Sample Category Title

Fed’s Barkin optimistic on inflation, emphasizes “sustainment” and “broadening”

Richmond Fed President Thomas Barkin expressed optimism about the inflation outlook in an interview with MNI Webcast. Barkin noted that we are "on the back side of inflation," indicating that inflationary pressures are easing.

He highlighted that the next several months will be critical in gaining more insights and that Fed is well-positioned from a policy standpoint to react and ease montary policy.

Barkin emphasized two key themes: "sustainment" and "broadening."

Sustainment refers to maintaining a downward trend in both headline and core inflation, ensuring that it continues on a path towards 2% target. Broadening implies that this trend should be consistent across a wide range of goods and services in the inflation basket.

Fed’s Williams foresees gradual rate cuts amid continued disinflation

New York Fed President John Williams shared optimistic views on the US economy in an interview with FOX Business today. Williams highlighted encouraging signs that supply and demand are rebalancing, contributing to a "disinflationary process continuing." He anticipates that inflation will keep decreasing throughout the second half of this year and into the next.

Williams expects interest rates to "come down gradually over the next couple of years" as inflation moves back towards the Fed's 2% target and the economy follows a strong, sustainable path.

However, he refrained from specifying the timing of the first rate cut, stating, "I'm not going to make a prediction" about the exact path of policy.

Williams emphasized that future decisions will be data-dependent, noting, "I think that things are moving in the right direction" for eventual policy easing.

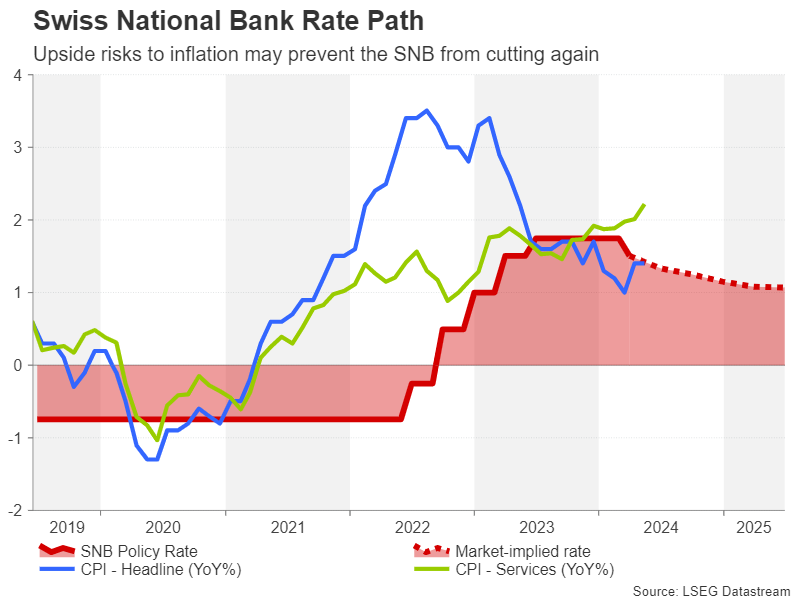

SNB Expected to Cut, But Risk of Disappointment

- Expectations of a June cut by the SNB have been gaining traction

- But inflation picture isn't entirely favourable; weak franc doesn’t help

- A lot of uncertainty awaits the SNB’s decision due Thursday at 07:30 GMT

Will the SNB cut rates again?

The Swiss National Bank (SNB) got the ball rolling with interest rate cuts back in March, becoming the first major central bank to start its easing cycle. Inflation in Switzerland only peaked at 3.5% y/y and has been within the Bank’s 0-2% target for the past year. Investors might therefore be right to think that further easing is on the cards at the June meeting.

However, inflation may not be quite as subdued as the headline CPI figures suggest. Services inflation remains on an uptrend, reaching 2.2% y/y in May - the highest since 2001. But even headline CPI has started to creep up again, rising to 1.4% y/y in April and holding steady in May. Moreover, the Swiss franc has been on the slide this year, adding to price pressures via higher import costs.

SNB President Thomas Jordan, who is due to step down from his post in September, recently said he sees small upside risks to inflation, with the weaker Swiss franc being the likely source. Those comments at the end of May caught investors off guard, triggering a sizeable reversal in the franc against both the US dollar and the euro (although possible SNB intervention in the foreign exchange market may also have been a factor for the rebound).

Are expectations of a cut justified?

Yet, most investors have been ratcheting up their bets of a follow-up 25-basis-point cut in June since Jordan’s remarks and market pricing currently points to around a 68% probability of such an action. Quite possibly, the rally in the franc is seen as lessening the upside risks to inflation and that’s why rate cut expectations have been moving in tandem with franc appreciation.

