Sample Category Title

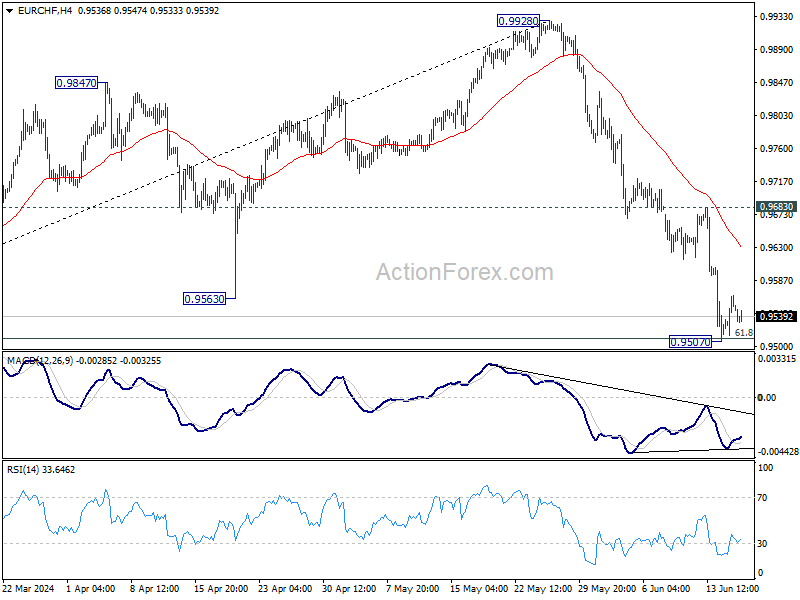

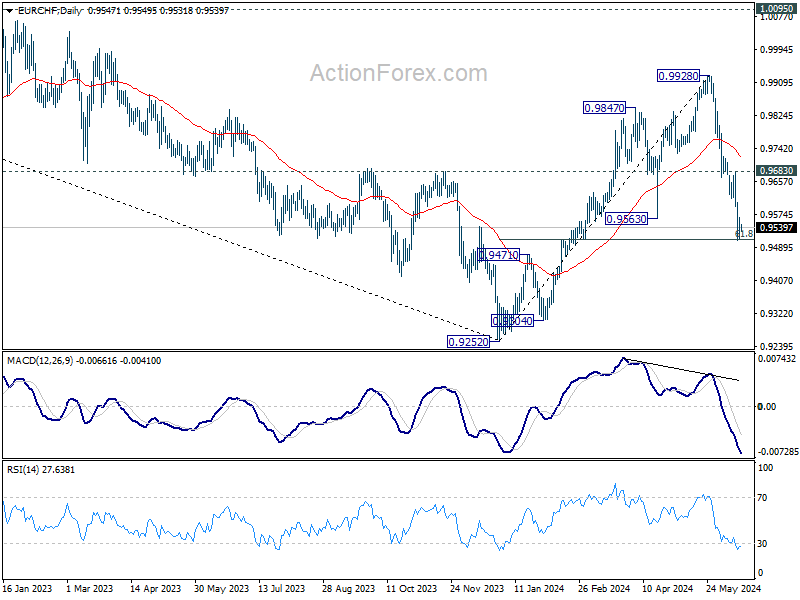

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9520; (P) 0.9544; (R1) 0.9572; More....

Intraday bias in EUR/CHF is turned neutral first with current recovery. Some consolidations would be seen first, but upside should be limited below 0.9683 resistance to bring another fall. On the downside, sustained trading below 61.8% retracement of 0.9252 to 0.9928 at 0.9510 will raise the chance of long term down trend resumption, and target 0.9252 low next.

In the bigger picture, the break of 0.9563 support, as well as 55 W EMA (now at 0.9672) argues that rebound from 0.9252 has completed at 0.9928. Medium term bearish is maintained with both 1.0095 resistance intact. Firm break of 0.9252 will resume the down trend from 1.2004 (2018 high).

Dollar Took a Breather But Shows Resilience Despite More Constructive Risk Sentiment

Markets

The European risk-off from last week shifted into a lower gear. Markets pondered comments from Marine Le Pen of the far right Rassemblement National as she indicated she would respect France’s institutions and was prepared to cooperate with President Macron after the elections. Bunds returned part of their safe haven gains with yields rebounding 5-6 bps across the curve. Bund yields also rose more than swaps. The French 10-y yield spread vs Bunds still widened slightly further (+2 bps to 0.79%). Spreads of other South-European bonds (Italy, Spain, Portugal, Greece) that faced material collateral damage last week narrowed about 3-4 bps (vs Bunds). European equities (EuroStoxx 50 + 0.85%, CAC 40 + 0.91%) tried a bottoming out process after recent sell-off. ECB policymakers including Chief Economist Lane still labelled last week’s repositioning as orderly. The ECB currently has no intention to step in/activate the TPI mechanism. US yields which are still mainly driven by monetary policy considerations rather than by risk sentiment, also rebounded after last week’s soft May price data. A better than expected Empire Manufacturing survey helped US yields to cautiously move away from recent lows/key support levels. US yields rose 5.5-6.5 bps across the curve. In an outright disconnect from European markets, the S&P500 (+0.77%) and the Nasdaq (+ 0.95%) continued their record race. The dollar took a breather (DXY 105.32 from 105.51) but shows resilience despite a more constructive risk sentiment overall. EUR/USD closed at 1.0734 from 1.07 at the open. Still, the picture looks fragile. EUR/GBP also tries to move away from the 0.84 support area (close 0.845) as markets prepare for tomorrow’s UK CPI data and Thursday’s Bank of England policy decision.

