Sample Category Title

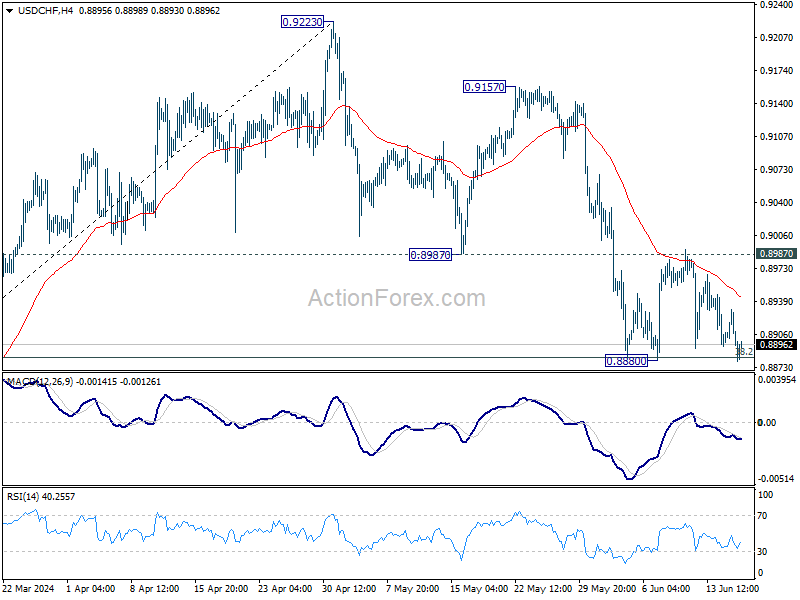

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8883; (P) 0.8908; (R1) 0.8921; More….

Intraday bias in USD/CHF remains neutral as range trading continues. On the downside, sustained break of 0.8883 fibonacci level will carry larger bearish implications and bring deeper decline. On the upside, firm break of 0.8987 support turned resistance will argue that correction from 0.9223 has completed, after drawing support from 0.8883 fibonacci level. Intraday bias will be back on the upside for 0.9157/9223 resistance zone.

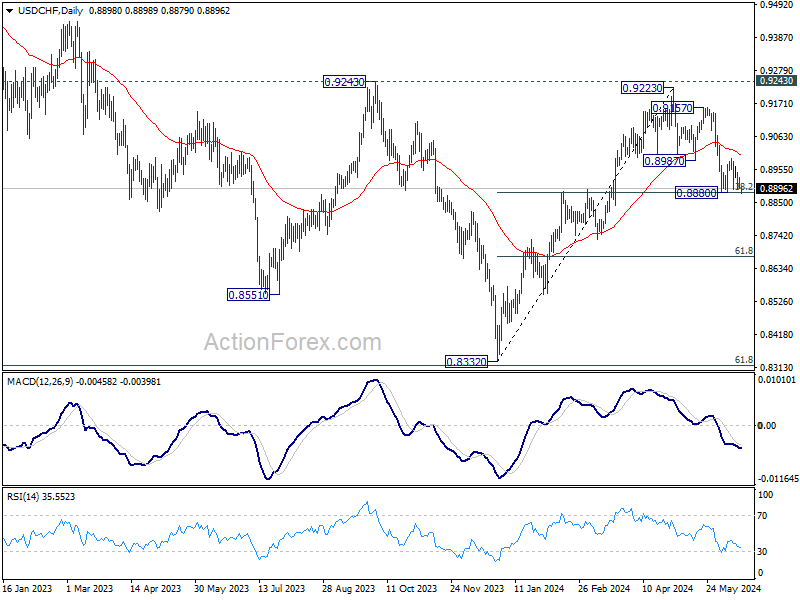

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146..

The US and the Rest

The S&P500 hit a record high yesterday, its 30th record high since the beginning of this year. The technology stocks led the rally. Apple, which revealed its plans to integrate ChatGPT into its iPhones last week, gained 2% and Tesla jumped more than 5% on news that it has been given approval to test its advanced driver-assistance system on some streets in Shanghai. Nasdaq 100 is now a few points below the 20’000 psychological mark and it’s not about if but when it will take out this level. Nasdaq’s PE forward ratio is around 26, high but still lower than the 2020 peak, and much lower than the dot.com levels. IMF said that almost a third of global capital flew int the US since Covid, compared to only 18% before the pandemic. The slow recovery and political turmoil in Europe, war in Ukraine and the geopolitical tensions with China help driving funds toward fertile American markets thanks to new AI opportunities – and high interest rates. Bloomberg points that some market optimists believe that around $6 trillion that’s sitting in money-market cash could be reallocated to equities to further boost the equity rally. And today, big banks revise their price targets for the S&P500 higher. Citi and Goldman for example expect the S&P500 to end the year at 5600, while Evercore thinks that the S&P500 stocks will advance to 6000.

