Sample Category Title

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2733; (P) 1.2796; (R1) 1.2862; More...

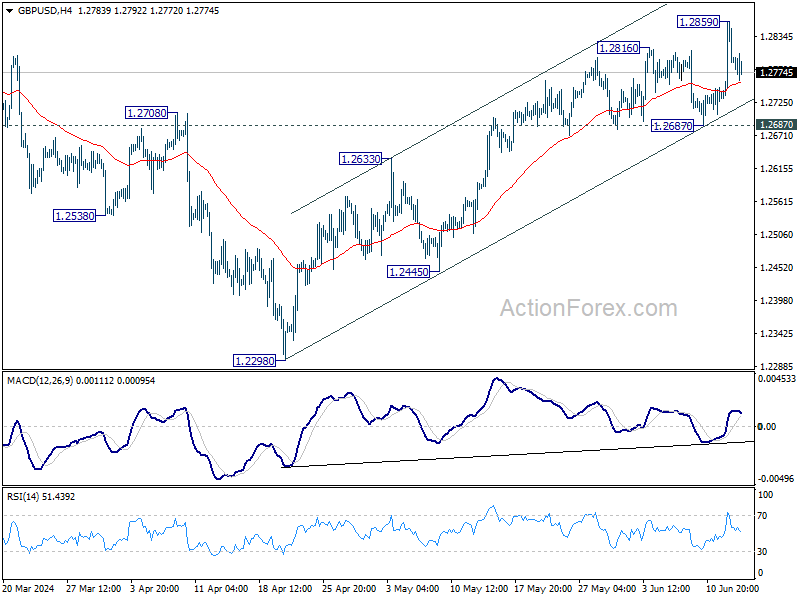

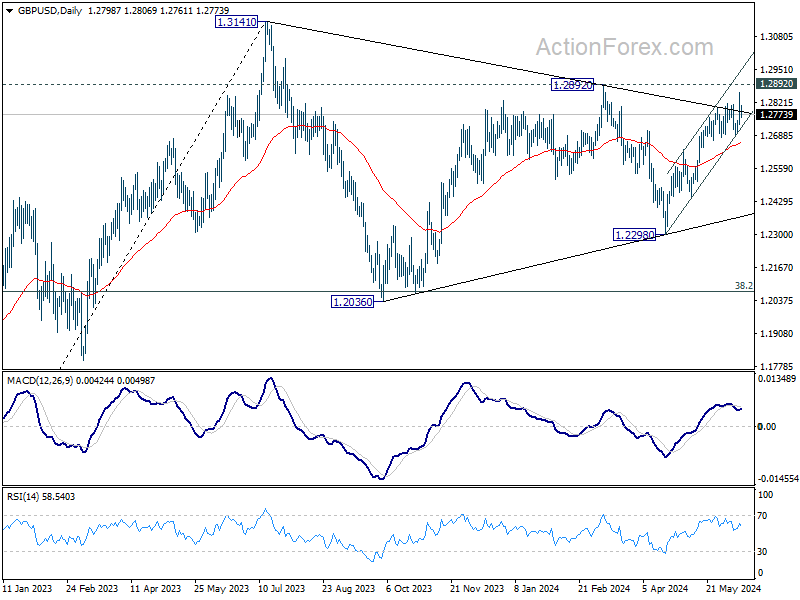

Intraday bias in GBP/USD is turned neutral first but further rally is expected as long as 1.2687 support holds. Above 1.2869 will target 1.2892 resistance. Decisive break there will strengthen the case that correction from 1.3141 has completed, and bring further rally to retest this high.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2445 support will extend the corrective pattern with another decline instead.

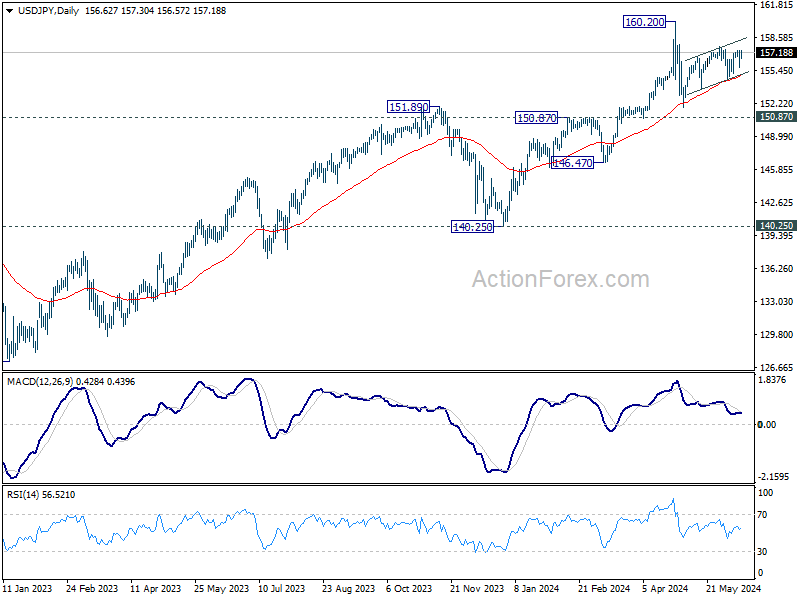

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 155.84; (P) 156.61; (R1) 157.49; More...