This morning, Asian equities join the constructive sentiment on WS yesterday, mostly rising 0.5%-1.0%. Dollar gains marginally (EUR/USD 1.072, DXY 105.45). Later today, US May retail sales are scheduled for release. After a poor showing in April (0.0% M/M headline) markets look out whether the US consumer is able to keep growth afloat (headline 0.2% expected, control group +0.4%). After last week’s softer than expected price data (CPI, PPI and import prices) markets already frontloaded more easing, both for this and next year, than what the Fed is guiding. Still we see an asymmetrical risk for yields to again test the downside in case of a poor outcome. In Europe, political uncertainty will continue to linger. EUR/USD probably remains captured in a sell-on-upticks dynamics.

News & Views

Australia’s central bank left its policy rate unchanged at 4.35%. The pace of disinflation is slowing, but inflation still stays some way above the midpoint of the 2–3 per cent target range. The April CPI indicator rose by 3.6% y/y (up from 3.5% the month before) and core (ex. volatile items and holiday travel) by 4.1%. The May forecast assumed a return within the target in H2 2025 and to the midpoint in 2026. The economy remains in a state of excess demand and domestic cost pressures stay elevated. Labour market conditions eased but remain tighter than is consistent with full employment and inflation at target. The RBA concludes that while recent data have been mixed, they have been reinforcing the need to be vigilant for upside risks to inflation. The RBA ended the statement with the small yet meaningful addition that it will do what is necessary to achieve its goal. Board chair Bullock during the press conference later revealed they discussed the case for a rate hike. These hawkish tweaks pushed up Australian swap yields marginally intraday, allowing the curve to pare net daily declines to 0.5-1.9 bps with the long end outperforming. Money markets have changed little to their policy rate expectations and still pencil in a first cut in February next year. The Australian dollar trades basically unchanged just north of AUD/USD 0.66.

Germany’s electrical and metal workers union, the country’s largest industrial one, is upping the ante ahead of wage negotiations due to kick off this September. It is demanding a 7% increase for a 12-month period for the roughly 4 mln workers in a sector that’s a bellwether for wage agreements in other sectors. Given the industrial malaise in Germany and the fact that inflation was only 2.8% in May, the demand showcases ongoing efforts of union to recover some of the lost purchasing power over the previous years. It’s also closely watched by the ECB as it seeks signs for wage growth to slow down to help bringing back inflation sustainably to its 2% target.

Graphs

GE 10y yield

The ECB cut its key policy rates by 25 bps at the June policy meeting. A more bumpy inflation path in H2 2024, the EMU economy gradually regaining traction and the Fed’s higher for longer US strategy make follow-up moves difficult. Markets are coming to terms with that. For the time being, though, the political narrative dominates. After hitting a new YtD top at 2.7%, the German 10-yr yield corrected lower on safe haven bids.

US 10y yield

The Fed is seeking more evidence than just one slower-than-expected (May) CPI is providing. Upgraded inflation forecasts and a higher neutral rate complicate the exact timing of a first cut further. June dots suggest one move in 2024 followed by four more next year. Markets are positioned more aggressively, turning the recent low in yields into a technical support zone. The US 10-y yield is testing the downside of the 4.2/4.7% trading range.

EUR/USD

EUR/USD is trapped in the 1.06-1.09 range. The desynchronized rate cut cycle with the ECB exceptionally taking the lead, strong US May payrolls and a swing to the right in European elections pulled the pair away from 1.09 resistance. The Fed meeting balanced the weaker than expected US CPI outcome. Euro fragility makes a return to the 1.06 downside more likely than not.

EUR/GBP

Debate at the Bank of England is focused at the timing of rate cuts. Slower than expected April disinflation and a surprise general election on July 4 suggest that a June cut in line with the ECB looks improbable. Sterling gained momentum with money markets now discounting a Fed-like scenario. EUR/GBP tested the 2023 & 2024 lows near 0.85. Euro weakness eventually pulled the trick after French president Macron called snap elections following a weak showing in EU elections.

