Sample Category Title

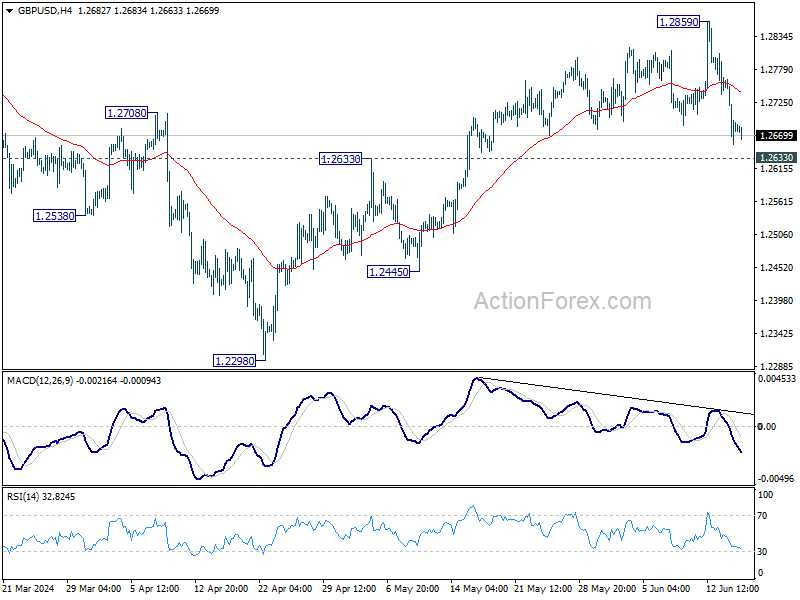

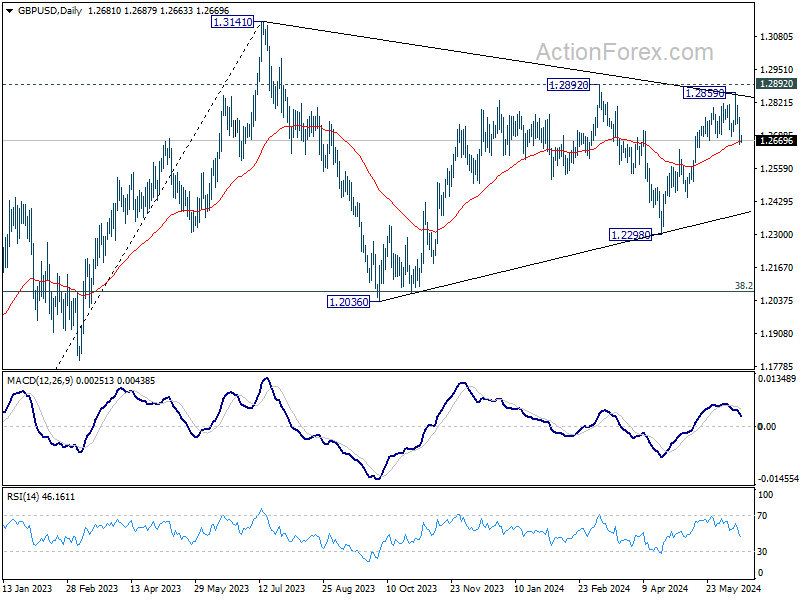

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2640; (P) 1.2702; (R1) 1.2748; More...

Intraday bias in GBP/USD remains mildly on the downside. Fall from 1.2859 short term top would target 1.2633 resistance turned support first. Firm break there will argue that whole rise from 1.2298 has completed, and target 1.2445 and below. For now, risk will be on the downside as long as 1.2859 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2445 support will extend the corrective pattern with another decline instead.

