Sample Category Title

USD/JPY’s Upward Trajectory: Can the Pair Hit New Peaks?

Key Highlights

- USD/JPY is holding gains above the 156.20 support zone.

- A major bullish trend line is forming with support at 156.50 on the 4-hour chart.

- Gold prices are again slipping lower toward the $2,280 level.

- EUR/USD failed to recover above the 1.0850 resistance zone.

USD/JPY Technical Analysis

The US Dollar remained well-supported above the 155.50 level against the Japanese Yen. After the Fed decision, USD/JPY started another increase above 156.20.

Looking at the 4-hour chart, the pair cleared the 156.50 resistance and settled above the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour). The pair surpassed the 76.4% Fib retracement level of the downward move from the 157.40 swing high to the 155.72 low.

Therefore, there is a high chance of a move above the 157.40 resistance. The first major resistance is near the 158.00 level.

A clear move above the 158.00 resistance might send it toward the 159.20 level. Any more gains might call for a move toward the 160.00 level in the near term.

If not, the pair might correct gains. Immediate support is near the 156.75 level. The next major support is near the 156.50 zone. There is also a major bullish trend line forming with support at 156.50 on the same chart.

A downside break and close below the 156.50 support zone could open the doors for a larger decline. In the stated case, the pair could decline toward the 155.20 level.

Looking at gold, the bears are in again and they might aim for a move toward the $2,280 support in the near term.

Economic Releases

- Michigan Consumer Sentiment Index for June 2024 (Prelim) – Forecast 72, versus 69.1 previous.

- Fed's Goolsbee speech.

NZ BNZ manufacturing falls to 47.2 in 15th month of contraction

New Zealand's BusinessNZ Performance of Manufacturing Index dropped from 48.8 to 47.2 in May, marking the sector's 15th consecutive month of contraction.

Looking as some details, production plummeted from 50.3 to 44.5, indicating a sharp return to contraction. Employment showed a slight decline from 50.9 to 50.6. New orders fell further from 45.4 to 44.4, maintaining their contraction for the 21st straight month. Finished stocks rose from 50.7 to 52.4, but deliveries fell from 48.1 to 45.2.

Despite the decline in the overall index, the proportion of negative comments decreased to 63.5% from 69% in April and 65% in March. Most negative feedback highlighted the general economic slowdown and the current recessionary pressures.

NZD: A Few Swing Trade Ideas to Consider

The NZDUSD pair climbed to a peak of 0.6217 before settling at 0.6170. The pair has faced resistance around the 0.6220 level, with attempts to break through being unsuccessful. On the daily chart, the Relative Strength Index (RSI) is at 56 and trending downwards, indicating a slight drop in buying pressure. This is supported by the flat red bars on the Moving Average Convergence Divergence (MACD), which suggest a continuing consolidation pattern. Overall, the NZDUSD pair is experiencing resistance and consolidation after a brief rise.

NZDUSD – H3 Timeframe

NZDUSD on the 3-hour timeframe chart broke two previous highs; creating a formidable demand zone that has already been tested once before. The addition of the 200-period moving average support into the mix adds the much-needed flavour in support of a bullish sentiment. Finally, the trendline support and the fact that all of these converge around the 88% of the Fibonacci retracement seems reason enough for a bullish reaction from the highlighted zone.

Analyst’s Expectations:

