Sample Category Title

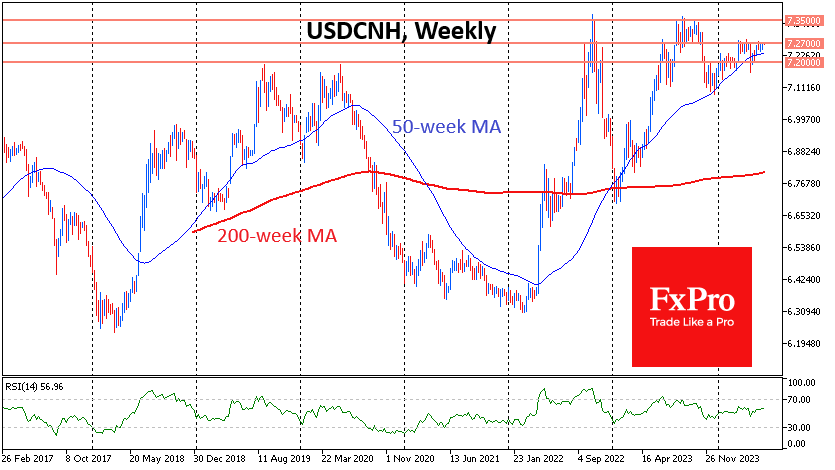

USDCNH Hits the Ceiling

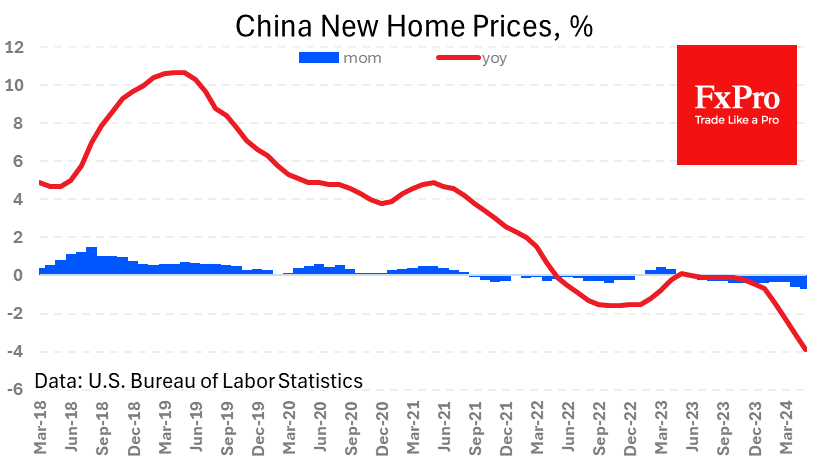

China’s housing price decline is gaining momentum. New home prices for May fell 0.71% vs. 0.58% and 0.34% in the previous two months. The year-over-year decline increased to 3.9%, with back-to-back slides over the 12 months. China has repeatedly announced measures to support the property market, but they have been limited, failing to reverse the trend. The problems in the housing market are very toxic for stocks as housing prices and sales volumes drag down property developers and banks, sucking liquidity out of the financial system.