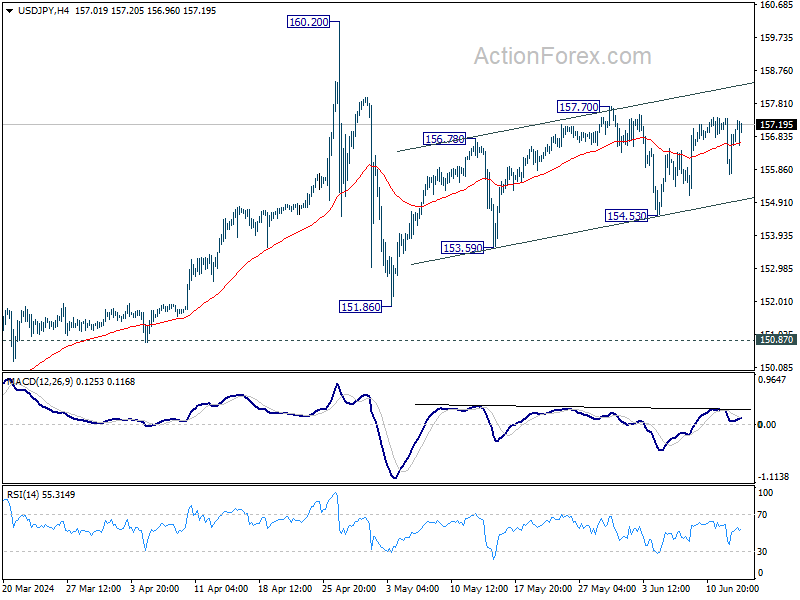

No change in USD/JPY's outlook as range trading continues. Intraday bias remains neutral. On the downside, break of 154.53 will turn bias to the downside for 151.86 support and possibly below, as the third leg of the corrective pattern from 160.20. On the upside, break of 157.70 will resume the whole rise from 151.86 and target 160.20 high.

In the bigger picture, a medium term top should be formed at 160.20. As long as 55 W EMA (now at 147.77) holds, fall from 160.20 is seen as correcting the rise from 140.25 only. However, sustained break of 55 W EMA will argue that larger correction is possibly underway, and target 146.47 support next.

Aussie Shrugs After Strong Employment Data

The Australian dollar has edged lower on Thursday. AUD/USD is trading at 0.6674 in the North American session, up 0.14% on the day. The Aussie didn’t show much reaction to today’s solid Australian employment report.

Australian employment beats forecasts

Australia’s economy has been slowing but the May employment report indicated that the labor market remains robust despite the uncertain economic landscape. The economy added 39.7 thousand jobs, above the revised gain of 37.4 thousand in April and the market estimate of 30 thousand. Full-time employment surged with a gain of 41.7 thousand, after two soft months. The unemployment rate dipped to 4.0%, down from 4.1%.

Today’s employment report is the final tier-1 event before the Reserve Bank of Australia meets on June 14th. The RBA has kept rates unchanged at 4.35% for six straight times and is expected to hold rates again next week. The central bank remains concerned about inflation, which has proven to stubborn and rose unexpectedly in April to 3.6%, up from 3.5%.

The Reserve Bank remains hawkish and has warned that it could raise rates if inflation continued to rise. A rate hike is an unlikely scenario but the message from the RBA is that inflation is too high and rate cuts will be delayed, perhaps until early 2025.

US inflation lower than expected

US inflation decelerated in May, raising hopes that inflationary pressures will continue to decline. The headline figure fell from 3.4% to 3.3% and core CPI dropped to 3.4%, down from 3.6%. The inflation release did not have a significant impact on rate cut expectations, with the markets currently pricing in quarter-point cut in September at 57%, according to the CME’s FedWatch.

AUD/USD Technical

- AUD/USD tested support at 0.6655 earlier. Below, there is support at 0.6605

- 0.6713 and 0.6763 are the next resistance lines

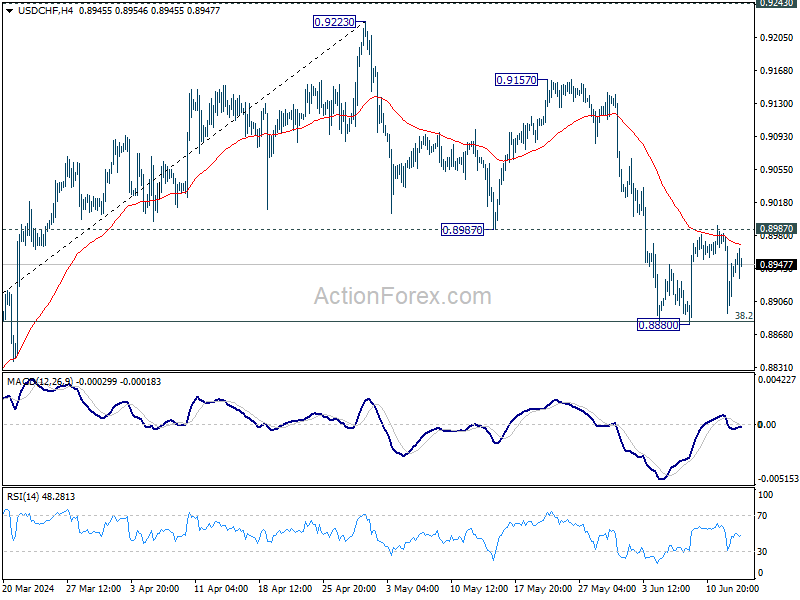

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8897; (P) 0.8940; (R1) 0.8988; More….