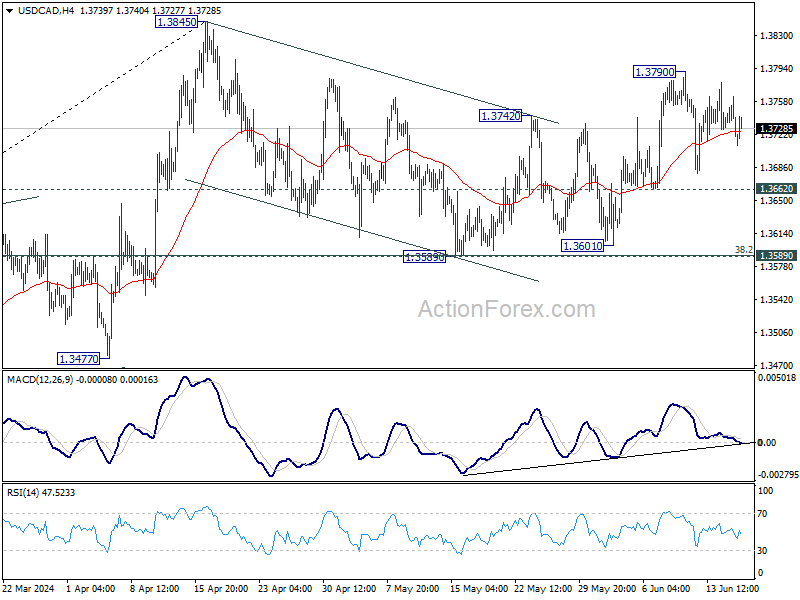

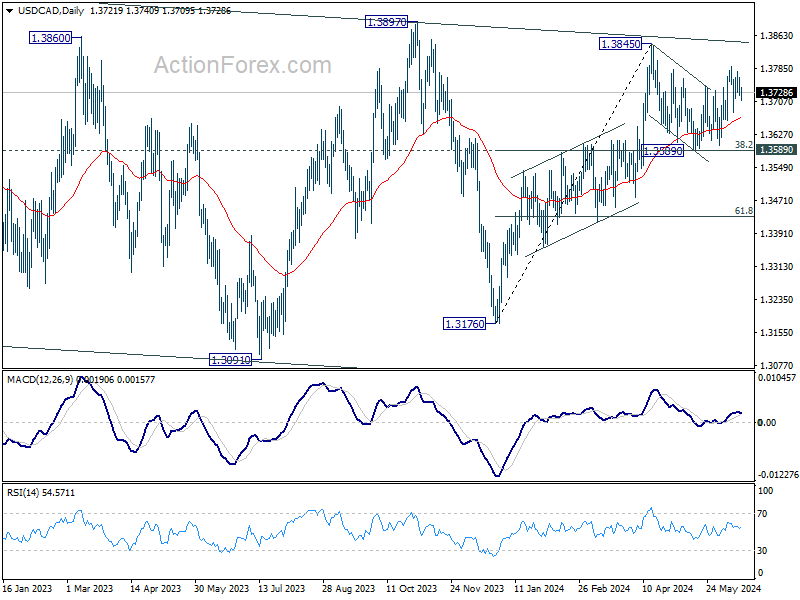

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3709; (P) 1.3736; (R1) 1.3752; More...

Intraday bias in USD/CAD stays neutral as range trading continues. Corrective fall from 1.3845 should have completed already. Further rally is expected as long as 1.3662 support holds. Break of 1.3790 will target a retest on 1.3845 first. Nevertheless, break of 1.3662 will turn bias to the downside to extend the corrective pattern from 1.3845 with another falling leg.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

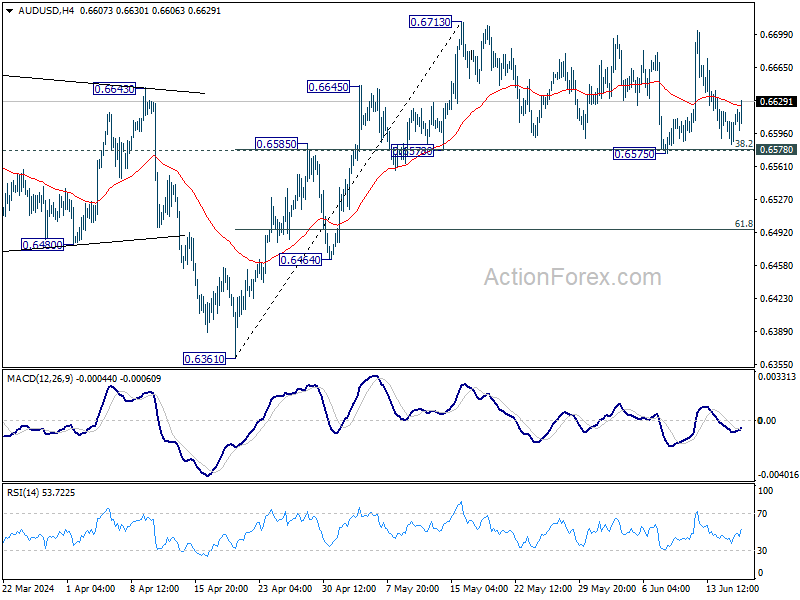

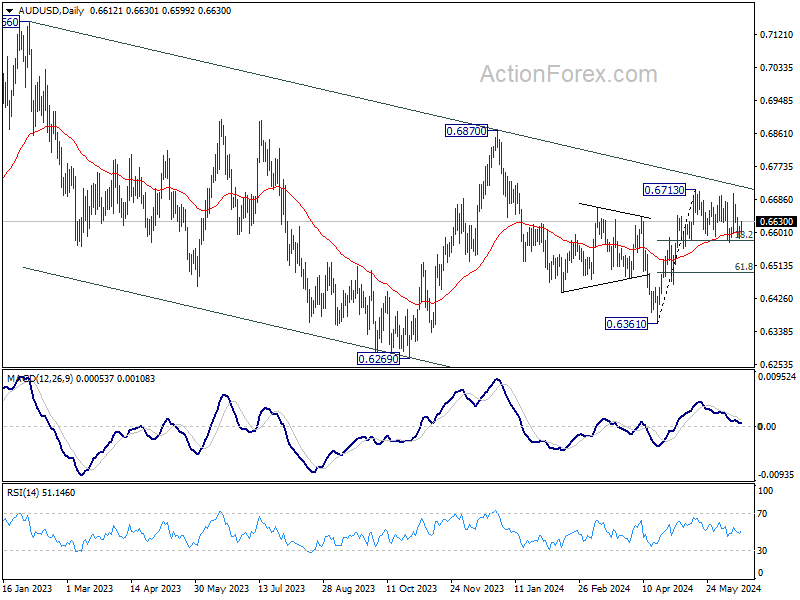

AUD/USD Daily Report

Daily Pivots: (S1) 0.6592; (P) 0.6606; (R1) 0.6626; More...

