Sample Category Title

AUD/USD Daily Report

Daily Pivots: (S1) 0.6617; (P) 0.6646; (R1) 0.6666; More...

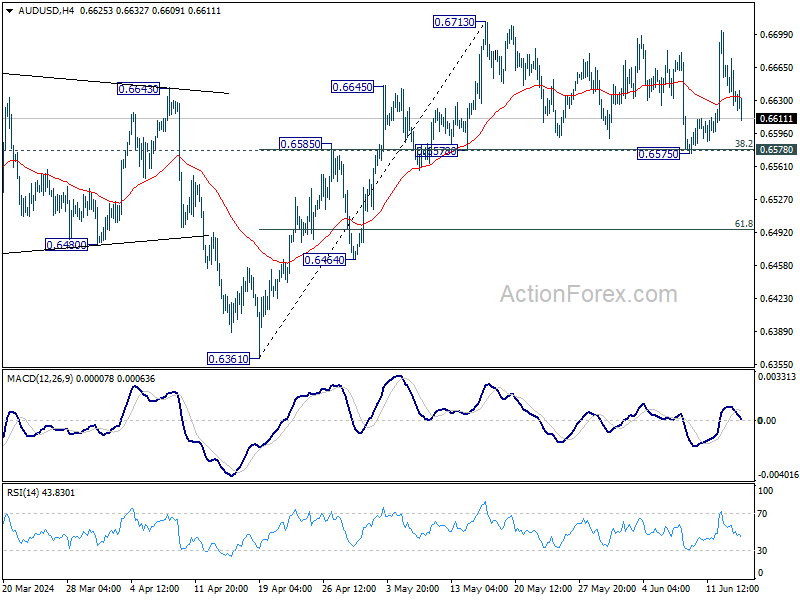

Intraday bias in AUD/USD remains neutral for the moment as range trading continues. On the upside, firm break of 0.6713 will resume whole rise from 0.6361 to 0.6870 resistance next. However, sustained break of 0.6578 cluster support (38.2% retracement of 0.6361 to 0.6713 at 0.6579) will bring deeper fall to 61.8% retracement at 0.6495 instead.

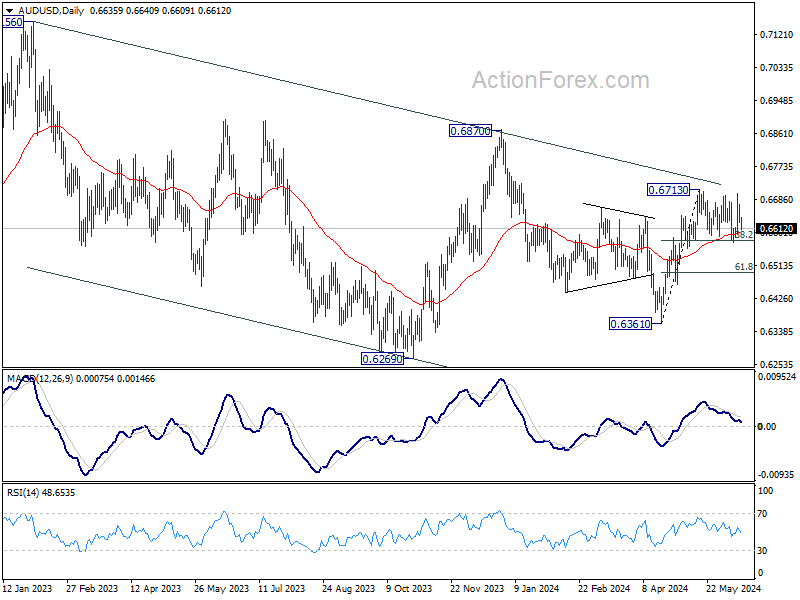

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could have completed at 0.6269 already. Rise from there is seen as the third leg which is now trying to resume through 0.6870 resistance.

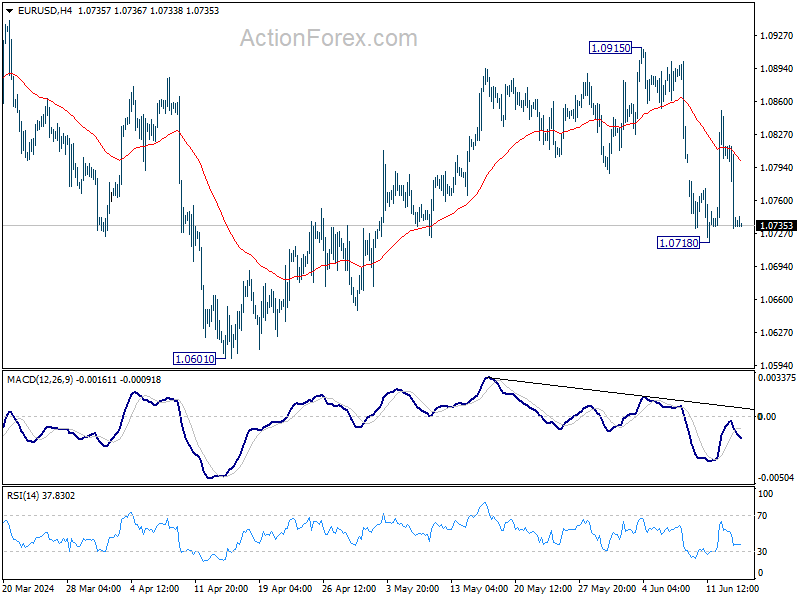

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0709; (P) 1.0763; (R1) 1.0793; More....