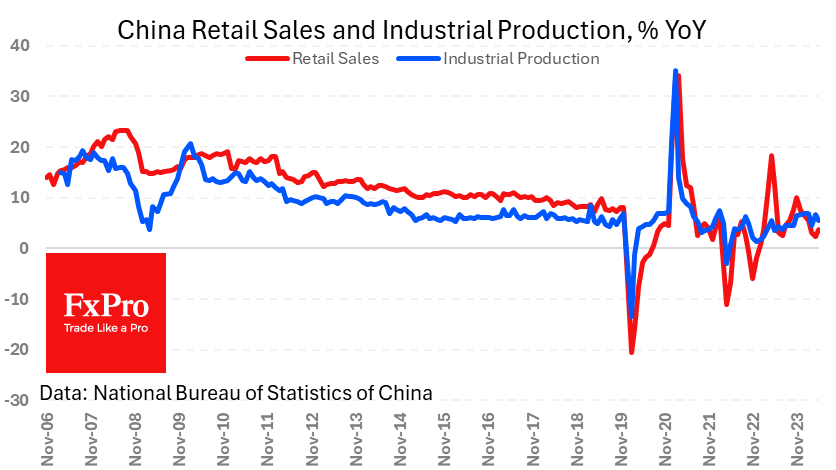

The other bad news was the slowdown in industrial production growth to 5.6% from 6.7% a month earlier, worse than the expected 6.2%. The slowing trend in China’s industrial growth has been in place since the peak in February. China’s industrial production can be seen as a leading indicator of the global economy, and the fresh data raises the risk of a recession in developed economies before the end of the year. Fixed asset investment is also losing momentum, falling to 4.0% against a peak of 4.5% in March and an expected 4.2%.

Retail sales, on the other hand, strengthened growth and beat expectations. The year-to-date gain to May was 3.7% vs. 2.3% previously and 3.0% expected. It cannot be ruled out that this is only a temporary surge, and its positive effect is unlikely to be global.

These data and statistical reports last week failed to lift renminbi volatility. The USDCNH pair seems to have found its ceiling just below 7.27, having been turning downwards from there since the end of March. That said, the downside momentum is getting smaller and smaller, preparing us for a new floor. Next, which seems to be more important for the Chinese authorities, is 7.35. From here, USDCNH was actively sold from August to November last year, and there was a powerful reversal in November 2022. The yuan will be able to sag to this level if there is still a pullback from risks and towards the dollar in global markets. But it will probably take an economic crisis to overcome it.

Technically, it is now more comfortable to be bullish in USDCNH as the previous 2019-2020 global “ceiling” below 7.20 this year works as a “floor”.

