Sample Category Title

Yen Appreciation and Policy Normalisation are Still Some Way for Japan

A weak Yen is aiding the Bank of Japan's inflation objective for now by dislodging the deflationary mindset. But homegrown inflation needs further wage increases and investment.

The Bank of Japan (BoJ) raised rates at its March meeting. Since then, the Yen has held above USD/JPY150, a level traditionally regarded as a trigger for intervention. While there is evidence that the Ministry of Finance has intervened in recent months, its actions have come only as the spot rate threatened JPY160 and have also been limited in duration, leaving USD/JPY currently trading towards the top end of the recent range at JPY157.

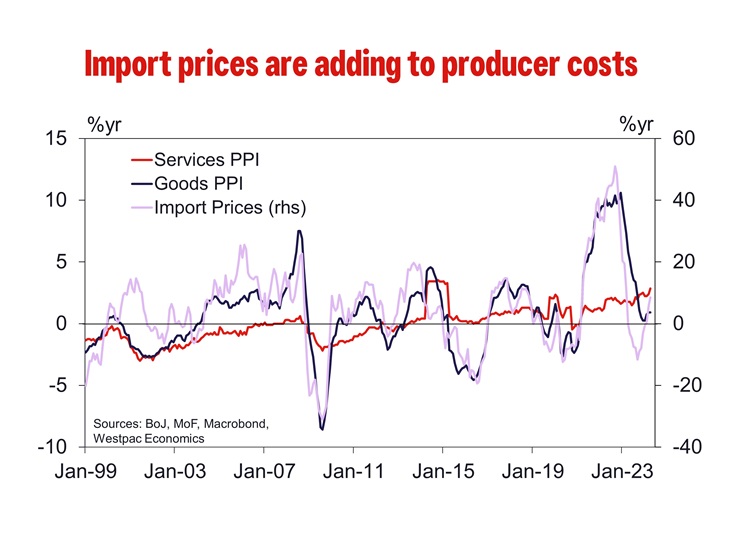

We take from this market activity that authorities are reticent to allow a further rapid depreciation in the Yen but are not overly concerned by sustained weakness in the currency. Arguably that is because a higher rate structure (and lower USD/JPY) can only be justified by the inflation target being sustainably achieved. The weak Yen fosters cost-push inflation, furthering the BoJ’s inflation objective in two important ways: 1) via the pass-through of input inflation to consumer prices; and 2) the reshaping of inflation expectations amongst businesses and households.

Historically, higher costs have prompted Japanese firms to cut costs by narrowing profit margins, bargaining with suppliers or reducing their wage bills. However, in this episode, the persistence of input price pressures, significant (largely co-incident) wage gains, and the global narrative around inflation have helped to dislodge the traditional mindset of Japanese firms. Normalising price increases is also proving to be the first step towards sustained real wage gains and businesses investing in future capacity, alleviating any lingering concerns amongst businesses that higher prices will sap demand.

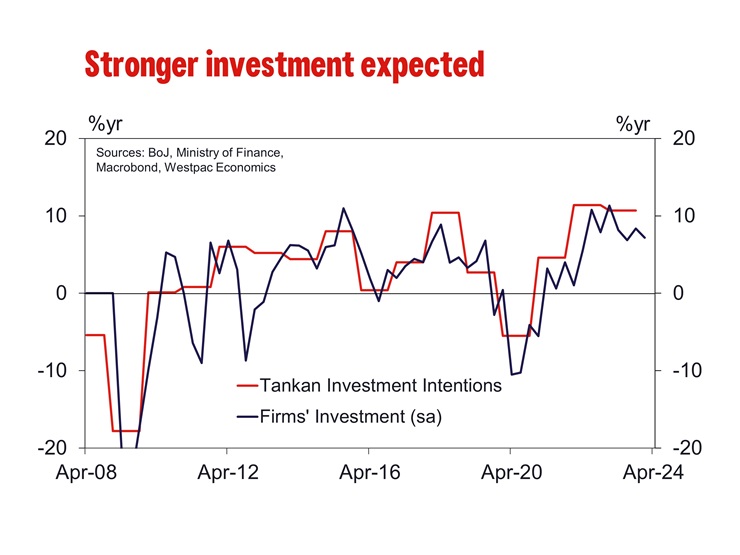

Innovation in particular has taken a considerable hit in recent decades amongst businesses focused on the domestic economy as firms perceived an unwillingness on the part of households to pay for new or improved goods and services. However, this may finally be taking a turn. Investment in plant and equipment grew rapidly through 2023, beating the peak set in 2007 and second only to the record set in Q4 1991. The Tankan’s surveyed investment intentions also peaked in Q3 2022 at the second highest level since 1989. Strong profits have certainly helped businesses invest, but so has the shifting inflation mindset. A survey conducted by the BoJ showed that participants in the corporate sector preferred moderate rises in prices and wages as it removed the ‘need for cost cuts to avoid raising prices enabling active fixed investment and wage hikes’.

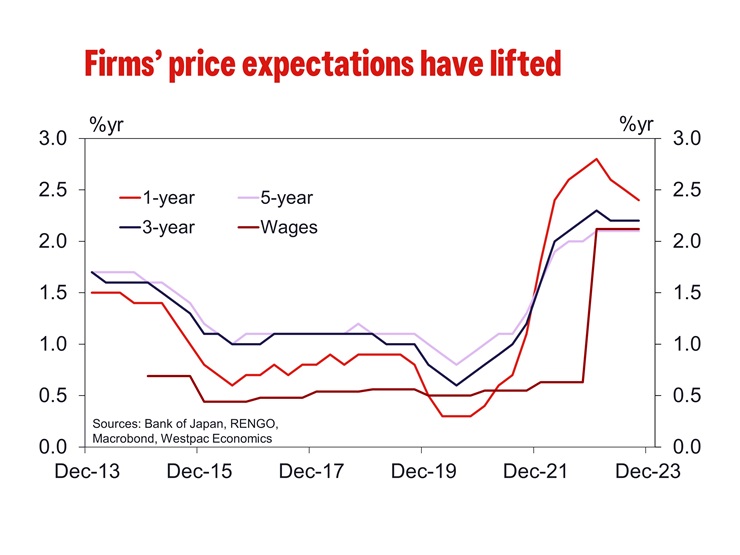

Inflation above target for a sustained period has also lifted inflation expectations. Japan’s inflation expectations are responsive to price shocks. This is supported by our analysis of historic shocks and financial market measures of inflation expectations. The BoJ also characterise price expectations as ‘adaptive rather than forward-looking’, evinced through history with inflation expectations settling close to 1% as headline inflation averaged 0.5% between 1990 and 2019.

