Sample Category Title

Japanese Yen Fell to a Six-Week Low after Bank of Japan Ended Its Meeting

The Japanese yen exchange rate paired with the US dollar looks unimpressive by the end of this week. The USD/JPY pair rose to almost 158.00 immediately after the end of the June meeting of the Bank of Japan, which left the interest rate unchanged. Everything went according to expectations.

In March, the BoJ raised the rate for the first time in seven years, moving it from negative territory to zero.

In its comments, the regulator noted that it will continue to buy Japanese government bonds at the same pace as agreed in March until its July meeting. Thus, market expectations were ignored, which worked against the JPY. Investors hoped that the BoJ would at least carefully consider gradually reducing its balance sheet through government bonds as part of a smooth monetary policy transition from quantitative easing to tightening.

Previously, Bank of Japan Governor Kazuo Ueda confirmed the regulator's intention to gradually reduce its substantial balance sheet in the future. However, the timing of this action remains uncertain.

USD/JPY Technical Analysis

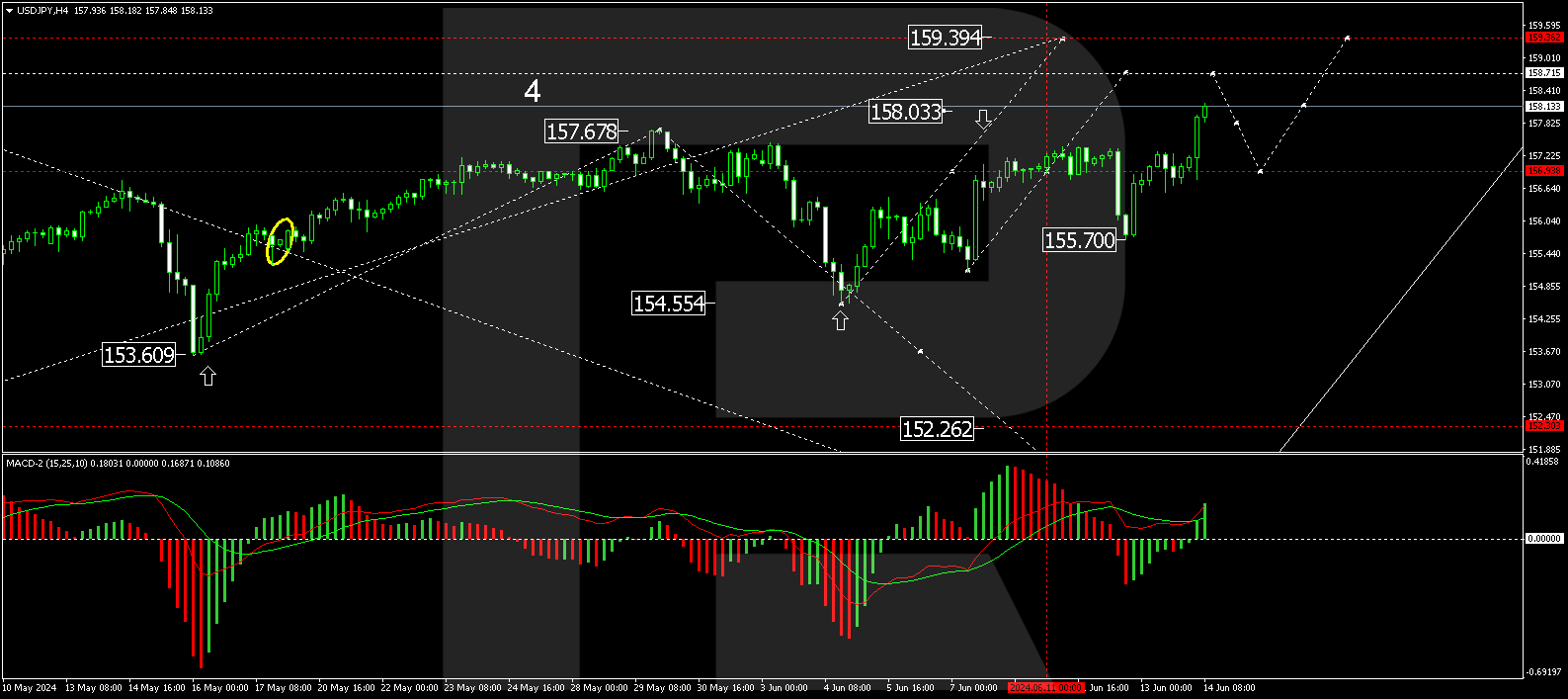

On the H4 USD/JPY chart, the market has breached 157.47 upwards and is continuing to develop a growth wave towards 158.74. After reaching this level, a correction down to the level of 157.47 is a possibility (test from above). We will then assess the probability of continuing the growth wave to 159.36. Technically, this scenario is supported by the MACD indicator, with its signal line above the zero level and pointing upwards.

