Sample Category Title

EUR/JPY Weekly Outlook

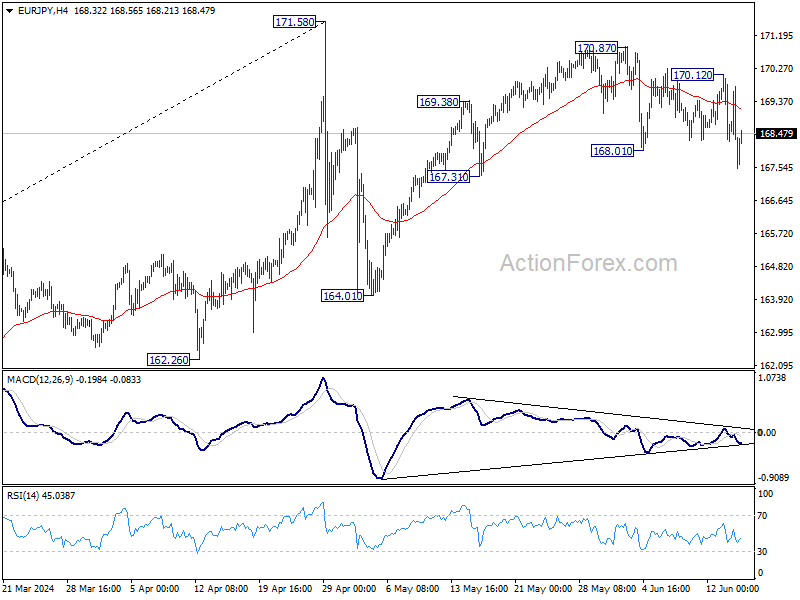

EUR/JPY engaged in sideway trading most of last week but late break of 168.01 support is inline with the case that rise from 164.01 has completed already. Initial bias is back on the downside this week. Sustained trading below 55 D EMA (now at 167.41) will extend the fall from 170.87, as the third leg of the pattern from 151.58, to 164.01 support next. For now, risk will stay on the downside as long as 170.12 resistance holds, in case of recovery.

In the bigger picture, as long as 55 W EMA (now at 159.51) holds, price actions from 171.58 medium term top are seen as as correcting the rise from 153.15 only. That is, larger up trend remains in favor to continue as a later stage. However, sustained break of 55 W EMA will argue that larger scale correction is underway and target 153.15 support.

In the long term picture, rise from 114.42 (2020 low) is seen as the third leg of the whole up trend from 94.11 (2012 low). 100% projection of 94.11 to 149.76 from 114.42 at 170.07 was already met but there is no signal of reversal yet. Firm break of 170.07 will target 138.2% projection at 191.32. This will remain the favored case as long as 153.15 support holds.

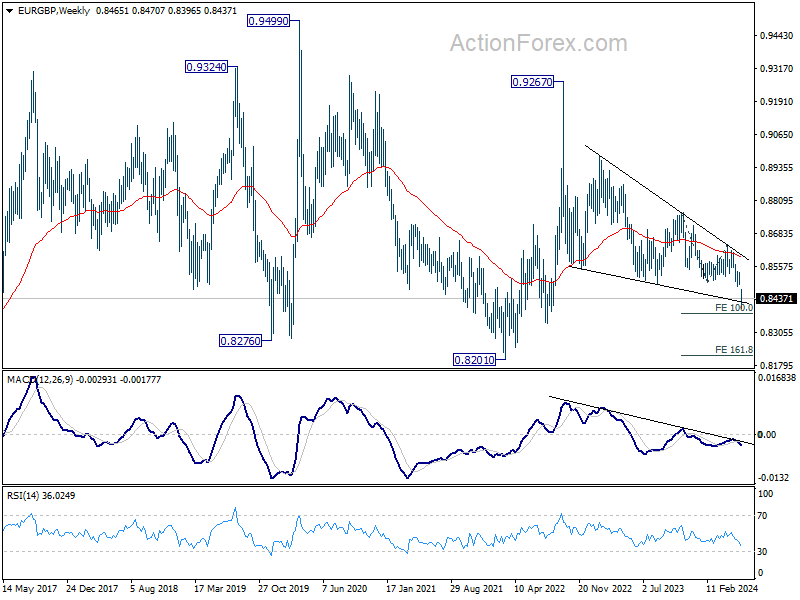

EUR/GBP Weekly Outlook

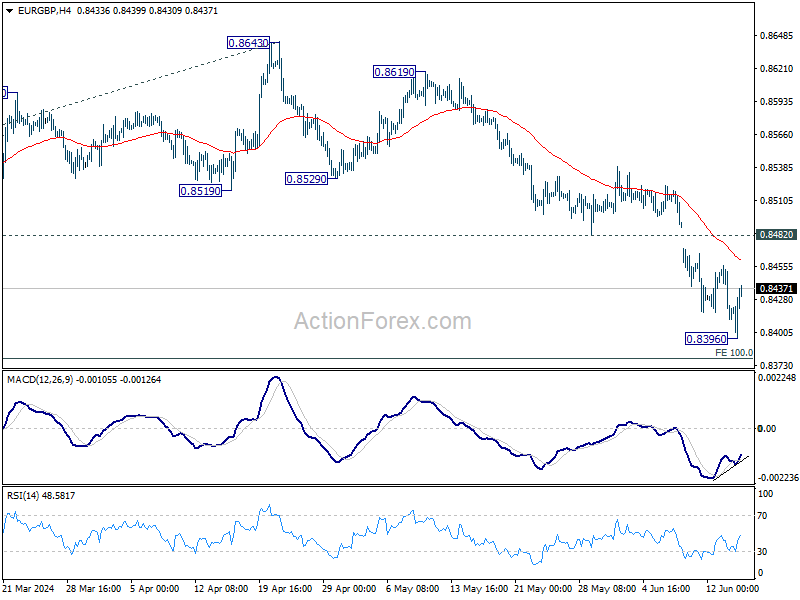

EUR/GBP fell sharply to 0.8396 last week but recovered since then. Initial bias is neutral this week for consolidations first. But outlook will remain bearish as long as 0.8482 support turned resistance holds. Below 0.8396 will resume larger down trend to 0.8376 projection level next.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 100% projection of 0.8764 to 0.8497 from 0.8643 at 0.8376. Sustained break there will target 161.8% projection at 0.8211 next. For now, outlook will remain bearish as long as 0.8643 resistance holds, even in case of stronger rebound.

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Range trading should continue between 0.8201 and 0.9499, until there is clear signal of imminent breakout.

