Sample Category Title

Fed’s Williams: No urgency to cut interest rates

At the Semafor World Economy Summit today, New York Fed President John Williams there is no urgency in current monetary policy stance.

"We've got interest rates in a place that is moving us gradually to our goals. So I definitely don't feel urgency to cut interest rates. I think monetary policy is doing exactly what we would like to see," he said.

Williams underscored that while an increase in rates is not the expected course, it remains a possibility should the economic indicators necessitate such action to achieve Fed's inflation objectives.

Sunset Market Commentary

Markets

German Bund yields in fixed income markets gapped lower at the open this morning, catching up with US Treasuries late yesterday and in Asian dealings this morning. The drop was followed by a drift higher only to reverse course again after some comments from Villeroy. The French ECB governor said he’s open to rate cuts at each meeting after June, which would mean a total of five this year. Unrealistic, clearly, but after the recent Bund sell-off it didn’t go unnoticed. The Dutch policymaker Knot was more neutral, keeping the door open for June but calling discussions about what happens afterwards premature. We also want to give him credit for pimping Lagarde’s now widely used “we are not Fed-dependent” one-liner to “we aren’t the 13th Fed district”. Anyway, German yields do add a few basis points but that was probably inspired by reports of Israel and the US holding talks on a Rafah offensive. Oil prices extended earlier gains amid risks of geopolitical tensions flaring up again and that supported yields too. German rates add up to 3 bps at the front. US Treasuries marginally underperform, triggered by lower-than-expected weekly jobless claims (212k vs 215k) and an unexpected sharp improvement in the Philly Fed business outlook from 3.2 to 15.5 (2 expected) – the highest since April 2022. Prices paid, new orders and shipments all jumped with this 6-month ahead gauge suggesting solid growth going forward. On the flipside, the employment index edged down to -10.7 and the workweek index fell sharply from -0.2 to -18.7. US rates nevertheless extended earlier gains to trade between 2 and 4.2 bps higher across the curve. The US dollar found a bottom at the start of European dealings and clawed back some more losses after the data releases. DXY tries to recapture 106. EUR/USD is slightly down for the day, trading at around 1.065. USD/JPY bounced of the 154 big figure. Sterling found its composure after sliding against the euro yesterday. EUR/GBP eased to 0.8556 in, yet again, technically insignificant trading. European stock markets rise marginally to the tune of 0.2%. Equity markets on Wall Street open mixed with the likes of the S&P and Nasdaq coming close to first support levels around 4990 and 15596.

News & Views

The German Bundesbank turned a bit less negative the economy in its April monthly report. Contrary to what was expected last month, the Buba now thinks real GDP increased slightly in Q1. This expectations is based on recent slight increase in industrial production, which was supported by a rise in goods exports. Exceptionally mild weather in February also led to an extraordinarily strong increase in construction output. Even so, the Buba stays cautious on the recovery going forward. Higher financing costs and increased economic uncertainty are dampening investment activity. Demand for German industrial products from Germany and abroad remains weak. Private households continue to be hesitant in their spending, despite a fairly stable labor market, sharply rising wages & falling inflation rates. The Buba concludes that an increase in output in Q2 remains uncertain, but at the same time acknowledges recent improvement in business sentiment (Ifo), opening the possibility of the economy picking up more significantly than was expected until last month.

MPC member Jan Prochazka of the Czech National Bank (CNB) in an interview indicated that the bank should maintain the current pace of 50 bps rate cuts at the next policy meeting on May 2. Prochazka sees little room for the CNB to accelerate the process going forward. Prochazka draws comfort from headline inflation having returned to the 2% target, but remains concerned about the structure of price developments. The decline in headline inflation was mainly driven by food and energy costs, but there is basically no disinflation happening in services. In this respect an improvement in economic activity/domestic demand also is a reason for caution. Aside from persistent inflationary risks, hawkish signals from the US Fed are also seen as preventing the CNB from accelerating rate cuts. He labelled the delay in rate cuts abroad as the ‘biggest source of change’ in the CNB forecast. In this respect Prochazka indicated that he doesn’t see the need to push back against current market pricing which discounts the policy rate to be reduced to 4.0% in a 12-month horizon from 5.75% currently.

US, Japan Express Concern Over Japanese Yen

The Japanese yen is almost unchanged on Thursday. In the North American session, USD/JPY is trading at 154.44, up 0.03%.