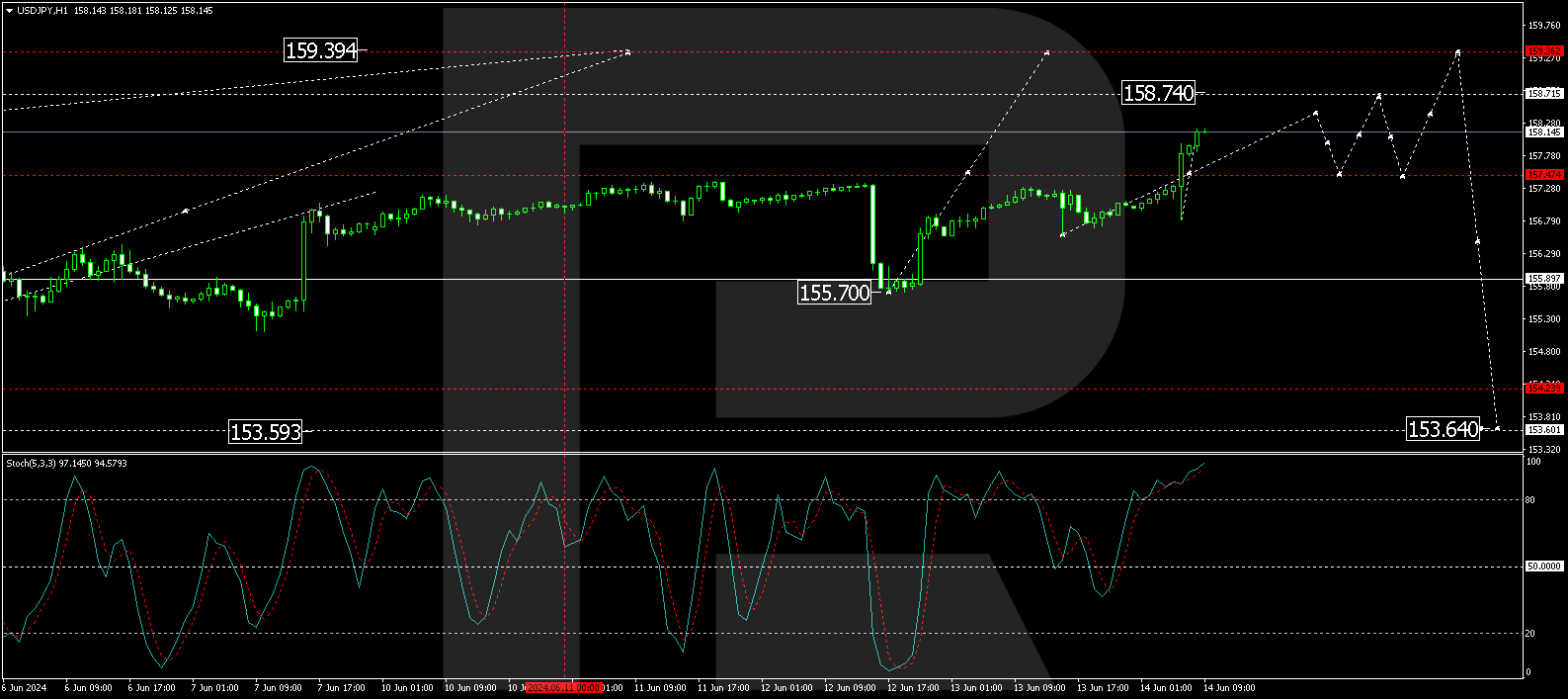

On the H1 USD/JPY chart, the market continues to develop a wave of growth to the level of 158.40. Further, a correction wave to 157.47 is possible, followed by growth to 158.74, the local target. Technically, this scenario is confirmed by the Stochastic oscillator, with its signal line above level 80 and preparing to decline to level 20.

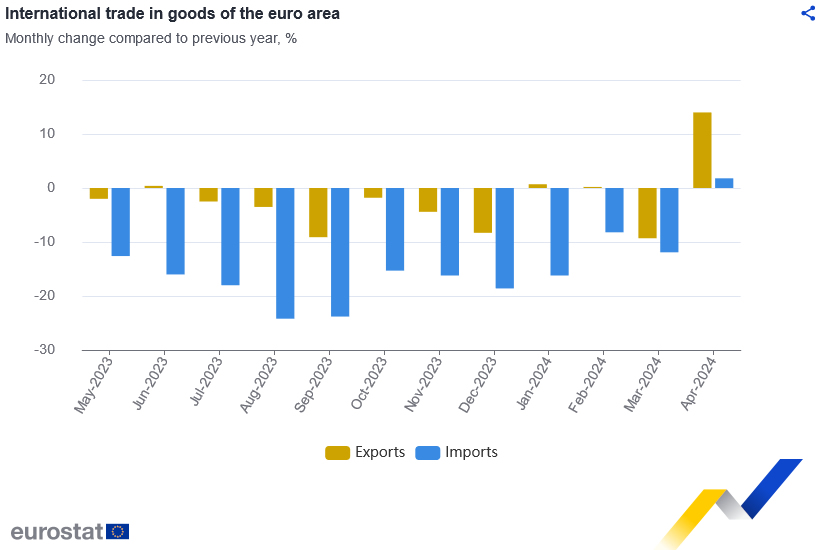

Eurozone exports rises 14.0% yoy, imports up 1.8% yoy in Apr

Eurozone goods exports rose 14.0% yoy to EUR 247.6B in April. Goods imports rose 1.8% yoy to EUR 232.5B. Trade balance showed EUR 15.0B surplus. Intra-Eurozone trade rose 5.8% yoy to EUR 222.89B.

In seasonally adjusted term, goods exports rose 3.1% mom to EUR 245.3B. imports rose 2.3% mom to EUR 225.9B. Trade balance reported EUR 19.4B surplus, above expectation of EUR 17.0B. Intra-Eurozone trade rose 1.5% mom to EUR 217.7B.