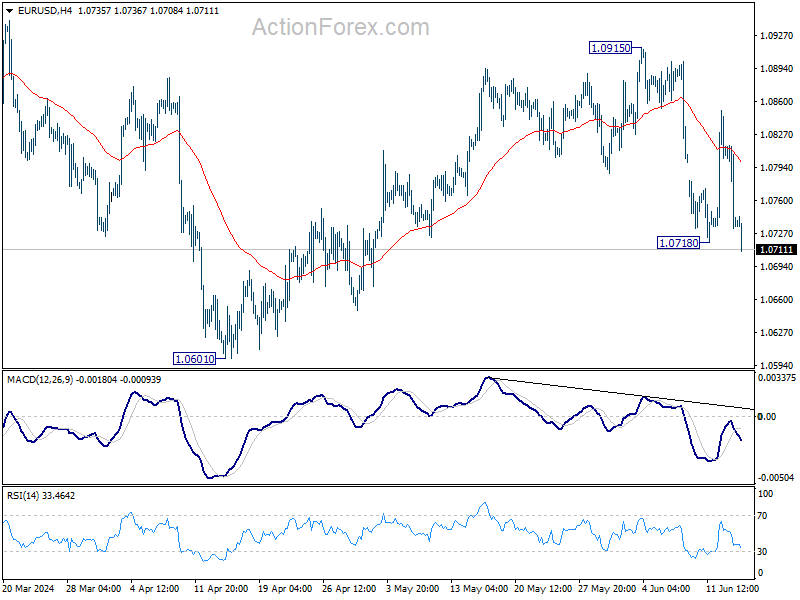

EUR/USD's break of 1.0718 support revives that case that rise from 1.0601 has completed at 1.0915. Fall from there is seen as another leg inside the corrective pattern from 1.1274 high. Intraday bias is back on the downside for 1.0601 support first. Firm break there will target 1.0447 next.

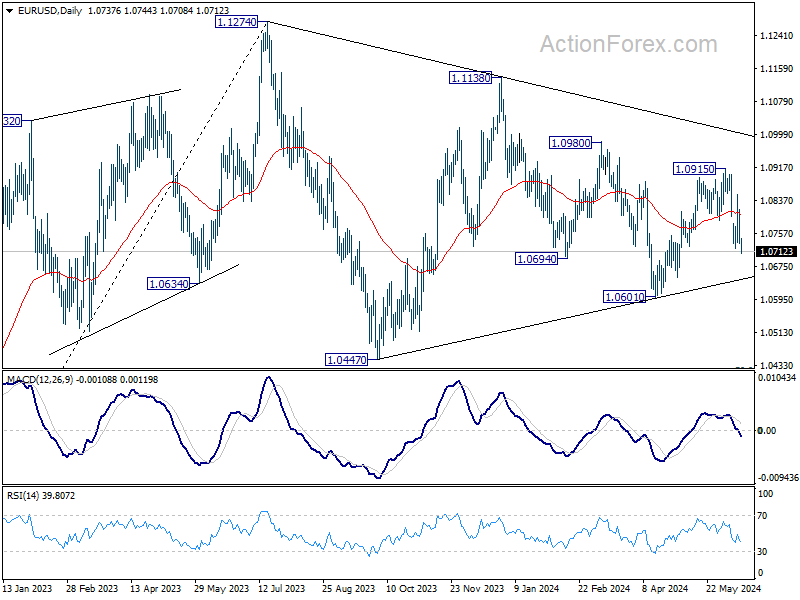

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern, which might still be in progress. Break of 1.0601 will target 1.0447 support and possibly below. Nevertheless, on the upside, firm break of 1.1138 will argue that larger up trend from 0.9534 (2022 low) is ready to resume through 1.1274 high.

