Sample Category Title

Oil, Gold Jump as Israel Responds

Oil and gold jumped on rising geopolitical tensions after Israel struck targets in western Iran as a response to last weekend’s attacks. One of the concerned cities is Isfahan, home to several military bases and facilities, but also to nuclear facilities including the main technology center. Iran said that the nuclear site is safe. Bloomberg journalists highlighted that as Iran’s weekend attack – which was designed to warn rather than to destroy - Israel bombing remained in the ‘realm of gaming out ‘calibrated’ actions to send messages without raising stakes. But uncertainty looms. Brent crude traded above the $90pb before easing to around $88.50 at the time of writing, US crude shortly trade past the $86pb level, wheat futures jumped 2%, gold rebounded to a near-record level and Swiss franc gained. We will likely see a further flight to safety before the weekly closing bell on fear of further escalation of tensions during the weekend. Shorting oil and gold is risky as Middle East is boiling. Having exposure to these commodities is a good hedge against the rising geopolitical tensions in the region.

In other hot commodity news, cocoa futures jumped close to 10% yesterday to above $11’000 per ton, and a hedge manager called Pierre Andurand said that the shortages will push the price of a ton of cocoa to $20K. For those who love speculation and adrenaline, cocoa futures is the place to be.

Unimpressed

Elsewhere, tech investors didn’t necessarily bought into TSM’s better-than-expected revenue and earnings compared to the same time last year. They were rather disappointed with a 5% decline in revenue and income compared to the last quarter. The company dialed back its outlook for the chip market expansion due to weakness in smartphones, personal computers and car industry but said that accelerating demand for AI chips should compensate for that weakness and justify spending for capacity expansion and upgrades. They expect their revenue to grow at least 20% this year. But alas, anything less than mind-blowing is not enough for the chip rally to continue given the latest exponential rise. TSM shares fell nearly 5% after the results yesterday, while Micron Technology, which was up pre-market on news that they will get more than $6 billion in grants from the US government for their domestic factory projects, ended up falling almost 4%. The S&P500 extended losses and Nasdaq 100 retreated to near its 100-DMA.

Netflix reported results after the closing bell yesterday and surprised with a third month of blowout subscriptions growth. The company added more than 9 million new watchers in Q1 2024 and posted its best start to a year since the pandemic. The password sharing ban continued to boost Netflix subscriptions as company estimated that they were around 100 mio people using an account without paying for it. Apparently, the password sharing ban convinced a lot of them that Netflix is worth paying for. Unfortunately, Netflix lost almost 5% in the afterhours trading as its Q2 revenue forecast failed to impress. They also said that they will stop reporting quarterly subscribers next year… What a disappointment, that was the most interesting thing to watch in Netflix quarterly results… In terms of market price, Netflix will slip below its 50-DMA today and the toppish signs goes beyond Netflix.

Overall

US jobless claims came in lower than expected, the Philly Fed manufacturing index unexpectedly jumped . Fed’s Raphael Bostic said that he doesn’t expect a rate cut until the end of this year, Neel Kashkari said that the Fed could ‘potentially’ hold its rates steady all year and John Williams said that there is no urgency to cut rates and that he doesn’t rule out a rate hike, though this is not his base case scenario. But the US 2-year yield remained capped near the 5% psychological mark despite strong data and hawkish comments indicating that investors are hesitant to give up their final hope of seeing the Fed loosen its policy.

The EURUSD is under a renewed downside pressure as the divergence between the hawkish Fed and dovish ECB expectations justifies a further weakness in the single currency. The USDJPY remained offered as core inflation in Japan eased more than expected by analysts to 2.6%. We are still waiting for the Japanese authorities to stop the bleeding as they said they would if the selloff became unsustainable…

The US futures are in the negative at the time of writing. The rising hawkish voices from the Fed back further weakness in stocks, especially the rate-sensitive tech stocks. Unfortunately, the quarterly results from the world’s leading chip and chip equipment makers failed to satisfy this week and set the tone for a – maybe – challenging earnings season for chip companies. And if that’s the case, we could see the risk rally fade into May… which is known to be the month where investors sell and go away.