However, the Swiss currency is still more than 5% down against the dollar in the year-to-date and more than 2% lower versus the euro. When also considering the acceleration in services inflation and the stronger-than-expected GDP growth in the first quarter, there is little urgency for SNB policymakers to cut again so soon.

Swissie could be in for a bumpy ride

All this has set the stage for some heightened volatility on Thursday as a ‘surprise’ decision to stand pat would wrong foot many investors, while a rate cut would also come as unexpected to some traders. For the franc, the June decision will likely be critical for its near-term outlook as the chances of further gains depend on it.

Dollar/franc is in danger of breaching the key support barrier of the 200-day moving average (MA) in the 0.8890 area. If the SNB disappoints the dovish expectations and keeps rates unchanged at 1.50%, this could drag the pair down to the 50% Fibonacci retracement of the late December-early May uptrend at 0.8777 before testing the 61.8% Fibo of 0.8672.

But if the Bank does deliver a cut and hints at more to follow, dollar/franc could rebound towards the June peak of 0.8993 before aiming for the 50-day MA at 0.9061.

All in all, the SNB’s decision of whether to ease policy again in June is likely to be much more of a close call than the market pricing suggests and there will be a surprise element whatever the outcome.

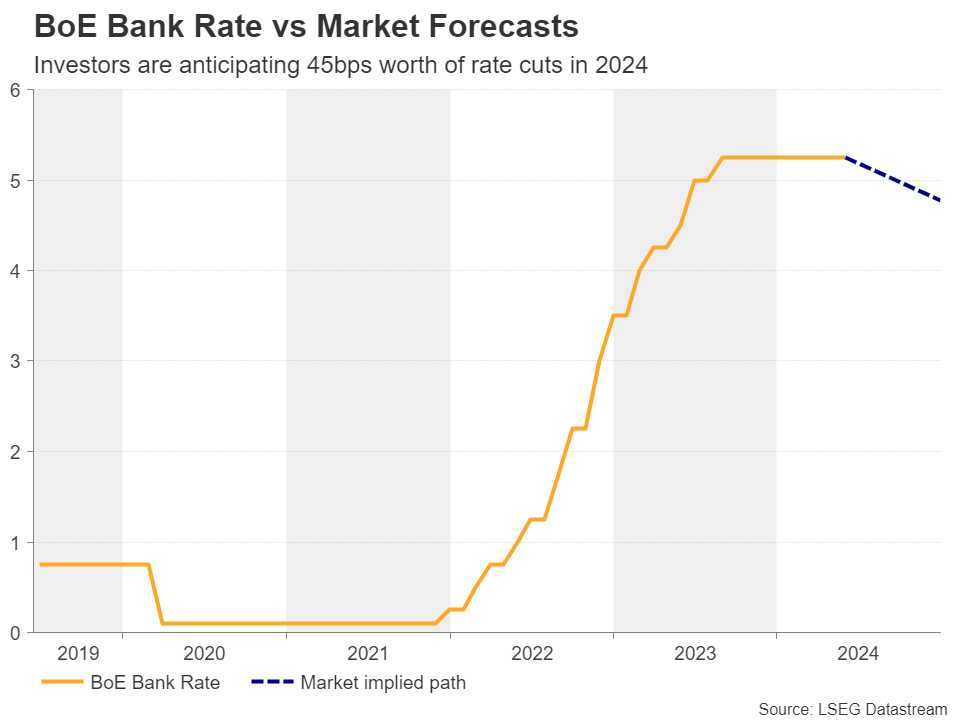

Will BoE Signal Rate Cuts Looming?

- Soft UK data increase chances for September rate cut

- But wage growth remains elevated

- BoE meets on Thursday at 11:00 GMT

- But looming election could be a reason for cautiousness

Investors more convinced about a September cut

At its latest gathering, the Bank of England (BoE) appeared dovish enough to encourage market participants to assign a decent chance for a first quarter-point rate cut in June, but that didn’t last for long as the hotter-than-expected inflation data for April, and especially the stickiness in underlying price pressures, prompted investors to take their summer rate cut bets off the table.

That said, from pricing in around 30bps worth of reductions by December after the inflation numbers, investors are now expecting around 45, with the probability of a September move rising to around 80% after the April jobs report pointed to further cooling in the labor market and after GDP data for the same month revealed stagnation.