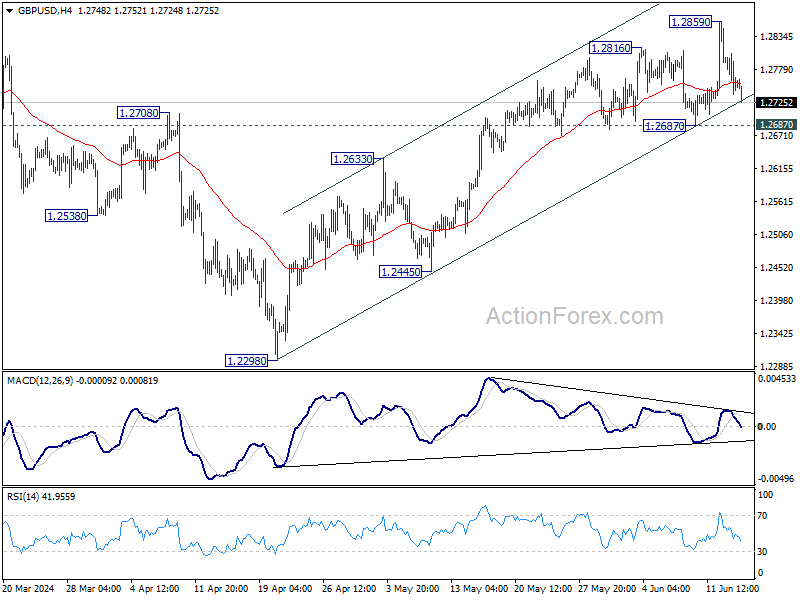

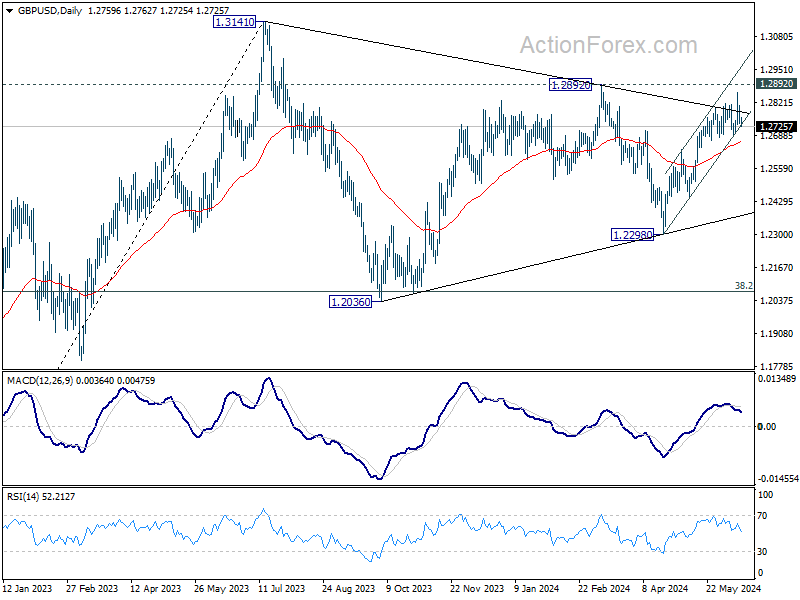

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2732; (P) 1.2770; (R1) 1.2802; More...

Intraday bias in GBP/USD remains neutral at this point. Further is expected with 1.2687 support intact. Break of 1.2859 will target 1.2892 resistance. Decisive break there will strengthen the case that correction from 1.3141 has completed, and bring further rally to retest this high. However, firm break of 1.2687 will suggest near term reversal, and turn bias back to the downside for 1.2445/2633 support one instead.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2445 support will extend the corrective pattern with another decline instead.