AUD/USD recovered ahead of 0.6578 cluster support (38.2% retracement of 0.6361 to 0.6713 at 0.6579), but stays well below 0.6713 resistance. Intraday bias remains neutral first. Further rally remains in favor with 0.6578 intact. On the upside, firm break of 0.6713 will resume whole rise from 0.6361 to 0.6870 resistance next. However, sustained break of 0.6578 will dampen this bullish view, and bring deeper fall to 61.8% retracement at 0.6495.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could have completed at 0.6269 already. Rise from there is seen as the third leg which is now trying to resume through 0.6870 resistance.

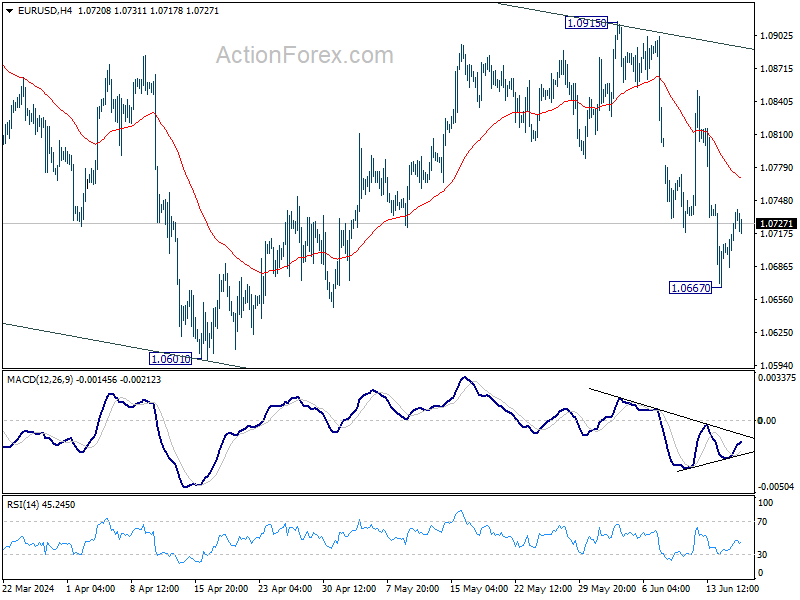

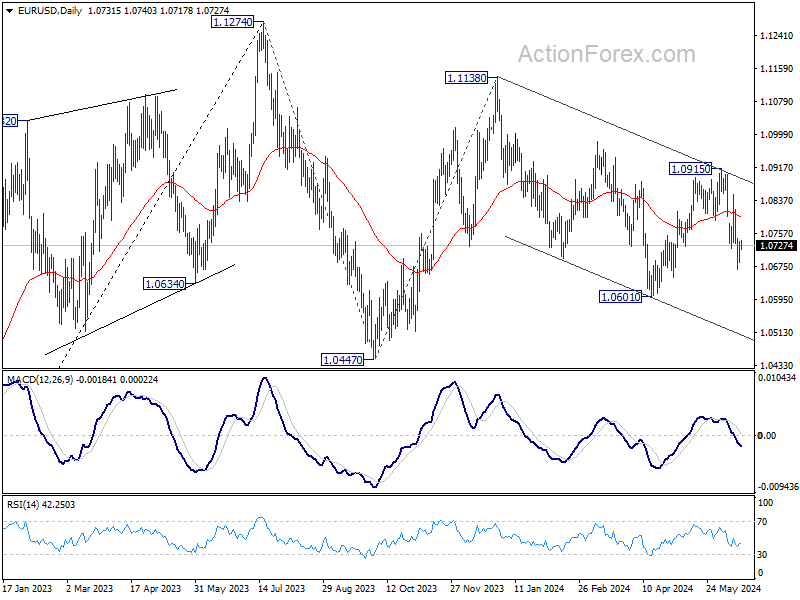

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0701; (P) 1.0719; (R1) 1.0753; More....

Intraday bias in EUR/USD is turned neutral with current retreat. Further fall is expected as long as 55 4H EMA (now at 1.0770) holds. Fall from 1.0915 is seen as another leg in the larger corrective pattern. Below 1.0677 will target 1.0601 low first. Firm break there will target channel support at 1.0510 next.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's still in progress. Break of 1.0601 will target 1.0447 support and possibly further to 100% projection of 1.1274 to 1.0447 from 1.1138 at 1.0311. For now, this will remain the favored case as long as 1.0915 resistance holds, in case of rebound.