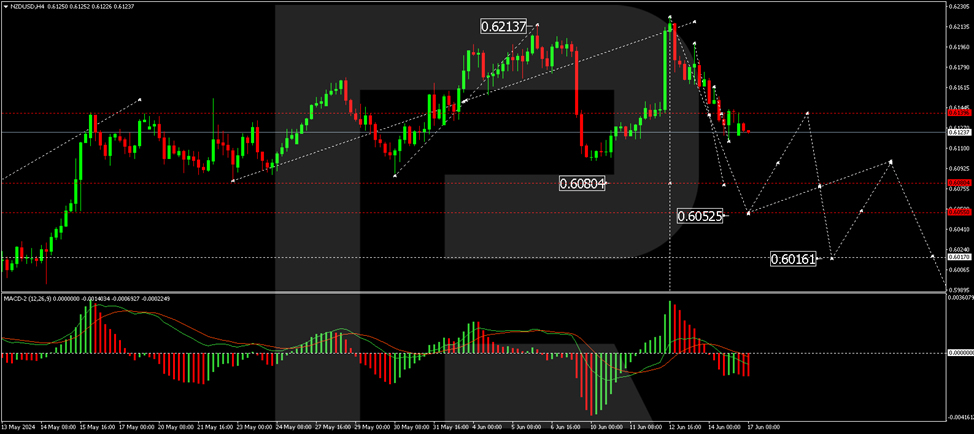

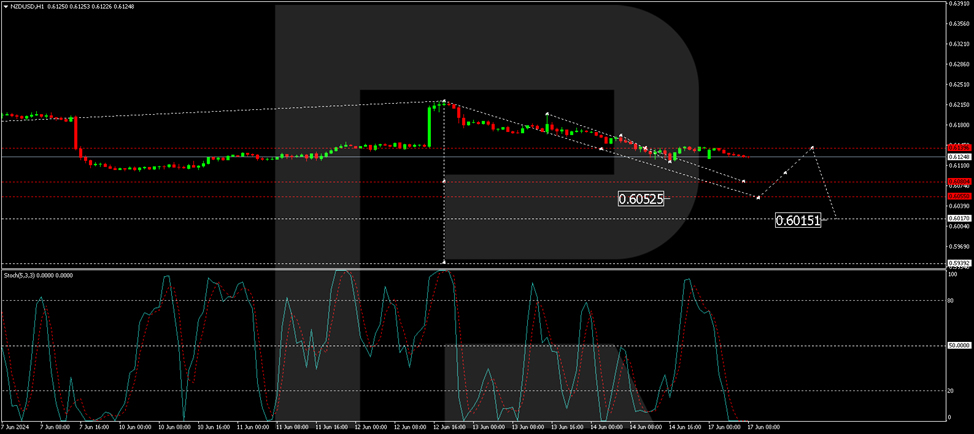

NZDUSD: Expanding Wedge

On the H4, NZDUSD formed an expanding wedge pattern after a prolonged rise. The price bouncing off the upper trend line almost reached a vital support area, which creates two possible options.

- If the price falls below the support at 0.6100, breaking the lower trend line, a fall to 0.6040 can be expected;

- A rebound from the trend line will open the way for a rise to 0.6170;

New Zealand Dollar is Falling

Like other major currencies, the New Zealand dollar is under pressure from the strong US dollar. This development comes after the Federal Reserve's updated forecasts last week. Stock market expectations point to only one interest rate cut this year, most likely in December.

Earlier, some American monetary policymakers confirmed these expectations, calling them reasonable.

The New Zealand services sector experienced a significant downturn in May, dropping the indicator to its lowest value since 2007. This reflects the country's economic state, which is already in recession. The business activity index also decreased to 43.0 points from 46.6 points previously. Everything below the 50.0-point mark indicates a deterioration in the market situation.

Such data increases the likelihood that the Reserve Bank of New Zealand will decide to cut rates eventually. The main forecast is November. However, the RBNZ's position, which has been voiced repeatedly, is that in 2024, the rates are unlikely to be revised down. The Central Bank believes that any reduction is not likely before mid-2025.

NZD/USD Technical Analysis

On the H4 NZD/USD chart, the market executed a correction wave to the level of 0.6220. At the moment, the market is forming another wave following the downward trend. The first target is at 0.6055. After reaching this level, a correction link to 0.6140 is possible (test from below). Next, we will consider a new wave of decline to 0.6016, the local target. Technically, this scenario is confirmed by the MACD indicator. Its signal line is located below the zero mark and is directed strictly downwards.

On the H1 NZD/USD chart, a downward impulse has been executed towards 0.6140. At the moment, a consolidation range has formed around this level. Today, we expect an exit from this range down to 0.6080. After reaching this level, a correction link to 0.6140 is possible (test from below), followed by a further decrease to 0.6055. The first target is trending down. Technically, this scenario is also confirmed by the Stochastic oscillator. Its signal line is located below the 20 mark and is directed strictly downwards.