Markets on Alert After Reports of Explosion Near Iranian Military Base

In focus today

Today is a quiet day on the data front. We will monitor the situation in the Middle East after reports of explosions in the Iranian city of Isfahan which houses a military base. See more below.

In Sweden, the market is likely to continue to digest the messages from Riksbank's Bunge and Jansson yesterday, arguing the weaker SEK and delayed Fed monetary easing will influence the decision between a May and June rate cut. We believe this supports our take for the latter.

Economic and market news

What happened overnight

Reports of an explosion in Iran, near the city of Isfahan which houses a major military base, renewed fears about an escalation in the Israel/Iran conflict. Iranian officials say explosions were due to Iran's air defence system destroying three drones rather than missiles, Reuters reports. Israel has not commented, but Bloomberg reports Israeli officials had notified the US earlier Thursday that they planned to retaliate in the next 24-48 hours, according to two US officials who asked not to be identified discussing private conversations. Oil prices regained some of its earlier losses to hit 89.1 USD/bbl. (+2%) as of this morning, and safe-haven assets such as gold (+0.4%) and the CHF gained, while Asian equities slid.

Japan nationwide CPI was largely in line with earlier Tokyo data, as the core CPI slowed to 2.6% y/y in March, and "core-core" CPI (excl. fresh food and energy) slowed to 2.9% from 3.2% in February. The moves were in line with market expectations.

What happened yesterday

More hawkish signals from the US, with the Philly Fed's prices paid index jumping to 23.0 in April (prior: 3.7) which markets took as another sign that price pressures are still too high. Flat jobless claims and hawkish comments from Fed officials once again pointed to fewer rate cuts this year. The greenback gained during the day and the US 10Y government yield was up 6bp as of last night.

In Japan, the fourth wage tally from Rengo showed a total pay rise of 5.2%. This is promising news for the Bank of Japan's hopes of sustained demand driven inflation. However, it is still unclear how broad-based these wage jumps will be, with signs that there will be a big pay rise gap between large and small businesses as a Teikoku survey showing 23% of surveyed businesses have not raised wages at all, meaning the effect on domestic demand may not be as great as the BoJ could hope.

Several ECB policymakers all but confirmed a June rate cut with Villeroy saying there was a "very large consensus" for a June cut, and ECB VP de Guindos stating the central bank would be "ready to reduce the restriction" of monetary policy if things evolve as expected. Things are less clear for the meetings in between quarterly projections. Villeroy, Simkus and Cipollone have all suggested that July is not off the table while others (Knot) have indicated potential cuts will coincide with new quarterly forecasts.

Metal price indices continued to trend up with the LMEX index up 1.5% for the day. The turn in the manufacturing cycle has been supporting metal prices which have increased for a while now (LMEX +13.1% YTD). On top of this, new US and UK sanctions on Russian metals have given supply-side pressure. Rising commodity prices are an upside risk to inflation and thus could complicate the outlook for global rates.

Equities: Global equities were lower again yesterday increasing the streak of losses to 5 days with MSCI world being down almost 5% from the peak. Sell-off again led by US tech sector, growth, and long duration stocks. While the sell-off initially happened alongside higher yields and increasing VIX, that has not been the case the last couple of days when yields have been moving more sideways while VIX has been ticking lower. In US yesterday, Dow +0.1%, S&P 500 -0.2%, Nasdaq -0.5% and Russell 2000 -0.3%. Markets in Asia are lower this morning, though off their lows as the Middel East crisis and uncertainty has increased this morning after Israel launched a retaliatory attack on Iran. Futures in US and Europe are lower this morning as well.

FI: Long-end rates drifted higher in yesterday's session as Philly-Fed confirmed the recent signs of a global manufacturing rebound taking place. The UST curve flattened slightly from the front end with the 10Y tenor peaking at 4.65%. 10Y Bunds ended the session 3bp higher at 2.50%. Overnight, the Israeli attacks on Iranian territory have led to a classic risk-off reaction in markets with Asian equity indices down, oil prices rising (Brent briefly above USD90) and bonds gaining traction (10Y USTs now at 4.55%). The risk of further escalation will be today's focus.