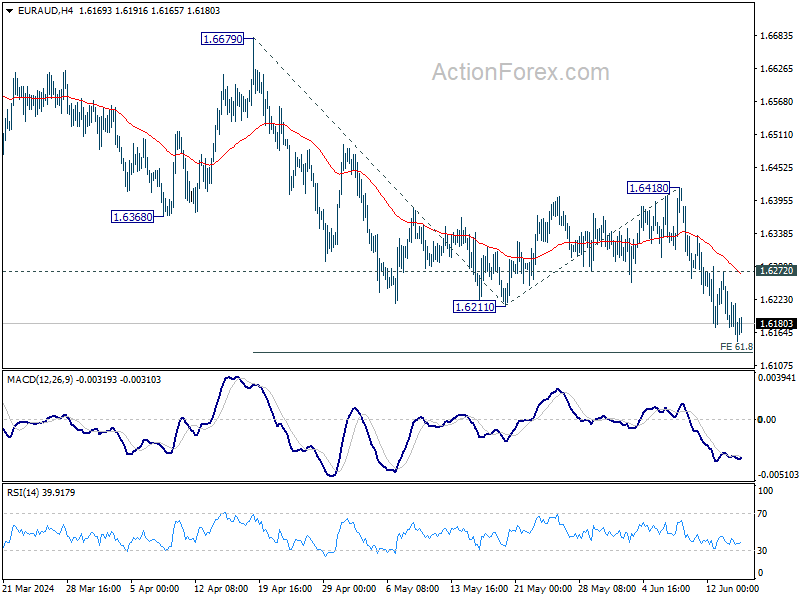

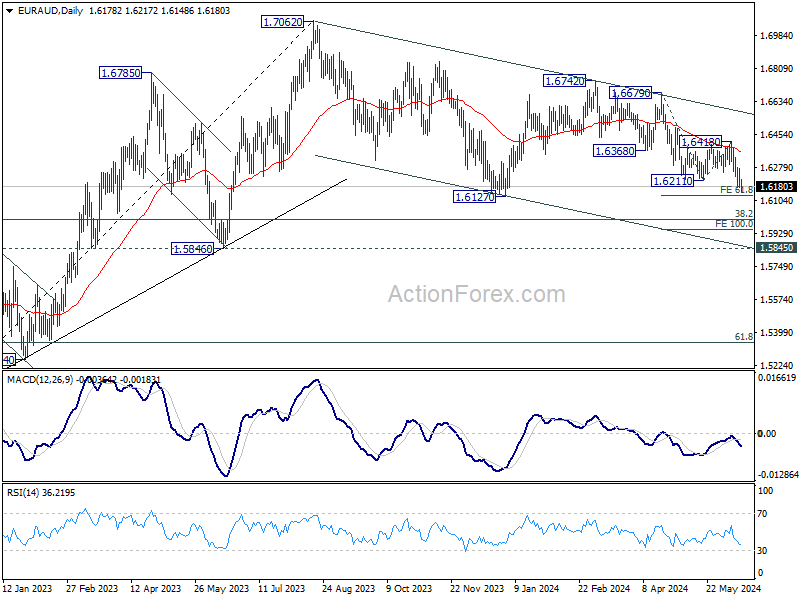

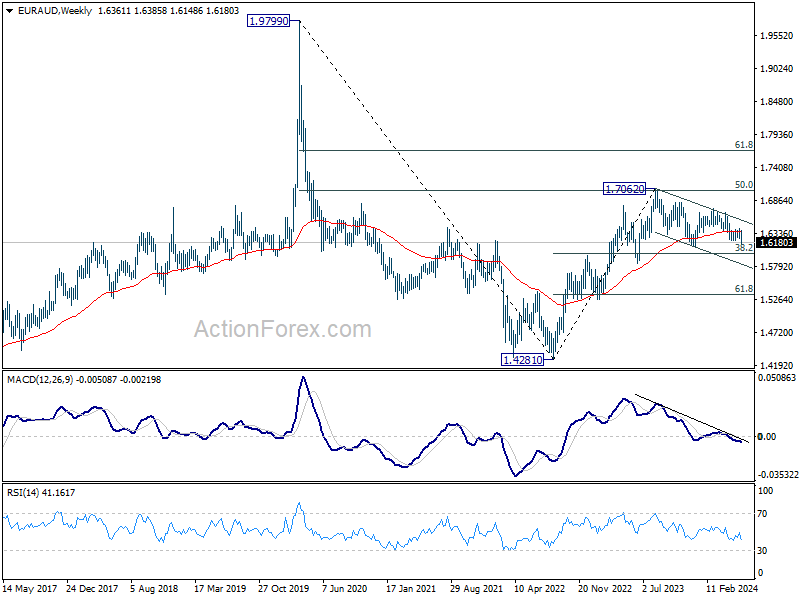

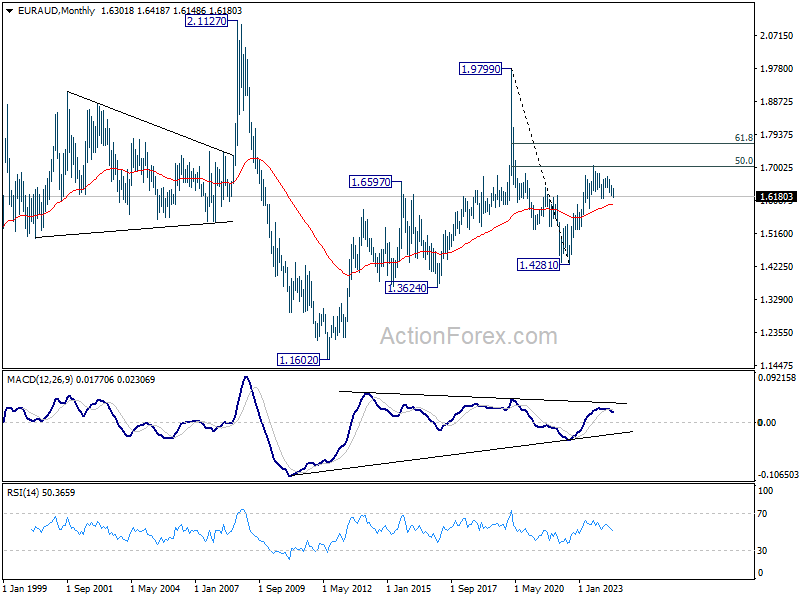

EUR/AUD Weekly Outlook

EUR/AUD's down trend resumed by breaking through 1.6211 support last week. While downside momentum is a bit unconvincing, there is no sign of bottoming yet. Initial bias is on the downside this week for 61.8% projection of 1.6679 to 1.6211 from 1.6418 at 1.6129. Firm break there will target 100% projection at 1.5950. On the upside, above 1.6272 minor resistance will turn intraday bias neutral first.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). In case of deeper fall, strong support is expected around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound. Break of 1.7062 is in favor as a later stage.

In the longer term picture, price actions from 1.9799 (2020 high) are seen as a long term decline at the same scale as the rise from 1.1602 (2012 low). Rebound from 1.4281 is seen as the second leg. As long as 55 M EMA (now at 1.5970) holds, this second leg could still extend higher. However, sustained trading below 55 M EMA will open up the bearish case for extending the decline through 1.4281 low.

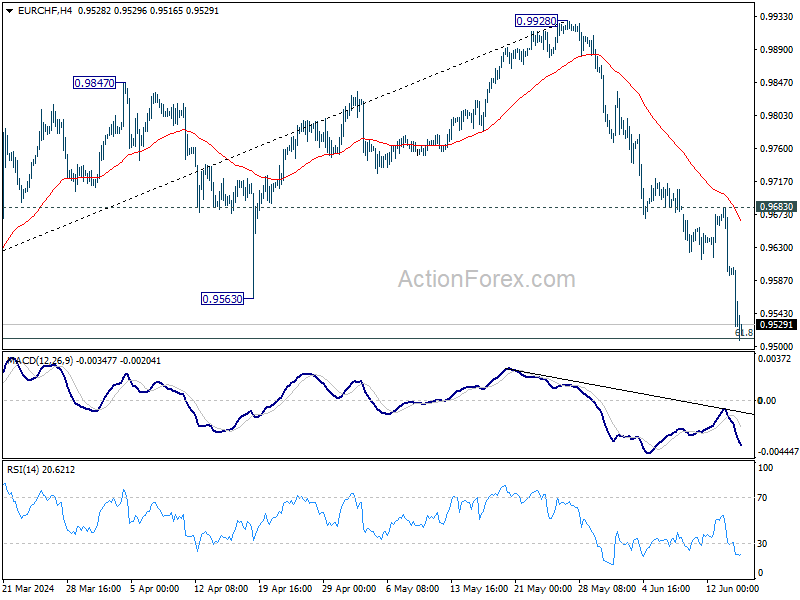

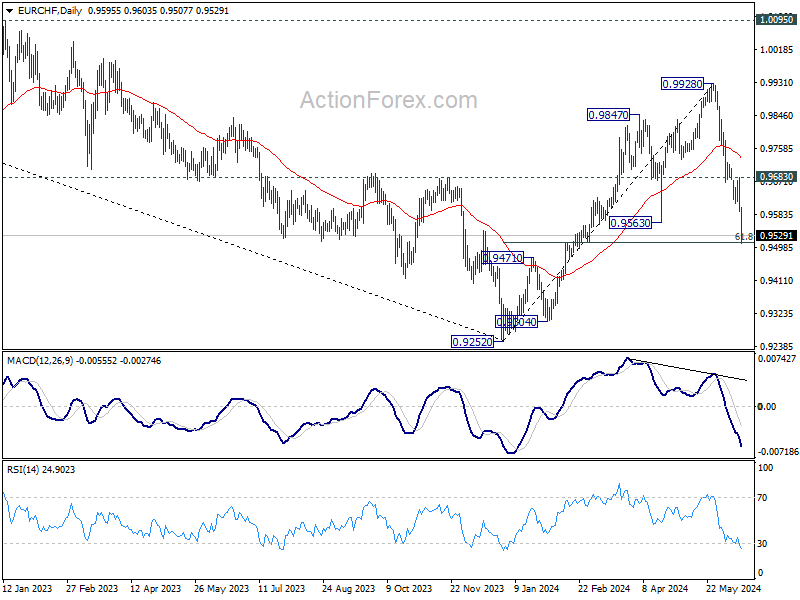

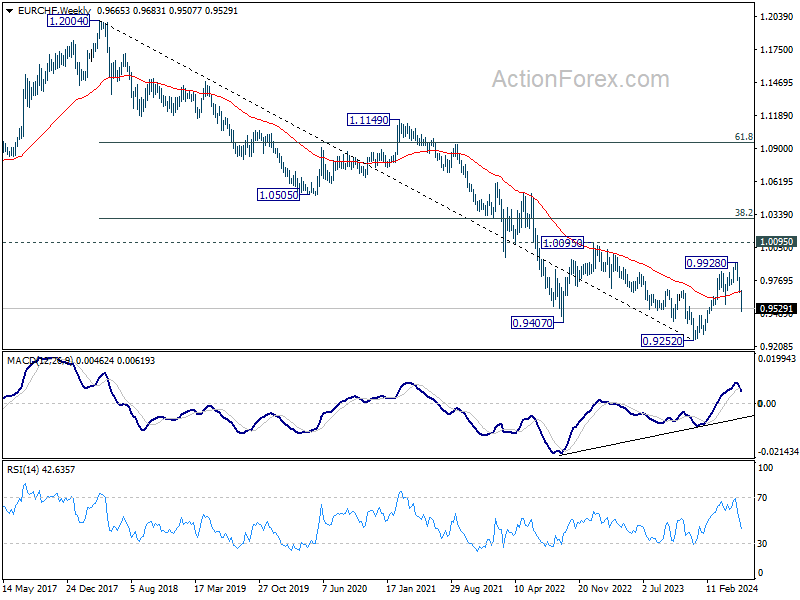

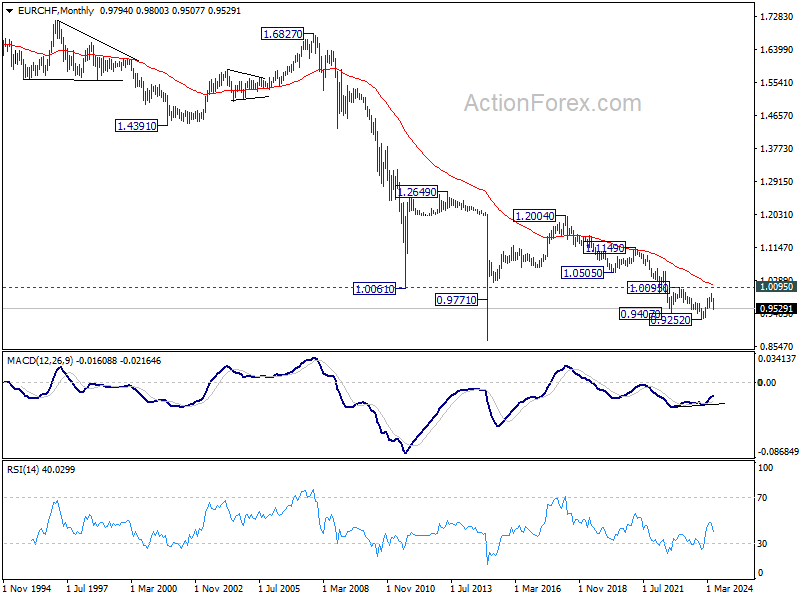

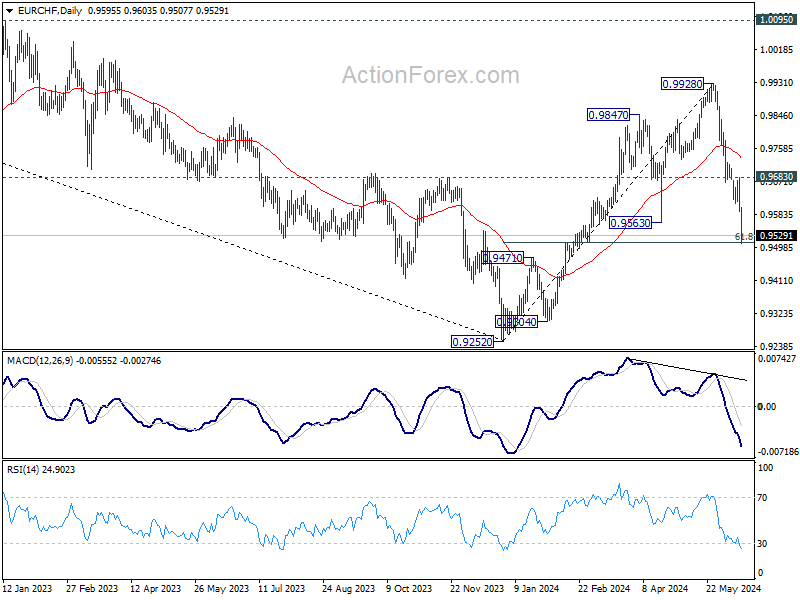

EUR/CHF Weekly Outlook

EUR/CHF's sharp decline last week suggests that rise from 0.9252 has already completed at 0.9928 already. Initial bias stays on the downside this week. Sustained trading below 61.8% retracement of 0.9252 to 0.9928 at 0.9510 will raise the chance of long term down trend resumption, and target 0.9252 low next. For now, outlook will remain bearish as long as 0.9683 resistance holds, in case of recovery.