- Direction: Bullish

- Target: 0.61993

- Invalidation: 0.60937

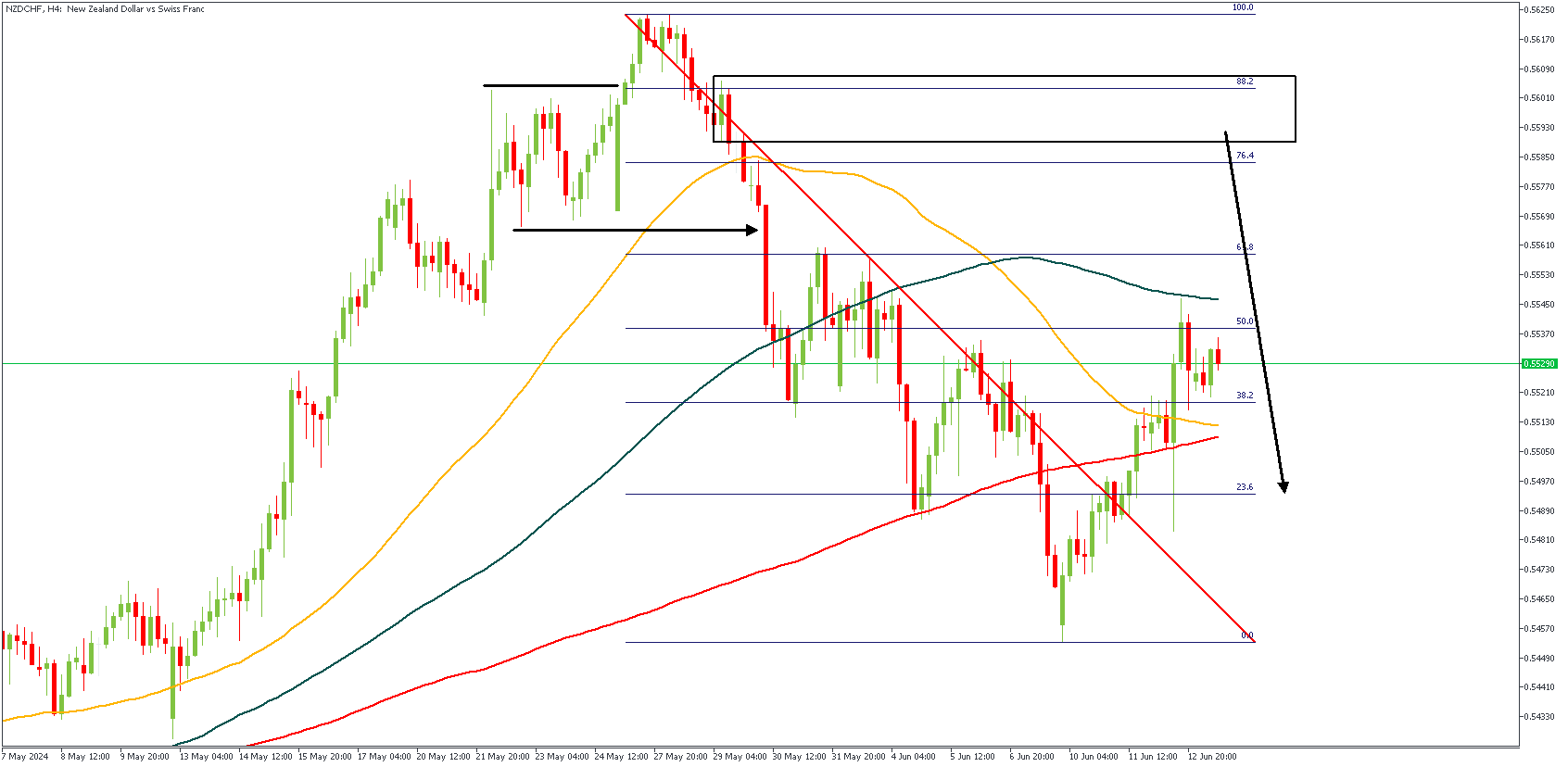

NZDCHF – H4 Timeframe

In my usual flow, I spotted this sweet trade idea on the 4-hour timeframe chart of NZDCHF. Breaking down the highlights on the chart, you would notice the previous high being swept clean of liquidity, after which the proper break of structure occurred. It is my expectation that the retracement of price into the supply zone area that aligns with the 88% of the Fibonacci retracement tool would yield the next bearish impulse.

Analyst’s Expectations:

- Direction: Bearish

- Target: 0.54846

- Invalidation: 0.56183

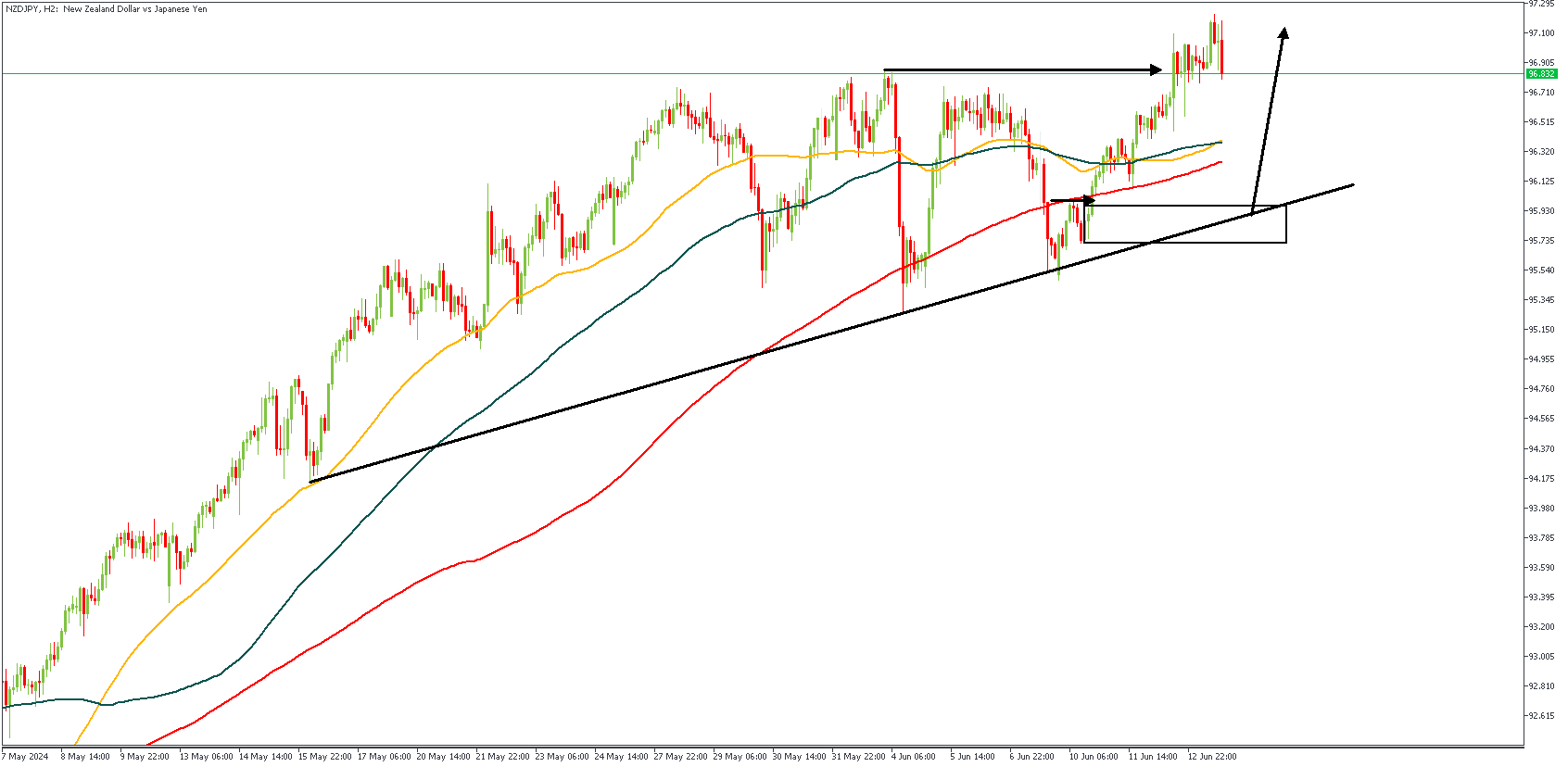

NZDJPY – H2 Timeframe

After making a clean breakout on the 2-hour timeframe chart, we see the price action on NZDJPY slowly grinding downwards in possible search of an area of demand from which new buyers could be lured in. The highlighted demand zone fits perfectly within the 88% Fibonacci retracement level, as well as the trendline support, thereby increasing my confluences in favor of a bullish sentiment.

Analyst’s Expectations:

- Direction: Bullish

- Target: 96.879

- Invalidation: 95.483

CONCLUSION

The trading of CFDs comes at a risk. Thus, to succeed, you have to manage risks properly. To avoid costly mistakes while you look to trade these opportunities, be sure to do your due diligence and manage your risk appropriately.

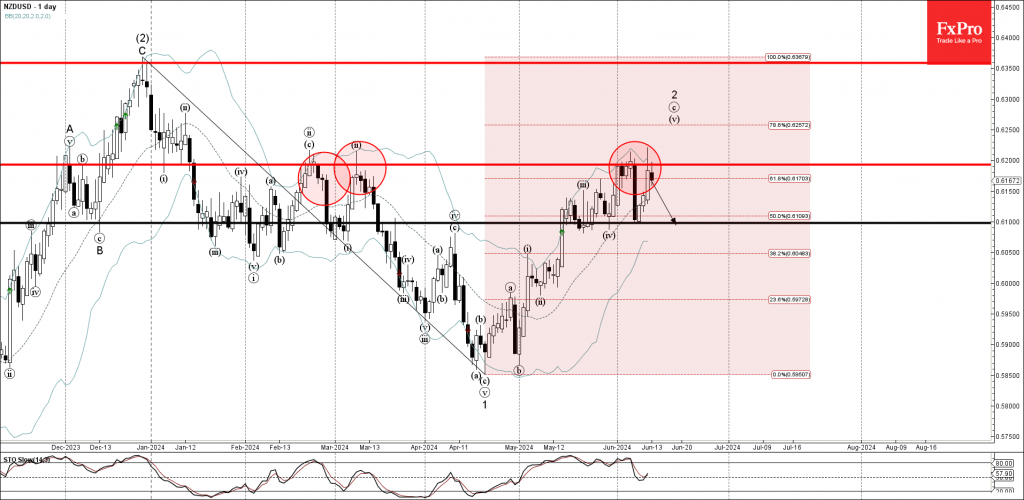

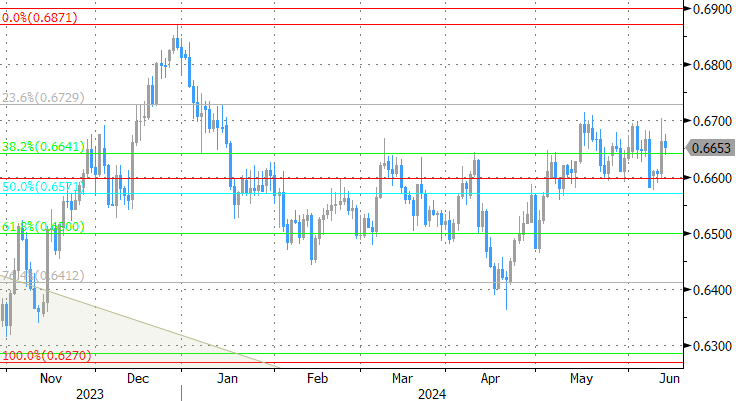

NZDUSD Wave Analysis

- NZDUSD reversed from key resistance level 0.6200

- Likely to fall to support level 0.6100

NZDUSD currency pair recently reversed down from the key resistance level 0.6200 (which has been reversing the price from February).