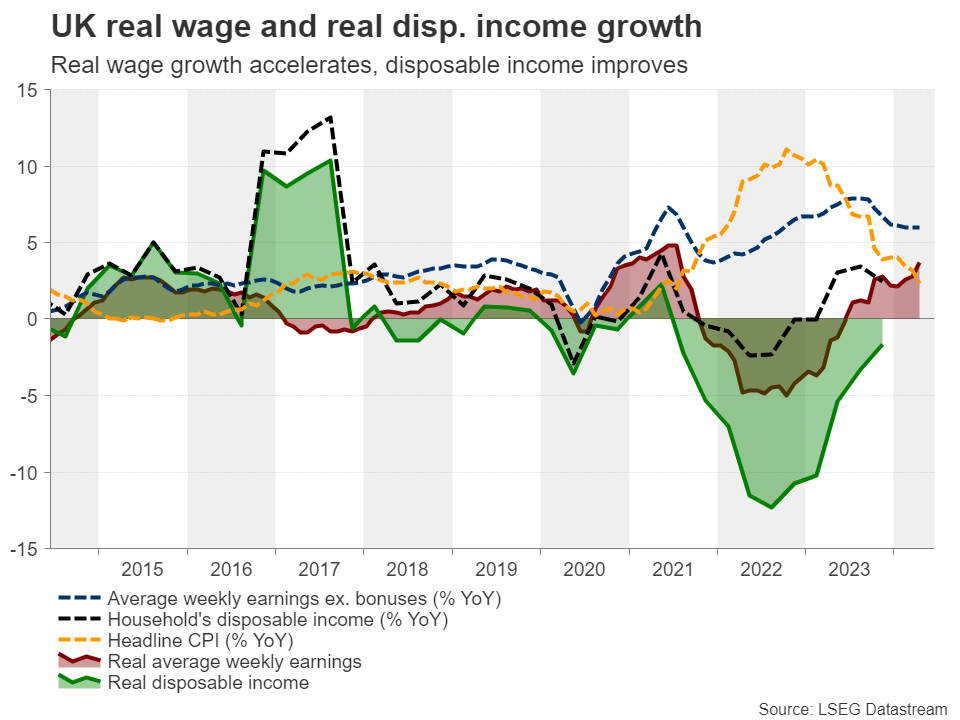

What makes the picture even more complicated is the fact that wage growth remained elevated, with average weekly earnings excluding bonuses rising at a 6% y/y rate. The inflation numbers for May are scheduled to be released on Wednesday, and with the services PMI for the month suggesting that charges rose at the slowest rate in over three years, the risks to the CPI numbers may be tilted to the downside.

Keeping cards close to chest

With all that in mind and as investors try to figure out when and by how much UK interest rates will fall, attention this week is likely to fall on the BoE policy decision on Thursday. No action is expected and thus, given that no updated projections are published this time, nor will a press conference be held, the spotlight is likely to fall on the accompanying statement and the meeting minutes.

However, with the UK general election scheduled just two weeks after the decision, policymakers are unlikely to upset the apple cart. They may prefer to wait and evaluate how the outcome may impact fiscal policy and thereby their own decisions. The Labor party, which is predicted to win the election on July 4, has pledged to keep spending tight. This could make the BoE’s work easier, allowing policymakers to cut interest rates earlier and faster.

Currently, the probability for an August reduction rests at 42% and a potential Labor victory could take it higher. However, until the August meeting, investors will have to digest several data releases as well, including the CPI figures for June.

Pound/dollar remains range bound

From a technical standpoint, pound/dollar has been trading in a sideways manner lately, with most of the price action contained between the 1.2500 level and the resistance barrier of 1.2800.

Last week, the pair was sold off after it hit resistance slightly above the upper end of the aforementioned range, and if the BoE provides the slightest hint that interest rates may start to decrease soon, the slide may continue perhaps until the bears challenge the lower bound of the range at 1.2500. For the picture to brighten, the price may need to climb and close decently above 1.2800.

U.S. Retail Sales Eked Out a Gain in May

Retail sales rose 0.1% for the month of May. Additionally, April's figure was revised downward to -0.2% month/month (previously flat). The reading was lower than the consensus forecast calling for an increase of 0.3%.

Trade in the auto sector was up 0.8% m/m, reflecting increases both at motor vehicle dealers (0.8%), and automotive parts and accessory stores (1.2%).

Sales at gasoline stations fell a sizeable -2.2% m/m, reversing last month's 1.9% m/m gain. This largely reflected a pullback in gas prices. The building materials and equipment category fell by a smaller -0.8% m/m.