Of course, this much optimism is never good sign and when you start hearing big revisions to price targets, it’s generally time to sell. But sell to go where? The European and the British stocks were supposed to perform well in the reflation context and now they are falling off the race. China is sputtering with housing crisis, geopolitical tensions and slow recovery. Other emerging markets are bearing the brunt of a polarized world and uncertain global outlook.

Yesterday, Federal Reserve’s (Fed) Neel Kashkari said that they’re in a good position to take their time before announcing the first rate cut and Philadelphia Fed’s Patrick Harker said that one rate cut would be appropriate this year. The US 2-year yield hovers around 4.75% and the 10-year yield is just below the 4.30% mark. Today, all eyes are on the US retail sales and industrial production data. A softer-than-expected set of figures could fuel the Fed doves, while stronger-than-expected data could fuel the goldilocks optimism. If investors want to see the glass half full, they will find a reason to do so.

Politics and monetary politics

The US dollar will likely continue to take advantage of the European political uncertainties regardless of the data and Fed talk. The EURUSD traded below the 1.07 mark for the second session yesterday but managed to throw itself above this level on relief that Marine Le Pen is willing to work with Macron if she wins the legislative elections.

The French equities were better bid yesterday, near the oversold levels, as some investors saw opportunity in French companies at discounted prices. Those who bought justified their decision by the fact that the French political turmoil never had a significant impact on economics and that the politically-motivated selloff has certainly been overdone.

Zooming out, the euro traders will keep an eye on the latest EZ inflation figures due to be released this morning, and show that inflation in the Eurozone may have ticked higher both for headline and core figures amid wages growth acerated 5.3% in Q1 – a nightmare for the ECB doves. If that’s the case, we could maybe see a certain upside pressure from fading next European Central Bank (ECB) cut expectations. But the political jitters will continue to carry a downside risk for the euro in the coming weeks, both against the greenback and sterling.

Elsewhere, the Reserve Bank of Australia (RBA) maintained its cash rate unchanged for the fifth time at today’s policy meeting and reiterated caution regarding inflation. The Bank of England (BoE) is expected to stay pat at Thursday’s policy meeting even though some think that we could see a surprise rate cut from the Brits because a last minute cut would hardly interfere with the election outcome – and certainly not offer Tories any additional vote, while the Swiss National Bank (SNB) is expected to announce status quo on Thursday given the latest uptick in Swiss inflation and the ECB’s reluctance to cut more. The EURCHF is heavily hit by the French uncertainties and will likely remain under pressure until the election dust settles while the USDCHF is testing a critical Fibonacci support, the 38.2% level. If this level is cleared, we could see the pair snap back into the bearish consolidation zone but that’s not my base case scenario. While the current worldwide political setup is favourable for safe haven inflows into the franc, the easing bias from the SNB should limit the franc’s appreciation and keep the franc on a softening path.

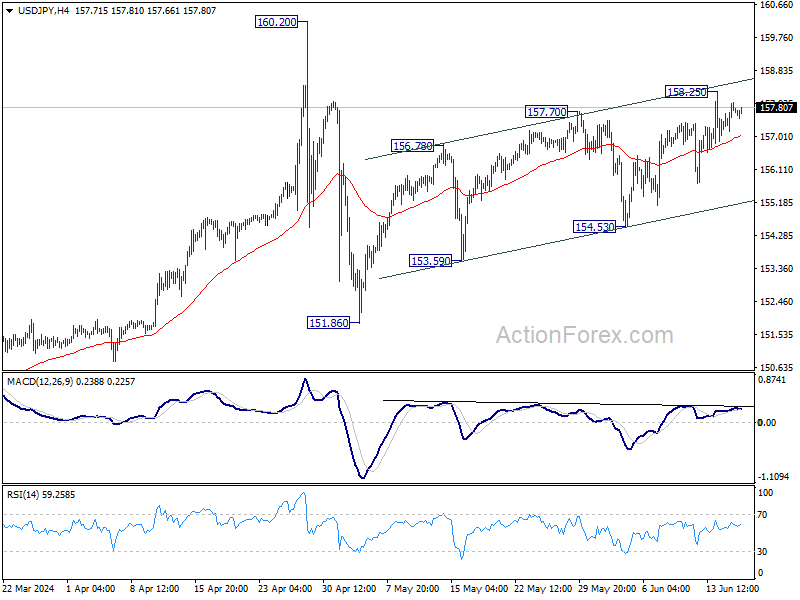

USD/JPY Daily Outlook

Daily Pivots: (S1) 157.27; (P) 157.62; (R1) 158.07; More...

USD/JPY is staying in tight range below 158.25 temporary top and intraday bias remains neutral. Further rally would be in favor as long as 154.53 support holds. Break of 158.25 will resume the choppy rise from 151.86 towards 160.20 high. But upside should be limited there, at least on first attempt.