The resistance level 0.6200 was strengthened by the upper daily Bollinger Band and by the 61.8% Fibonacci correction of the previous downward impulse 1 from December.

Given the strength of the resistance level 0.6200, NZDUSD currency pair can be expected to fall further to the next support level 0.6100, low of the previous minor correction iv.

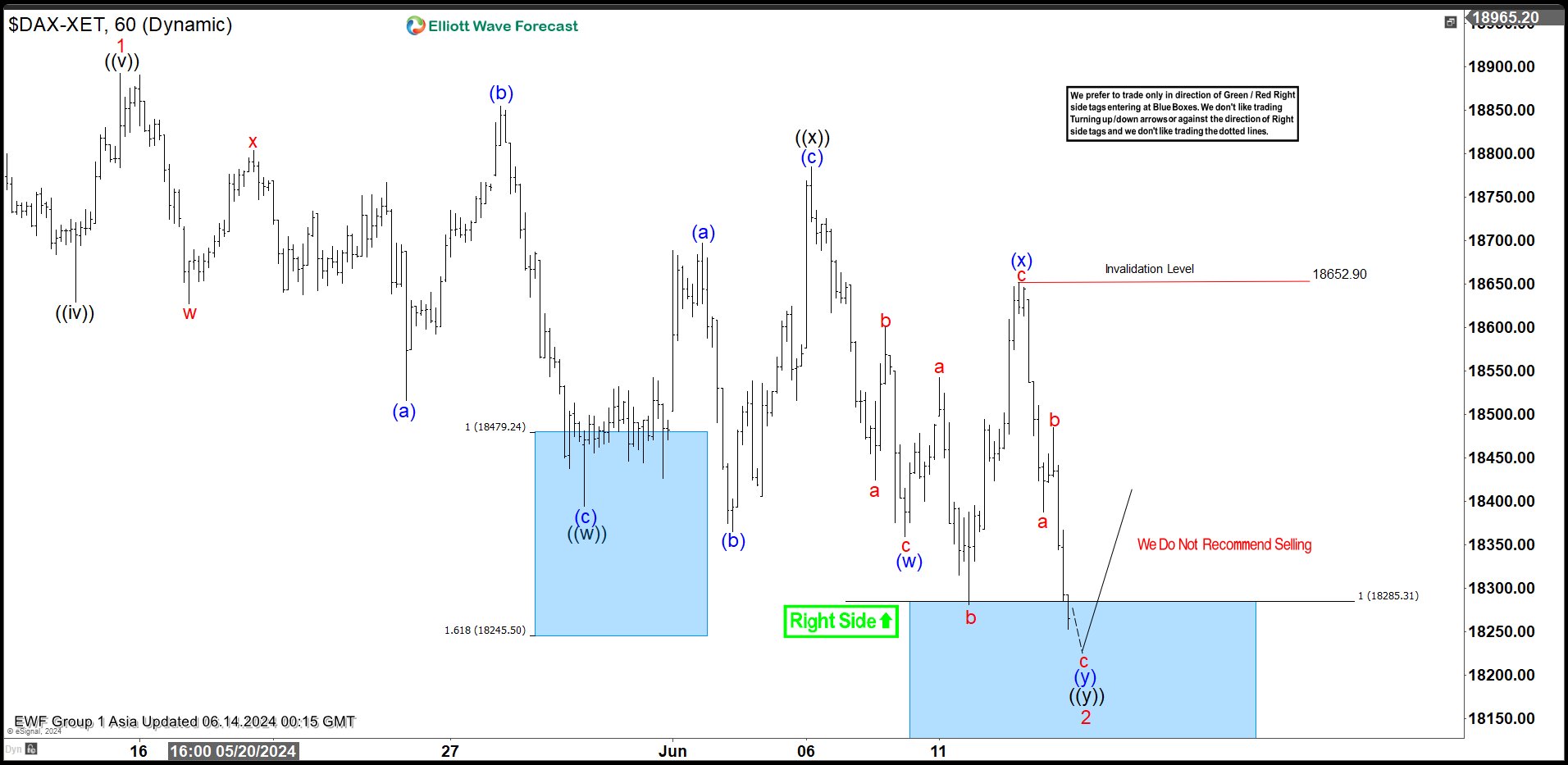

Elliott Wave Intraday Analysis on DAX Looking for Support Soon

Short Term Elliott Wave in DAX suggests the Index is correcting cycle from 4.19.2024 low. The rally from 4.19.2024 low ended wave 1 at 18892.92. Wave 2 pullback is currently in progress as a double three Elliott Wave structure. Down from wave 1, wave (a) ended at 18515.84 and wave (b) ended at 18855.05. Wave (c) lower ended at 18394.43 which completed wave ((w)) in higher degree. Wave ((x)) unfolded as an expanded flat Elliott Wave structure. Up from wave ((w)), wave (a) ended at 18697.09 and wave (b) ended at 18365.53. Wave (c) higher ended at 18784.65 which completed wave ((x)) in higher degree.