It’s a light data calendar today. US unemployment claims were unchanged at 212,000 and the Philly Fed Manufacturing index surged to 15.5 in April, up from 3.5 in March and crushing the market estimate of 1.5. Early on Friday, Japan releases CPI for March, which is expected to tick higher to 2.8%, up from 2.7% in February.

It was just over a week ago that I posed the question of whether the 152 level was a line in the sand which would trigger intervention from Tokyo. The yen has broken below 152 and then some, dropping this week to 154.78, a new 34-low. Japan’s Ministry of Finance hasn’t intervened but the threat continues to hover over the markets.

The decline of the yen prompted the finance ministers of the US and Japan to issue a statement expressing their concern at a G-20 meeting in Washington this week. US Treasury Secretary Yellen and Japanese Finance Minister Suzuki agreed to “consult closely” on exchange rates and acknowledged “serious concerns” over the yen’s sharp depreciation.

With Fed Chair Powell dampening expectations of a Fed rate cut due to rising inflation, the yen could lose even more ground, which will increase the possibility of intervention to prop up the yen. It has been a dismal few months for the yen, which has plunged 9.7% against the dollar in 2024.

USD/JPY Technical

- USD/JPY tested resistance at 154.43 earlier. Above, there is resistance at 154.71

- There is support at 154.11 and 153.83

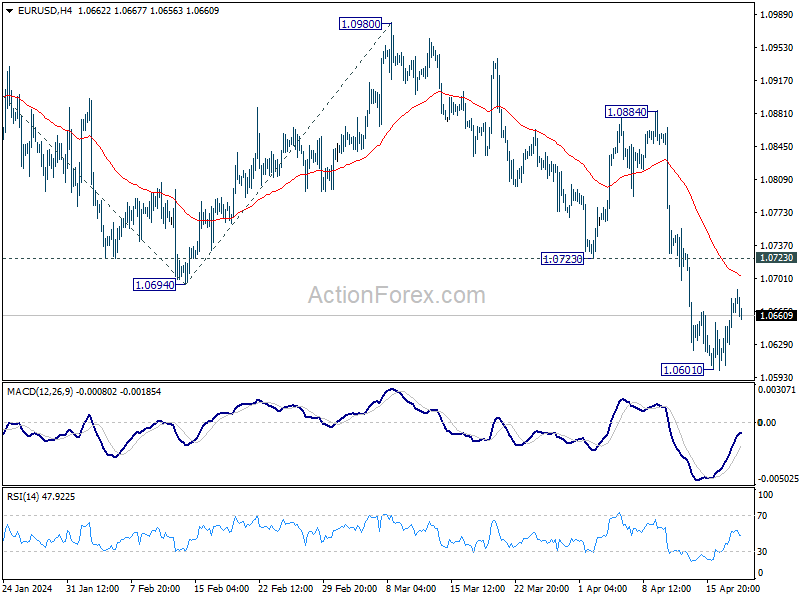

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0626; (P) 1.0653; (R1) 1.0700; More...

EUR/USD is staying in consolidation from 1.0601 and intraday bias stays neutral. While stronger recovery cannot be ruled out, upside should be limited by 1.0723 support turned resistance. On the downside, break of 1.0601 will resume the decline from 1.1138 to 100% projection of 1.1138 to 1.0694 from 1.0980 at 1.0536 next.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Current fall from 1.1138 is seen as the third leg. While deeper decline is would be seen to 1.0447 and possibly below. Strong support should emerge from 61.8% retracement of 0.9534 to 1.1274 at 1.0199 to complete the correction.