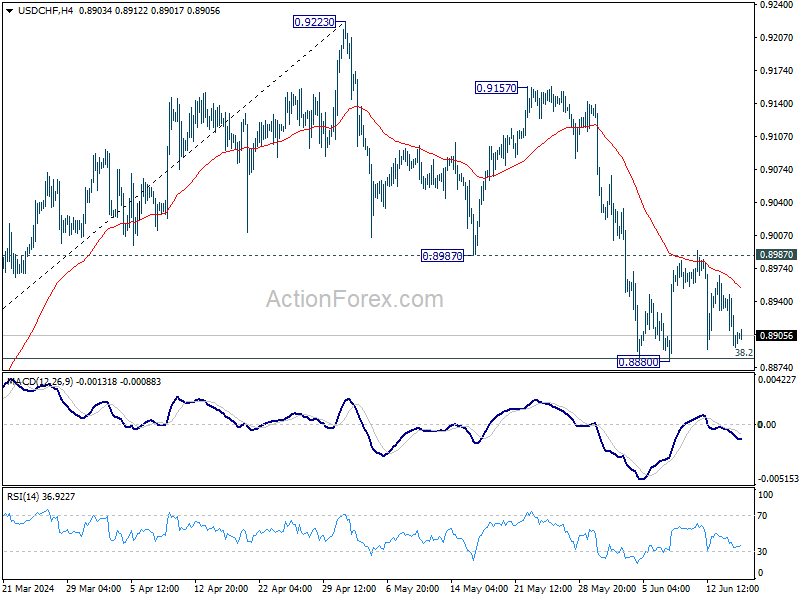

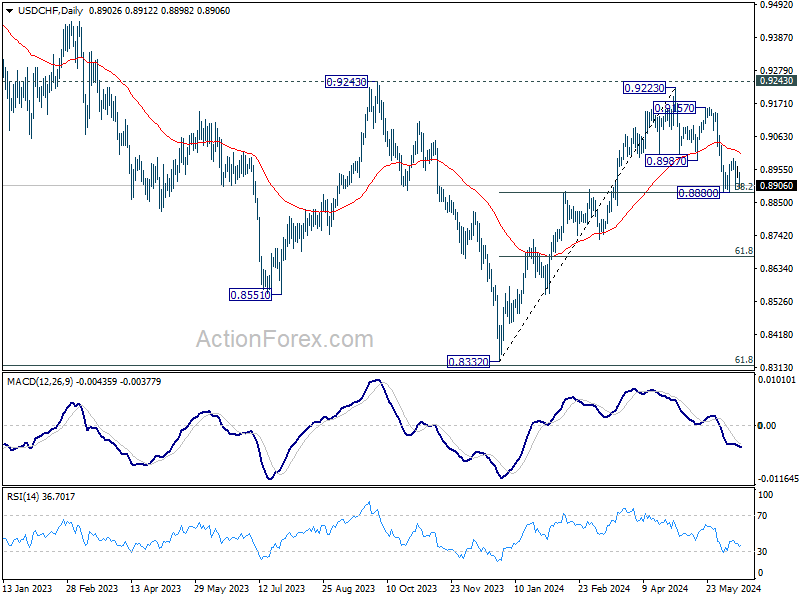

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8876; (P) 0.8921; (R1) 0.8946; More….

Intraday bias in USD/CHF remains neutral as range trading continues. On the downside, sustained break of 0.8883 fibonacci level will carry larger bearish implications and bring deeper decline. On the upside, firm break of 0.8987 support turned resistance will argue that correction from 0.9223 has completed, after drawing support from 0.8883 fibonacci level. Intraday bias will be back on the upside for 0.9157/9223 resistance zone.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