In the bigger picture, price actions from 160.20 medium term top are seen as a corrective pattern to rise from 150.25 only. Another rally is still expected at a later stage through 160.02 to resume the larger up trend. However, decisive break of 150.87 will argue that larger correction is possibly underway, and target 146.47 support next.

Yen Recovers as BoJ’s Ueda Reiterates July Hike Possibility, But Gains Capped by Uncertainty

Japanese Yen had a modest recovery in Asian session, accompanied by an uptick in 10-year JGB yield and Nikkei. This comes as BoJ Governor Kazuo Ueda continued to prepare the markets for more tightening ahead, by reiterating that another rate hike in July is a possibility. Additionally, Ueda emphasized the impact of the weak Yen on import prices and overall inflation. However, opinions are divided on the timing of BoJ's next rate hike after the historical move in March. Thus, Yen's recovery might remain limited until there is more clarity.

Simultaneously, Australian Dollar edged higher following RBA's decision to keep interest rates unchanged at 4.35%, a move that was widely anticipated by the markets. RBA maintained its flexible stance, stating it is "not ruling anything in or out" regarding future rate changes. It believed that the board would need to wait at least until when Q2 inflation data is available before having a clearer idea on even the direction of the next move in interest rate, not to mention the timing.

Across the broader currency markets, trading remains relatively subdued, with most major currency pairs and crosses confined within the previous day's ranges. New Zealand Dollar is the weakest performer today so far , followed by Canadian Dollar and Euro. In contrast, Yen and the Australian Dollar are showing the most strength, while Dollar, Swiss Franc, and British Pound are trading in a mixed manner.

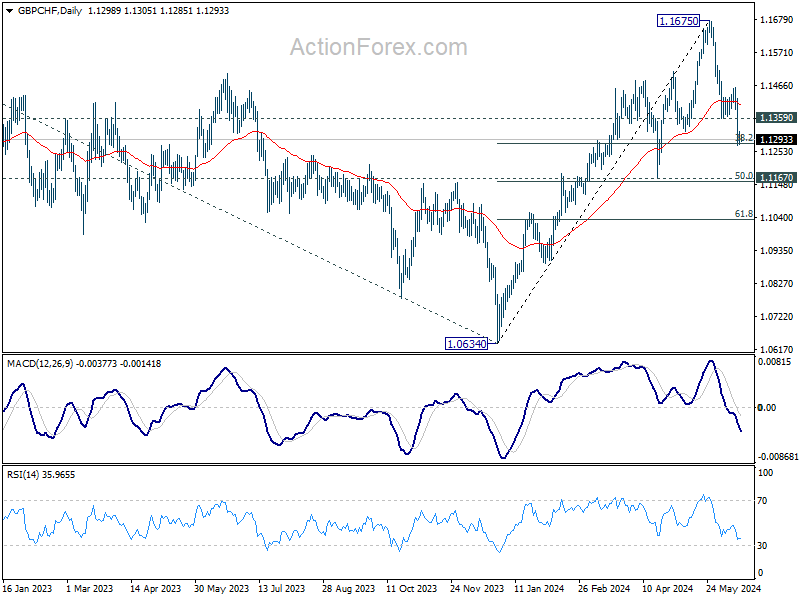

Technically, GBP/CHF's correction from 1.1675 medium term top extended lower last week and it's now pressing 38.2% retracement of 1.0634 to 1.1675 at 1.1277. Strong support could be seen from current level and bring of 1.1359 support turned resistance will bring more sustainable rebound. However, firm break of 1.1277 will bring deeper decline to 1.1167 cluster support next (50% retracement at 1.1155). With a combination of events of UK CPI tomorrow, BoE and SNB rate decision on Thursday, the next move will be revealed soon.

In Asia, at the time of writing, Nikkei is up 0.76%. Hong Kong HSI is up 0.02%. China Shanghai SSE is up 0.48%. Singapore Strait Times is up 0.16%. Japan 10-year JGB yield is up 0.015 at 0.946. Overnight, DOW rose 0.49%. S&P 500 rose 0.77%. NASDAQ rose 0.95%. 10-year yield rose 0.066 to 4.279.

RBA stands pat, still not ruling anything in or out

RBA left its cash rate target unchanged at 4.35%, as widely anticipated. It maintained its stance of "not ruling anything in or out," indicating a cautious approach and open stance amid ongoing economic uncertainties.

While inflation is easing, RBA noted that it is doing so "more slowly than previously expected," and inflation "remains high." The central bank acknowledged that it will be "some time yet" before inflation is sustainably within the target range.

RBA added that recent economic data have been "mixed," reinforcing the need to remain "vigilant to upside risks to inflation." Consequently, the path of interest rates "remains uncertain".

BoJ's Ueda reiterates possibility of July rate hike

BoJ Governor Kazuo Ueda reiterated today that the central bank could raise interest rates again in July, stressing that this decision would be independent of the plan to taper bond purchases.