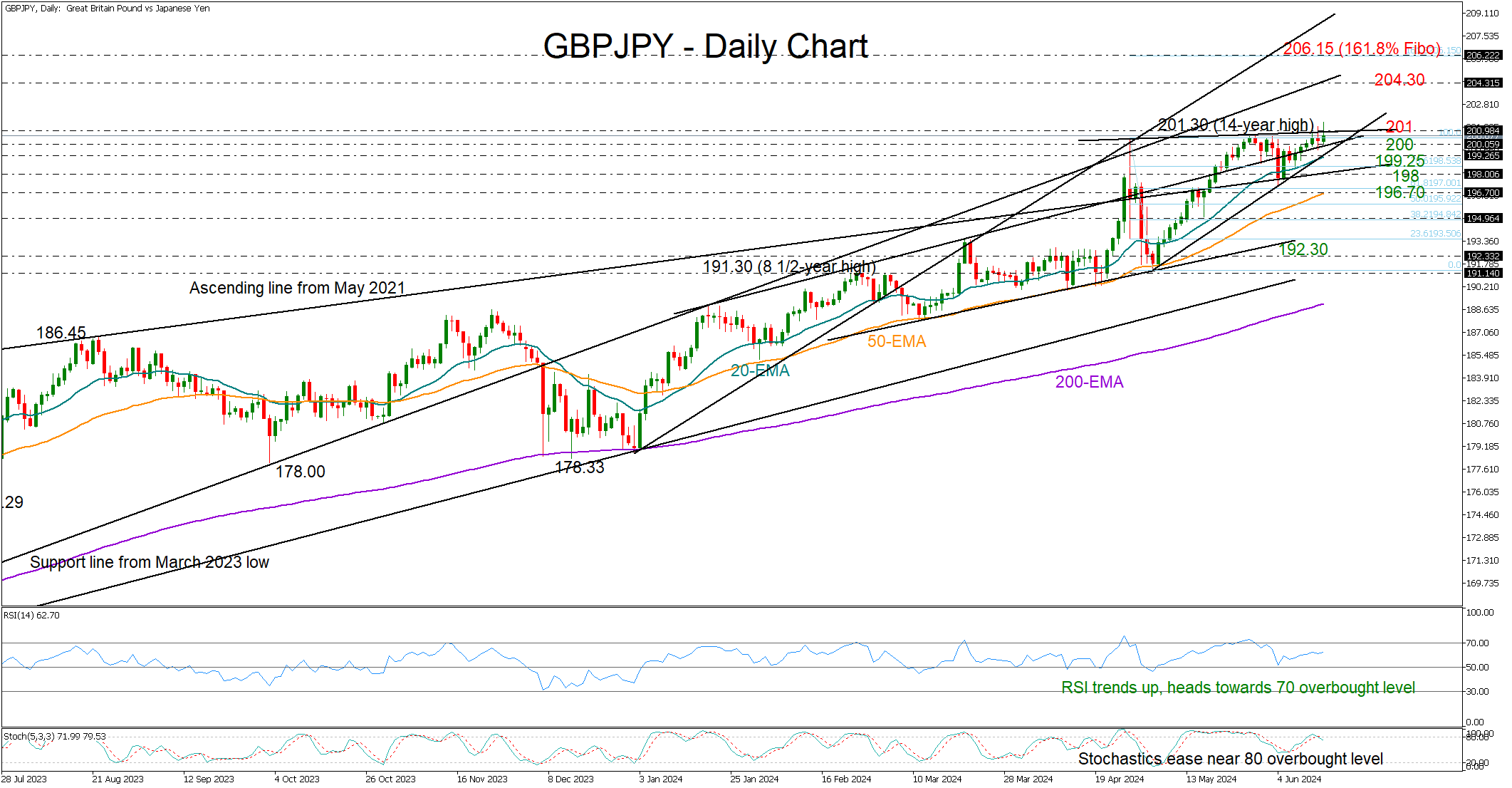

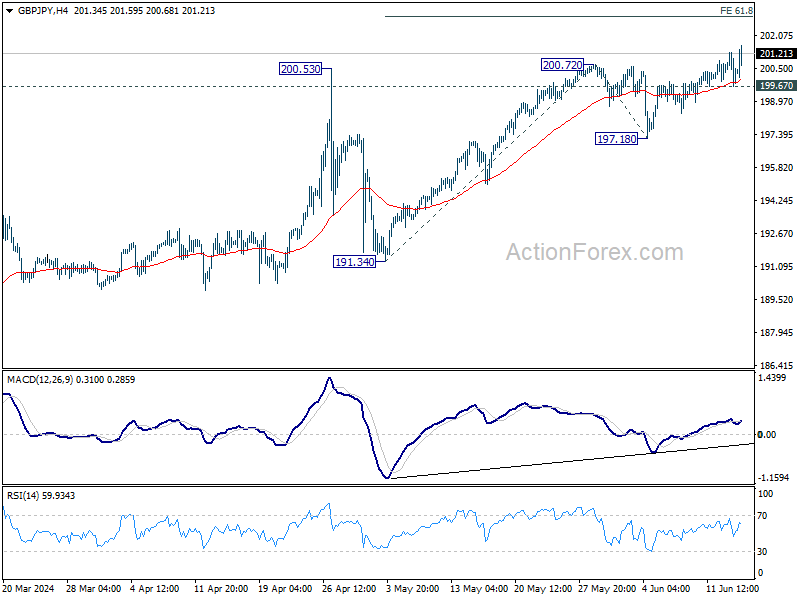

GBPJPY Bounces to 14-Year High; Eyes on 201 Resistance

- GBPJPY unlocks a new high after the Bank of Japan defies expectations of reduced bond purchases

- Technical signs are positive, but the bulls need to breach the 201 obstacle

GBPJPY stepped on the long-term ascending line at 200 and jumped to a new 14-year high of 201.59 in the BoJ aftermath on Friday with scope to continue its long-term positive trend.