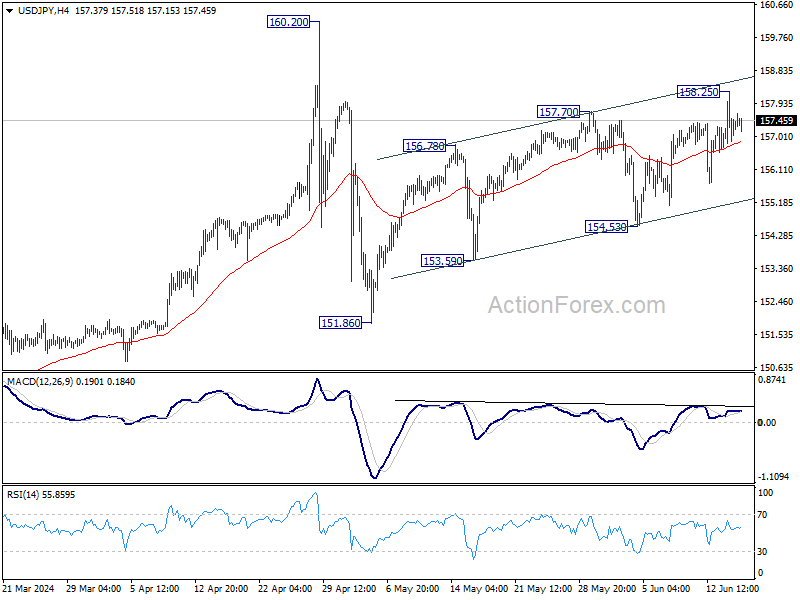

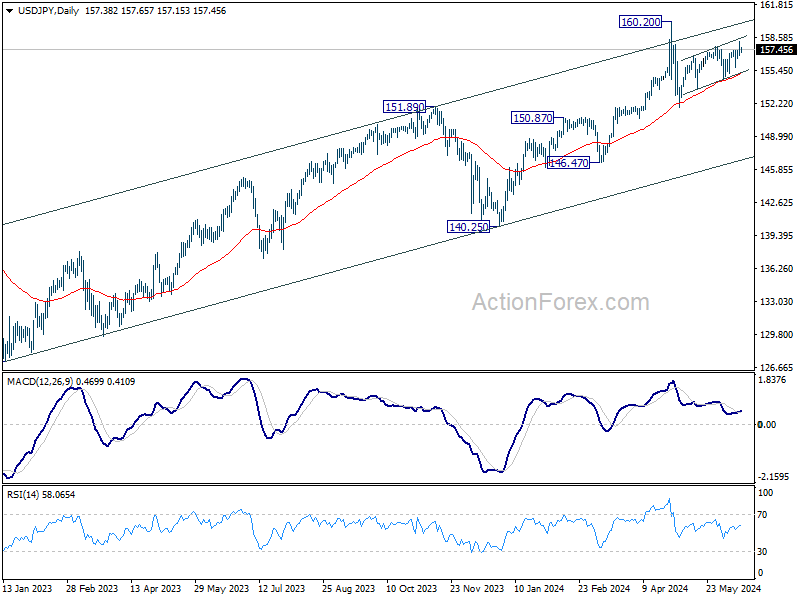

USD/JPY Daily Outlook

Daily Pivots: (S1) 156.73; (P) 157.50; (R1) 158.23; More...

Intraday bias in USD/JPY is turned neutral first with current retreat. Further rally would remain in favor as long as 154.53 support holds. Break of 158.25 will resume the choppy rise from 151.86 towards 160.20 high. But upside should be limited there, at least on first attempt.

In the bigger picture, price actions from 160.20 medium term top are seen as a corrective pattern to rise from 150.25 only. Another rally is still expected at a later stage through 160.02 to resume the larger up trend. However, decisive break of 150.87 will argue that larger correction is possibly underway, and target 146.47 support next.

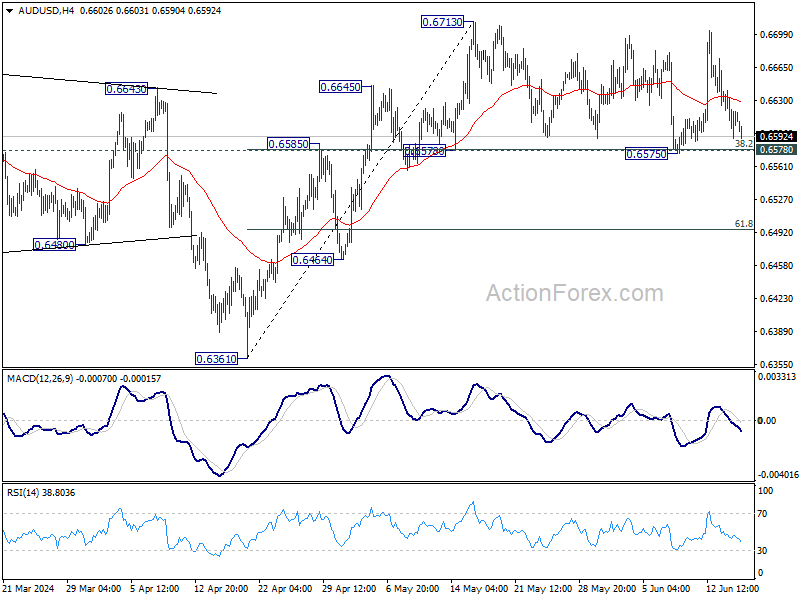

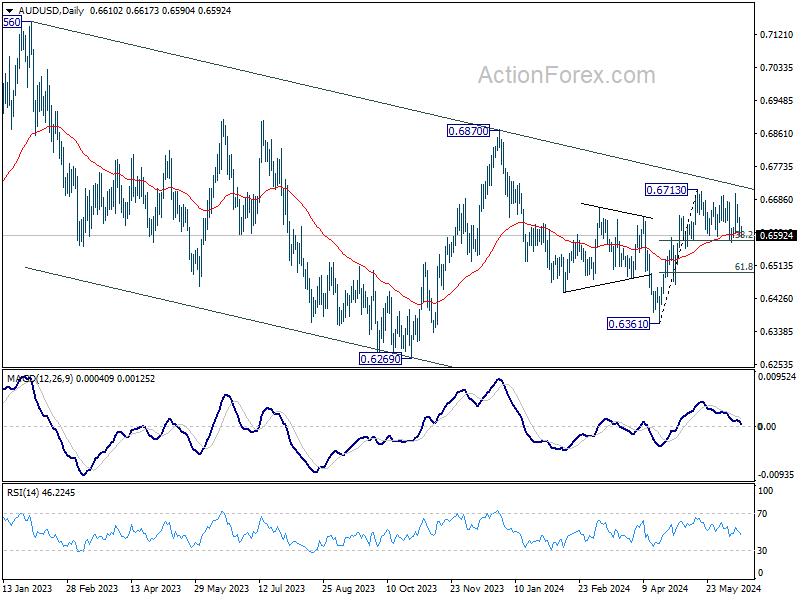

AUD/USD Daily Report

Daily Pivots: (S1) 0.6590; (P) 0.6617; (R1) 0.6643; More...