Speaking to parliament, Ueda clarified, "Our decision on bond-buying taper and interest rate hikes are two different things." He emphasized that a rate hike at the next policy meeting will depend on the economic, price, and financial data available at the time.

A recent Reuters poll on Monday revealed that 31% of economists surveyed expect BoJ to raise interest rates at its next policy meeting on July 30-31. Another 41% predict the next hike will occur in October, while slightly more than 20% anticipate a September increase. The remaining economists do not foresee a rate hike until 2025. This diversity of expectations underscores the uncertainty in forecasting BoJ's policy move.

Fed's Harker sees one rate cut by year-end, stresses data dependence

Philadelphia Fed President Patrick Harker indicated overnight that his base case scenario includes one interest rate cut by the end of the year, contingent on several more months of improving inflation data.

Harker emphasized the need for ongoing assessment, stating, "If all of it happens to be as forecasted, I think one rate cut would be appropriate by year's end."

However, he also left room for adjustments based on new economic data, noting, "I see two cuts, or none, for this year as quite possible if the data break one way or another...we will remain data dependent."

Harker believes that the current policy interest rate, which has been steady for nearly 11 months, remains effective in maintaining restrictive conditions to bring inflation back to target and mitigate upside risks.

His outlook includes slowing but above-trend economic growth, a modest rise in the unemployment rate, and a gradual return to target inflation, which he describes as a "long glide."

Looking ahead

German ZEW economic sentiment is the main focus in European while Eurozone CPI final will be released too. Later in the day, US retail sales will be on the spotlight, industrial production and business invesntories will be released.

USD/JPY Daily Outlook

Daily Pivots: (S1) 157.27; (P) 157.62; (R1) 158.07; More...

USD/JPY is staying in tight range below 158.25 temporary top and intraday bias remains neutral. Further rally would be in favor as long as 154.53 support holds. Break of 158.25 will resume the choppy rise from 151.86 towards 160.20 high. But upside should be limited there, at least on first attempt.

In the bigger picture, price actions from 160.20 medium term top are seen as a corrective pattern to rise from 150.25 only. Another rally is still expected at a later stage through 160.02 to resume the larger up trend. However, decisive break of 150.87 will argue that larger correction is possibly underway, and target 146.47 support next.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 04:30 | AUD | RBA Interest Rate Decision | 4.35% | 4.35% | 4.35% | |

| 09:00 | EUR | Eurozone CPI Y/Y May F | 2.60% | 2.60% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y May F | 2.90% | 2.90% | ||

| 09:00 | EUR | Germany ZEW Economic Sentiment Jun | 50 | 47.1 | ||

| 09:00 | EUR | Germany ZEW Current Situation Jun | -69 | -72.3 | ||

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Jun | 47.2 | 47 | ||

| 12:30 | USD | Retail Sales M/M May | 0.30% | 0.00% | ||

| 12:30 | USD | Retail Sales ex Autos M/M May | 0.20% | 0.20% | ||

| 13:15 | USD | Industrial Production M/M May | 0.40% | 0.00% | ||

| 13:15 | USD | Capacity Utilization May | 78.60% | 78.40% | ||

| 14:00 | USD | Business Inventories Apr | 0.30% | -0.10% |

RBA stands pat, still not ruling anything in or out

RBA left its cash rate target unchanged at 4.35%, as widely anticipated. It maintained its stance of "not ruling anything in or out," indicating a cautious approach and open stance amid ongoing economic uncertainties.

While inflation is easing, RBA noted that it is doing so "more slowly than previously expected," and inflation "remains high." The central bank acknowledged that it will be "some time yet" before inflation is sustainably within the target range.

RBA added that recent economic data have been "mixed," reinforcing the need to remain "vigilant to upside risks to inflation." Consequently, the path of interest rates "remains uncertain".

(RBA) Statement by the Reserve Bank Board: Monetary Policy Decisions

At its meeting today, the Board decided to leave the cash rate target unchanged at 4.35 per cent and the interest rate paid on Exchange Settlement balances unchanged at 4.25 per cent.

Inflation remains above target and is proving persistent.

Inflation has fallen substantially since its peak in 2022, as higher interest rates have been working to bring aggregate demand and supply closer towards balance. But the pace of decline has slowed in the most recent data, with inflation still some way above the midpoint of the 2–3 per cent target range. Over the year to April, the monthly CPI indicator rose by 3.6 per cent in headline terms, and by 4.1 per cent excluding volatile items and holiday travel, which was similar to its pace in December 2023.

Broader data indicate continuing excess demand in the economy, coupled with elevated domestic cost pressures, for both labour and non-labour inputs. Conditions in the labour market eased further over the past month but remain tighter than is consistent with sustained full employment and inflation at target. Wages growth appears to have peaked but is still above the level that can be sustained given trend productivity growth. Recent data revisions suggest that consumption over the past year was stronger than previously suggested. At the same time, output growth has been subdued, and consumption per capita has been declining, as households restrain their discretionary expenditure and inflation weighs on real incomes.