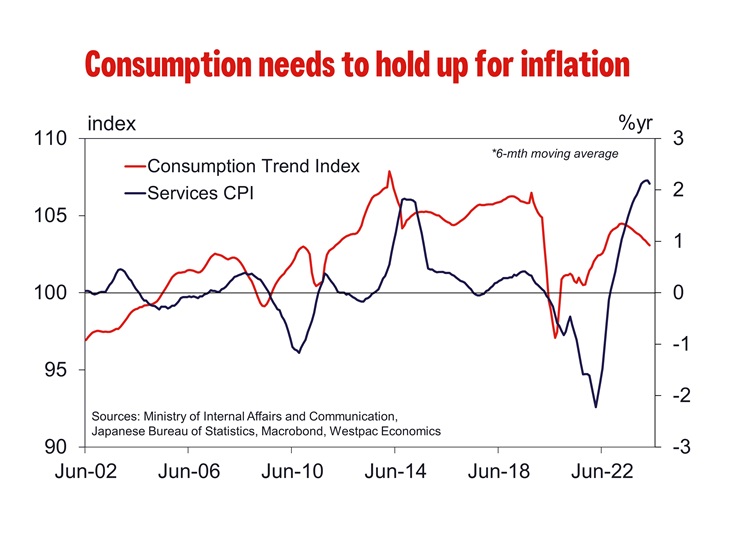

Recently, expectations have risen and settled around the 2% target according to both the outlook in general and output price expectations collected in the Tankan survey. High imported inflation from a weak Yen have clearly bought time for demand-pull inflation to build strength. For inflation to persist at target however, demand pressures must become dominant and sustainable, particularly with the Yen near the level authorities have recently intervened at, and with global rates now falling.

The demographic challenge in Japan means that savings will remain high, posing a risk to reestablishing a healthier demand-driven inflation. Whether there is a shift in consumption will be seen in the household spending data in the second half of 2024, when most wage increases will be received. While strong services inflation implies wages are already feeding through to inflation, assessment is difficult due to the surge in foreign tourist spending. A pick-up in household spending in late-2024 would signal that consumers are looking to make purchases sooner to avoid price increases – a deviation from the deflationary mindset of the past. Further robust increases in wages in the 2025 Shunto negotiations would provide additional support for consumer confidence and spending, and entrench a change in the consumer psychology around prices.

While this transition takes hold, it is also important that businesses focus on expansion and productivity over efficiency. In doing so, lasting weakness in the Yen can add to inflation as wages, consumption and investment continue to expand. Arguably, GDP growth sustainably at or above trend is a necessary prerequisite for households to feel as though the economy is fully employed and inflation at target is justified.

It is only after expectations are fully reset and inflation consistently at or above target that the BoJ will be justified in lifting the policy rate materially above the lower bound. This is not to say they will not edge policy rates higher in coming months, but to emphasise that policy will need to be restrained if its to avoid jeopardising the years (indeed decades) of progress that have been required to get to this point.