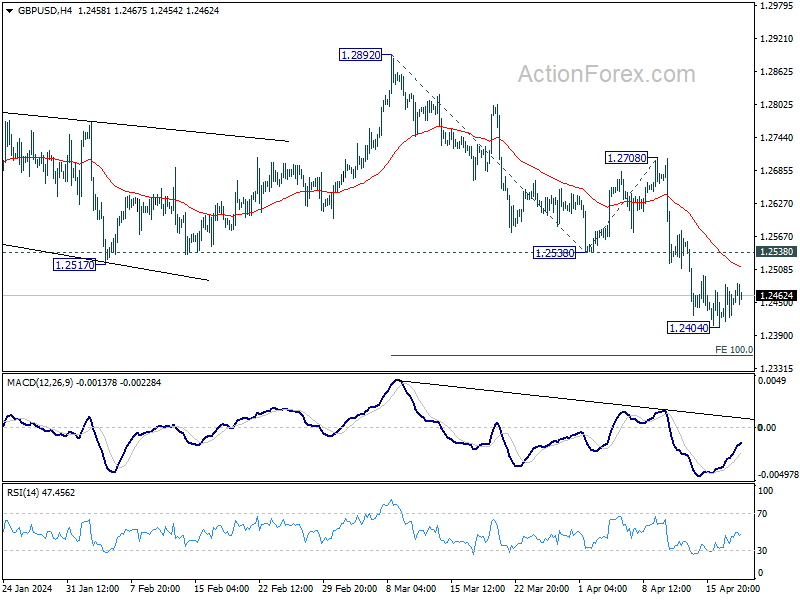

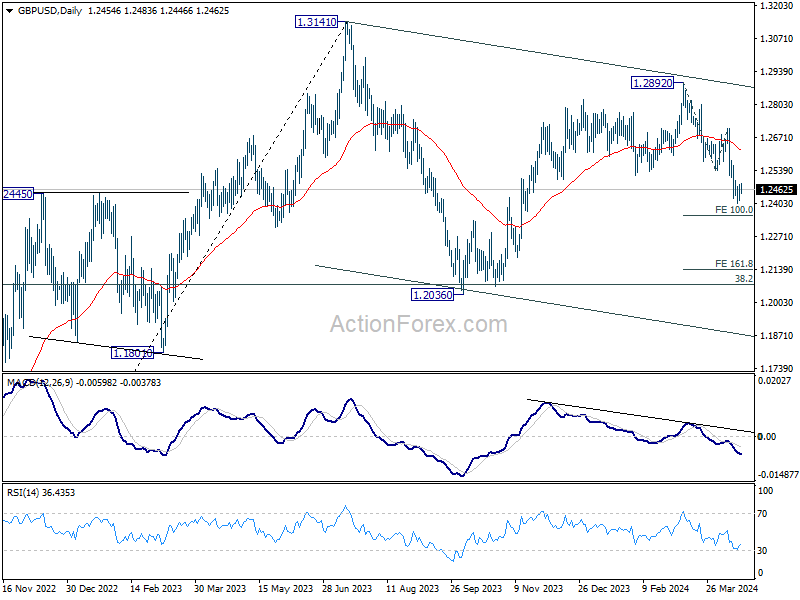

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2421; (P) 1.2451; (R1) 1.2486; More...

Intraday bias in GBP/USD remains neutral as consolidation from 1.2404 is extending. Upside of recovery should be limited by 1.2538 support turned resistance to bring another fall. On the downside, firm break of 1.2404 will resume the decline from 1.2892 to 100% projection of 1.2892 to 1.2538 from 1.2708 at 1.2354. Firm break there will target 161.8% projection at 1.2207 next.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Fall from 1.2892 is seen as the third leg. Deeper decline would be seen to 1.2036 support and possibly below. But strong support should emerge from 61.8% retracement of 1.0351 to 1.2452 at 1.1417 to complete the correction.