The outlook remains highly uncertain.

The economic outlook remains uncertain and recent data have demonstrated that the process of returning inflation to target is unlikely to be smooth.

The central forecasts published in May were for inflation to return to the target range of 2–3 per cent in the second half of 2025 and to the midpoint in 2026. Since then, there have been indications that momentum in economic activity is weak, including slow growth in GDP, a rise in the unemployment rate and slower-than-expected wages growth. At the same time, the revisions to consumption and the saving rate and the persistence of inflation suggest that risks to the upside remain. Recent budget outcomes may also have an impact on demand, although federal and state energy rebates will temporarily reduce headline inflation. The persistence of services price inflation is a key uncertainty. Also, although growth in unit labour costs has eased, it remains high. Productivity growth needs to pick up in a sustained way if inflation is to continue to decline.

There is uncertainty around consumption growth. Real disposable incomes have now stabilised and are expected to grow later in the year, assisted by lower inflation and tax cuts. There has also been an increase in wealth, driven by housing prices. Together, these factors are expected to support growth in consumption over the coming year. But there is a risk that household consumption picks up more slowly than expected, resulting in continued subdued output growth and a noticeable deterioration in the labour market.

More broadly, there are uncertainties regarding the lags in the effect of monetary policy and how firms' pricing decisions and wages will respond to the slower growth in the economy at a time of excess demand, and while conditions in the labour market remain tight.

There also remains a high level of uncertainty about the overseas outlook. Output growth in most advanced economies appears to have troughed. There has been improvement in the outlook for the Chinese and US economies, and many commodity prices have picked up. Some central banks have eased policy, although they remain alert to the risk of persistent inflation. Nevertheless, geopolitical uncertainties, including those related to the conflicts in the Middle East and Ukraine, remain elevated, which may have implications for supply chains.

Returning inflation to target is the priority.

Returning inflation to target within a reasonable timeframe remains the Board's highest priority. This is consistent with the RBA's mandate for price stability and full employment. The Board needs to be confident that inflation is moving sustainably towards the target range. To date, medium-term inflation expectations have been consistent with the inflation target and it is important that this remains the case.

Inflation is easing but has been doing so more slowly than previously expected and it remains high. The Board expects that it will be some time yet before inflation is sustainably in the target range. While recent data have been mixed, they have reinforced the need to remain vigilant to upside risks to inflation. The path of interest rates that will best ensure that inflation returns to target in a reasonable timeframe remains uncertain and the Board is not ruling anything in or out. The Board will rely upon the data and the evolving assessment of risks. In doing so, it will continue to pay close attention to developments in the global economy, trends in domestic demand, and the outlook for inflation and the labour market. The Board remains resolute in its determination to return inflation to target and will do what is necessary to achieve that outcome.

BoJ’s Ueda reiterates possibility of July rate hike

BoJ Governor Kazuo Ueda reiterated today that the central bank could raise interest rates again in July, stressing that this decision would be independent of the plan to taper bond purchases.

Speaking to parliament, Ueda clarified, "Our decision on bond-buying taper and interest rate hikes are two different things." He emphasized that a rate hike at the next policy meeting will depend on the economic, price, and financial data available at the time.

A recent Reuters poll on Monday revealed that 31% of economists surveyed expect BoJ to raise interest rates at its next policy meeting on July 30-31. Another 41% predict the next hike will occur in October, while slightly more than 20% anticipate a September increase. The remaining economists do not foresee a rate hike until 2025. This diversity of expectations underscores the uncertainty in forecasting BoJ's policy move.

Fed’s Harker sees one rate cut by year-end, stresses data dependence

Philadelphia Fed President Patrick Harker indicated overnight that his base case scenario includes one interest rate cut by the end of the year, contingent on several more months of improving inflation data.

Harker emphasized the need for ongoing assessment, stating, "If all of it happens to be as forecasted, I think one rate cut would be appropriate by year's end."

However, he also left room for adjustments based on new economic data, noting, "I see two cuts, or none, for this year as quite possible if the data break one way or another...we will remain data dependent."

Harker believes that the current policy interest rate, which has been steady for nearly 11 months, remains effective in maintaining restrictive conditions to bring inflation back to target and mitigate upside risks.

His outlook includes slowing but above-trend economic growth, a modest rise in the unemployment rate, and a gradual return to target inflation, which he describes as a "long glide."