GBP/USD Dips as Bulls Take a Breather, Key Levels To Watch

Key Highlights

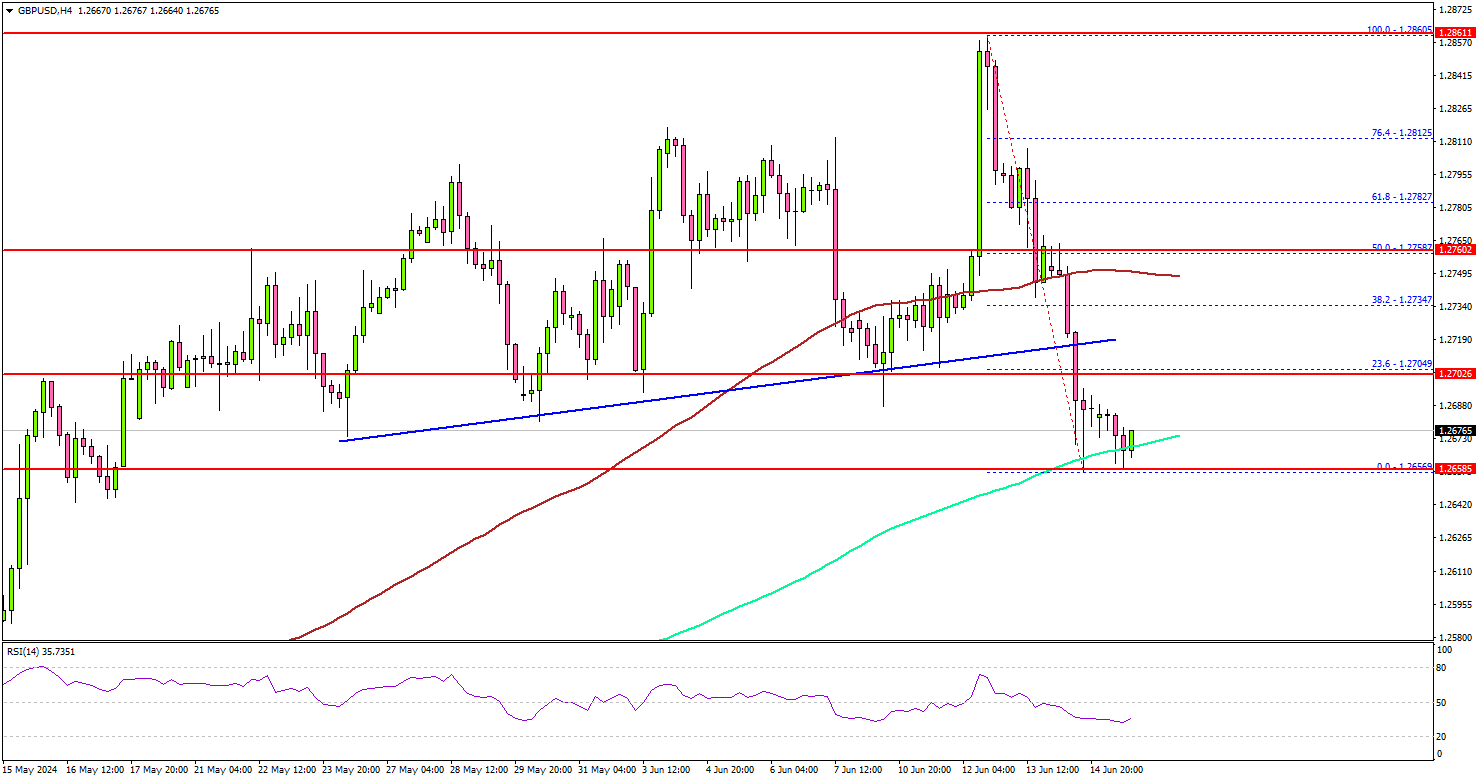

- GBP/USD started a downside correction from the 1.2860 resistance.

- It traded below a key bullish trend line with support at 1.2720 on the 4-hour chart.

- EUR/USD is eyeing a recovery wave from the 1.0665 support zone.

- Oil prices are moving higher toward the $80.80 resistance.

GBP/USD Technical Analysis

The British Pound peaked near 1.2860 and started a fresh decline against the US Dollar. GBP/USD traded below 1.2800 and 1.2740 support levels to enter a short-term bearish zone.

Looking at the 4-hour chart, the pair traded below a key bullish trend line with support at 1.2720. The bears were able to push the pair below the 100 simple moving average (red, 4-hour) and it tested the 200 simple moving average (green, 4-hour).

A low was formed at 1.2655 and the pair is now consolidating losses. If there is a fresh increase, the pair might face resistance near the 23.6% Fib retracement level of the downward move from the 1.2860 swing high to the 1.2655 low.

The first major resistance is near the 1.2740 level. A clear move above the 1.2740 resistance might send it toward the 1.2780 level. Any more gains might call for a move toward the 1.2860 level in the near term.

If not, the pair might dip again. Immediate support is near the 1.2655 level. The next major support is near the 1.2620 zone. A downside break and close below the 1.2620 support zone could open the doors for a larger decline. In the stated case, the pair could decline toward the 1.2550 level.

Looking at EUR/USD, the pair found support near the 1.0665 zone and it could now aim for a recovery wave in the near term.

Economic Releases

- US Retail Sales for May 2024 (MoM) – Forecast +0.2%, versus 0% previous.

- Fed's Logan speech.

Instrument of the Week (June 17—21): EURGBP Overview

The EURGBP pair, representing the exchange rate between the Euro and the British Pound, encapsulates the economic dynamics of the Eurozone and the United Kingdom. The Euro is influenced by economic growth, inflation, and the monetary policies of the European Central Bank, primarily driven by major economies like Germany and France. On the other hand, the British Pound is affected by the UK’s economic indicators, such as GDP growth, inflation, and decisions made by the Bank of England.

Eurozone Consumer Price Index (CPI) YoY, June 18, 11:00 (GMT+2)

The forecast for the Eurozone’s CPI suggests an increase of 2.6% from the previous 2.4%. If the actual CPI data exceeds this forecast, indicating higher-than-expected inflation, it might prompt the European Central Bank to consider tightening its monetary policy sooner than anticipated. This prospect would likely bolster the Euro, causing the EURGBP pair to rise. Conversely, should the CPI fall short of expectations, suggesting less inflationary pressure than anticipated, it could weaken the Euro as investors adjust their expectations for continued accommodative policy. In this case, the EURGBP rate could potentially decrease.

UK Consumer Price Index (CPI) YoY, June 19, 08:00 (GMT+2)

In the UK, the CPI is expected to decline to 1.9% from the previous rate of 2.3%. If the released data confirms the forecast and shows a decrease, it might reduce the urgency for the Bank of England to tighten monetary policy, leading to a weaker Pound. This weakening would likely cause an increase in the EURGBP rate. However, if the actual CPI data comes in higher than expected, suggesting persistent inflationary pressures, it could push the Bank of England towards a more aggressive monetary stance, thereby strengthening the Pound and likely causing a decrease in the EURGBP exchange rate.

In the daily timeframe, EURGBP, in a long-term bearish trend, has formed a descending channel pattern. The price fell to the lower trend line, and it is testing it. The moving averages show a clear bearish signal, but the RSI is at 30.0, which creates two possible scenarios:

- If EURGBP breaks the lower trend line and falls below 0.8430, the price will fall to 0.8300;

- A rebound from the trend line will open the way for a rise to the upper trend line of 0.8550.

Euro Steadies After Market Jitters Subside

The euro is steady on Monday. EUR/USD is trading at 1.0714 in the North American session, up 0.10% on the day.

French election triggers market turmoil

France’s financial markets took a tumble late last week, as investors are nervous about the snap parliamentary election at the end of June. There are fears that the extreme right could make strong gains, as was the case in the recent European Union parliamentary elections. The market turmoil led to a sell-off in France’s financial markets and the euro losing 1% over Thursday and Friday.

ECB Chief Economist Philip Lane sought to reassure nervous investors and said on Monday that the ECB would not intervene since the recent market turmoil was “not disorderly”. Lane also said the ECB was confident that inflation would fall to the 2% target in 2025.

Lane may have sounded optimistic, but the ECB was not happy with the June CPI release, which showed inflation accelerating in the preliminary estimate. Headline CPI rose from 2.4% in May to 2.6% in June and the core rate climbed to 2.9%, up from 2.7% in May. The final estimate, which will released on Tuesday, is expected to confirm the initial release. The markets expect one or two rate cuts before the end of the year, but higher inflation will complicate the ECB’s plans to lower interest rates.

In the US, the UoM consumer sentiment index fell for a third successive month to 65.6 in June. This was down from 69.1 in May and shy of the market estimate of 72. Inflation expectations remained unchanged at 3.3%, another signal that inflation remains sticky and the Fed will have a tough time bringing inflation down to the 2% target.

EUR/USD Technical

- EUR/USD is testing resistance at 1.0709. Above, there is resistance at 1.0743

- 1.0666 and 1.0628 are the next support levels.