Intraday bias in AUD/USD remains neutral as range trading continues. Further rally is in favor with 0.6578 cluster support (38.2% retracement of 0.6361 to 0.6713 at 0.6579) intact. On the upside, firm break of 0.6713 will resume whole rise from 0.6361 to 0.6870 resistance next. However, sustained break of 0.6578 will dampen this bullish view, and bring deeper fall to 61.8% retracement at 0.6495.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could have completed at 0.6269 already. Rise from there is seen as the third leg which is now trying to resume through 0.6870 resistance.

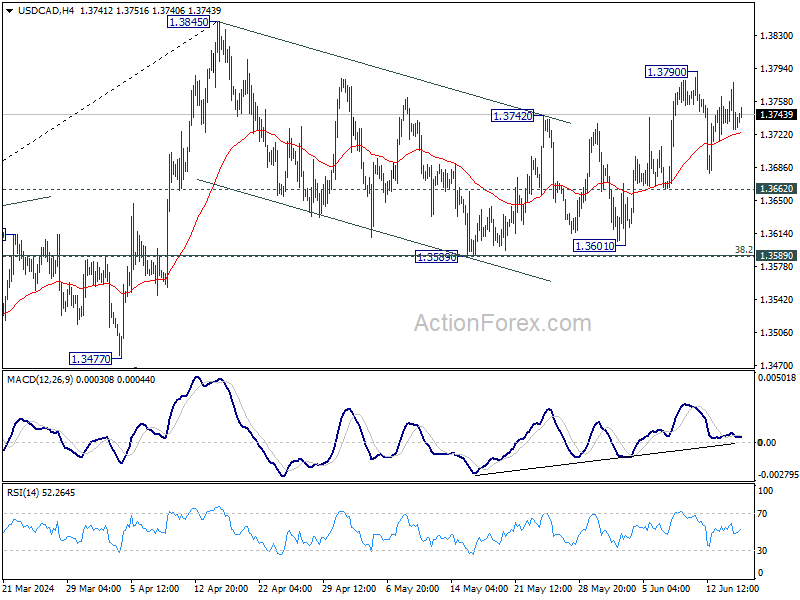

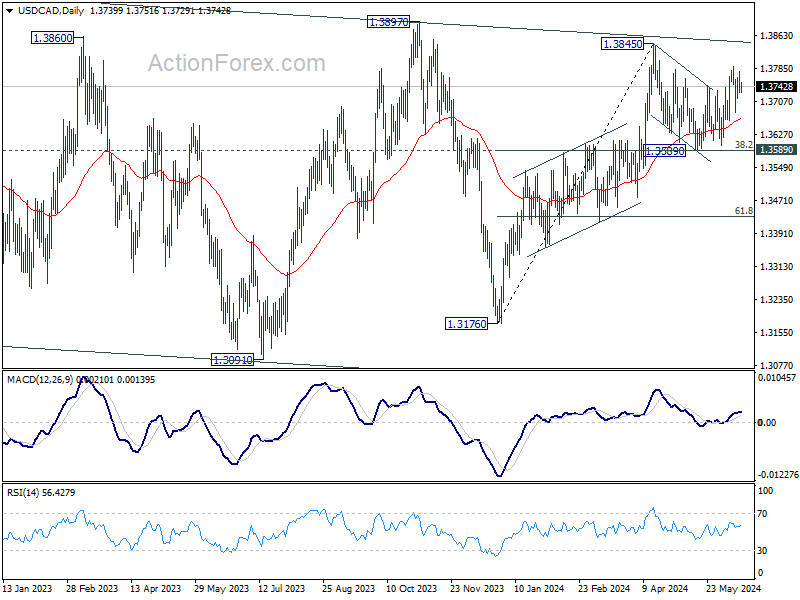

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3713; (P) 1.3747; (R1) 1.3766; More...

Range trading continues in USD/CAD and intraday bias stays neutral. Corrective fall from 1.3845 should have completed already. Further rally is expected as long as 1.3662 support holds. Break of 1.3790 will target a retest on 1.3845 first. Nevertheless, break of 1.3662 will turn bias to the downside to extend the corrective pattern from 1.3845 with another falling leg.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