The Index has resumed lower in wave ((y)). Down from wave ((x)), wave (w) ended at 18359.42 and wave (x) rally ended at 18652.90. Wave (y) lower is now in progress to complete wave ((y)) of 2 in higher degree. The Index has reached the extreme area from wave 1 peak. This area of support is at 100% – 161.8% Fibonacci extension of wave ((w)), which comes at 17981 – 18287.2. From this area, the Index should turn and resume higher or at minimum rally in 3 waves.

DAX 60 Minutes Elliott Wave Chart

DAX Elliott Wave Video

https://www.youtube.com/watch?v=IF9XAi9KmWk

Bank of Japan (BoJ) Preview: Potential Cut in Bond Buying to Aid Ailing Yen?

- Hawkish FOMC adds further pressure on the BoJ as USD/JPY advances.

- Speculation builds that the BoJ will announce a more comprehensive cut to its bond buying programme.

Fundamental Overview: FOMC Recap and BoJ Outlook

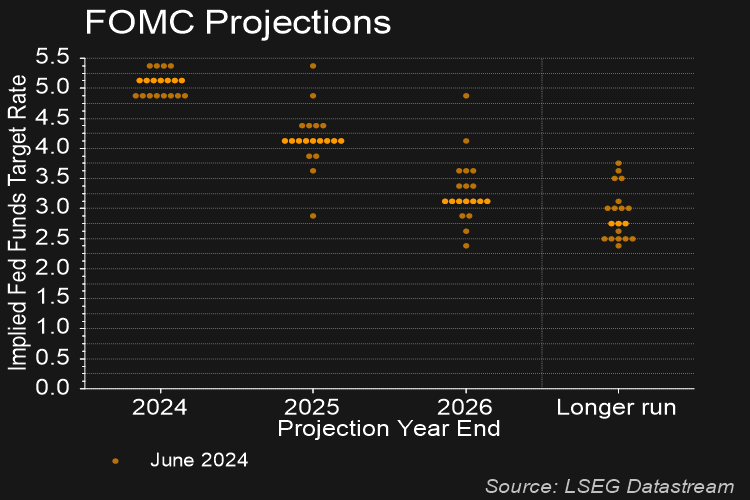

The Japanese continued its slide this morning as USD/JPY edged higher toward the 160.00 psychological level. A brief respite yesterday for USD/JPY which was somewhat of a surprise given the outcome of the Federal Reserve (FOMC) meeting. The Fed left its benchmark lending rate steady in the range of 5.25%-5.50% while delivering a somewhat hawkish update to the summary of economic projections (dot plot).

The Fed adjusted its rate cut expectation for 2024 down to one 25bps cut from the previous three, while at the same time increasing their expectations for rate cuts in 2025 from three to four. A comment that surprised many was Fed Chair Powell stating that the Fed does not have a high degree of confidence in their forecasts, something which may have cast a shadow on the updated dot plot and inflation projections moving forward. Given the higher-for-longer narrative, market participants may be eyeing further gains for the US Dollar against the Japanese Yen, which adds an extra layer of intrigue around the BoJ policy meeting

FOMC Dot Plot Updated, Showing 1 Rate Cut in 2024

Source: LSEG Datastream, June 12, 2024

The BoJ meeting tomorrow will now take center stage as market participants look for further cues from the Central Bank. Governor Ueda has been on the right path in terms of policy normalization but has constantly reiterated the need for caution as the BoJ continues to keep a close watch on wage growth.

In March, the BoJ ended 8 years of short-term negative interest rates and the yield curve control (YCC) policy on the 10-year Japanese Government Bond (JGB). Despite the removal of the YCC policy the Central Bank pledged to keep buying roughly $38 billion worth of government bonds each month to maintain its balance sheet. A surprise cut in bond buying on May 13 has led to increased speculation that the BoJ may be ready to move to a more comprehensive reduction in its bond purchases.

The Nikkei Newspaper reported as much earlier today as well, which begs the question, will such a move provide support to the ailing Japanese Yen? In theory, this would be correct as a reduction in bond buying leads to a decrease in the money supply which tends to strengthen a country’s domestic currency. It is also seen as a prelude to rate hikes and a sign that the Central Bank has confidence in the economy thereby increasing foreign investment and demand for the Japanese Yen.

The Japanese Yen could really use a ‘pick me up’ narrative, following months of struggles against its G7 counterparts. Given that FX intervention has only led to a short-term appreciation for the Yen, it may be time for Governor Ueda to get the ball rolling and offer bolder guidance in the context of policy normalisation.