Soft Retail sales Could Curb Fed Hawks’ Rhetoric

- Market ponders the Fed’s stance after a hawkish gathering

- Retail sales to reveal the strength of domestic demand

- Dollar on the front foot; could suffer if data weaken this week

- The May retail sales report will be released on Tuesday 12:30 GMT

At last week’s Fed meeting, consumer spending featured briefly in Chairman Powell’s press conference. The focus was firmly on the May inflation report and the Fed’s dot plot. Even though Powell tried to reduce the importance of the latter, the Fed members’ median expectation of one rate move in 2024 monopolized the market’s interest.

Fed hawks could become more aggressive this week

With the blackout period over, Fed speakers are expected to be on the wires on a daily basis and it will be interesting if the hawks adopt a more aggressive rhetoric. The market is currently assigning a 72% probability of a 25bps rate cut in September with two rate moves expected by year-end. However, the market’s favorite hawk, Minneapolis Fed President Kashkari, has already commented that “it’s reasonable that a rate cut could come in December”.

Data to determine the Fed’s action plan

However, as Chairman Powell highlighted at the press conference, the data will determine if the Fed cuts rates in September or postpones its decision for December. With the Atlanta Fed GDPNow growth estimate for the second quarter of 2024 rising to 3.1%, Fed doves have a mountain to climb in order to convince the rest of the Committee of the need for a rate cut at this juncture.

Retail sales data will be published report on Tuesday

The first piece of the puzzle following the June 12 Fed meeting comes on Tuesday when the May retail sales report will be published. Domestic demand remains the key difference between the USA and the remaining developed countries, and especially Japan where the BoJ is anxiously trying to boost domestic inflation.

The ongoing slowdown in inflation and the consistent increases in earnings have been supporting domestic demand, although a good part of consumer spending has been funded by credit card borrowing, which stood at $1,115 trillion in the first quarter of 2024 and is expected to continue climbing.

Headline retail sales are forecast to record a monthly 0.2% jump, with the retail sales indicator that excludes autos also expected to record a positive monthly print. Interestingly, the retail control group index, which focuses on retail and food stores, is seen rising by 0.4% and thus reversing April’s correction.

As made evident by these forecasts, the market is expecting positive figures, which are unlikely to be welcomed by the doves. However, there is a good possibility of a downside surprise when considering the latest prints from both the Consumer Confidence and the University of Michigan consumer sentiment indices.

Dollar holds most of its recent strong gains

The US dollar has been benefiting from both the heightened political risks in the euro area and the hawkish Fed meeting. As a result, the euro/dollar pair dropped aggressively to its lowest level since late April. With the Fed still pondering its next move, the dollar’s outlook remains somewhat positive even though the ECB is not expected to follow a normal monetary policy easing cycle.

Any indication of a slowdown in consumer spending could result in a gradual unwind of the dollar’s recent gains as the market is anxiously looking for weak economic data prints. A move towards the key 1.0769-1.0780 range could quickly really raise questions about the euro/dollar’s negative short-term outlook.

On the flip side, another strong report is unlikely to massively benefit the dollar with the focus being mostly on the likely US stock market's reaction. In this case, euro/dollar could try to test the 1.0635 level with profit taking potentially limiting the bearish move.

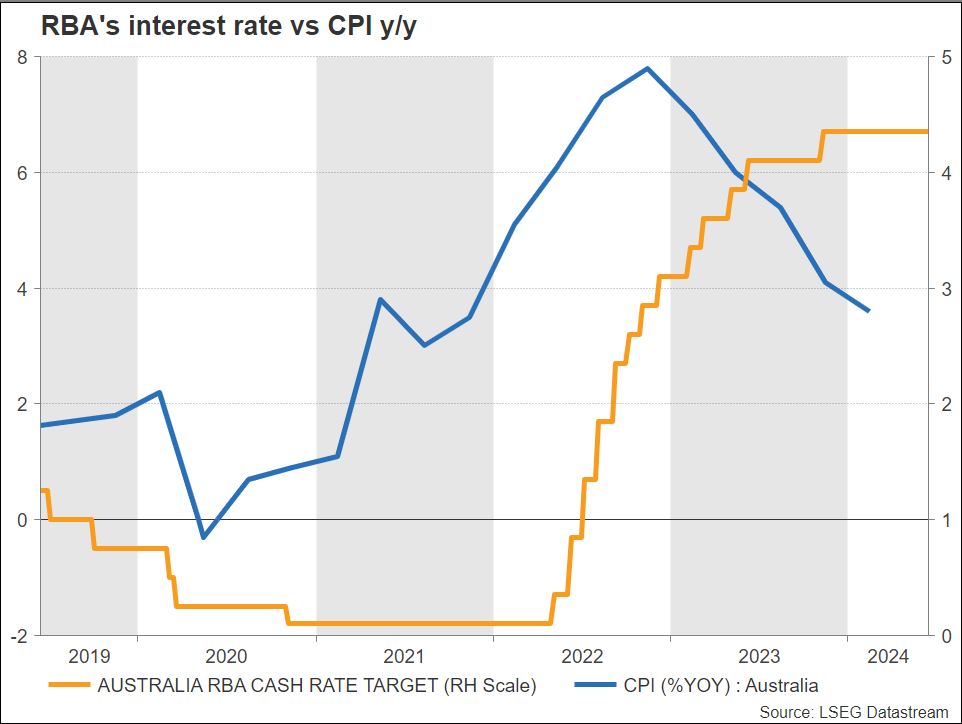

RBA Policy Meeting May Be Muted; Aussie Remains Choppy

- RBA interest rate expected to remain unchanged

- Sticky inflation and economy’s uncertainty still a concern

- Aussie holds in downward channel ahead of Tuesday’s decision at 04:30 GMT

Australia’s uncertain economy and sustained inflation

The Reserve Bank of Australia (RBA) is scheduled to announce its June policy decision early on Tuesday, likely maintaining the central bank's agenda. The policymakers had anticipated that their responsibilities would become significantly less challenging in the current year. However, persistent inflation and ongoing economic uncertainty have made policy decision-making quite challenging for RBA officials.