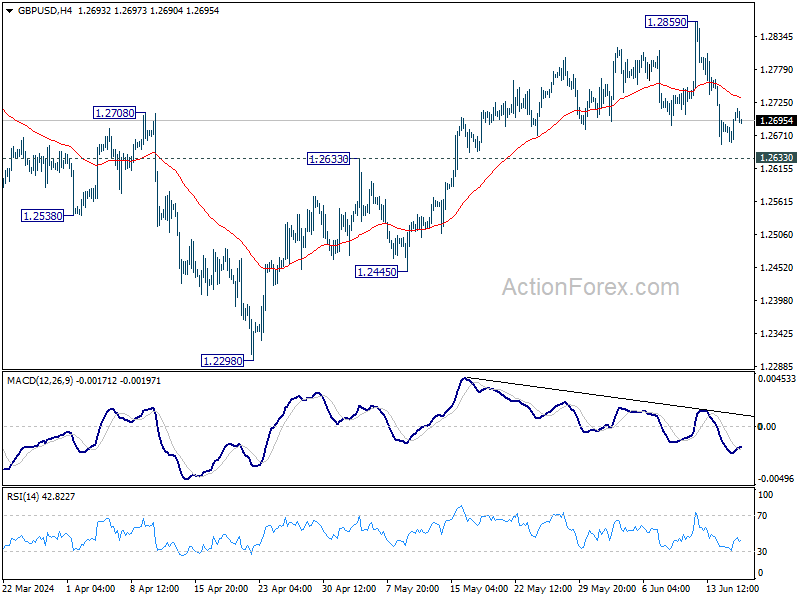

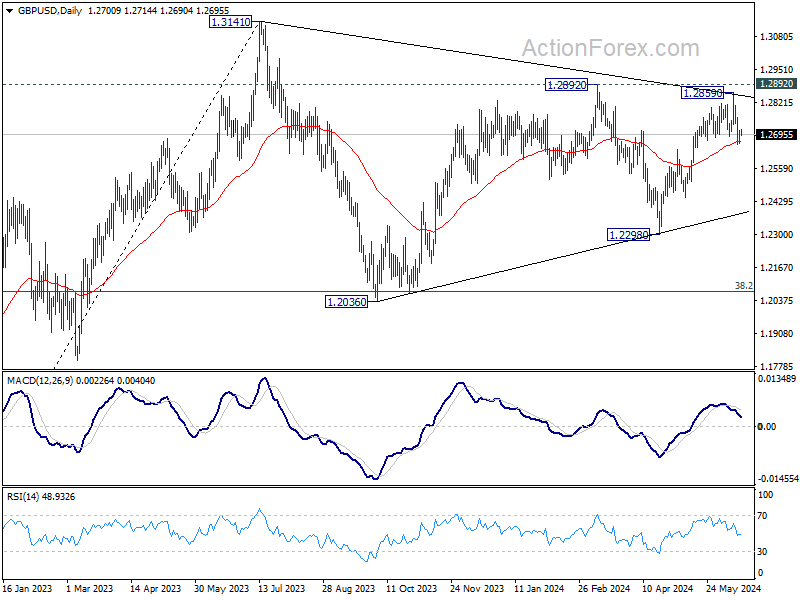

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2673; (P) 1.2691; (R1) 1.2724; More...

Intraday bias in GBP/USD is turned neutral with current recovery. Risk will stay on the downside as long as 1.2859 resistance holds. Firm break of 1.2633 resistance turned support will argue that whole rise from 1.2298 has completed, and target 1.2445 and below.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2445 support will extend the corrective pattern with another decline instead.