No change in USD/CHF's outlook as range trading continues. Intraday bias remains neutral. On the downside, sustained break of 0.8883 fibonacci level will carry larger bearish implications and bring deeper decline. On the upside, firm break of 0.8987 support turned resistance will argue that correction from 0.9223 has completed, after drawing support from 0.8883 fibonacci level. Intraday bias will be back on the upside for 0.9157/9223 resistance zone.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

Dollar’s Rebound Stalls Amid Weak PPI and Jobless Claims; Focus Shifts to BoJ

Trading activity slowed notably today as the markets turned relatively quiet. Dollar attempted a rebound from its losses earlier this week but struggled to gain momentum after worse-than-expected PPI and jobless claims data. Despite being one of the weaker performers this week, Dollar has managed to stay above last week's lows against all major currencies. The brief breakout against British Pound also quickly reversed, bringing Dollar back within its established range.

Japanese Yen has been the weakest performer this week. Attention now shifts to the upcoming BoJ monetary policy decision. While no changes in interest rates are anticipated, there is speculation that BoJ may begin tapering its monthly purchases of JGBs. Due to opposition from some BoJ board members, BoJ might only offer vague language about reduction in future bond buying rather than a detailed plan.

In the broader forex market, Euro is currently the third weakest performer. New Zealand Dollar continues to lead as the strongest currency, followed by Australian Dollar and British Pound. Swiss Franc and Canadian Dollar are positioned in the middle.

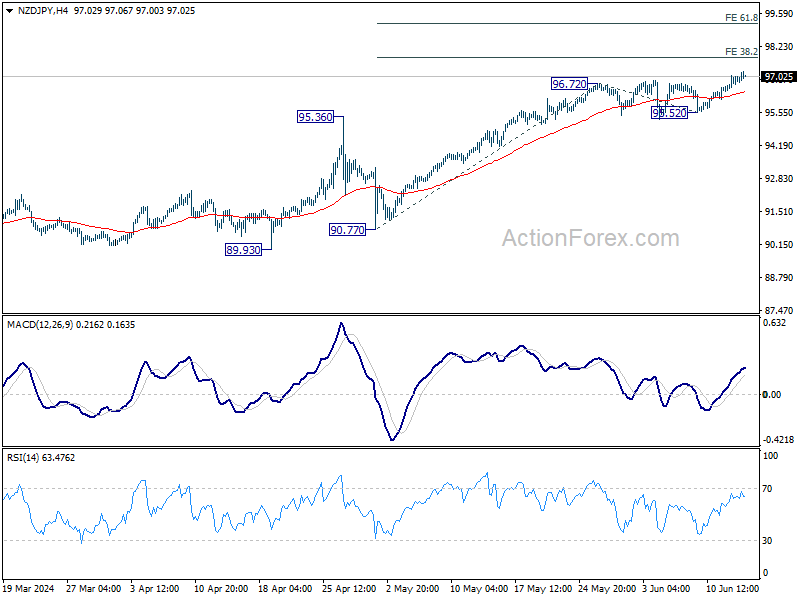

Technically, NZD/JPY's up trend resumes this week and further rise is now expected to 38.2% projection of 90.77 to 96.72 from 95.52 at 97.79. Considering overall sluggishness in Yen's decline, NZD/JPY's upside could be capped by 97.79 on first attempt. Nevertheless, firm break there would pave the way to 61.8% projection at 99.19 next.

In Europe, at the time of writing, FTSE is down -0.36%. DAX is down -1.155%. CAC is down -1.25%. UK 10-year yield is up 0.0297 at 4.161. Germany 10-year yield is up 0.0008 at 2.532. Earlier in Asia, Nikkei fell -0.40%. Hong Kong HSI rose 0.97%. China Shanghai SSE fell -0.28%. Singapore Strait Times rose 0.52%. Japan 10-year JGB yield fell -0.0174 to 0.972.

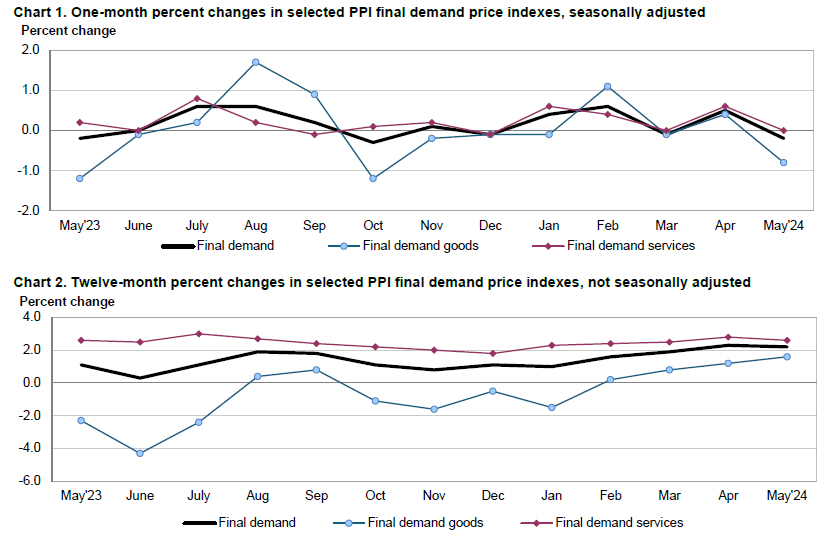

US PPI at -0.2% mom, 2.2% yoy in May.