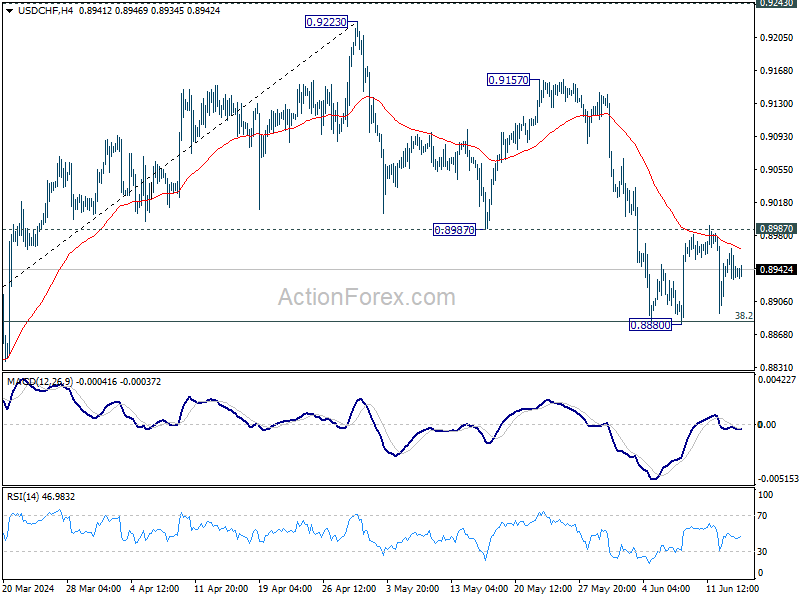

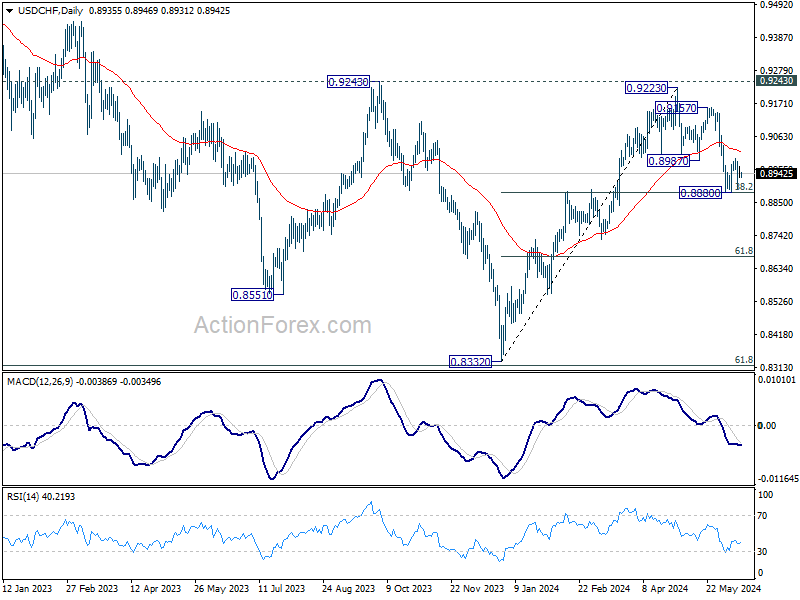

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8921; (P) 0.8945; (R1) 0.8962; More….

Intraday bias in USD/CHF remains neutral for the moment and more sideway trading could be seen. On the downside, sustained break of 0.8883 fibonacci level will carry larger bearish implications and bring deeper decline. On the upside, firm break of 0.8987 support turned resistance will argue that correction from 0.9223 has completed, after drawing support from 0.8883 fibonacci level. Intraday bias will be back on the upside for 0.9157/9223 resistance zone.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

USD/JPY Nearing April JPY-Intervention Levels in Wake of BoJ

Markets

Core bond yields stumbled yesterday. US yields dropped between 5.5 (2-yr) and 7.8 bps (30-yr) on a combination of slower than expected PPI numbers (negative even in the headline reading), a jump in weekly jobless claims to the highest in nine months (242k) and a $22bn 30-yr auction that stopped through (4.403% vs 4.418% WI) and attracted solid investor demand. The US 2-yr tested the post-Fed low but prevented a break/close below for the time being. The 10-yr hit the lower bound of a downward sloping trend channel in place since end April. German yields slipped 4.7 (30-yr) to 8.2 (2-yr) bps. The move was inspired by the US as well as the result of lingering European/French political uncertainty with another round of disastrous polls for Macron’s group hitting the wires. The French president reiterated he plans to stay in power until 2027. But it appears that the more he does so, the less markets believe him. The 10-yr OAT/swapspread jumped to the highest level since early 2014 and is trading a mere 2 bps below Portugal’s. European stock markets tanked about 2%, contrasting with the S&P500 and Nasdaq in the US extending their record run. The euro didn’t escape the sharp European repricing and slid from EUR/USD 1.0809 at the open to 1.0737. The common currency hit a new YtD low against sterling with EUR/GBP closing at 0.8413, the weakest level since August 2022. The Swiss franc banked on its safe haven status. EUR/CHF eased to 0.959 as a weak euro is now taking over from/complementing a SNB-powered CHF. USD/JPY finished only slightly higher yesterday as both a strong US dollar and JPY against the risk-off background kept each other in check. That changed this morning though with the pair nearing the April JPY-intervention levels in the wake of the BoJ policy meeting (cfr. infra). The remaining eco calendar contains US consumer sentiment (Michigan University), which is unlikely to leave a material mark on markets. US bond yields currently recover some ground by adding less than 3 bps across the curve. We continue to err on the side of caution going into the weekend though, especially for Europe. Reports of the 2025 budget stand-off pushing the German government to the brink are obviously not helping in the current environment. The ruling coalition also got a beating in the European elections while the far-right gained. The vote is seen as a gauge for next year’s federal elections in Germany. In case of renewed risk aversion, first support in the German 10-yr yield pops up at 2.4%. If EUR/USD 1.0695/1.0712 breaks, there’s little in the way for a return towards 1.06.