Ethereum Bolstered by Hopes, Bitcoin Waits for a Signal

Market picture

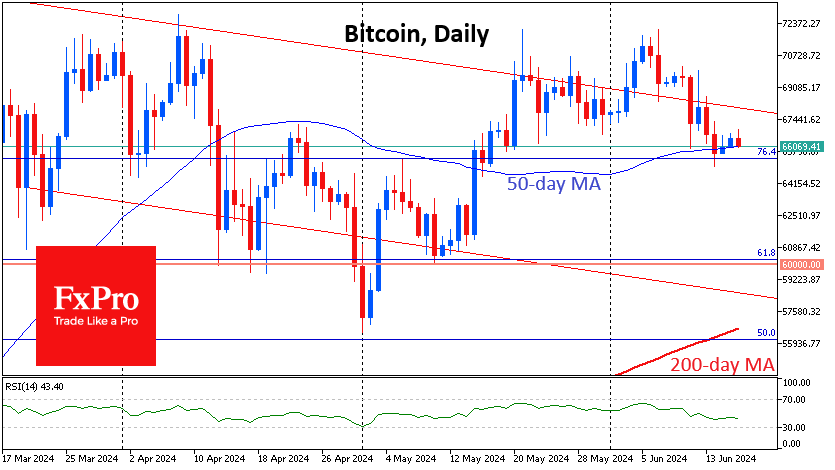

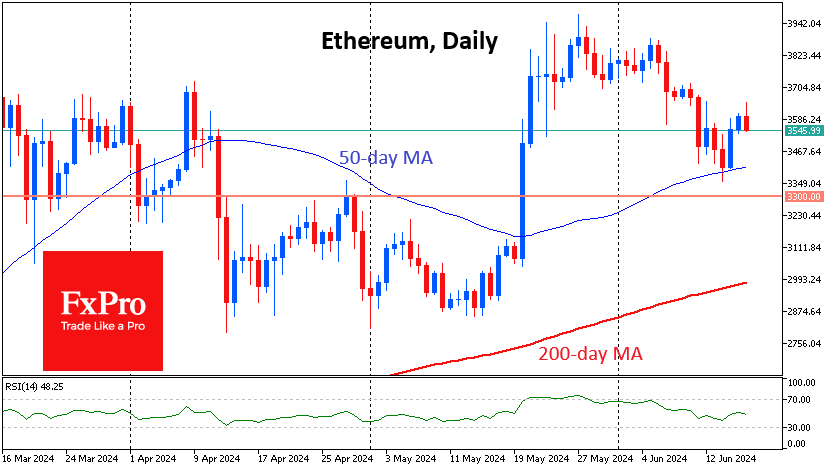

The cryptocurrency market has lost almost 5% over the past seven days. It has not given up important support levels but also has no significant drivers to resume growth. Bitcoin lost 4.7% over the week, in unison with the market. Ethereum lost 3%, while the top altcoins’ performance ranged between -7.7% (Solana) and +11.7% (Toncoin).

Bitcoin has been trading close to $66K since Friday, hovering around the 50-day moving average, testing the medium-term uptrend. The outcome of this test, as well as the market’s direction in the short term, depends on risk appetite in global markets. It has waned due to fears over the French election and a series of weak data from the US and China in recent days.

Ethereum, on optimistic expectations about the ETF, was able to add over 6% after briefly dipping under its 50-day MA on Friday. However, a loss of nearly 1.5% since the start of the day on Monday makes one wary of the near-term performance. The increased liquidity on weekdays will likely play into the hands of bears rather than bulls by increasing selling interest.

News background

Bernstein raised the target price of the first cryptocurrency by the end of 2025 from $150K to $200K. The forecast revision is due to expectations of “unprecedented demand from spot bitcoin-ETFs” managed by BlackRock, Fidelity, Franklin Templeton and others. Bernstein’s baseline estimate is for BTC to reach $500K by the end of 2029 and $1 million by 2033.

Peter Brandt, Factor CEO, suggested that a massive sell-off of Bitcoins by mining companies could lead to a short-term drop in BTC to $60K and even $48K.

SEC head Gary Gensler said approval of Form S-1 for the Ethereum-ETF is possible “sometime by the end of this summer.” According to him, “individual issuers are still going through the registration process. Everything is going smoothly.”

According to CryptoQuant, Ethereum traders bought up 298,000 ETH (worth around $1.34B) after the Fed meeting, the second-highest daily number of coins in history.

Ripple Labs filed a letter demanding that the SEC reduce the fine it is requesting from $2B to $10M, using an agreement between the regulator and Terraform Labs as its argument.

El Salvador President Nayib Bukele proposed creating a private equity bank to “diversify the financing options offered to potential investors in dollars and bitcoin.”

Nikkei Index Falls Below 38,000 Points This Month for First Time

According to today's Nikkei 225 (Japan 225 on FXOpen) chart, the index quote dropped below 38,000 points at Monday's low, followed by a recovery (shown by an arrow).

One of the drivers of the decline was the automotive sector, whose shares led during the downturn. In particular, according to Reuters, Toyota Motors' shares fell by more than 2% as the company faces difficulties due to a certification scandal. Japanese national broadcaster NHK reported that Toyota will extend the production halt for some models until the end of July.