The short-term risk is more on the upside than on the downside. Specifically, the exponential moving averages (EMAs) are sloping upwards, promoting the bullish trajectory in the market. In technical indicators, the RSI keeps strengthening above its 50 neutral mark and towards its 70 level, although the stochastic oscillator is already hovering near its 80 overbought level.

Buyers would like to see a clear close above the 201 number in order to stage an exciting rally towards the constraining line from March 2023 at 204.30. Even higher, the pair could target the 161.8% Fibonacci extension of May’s downfall at 206.15.

Alternatively, a pullback could retest the 200 level and perhaps seek support near the 20-day EMA at 190.25 before heading for the key 198.00 area. If a slide occurs below the latter, it could indicate a bearish reversal and potentially lead to a sharp correction towards the 50-day EMA at 196.70.

In summary, GBPJPY remains bullish in the short-term, and traders are looking for a close above 201 to drive additional buying.

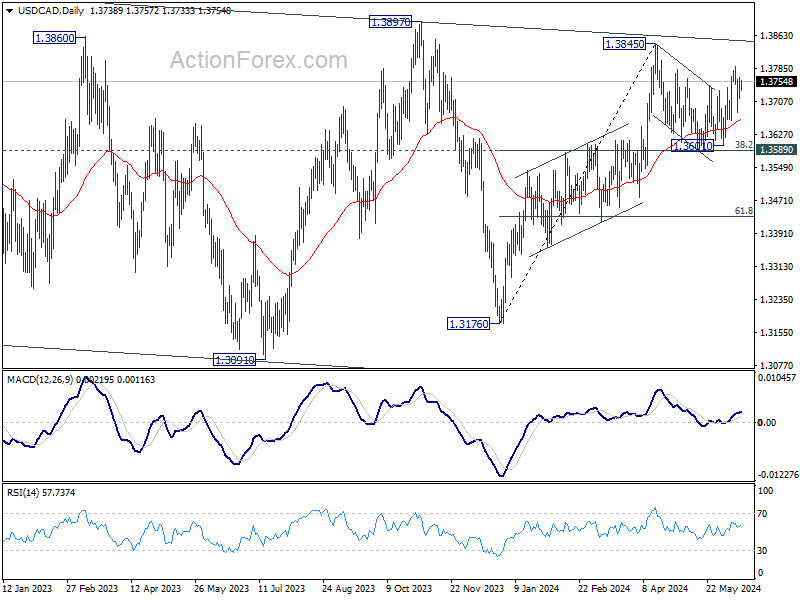

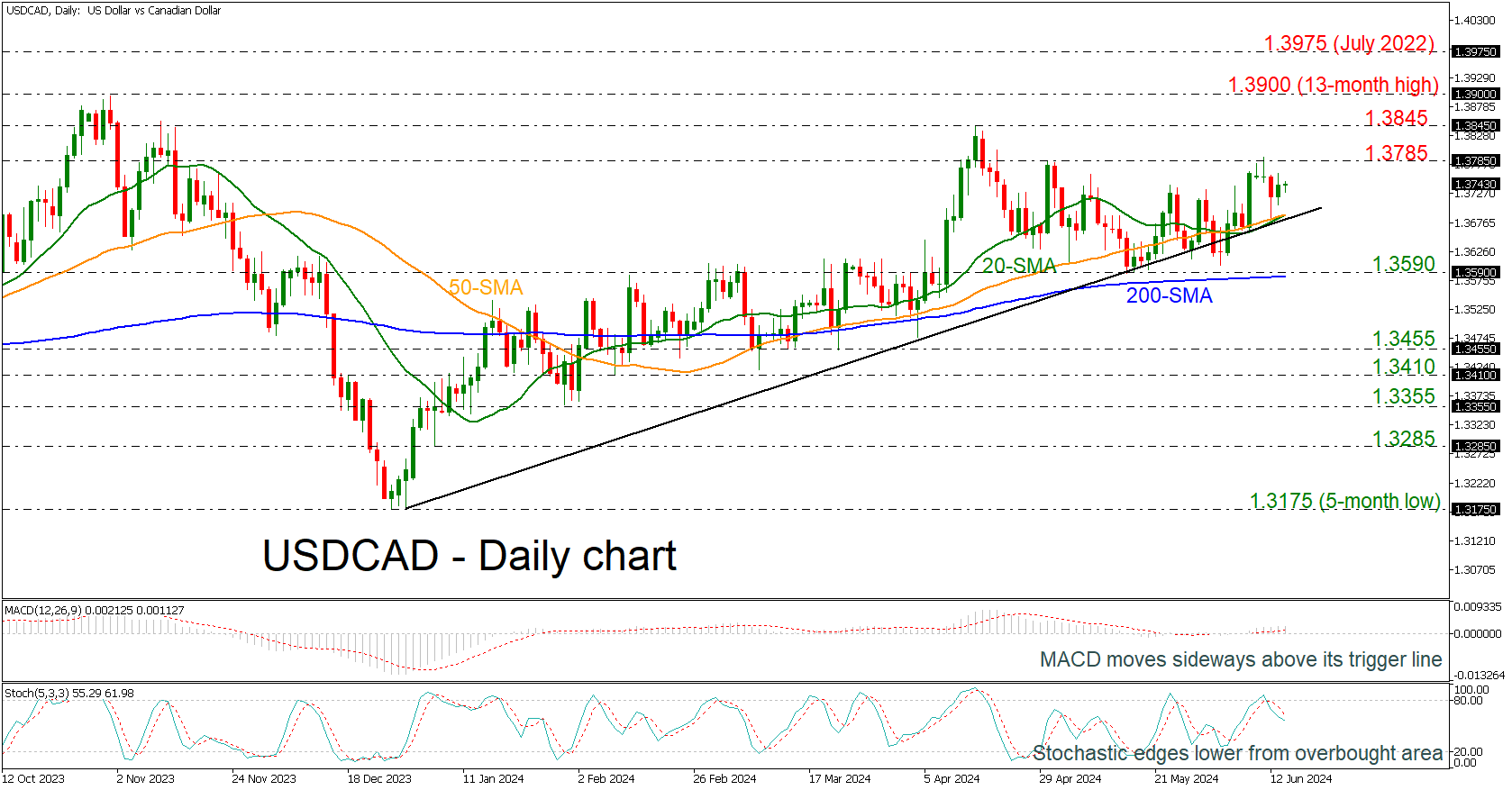

USDCAD Remains Bullish With Weak Momentum

- USDCAD fails to extend above 1.3785