FX: Safe haven currencies rallied alongside US Treasuries, Brent oil temporarily moved back above USD 90/bbl and equities took a dive as the conflict in the Middle East escalated overnight. Some of the initial moves have reversed though. EUR/USD tested the downside but remains within 1.06-1.07. USD/JPY dropped sharply but is back above 154. USD/CHF knee-jerked toward 0.90 but has recovered closer to 0.91. Scandies in general came under pressure. USD/SEK made a new year high at 11.03 but is back below the 11.00 mark.

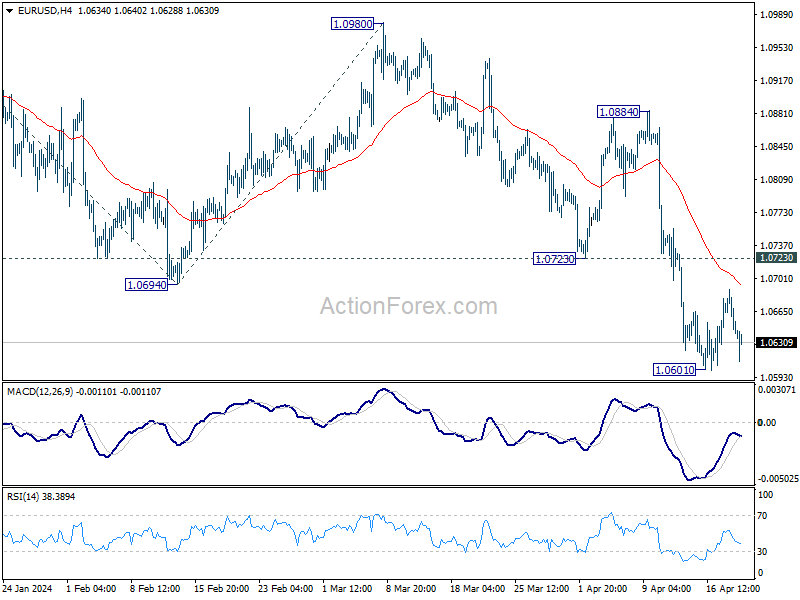

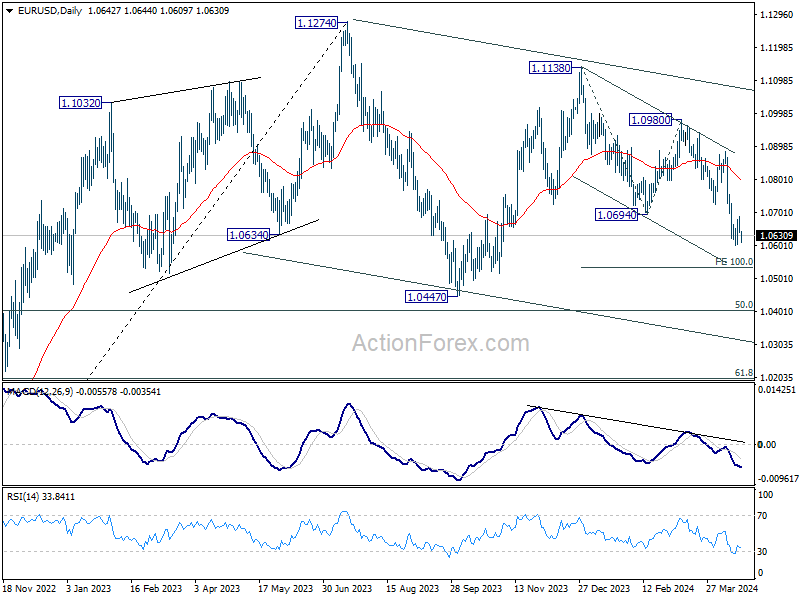

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0626; (P) 1.0658; (R1) 1.0675; More...