The fact that the Nikkei 225 (Japan 225 on FXOpen) price is recovering after dropping below the 38,000 mark suggests a false bearish breakout below this psychological level.

Technical analysis of the Nikkei 225 (Japan 225 on FXOpen) chart provides more insight into market dynamics:

→ Since the beginning of 2024, there has been a sharp rise from point A to point B by more than 20%;

→ This was followed by a retracement to point C, which constituted a Fibonacci 0.500 proportion of the A→B impulse;

→ Then there was a rise from C to D, forming a Fibonacci 0.382 proportion of the B→C impulse.

Thus, in the first half of the year, there has been a series of diminishing oscillations forming a triangle pattern, indicating a balance between demand and supply around the 38,380 axis.

Today's potential bullish reversal (which is not yet fully formed) could confirm the relevance of the triangle's lower boundary and direct the price towards its axis.

It is worth noting that the triangle boundaries are narrowing, and a possible imminent breakout of this graphical pattern, formed in the first half of 2024, could lead to the establishment of a noticeable trend.

Trade global index CFDs with zero commission and tight spreads. Open your FXOpen account now or learn more about trading index CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

ECB’s Lane confidence on inflation, cautions on interpreting data noise

ECB's Chief Economist Philip Lane expressed "a lot, a fair amount of confidence" today that Eurozone inflation is on track to return to 2% target by the latter half of next year.

In his remarks, Lane highlighted the importance of judiciously interpreting incoming economic data, emphasizing the need to "differentiate the noise and the signal."

Lane's confidence stems from anticipated "muted" cost pressures in the coming year. However, he underscored the critical need for a reduction in "domestic services inflation momentum" as a necessary condition for achieving the inflation targets.

Gold Attempts to Erase Latest Slump

- Gold falls to its lowest level in a month

- But recovers some ground, eyeing 50-day SMA

- Oscillators improve but remain negatively tilted

Gold has been experiencing a pullback from its all-time high of 2,450, breaking below the 50-day simple moving average (SMA). Although the price posted a fresh one-month low on June 7, it has been in a recovery mode since then as the bulls appear to have locked their gaze on the short-term SMA.

If the price violates the 50-day SMA, immediate resistance could be found at the June high of 2,388. Surpassing that zone, gold could ascend towards the April peak of 2,430. Failing to halt there, the price may revisit its record high of 2,450.

On the flipside, bearish actions could come to a halt at the 2,286-2,777 range, defined by the May and June lows. Sliding beneath that floor, the price could challenge the March resistance of 2,223, which could serve as support in the future. Further declines could then stall at 2,145, a region that has acted both as support and resistance in recent months.

In brief, gold has been slowly regaining ground in the near term, attempting to reclaim the 50-day SMA. However, a failure to surpass that crucial barrier could easily trigger a fresh round of weakness.