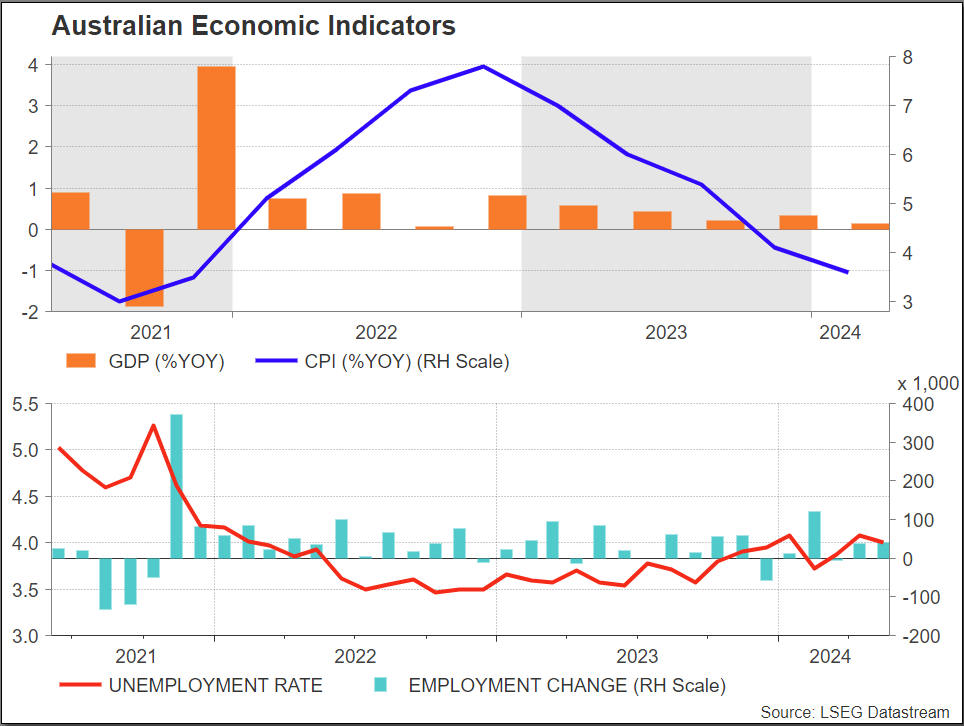

Australia experienced a year-on-year inflation rate of 3.6% in the first quarter of 2024, which was lower than the 4.1% recorded in the previous period but higher than the market's anticipated rate of 3.4%. The latest data shows that the figure reached its lowest point since the fourth quarter of 2021. This was due to a decrease in goods inflation for the sixth consecutive quarter and a slowdown in services inflation for the third consecutive quarter.

In the first quarter of 2024, the Australian economy grew by 0.1% compared to the previous quarter, which was lower than the revised 0.3% increase in the previous quarter and fell short of market expectations of 0.2%. Following a three-month high of 4.1% in April, the unemployment rate fell 4.0%, in line with market expectations.

June’s meeting expected to remain unchanged

During the May meeting, policymakers considered increasing interest rates. However, they finally determined that risks to the inflation predictions were evenly balanced. This month’s statement is anticipated to adopt a comparable stance, with the cash rate projected to remain unchanged at 4.35%.

Even though investors have priced out any possibility of a rate increase in recent weeks, the inflation path in Australia continues to be more concerning, as it is holding well above the 2-3% target, higher than that of other developed countries, and it may be too soon to rule out a rate increase. Despite this, it is highly improbable that there will be any changes to the policy until the meeting in August, when new economic estimates will be published.