Range trading continues in EUR/USD and intraday bias remains neutral. While stronger recovery cannot be ruled out, upside should be limited by 1.0723 support turned resistance. On the downside, break of 1.0601 will resume the decline from 1.1138 to 100% projection of 1.1138 to 1.0694 from 1.0980 at 1.0536 next.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Current fall from 1.1138 is seen as the third leg. While deeper decline is would be seen to 1.0447 and possibly below. Strong support should emerge from 61.8% retracement of 0.9534 to 1.1274 at 1.0199 to complete the correction.

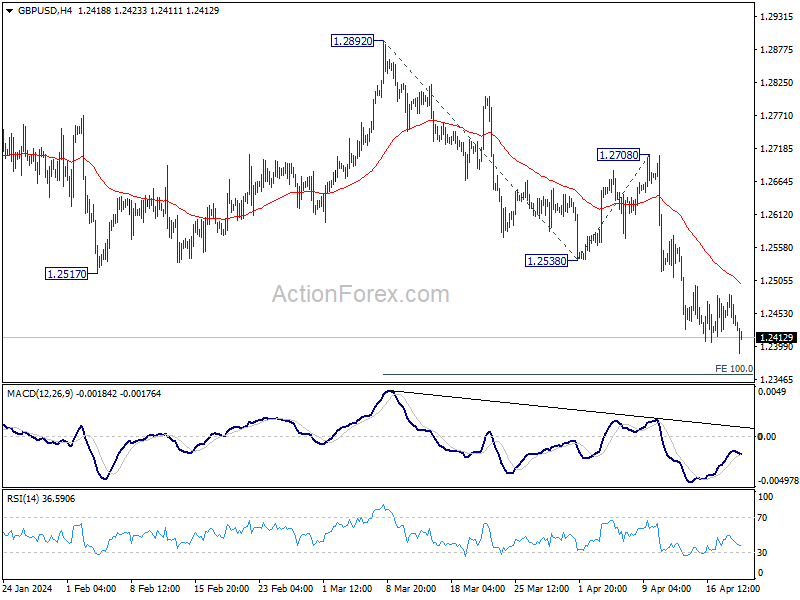

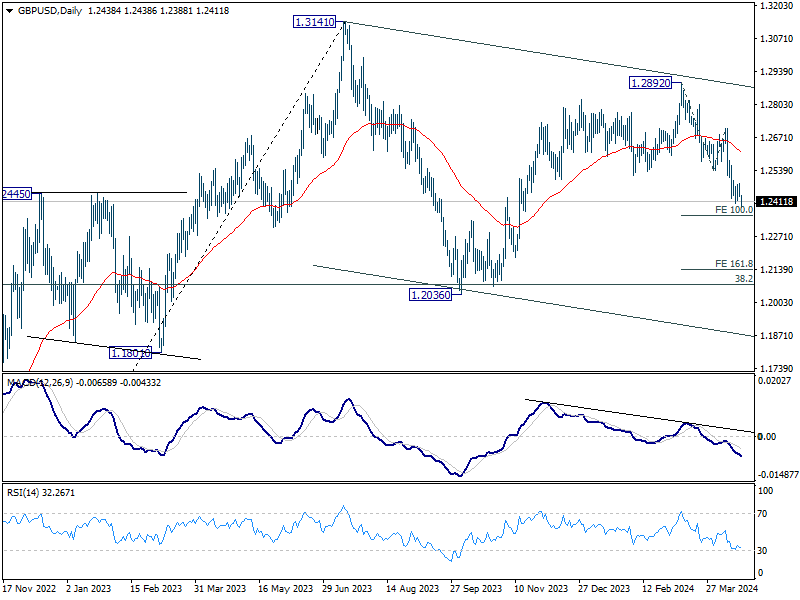

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2418; (P) 1.2452; (R1) 1.2469; More...

Intraday bias in GBP/USD is back on the downside as fall from 1.2892 resumes. Deeper decline would be seen to 100% projection of 1.2892 to 1.2538 from 1.2708 at 1.2354. Firm break there will target 161.8% projection at 1.2207 next. On the upside, above 1.2483 resistance will turn intraday bias neutral again first.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Fall from 1.2892 is seen as the third leg. Deeper decline would be seen to 1.2036 support and possibly below. But strong support should emerge from 61.8% retracement of 1.0351 to 1.2452 at 1.1417 to complete the correction.