US PPI for final demand fell -0.2% mom in May, below expectation of 0.2% mom rise. PPI goods fell -0.8% mom, largest decline since October 2023. PPI energy fell -4.8% mom. PPI food fell -0.1% mom while PPI ex food and energy rose 0.3% mom. PPI services was unchanged. PPPI less foods, energy, and trade services was also unchanged.

For the 12-month period, PPI rose 2.2% yoy, matched expectations. final demand less foods, energy, and trade services rose 3.2% yoy.

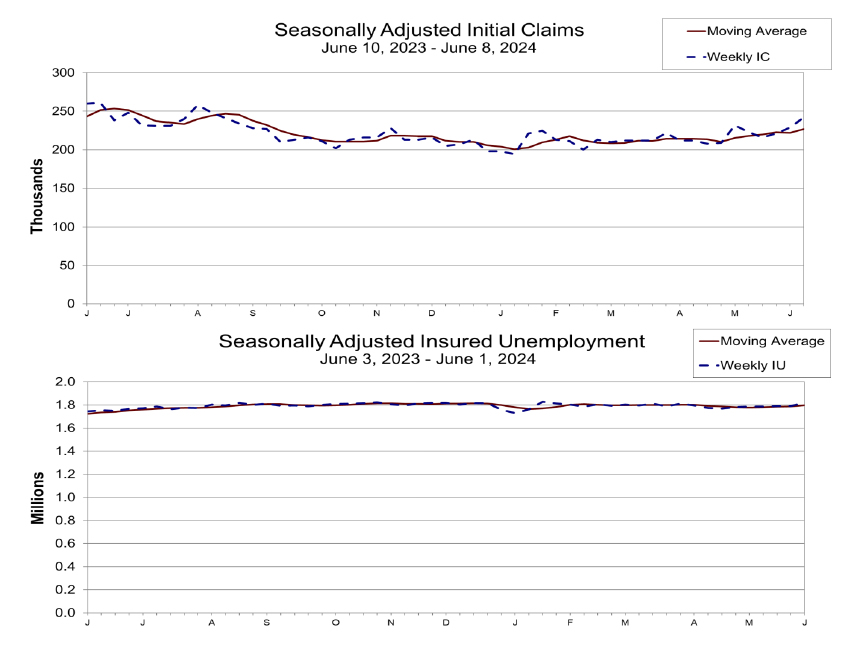

US initial jobless claims jump to 242k, vs exp 227k

US initial jobless claims rose 13k to 242k in the week ending June 8, above expectation of 227k. Four-week moving average of initial claims rose 5k to 222k.

Continuing claims rose 30k to 1820k in the week ending June 1. Four-week moving average of continuing claims rose 8.5k to 1797k.

Eurozone industrial production down -0.1% mom in Apr, EU up 0.5% mom

Eurozone industrial production fell -0.1% mom in April, worse than expectation of 0.1% mom growth. Industrial production, decreased by -0.4% for intermediate goods. Production increased by by 0.4% for energy, 0.7% for capital goods, 0.3% for durable consumer goods, and 3.4% for non-durable consumer goods.

EU industrial production rose 0.5% mom. The highest monthly increases were recorded in Denmark (+10.4%), Greece (+7.0%) and Poland (+6.7%). The largest decreases were observed in Luxembourg (-6.7%), Latvia (-4.9%) and Ireland (-3.4%).

ECB's Vasle: Further rate cuts possible this year if data remains favorable

ECB Governing Council member Bostjan Vasle has hinted at the possibility of further rate cuts this year, provided the baseline scenario holds and economic data supports such a move.

Speaking to Finance newspaper, Vasle said, "If the baseline scenario is realized and the data are favorable, then we can probably expect further rate cuts already this year, and then also next year."

However, he cautioned that if the economic conditions are not as supportive, it would be prudent to "wait some more time with further steps."

Vasle also highlighted several risks that could slow down the disinflation process, pointing to "relatively strong" momentum in wages, ongoing economic growth, and geopolitical uncertainties. These factors could impact the ECB's decision-making process regarding future rate cuts.

Australia's employment rises 39.7k, labor market remains relatively tight

Australia's labor market demonstrated resilience in May, with employment increasing by 39.7k, slightly surpassing expectations of 39.0k. Full-time jobs saw a significant rise of 41.7k, while part-time jobs experienced a slight decline of -2.1k.

Unemployment rate decreased from 4.1% to 4.0%, aligning with market forecasts. Key labor metrics, such as the employment-to-population ratio and the participation rate, remained steady at 64.1% and 66.8%, respectively. However, monthly hours worked dipped by -0.5% on a month-over-month basis.

Bjorn Jarvis, ABS head of labor statistics, highlighted that the number of unemployed people, though nearing 600k, is still about 110k fewer than in March 2020, before the pandemic.