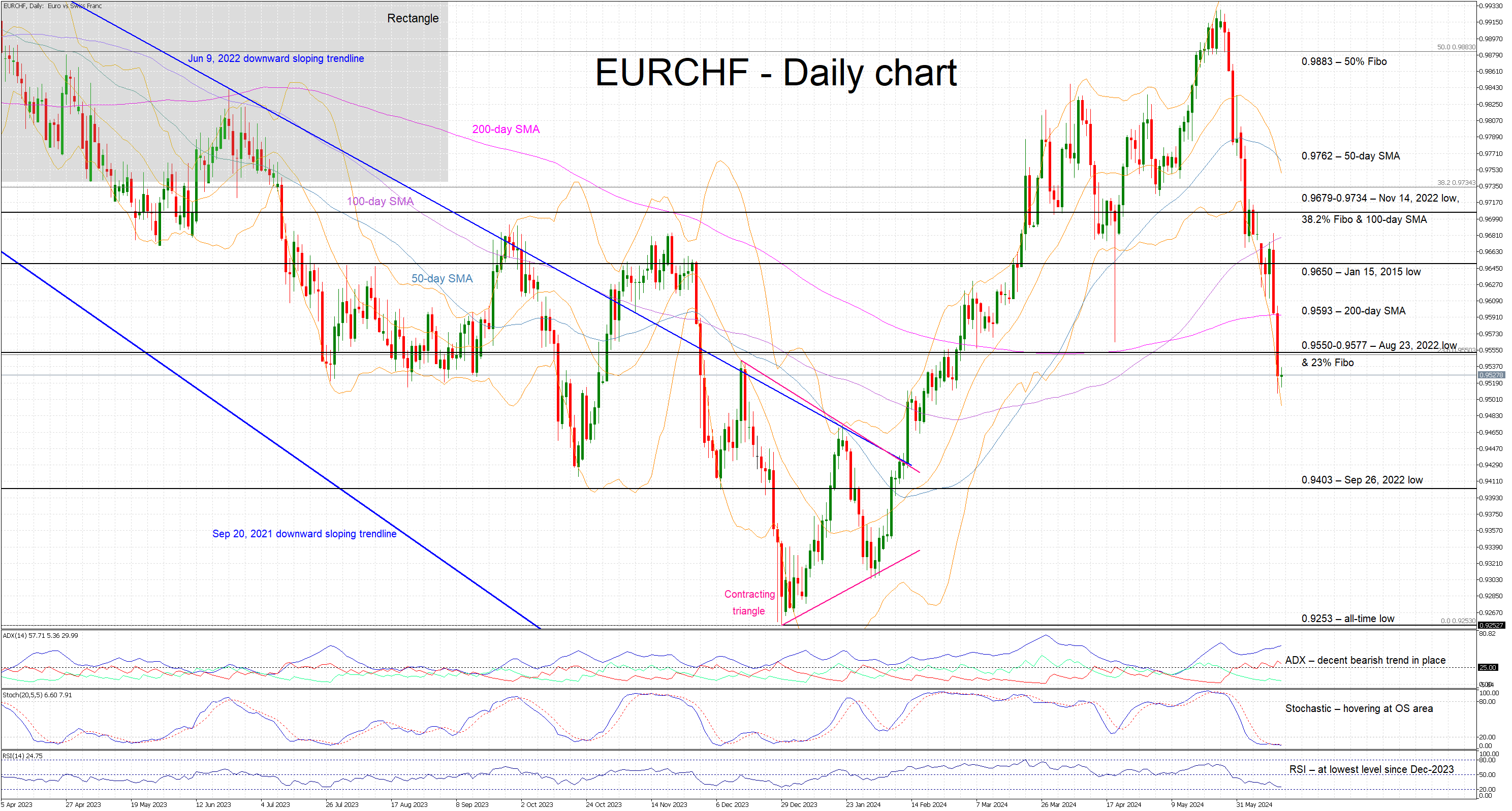

Does EURCHF Correction Have Legs?

- EURCHF drops to a 4-month low

- Significant correction over the past 15 days

- Momentum indicators confirm the bearish pressure

EURCHF has been on a freefall since late May with the move picking up pace following the recent European elections and the first ECB rate cut. This pair is currently trading at a 4-month low, around 4% lower than the recent May 27 peak, and on Friday it managed to successfully break through a strong support area.

In the meantime, the momentum indicators are firmly supporting the current downleg. In more detail, the Average Directional Movement Index (ADX) is acknowledging the strong bearish trend in the market despite the muted performance of the D- indicator. Similarly, the RSI has dropped to the lowest level since December 2023 and is thus confirming the current strong bearish pressure. Unsurprisingly, the stochastic oscillator is hovering at its oversold (OS) territory, where it can stay for a while before signalling a reversal.

Should the bearish appetite remain strong, the bears will try to keep EURCHF below the 0.9550-0.9577 area and then gradually push it towards the September 26, 2002 low at 0.9403. The path then looks unhindered for a much stronger correction towards the 0.9253 level.

On the flip side, the bulls are trying to catch a falling knife. Should they manage to regain control, they could try to push EURCHF back above the 0.9550-0.9577 range and towards the 200-day simple moving average at 0.9593. If successful, the bulls could then have the chance to overcome the January 15, 2015 low at 0.9650 and then gradually retest the much busier 0.9679-0.9734 area.