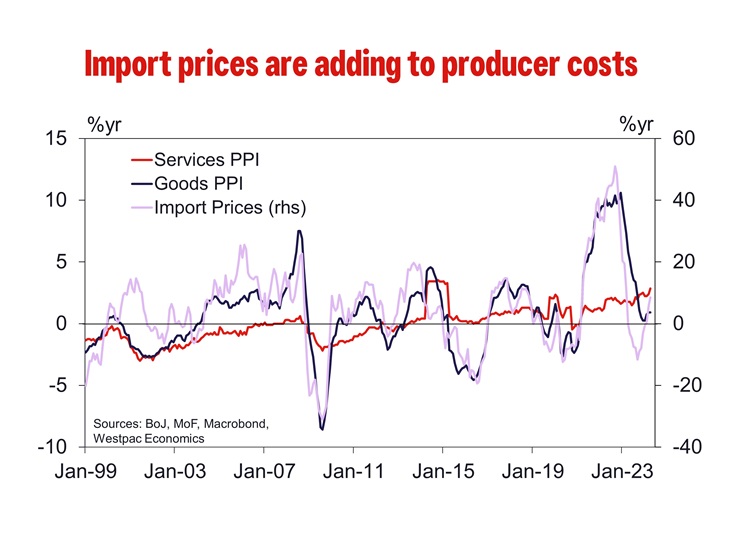

Yen Appreciation and Policy Normalisation are Still Some Way for Japan

A weak Yen is aiding the Bank of Japan's inflation objective for now by dislodging the deflationary mindset. But homegrown inflation needs further wage increases and investment.

The Bank of Japan (BoJ) raised rates at its March meeting. Since then, the Yen has held above USD/JPY150, a level traditionally regarded as a trigger for intervention. While there is evidence that the Ministry of Finance has intervened in recent months, its actions have come only as the spot rate threatened JPY160 and have also been limited in duration, leaving USD/JPY currently trading towards the top end of the recent range at JPY157.

We take from this market activity that authorities are reticent to allow a further rapid depreciation in the Yen but are not overly concerned by sustained weakness in the currency. Arguably that is because a higher rate structure (and lower USD/JPY) can only be justified by the inflation target being sustainably achieved. The weak Yen fosters cost-push inflation, furthering the BoJ’s inflation objective in two important ways: 1) via the pass-through of input inflation to consumer prices; and 2) the reshaping of inflation expectations amongst businesses and households.

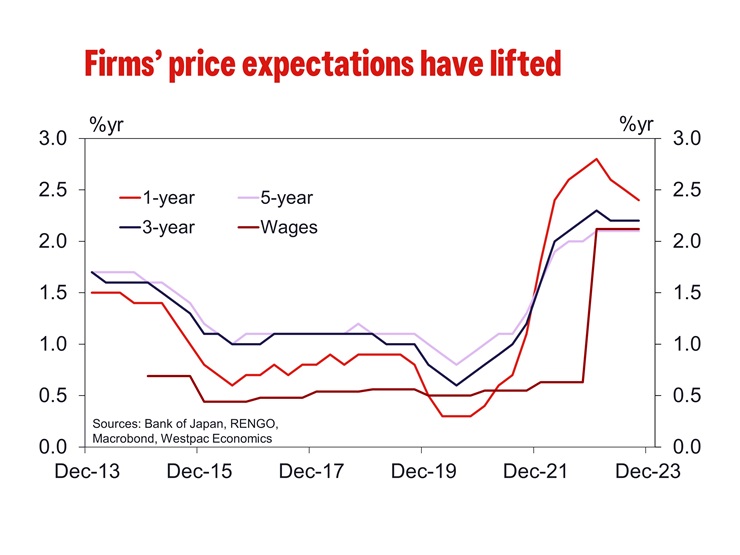

Historically, higher costs have prompted Japanese firms to cut costs by narrowing profit margins, bargaining with suppliers or reducing their wage bills. However, in this episode, the persistence of input price pressures, significant (largely co-incident) wage gains, and the global narrative around inflation have helped to dislodge the traditional mindset of Japanese firms. Normalising price increases is also proving to be the first step towards sustained real wage gains and businesses investing in future capacity, alleviating any lingering concerns amongst businesses that higher prices will sap demand.