News & Views

The Bank of Japan kept its policy target range unchanged at 0%-0.1% this morning as expected. The central bank will continue conducting bond purchases as set out on March until the next, July, meeting. The BoJ also decided in a 8-1 majority vote that it would reduce its purchase amount of JGB’s to ensure that long-term interest rates would be formed more freely in financial markets. At the July meeting, a detailed taper plan will be communicated. In order not to shock markets, the process will last one to two years. Japan’s economy is likely to keep growing at a pace above its potential growth rate. Simultaneously, the year-on-year rate of increase in the CPI is projected to be pushed up through fiscal 2025 by factors such as a waning of the effects of fiscal measures. Underlying CPI is expected to gradually increase as the output gap improves and medium- to long-term inflation expectations rise with a virtuous cycle between wages and prices continuing to intensify. BoJ governor Ueda will still hold a press conference at 8:30 am CET. The Japanese yen already faces renewed selling pressure because of the ultra-cautious policy normalization process of the BoJ. USD/JPY hits 158 for the first time since end-of-April FX interventions.

Czech National Bank governor Michl in a speech yesterday set out his strategy for the next CNB meetings. The debate at the next meeting at the end of June will probably be about whether to cut by 50 or by 25 bps (currently 5.25%). Both options are open, and in both cases, the CNB will still be in restrictive territory. Then they will be very cautious about further rate cuts. They will assess new data at each meeting and decide accordingly. The rate cutting process can be paused or stopped at any time if inflation, especially core inflation, is not in line with their forecast. The CNB will stay hawkish and do everything in its power to achieve long-term price stability and not trigger inflation. The closer they get to neutral (current estimate 3%-3.5%), the more likely that they’ll slow down or even interrupt policy normalization.

Graphs

GE 10y yield

The ECB cut its key policy rates by 25 bps at the June policy meeting. A more bumpy inflation path in H2 2024, the EMU economy gradually regaining traction and the Fed’s higher for longer US strategy make follow-up moves difficult. Markets are coming to terms with that. For the time being, though, the political narrative dominates. After hitting a new YtD top at 2.7%, the German 10-yr yield corrected lower on safe haven bids.

US 10y yield

The Fed is seeking more evidence than just one slower-than-expected (May) CPI is providing. Upgraded inflation forecasts and a higher neutral rate complicate the exact timing of a first cut further. June dots suggest one move in 2024 followed by four more next year. Markets are positioned more aggressively, turning the recent low in yields into a technical support zone. The US 10-y yield remains stuck in the 4.3/4.7% trading range.

EUR/USD

EUR/USD is trapped in the 1.06-1.09 range. The desynchronized rate cut cycle with the ECB exceptionally taking the lead, strong US May payrolls and a swing to the right in European elections pulled the pair away from 1.09 resistance. The Fed meeting balanced the weaker than expected US CPI outcome. Euro fragility makes a return to the 1.06 downside more likely than not.

EUR/GBP

Debate at the Bank of England is focused at the timing of rate cuts. Slower than expected April disinflation and a surprise general election on July 4 suggest that a June cut in line with the ECB looks improbable. Sterling gained momentum with money markets now discounting a Fed-like scenario. EUR/GBP tested the 2023 & 2024 lows near 0.85. Euro weakness eventually pulled the trick after French president Macron called snap elections following a weak showing in EU elections.

A Growing Divergence

Market sentiment was once again very different on both sides of the Atlantic. The European markets remained under the pressure of tense political environment in France and a 3% slump in April manufacturing production across the Eurozone. The CAC40 dropped 2%, the Stoxx 600 fell 1.30%, the EU bonds were sold off, as well, after MSCI said that it won’t add them to it government indices, the spread between the German and French 10-year papers widened past 70bp – the highest since 2017, and the EURUSD retraced back below its 50, 100 and 200-DMA – after spending just one session above these levels.

And even a softer-than-expected PPI read from the US couldn’t prevent the EURUSD’s decline yesterday. But on the other side of the Atlantic Ocean, the producer prices fell on a monthly basis – the first monthly decline since January and the yearly figure eased to 2.2% while analysts were prepared for a rebound to 2.5%. Cherry on top, the jobless claims jumped to the highest levels in 9 months. Both data played in favour of the Fed doves a day after the Federal Reserve (Fed) hinted that they see little progress regarding inflation instead of ‘none’ at their previous communication and should’ve pulled the US dollar lower – in theory, but the selloff in the euro against the greenback weighed heavier, and the Bank of Japan (BoJ) decided not to reduce its JGB holdings until the July meeting – and that also fueled a yen selloff and sent the USDJPY toward the 158 this morning. In summary, the US dollar bears couldn’t take advantage of softer data yesterday due to contradictory dynamics elsewhere.

But the US yields eased, the US 2-year yield tipped a toe below the 4.70% for the second consecutive session and the 10-year yield fell all the way down to 4.22%. Both yields rebounded since then, but this week’s softer-than-expected inflation updates maintained the expectation of a rate cut alive for the end of the year. The probability of a September rate cut rose to 65%, the probability of a November cut stands at around 80%, while a December cut is now given around 95% chance. Many investors are still skeptical regarding the feasibility of a 2024 cut – and inflation figures haven’t been appetizing so far this year, but the latest figures are encouraging. Yesterday’s PPI for example also hint that declines in some categories in the PPI like airfare and prices for portfolio management services which also feed into the Fed’s favourite gauge of inflation – the PCE index - hint that we could see the PCE index show the slowest advance since November when released later this month.