- Stochastics suggest bearish retracement

USDCAD is still developing above the short-term simple moving averages (SMAs), which are ready for a bullish crossover, and above the medium-term uptrend line.

Technically, the MACD oscillator is moving sideways above the zero level; however, the stochastic oscillator is indicating a negative movement as it posted a bearish cross with %K and %D lines in the overbought region.

If there are some negative retracements, immediate support could come from the uptrend line at 1.3685 ahead of the strong 200-day SMA near the 1.3590 barrier. A dive beneath this obstacle could switch the bias to a more bearish one, hitting 1.3455.

On the other hand, a climb beyond the 1.3785 resistance could meet immediate resistance at 1.3845 before challenging the 13-month peak of 1.3900. Even higher, the July 2022 top at 1.3975 could endorse the longer-term bullish structure.

All in all, USDCAD is showing some signs of weakening momentum, but the broader outlook remains positive.

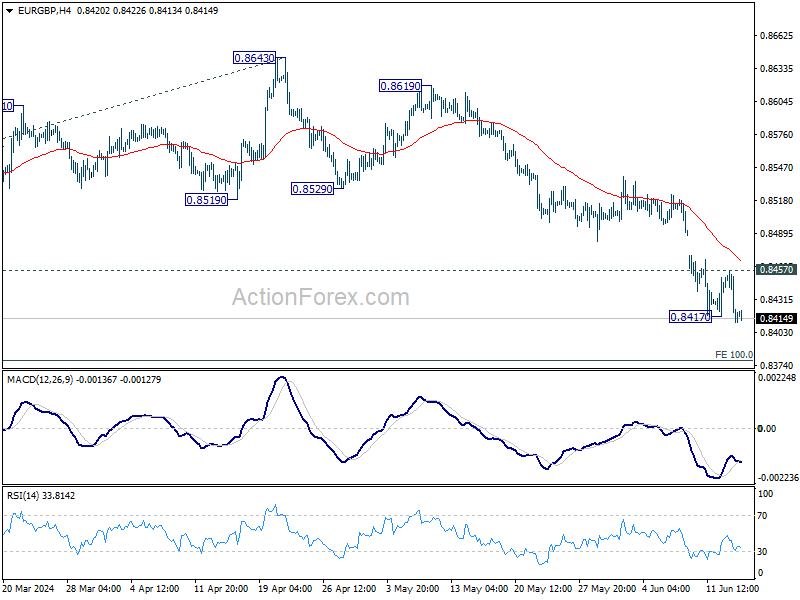

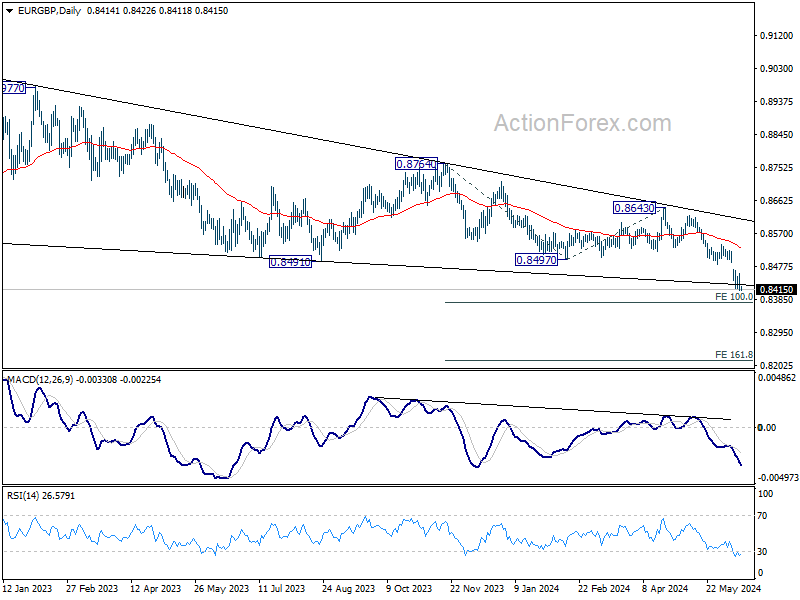

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8399; (P) 0.8428; (R1) 0.8444; More...