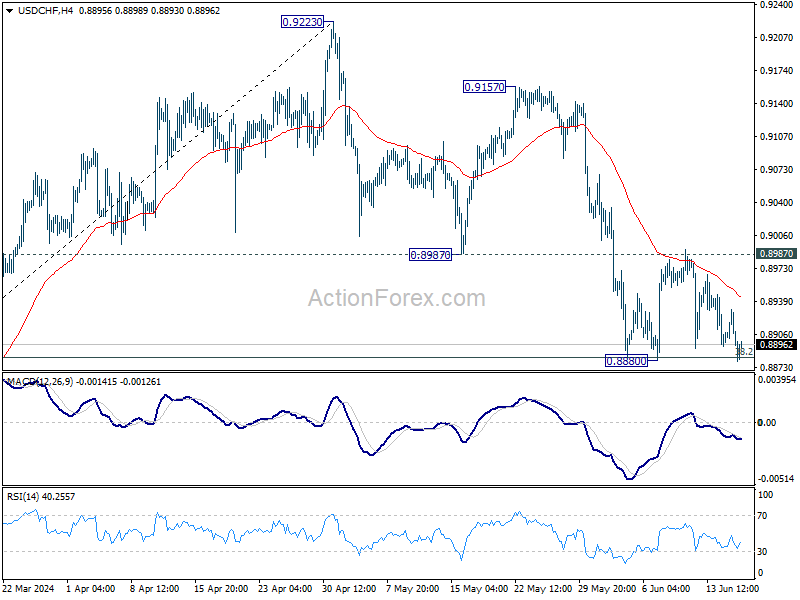

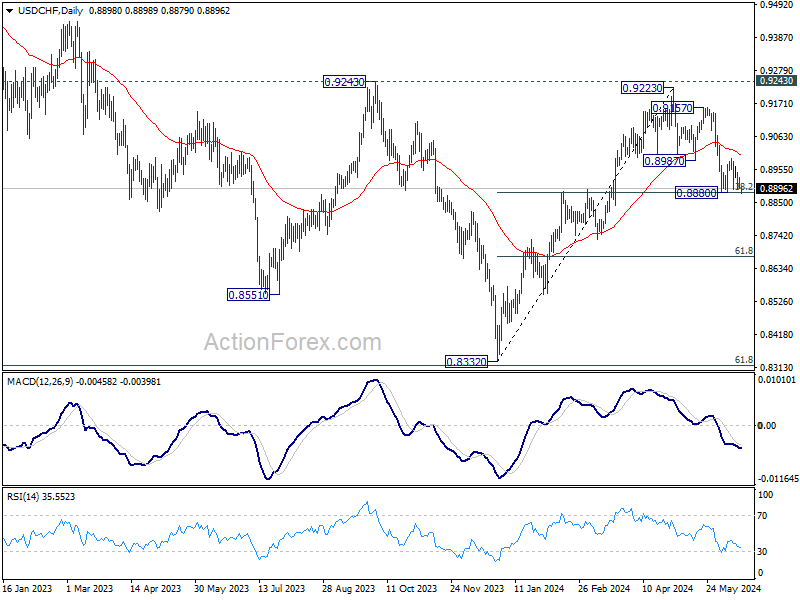

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8883; (P) 0.8908; (R1) 0.8921; More….

Intraday bias in USD/CHF remains neutral as range trading continues. On the downside, sustained break of 0.8883 fibonacci level will carry larger bearish implications and bring deeper decline. On the upside, firm break of 0.8987 support turned resistance will argue that correction from 0.9223 has completed, after drawing support from 0.8883 fibonacci level. Intraday bias will be back on the upside for 0.9157/9223 resistance zone.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146..

The US and the Rest

The S&P500 hit a record high yesterday, its 30th record high since the beginning of this year. The technology stocks led the rally. Apple, which revealed its plans to integrate ChatGPT into its iPhones last week, gained 2% and Tesla jumped more than 5% on news that it has been given approval to test its advanced driver-assistance system on some streets in Shanghai. Nasdaq 100 is now a few points below the 20’000 psychological mark and it’s not about if but when it will take out this level. Nasdaq’s PE forward ratio is around 26, high but still lower than the 2020 peak, and much lower than the dot.com levels. IMF said that almost a third of global capital flew int the US since Covid, compared to only 18% before the pandemic. The slow recovery and political turmoil in Europe, war in Ukraine and the geopolitical tensions with China help driving funds toward fertile American markets thanks to new AI opportunities – and high interest rates. Bloomberg points that some market optimists believe that around $6 trillion that’s sitting in money-market cash could be reallocated to equities to further boost the equity rally. And today, big banks revise their price targets for the S&P500 higher. Citi and Goldman for example expect the S&P500 to end the year at 5600, while Evercore thinks that the S&P500 stocks will advance to 6000.

Of course, this much optimism is never good sign and when you start hearing big revisions to price targets, it’s generally time to sell. But sell to go where? The European and the British stocks were supposed to perform well in the reflation context and now they are falling off the race. China is sputtering with housing crisis, geopolitical tensions and slow recovery. Other emerging markets are bearing the brunt of a polarized world and uncertain global outlook.

Yesterday, Federal Reserve’s (Fed) Neel Kashkari said that they’re in a good position to take their time before announcing the first rate cut and Philadelphia Fed’s Patrick Harker said that one rate cut would be appropriate this year. The US 2-year yield hovers around 4.75% and the 10-year yield is just below the 4.30% mark. Today, all eyes are on the US retail sales and industrial production data. A softer-than-expected set of figures could fuel the Fed doves, while stronger-than-expected data could fuel the goldilocks optimism. If investors want to see the glass half full, they will find a reason to do so.

Politics and monetary politics

The US dollar will likely continue to take advantage of the European political uncertainties regardless of the data and Fed talk. The EURUSD traded below the 1.07 mark for the second session yesterday but managed to throw itself above this level on relief that Marine Le Pen is willing to work with Macron if she wins the legislative elections.

The French equities were better bid yesterday, near the oversold levels, as some investors saw opportunity in French companies at discounted prices. Those who bought justified their decision by the fact that the French political turmoil never had a significant impact on economics and that the politically-motivated selloff has certainly been overdone.

Zooming out, the euro traders will keep an eye on the latest EZ inflation figures due to be released this morning, and show that inflation in the Eurozone may have ticked higher both for headline and core figures amid wages growth acerated 5.3% in Q1 – a nightmare for the ECB doves. If that’s the case, we could maybe see a certain upside pressure from fading next European Central Bank (ECB) cut expectations. But the political jitters will continue to carry a downside risk for the euro in the coming weeks, both against the greenback and sterling.

Elsewhere, the Reserve Bank of Australia (RBA) maintained its cash rate unchanged for the fifth time at today’s policy meeting and reiterated caution regarding inflation. The Bank of England (BoE) is expected to stay pat at Thursday’s policy meeting even though some think that we could see a surprise rate cut from the Brits because a last minute cut would hardly interfere with the election outcome – and certainly not offer Tories any additional vote, while the Swiss National Bank (SNB) is expected to announce status quo on Thursday given the latest uptick in Swiss inflation and the ECB’s reluctance to cut more. The EURCHF is heavily hit by the French uncertainties and will likely remain under pressure until the election dust settles while the USDCHF is testing a critical Fibonacci support, the 38.2% level. If this level is cleared, we could see the pair snap back into the bearish consolidation zone but that’s not my base case scenario. While the current worldwide political setup is favourable for safe haven inflows into the franc, the easing bias from the SNB should limit the franc’s appreciation and keep the franc on a softening path.