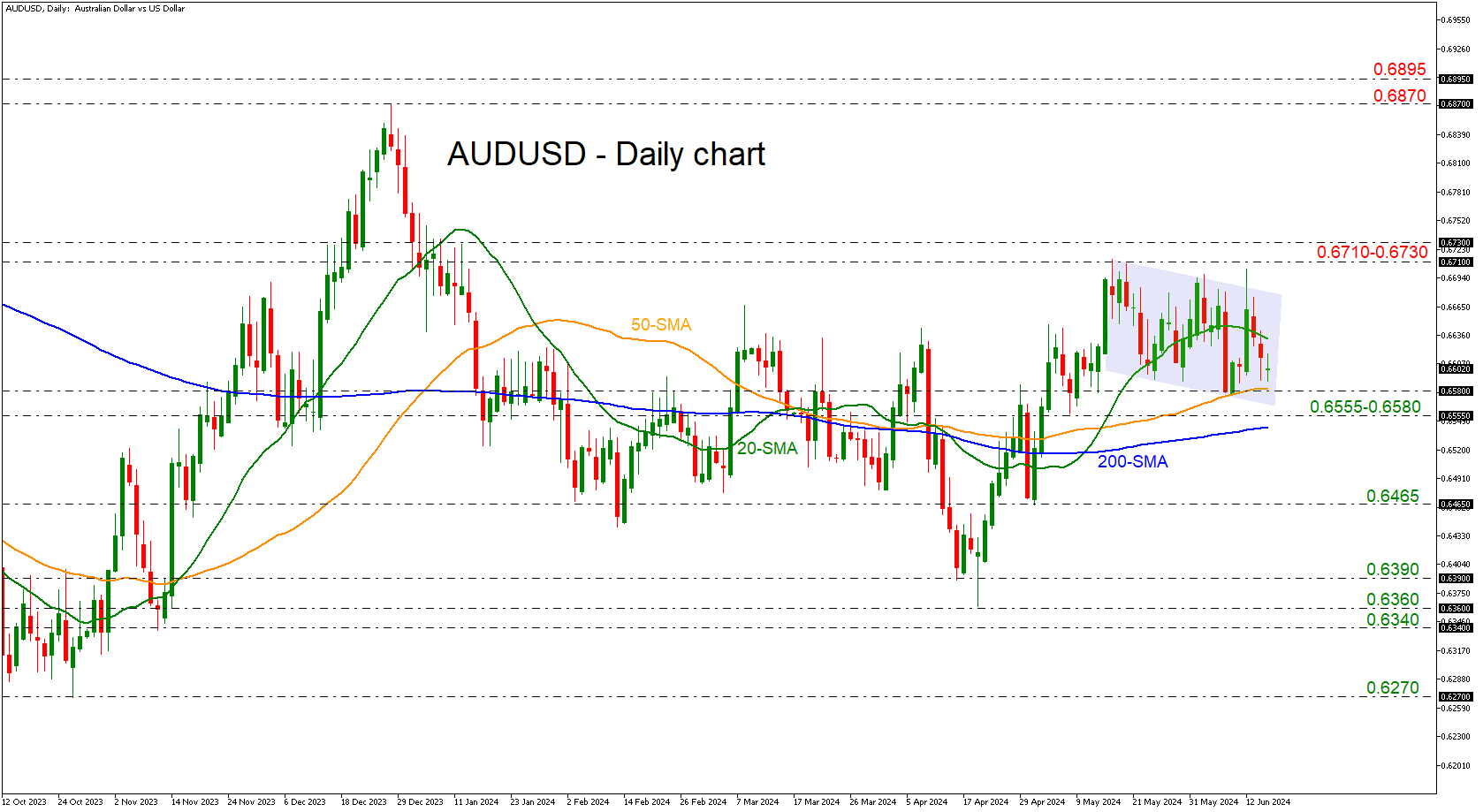

Technical look: AUDUSD

The aussie may not be affected much by RBA’s decision because of the lack of clarity on interest rates in the US as well. Currently, AUDUSD has been developing within a tight downward sloping channel since May 16 with strong support provided by the 50-day simple moving average (SMA) around 0.6580. A dive beneath this area could endorse the short-term bearish outlook, hitting the 0.6555 area, ahead of the 200-day simple moving average (SMA) at 0.6543. Alternatively, a successful climb above the 20-day SMA at 0.6630 could open the door for a retest of the upper boundary of the range at 0.6675. Above this line, the 0.6710-0.6730 restrictive regions would change the picture to a more positive one.

Sunset Market Commentary

Markets

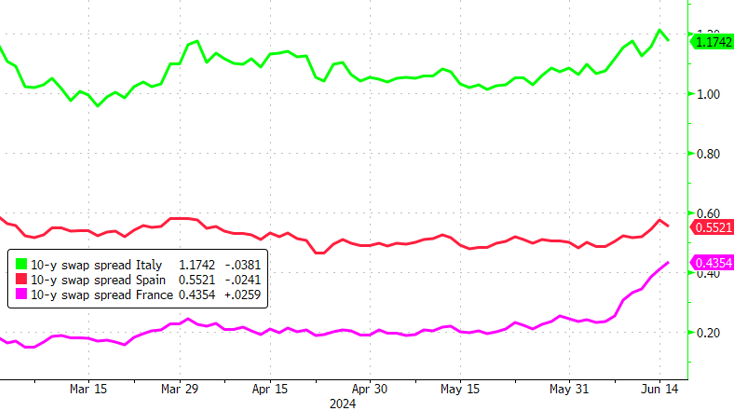

A sense of calm returned to European markets for now. Le Pen from the poll-leading Rassemblement National sought to reassure investors on the budgetary front if her party were to win the elections. It may have helped to stop the rout in European/French assets in a daily perspective after a disastrous week. Equities in the region stabilize and in some cases eke out a small gain (EuroStoxx50 +0.5%). Global core bond yields add a few basis points as safe haven bids ease for the time being. US rates rise between 4 (2-yr) and 7.8 (30-yr) bps. The move offer the likes of the 10-yr yield some wiggling room north of the lower bound of the short-term downward trend channel. German bunds tentatively underperform, adding 5.3 to 6.3 bps across the curve with the 10-yr yield trying to undo Friday’s break below the 2.4% support level (38.2% retracement on the 2024 rally, mid-May correction low). 10-yr spreads vs swaps creep a few bps higher in the case of Germany but decline for the likes of Italy, Spain and Portugal. France’s is up but is biased due to a benchmark change. It’s worth noting that several ECB members are not (yet, at least) concerned with the European repricing. Both chief economist Lane and de Guindos said it happened orderly and with sufficient liquidity, suggesting the Transmission Protection Instrument won’t be deployed any time soon. The former also touched on monetary policy but did not want to speculate on rate cuts even though he labeled every meeting as a live one. Either way, the current phase is about remaining restrictive. The euro struggled in Asian dealings but for now manages to hold north of EUR/USD 1.07. It does eke out a nice gain against sterling in the wake of the pound’s failed test of the EUR/GBP 0.84 support zone. The pair is currently changing hands in the 0.846 region. In a final sign of markets starting the week with a less grim mood, EUR/CHF recovers some of the lost ground (0.956, up from 0.952 at Friday’s close).

News & Views

Both the Swiss Federal State department for Economic Affairs (SECO) and the KoF Economic Institute updated forecasts for the Swiss economy. SECO slightly upwardly revised economic growth for this year to 1.2% (from 1.1% in March), leaving growth still at a below-average pace. SECO sees a difficult environment for investments this year. Exports will offer some degree of support, but growth should mainly be driven by private consumption, buoyed by a further rise in employment and a fairly stable rate of inflation. The latter is expected to average 1.4% this year (vs 1.5% in March). For next year SECO expects growth (1.7%) to return closer the historical average also supported by better exports and investments. Inflation is expected to cool further to 1.1%. Growth expectations from the KoF Institute are close to SECO (2024 1.2%, 2025, 1.8%). The Institute is slightly more optimistic on disinflation (1.3% this year and 1.0% next year). In this context, KoF expects the SNB to cut rates by other 25 bps this week with an additional step to 1.25% in March next year. This week’s SNB decision might be affected/complicated by recent swings the Swiss franc. End May, Governor Jordan warned that a weaker franc at that time could be a risk for the inflation outlook. However, after Jordan’s comment and due to the European risk-off last week, the franc again trades about 4.0% stronger against the euro compared to end May, raising the chance of a SNB rate cut Thursday.

Polish core inflation decelerated further in May, the national bank reported. CPI excluding food and energy prices slowed to 0.1% M/M and 3.8% Y/Y (from 0.7% M/M and 4.1% ) in April. A similar trend was also visible for the series excluding administered prices (0.1% M/M and 2.4% Y/Y from 1.2% M/M and 2.3%) and the series excluding most volatile prices (0.3% M/M and 3.1%). The data confirmed the trend in the release of headline May inflation published by the Statistical office end last month (0.1% M/M and 2.5% Y/Y). Despite current softening in the inflation dynamics, most NBP members including Governor Glapinski see no room to cut rates this year as they see inflation rising back above 5.0% in H2 2024 due to a phasing out of price caps by the government and as high real wage growth might support demand and prices. The zloty rebounded from EUR/PLN 4.38 to 4.357 today, but this was mainly driven by a softening in E(M)U related risk sentiment that weighed on the currency last week.