To sum up, the continued bearish pressure has pushed EURCHF to a new 4-month low with the bulls still unable to record a proper reaction.

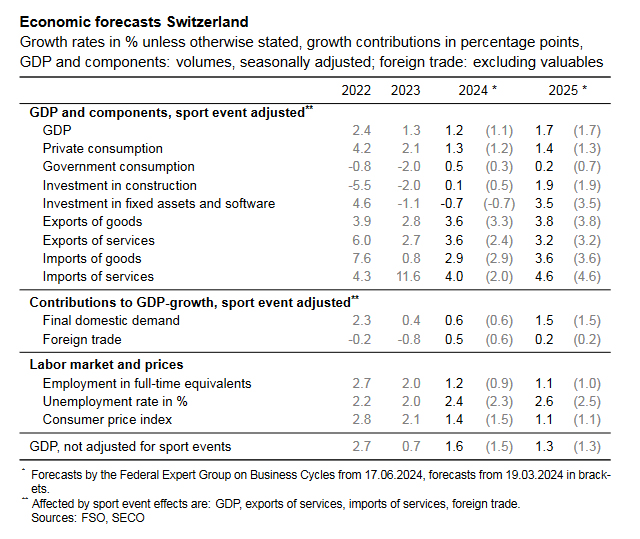

SECO slightly upgrades Swiss economic forecasts, but below-average growth persists

The State Secretariat for Economic Affairs said that Swiss economic forecasts remain largely unchanged, with growth expected to stay below average this year. The Expert Group on Business Cycles projects a modest growth rate of 1.2% for the Swiss economy in 2024, slightly up from March forecast of 1.1%.

Challenges such as low capacity utilisation in industrial production and high financing costs are likely to curb investments. However, exports will provide some support, aided by the recent depreciation the Swiss Franc. More significantly, growth will be driven by private consumption, buoyed by rising employment and a stable inflation rate, which is expected to average 1.4% for the current year, a slight decrease from the March forecast of 1.5%.

Looking ahead, GDP growth for 2025, adjusted for sporting events, is projected to reach 1.7%, with inflation at 1.1%. Both were unchanged from prior forecasts.

For EUR/USD, Further Decline to 1.06 Support the Path of Least Resistance

Markets

The French/Macron-driven risk-off continued to rage across European markets last Friday. European risk premia again leaped aggressively higher. After a protracted period of underperformance against swap, German Bunds fully picked-up their traditional safe haven role. German yields declined between 10.7 bps (5-y) and 14.1 bps (30-y), a move that is difficult to link to ECB interest rate expectations. Intra-EMU spreads widened sharply not only for France (+7 bps against Bunds) but also with substantial collateral damage for the likes of Italy (+10 bps), Greece (+11 bps), Spain (+7 bps) or Portugal (8 bps). Even core and semi-core countries didn’t escape the repricing. European equities remained in free-fall (EuroStoxx 50 -1.95%, CAC 40 -2.66%). The euro didn’t escape the forces of gravity. EUR/USD intraday dropped below the 1.07 level, but managed to end the week near the big figure. The fall-out on US markets evidently was modest. US equities closed the session little changed, holding near (S&P 500) or even closing at record levels (Nasdaq). US yields moved between +0.8 bps (2-y) and -4.9 bps (30-y), testing (2-y, 4.70%) or tentatively breaking key downside resistance (10-y 4.25-30% area). Consumer confidence of the U. of Michigan also didn’t provide much comfort with sentiment sharply deteriorating (62.5 from 69.1 vs 72.0 expected) but inflation expectations at the same time holding stubbornly high (1-y 3.3%). Still the impact on markets was limited. Fed Kashkari and Fed Mester kept a balanced wait-and-see approach on Fed policy going forward even as price data last week mostly surprised to the downside (CPI, PPI but also may import prices published on Friday).