EUR/GBP's fall resumed after brief recovery and intraday bias is back on the downside. Current down trend should target 0.8376 projection level next. For now, risk will remain on the downside as long as 0.8457 resistance holds, in case of another recovery.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 100% projection of 0.8764 to 0.8497 from 0.8643 at 0.8376. Sustained break there will target 161.8% projection at 0.8211 next. For now, outlook will remain bearish as long as 0.8643 resistance holds, even in case of stronger rebound.

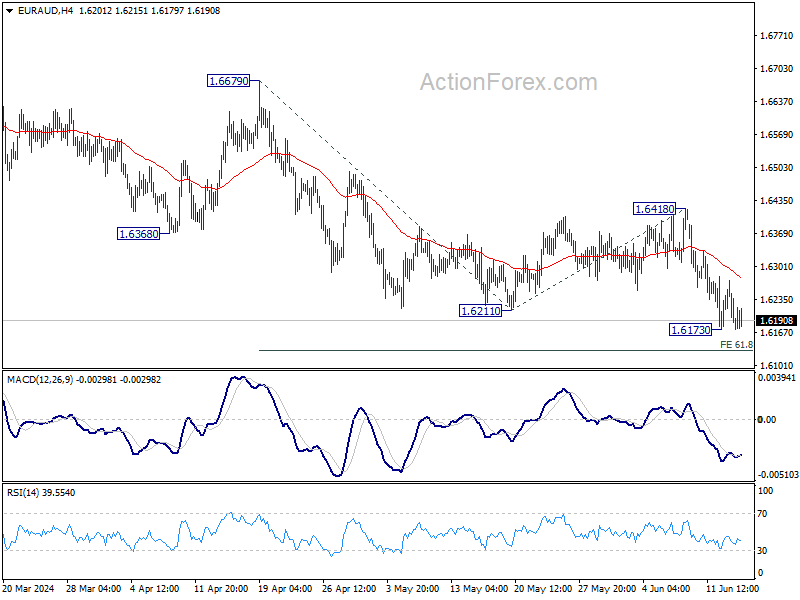

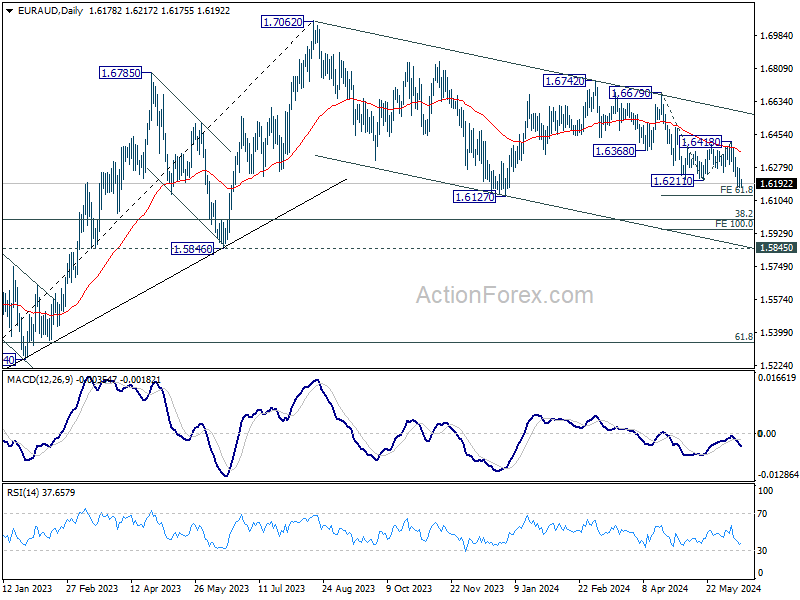

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6146; (P) 1.6210; (R1) 1.6245; More...

Intraday bias in EUR/AUD remains neutral at this point, and outlook stays bearish with 1.6418 resistance intact. On the downside, break of 1.6173 will resume the decline from 1.6742, as the third leg of the correction from 1.7062. Next target is 61.8% projection of 1.6679 to 1.6211 from 1.6418 at 1.6129.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). In case of deeper fall, strong support is expected around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound. Break of 1.7062 is in favor as a later stage.