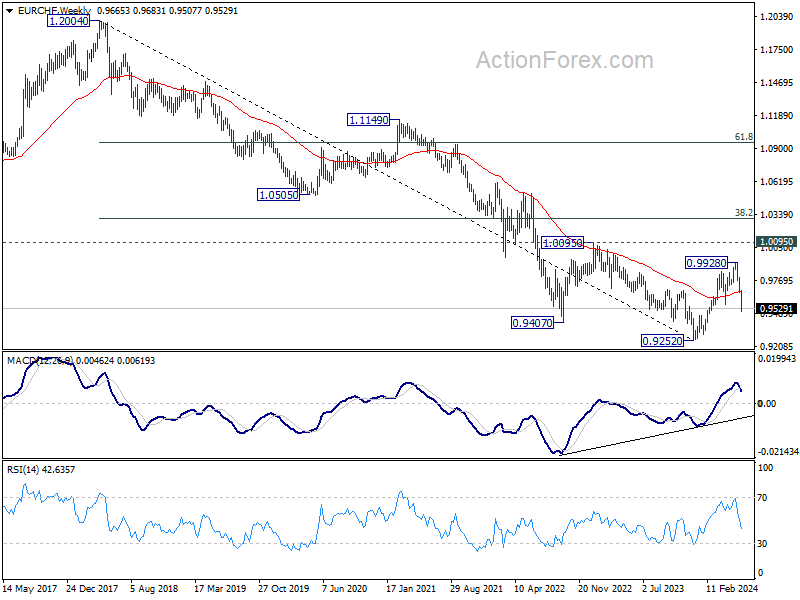

In the bigger picture, the break of 0.9563 support, as well as 55 W EMA (now at 0.9672) argues that rebound from 0.9252 has completed at 0.9928. Medium term bearish is maintained with both 1.0095 resistance intact. Firm break of 0.9252 will resume the down trend from 1.2004 (2018 high).

In the long term picture, fall from 1.2004 (2018 high) is part of the multi-decade down trend. Firm break of 1.0095 resistance is needed to be the first sign of long term bottoming. Otherwise, outlook will remain bearish.

Sharp Declines in Euro and European Markets Triggered by French Political Drama

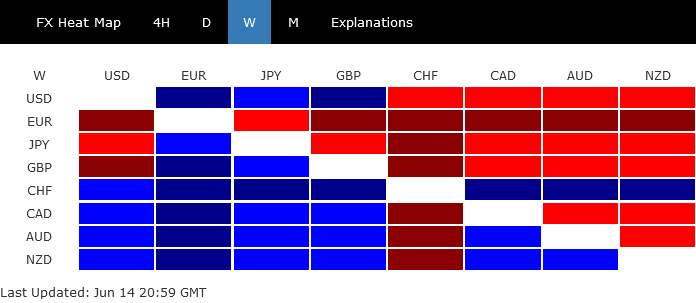

Global financial markets were abuzz with several high-profile events last week, including critical meetings of Fed and BoJ, alongside release of US inflation data. However, it was the escalating political turmoil in France that captured the most attention, significantly impacting Euro and overshadowing other major economic news. The common currency emerged as the week's weakest performer. Meanwhile, pronounced selloffs rippled through both French and German stock markets as political uncertainty loomed large.

The unfolding political drama in France, sparked by President Emmanuel Macron's decision to call snap parliamentary elections, has thrown the European Union into a state of heightened anxiety. Investors are now bracing for the possibility that volatility could extend until the election results are in, which could either exacerbate the current downturn or provide some relief if the outcomes are market-friendly.

Simultaneously, Japanese Yen also experienced late turbulence, mainly due to disappointment with BoJ's ambiguous stance on tapering its bond purchases. While a late-week decline in US and European bond yields provided a temporary lift, it remains to be seen whether this support is robust enough to catalyze a turnaround for Yen.

British Pound wasn't spared from the market upheaval, ending up as the third weakest performer. Dragged down by Euro's decline and its own domestic political uncertainties, with a general election looming in early July, Sterling found itself under considerable pressure.

In contrast, Swiss Franc shone as the week's standout performer, capitalizing on its safe-haven appeal amid the escalating instability in the European Union. This status helped it attract significant flows, distancing itself from the turmoil affecting its European counterparts. Following closely behind were the New Zealand and Australian Dollars, which strengthened mainly due to their relative detachment from the problems plaguing Europe.

Canadian Dollar remained relatively stable, positioned in the middle of the currency spectrum, while Dollar saw a rollercoaster week. Initially depressed by softer CPI data suggesting continued slowdown in inflation, the greenback later gained on safe-haven flows triggered by escalating concerns in Europe.

European Political Uncertainty Shakes Markets, Euro and CAC 40 Take Major Hits

Europe was thrust into the spotlight of the global financial markets following unexpected political developments, with the sudden decision by French President Emmanuel Macron to call snap parliamentary elections following European Parliament elections. These events have injected significant uncertainty into the markets, with Euro experiencing sharp declines and French stocks taking a substantial hit.

Euro ended the week as the poorest performer among major currencies, depreciating by -1.66% against Swiss Franc and over -1.5% against Australian and New Zealand Dollars. This downturn reflects growing investor apprehension about political stability and economic future of the European Union.

France's benchmark stock index, CAC 40, posted its worst weekly performance since March 2022, plummeting by -6.23%. Moreover, the spread between French and German bond yields widened dramatically to a seven-year high, signaling a sharp increase in perceived risk for French government debt relative to its German counterpart. The last time such a yield divergence occurred was in 2017, just before Macron's first presidential victory over Marine Le Pen.

The initial opinion polls following Macron's call for elections have only added to the pessimism, showing his centrist party lagging significantly behind not only the far-right National Rally led by Marine Le Pen but also a unified left-wing bloc. A potential heavy loss for centrist candidates could critically endanger Macron's agenda for pro-growth reforms.

Further dampening investor confidence, projections based on the results of the European Parliament elections suggest a grim scenario for Macron's party in the upcoming legislative elections scheduled for June 30 and July 7. According to these forecasts, only about 40 of Macron's MPs are expected to qualify for the second round in the contest for France's 577-seat National Assembly. This potential outcome raises the specter of a fragmented and polarized parliament where extremist agendas could dominate.

Economists have voiced concerns that if Le Pen influences the new parliament and begins implementing her costly fiscal and protectionist "France first" agenda, France could face a financial crisis similar to that seen in the UK under Liz Truss. Additionally, the coalition of four left-wing parties has made extravagant, unfunded spending pledges worth tens of billions of Euros, further compounding the risk of fiscal irresponsibility.

Technically, while deeper fall cannot be ruled out yet, CAC is now close to an important support zone and recovery should be due shortly. The zone include trend line support at 7440, 61.8% retracement of 6773.81 to 85290.19 at 7341.22, and 38.2% retracement of 5268.41 to 8259.19 at 7254.23. However, risk will remain heavily on the downside ahead as long as 55 D EMA (now at 7984.35) holds, even in case of stronger rebound.

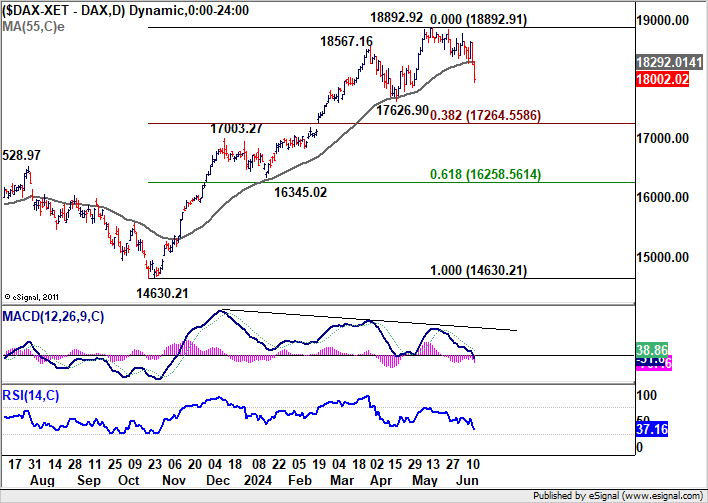

DAX also lost nearly -3% as dragged down by the sharp turn in sentiment in Europe. Rise from 14630.21 should have completed a five-wave sequence to 18892.92, on bearish divergence condition in D MACD. Further decline is expected as long as 55 D EMA (now at 18292.01) holds, to 17626.90 support. But for now, strong support is expected from 38.2% retracement of 14630.21 to 18892.91 at 17264.55 to bring rebound, and keep the long term up trend intact.

EUR/CHF's steep decline and strong break of 55 W EMA (now at 0.9672) indicates that whole rally from 0.9252 has completed already. For now, near term outlook will remain bearish as long as 0.9683 resistance holds. Sustained trading below 61.8% retracement of 0.9252 to 0.9928 at 0.9510, will raise the chance of long term down trend resumption, and target 0.9252 low next.

S&P 500 and NASDAQ Reach New Highs, Dollar Index Rebounds

In the US, investors cheered lower than expected May CPI data that showed disinflation remained on track. Nevertheless, reactions to FOMC's new economic projections were muted. Overall, S&P 500 and NASDAQ capitalized on the positive momentum from the CPI report, both reaching new record highs. In contrast, DOW did not partake in this upward trend and remained noticeably behind its counterparts.

Fed's decision to maintain interest rates at the current range of 5.25-5.50% aligned with broad market expectations. However, the details within Fed's updated economic projections introduced a slightly hawkish tilt that moderated some of the initial enthusiasm from the disinflation news.

On the hawkish front, Fed's median projections have been revised to indicate only one rate cut for this year, significantly down from the three anticipated cuts noted in March. This was further reflected in the updated dot plot, which showed a majority of 11 members now favoring one or no rate cuts, compared to eight members who still advocate for two cuts. This sets a high threshold for shifting back to two rate cuts this year.

Additionally, the upward revision of the long-term "neutral" rate from 2.6% to 2.8%—an increase of over a quarter of a percentage point since the last two sets of projections—signals Fed's growing concern that inflation may be tougher to tame in the coming years. This change implies that the baseline rate for managing economic growth without sparking inflation may need to be higher than previously estimated.