Asian markets continue to trade in risk-off modus this morning (Nikkei -1.90%). infra). US yields tentatively gain 2-3 bps. The dollar maintains last week’s gains (DXY 105.53, USD/JPY 157.50, EUR/USD 1.07). Today’s eco calendar is thin. Later this week, US retail sales (Tuesday) and the PMI’s (Friday) are interesting, but will be overshadowed by the developments in France and the broader risk context. Several central banks (National Bank of Hungary and RBA tomorrow, Swiss national Bank, Norges Bank and Bank of England on Thursday) decide on policy. Yields both in the US and Europe almost fully discount two rate cuts this year. In normal times this should help to build some bottoming, but especially in Europe, the risk-off might persist as first opinion polls on the French elections are filtering through. For EUR/USD, a further decline to the 1.06 support remains the path of least resistance.

News & Views

Rating agency Fitch affirmed Hungary’s BBB rating with a negative outlook. Strengths underpinning the rating are strong structural indicators relative to BBB peers, investment-fueled growth and solid net FDI inflows. Fitch balances these against high public debt compared, unorthodox policy moves and a worsening of governance indicators in recent years. The negative outlook reflects risks around the policy environment and the performance of public finances. It expects the budget deficit to narrow to 4.9%, above the 4.5% government target. The debt ratio could rise to 74.1% in 2024, before falling to 73.3% end-2025. GDP growth is expected to pick up to 2.3% this year on a recovery of private consumption and improving sentiment. Exports should boost growth to 3.8% next year and helps widening the current account surplus to 2% that year. Average annual inflation is seen at 4.4% in 2024 and 3.9% in 2025.

China’s monthly batch of economic data offered mixed signals. Industrial production rose 5.6% y/y in May, both easing from 6.7% the month before and missing estimates for a 6.2%. Retail sales surprised to the upside, coming in at 3.7% vs 3% expected and 2.3% in April. The jury is still out whether it’s the start of a bottoming out process after a drawn out period of consumer weakness. China’s National Bureau of Statistics also warned that domestic demand remains insufficient, adding that the external environment is complex and grim. The property markets shows little improvement, despite the government’s efforts. Property investments slumped 10.1% in the first five months YTD from a year earlier, deepening from -9.8% in January to April. Residential property sales tanked 30.5% YtD y/y. New home (-0.71%) and used home (-1%) prices declined further The yuan stabilizes near 8-month lows (USD/CNY 7.255).

Graphs

GE 10y yield

The ECB cut its key policy rates by 25 bps at the June policy meeting. A more bumpy inflation path in H2 2024, the EMU economy gradually regaining traction and the Fed’s higher for longer US strategy make follow-up moves difficult. Markets are coming to terms with that. For the time being, though, the political narrative dominates. After hitting a new YtD top at 2.7%, the German 10-yr yield corrected lower on safe haven bids.

US 10y yield

The Fed is seeking more evidence than just one slower-than-expected (May) CPI is providing. Upgraded inflation forecasts and a higher neutral rate complicate the exact timing of a first cut further. June dots suggest one move in 2024 followed by four more next year. Markets are positioned more aggressively, turning the recent low in yields into a technical support zone. The US 10-y yield is testing the downside of the 4.3/4.7% trading range.

EUR/USD

EUR/USD is trapped in the 1.06-1.09 range. The desynchronized rate cut cycle with the ECB exceptionally taking the lead, strong US May payrolls and a swing to the right in European elections pulled the pair away from 1.09 resistance. The Fed meeting balanced the weaker than expected US CPI outcome. Euro fragility makes a return to the 1.06 downside more likely than not.

EUR/GBP

Debate at the Bank of England is focused at the timing of rate cuts. Slower than expected April disinflation and a surprise general election on July 4 suggest that a June cut in line with the ECB looks improbable. Sterling gained momentum with money markets now discounting a Fed-like scenario. EUR/GBP tested the 2023 & 2024 lows near 0.85. Euro weakness eventually pulled the trick after French president Macron called snap elections following a weak showing in EU elections.