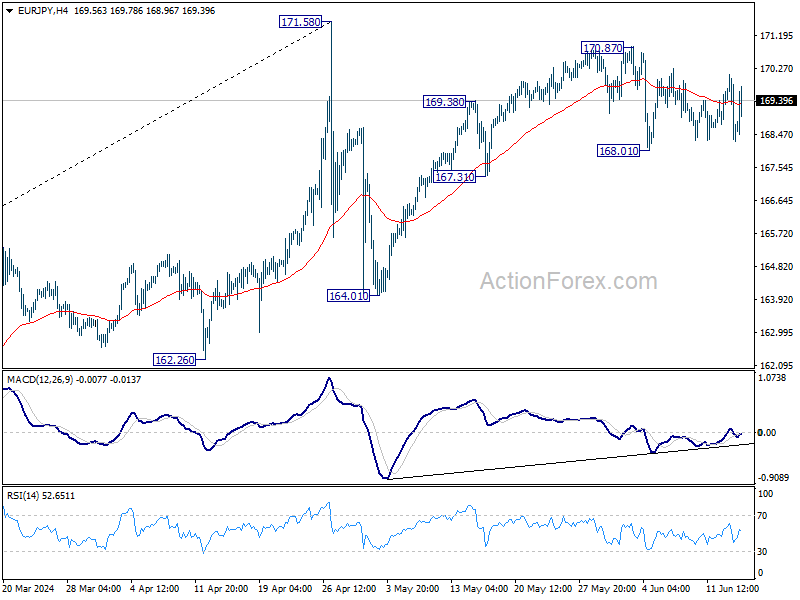

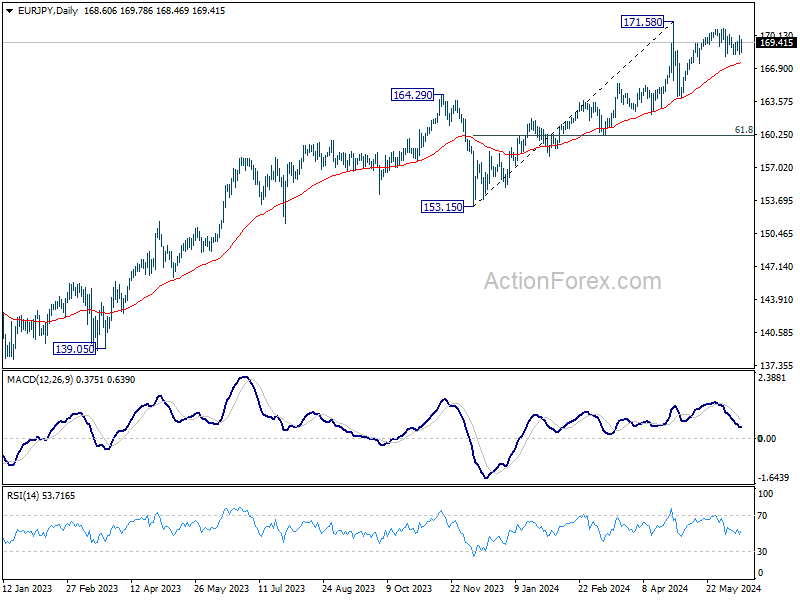

EUR/JPY Daily Outlook

Daily Pivots: (S1) 167.88; (P) 169.01; (R1) 169.74; More...

EUR/JPY is still bounded in sideway trading and intraday bias remains neutral. On the downside, break of 168.01 support will strengthen the case that rise from 164.31 has completed at 170.78 already. Intraday bias will be back on the downside for 167.31 support, and then 164.01. Nevertheless, break of 170.87 will resume the rally to retest 171.58 high instead.

In the bigger picture, a medium top was formed at 171.58 after brief breach of 169.96 (2008 high). But as long as 55 W EMA (now at 159.51) holds, price actions from there is seen as correcting the rise from 153.15 only. That is, larger up trend remains in favor to continue. However, sustained break of 55 W EMA will argue that larger scale correction is underway and target 153.15 support.

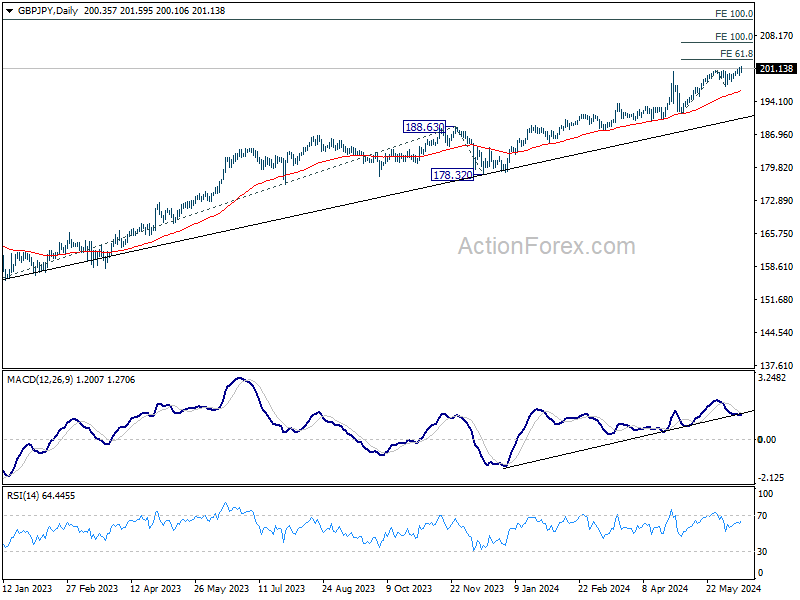

GBP/JPY Daily Outlook

Daily Pivots: (S1) 199.62; (P) 200.47; (R1) 201.25; More...

While upside moment isn't too unconvincing, intraday bias in GBP/JPY stays on the upside for now. Current up trend should target Next target is 61.8% projection of 191.34 to 200.72 from 197.18 at 202.97. On the downside, below 199.67 minor support will turn intraday bias neutral and bring consolidations first, before staging another rally.

In the bigger picture, as long as 188.63 resistance turned support holds, long term up trend is expected to continue. Next target is 100% projection of 155.33 to 188.63 from 178.32 at 211.62.