Conversely, the dovish elements in Fed's projections included a significant shift in the committee's stance on future rate hikes. Notably, no FOMC members currently project further rate increases, compared to previous projections where two members anticipated additional hikes might be needed. This consensus to avoid tightening further could be seen as a reassurance to investors

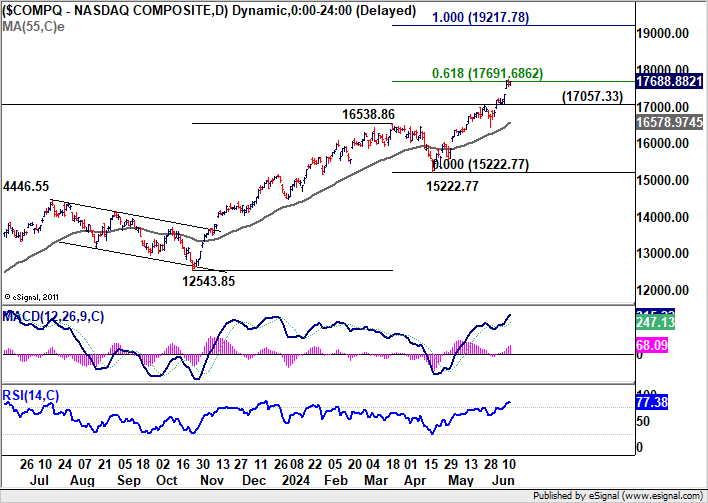

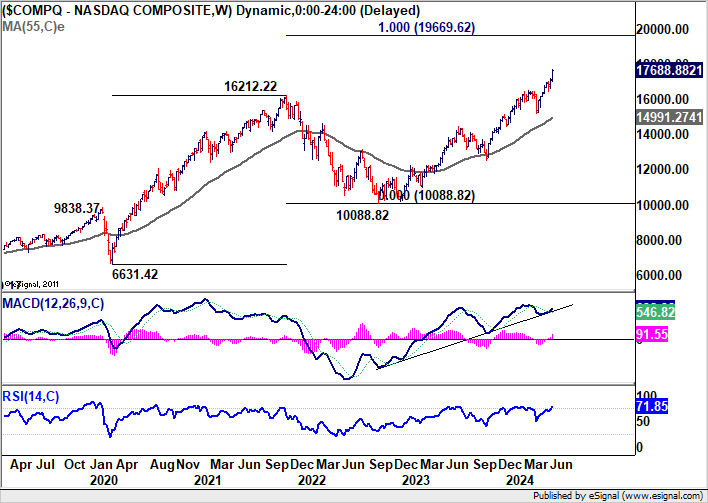

Technically, near term outlook in NASDAQ will remain bullish as long as 17057.33 support holds. Sustained break of 61.8% projection of 12543.85 to 16538.86 from 15222.77 at 19217.78. The long term up trend is also looking healthy, with next target at 100% projection of 6631.42 to 16212.22 from 10088.82 at 19669.62.

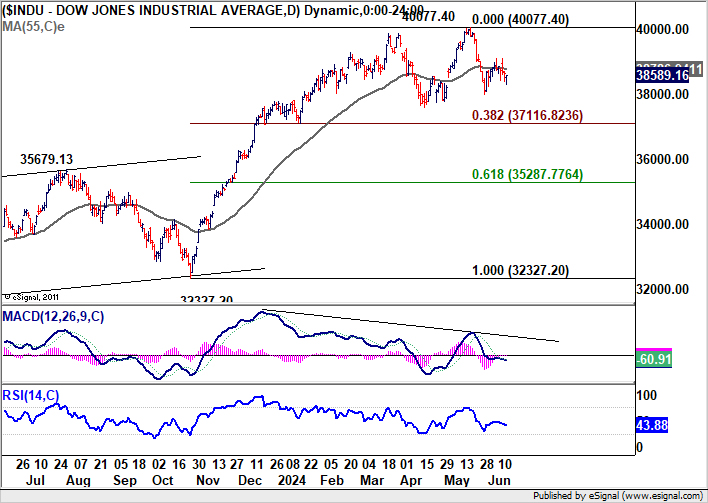

DOW, on the other hand, continued to struggle in sideway trading. While deeper pullback cannot be ruled out, downside should be contained by 38.2% retracement of 32327.20 to 40077.40 at 37116.82 to bring rebound. As long 55 E EME (now at 36900.74) holds, the long term up trend is still in favor to resume at a later stage, to 100% projection of 18213.65 to 36952.65 from 28660.94 at 47399.94.

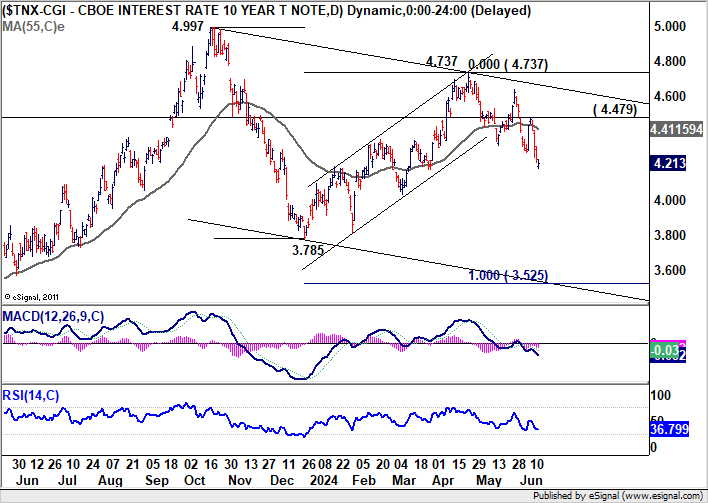

10-year yield's fall from 4.747 resumed last week to close at 4.213, largely due to safe haven flows. Current development is inline with the view that fall from 4.737 is the third leg of the corrective pattern from 4.997. Immediate focus is on 55 W EMA (now at 4.174). Sustained break there will strengthen this bearish case and target 3.785 support and below. Nevertheless, strong rebound from current levels, followed by break of 4.479 resistance, will argue that rise from 3.785 might not be over yet.

Dollar Index rebounded strongly thanks to the selloff in both Euro, and to a lesser extend Yen. The development argues that fall from 106.51 has completed as a correction to 103.99, after drawing support from 55 W EMA (now at 104.17). More importantly, rise from 100.61 is not over. Further rally is now in favor as long as 103.99 holds, to retest 106.51 resistance first. Firm break there will resume the rise from 100.61, as the third leg of the pattern from 99.57, to 107.34 resistance and possibly above.

Yen Struggles Amid BoJ's Uncertainty, CHF/JPY Hits New Highs

Japanese Yen ended as the second-worst performer in the forex markets, despite a late rebound that sparked some optimism that the selloff might be short-lived. BoJ's decision to maintain its policy interest rate unchanged did not come as a surprise. However, the central bank's vague stance on the future of its bond purchase program has injected a significant level of uncertainty into the markets.

BoJ only stated its intention to scale back debt purchases but postponed any detailed announcements until its next policy meeting. This cautious approach is understandable from a strategic perspective, as the board prefers to wait for the upcoming economic projections in July before committing to a specific tapering strategy.

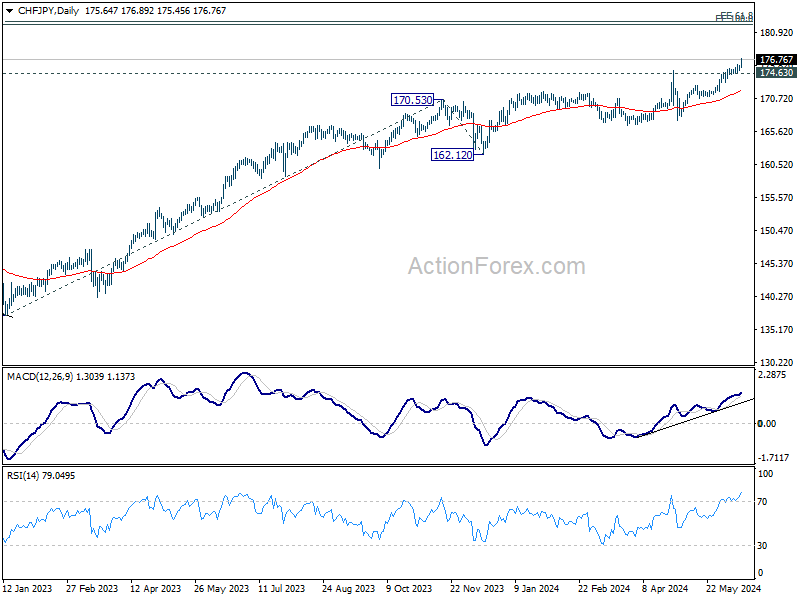

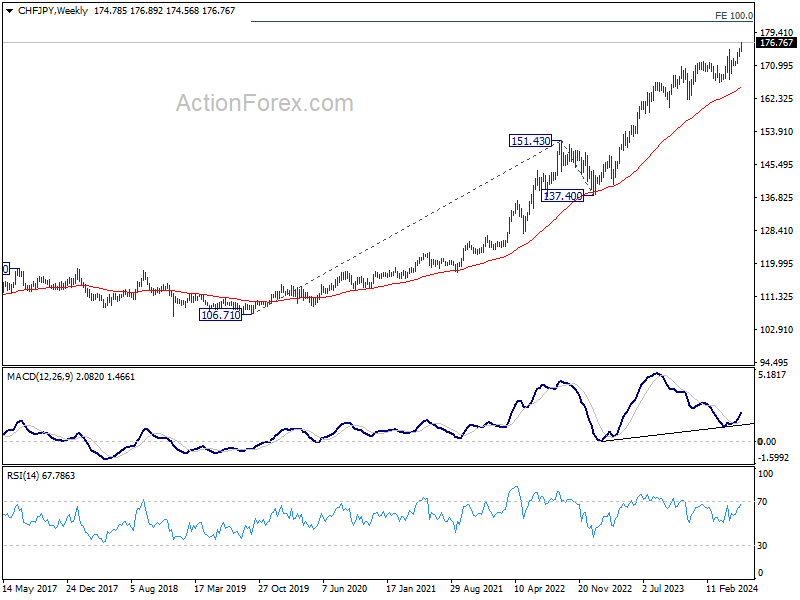

CHF/JPY surged to new record high as the cross builds up momentum again, as seen in both D and W MACD. Near term outlook will stay bullish as long as 174.63 support holds. Next target is 61.8% projection of 137.40 to 170.53 from 162.12 at 182.59. This is slightly above long term level of 100% projection of 106.71 to 141.43 from 137.40 at 182.12.