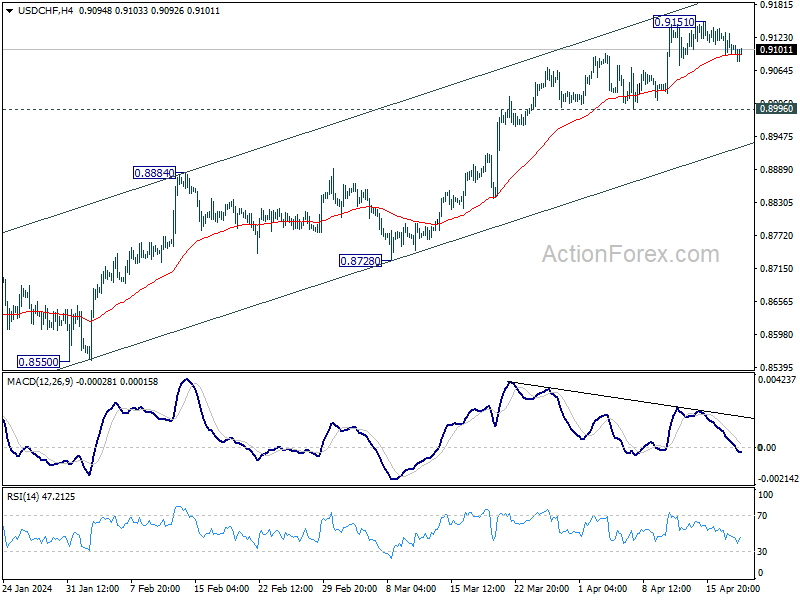

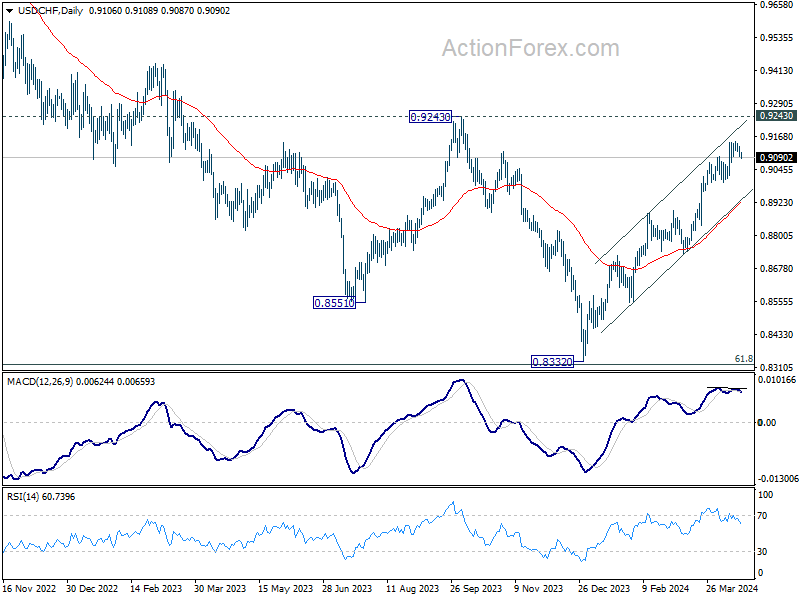

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9088; (P) 0.9115; (R1) 0.9135; More....

No change in USD/CHF's outlook as consolidation from 0.9151 is extending. While deeper pullback cannot be ruled out, further rally is expected as long as 0.8996 support holds. Firm break of 0.9151 will target 0.9243 key resistance next.

In the bigger picture, price actions from 0.8332 medium term bottom as tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8728 support holds. But upside should be limited by 0.9243 resistance, at least on first attempt. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish.