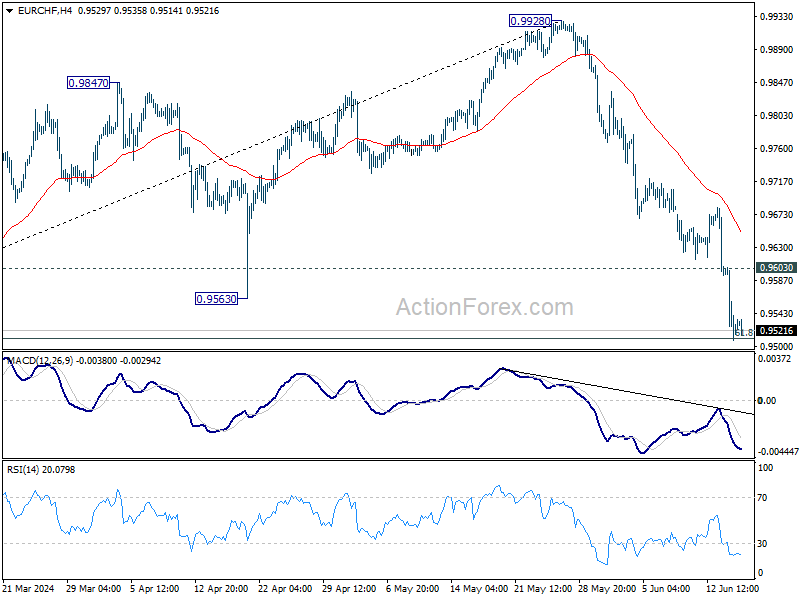

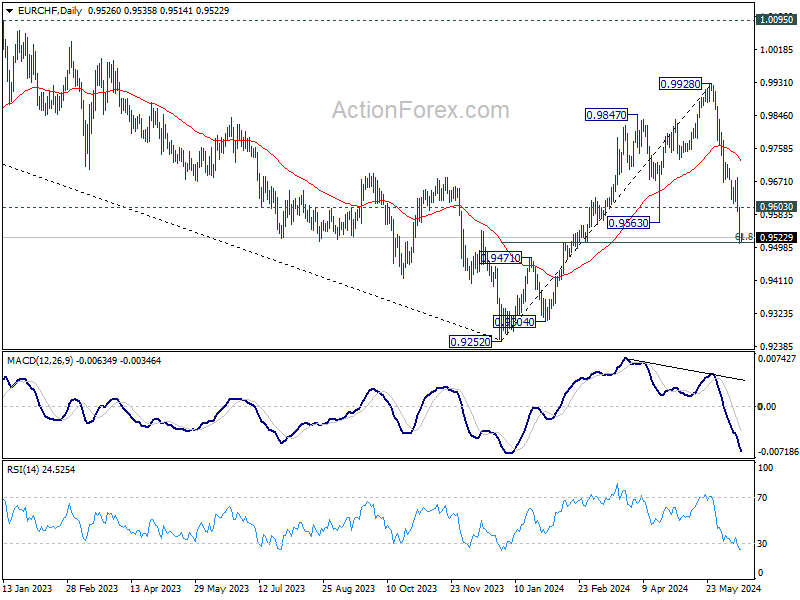

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9482; (P) 0.9555; (R1) 0.9599; More....

Intraday bias in EUR/CHF remains on the downside for the moment. Sustained trading below 61.8% retracement of 0.9252 to 0.9928 at 0.9510 will raise the chance of long term down trend resumption, and target 0.9252 low next. On the upside, above 0.9604 minor resistance will turn intraday bias neutral and bring consolidations first, before staging another fall.

In the bigger picture, the break of 0.9563 support, as well as 55 W EMA (now at 0.9672) argues that rebound from 0.9252 has completed at 0.9928. Medium term bearish is maintained with both 1.0095 resistance intact. Firm break of 0.9252 will resume the down trend from 1.2004 (2018 high).