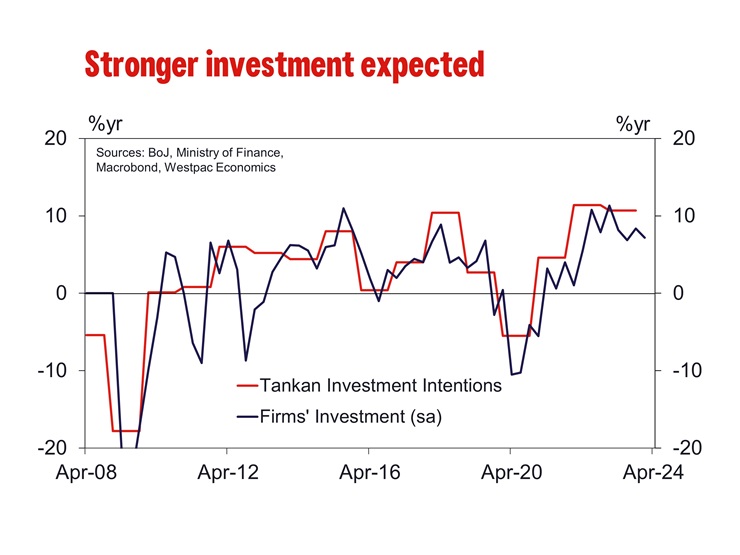

Innovation in particular has taken a considerable hit in recent decades amongst businesses focused on the domestic economy as firms perceived an unwillingness on the part of households to pay for new or improved goods and services. However, this may finally be taking a turn. Investment in plant and equipment grew rapidly through 2023, beating the peak set in 2007 and second only to the record set in Q4 1991. The Tankan’s surveyed investment intentions also peaked in Q3 2022 at the second highest level since 1989. Strong profits have certainly helped businesses invest, but so has the shifting inflation mindset. A survey conducted by the BoJ showed that participants in the corporate sector preferred moderate rises in prices and wages as it removed the ‘need for cost cuts to avoid raising prices enabling active fixed investment and wage hikes’.

Inflation above target for a sustained period has also lifted inflation expectations. Japan’s inflation expectations are responsive to price shocks. This is supported by our analysis of historic shocks and financial market measures of inflation expectations. The BoJ also characterise price expectations as ‘adaptive rather than forward-looking’, evinced through history with inflation expectations settling close to 1% as headline inflation averaged 0.5% between 1990 and 2019.

Recently, expectations have risen and settled around the 2% target according to both the outlook in general and output price expectations collected in the Tankan survey. High imported inflation from a weak Yen have clearly bought time for demand-pull inflation to build strength. For inflation to persist at target however, demand pressures must become dominant and sustainable, particularly with the Yen near the level authorities have recently intervened at, and with global rates now falling.

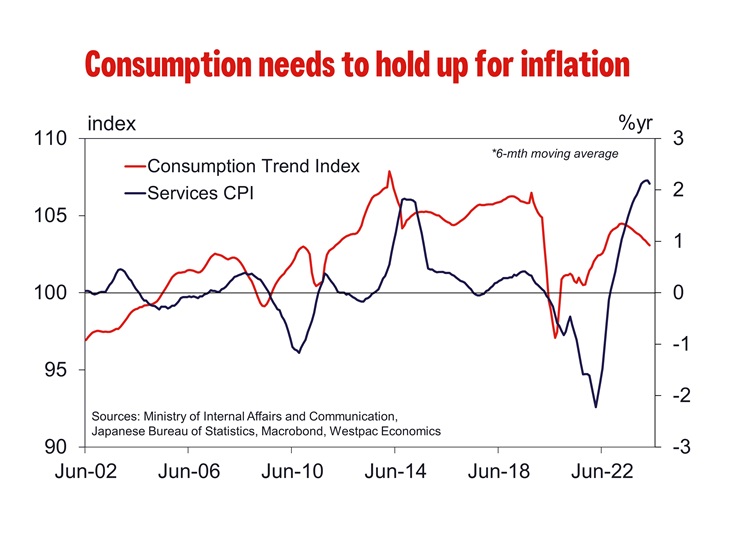

The demographic challenge in Japan means that savings will remain high, posing a risk to reestablishing a healthier demand-driven inflation. Whether there is a shift in consumption will be seen in the household spending data in the second half of 2024, when most wage increases will be received. While strong services inflation implies wages are already feeding through to inflation, assessment is difficult due to the surge in foreign tourist spending. A pick-up in household spending in late-2024 would signal that consumers are looking to make purchases sooner to avoid price increases – a deviation from the deflationary mindset of the past. Further robust increases in wages in the 2025 Shunto negotiations would provide additional support for consumer confidence and spending, and entrench a change in the consumer psychology around prices.

While this transition takes hold, it is also important that businesses focus on expansion and productivity over efficiency. In doing so, lasting weakness in the Yen can add to inflation as wages, consumption and investment continue to expand. Arguably, GDP growth sustainably at or above trend is a necessary prerequisite for households to feel as though the economy is fully employed and inflation at target is justified.

It is only after expectations are fully reset and inflation consistently at or above target that the BoJ will be justified in lifting the policy rate materially above the lower bound. This is not to say they will not edge policy rates higher in coming months, but to emphasise that policy will need to be restrained if its to avoid jeopardising the years (indeed decades) of progress that have been required to get to this point.