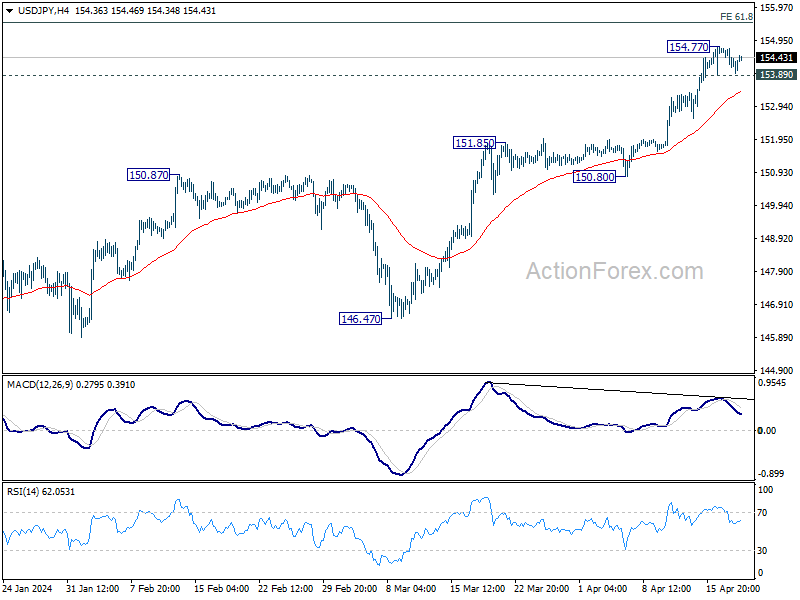

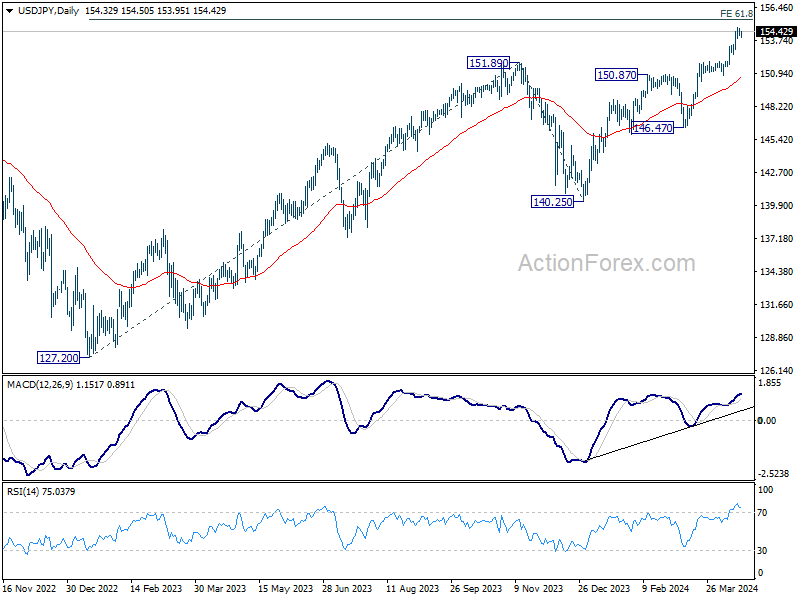

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 154.11; (P) 154.43; (R1) 154.71; More...

Intraday bias in USD/JPY remains neutral for the moment. Considering bearish divergence condition in 4H MACD, in case of another rise, upside should be limited by 155.20 fibonacci projection level. On the downside, break of 153.89 minor support will turn bias back to the downside for 55 4H EMA (now at 153.41) and possibly below.

In the bigger picture, current rise from 140.25 is seen as the third leg of the up trend from 127.20 (2023 low). Next target is 61.8% projection of 127.20 to 151.89 from 140.25 at 155.20. Outlook will now remain bullish as long as 146.47 support holds, even in case of deep pullback.

Currency Markets in Consolidations, Stocks Could be Stabilizing

The forex markets are still generally staying in consolidative mode today, showing minimal reaction to the latest economic data and comments from central bank officials. Commodity currencies, along with Swiss Franc, are displaying relative strength. Meanwhile, Euro, Dollar, and Yen are on the weaker side.

In the broader financial markets, the recent selloff in global equities seems to have found some temporary stability, though downside risks persist. Gold hovering just below 2400 mark, with prospect for an rising leg towards the critical 2500 resistance level, before forming a major bottom. WTI crude oil is retreating this week, but market participants remaining vigilant for any geopolitical escalations, particularly any retaliatory actions by Israel against Iran.

Technically, buying appeared to be emerging in Nikkei today as it approached 38.2% retracement of 30487.67 to 41087.75 at 37038.51. Firm break of 55 D EMA (now at 38058.00) will argue that the pull back from 41087.75 has completed, and bring stronger rebound. The upcoming CPI data from Japan could be crucial in determining the Nikkei's next moves.

In Europe, at the time of writing, FTSE is up 0.14%. DAX is down -0.10%. CAC is up 0.16%. UK 10-year yield is down -0.002 at 4.262. Germany 10-year yield is up 0.009 at 2.478. Earlier in Asia, Nikkei rose 0.31%. Hong Kong HSI rose 0.82%. China Shanghai SSE rose 0.09%. Singapore Strait Times rose 1.05%. Japan 10-year JGB yield is down -0.0165 at 0.871.