Sales in the retail sales "control group", which excludes the volatile components above (autos, building materials and gas) and is used to estimate personal consumption expenditures (PCE), rose 0.4% on the month after declining by -0.5% m/m in April (revised from -0.3% previously).

- Among the control group, the largest positive contributions came from sporting goods stores (2.8% m/m), clothing and accessory stores (0.9% m/m) and non-store retailers (0.8% m/m).

- The largest declines were at home furnishings and electronics stores (-0.4% m/m) and food and beverage stores (-0.2% m/m).

Food services & drinking places – the only services category in the retail sales report –fell by -0.4% m/m.

Key Implications

After a breather in April, consumers were back at it in May. While not large, retail spending growth edged back into positive territory. With other evidence (slowing hire rate, uptick in unemployment rate etc.) pointing to the labor market cooling however, any deceleration there is likely to see retail spending follow suit. With two months of data in for the quarter, retail spending is currently tracking 1.6% q/q (annualized) for Q2 - an uptick from a -0.8% (annualized) decline last quarter.

On the inflation front, while there is good news stemming from lower inflation readings in May, today's report is unlikely to do much to move the Fed's thinking with respect to the first rate cut. Retail spending was only modestly positive, and the number was below expectations. Of more interest to the Fed, is the fact that the improvement in inflation over the last two months was partially offset by a resurgence in payrolls in May combined with an acceleration in wage growth (average hourly earnings). We expect the Fed will continue awaiting a consistent flow of data in support of lower inflation, with a rate cut unlikely before December.

Sunset Market Commentary

Markets

European markets for the second consecutive day enjoyed an interludium of calm after last week’s turbulence. There was little ‘new news’ from the political scene in France. Jordan Bardella of the far right Rassemblement National (RN) in an interview said his party needs an absolute majority in order to realize its program. At the same time, he indicated that his first move as prime ministers would be to execute an audit of public finances to determine its room for policy. It’s doubtful whether this will be enough remove markets’ uncertainty on the country’s fiscal path going forward. Still, intra-EMU spreads of France (and other countries) versus German Bunds narrowed slightly (France -3 bps, Italy -5 bps, Greece -5 bps, Portugal and Spain -3 bps). With safe haven demand fading (at least temporarily) German yields tentatively rose a few bps this morning (up 3.5bps). German ZEW confidence disappointed (cf infra) but initially had little impact on EMU yields. However, any tentative rise in yields on both sides of the Atlantic was blocked as US May retail sales for the second month in row surprised to the downside. Headline May sales grew only 0.1% M/M (vs a downwardly revised -0.2% M/M in April). Control sales (which is seen as a pointer for overall consumption in the GDP release) rebounded a slightly softer than expected 0.5%, but last month’s figure was also downwardly revised (-0.5%). Later in the session US May industrial production data printed much stronger than expected (0.9% VS 0.3% expected). Still, it only slightly mitigated the market reaction post the retail sales report.

After last week’s softer US price data, markets see today’s retail sales as further evidence that the supply-demand balance is moving better in line with what the Fed deems necessary to return inflation to the 2% target. US yields in a steepening move currently decline between 5 bps (2-y) and 1.5 bps (30-y). Markets are a moving ever closer to a scenario of the Fed delivering two 25 bps rate cuts this year (90%). For now US yields are holding above last week bottom levels. German yields after the US data swapped modest morning gains to change between +1.0 bp (2-y) and -1.5 bps (30-y). US equities are little moved by the sales data. The S&P 500 and Nasdaq open almost unchanged, with record levels still within striking distance. The Eurostoxx 50 rebounds 0.5%, but he technical picture remains fragile as the index struggles to sustainably regain the previous range bottom (4884 area). On FX markets, the dollar returned initial gains but basically trades little changed in a daily perspective (DXY 105.4, EUR/USD1.073). EUR/GBP hovers in a tight sideways range between 0.8445 and 0.8460 as investors are looking forward to the UK CPI/price data tomorrow, the BoE policy decision on Thursday and May retail sales scheduled for release on Friday.

News & Views

German ZEW investor expectation rose marginally in June from 47.1 to 47.5. While being the highest level since February 2022, consensus expected a bigger jump to 50. In contrast, the assessment of the economic situation in Germany has slightly deteriorated. The corresponding indicator fell from -72.3 to -73.8 (vs -65 expected). ZEW president Wambach added that inflation expectations of respondents increased which is likely related to the May increase inf inflation. The financial market experts’ sentiment concerning the economic development of the EMU increased from 47 to 51.3. The situation indicator for the eurozone remained unaltered at -38.6.