Graphs

German 10-yr yield seeks to recover lost support at 2.4% as calm returns at the start of the week

Peripheral swapspreads decline a few bps in a sign of market stress easing slightly

EUR/PLN: Polish zloty catches a breather after European risk off pushed the currency (and other regional peers) lower

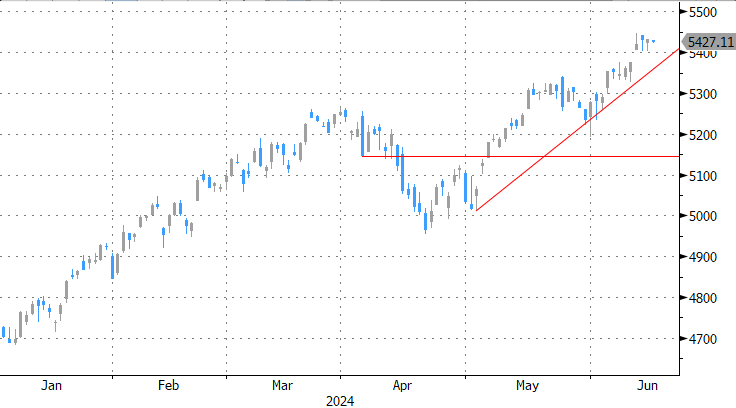

S&P500 - unfazed by European risk-off last week - opens near record highs as markets look for direction

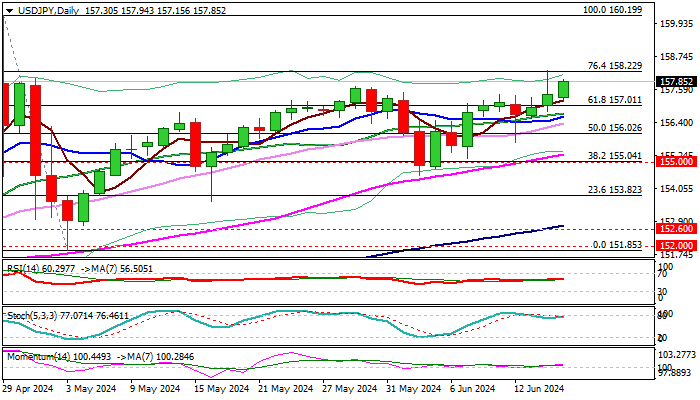

USD/JPY: Bulls Hold Grip for Retest of Pivotal Fibo Barrier

USDJPY firmed further on Monday and partially offset warning from long upper shadow of Friday’s daily candle, as fresh strength looks for retest of pivotal Fibo resistance at 158.22 (76.4% of 160.19/151.85) which capped Friday’s rally.

Firm break here to open way towards targets at 160.00/19 (psychological/2024 high, posted on Apr 29).

Technical picture on daily chart is bullish, although with warning of increased headwinds expected at 158.22 Fibo barrier, as stochastic continues to fluctuate around the borderline of overbought territory.

Near-term bias to stay with bulls while the action stays above 157.00 (broken Fibo 61.8% level.

Res: 158.22; 158.43; 159.00; 160.00.

Sup: 157.16; 157.00; 156.63; 156.00.