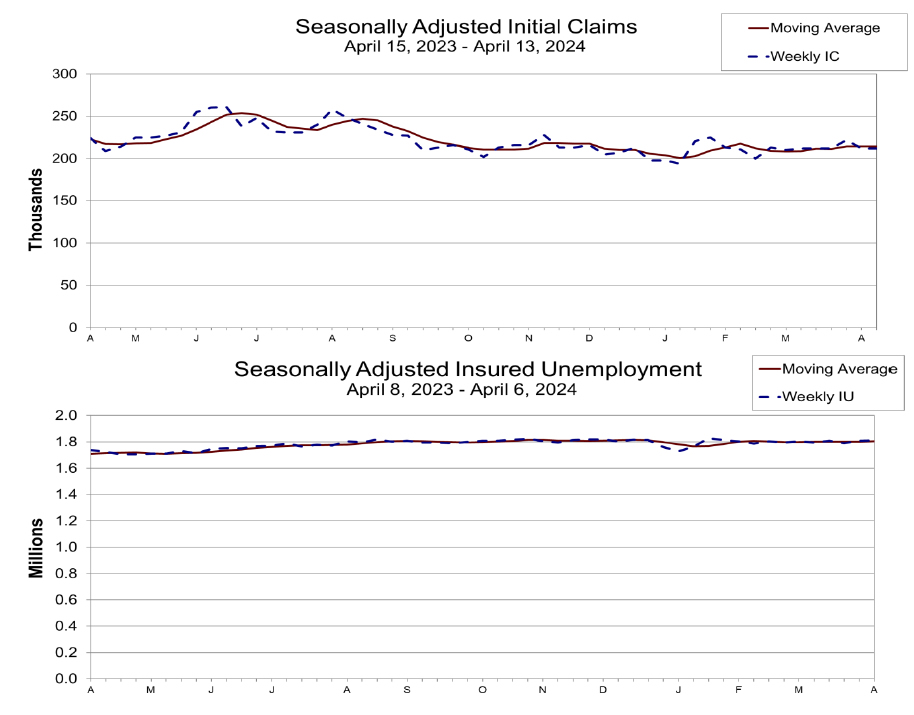

US initial jobless claims unchanged at 212k, vs exp 214k

US initial claims was unchanged at 212k in April 13, slightly below expectation of 214k. Four-week moving average of initial claims was also unchanged at 214.5k.

Continuing claims rose 2k to 1812k in the week ending April 6. Four-week moving average of continuing claims rose 4k to 1805k.

Bundesbank highlights modest improvement in German economy with ongoing risks

Bundesbank, in its latest monthly report, suggested some improvement in the German economy though underlying weaknesses remain. The report notes, "Germany's economic situation has brightened somewhat, but it remains weak at its core," signaling uncertainty about the sustainability of economic growth into the second quarter.

Despite these challenges, there has been a noticeable rise in optimism among consumers, businesses, and investors, potentially setting the stage for a stronger economic recovery than previously anticipated. The Bundesbank highlights, "If this improvement continues, the economy could also pick up more significantly than was expected a month ago."

However, the report also points out several areas of concern. Industry continues to struggle, and the construction sector might see a downturn following a temporary boost from a mild winter. Furthermore, high interest rates are suppressing investment activities, and while export demand shows weakness, consumer spending remains restrained despite favorable conditions in the labor market, such as rising wages and slowing inflation.

ECB's de Guindos: We have been crystal clear on June rate cut

During a European Parliament hearing today, ECB Vice President Luis de Guindos stated that ECB has been "crystal clear" on its conditional guidance regarding interest rate cut.

"If things continue as they have been evolving lately, in June we'll be ready to reduce the restriction of our monetary policy stance," he said.

While financial markets anticipate a total of 75bps in rate cuts for the year, de Guindos remained non-committal about specific future rate levels.

He pointed out several risks to inflation outlook, including wage dynamics, productivity, unit labor costs, profit margins, and geopolitical tensions.

BoJ's Noguchi: Poicy rate adjustment expected to be slow

BoJ Board Member Asahi Noguchi highlighted in a speech today the unique economic conditions facing Japan compared to other major economies. He pointed out that any changes to the policy rate are expected to occur at a slower pace than those seen in recent actions by other major central banks.

"With regard to the pace of policy rate adjustment, it is expected to be slow, at a pace that cannot be compared to that of other major central banks in recent years," Noguchi stated. This approach reflects the central bank's assessment that it will take considerable time for Japan to consistently achieve its price stability target of 2% inflation.

Noguchi also noted the recent significant wage increases in Japan, describing them as unprecedented. However, he cautioned that these wage hikes alone are not yet sufficient to drive up prices to the level needed for trend inflation to stabilize at the 2% target.

"It is essential for the BoJ to maintain its ultra-loose monetary policy to seek an appropriate balance in the labour supply-demand," he added.

Australia's employment contracts -6.6k in Mar, labor market still relatively tight

Australia's employment figures for March revealed a slight contraction of -6.6k, worse than expectation of 7.2k growth. This downturn was primarily due to drop in part-time employment by -34.5k, partially offset by rise in full-time by 27.9k.

Unemployment rate rose from 3.7% to 3.8%, below expectation of 3.9%. Participation rate fell from 66.7% to 66.6%. Monthly hours worked rose 0.9% mom.