As such, sentiment in the US equities remains quite cheery. The stock rally slowed yesterday, but the S&P500 eked out a small gain near its ATH level, while Nasdaq advanced to a fresh record. Apple advanced another 0.55%, Super Micro Computer jumped 12% and Tesla advanced nearly 3% after shareholders’ backed Elon Musk’s $56 billion pay deal and his proposal to move the company’s jurisdiction to Texas. Adobe jumped nearly 15% in the afterhours trading after giving a strong outlook for its products as its customers adopt new AI-based tools.

Zooming out, we started seeing a clear divergence between sentiment regarding the European and the US stocks this week and the latter has room to widen. While dark clouds are gathering near the peaks of the Stoxx 600, appetite for the US stocks remains solid – especially for the technology stocks. This positive divergence in favour of the US stocks will likely continue but for this rally to sit on a solid ground, we need gains to widen toward the non-technology names – which is not yet the case; the S&P500’s equal weight index is sitting still and watching the normal-weight index – heavy in tech stocks – travel through uncharted territories. The softening Fed expectations is supportive of such widening of the rally, but investors should show a minimum envy. For now, that’s not necessarily the case. The energy stocks for example continue to be sold off; the SPDR’s energy fund is down by more than 10% since the April peak, financials and utilities are down nearly 5% since May while industrials are down by 3%. Only technology is carrying the rally higher and the rally, there, looks overstretched.

In energy, US crude eased after failure to clear a major Fibonacci resistance at $78.30pb level. That’s the major 38.2% Fibonacci retracement and clearing this resistance should in theory allow the price of a barrel to step into a medium-term bullish consolidation zone. And that’s certainly why we see a solid resistance. The softer Fed expectations as a result of soft inflation reads remains supportive of a further rise, but the rise should be soft and sweet to not awaken the inflation worries, otherwise it would jeopardize the soft Fed expectations.

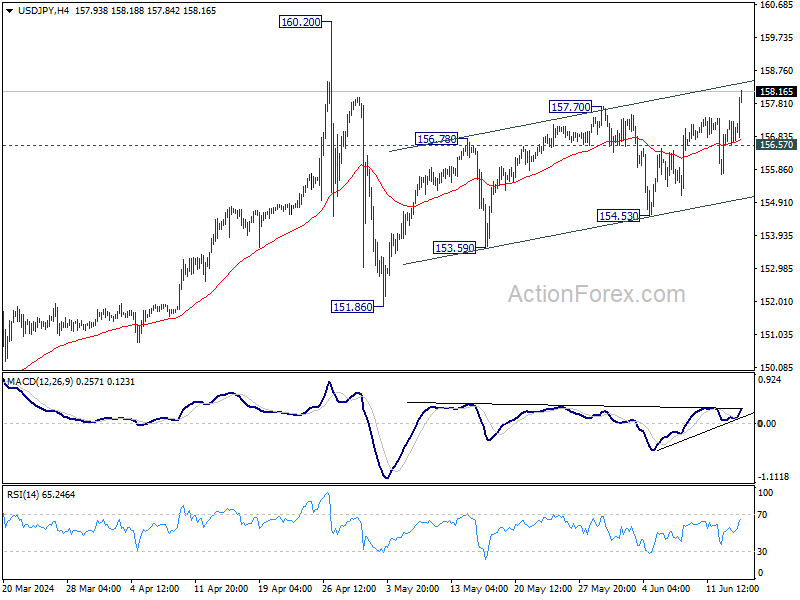

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 155.84; (P) 156.61; (R1) 157.49; More...

No change in USD/JPY's outlook as range trading continues. Intraday bias remains neutral. On the downside, break of 154.53 will turn bias to the downside for 151.86 support and possibly below, as the third leg of the corrective pattern from 160.20. On the upside, break of 157.70 will resume the whole rise from 151.86 and target 160.20 high.

In the bigger picture, a medium term top should be formed at 160.20. As long as 55 W EMA (now at 147.77) holds, fall from 160.20 is seen as correcting the rise from 140.25 only. However, sustained break of 55 W EMA will argue that larger correction is possibly underway, and target 146.47 support next.

BoJ Decision Sends Yen Plummeting as Taper Plan Delayed

The Japanese Yen has taken a significant hit today, losing ground against all major currencies after BoJ refrained from detailing an immediate plan to taper its bond purchases. In the lead-up to the announcement, expectations were high among traders and investors that BoJ would begin tapering soon, fueled by multiple media reports. However, the central bank only indicated an intention to taper, deferring detailed discussions until its July meeting.