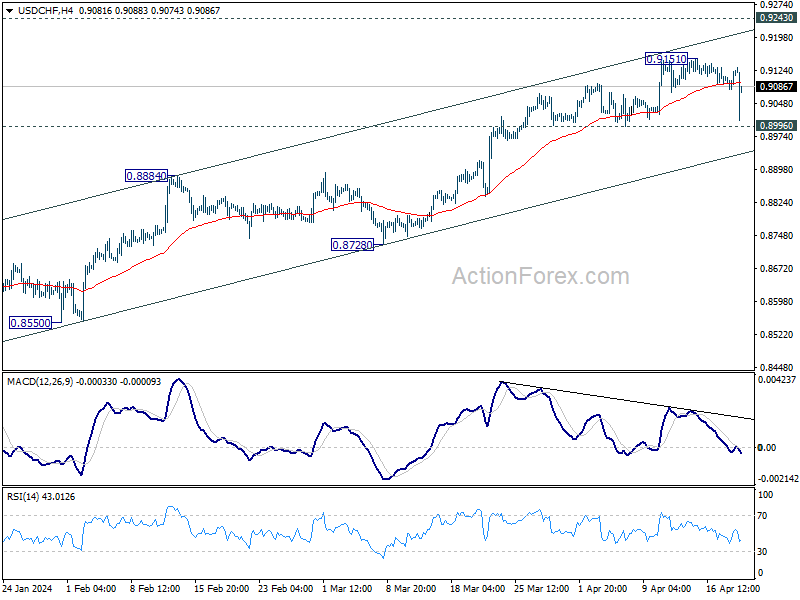

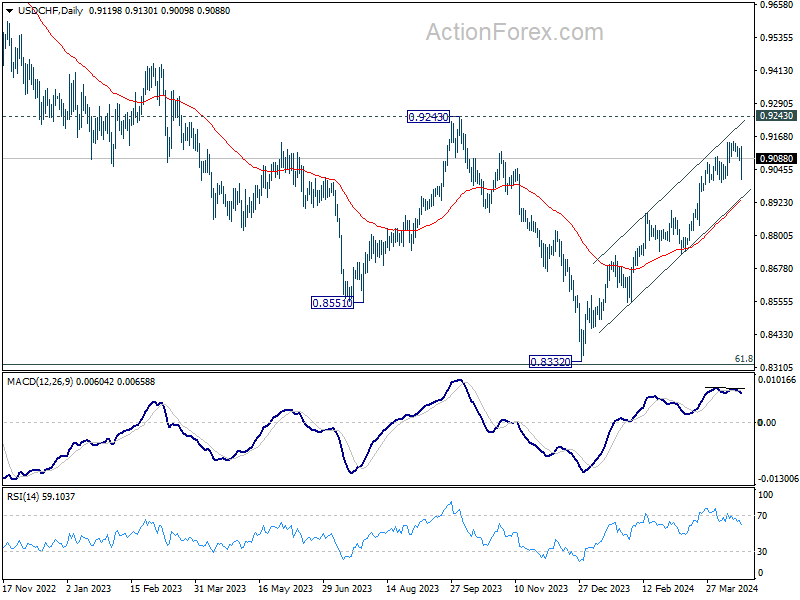

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9095; (P) 0.9110; (R1) 0.9140; More....

While USD/CHF's pull back from 0.9151 extended lower, down side is supported above 0.8996 support so far. Intraday bias remains neutral and further rally is expected. Break of 0.9151 will resume larger rally from 0.8332 to 0.9243 resistance. However, firm break of 0.8996 will confirm short term topping, and turn bias to the downside for 55 D EMA (now at 08932).

In the bigger picture, price actions from 0.8332 medium term bottom as tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8728 support holds. But upside should be limited by 0.9243 resistance, at least on first attempt. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish.