Additionally, both the employment-to-population ratio and participation rate are significantly higher than pre-pandemic levels. Jarvis pointed out that these factors, along with sustained high job vacancy levels, indicate that the labor market "remains relatively tight, though less so than in late 2022 and early 2023."

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8897; (P) 0.8940; (R1) 0.8988; More….

No change in USD/CHF's outlook as range trading continues. Intraday bias remains neutral. On the downside, sustained break of 0.8883 fibonacci level will carry larger bearish implications and bring deeper decline. On the upside, firm break of 0.8987 support turned resistance will argue that correction from 0.9223 has completed, after drawing support from 0.8883 fibonacci level. Intraday bias will be back on the upside for 0.9157/9223 resistance zone.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | RICS Housing Price Balance May | -17% | -5% | -5% | -7% |

| 23:50 | JPY | BSI Large Manufacturing Index Q2 | -1 | -5.2 | -6.7 | |

| 01:30 | AUD | Employment Change May | 39.7K | 39.0K | 38.5K | 37.4K |

| 01:30 | AUD | Unemployment Rate May | 4.00% | 4.00% | 4.10% | |

| 06:30 | CHF | PPI M/M May | -0.30% | 0.50% | 0.60% | |

| 06:30 | CHF | PPI Y/Y May | -1.80% | -1.80% | ||

| 09:00 | EUR | Eurozone Industrial Production M/M Apr | -0.10% | 0.10% | 0.60% | 0.50% |

| 12:30 | USD | PPI M/M May | -0.20% | 0.20% | 0.50% | |

| 12:30 | USD | PPI Y/Y May | 2.20% | 2.20% | 2.20% | 2.30% |

| 12:30 | USD | PPI Core M/M May | 0.00% | 0.30% | 0.50% | |

| 12:30 | USD | PPI Core Y/Y May | 2.30% | 2.30% | 2.40% | |

| 12:30 | USD | Initial Jobless Claims (Jun 7) | 242K | 227K | 229K | |

| 14:30 | USD | Natural Gas Storage | 75B | 98B |

US initial jobless claims jump to 242k, vs exp 227k

US initial jobless claims rose 13k to 242k in the week ending June 8, above expectation of 227k. Four-week moving average of initial claims rose 5k to 222k.

Continuing claims rose 30k to 1820k in the week ending June 1. Four-week moving average of continuing claims rose 8.5k to 1797k.

US PPI at -0.2% mom, 2.2% yoy in May

US PPI for final demand fell -0.2% mom in May, below expectation of 0.2% mom rise. PPI goods fell -0.8% mom, largest decline since October 2023. PPI energy fell -4.8% mom. PPI food fell -0.1% mom while PPI ex food and energy rose 0.3% mom. PPI services was unchanged. PPPI less foods, energy, and trade services was also unchanged.

For the 12-month period, PPI rose 2.2% yoy, matched expectations. final demand less foods, energy, and trade services rose 3.2% yoy.

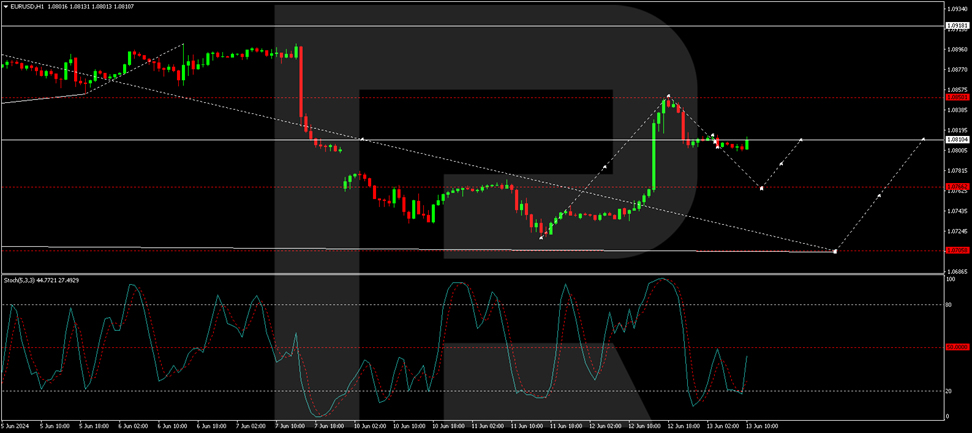

US Dollar Declines as Fed Signals Potential Rate Cut and Inflation Eases

The EUR/USD pair is holding steady around 1.0805 on Thursday, following a surge in volatility the previous evening. The Federal Reserve concluded its meeting with a neutral stance, maintaining the interest rate at 5.25% per annum as anticipated. The Fed's comments hinted at a possible interest rate cut by December while projecting more aggressive rate reductions for 2025, which the market viewed positively.

However, it was the US inflation data that significantly impacted the EUR/USD pair, more so than the Fed's announcement. The Consumer Price Index (CPI) for May showed a year-on-year increase of 3.3%, down from 3.4% in the previous month. On a month-on-month basis, the CPI was flat, compared to a 0.3% increase in April. Core inflation, which excludes volatile food and energy prices, also decreased to 3.4% year-on-year, surpassing expectations. This decline in price pressures followed unexpectedly robust employment market reports.