BoJ's cautious stance underscores its strategy to wait for the new economic outlook and projections due in July before making any firm decisions. And that's understandable. However, this delay has left the market in a state of uncertainty and unease, prompting speculation on whether there will eventually be a definitive cut in purchase amounts...

Simultaneously, Dollar is continuing to rebound and reverse the losses incurred after the recent CPI data release. Canadian Dollar is emerging as the day's second strongest performer at this point, followed by Euro and Swiss Franc. In contrast, New Zealand and Australian Dollars are underperforming, marginally better than Yen, with British Pound also showing some weakness.

Technically, Euro is a focus today as the near term decline in both EUR/GBP and EUR/CHF resumed after brief recovery. Now, break of 1.0718 support in EUR/USD will also indicate resumption of fall from 1.0915. That would strengthen the case that whole rise from 1.0601 has completed at 1.0915, and bring retest of this low.

In Asia, at the time of writing, Nikkei is up 0.39%. Hong Kong HSI is down -0.47%. China Shanghai SSE is up 0.06%. Singapore Strait Times is down -0.49%. Japan 10-year JGB yield is down -0.034 at 0.937. Overnight, DOW fell -0.17%. S&P 500 rose 0.23%. NASDAQ rose 0.34%. 10-year yield fell -0.057 to 4.238.

BoJ holds interest rates, prepares for bond purchase reduction plan in next month

BoJ left uncollateralized overnight call rate unchanged at 0-0.10% as widely expected. In addition, BoJ will continue its asset purchase program until the end of June. The central bank, by an 8-1 majority vote, has also decided to reduce its JBG purchase amounts afterward.

The detailed plan for the reduction in JGB purchases, which will cover the next one to two years, is set to be determined by at next meeting. Apparently, BoJ would likely to have access to the new economic and price output report before laying out the plan.

BoJ is optimistic about Japan's economic prospects, projecting that the economy will grow at a rate above its potential growth rate. Core CPI is expected to increase through fiscal 2025 due to factors such as the waning effects of government economic measures. Furthermore, underlying inflation is predicted to gradually rise as the output gap improves and medium-to long-term inflation expectations climb.

NZ BNZ manufacturing falls to 47.2 in 15th month of contraction

New Zealand's BusinessNZ Performance of Manufacturing Index dropped from 48.8 to 47.2 in May, marking the sector's 15th consecutive month of contraction.

Looking as some details, production plummeted from 50.3 to 44.5, indicating a sharp return to contraction. Employment showed a slight decline from 50.9 to 50.6. New orders fell further from 45.4 to 44.4, maintaining their contraction for the 21st straight month. Finished stocks rose from 50.7 to 52.4, but deliveries fell from 48.1 to 45.2.

Despite the decline in the overall index, the proportion of negative comments decreased to 63.5% from 69% in April and 65% in March. Most negative feedback highlighted the general economic slowdown and the current recessionary pressures.

Looking ahead

Eurozone trade balance will be released in Euroepan session. Later in the data, Canada manufacturing sales and wholesale sales, and US import prices and U of Michigan consumer sentiment will be published.

USD/JPY Daily Outlook

Daily Pivots: (S1) 156.62; (P) 156.97; (R1) 157.35; More...

USD/JPY's choppy rise from 151.86 resumed by breaking through 157.70 resistance and intraday bias back on the upside. Further rise should be seen to retest 160.20 high but strong resistance could be seen there to limit upside. On the downside, below 156.57 minor support will turn intraday bias neutral first.

In the bigger picture, a medium term top should be formed at 160.20. As long as 55 W EMA (now at 147.77) holds, fall from 160.20 is seen as correcting the rise from 140.25 only. However, sustained break of 55 W EMA will argue that larger correction is possibly underway, and target 146.47 support next.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PMI May | 47.2 | 48.9 | 48.8 | |

| 03:23 | JPY | BoJ Interest Rate Decision | 0.10% | 0.10% | 0.10% | |

| 04:30 | JPY | Tertiary Industry Index M/M Apr | 1.90% | 0.40% | -2.40% | -2.30% |

| 04:30 | JPY | Industrial Production M/M Apr F | -0.90% | -0.10% | -0.10% | |

| 09:00 | EUR | Eurozone Trade Balance (EUR) Apr | 17.0B | 17.3B | ||

| 12:30 | CAD | Manufacturing Sales M/M Apr | 1.30% | -2.10% | ||

| 12:30 | CAD | Wholesale Sales M/M Apr | 2.50% | -1.10% | ||

| 12:30 | USD | Import Price Index M/M May | 0.10% | 0.90% | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Jun P | 73 | 69.1 |

Cliff Notes: Cautious Steps Towards Easing

Key insights from the week that was.