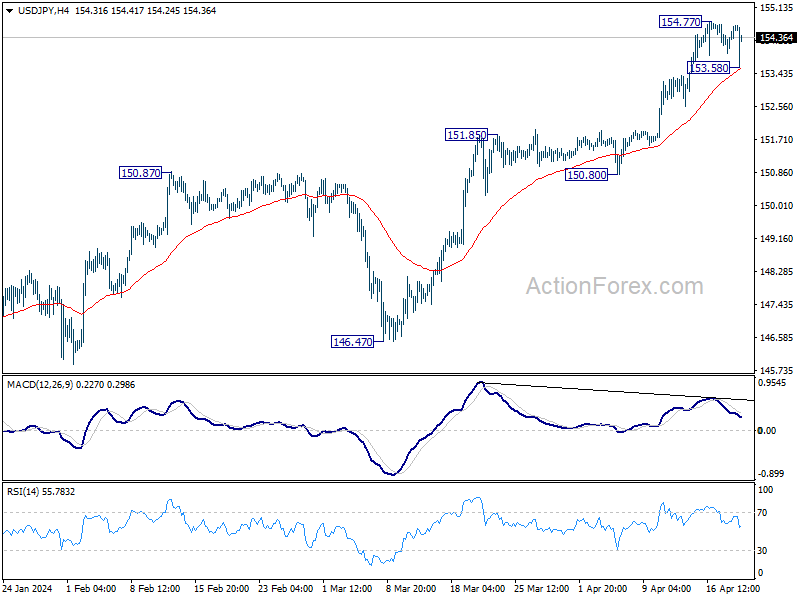

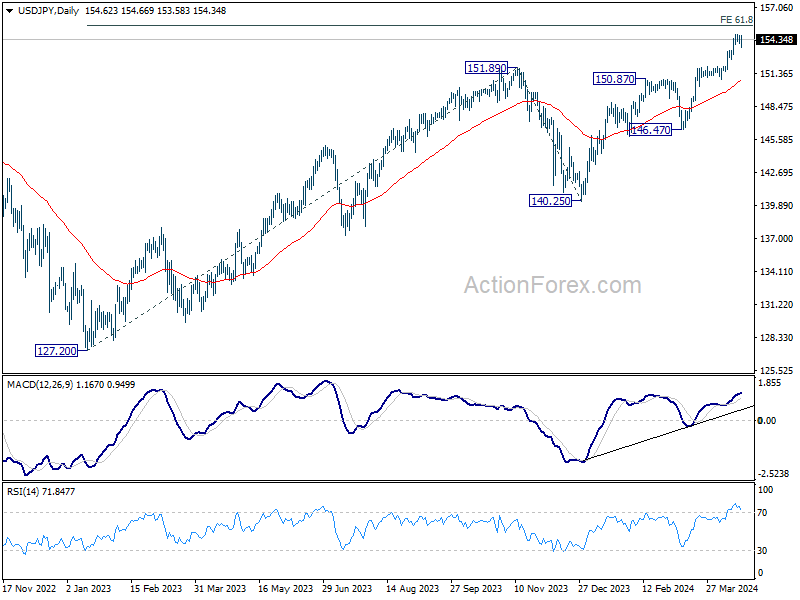

USD/JPY Daily Outlook

Daily Pivots: (S1) 154.18; (P) 154.43; (R1) 154.90; More...

USD/JPY's correction from 154.77 extended lower to 153.58 but recovered just ahead of 55 4H EMA (now at 153.56). Intraday bias remains neutral first. On the upside, break of 154.77 will resume larger up trend. But considering divergence condition in 4H MACD upside should be limited by 155.20 fibonacci projection level. On the downside, below 153.58 will turn bias to the downside for deeper pullback.

In the bigger picture, current rise from 140.25 is seen as the third leg of the up trend from 127.20 (2023 low). Next target is 61.8% projection of 127.20 to 151.89 from 140.25 at 155.20. Outlook will now remain bullish as long as 146.47 support holds, even in case of deep pullback.