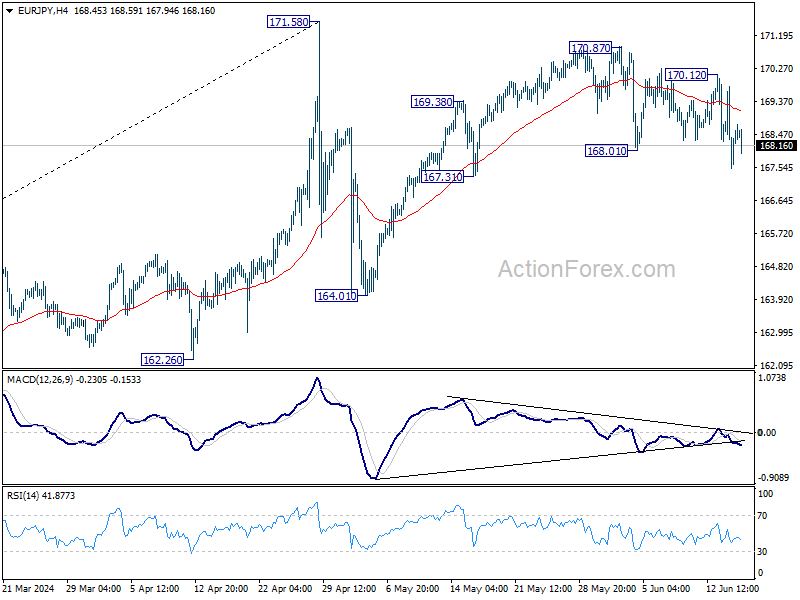

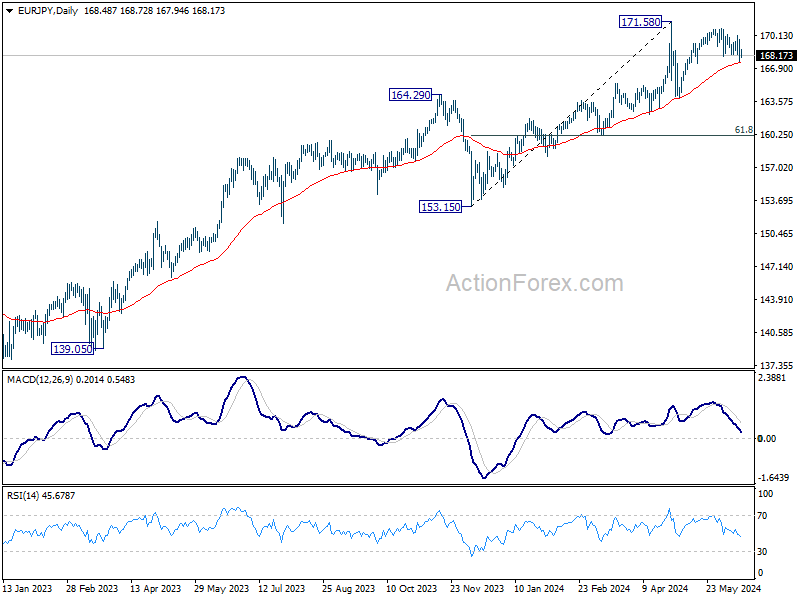

EUR/JPY Daily Outlook

Daily Pivots: (S1) 167.42; (P) 168.61; (R1) 169.69; More...

Intraday bias in EUR/JPY remains mildly on the downside for the moment. Sustained trading below 55 D EMA (now at 167.43) will extend the fall from 170.87, as the third leg of the pattern from 151.58, to 164.01 support next. For now, risk will stay on the downside as long as 170.12 resistance holds, in case of recovery.

In the bigger picture, as long as 55 W EMA (now at 159.51) holds, price actions from 171.58 medium term top are seen as as correcting the rise from 153.15 only. That is, larger up trend remains in favor to continue as a later stage. However, sustained break of 55 W EMA will argue that larger scale correction is underway and target 153.15 support.