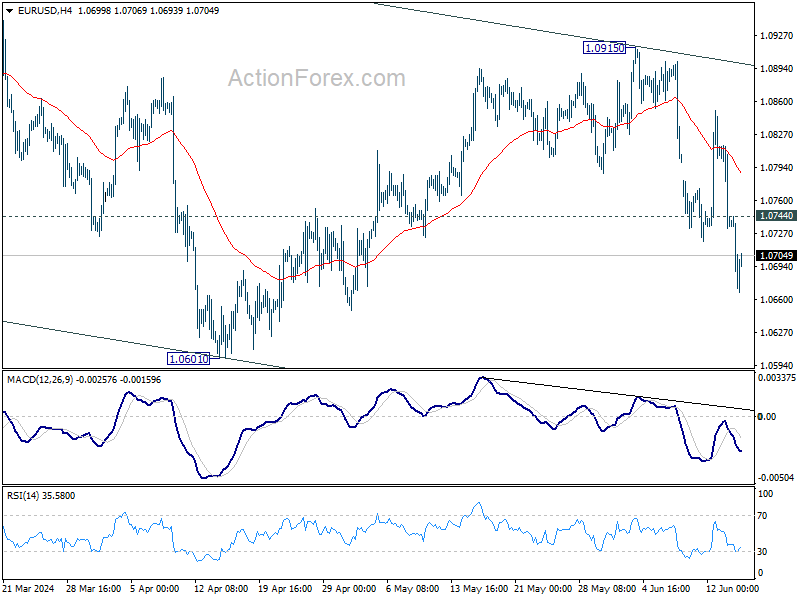

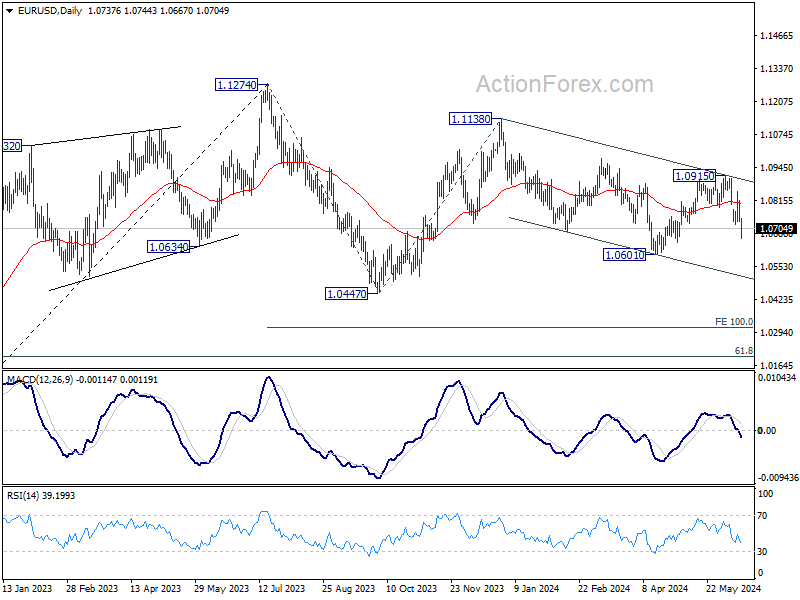

EUR/USD Weekly Outlook

Euro's strong decline last week suggests that rebound from 1.0601 has already completed as a correction to 1.0915. Initial bias stays on the downside this week for retesting 1.0601 low first. Firm break there will target channel support at 1.0510 next. On the upside, above 1.0744 minor resistance will turn intraday bias neutral again first.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's still in progress. Break of 1.0601 will target 1.0447 support and possibly further to 100% projection of 1.1274 to 1.0447 from 1.1138 at 1.0311. For now, this will remain the favored case as long as 1.0915 resistance holds, in case of rebound.

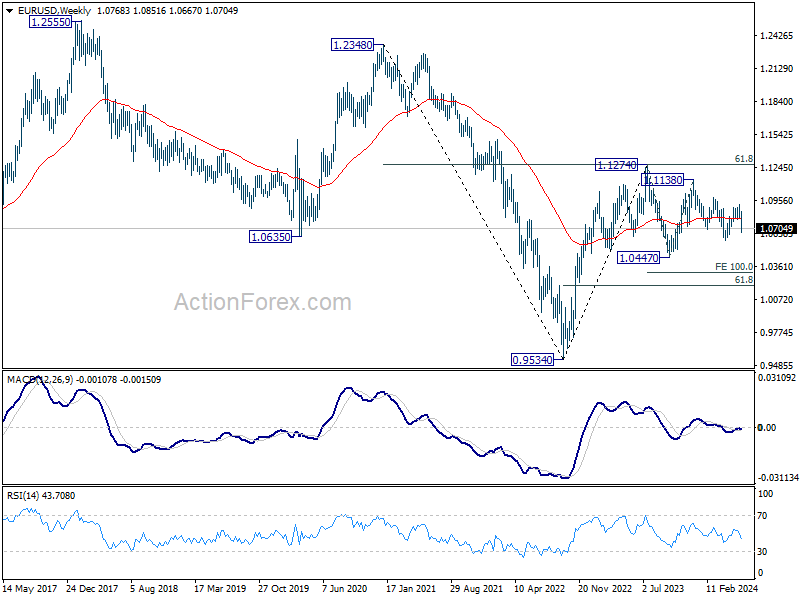

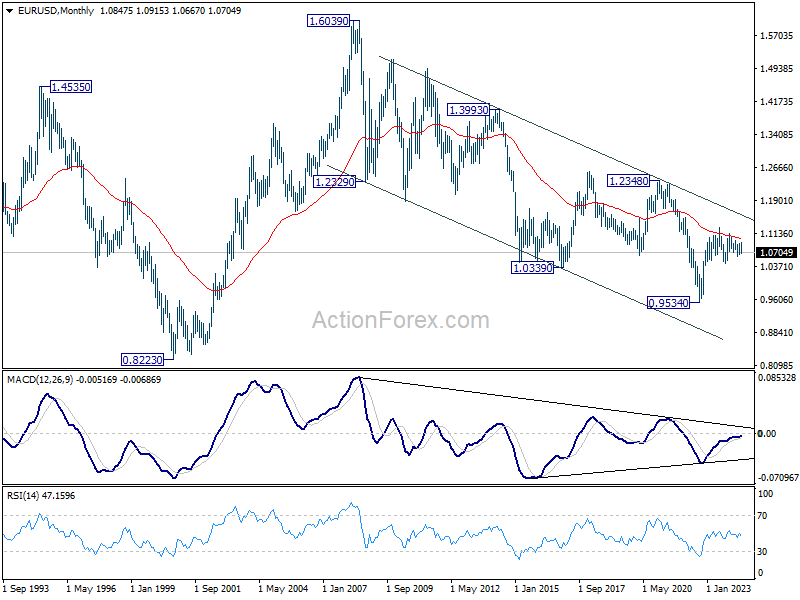

In the long term picture, a long term bottom is in place at 0.9534 (2022 low). But considering that upside is still capped below 55 M EMA (now at 1.1030), there is no sign of trend reversal yet. Down trend from 1.6039 (2008 high) could resume at a later stage if current selloff picks up momentum.

Summary 6/17 – 6/21

Monday, Jun 17, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 22:30 | NZD | Business NZ PSI May | 47.1 | |

| 23:01 | GBP | Rightmove House Price Index M/M Jun | 0.80% | |

| 23:50 | JPY | Machinery Orders M/M Apr | -3.10% | 2.90% |

| 02:00 | CNY | Industrial Production Y/Y May | 6.00% | 6.70% |

| 02:00 | CNY | Retail Sales Y/Y May | 3.00% | 2.30% |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y May | 4.20% | 4.20% |

| 07:00 | CHF | SECO Economic Forecasts | ||

| 12:15 | CAD | Housing Starts Y/Y May | 241K | 240K |

| 12:30 | USD | Empire State Manufacturing Index Jun | -13 | -15.6 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 22:30 | NZD | Business NZ PSI May | |

| Forecast: | Previous: 47.1 | ||

| 23:01 | GBP | Rightmove House Price Index M/M Jun | |

| Forecast: | Previous: 0.80% | ||

| 23:50 | JPY | Machinery Orders M/M Apr | |

| Forecast: -3.10% | Previous: 2.90% | ||

| 02:00 | CNY | Industrial Production Y/Y May | |

| Forecast: 6.00% | Previous: 6.70% | ||

| 02:00 | CNY | Retail Sales Y/Y May | |

| Forecast: 3.00% | Previous: 2.30% | ||

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y May | |

| Forecast: 4.20% | Previous: 4.20% | ||

| 07:00 | CHF | SECO Economic Forecasts | |

| Forecast: | Previous: | ||

| 12:15 | CAD | Housing Starts Y/Y May | |

| Forecast: 241K | Previous: 240K | ||

| 12:30 | USD | Empire State Manufacturing Index Jun | |

| Forecast: -13 | Previous: -15.6 | ||

Tuesday, Jun 18, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 04:30 | AUD | RBA Interest Rate Decision | 4.35% | 4.35% |

| 09:00 | EUR | Eurozone CPI Y/Y May F | 2.60% | 2.60% |

| 09:00 | EUR | Eurozone CPI Core Y/Y May F | 2.90% | 2.90% |

| 09:00 | EUR | Germany ZEW Economic Sentiment Jun | 50 | 47.1 |

| 09:00 | EUR | Germany ZEW Current Situation Jun | -69 | -72.3 |

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Jun | 47.2 | 47 |

| 12:30 | USD | Retail Sales M/M May | 0.30% | 0.00% |

| 12:30 | USD | Retail Sales ex Autos M/M May | 0.20% | 0.20% |

| 13:15 | USD | Industrial Production M/M May | 0.40% | 0.00% |

| 13:15 | USD | Capacity Utilization May | 78.60% | 78.40% |

| 14:00 | USD | Business Inventories Apr | 0.30% | -0.10% |

| 22:45 | NZD | Current Account (NZD) Q1 | -4.65B | -7.84B |

| 23:50 | JPY | Trade Balance (JPY) May | -0.63T | -0.56T |

| 23:50 | JPY | BoJ Minutes |

| GMT | Ccy | Events | |

|---|---|---|---|

| 04:30 | AUD | RBA Interest Rate Decision | |

| Forecast: 4.35% | Previous: 4.35% | ||

| 09:00 | EUR | Eurozone CPI Y/Y May F | |

| Forecast: 2.60% | Previous: 2.60% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y May F | |

| Forecast: 2.90% | Previous: 2.90% | ||

| 09:00 | EUR | Germany ZEW Economic Sentiment Jun | |

| Forecast: 50 | Previous: 47.1 | ||

| 09:00 | EUR | Germany ZEW Current Situation Jun | |

| Forecast: -69 | Previous: -72.3 | ||

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Jun | |

| Forecast: 47.2 | Previous: 47 | ||

| 12:30 | USD | Retail Sales M/M May | |

| Forecast: 0.30% | Previous: 0.00% | ||

| 12:30 | USD | Retail Sales ex Autos M/M May | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 13:15 | USD | Industrial Production M/M May | |

| Forecast: 0.40% | Previous: 0.00% | ||

| 13:15 | USD | Capacity Utilization May | |

| Forecast: 78.60% | Previous: 78.40% | ||

| 14:00 | USD | Business Inventories Apr | |

| Forecast: 0.30% | Previous: -0.10% | ||

| 22:45 | NZD | Current Account (NZD) Q1 | |

| Forecast: -4.65B | Previous: -7.84B | ||

| 23:50 | JPY | Trade Balance (JPY) May | |

| Forecast: -0.63T | Previous: -0.56T | ||

| 23:50 | JPY | BoJ Minutes | |

| Forecast: | Previous: | ||

Wednesday, Jun 19, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 06:00 | GBP | CPI M/M May | 0.30% | |