Risk Events: US PPI Data and Initial Jobless Claims

Looking ahead to the rest of the day, two key US data releases are due later in the day which could stoke volatility in USD/JPY heading into the BoJ meeting. A positive beat of consensus for the US PPI data and initial jobless claims releases could provide further impetus to the US Dollar Index and push USD/JPY closer to the 160.00 handle. A miss to the downside may add some weakness to the US dollar which in my view may not be sustainable.

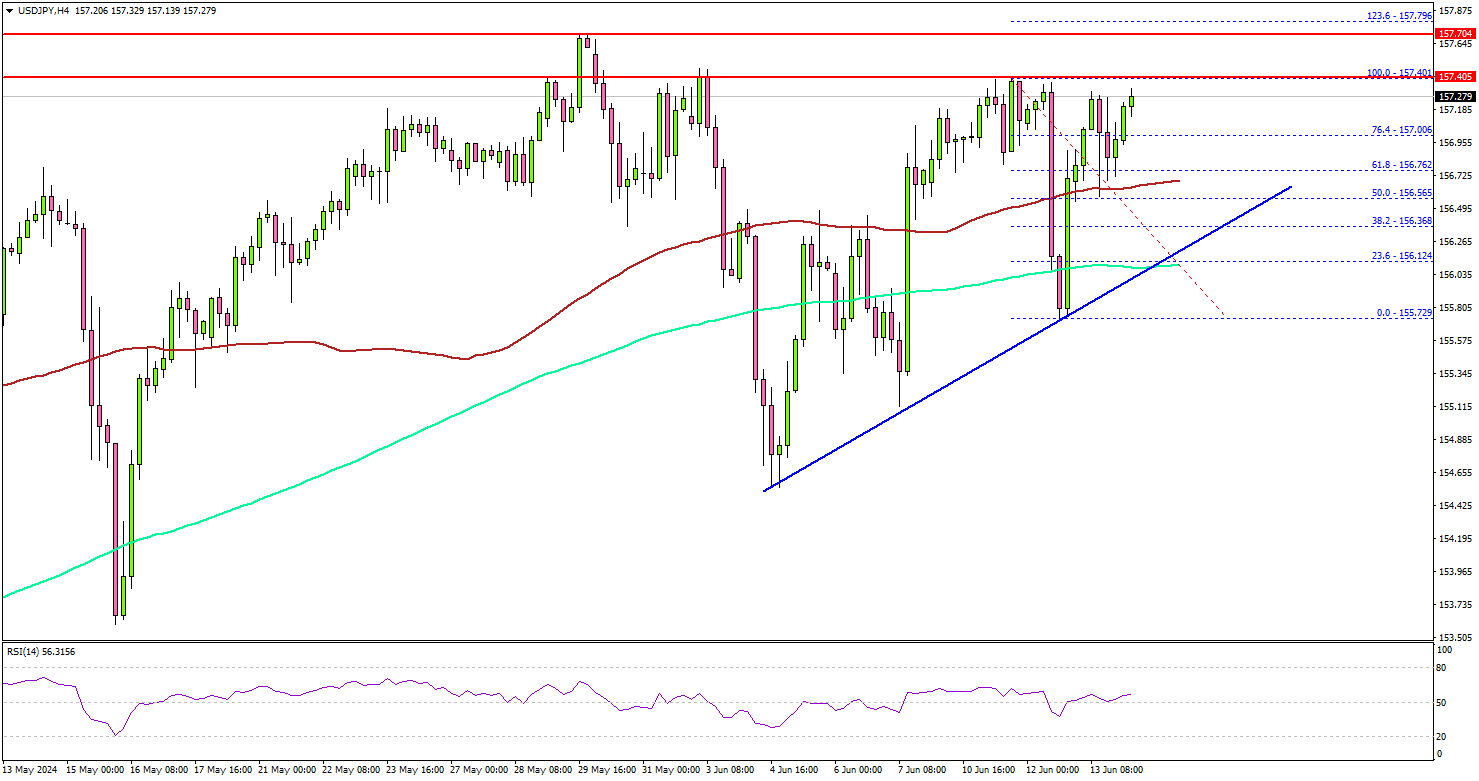

Technical Outlook for USD/JPY

Looking at USDJPY from a technical perspective, the pair has been stuck in a range for the past four weeks, trading between the 155.00 support level and the most recent high around 157.73. Price action has been choppy on USDJPY as the lack of clarity from the BoJ weighs on the mind of market participants.

As you can see on the chart below, USDJPY is supported by the 50-day MA which rests just above the psychological 155.00 handle with a long-term ascending trendline just below it. A break of the 50-day MA could see USDJPY retest the trendline in a break or bounce scenario.

Looking at the upside and immediate resistance is provided by the May 29 high around the 157.73 handle. A break of this level clears a path for a run up all the way to the 160.00 handle. Beyond the 160.00 handle it becomes increasingly challenging to look at the technical outlook given the lack of recent price action data at these levels.