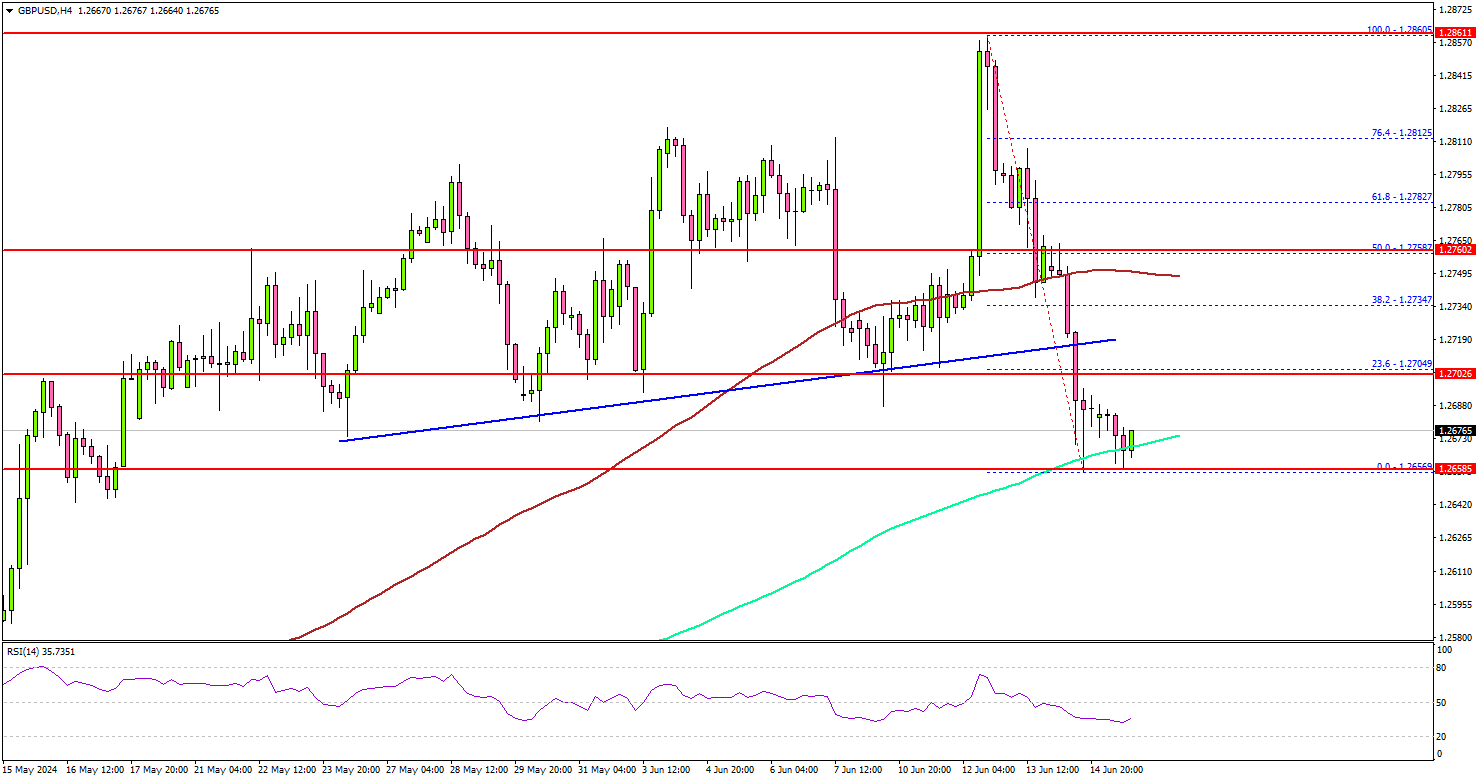

GBP/USD Dips as Bulls Take a Breather, Key Levels To Watch

Key Highlights

- GBP/USD started a downside correction from the 1.2860 resistance.

- It traded below a key bullish trend line with support at 1.2720 on the 4-hour chart.

- EUR/USD is eyeing a recovery wave from the 1.0665 support zone.

- Oil prices are moving higher toward the $80.80 resistance.

GBP/USD Technical Analysis

The British Pound peaked near 1.2860 and started a fresh decline against the US Dollar. GBP/USD traded below 1.2800 and 1.2740 support levels to enter a short-term bearish zone.

Looking at the 4-hour chart, the pair traded below a key bullish trend line with support at 1.2720. The bears were able to push the pair below the 100 simple moving average (red, 4-hour) and it tested the 200 simple moving average (green, 4-hour).

A low was formed at 1.2655 and the pair is now consolidating losses. If there is a fresh increase, the pair might face resistance near the 23.6% Fib retracement level of the downward move from the 1.2860 swing high to the 1.2655 low.

The first major resistance is near the 1.2740 level. A clear move above the 1.2740 resistance might send it toward the 1.2780 level. Any more gains might call for a move toward the 1.2860 level in the near term.

If not, the pair might dip again. Immediate support is near the 1.2655 level. The next major support is near the 1.2620 zone. A downside break and close below the 1.2620 support zone could open the doors for a larger decline. In the stated case, the pair could decline toward the 1.2550 level.

Looking at EUR/USD, the pair found support near the 1.0665 zone and it could now aim for a recovery wave in the near term.

Economic Releases

- US Retail Sales for May 2024 (MoM) – Forecast +0.2%, versus 0% previous.

- Fed's Logan speech.