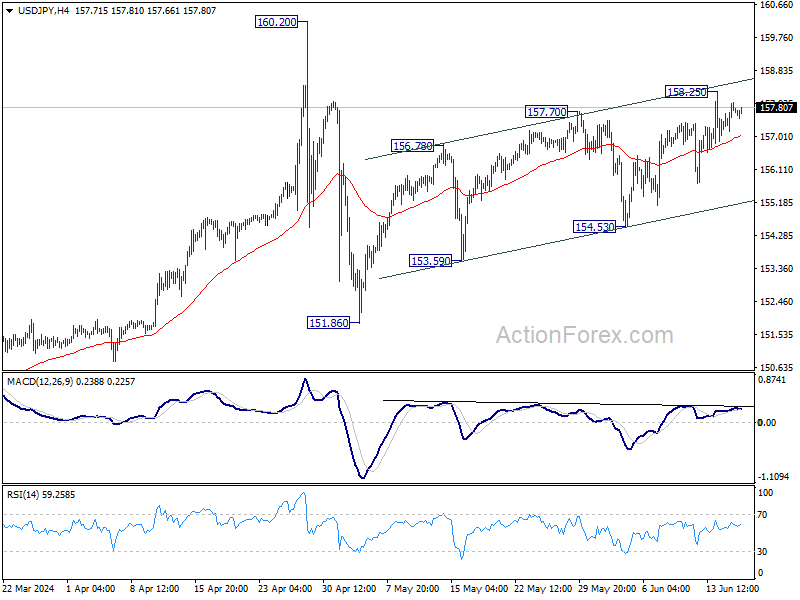

USD/JPY Daily Outlook

Daily Pivots: (S1) 157.27; (P) 157.62; (R1) 158.07; More...

USD/JPY is staying in tight range below 158.25 temporary top and intraday bias remains neutral. Further rally would be in favor as long as 154.53 support holds. Break of 158.25 will resume the choppy rise from 151.86 towards 160.20 high. But upside should be limited there, at least on first attempt.

In the bigger picture, price actions from 160.20 medium term top are seen as a corrective pattern to rise from 150.25 only. Another rally is still expected at a later stage through 160.02 to resume the larger up trend. However, decisive break of 150.87 will argue that larger correction is possibly underway, and target 146.47 support next.

Yen Recovers as BoJ’s Ueda Reiterates July Hike Possibility, But Gains Capped by Uncertainty

Japanese Yen had a modest recovery in Asian session, accompanied by an uptick in 10-year JGB yield and Nikkei. This comes as BoJ Governor Kazuo Ueda continued to prepare the markets for more tightening ahead, by reiterating that another rate hike in July is a possibility. Additionally, Ueda emphasized the impact of the weak Yen on import prices and overall inflation. However, opinions are divided on the timing of BoJ's next rate hike after the historical move in March. Thus, Yen's recovery might remain limited until there is more clarity.

Simultaneously, Australian Dollar edged higher following RBA's decision to keep interest rates unchanged at 4.35%, a move that was widely anticipated by the markets. RBA maintained its flexible stance, stating it is "not ruling anything in or out" regarding future rate changes. It believed that the board would need to wait at least until when Q2 inflation data is available before having a clearer idea on even the direction of the next move in interest rate, not to mention the timing.

Across the broader currency markets, trading remains relatively subdued, with most major currency pairs and crosses confined within the previous day's ranges. New Zealand Dollar is the weakest performer today so far , followed by Canadian Dollar and Euro. In contrast, Yen and the Australian Dollar are showing the most strength, while Dollar, Swiss Franc, and British Pound are trading in a mixed manner.