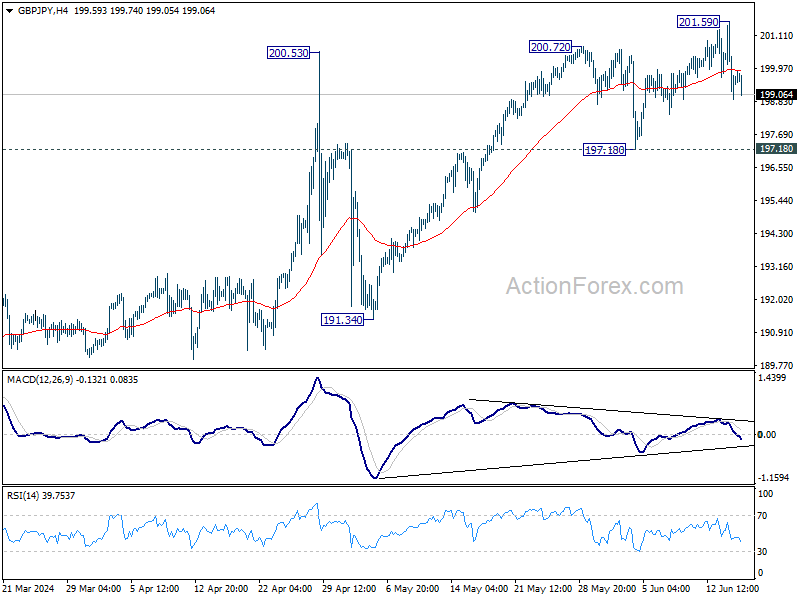

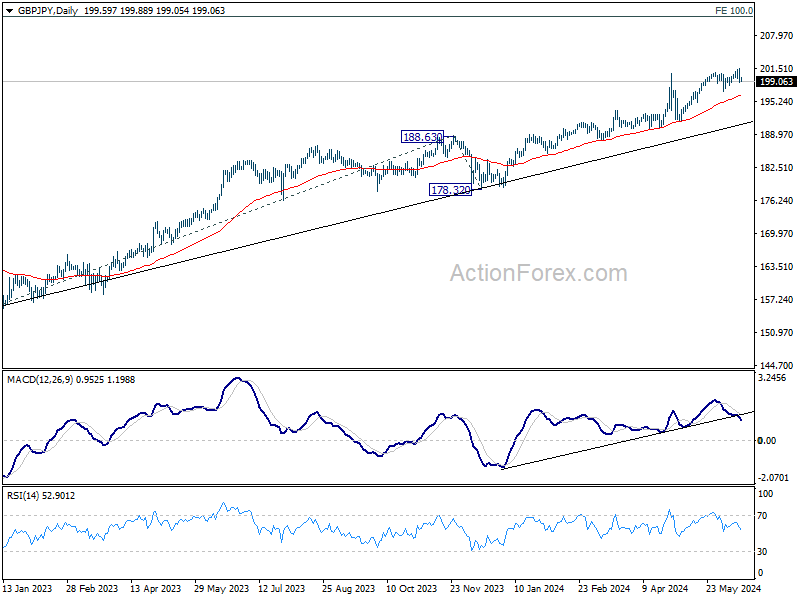

GBP/JPY Daily Outlook

Daily Pivots: (S1) 198.57; (P) 200.09; (R1) 201.27; More...

Intraday bias in GBP/JPY remains neutral for the moment, and some consolidations could be seen below 201.59. Further rally is expected as long as 197.18 support holds. However, considering bearish divergence condition in 4H MACD, firm break of 197.18 will confirm short term topping, and turn bias back to the downside for 191.34 support instead.

In the bigger picture, as long as 188.63 resistance turned support holds, long term up trend is expected to continue. Next target is 100% projection of 155.33 to 188.63 from 178.32 at 211.62.

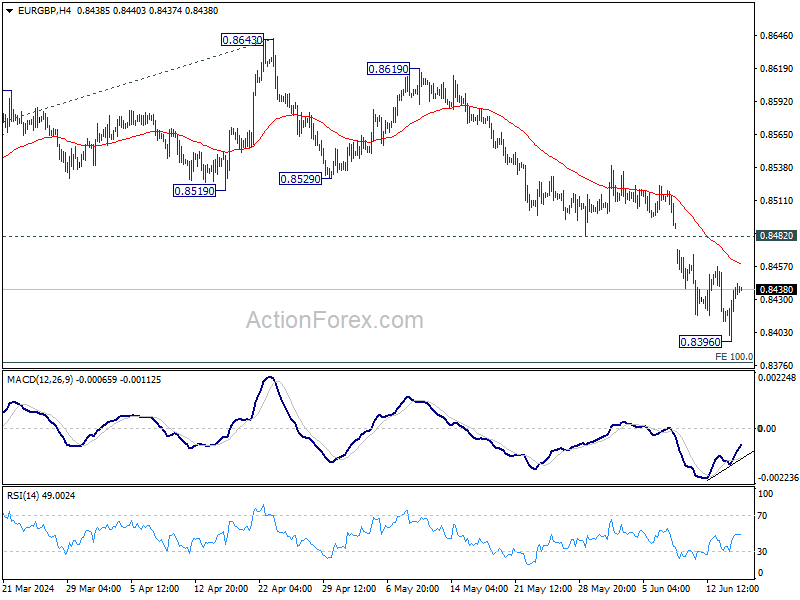

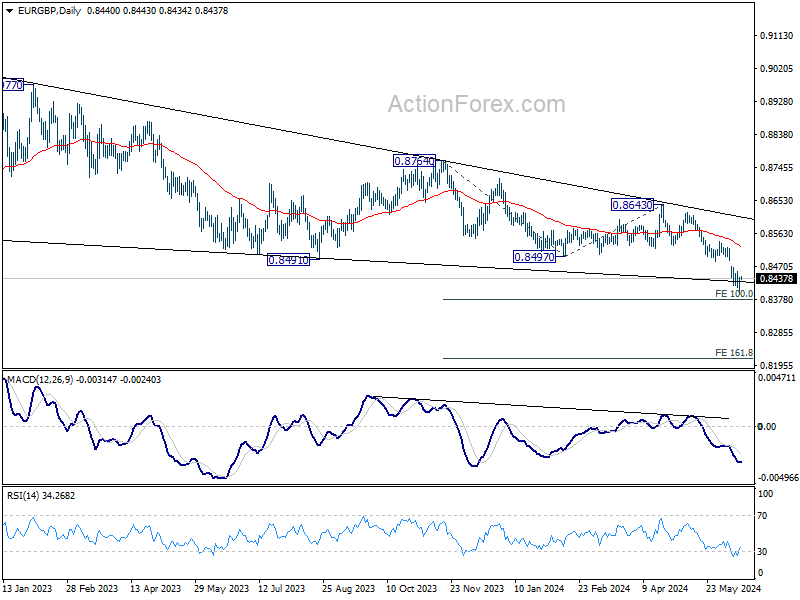

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8408; (P) 0.8425; (R1) 0.8452; More...