USD/JPY Daily Chart – June 13, 2024

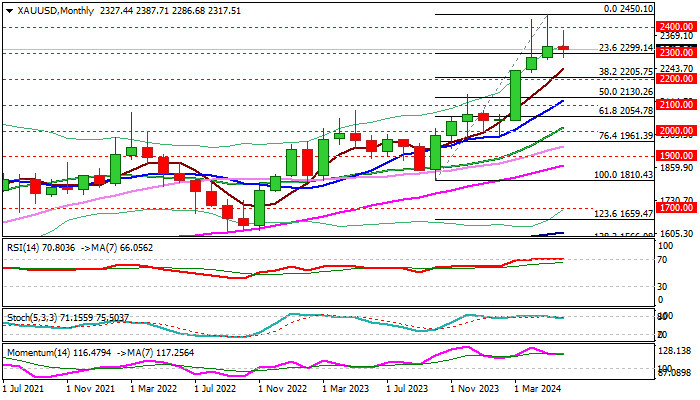

XAU/USD: $2,500 Target Remains in Focus But Consolidation Likely to Precede Fresh Rally

Gold is likely to retest the latest record high and attack psychological $2500 level in coming months, as all key factors that drive the metal’s price remain supportive.

Persisting geopolitical tensions and threats of escalation continue to underpin demand, along with growing signals of stronger monetary easing and one of the most significant – gold purchases by central banks – led by China.

However, overbought conditions on monthly chart and long upper shadows of April/May monthly candlesticks, as well as June’s candlestick so far being in the shape of long-legged Doji, signal rising offers and indecision, indicating that bulls might be running out of steam.

This suggests that metal’s price may hold in extend consolidation, which so far finds ground at $2300 zone, with dips not to exceed solid supports at $2200 (psychological / Fibo 38.2% of $1810/$2450) to keep larger bulls intact for fresh push higher.

Sunset Market Commentary

Markets

Yesterday’s ‘hawkish’ Fed dots raising governors’ 2024/25 inflation projections, a higher reference for the neutral rate (2.75% ) and indicating only one rate cut this year as the FOMC’s preferred interest rate scenario only limited the big decline in US yields post a softer than expected US may CPI release. US 2-y and 10-y yields were saved by the bell not to drop below key support zones respectively at 4.70% (mid-May low) and 4.26% (50% retracement rise December/April & recent correction low). Still, markets clearly saw a more than 50% chance of the Fed again backtracking on its guidance and deploy two rate cuts starting in September rather December. Given Fed guidance yesterday, it would be reasonable to expect money markets to continue switching between a first Fed rate cut in September rather than December or vice-versa and above mentioned yields’ levels to provide solid support. Today’s US jobless claims and PPI data for sure are second tier compared to yesterday’s CPI. Even so, as they pointed in the same direction yesterday’s lows/key supports are again at risk. US jobless claims jumped from 229k to 242k, the highest level in nine months. US (headline) PPI even declined 0.2% M/M to slow the Y/Y-measure to 2.2% from 2.3%. Core PPI didn’t rise in May (0.0%). US yields currently decline between 3 bps (30-y) and 5 bps (5-y). Markets further embrace a September Fed rate cut (75%). Going into this evening’s sale of $ 22bln of 30-y US notes, yesterday’s and today’s moves again made treasuries far more expensive compared to Tuesday’s successful 10-y sale. Interesting the see investors’ interest at current pricing. German Bunds again substantially underperform Treasuries showing changes of less than 1 bp across the curve. ECB’s Vasle and Muller joined comments from colleagues recently that it’s too early communicate on the timing of further steps, among others as wage growth remains and upside risk to inflation. For EMU yields, especially for longer maturities, the upward tendency still holds even after recent correction. Higher EMU yields/underperformance also suggests a gradual tentative rise in EMU risk premia. In this respect, intra-EMU spreads (VS Germany) continued this week’s uptrend (France, Italy, Greece +4 bps, Spain, Portugal, Belgium, Ireland + 3 bps). Lower yields gains again don’t help (European) equities. The Eurostoxx50 again cedes 1.1%. US indices are holding near recent record levels (S&P 500 + 0.25% , Nasdaq + 0.70%).

On FX markets, the dollar, despite a diminishing interest rate differential, still marginally outperforms the likes of the euro or the yen. DXY gains modestly (104.8 from 104.7). EUR/USD struggles to hold to 1.08 big figure. USD/JPY, admittedly in low volatility trading, surpasses the 157 barrier as market await tomorrow’s BOJ decision. Markets see a chance of the BOJ reducing its bond buying. A further rate cut is expected later this summer.

News & Views

Germany’s finance ministry is considering a supplementary budget for this year, Bloomberg reported after Bild newspaper aired the news earlier today. The revision to the 2024 finance plan, which is still being discussed, would allow the government to borrow an additional €11bn on top of the net new €40bn expected before (down from €70bn). Germany’s constitutional debt brake limits deficit spending to just 0.35% of GDP. This structural component is complemented with a cyclical element, however, to smoothen out business cycles. As the economy grew more modestly than expected during the previous budget preparations, some leeway opened up for the government.