| 06:00 | GBP | CPI Y/Y May | 2.00% | 2.30% |

| 06:00 | GBP | Core CPI Y/Y May | 3.50% | 3.90% |

| 06:00 | GBP | RPI M/M May | 0.50% | |

| 06:00 | GBP | RPI Y/Y May | 3.10% | 3.30% |

| 06:00 | GBP | PPI Input M/M May | -0.20% | 0.60% |

| 06:00 | GBP | PPI Input Y/Y May | -1.60% | |

| 06:00 | GBP | PPI Output M/M May | 0.10% | 0.20% |

| 06:00 | GBP | PPI Output Y/Y May | 1.10% | |

| 06:00 | GBP | PPI Core Output M/M May | 0% | |

| 06:00 | GBP | PPI Core Output Y/Y May | 0.20% | |

| 08:00 | EUR | Eurozone Current Account (EUR) Apr | 35.2B | 35.8B |

| 14:00 | USD | NAHB Housing Index Jun | 46 | 45 |

| 17:30 | CAD | BoC Summary of Deliberations | ||

| 22:45 | NZD | GDP Q/Q Q1 | 0.10% | -0.10% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 06:00 | GBP | CPI M/M May | |

| Forecast: | Previous: 0.30% | ||

| 06:00 | GBP | CPI Y/Y May | |

| Forecast: 2.00% | Previous: 2.30% | ||

| 06:00 | GBP | Core CPI Y/Y May | |

| Forecast: 3.50% | Previous: 3.90% | ||

| 06:00 | GBP | RPI M/M May | |

| Forecast: | Previous: 0.50% | ||

| 06:00 | GBP | RPI Y/Y May | |

| Forecast: 3.10% | Previous: 3.30% | ||

| 06:00 | GBP | PPI Input M/M May | |

| Forecast: -0.20% | Previous: 0.60% | ||

| 06:00 | GBP | PPI Input Y/Y May | |

| Forecast: | Previous: -1.60% | ||

| 06:00 | GBP | PPI Output M/M May | |

| Forecast: 0.10% | Previous: 0.20% | ||

| 06:00 | GBP | PPI Output Y/Y May | |

| Forecast: | Previous: 1.10% | ||

| 06:00 | GBP | PPI Core Output M/M May | |

| Forecast: | Previous: 0% | ||

| 06:00 | GBP | PPI Core Output Y/Y May | |

| Forecast: | Previous: 0.20% | ||

| 08:00 | EUR | Eurozone Current Account (EUR) Apr | |

| Forecast: 35.2B | Previous: 35.8B | ||

| 14:00 | USD | NAHB Housing Index Jun | |

| Forecast: 46 | Previous: 45 | ||

| 17:30 | CAD | BoC Summary of Deliberations | |

| Forecast: | Previous: | ||

| 22:45 | NZD | GDP Q/Q Q1 | |

| Forecast: 0.10% | Previous: -0.10% | ||

Thursday, Jun 20, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:15 | CNY | 1-y Loan Prime Rate | 3.45% | |

| 01:15 | CNY | 5-y Loan Prime Rate | 3.95% | |

| 06:00 | CHF | Trade Balance (CHF) May | 4.32B | |

| 06:00 | EUR | Germany PPI M/M May | 0.10% | 0.20% |

| 06:00 | EUR | Germany PPI Y/Y May | -3.30% | |

| 07:30 | CHF | SNB Interest Rate Decision | 1.50% | |

| 08:00 | CHF | SNB Press Conference | ||

| 08:00 | EUR | ECB Economic Bulletin | ||

| 11:00 | GBP | BoE Interest Rate Decision | 5.25% | 5.25% |

| 11:00 | GBP | MPC Official Bank Rate Votes | 0--2--7 | 0--2--7 |

| 12:30 | CAD | New Housing Price Index M/M May | 0.20% | 0.20% |

| 12:30 | USD | Building Permits May | 1.46M | 1.44M |

| 12:30 | USD | Housing Starts May | 1.38M | 1.36M |

| 12:30 | USD | Current Account (USD) Q1 | -206B | -195B |

| 12:30 | USD | Initial Jobless Claims (Jun 14) | 240K | 242K |

| 12:30 | USD | Philadelphia Fed Survey Jun | 4.5 | 4.5 |

| 14:00 | EUR | Eurozone Consumer Confidence Jun P | -14 | -14 |

| 15:00 | USD | Crude Oil Inventories | 3.7M | |

| 23:00 | AUD | Manufacturing PMI Jun P | 49.7 | |

| 23:00 | AUD | Services PMI Jun P | 52.5 | |

| 23:01 | GBP | GfK Consumer Confidence Jun | -16 | -17 |

| 23:30 | JPY | National CPI Y/Y May | 2.50% | |

| 23:30 | JPY | National CPI ex Fresh Food Y/Y May | 2.60% | 2.20% |

| 23:30 | JPY | National CPI ex Food Energy Y/Y May | 2.40% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:15 | CNY | 1-y Loan Prime Rate | |

| Forecast: | Previous: 3.45% | ||

| 01:15 | CNY | 5-y Loan Prime Rate | |

| Forecast: | Previous: 3.95% | ||

| 06:00 | CHF | Trade Balance (CHF) May | |

| Forecast: | Previous: 4.32B | ||

| 06:00 | EUR | Germany PPI M/M May | |

| Forecast: 0.10% | Previous: 0.20% | ||

| 06:00 | EUR | Germany PPI Y/Y May | |

| Forecast: | Previous: -3.30% | ||

| 07:30 | CHF | SNB Interest Rate Decision | |

| Forecast: | Previous: 1.50% | ||

| 08:00 | CHF | SNB Press Conference | |

| Forecast: | Previous: | ||

| 08:00 | EUR | ECB Economic Bulletin | |

| Forecast: | Previous: | ||

| 11:00 | GBP | BoE Interest Rate Decision | |

| Forecast: 5.25% | Previous: 5.25% | ||

| 11:00 | GBP | MPC Official Bank Rate Votes | |

| Forecast: 0--2--7 | Previous: 0--2--7 | ||

| 12:30 | CAD | New Housing Price Index M/M May | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 12:30 | USD | Building Permits May | |

| Forecast: 1.46M | Previous: 1.44M | ||

| 12:30 | USD | Housing Starts May | |

| Forecast: 1.38M | Previous: 1.36M | ||

| 12:30 | USD | Current Account (USD) Q1 | |

| Forecast: -206B | Previous: -195B | ||

| 12:30 | USD | Initial Jobless Claims (Jun 14) | |

| Forecast: 240K | Previous: 242K | ||

| 12:30 | USD | Philadelphia Fed Survey Jun | |

| Forecast: 4.5 | Previous: 4.5 | ||

| 14:00 | EUR | Eurozone Consumer Confidence Jun P | |

| Forecast: -14 | Previous: -14 | ||

| 15:00 | USD | Crude Oil Inventories | |

| Forecast: | Previous: 3.7M | ||

| 23:00 | AUD | Manufacturing PMI Jun P | |

| Forecast: | Previous: 49.7 | ||

| 23:00 | AUD | Services PMI Jun P | |

| Forecast: | Previous: 52.5 | ||

| 23:01 | GBP | GfK Consumer Confidence Jun | |

| Forecast: -16 | Previous: -17 | ||

| 23:30 | JPY | National CPI Y/Y May | |

| Forecast: | Previous: 2.50% | ||

| 23:30 | JPY | National CPI ex Fresh Food Y/Y May | |

| Forecast: 2.60% | Previous: 2.20% | ||

| 23:30 | JPY | National CPI ex Food Energy Y/Y May | |

| Forecast: | Previous: 2.40% | ||

Friday, Jun 21, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Jun P | 50.6 | 50.4 |

| 06:00 | GBP | Retail Sales M/M May | 1.50% | -2.30% |

| 06:00 | GBP | Public Sector Net Borrowing (GBP) May | 14.8B | 19.6B |

| 07:15 | EUR | France Manufacturing PMI Jun P | 46.8 | 46.4 |

| 07:15 | EUR | France Services PMI Jun P | 50 | 49.3 |

| 07:30 | EUR | Germany Manufacturing PMI Jun P | 46.4 | 45.4 |

| 07:30 | EUR | Germany Services PMI Jun P | 54.4 | 54.2 |

| 08:00 | EUR | Eurozone Manufacturing PMI Jun P | 48 | 47.3 |

| 08:00 | EUR | Eurozone Services PMI Jun P | 53.5 | 53.2 |

| 08:00 | EUR | Composite PMI Jun P | 52.2 | |

| 08:30 | GBP | Manufacturing PMI Jun P | 51 | 51.2 |

| 08:30 | GBP | Services PMI Jun P | 53.2 | 52.9 |

| 12:30 | CAD | Industrial Product Price M/M May | 1.50% | |

| 12:30 | CAD | Raw Material Price Index May | 5.50% | |

| 12:30 | CAD | Retail Sales M/M Apr | 0.90% | -0.20% |

| 12:30 | CAD | Retail Sales ex Autos M/M Apr | 0.50% | -0.60% |

| 13:45 | USD | Manufacturing PMI Jun P | 51 | 51.3 |

| 13:45 | USD | Services PMI Jun P | 53.5 | 54.8 |

| 14:00 | USD | Existing Home Sales May | 4.10M | 4.14M |

| 14:30 | USD | Natural Gas Storage | 74B |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Jun P | |

| Forecast: 50.6 | Previous: 50.4 | ||

| 06:00 | GBP | Retail Sales M/M May | |

| Forecast: 1.50% | Previous: -2.30% | ||

| 06:00 | GBP | Public Sector Net Borrowing (GBP) May | |

| Forecast: 14.8B | Previous: 19.6B | ||

| 07:15 | EUR | France Manufacturing PMI Jun P | |

| Forecast: 46.8 | Previous: 46.4 | ||

| 07:15 | EUR | France Services PMI Jun P | |

| Forecast: 50 | Previous: 49.3 | ||

| 07:30 | EUR | Germany Manufacturing PMI Jun P | |

| Forecast: 46.4 | Previous: 45.4 | ||

| 07:30 | EUR | Germany Services PMI Jun P | |

| Forecast: 54.4 | Previous: 54.2 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Jun P | |

| Forecast: 48 | Previous: 47.3 | ||

| 08:00 | EUR | Eurozone Services PMI Jun P | |

| Forecast: 53.5 | Previous: 53.2 | ||

| 08:00 | EUR | Composite PMI Jun P | |

| Forecast: | Previous: 52.2 | ||

| 08:30 | GBP | Manufacturing PMI Jun P | |

| Forecast: 51 | Previous: 51.2 | ||

| 08:30 | GBP | Services PMI Jun P | |

| Forecast: 53.2 | Previous: 52.9 | ||

| 12:30 | CAD | Industrial Product Price M/M May | |

| Forecast: | Previous: 1.50% | ||

| 12:30 | CAD | Raw Material Price Index May | |

| Forecast: | Previous: 5.50% | ||

| 12:30 | CAD | Retail Sales M/M Apr | |

| Forecast: 0.90% | Previous: -0.20% | ||

| 12:30 | CAD | Retail Sales ex Autos M/M Apr | |

| Forecast: 0.50% | Previous: -0.60% | ||

| 13:45 | USD | Manufacturing PMI Jun P | |

| Forecast: 51 | Previous: 51.3 | ||

| 13:45 | USD | Services PMI Jun P | |

| Forecast: 53.5 | Previous: 54.8 | ||

| 14:00 | USD | Existing Home Sales May | |

| Forecast: 4.10M | Previous: 4.14M | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 74B | ||

The Weekly Bottom Line: The Data Will Light the Way

U.S. Highlights

- In a widely expected move, the Federal Reserve held the policy rate steady in the target range of 5.25%-5.5%.