Investors have been highly reactive to each successive set of statistics, partly because the Fed has emphasised the significance of these data releases in shaping its monetary policy decisions. Following the inflation report, the EUR/USD briefly spiked to 1.0852 before retreating slightly.

EUR/USD technical analysis

On the H4 chart, EUR/USD surged past the consolidation range on the news, executing a correction wave to 1.0851. Currently, a downward impulse has brought it to 1.0800. We anticipate the formation of a consolidation range around this level. A downward breakout could lead to a further decline to 1.0776, potentially extending to 1.0701. The MACD indicator supports this bearish outlook, with its signal line positioned below zero and pointing downward.

On the H1 chart, EUR/USD has completed a decline to 1.0800. A corrective movement to 1.0826 may occur, testing from below. Following this correction, a new downward wave is expected to target 1.0766, with a continuation towards 1.0706 likely. The Stochastic oscillator, with its signal line currently above 20, suggests an upward move to 80, confirming the potential for this bearish trajectory.

Market outlook

As the market digests the implications of the latest US economic data and the Federal Reserve's statements, fluctuations in the EUR/USD pair will likely continue. Investors should remain vigilant and prepared for further volatility as more economic indicators are released and the Fed's monetary policy evolves.

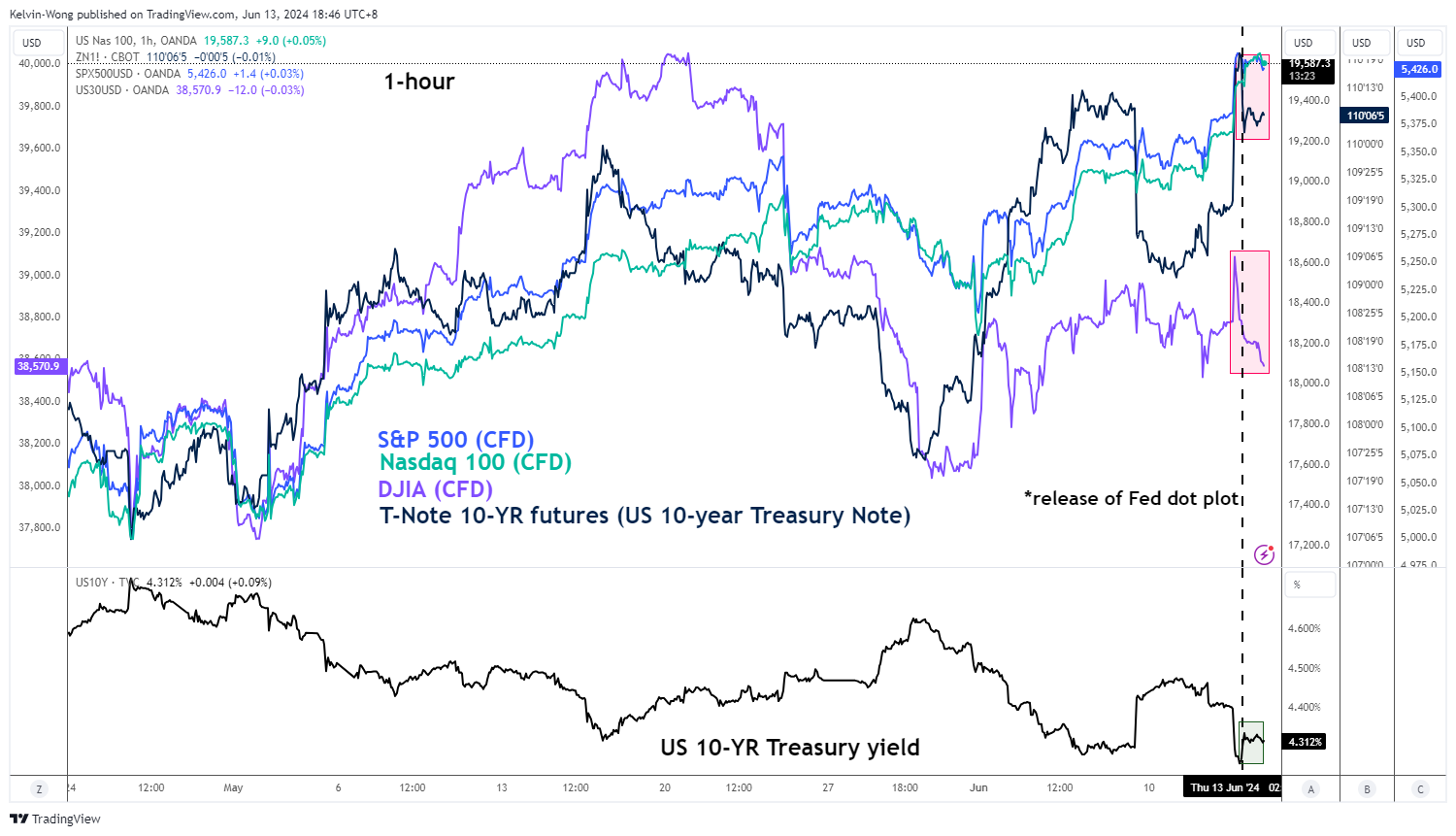

Nasdaq 100: Minor Melt-Up Sequence May Have Hit a Roadblock

- The Dow Jones Industrial Average (DJIA) has given up all its ex-post US CPI intraday gains triggered by losses inflicted on the 10-year US Treasury Note futures.