The National Bank of Hungary slowed the pace of interest rate cuts from 50 bps to 25 bps as they cut the policy rate from 7.25% to 7%. Lower inflation figures had to be balanced against a tougher risk climate which pushed the EUR/HUF cross rate dangerously close to 400. The statement and press conference of vice-governor Virag will follow later today including updated growth and inflation figures. Last month, Virag suggested little scope for more rate cuts after this June move. The forint profits in a first move with EUR/HUF returning below 395.

Graphs

DXY trade-weighted index: dollar keeps recent gains even as soft retail sales fuel Fed rate cut bets.

EUR/HUF: forint rebounds as MNB slows pace of rate cuts from 50 bps steps to 25 bps.

US 10-y yield nearing 4.20% support area as retail sales suggest consumer demand might be cooling.

Brent oil reversing post-OPEC+ decline even as uncertainty on demand persists.

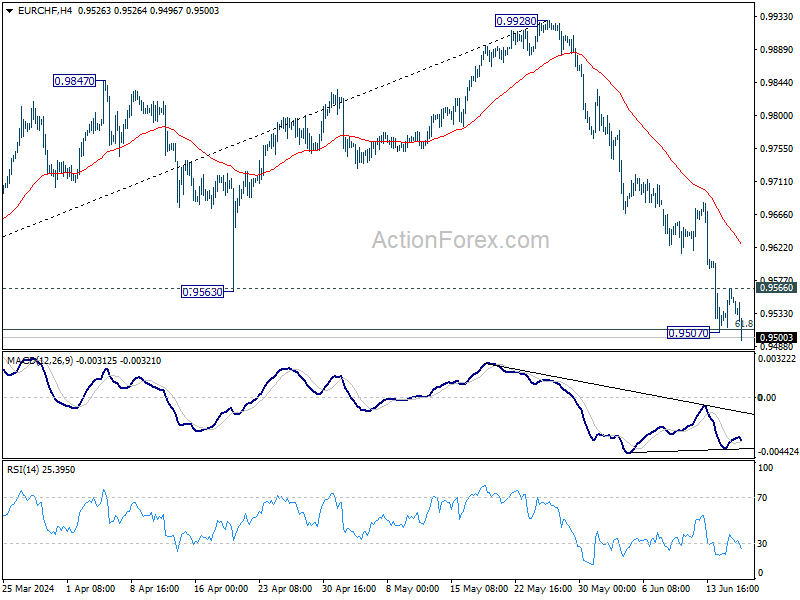

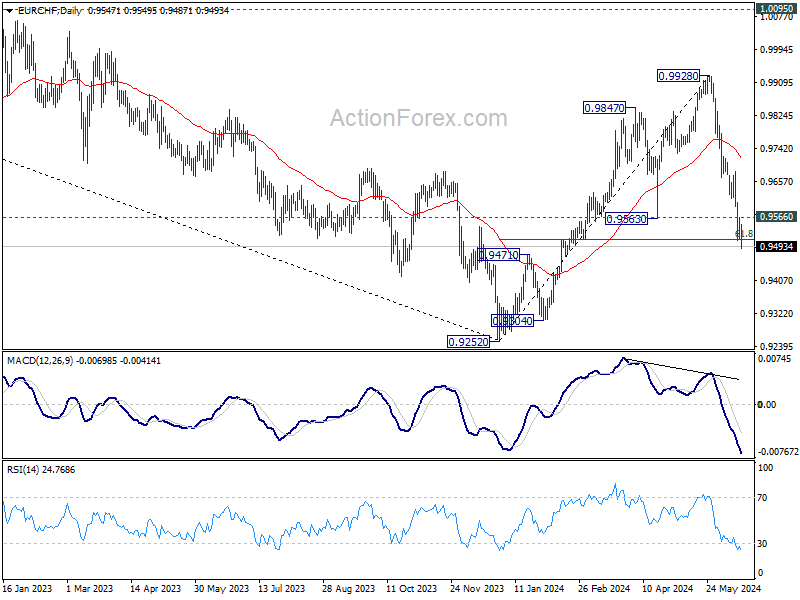

EUR/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9520; (P) 0.9544; (R1) 0.9572; More....

EUR/CHF's fall from 0.9928 resumed after brief recovery and intraday bias is back on the downside. Sustained trading below below 61.8% retracement of 0.9252 to 0.9928 at 0.9510 will raise the chance of long term down trend resumption, and target 0.9252 low next. On the upside, above 0.9566 minor resistance will turn intraday bias neutral again first.