- FOMC participants now expect fewer rate cuts this year, with the median projection showing just one cut by year-end (previously three).

- Consumer Price Index (CPI) inflation came in weaker than expected in May, with the core measure recording its softest monthly gain since August 2021.

Canadian Highlights

- A quiet week for Canadian economic data had fixed income markets taking their cue from the U.S. The Federal Reserve left interest rates unchanged, but an encouraging inflation report led markets to take yields lower.

- The national balance sheet data for the first quarter had some encouraging news. Canadians’ net worth improved, in part due to greater thrift among households.

- Household leverage and the debt service ratio have moved down a bit. Half of mortgages are still set to renew at higher rates over the next couple of years, and we will be watching how that burden evolves given the implications for consumer spending.

U.S. – The Data Will Light the Way

How quickly things can change! It was just six months ago that financial markets were positioned for six rate cuts by the end of this year. At the time, 50 basis points (bps) of cuts were expected to have happened by the June FOMC meeting. Well, that meeting has come and gone, and things haven’t quite shaped up as expected. The median forecast of FOMC participants is now showing just one rate cut by the end of this year. Bond traders are a bit more optimistic, currently pricing for two cuts, after a very soft CPI reading this week. A faster cooling in inflationary pressures helped to catapult the S&P 500 higher by over 1% on the week, while the 10-year Treasury dipped by 22 bps landing at 4.21%.

In a widely expected move, the Federal Reserve kept its policy rate unchanged holding the target range at 5.25%-5.5% for the seventh consecutive meeting. Accompanying the announcement, the FOMC also released a revised Summary of Economic Projects (SEP). In terms of the macroeconomic forecasts, there were few changes made relative to March. Expectations for growth this year and next remained unchanged at 2.1% and 2.0%, respectively, while the unemployment rate saw a modest upward revision of 0.1 percentage points in 2025 (to 4.2%) and 2026 (to 4.1%). The inflation forecast was nudged higher, with core PCE now expected to hold steady at 2.8% (previously 2.6%) through year-end, before slipping to 2.3% (previously 2.2%) by the end of the next year.

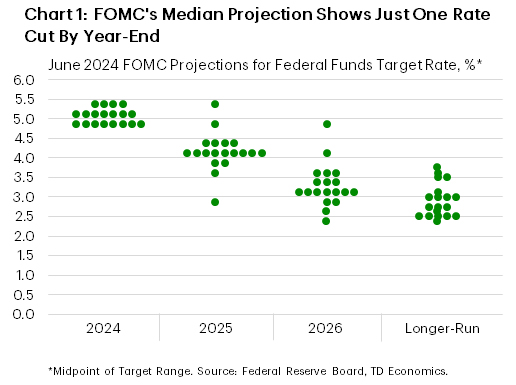

The most notable change in the SEP came from the Committee’s view on the future expectations of the policy rate. On the surface, the updated median Fed funds rate projection appears considerably more hawkish – now showing just one cut for this year as opposed to the three penciled in back in March. But a closer look at the dispersion of forecasts shows that FOMC members are nearly split between one (seven participants) and two (eight participants) cuts by year-end (Chart 1). Four members expect to keep the policy rate unchanged until next year.

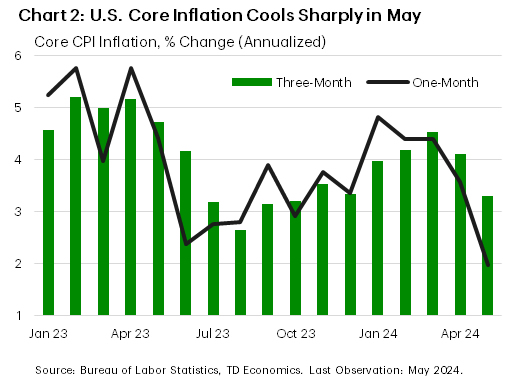

Broadly speaking, the upward revision to the ‘dots’ is a direct result of inflation having firmed through the first three-months of the year. However, the April inflation data showed some reprieve on that front, and this week’s May reading on CPI came in considerably below expectations. Core inflation rose by just 0.16% month-on-month – it’s softest monthly print since August 2021. The underlying details of the report were also constructive, with services inflation showing a notable cooling – entirely driven by the ‘supercore’ component – while goods prices were flat on the month. Encouragingly, the three-month annualized rate of change on core CPI slipped to 3.3% – a pace of price growth more consistent with late-2023 (Chart 2).

During the press conference, Chair Powell acknowledged the last two softer-than-expected readings on inflation. However, he also reiterated that inflation “remains far too high” and that the FOMC needs to “greater confidence” before easing monetary policy. Whether that can be achieved over the next few months remains to be seen. As Powell noted in the press conference, “the data will light the way”.

Canada – The Upside of Higher Interest Rates

It was a quiet week for Canadian economic data, with fixed income markets cuing off signals from the U.S. Federal Reserve and a soft U.S. inflation print. One week after the Bank of Canada’s interest rate cut, bond yields are down a bit further. Canadian equity markets have had a rough week, in contrast to a stronger outturn south of the border.

The most interesting release was the first quarter national balance sheet accounts, which measures the assets and liabilities of Canadian households, businesses, and governments. All told, the story is good news. Household net worth made solid gains in the first quarter of 2024, largely thanks to healthy growth in financial assets. Net worth has now surpassed its earlier peak in the first quarter of 2022, before the housing market dipped under the weight of higher interest rates.

These gains in financial assets are not all just increases in valuations. Canadians, on net, have rediscovered saving. That is likely due to a combination of increased precautionary savings and higher risk-free interest rates providing a stronger incentive to lock money away for a rainy day. Precautionary savings likely stems from a couple of sources: 1) worries about a potential recession over the past couple of years, and 2) households facing mortgage renewals at higher rates perhaps putting some money away to pay down principal. Whatever the reason, the household savings rate ticked up to 6.9% in the first quarter of 2024, more than double the rate in the five years prior to the pandemic.

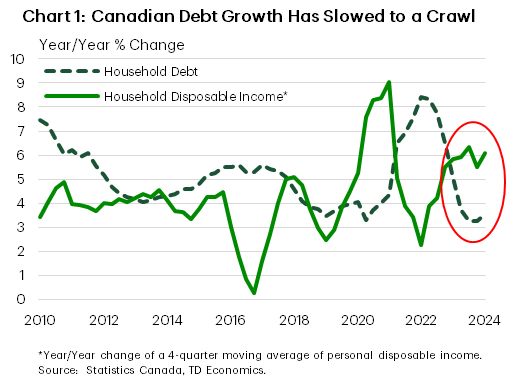

The other side of the coin in increased savings activity is less debt-financed consumption. Since the Bank of Canada (BoC) started raising interest rates in 2022, households have dramatically pared back borrowing. Canadians added debt at a very soft pace in the first quarter, and around a 3 ½% clip over the past year. This is modest on a historical basis, and now well below growth in income (Chart 1). This means that household leverage, as measured by the debt-to-income ratio, has been trending modestly downward from its peak at the end of 2021.

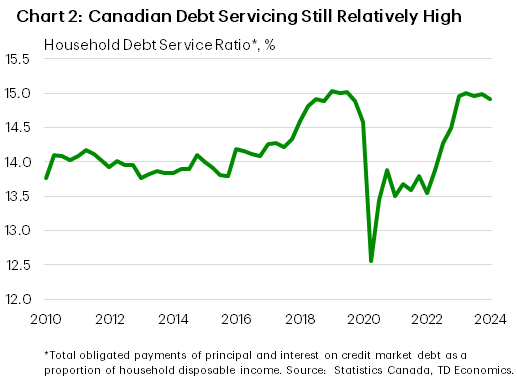

This has also helped the debt service ratio, which measures the share of total household income in Canada that goes towards servicing debt, has plateaued and come down very slightly (Chart 2). This is a better outcome than we had expected when the BoC first started raising interest rates. However, we are not out of the woods entirely yet. Many borrowers who took out mortgages at rock bottom interest rates in 2020 and 2021 will face renewals at much higher borrowing costs (see rate forecasts) over the next couple of years. According to the BoC’s Financial Stability Report released in May, about half of outstanding mortgages have yet to see payment increases due to higher rates. This is likely to keep the debt servicing burden elevated and weigh on consumer spending over the next couple of years. Thankfully Canadians have also seen their incomes grow, which should also help to cushion the strain of higher debt payments.

Weekly Economic & Financial Commentary: Inflation Cools as Summer Begins

Summary

United States: Inflation Cools as Summer Begins

- A bevy of soft inflation data for May fueled optimism that the Federal Reserve will begin cutting rates at the September FOMC meeting. On Wednesday, the May CPI data showed that consumer prices were unchanged in the month, the first flat reading for the CPI since July 2022. Excluding food and energy, core CPI increased by a "low" 0.2% (0.16% before rounding), the smallest monthly increase since August 2021.

- Next week: Retail Sales (Tue.), Industrial Production (Tue.), Existing Home Sales (Fri.)

International: Bank of Japan Holds Steady, but Signals Further Normalization Ahead

- The Bank of Japan (BoJ) did not announce any new concrete policy measures at its meeting this week, but did signal the likelihood of further policy normalization ahead. The BoJ said the virtuous cycle between wages and prices is continuing to intensify, and that it would decide on a detailed plan for the reduction in the pace of its bond purchases. We also expect the BoJ to eventually hike its policy rate further, but not until the October meeting.

- Next week: China Retail Sales & Industrial Output (Mon.), Reserve Bank of Australia (Tue.), Bank of England (Thu.)

Interest Rate Watch: FOMC Maintains Its Measured Approach to Easing

- There wasn't much surprise that came out of the FOMC's June monetary policy meeting this week. The Committee left rates unchanged, and now expects higher inflation and less easing this year than previously. It remains a close call between one and two 25 bps rate cuts this year.