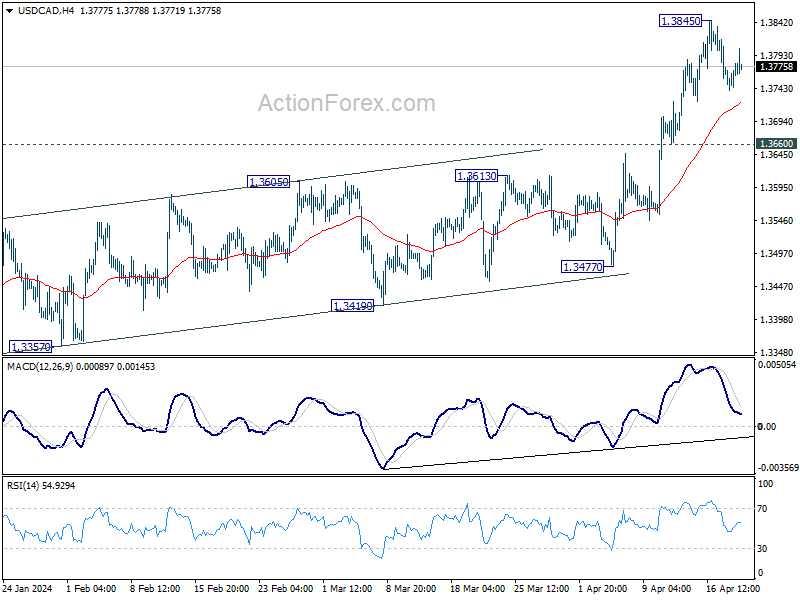

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3745; (P) 1.3765; (R1) 1.3788; More...

Intraday bias in USD/CAD is turned neutral with current recovery. Corrective pattern from 1.3845 could extend lower. But downside should be contained by 1.3660 support to bring another rally. Break of 1.3845 will resume the whole rally from 1.3716 to 1.3976 key resistance.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

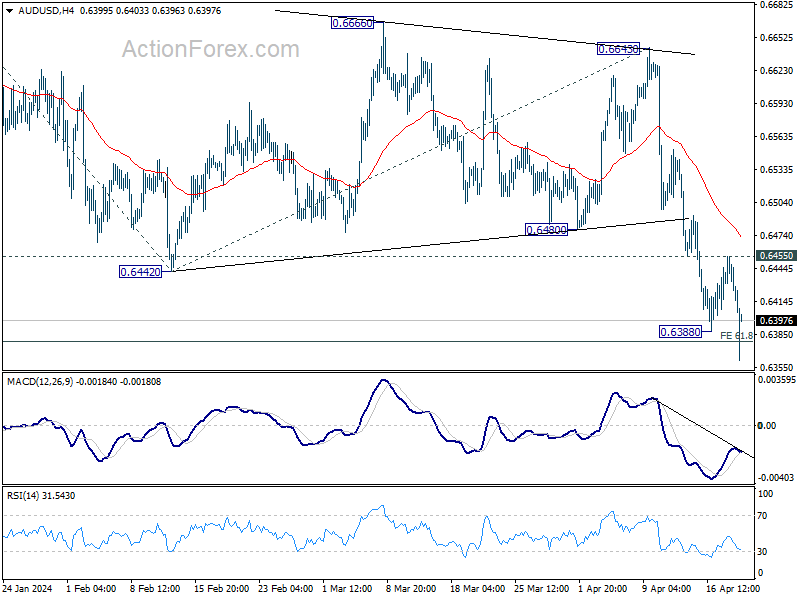

AUD/USD Daily Report

Daily Pivots: (S1) 0.6406; (P) 0.6432; (R1) 0.6446; More...

Intraday bias in AUD/USD is back on the downside a recent decline resumes through 0.6388 temporary low. Sustained break of 61.8% projection of 0.6870 to 0.6442 from 0.6643 at 0.6378 will extend the fall from 0.6870 to 100% projection at 0.6215. On the upside, break of 0.6455 resistance will turn intraday bias neutral again first.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which is still in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.