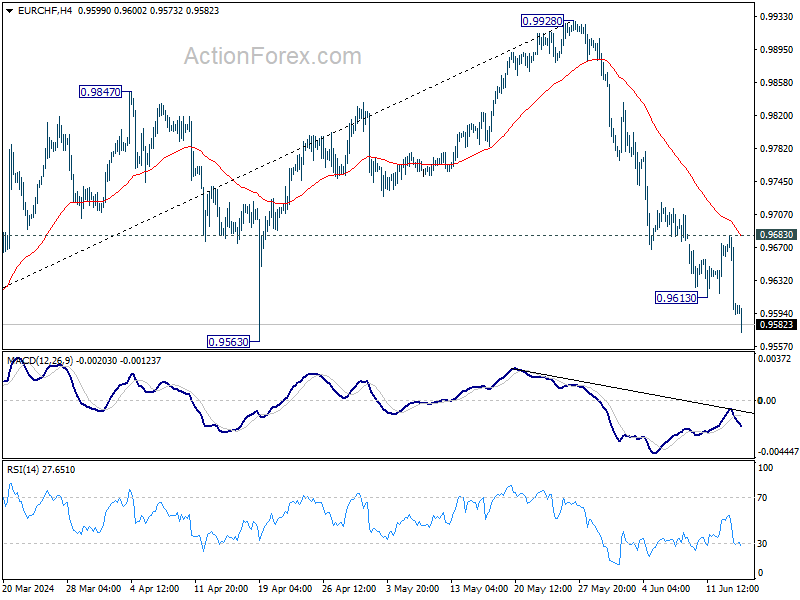

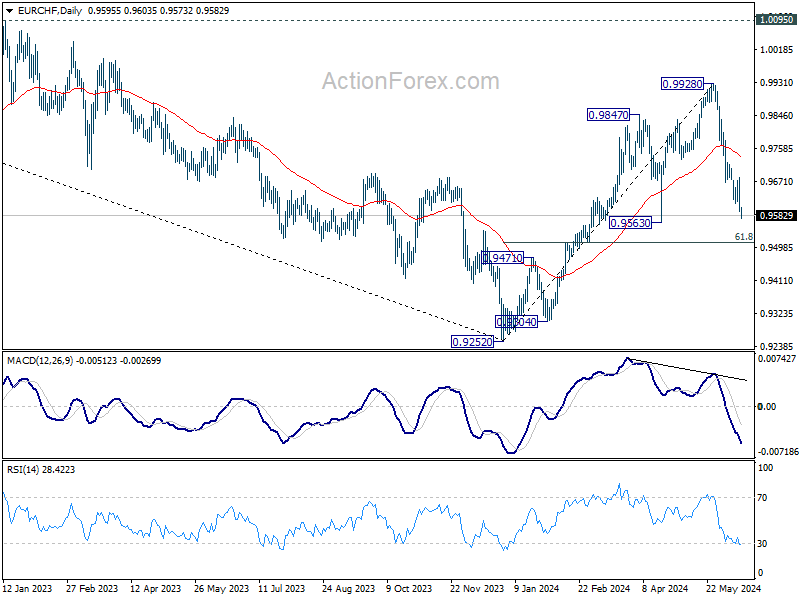

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9568; (P) 0.9626; (R1) 0.9658; More....

EUR/CHF's fall from 0.9928 resumed after brief recovery and intraday bias is back on the downside for 0.9563 support. Decisive break there will argue that whole rise from 0.9252 has completed, and bring deeper fall to 61.8% retracement of 0.9252 to 0.9928 at 0.9510. For now, risk will stay on the downside as long as 0.9683 resistance holds, in case of recovery.

In the bigger picture, as long as 0.9563 support holds, rise from 0.9252 medium term bottom is still in favor to continue. Next target is 38.2% retracement of 1.2004 (2018 high) to 0.9252 (2023 low) at 1.0303, even just as a correction to the down trend from 1.2004. However, firm break of 0.9563 will suggest that the rally has completed and retain medium term bearishness.

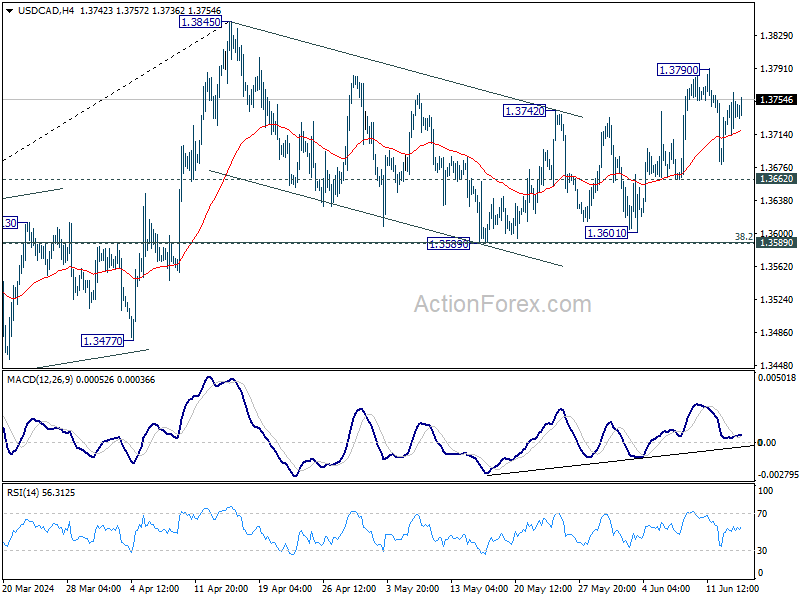

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3711; (P) 1.3738; (R1) 1.3765; More...

Intraday bias in USD/CAD remains neutral and further rise is in favor with 1.3662 support intact. On the upside, above 1.3790 will resume the rebound from 1.3589 to retest 1.3845 high. Firm break there will resume larger rally. Nevertheless, break of 1.3662 will turn bias to the downside to extend the corrective pattern from 1.3845 with another falling leg.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.