- The ongoing weakness seen on the DJIA may act as a drag on the Nasdaq 100.

- Watch the 19,800 pivotal resistance on the Nasdaq 100 for a potential short-term mean reversion decline scenario to unfold.

Since our last publication, the Nasdaq 100 has rocketed and surpassed the 19,160 short-term resistance as highlighted. Yesterday, 12 June, it printed another fresh all-time high of 19,557 on the backdrop of a softer-than-expected US inflationary trend for May.

The core US CPI print (excluding food and energy) continued decelerating to a three-year low of 3.4% y/y in May from 3.6% y/y in April and below the consensus estimates of 3.5% y/y.

However, there are several key intermarket and fundamental factors to highlight where the ongoing eight weeks of red-hot bullish price actions seen in the Nasdaq 100 may have hit a roadblock and the next occurrence is a potential “healthy” corrective decline within its medium-term and major uptrend phases.

Mildly hawkish Fed dot plot

The latest US Federal Reserve’s economic projections (dot plot) summary was released yesterday in conjunction with the FOMC meeting.

The Fed’s monetary policy decision outcome did not surprise market participants as it maintained its Fed funds rate at 5.25%-5.50% for the seventh consecutive meeting.

In contrast, the latest projections of the dot plot threw in a “mildly hawkish” surprise. The median projected Fed funds rate at the end of 2024 now stands at 5.1% which suggests an implied forecasted sole rate cut before 2024 ends, compared to previous forecasts of three cuts, and below market expectations of two rate cuts (potentially in September and December) priced in for 2024 as inferred from the CME FedWatch Tool as of 13 June 2024.

In addition, the median projection for the core PCE inflation for 2024 and 2025 has been revised upwards to 2.8% and 2.3% from 2.6% and 2.2% respectively as forecasted earlier in March.

Hence, the current implied forward guidance of the Fed still erred towards a cautious stance in executing its interest rate cut cycle and maintained its current data-dependent approach in the decision-making process.

This data-dependent mantra was echoed during Fed Chair Powell’s press conference where he stated that the Fed needs more data to be able to cut rates despite an acknowledgment that the inflationary trend in the US has shown further modest progress toward the Fed’s 2% target.

The only “celebratory takeaway” for the dovish camp was an additional projected rate cut to the Feds fund rate in 2025, an implied forecast of four cuts versus three cuts projected earlier in March’s dot plot.

Dow Jones Industrial Average sold off together with the 10-year US Treasury Note futures

Fig 1: 10-year US Treasury Note futures with S&P 500, Nasdaq 100 & DJIA as of 13 Jun 2024 (Source: Trading View, click to enlarge chart)

Fig 2: 10-year US Treasury notes futures (continuous contract) medium-term trend as of 13 Jun 2024 (Source: Trading View, click to enlarge chart)

Interestingly, upon the release of the “mildly hawkish” Fed dot plot, the Dow Jones Industrial Average (DJIA) staged a minor bearish reversal in line with similar movement seen in the 10-year US Treasury Note futures, and the DJIA gave up all its intraday gains fuelled by the ex-post US CPI data release (see the red boxes depicted in Fig 1).

On the contrary, the S&P 500 and Nasdaq 100 have been immune to the intraday sell-off of the Dow Jones Industrial Average triggered by a minor intraday recovery in the 10-year US Treasury yield to recapture its 4.30% support after it hit an intraday low of 4.25% on Wednesday, 12 June that in turn, led to a drop in the 10-year US Treasury Note futures (bond prices move in opposite direction with bond yields).

As seen on the technical analysis chart of the 10-year US Treasury Note futures (continuous contract), its rebound from Monday, 11 June low has now almost reached a key medium-term resistance zone of 110-12/111-08 (also the 200-day moving average) which suggests a potential mean reversion drop back towards its range support at 108-00/107-23 (see Fig 2) cannot be ruled out.

Hence, a further potential drop in the 10-year US Treasury Note futures may add further downside pressure seen currently in the price actions of the Dow Jones Industrial Average where it may act as a drag on the heavily concentrated mega-cap technology and AI-centric Nasdaq 100 and S&P 500 due to their direct intermarket correlation.

Nasdaq 100 melt-up has hit a medium-term resistance zone

Fig 3: US Nas 100 major and medium-term trends as of 13 Jun 2024 (Source: Trading View, click to enlarge chart)

Fig 4: US Nas 100 short-term trend as of 13 Jun 2024 (Source: Trading View, click to enlarge chart)

The recent medium-term uptrend phase of the US Nas 100 CFD Index (a proxy of the Nasdaq 100 futures) from its 19 April 2024 low of 16,985 has hit a 19,570/730 medium-term resistance zone which is defined by a cluster of Fibonacci extension levels and the upper boundary of the major ascending channel from 6 January 2023 low (see Fig 3).

In addition, the daily RSI is now fast approaching an extremely overbought level of 78.31 printed on 15 June 2023. These key technical elements suggest the current melt-up move may have reached an overstretched condition where the next move is probably a potential corrective mean reversion decline at least in the short term.

Watch the 19,800 pivotal resistance for a potential short-term mean reversion decline scenario to unfold that may expose the next intermediate supports at 19,240/19,100 and 18,910 (also the 20-day moving average) (see Fig 4).

