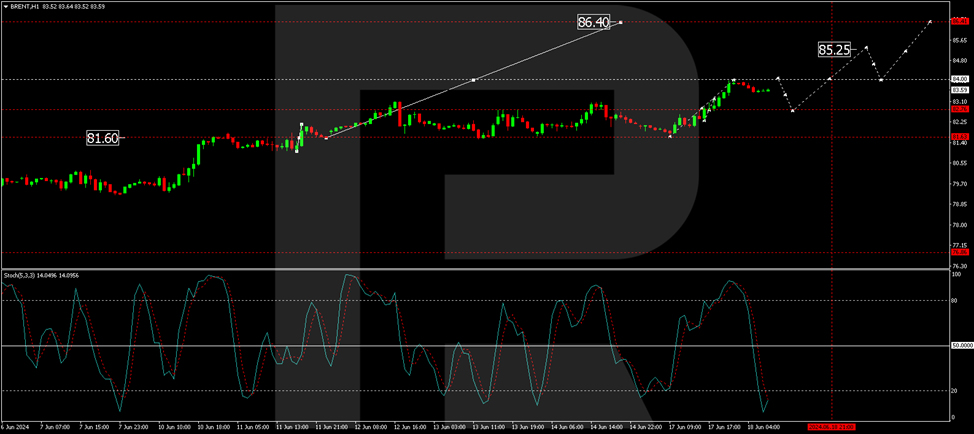

On the H1 Brent chart, the market received support at 81.56 and began the development of the second half of the growth wave. At the moment, the local target at the level of 83.98 is fulfilled. Today, a link of growth to 84.00 is possible. Next, we expect a correction link to the level of 82.76 (test from above), followed by an increase to the level of 86.40. Technically, this scenario is confirmed by the Stochastic oscillator. Its signal line is below the level of 20 and is preparing for the start of growth.

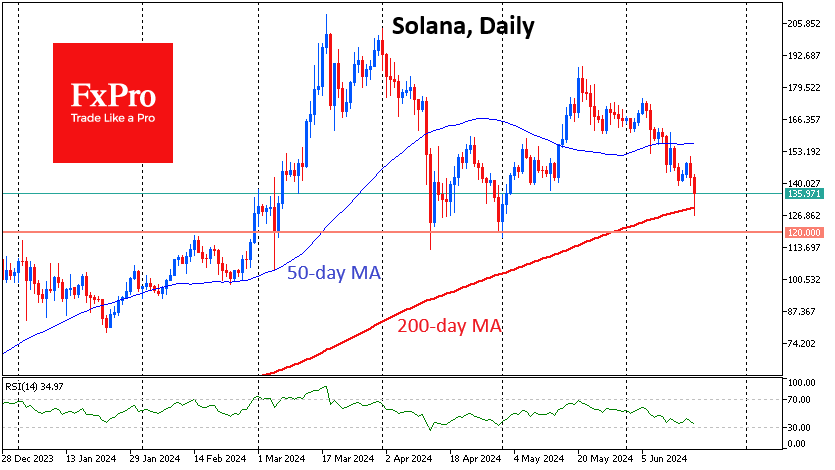

Crypto Continues Its Retreat

Market picture

In 24 hours, crypto capitalisation fell 2.2% to $2.36 trillion. Bitcoin’s relatively moderate 1% decline contrasts with a much deeper dive in altcoins. Ethereum fell 3.3%, Solana plunged 7.8%, and Dogecoin dropped 9.2%.

The main momentum of the decline came in early Asian trading, and at the time of writing, the crypto market had moved away from extremes. Nevertheless, the latest momentum shows that the bears in crypto are in control. This is somewhat surprising given the impressive renewal of all-time highs by the Nasdaq and S&P500 indices.

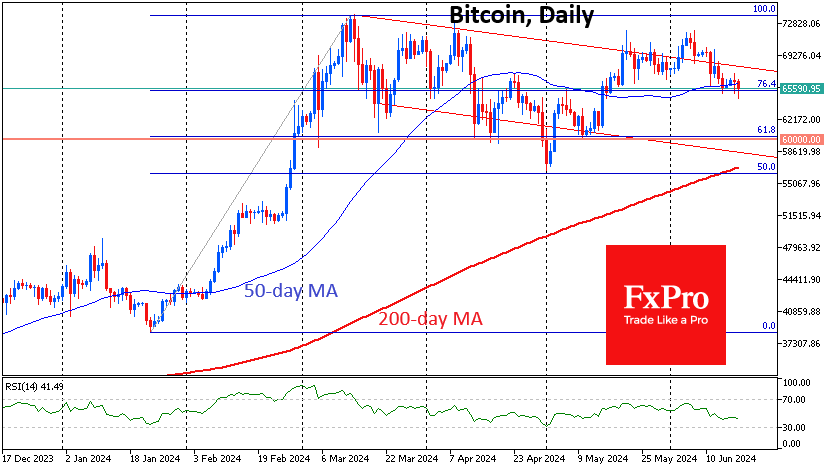

Bitcoin was down to $64.5K this morning, its lowest since 15 May. It has been declining for the past twelve days. It’s also attempting to gain ground below the 50-day moving average and the 76.4% retracement from the January-March rise.

However, the leading altcoins are suffering much larger losses due to shifting market sentiment. Solana has lost over 20% in 12 days of active declines, and the selling is picking up. At one point intraday on Tuesday, losses exceeded 11% but are down to 4.5% at the time of writing. The sell-off hunters came in buying on a touch of the 200-day average. The latest slip may turn the market to the upside for the coming days, as it did in April at roughly these same levels.

News background

According to CoinShares, crypto fund investments fell by $600 million last week after record inflows of $2.038 billion over the past 12 weeks; the notable outflow came after five weeks of rising indexes. Bitcoin investments were down $621 million; Ethereum investments were up $13 million. Outflows from Grayscale’s bitcoin-ETF rose sharply to $273 million for the week.

The Australian Securities Exchange will start trading the first spot bitcoin-ETF on 20 June. A product from VanEck has gained admission to trading, while applications from other issuers are still being reviewed.

The US SEC has agreed to reduce Ripple’s fine for violating securities laws from $2bn to $102.6m. The SEC was responding to a recent request from Ripple’s lawyers, who called the $2bn fine sought by the regulator unfair.

The total value of blocked assets in the TON network exceeded $605 million. Blockchain ranks 15th among the largest DeFi ecosystems.