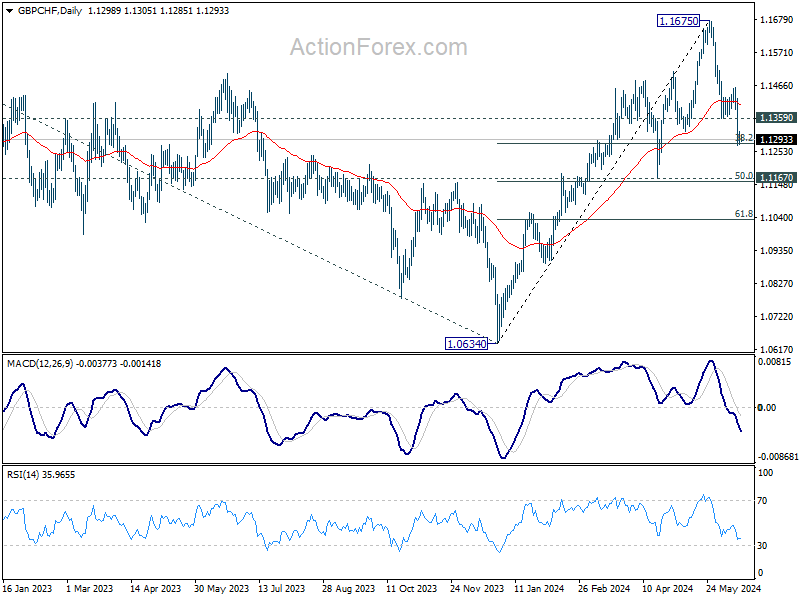

Technically, GBP/CHF's correction from 1.1675 medium term top extended lower last week and it's now pressing 38.2% retracement of 1.0634 to 1.1675 at 1.1277. Strong support could be seen from current level and bring of 1.1359 support turned resistance will bring more sustainable rebound. However, firm break of 1.1277 will bring deeper decline to 1.1167 cluster support next (50% retracement at 1.1155). With a combination of events of UK CPI tomorrow, BoE and SNB rate decision on Thursday, the next move will be revealed soon.

In Asia, at the time of writing, Nikkei is up 0.76%. Hong Kong HSI is up 0.02%. China Shanghai SSE is up 0.48%. Singapore Strait Times is up 0.16%. Japan 10-year JGB yield is up 0.015 at 0.946. Overnight, DOW rose 0.49%. S&P 500 rose 0.77%. NASDAQ rose 0.95%. 10-year yield rose 0.066 to 4.279.

RBA stands pat, still not ruling anything in or out

RBA left its cash rate target unchanged at 4.35%, as widely anticipated. It maintained its stance of "not ruling anything in or out," indicating a cautious approach and open stance amid ongoing economic uncertainties.

While inflation is easing, RBA noted that it is doing so "more slowly than previously expected," and inflation "remains high." The central bank acknowledged that it will be "some time yet" before inflation is sustainably within the target range.

RBA added that recent economic data have been "mixed," reinforcing the need to remain "vigilant to upside risks to inflation." Consequently, the path of interest rates "remains uncertain".

BoJ's Ueda reiterates possibility of July rate hike

BoJ Governor Kazuo Ueda reiterated today that the central bank could raise interest rates again in July, stressing that this decision would be independent of the plan to taper bond purchases.

Speaking to parliament, Ueda clarified, "Our decision on bond-buying taper and interest rate hikes are two different things." He emphasized that a rate hike at the next policy meeting will depend on the economic, price, and financial data available at the time.

A recent Reuters poll on Monday revealed that 31% of economists surveyed expect BoJ to raise interest rates at its next policy meeting on July 30-31. Another 41% predict the next hike will occur in October, while slightly more than 20% anticipate a September increase. The remaining economists do not foresee a rate hike until 2025. This diversity of expectations underscores the uncertainty in forecasting BoJ's policy move.

Fed's Harker sees one rate cut by year-end, stresses data dependence

Philadelphia Fed President Patrick Harker indicated overnight that his base case scenario includes one interest rate cut by the end of the year, contingent on several more months of improving inflation data.

Harker emphasized the need for ongoing assessment, stating, "If all of it happens to be as forecasted, I think one rate cut would be appropriate by year's end."

However, he also left room for adjustments based on new economic data, noting, "I see two cuts, or none, for this year as quite possible if the data break one way or another...we will remain data dependent."

Harker believes that the current policy interest rate, which has been steady for nearly 11 months, remains effective in maintaining restrictive conditions to bring inflation back to target and mitigate upside risks.

His outlook includes slowing but above-trend economic growth, a modest rise in the unemployment rate, and a gradual return to target inflation, which he describes as a "long glide."

Looking ahead

German ZEW economic sentiment is the main focus in European while Eurozone CPI final will be released too. Later in the day, US retail sales will be on the spotlight, industrial production and business invesntories will be released.

USD/JPY Daily Outlook

Daily Pivots: (S1) 157.27; (P) 157.62; (R1) 158.07; More...

USD/JPY is staying in tight range below 158.25 temporary top and intraday bias remains neutral. Further rally would be in favor as long as 154.53 support holds. Break of 158.25 will resume the choppy rise from 151.86 towards 160.20 high. But upside should be limited there, at least on first attempt.

In the bigger picture, price actions from 160.20 medium term top are seen as a corrective pattern to rise from 150.25 only. Another rally is still expected at a later stage through 160.02 to resume the larger up trend. However, decisive break of 150.87 will argue that larger correction is possibly underway, and target 146.47 support next.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 04:30 | AUD | RBA Interest Rate Decision | 4.35% | 4.35% | 4.35% | |

| 09:00 | EUR | Eurozone CPI Y/Y May F | 2.60% | 2.60% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y May F | 2.90% | 2.90% | ||

| 09:00 | EUR | Germany ZEW Economic Sentiment Jun | 50 | 47.1 | ||

| 09:00 | EUR | Germany ZEW Current Situation Jun | -69 | -72.3 | ||

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Jun | 47.2 | 47 | ||

| 12:30 | USD | Retail Sales M/M May | 0.30% | 0.00% | ||

| 12:30 | USD | Retail Sales ex Autos M/M May | 0.20% | 0.20% | ||

| 13:15 | USD | Industrial Production M/M May | 0.40% | 0.00% | ||

| 13:15 | USD | Capacity Utilization May | 78.60% | 78.40% | ||

| 14:00 | USD | Business Inventories Apr | 0.30% | -0.10% |