MSCI late yesterday denied debt sold by the European Union entrance to its government bond indices. The news came unexpected and is a setback for investors, who anticipated that MSCI inclusion would drastically improve liquidity and overall demand for the bonds. The current supranational status means that triple A rated EU bonds still trade with a discount compared to equally- (and in some cases even lower-)rated peers. A survey of investors conducted by the EU last year revealed that inclusion in such indices was “the single-most important remaining step in order for EU-bonds to trade and price similarly to European government bonds.” MSCI said it will re-evaluate the eligibility criteria in 2025Q2.

Graphs

EMU 10-y swap stays in gradual uptrend even as ECB started cutting rates. EMU risk premium in play?

US 2-y yield revisits yesterday’s lows as high jobless claims and soft US PPI challenge yesterday’s Fed guidance.

USD/JPY: dollar holding up well despite loss of interest rate support. Yen awaits BOJ decision.

AUD/USD tries upside test. Strong labour market data suggest RBA to stick to higher for longer narrative.

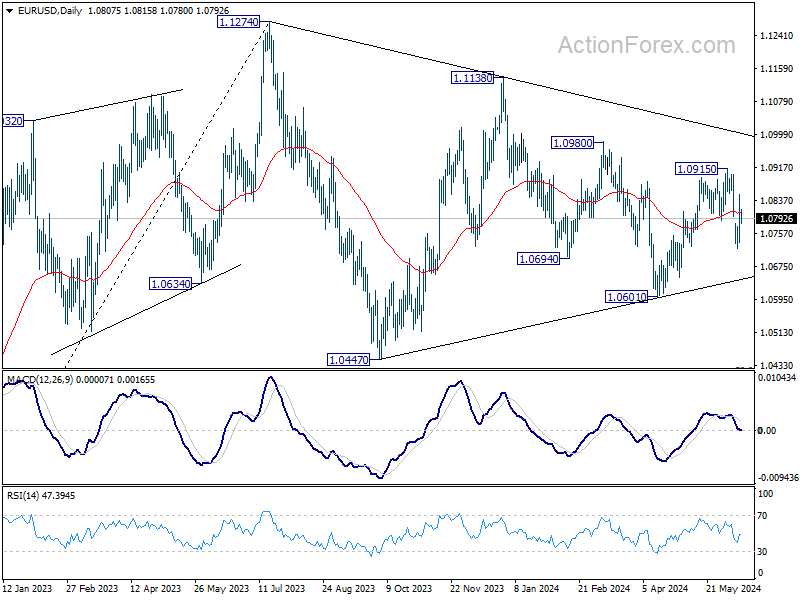

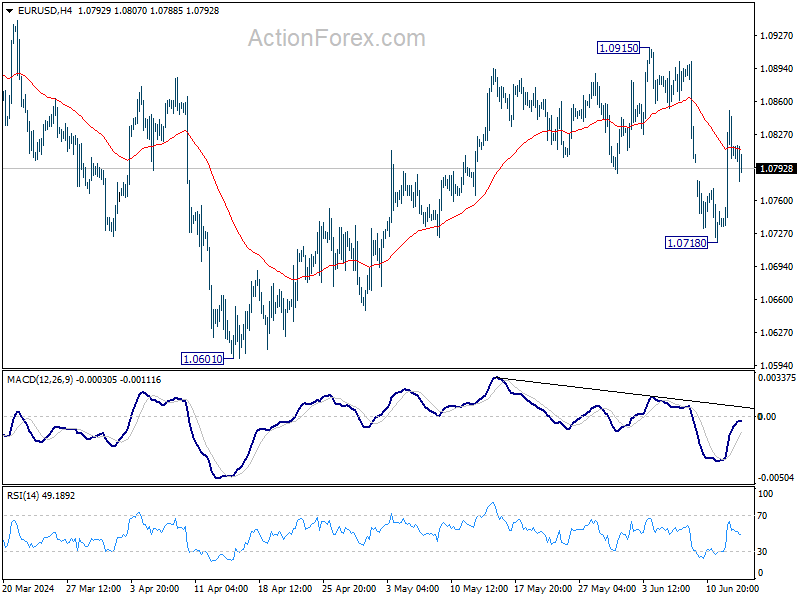

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0745; (P) 1.0799; (R1) 1.0862; More....

Intraday bias in EUR/USD remains neutral at this point. On the upside, firm break of 1.0915 will resume whole rise from 1.0601. On the downside, break of 1.0718 will resume the fall from 1.0915 instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern, which might still be in progress. Break of 1.0601 will target 1.0447 support and possibly below. Nevertheless, on the upside, firm break of 1.1138 will argue that larger up trend from 0.9534 (2022 low) is ready to resume through 1.1274 high.