However, a clearance above 19,800 invalidates the bearish scenario to see the continuation of the impulsive upmove sequence for the next intermediate resistances to come in at 19,900 and 20,120/155.

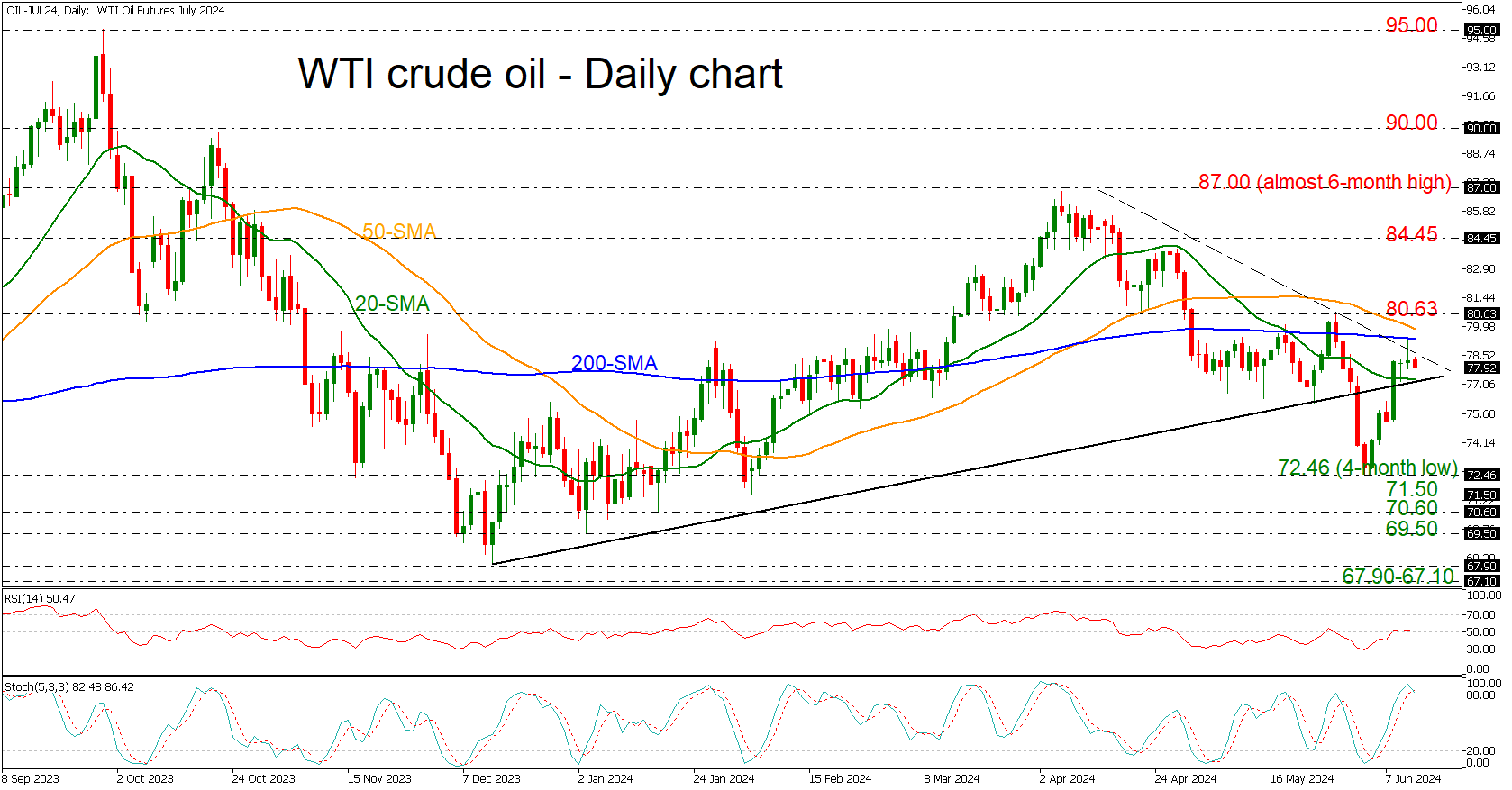

WTI Crude Oil Fails to Improve Upside Move

- WTI crude finds tough obstacle at 200-day SMA

- Technical oscillators head south

WTI crude oil returned above the medium-term ascending trend line, hitting the strong 200-day simple moving average (SMA) at 79.36 after bouncing off the four-month low of 72.46.

The technical oscillators are indicating a negative retracement in the short-term view. The RSI is sloping slightly down near the 50 level, while the stochastic oscillator posted a bearish crossover between the %K and %D lines in the overbought area.

If the market has a successful attempt above the 200-day SMA and the near-term downtrend line, it may challenge the 50-day SMA at 79.86 ahead of the 80.63 barrier. Above this area, the 84.45 obstacle and the almost six-month high of 87.00 could be the levels that may change the outlook back to a bullish one.

On the flip side, if the market dives below the 20-day SMA and the rising trend line, immediate support could come from 72.46 and the 71.50 bar.

To sum up, oil prices are creating an upside recovery but as the market remains beneath the 200-day SMA and the short-term downtrend line, the bias is still titled to the downside.