Bjorn Jarvis, Head of Labour Statistics at ABS, noted, "The labour market remained relatively tight in March, with an employment-to-population ratio and participation rate still close to their record highs in November 2023." He pointed out that although there has been a modest decline of 0.4 percentage points since the highs of last November, the metrics remain substantially above pre-pandemic levels.

Australia NAB business confidence rises to -2 in Q1, cost pressures ease slightly

Australia NAB Quarterly Business Confidence rose from -6 to -2 in Q1. Business Conditions was unchanged at 10. In terms of forward-looking expectations, businesses anticipate a slight downturn in conditions over the next three months, with expectations dipping from 14 to 12. However, the outlook for the next 12 months improved, rising from 16 to 17.

According to NAB Chief Economist Alan Oster, "Consistent with our monthly business survey, today's release shows business conditions remained resilient at above-average levels through the start of the year. Confidence remained weak but showed some improvement relative to the tail end of 2023."

The report also highlighted easing cost pressures, although the reduction was minimal. Labor costs grew at a slightly reduced rate of 1.2%, down from 1.3% in the previous quarter, and purchase costs increased by 1.1%, down from 1.2%. Meanwhile, final product price growth remained steady at 0.7%, and retail price growth decreased marginally to 0.8% from 0.9%.

Oster noted, "There continue to be some positive signs of easing cost pressures for businesses but progress was more incremental through Q1. Importantly, forward-looking indicators of firms' expectations for price growth suggest firms expect some further moderation."

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 154.11; (P) 154.43; (R1) 154.71; More...

Intraday bias in USD/JPY remains neutral for the moment. Considering bearish divergence condition in 4H MACD, in case of another rise, upside should be limited by 155.20 fibonacci projection level. On the downside, break of 153.89 minor support will turn bias back to the downside for 55 4H EMA (now at 153.41) and possibly below.

In the bigger picture, current rise from 140.25 is seen as the third leg of the up trend from 127.20 (2023 low). Next target is 61.8% projection of 127.20 to 151.89 from 140.25 at 155.20. Outlook will now remain bullish as long as 146.47 support holds, even in case of deep pullback.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | NAB Business Confidence Q1 | -2 | -6 | ||

| 01:30 | AUD | Employment Change Mar | -6.6K | 7.2K | 116.5K | 117.6K |

| 01:30 | AUD | Unemployment Rate Mar | 3.80% | 3.90% | 3.70% | |

| 01:30 | AUD | RBA Bulletin Q1 | ||||

| 04:30 | JPY | Tertiary Industry Index M/M Feb | 1.50% | 0.80% | 0.30% | -0.50% |

| 06:00 | CHF | Trade Balance (CHF) Mar | 3.54B | 3.22B | 3.66B | 3.68B |

| 08:00 | EUR | Eurozone Current Account (EUR) Feb | 29.5B | 45.2B | 39.4B | |

| 12:30 | USD | Initial Jobless Claims (Apr 12) | 212K | 214K | 211K | 212K |

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Apr | 15.5 | 0.8 | 3.2 | |

| 14:00 | USD | Existing Home Sales Mar | 4.20M | 4.38M | ||

| 14:30 | USD | Natural Gas Storage | 54B | 24B |

US initial jobless claims unchanged at 212k, vs exp 214k

US initial claims was unchanged at 212k in April 13, slightly below expectation of 214k. Four-week moving average of initial claims was also unchanged at 214.5k.

Continuing claims rose 2k to 1812k in the week ending April 6. Four-week moving average of continuing claims rose 4k to 1805k.

Bundesbank highlights modest improvement in German economy with ongoing risks

Bundesbank, in its latest monthly report, suggested some improvement in the German economy though underlying weaknesses remain. The report notes, "Germany's economic situation has brightened somewhat, but it remains weak at its core," signaling uncertainty about the sustainability of economic growth into the second quarter.

Despite these challenges, there has been a noticeable rise in optimism among consumers, businesses, and investors, potentially setting the stage for a stronger economic recovery than previously anticipated. The Bundesbank highlights, "If this improvement continues, the economy could also pick up more significantly than was expected a month ago."

However, the report also points out several areas of concern. Industry continues to struggle, and the construction sector might see a downturn following a temporary boost from a mild winter. Furthermore, high interest rates are suppressing investment activities, and while export demand shows weakness, consumer spending remains restrained despite favorable conditions in the labor market, such as rising wages and slowing inflation.