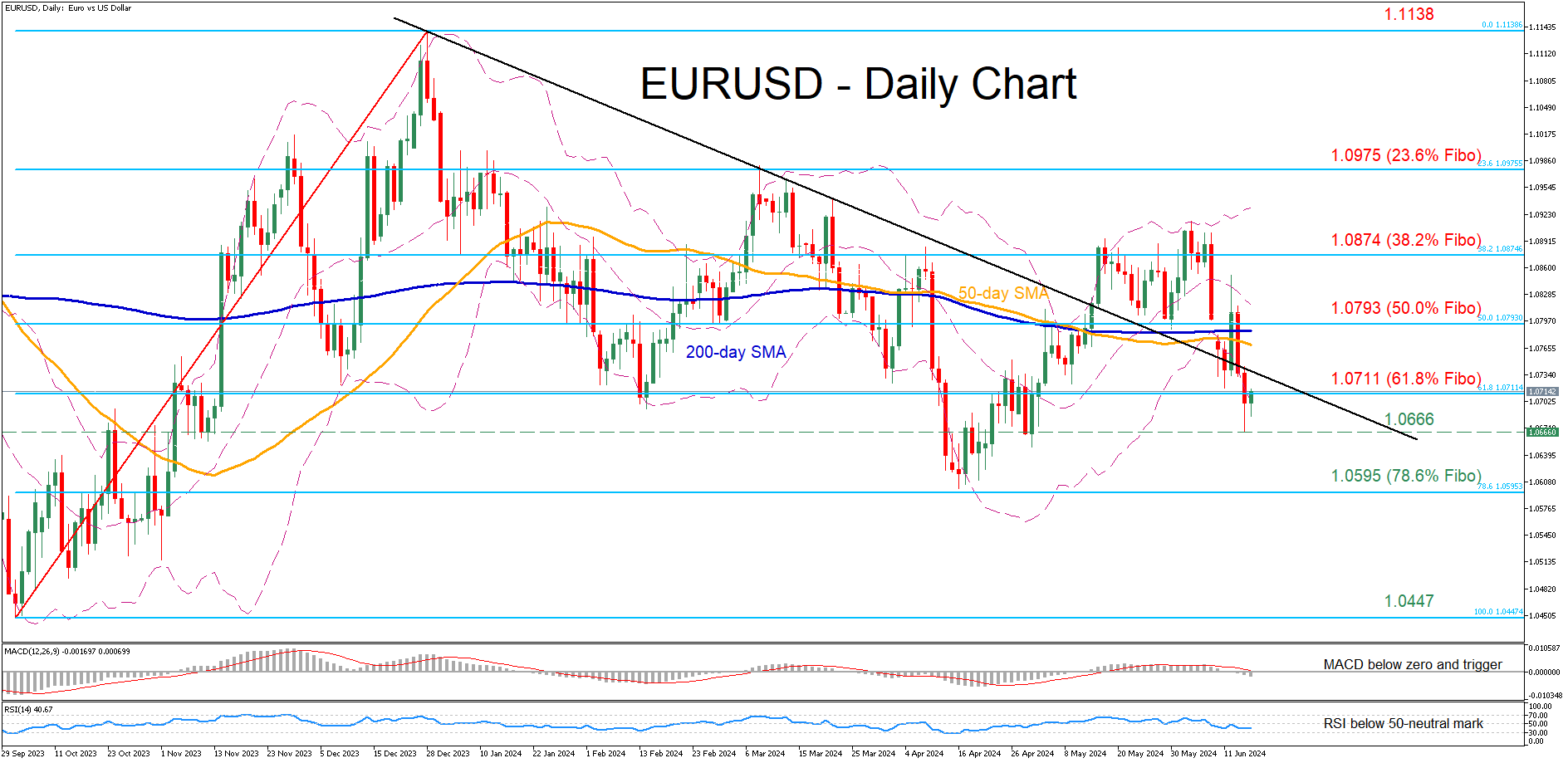

EURUSD Battles With 61.8% Fibo

- EURUSD drops to a fresh 1-month low after violating SMAs

- Quickly recoups some losses and challenges 61.8% Fibo

- Oscillators suggest that bearish forces are strengthening

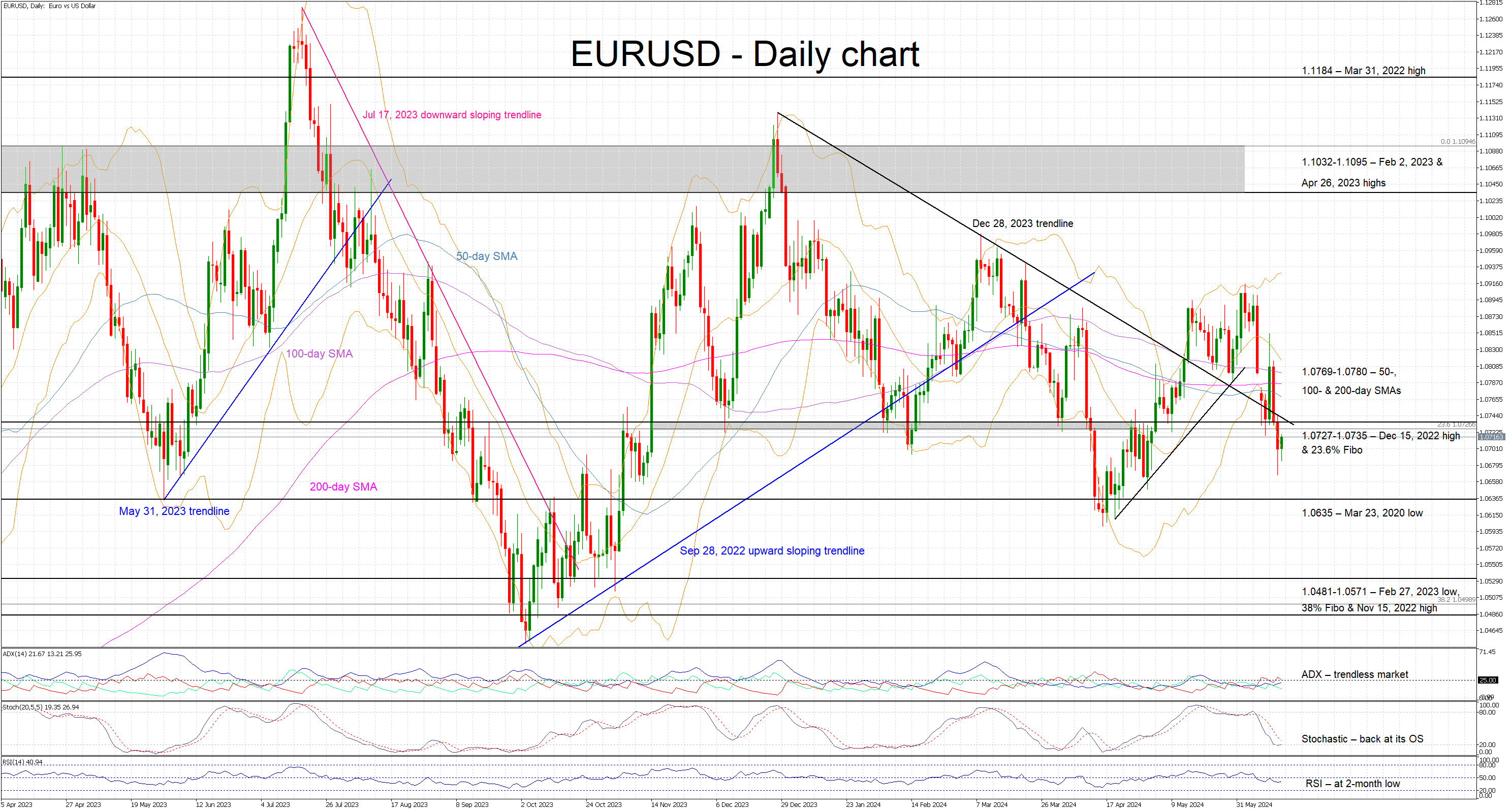

EURUSD has undergone some volatile sessions in the past few days, eventually dipping beneath both its 50- and 200-day simple moving averages (SMAs), to a fresh one-month low. Also, the pair broke below its descending trendline in place since December further deteriorating the technical outlook

Should the recent weakness persist, the price could challenge its one-month bottom of 1.0666. A break below that zone could pave the way for 1.0595, which is the 78.6% Fibonacci retracement of the 1.0447-1.1138 upleg. Failing to halt there, the pair could descend towards the October 2023 low of 1.0447.

Alternatively, if the price manages to surpass the 61.8% Fibo of 1.0711, initial resistance could be found at the 50.0% Fibo of 1.0793. Higher, the bulls could attack the 38.2% Fibo of 1.0874. Should that barricade also fail, attention could shift to the 23.6% Fibo of 1.0975, a region that curbed the pair’s advance in March.

In brief, EURUSD has come under some selling pressure lately, which led to a fresh one-month bottom. Moving forward, a failure to jump back above the restrictive medium-term trendline could increase the bears’ appetite for more downside.