In the bigger picture, the break of 0.9563 support, as well as 55 W EMA (now at 0.9672) argues that rebound from 0.9252 has completed at 0.9928. Medium term bearish is maintained with both 1.0095 resistance intact. Firm break of 0.9252 will resume the down trend from 1.2004 (2018 high).

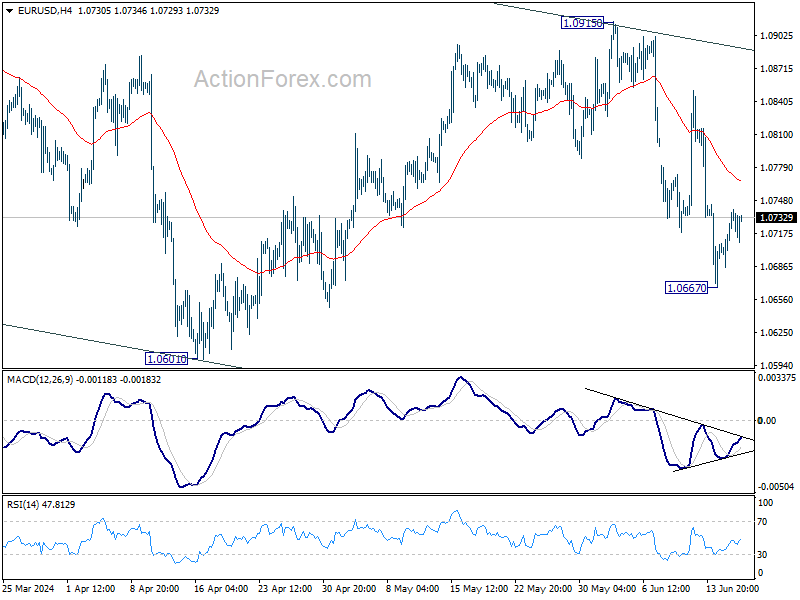

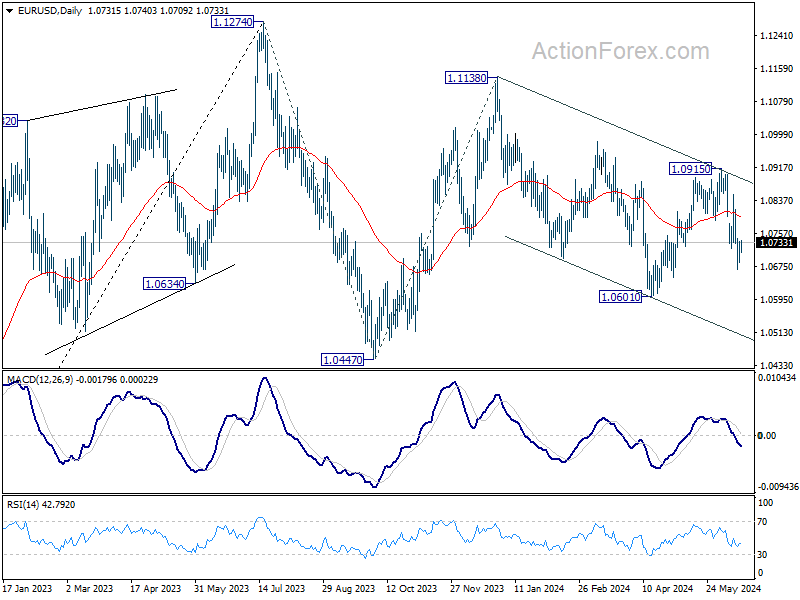

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0701; (P) 1.0719; (R1) 1.0753; More....

Intraday bias in EUR/USD remains neutral and some more consolidations could be seen above 1.0667. Further fall is expected as long as 55 4H EMA (now at 1.0765) holds. Fall from 1.0915 is seen as another leg in the larger corrective pattern. Below 1.0677 will target 1.0601 low first. Firm break there will target channel support at 1.0510 next.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's still in progress. Break of 1.0601 will target 1.0447 support and possibly further to 100% projection of 1.1274 to 1.0447 from 1.1138 at 1.0311. For now, this will remain the favored case as long as 1.0915 resistance holds, in case of rebound.