Intraday bias in EUR/GBP remains neutral and some more consolidations could be seen above 0.8396 temporary low. But outlook will remain bearish as long as 0.8482 support turned resistance holds. Below 0.8396 will resume larger down trend to 0.8376 projection level next.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 100% projection of 0.8764 to 0.8497 from 0.8643 at 0.8376. Sustained break there will target 161.8% projection at 0.8211 next. For now, outlook will remain bearish as long as 0.8643 resistance holds, even in case of stronger rebound.

Weekend Digest and a Quiet Start to the Week

In focus today

It will be a quiet start to the week on the data front. From Sweden, we get the Riksbank's Business Survey. Overnight, the Reserve Bank of Australia (RBA) is widely expected to leave monetary policy unchanged. Markets price in the first rate cut only for May 2025.

French politics will continue to be in focus this week. On Tuesday 18 June at 10:00 CEST we will host a webinar on the French election and the impact on markets (in Danish).

On Thursday, Norges Bank, the BoE, and the SNB will announce their monetary policy decisions. We expect all three central banks to keep rates unchanged, at 4.50%, 5.25%, and 1.50%, respectively. On Friday, we watch for June PMIs from the euro area and the US.

Economic and market news

What happened over the weekend

In France, on Friday markets were left spooked by the prospects of an uncertain French election outcome. A poll showing support for both the left- and right-wing coalitions was interpreted as continued uncertainty about French public finances, since both sides have large unfunded spending plans. This sent yield spreads lower with the DE10Y-FR10Y down 10bps. Then, over the weekend cracks started to appear in the left wing "Popular Front" alliance as far-left party leader Mélenchon removed critics and opponents of the alliance from his party's list of candidates. This resulted in members of other parties in the alliance questioning whether they could work with Mélenchon due to his "undemocratic" methods. However, on Sunday Mélenchon regained some of the coherence of the left-wing alliance by saying he would not insist on running as candidate for the prime minister of the alliance - which has previously been a key dividing factor in the alliance.

In geopolitics, the overall message from the G7 meeting in Italy, which ended Saturday, was a continued tough-on-Russia stance. Leaders agreed to a USD 50bn loan for Ukraine set to arrive towards the end of the year, while threatening further sanctions on Chinese entities that are supporting the war effort.

In China, the PBOC kept its one-year MLF loan rate unchanged at 2.50%, as widely expected. May industrial output came in slightly lower than expected at +6.0% y/y (cons.: 5.6%), while retail sales surprised to the upside at 3.7% y/y (cons.: 3.0%). The market reaction was mostly muted, though Chinese blue-ship stocks edged slightly higher.

What happened on Friday

Swedish inflation came in higher than expected as the CPI increased 0.2% m/m (cons.: -0.1%) in May. The main contributors were volatile food and flight prices, while service inflation had a setback. Overall, we see the factors contributing to this month's increase as temporary and maintain our Riksbank call with the next cut in September, followed by a 25bp cut every quarter bringing the policy rate to 2.25% at the end of 2025.

US consumers were much gloomier than expected as the flash University of Michigan consumer sentiment survey printed at 65.6 (cons.: 72.0). The market reaction was muted, however.

Market movements

Equities: Global equities ended lower on Friday, capping off a week dominated by political chaos in France and a US disinflationary environment that bolstered faith in Federal Reserve cuts, despite a slightly hawkish Summary of Economic Projections (SEP). Given the US's dominating size, equities still finished higher last week, driven by cyclical outperformance. In essence, US tech was the only game in town, while Europe and financial sectors significantly underperformed. Last week alone, tech outshone financials by a remarkable 8%. In the US on Friday, the Dow was down by 0.2%, S&P 500 decreased by 0.04%, Nasdaq increased by 0.1%, and Russell 2000 fell by 1.6%. Asian markets are trending lower this morning together with US futures. European futures are on the rise.

FI: It has been a very volatile week after the EU parliamentary elections and President Macron calling for a snap election for the French parliament after his party suffered a significant election loss and the nationalist party lead by Marine Le Pen won the EU parliamentary election. The 10Y spread between France and Germany widened almost 30bp during last week to reaching 80bp. This is similar to the level we saw ahead of the presidential election in 2016-2017, when Marine Le Pen argued for a"“Frexi"”. However, Le Pen stated during the weekend that she does not want to create a chaotic situation and the risk of Frexit seems very limited.

FX: EUR crosses remained heavy under pressure during Friday's session driven by uncertainty in European politics, most notably against the CHF and the USD. The news that the left-wing parties have formed an alliance to challenge Macron is likely the reason for the growing anxiety in the market about political uncertainty. USD/JPY edged slightly higher following the BoJ's decision to reduce bond purchases, which was interpreted as dovish. Later this week we look forward to the Norges Bank, Swiss National Bank and Bank of England meeting on Thursday.