In Australia, headline results from the May Labour Force Survey were in line with Westpac’s forecasts. Growth in employment was solid in the month, up +39.7k (+0.3%), in part due to an unwind of a seasonal dynamic from last month – more people than usual entering employment in May after lining up a job in April. Consequently, the unemployment rate edged lower, from 4.1% to 4.0%. At 2.6%yr, employment growth continues to ease gradually from October 2022’s high of 6.4%yr towards the 2.0%–2.5%yr pre-pandemic range (note these figures use three-month averages). Employment growth continues to keep pace with population growth, leaving the employment-to-population ratio little-changed over the month, near its historic high.

Growth in total hours worked has been much softer than employment, down –0.5% in May to be up just 0.6% from a year ago. The juxtaposition between these two indicators suggests employers are still eager to maintain or expand their capacity, and are using hours to balance current output with demand. This dynamic will be important moving into the second half of the year when we anticipate demand conditions will begin to improve in response to tax cuts and as cost-of-living pressures continue to ease.

Before moving offshore, a final note on the business sector. The latest NAB business survey confirmed that the easing in business conditions over the past two years persisted into May, the index posting another modest decline to be slightly below long-run average levels (–1pt to +6). Having experienced eight consecutive months of forward order declines, businesses are understandably circumspect over the outlook, with confidence moving sharply lower in the month (down 5pts to –3). The uptick in the survey’s cost and price gauges (1.9% and 1.1% respectively) bears close monitoring over the next few months given the RBA aim to maintain an appropriate pace of disinflation and eventually bring inflation sustainably back within the target band.

Over in the US, at the June FOMC meeting, the fed funds rate was held steady and there were minimal changes to projections. The Committee now expects to deliver just one rate cut in 2024 versus three back in March. Four cuts are now expected in 2025 (from three); while the end-2026 forecast is unchanged at 3.125%. The FOMC does not anticipate inflation will improve further in 2024 and also expects it to remain above target through 2025. On the labour market, the unemployment rate is expected to peak at 4.2% by end-2025 from 4.0% today after which it edges down to 4.1% at end-2026 – a figure consistent with full employment based on the Committee’s 4.2% ‘longer run’ view. This assessment of the labour market underpins an above trend GDP growth outlook, at 2.1%yr in 2024 then 2.0%yr in 2025 and 2026.

In the press conference, Chair Powell set a cautious tone regarding the durability of the FOMC’s forecasts. The projections were referenced as 'conservative' and Chair Powell noted that further inflation outcomes like May would lead to a more benign profile. Indeed, it seems most Committee members did not incorporate the below-expectations flat May CPI print into their forecasts, Chair Powell noting in the press conference that, when significant data is released during the meeting, participants are reminded they have the opportunity to revise their forecasts, but “most people generally don’t”. Westpac places greater weight on the recent evidence of decelerating momentum in prices and activity, leading us to expect two rate cuts in 2024 followed by four in 2025, the latter view in line with the FOMC’s expectation. Conversely, we see greater upside risk for inflation in 2026 and beyond, leading to a higher terminal rate of 3.375% in mid-2026 compared to the FOMC's 3.1% end-2026 and their ‘longer run’ estimate of 2.8%.

In the UK, the unemployment rate rose to 4.4% in April as employment fell 139k following a string of declines since the start of 2024. Weekly earnings growth excluding bonuses held around 6% for a fourth consecutive month. However, declining employment looks to be dampening wage expectations, the Bank of England’s Decision Maker Panel survey reporting wage growth expectations for the year ahead has come down from 5.2% a year ago to 4.1% in the latest reading. GDP meanwhile was flat in April as gains in the services sector were offset by declines in industrial production and construction. The BoE’s meeting next week will provide guidance on their assessment of incoming data and the likely timeline to a first cut.

In China, the CPI rose by 0.3%yr in May matching April's outcome. Services inflation remains the primary driver of consumer prices, though consumer demand is unlikely to support a material acceleration in inflation in services or goods for the foreseeable future. Producer prices fell -1.4%yr in May despite an increase in raw material prices (0.9%mth, 0.5%mth), potentially due, in part, to recent strength in shipping costs.

BoJ holds interest rates, prepares for bond purchase reduction plan in next month

BoJ left uncollateralized overnight call rate unchanged at 0-0.10% as widely expected. In addition, BoJ will continue its asset purchase program until the end of June. The central bank, by an 8-1 majority vote, has also decided to reduce its JBG purchase amounts afterward.

The detailed plan for the reduction in JGB purchases, which will cover the next one to two years, is set to be determined by at next meeting. Apparently, BoJ would likely to have access to the new economic and price output report before laying out the plan.

BoJ is optimistic about Japan's economic prospects, projecting that the economy will grow at a rate above its potential growth rate. Core CPI is expected to increase through fiscal 2025 due to factors such as the waning effects of government economic measures. Furthermore, underlying inflation is predicted to gradually rise as the output gap improves and medium-to long-term inflation expectations climb.