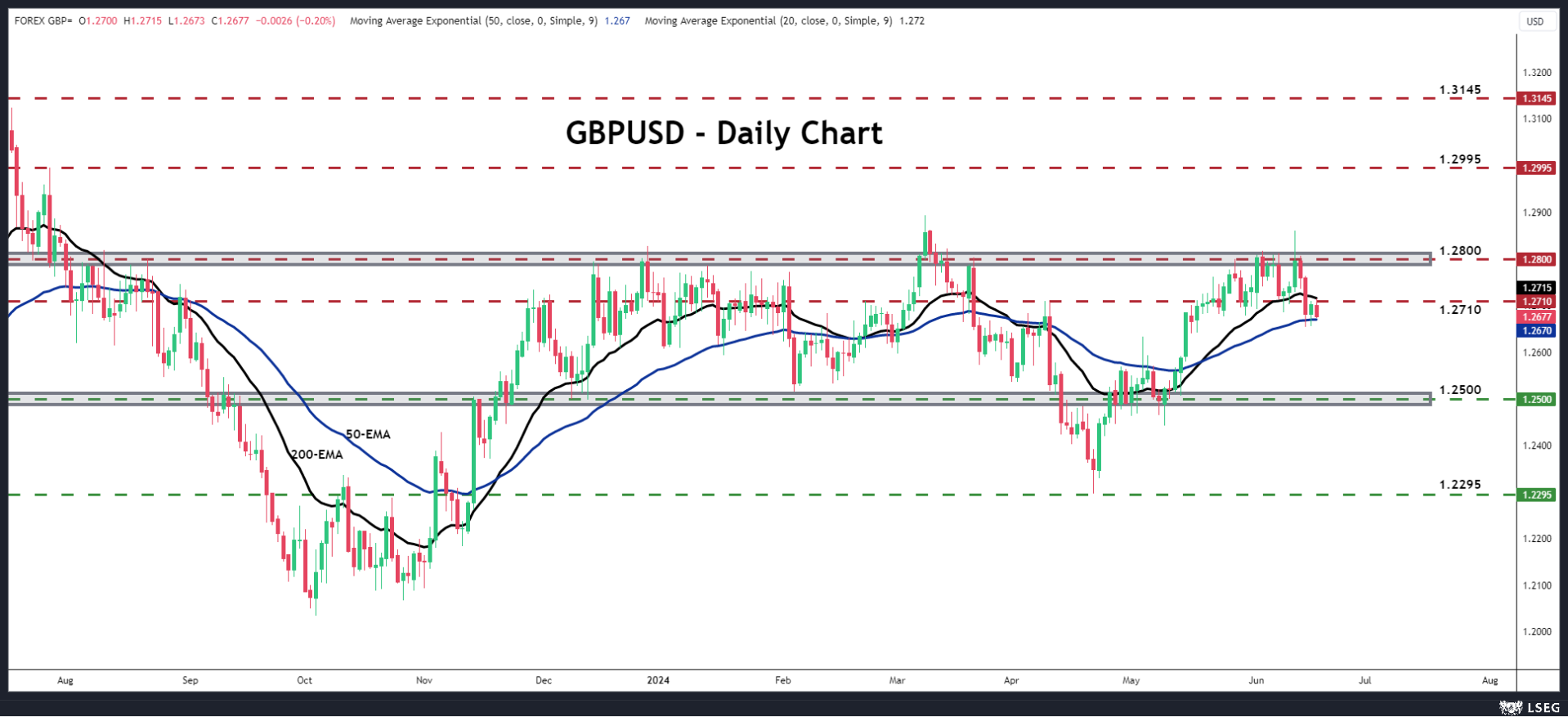

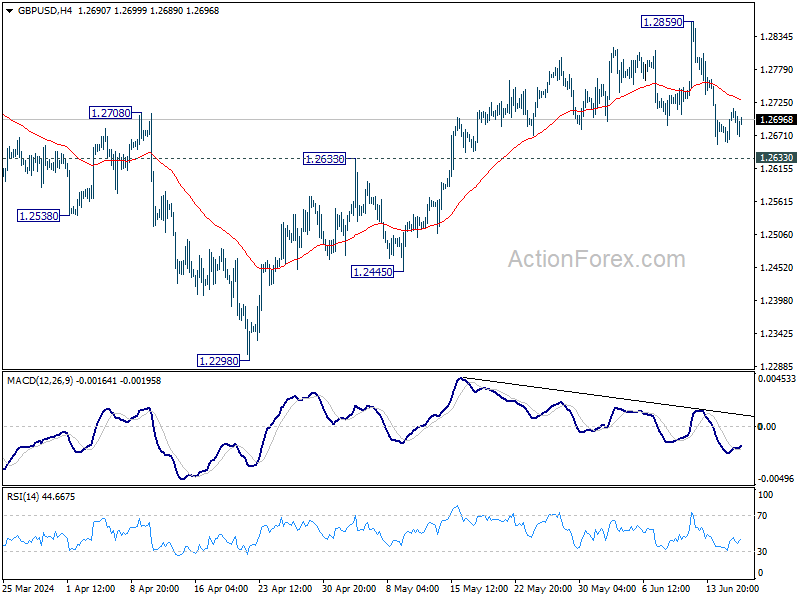

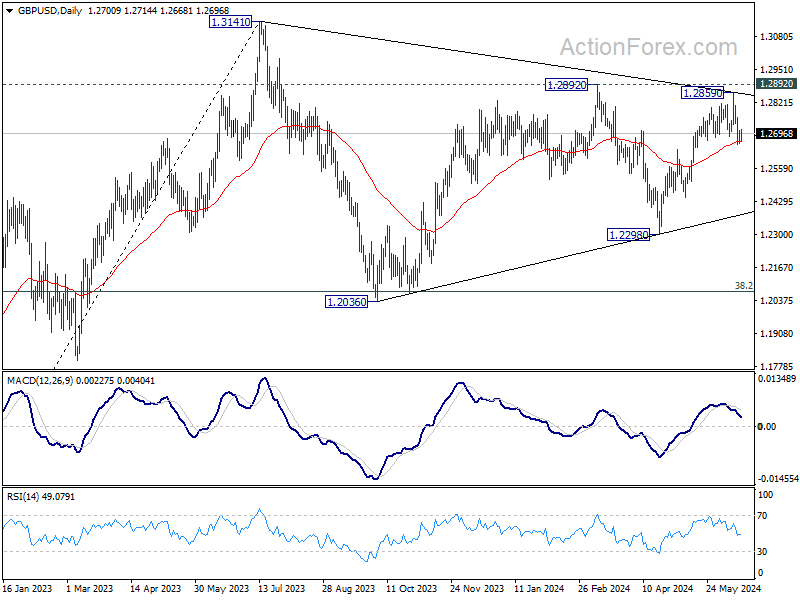

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2673; (P) 1.2691; (R1) 1.2724; More...

Intraday bias in GBP/USD remains neutral for the moment and some more consolidations would be seen. But risk will stay on the downside as long as 1.2859 resistance holds. Firm break of 1.2633 resistance turned support will argue that whole rise from 1.2298 has completed, and target 1.2445 and below.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2445 support will extend the corrective pattern with another decline instead.

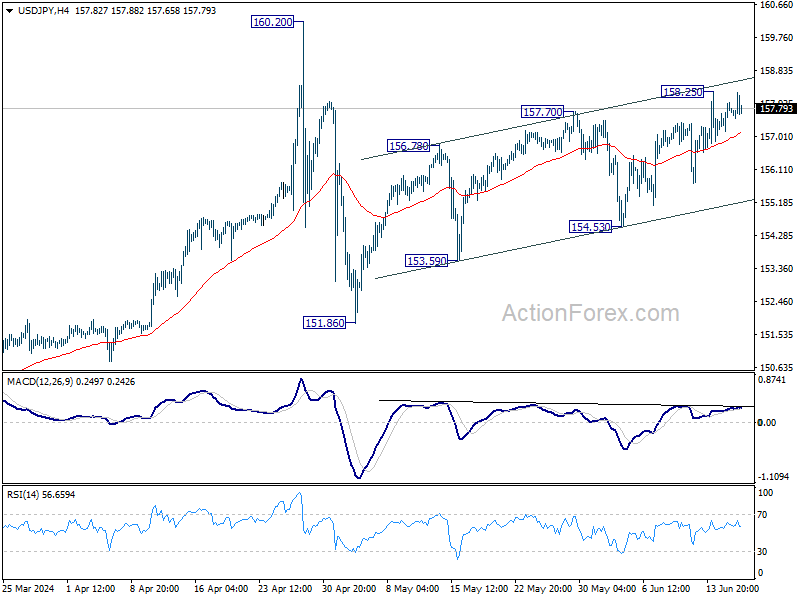

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 157.27; (P) 157.62; (R1) 158.07; More...

Intraday bias in USD/JPY remains neutral at this point. Further rally would be in favor as long as 154.53 support holds. Break of 158.25 will resume the choppy rise from 151.86 towards 160.20 high. But upside should be limited there, at least on first attempt.

In the bigger picture, price actions from 160.20 medium term top are seen as a corrective pattern to rise from 150.25 only. Another rally is still expected at a later stage through 160.02 to resume the larger up trend. However, decisive break of 150.87 will argue that larger correction is possibly underway, and target 146.47 support next.