Topic of the Week: Idiosyncratic Risks Weigh on Latin America's Financial Markets

- This week, Latin American financial markets—particularly currency markets—came under pressure. We can point to the election surprise in Mexico as the originator of regional market volatility; however, additional policy uncertainty in countries such as Brazil and Colombia also contributed to new volatility in local markets.

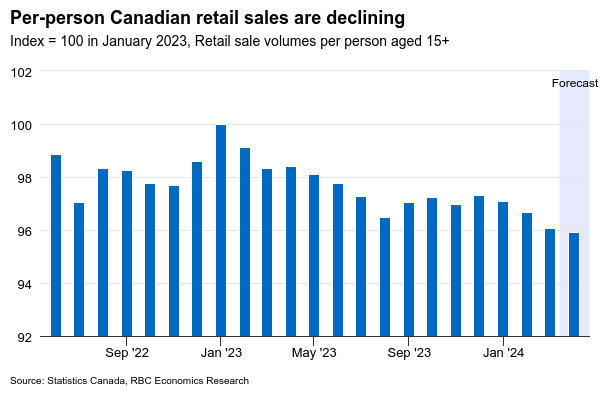

Housing and Retail Sales Data to Show Canadians Continue to Hold Back

Economic data in the week ahead should show further softening in Canadian (per-person) household spending before the Bank of Canada pivoted to lower interest rates in June.

Early reports from regional real estate boards suggested housing markets were in a holding pattern in May. Home resales edged lower in most regions including Toronto, Vancouver, and Montreal. That together with more new listings point to a rebalancing in market supply and demand, exerting more downward pressure on home prices that have largely stagnated this year.

Signs of persistent softness in housing markets could also be tied to potential buyers waiting on the sidelines for more clarity on the direction of interest rates. And housing isn’t the only spot where demand is lagging. April retail sales next Friday should also point to Canadian households continuing to cut back spending in the spring. Statistics Canada’s early estimate a month ago was for a 0.7% increase in total retail spending in April, with much of the increase likely driven by a 7% rise in gasoline prices. Auto sales also likely ticked higher from pent-up demand built up as a result of low inventories in recent years. Excluding gasoline and auto sales, “core” retail sales in Canada likely held steady in April, extending a softer trend after already having declined by an annualized 1.1% in Q1. And the volume of overall sales (excluding price impacts) likely ticked lower again on a per-person basis.

Lower interest rates from the BoC will help ease pressures on households, and our tracking of credit card transactions has pointed to higher spending on services in the spring even with inflation slowing. Still, monetary policy will remain broadly restrictive for a while, and we don’t expect a significantly rebound in per-capita consumer spending in Canada until next year.

Week ahead data watch

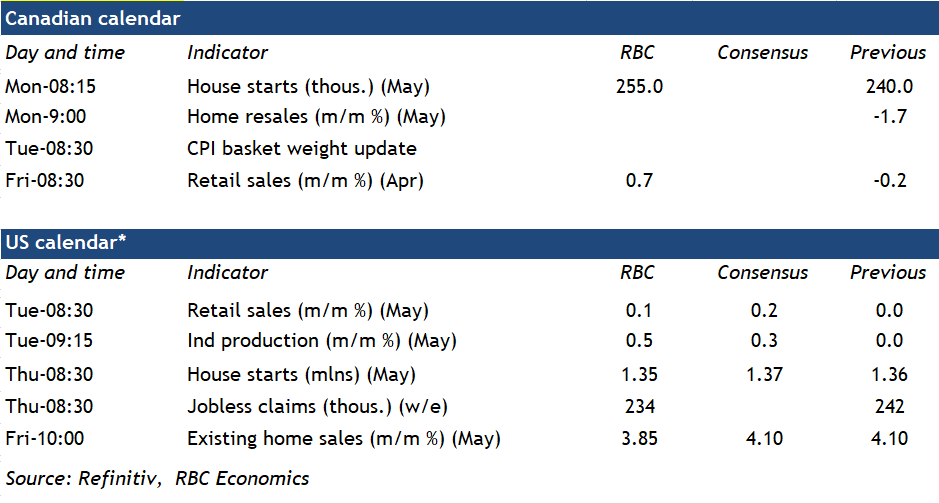

We expect Canadian housing starts to increase by 255,000 in May, given permit issuances jumped higher by 322,800 on a seasonally adjusted basis—the fastest pace increase since Dec. 2021.

On Tuesday, StatCan will release the 2024 CPI basket weights update, which reflects consumer expenditures in 2023. The new weights will account for changes in consumer spending patterns by looking at expenditure data from Household Final Consumption Expenditures, Survey of Household Spending, and alternative data sources.

U.S. retail sales likely ticked up 0.1% in May, and unit auto sales (0.8%) were up slightly, partially offsetting price-related declines in gasoline sales (seasonally adjusted gas prices were down 3% in May.)

We expect U.S. industrial production to edge up 0.5% in May, following the flat reading in April. Much of that growth was driven by higher output in the manufacturing sector, specifically higher motor vehicle production given a solid rise in hours worked in the sector.

WTI Oil Week Ahead: WTI Eyes $80 a Barrel on Demand Optimism

- WTI Oil on course for its best week in over two months.

- WTI unfazed as OPEC and IEA forecast paint differing demand pictures.

- WTI eyeing trendline break and psychological $80 a barrel mark.

Fundamental Overview and Week in Review

WTI oil prices are experiencing a resurgence this week, driven by demand optimism. This positions WTI for its best week in over two months. WTI is up 4.48% at the time of writing, with the $80 a barrel mark now firmly in sight.

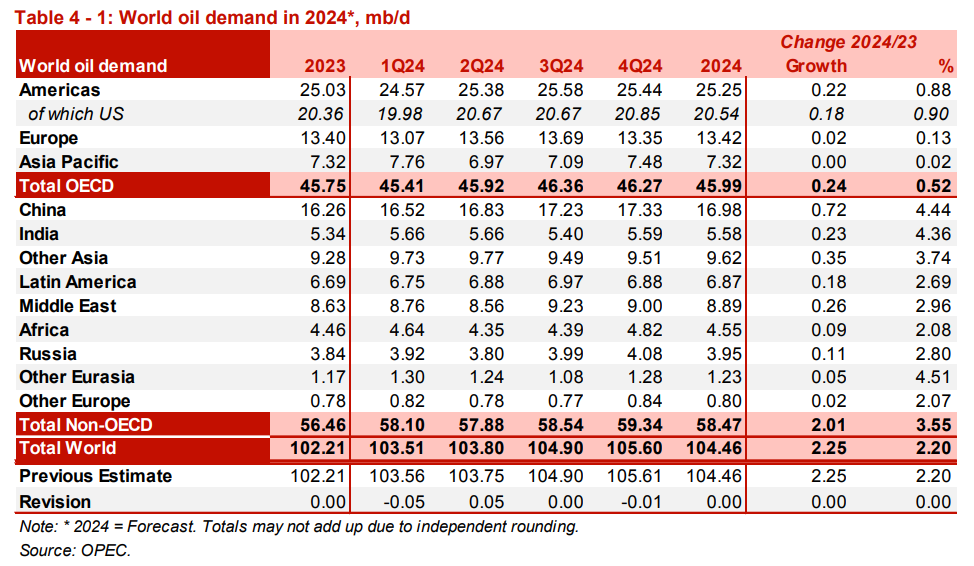

WTI prices rose in part due to OPEC maintaining its forecast for strong growth in 2024. Despite a somewhat disappointing first quarter, on Tuesday, OPEC reiterated its prediction of robust oil demand for the year, citing an improved outlook for travel and tourism in the second half of 2024. Furthermore, OPEC also cited steady global growth in the first half of 2024 with the services sector singled out as a key driver for growth to continue. This followed a Monday report by Goldman Sachs in which the investment bank stated that transport demand would push the market into a third quarter deficit.

OPEC Updated Oil Demand Forecasts as of Jun 11, 2024

Source: OPEC MOMR, June 2024

There is a lack of consensus however when it comes to demand forecasts for 2024, and this gap appears to be widening. The International Energy Agency (IEA) released its own report on Wednesday with the agency trimming its 2024 forecast down to 960k bpd. A drop of around a 100k bpd citing sluggish consumption in developed countries. This is in stark contrast to the OPEC forecast of 2.25 million bpd and the largest gap between the IEA and OPEC forecasts since 2008.

Heading into a new week with momentum and market participants will be keeping a close eye on WTI. Mixed US data saw rate cut hopes resurface post the FOMC meeting which adds another layer of confluence supporting higher oil prices. A stronger US dollar might challenge OPEC forecasts, as it could lead to higher prices for other countries (currency depreciation against the US dollar) and reduce demand.

The Week Ahead: US PMI Data and Oil Inventories

Looking ahead to next week, market participants will closely monitor whether WTI can maintain its recent rally. With a lighter economic calendar, the US PMI data on Friday may trigger some reactions, especially in light of OPEC’s comments. Since the US is primarily a service-driven economy, this data will offer insights into OPEC’s optimism regarding travel, tourism, and service sectors contributing to global growth in the second half of 2024.

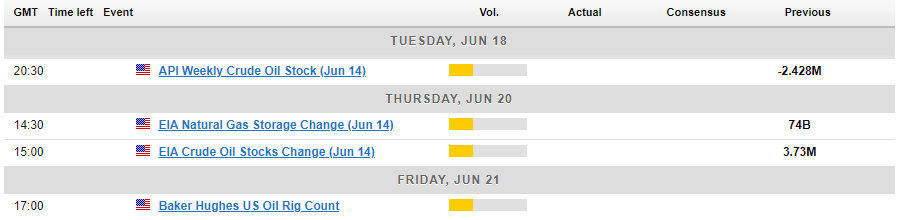

Other key events include US retail sales data on Tuesday with API and EIA crude oil data to be released on Tuesday and Thursday, respectively. If inventories are on the decline, it could signal a busy summer of travel in the US and boost optimism that WTI may continue to rise. Geopolitics should also be monitored as hostilities between Hezbollah and the IDF continue to intensify in norther Israel. Any sign of an Israeli offensive into Lebanon or further attacks by Hezbollah threaten a spillover in the region, something which could add a risk premium to oil prices moving forward.

WTI Oil Technical Outlook

Looking at WTI Oil from a technical perspective, the weekly chart is on course for a massive bullish engulfing candle close, off a key support level while at the same time printing a morningstar candlestick formation. All of the above hinting at a bullish continuation in the week ahead.

Dropping down to the daily timeframe chart and price appears to be flirting with a break of the descending trendline which is in play, another sign of bulls taking control. There is a just reason to approach with caution as just above the current price we have both the 100 and 200-day MAs resting around the 79.50 handle with the 80.00 psychological level the next resistance area. In simple words, there are a lot of hurdles for WTI to overcome if it is to find acceptance above the $80 a barrel mark.

Source: TradingView.Com

Key Levels to Consider:

Support:

- 77.90

- 76.40

- 75.00 (Psychological Level)

Resistance:

- 79.50

- 80.00 (Psychological Level)

- 82.03