Middle East Conflict Shakes Markets, But Risks Seem Contained for Now

Significant volatility was seen in Asian session, following the news of Israel's missile strike in retaliation against Iran. This geopolitical development initially led to steep decline in Asian stocks and concurrent surge in oil prices and safe-haven assets like Swiss Franc, Yen, and Dollar. Nevertheless, fund flows started to reverse partially as the situation seemed to stabilize somewhat, as likelihood of immediate further escalation appeared to diminish.

Iran attempted to downplay the severity as its state media denied any foreign military presence in their airspace. Temporary flight restrictions that had been placed near the Isfahan military base were also lifted quickly. Meanwhile, Israel maintained silence on the issue, neither confirming nor denying involvement in the strikes.

As the day progresses, Swiss Franc, Yen, and Dollar are trading as the strongest currencies, bolstered by their status as traditional safe havens during times of international tension. Conversely, Aussie, Kiwi, and Sterling are underperforming as investors shy away from riskier assets. Euro and Canadian Dollar are situated in the middle of the currency spectrum. But the picture could dramatically alter depending on further developments from the Middle East conflict.

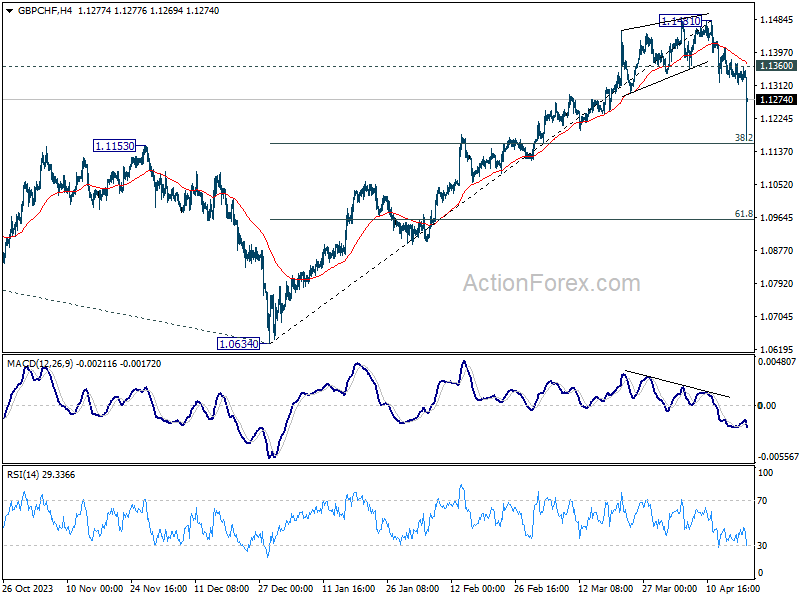

Technically, while GBP/CHF dived sharply today, downside is contained by 38.2% retraceent of 1.0634 to 1.1481 at 1.1157 so far. Price actions from 1.1481 are seen as developing into a consolidation pattern to rally from 1.0634 only, with range set between 1.1157 and 1.1481. Break of 1.1360 will bring further rebound to retest 1.1481 high. However, firm break of 1.1157 will bring deeper fall to 61.8% retracement at 1.0958, even just as a deep correction.

In Asia, at the time of writing, Nikkei is down -2.48%. Hong Kong HSI is down -1.23%. China Shanghai SSE is down -0.40%. Singapore Strait Times is down -0.59%. Japan 10-year JGB yield is down -0.0276 at 0.843. Overnight, DOW rose 0.06%. S&P 500 fell -0.22%. NASDAQ fell -0.52%. 10-year yield rose 0.062 to 4.647.

Oil and safe havens rally amid new Middle East conflict

Oil prices surges sharply in Asian session and there was a significant influx into safe-haven assets such as Gold, Dollar, Swiss Franc, and Japanese Yen.

This market reaction was triggered by escalating tensions in the Middle East, following a report by ABC News on a retaliatory missile strike by Israel against Iran. Meanwhile, Iran's Fars news agency also reported that explosions were heard near the Isfahan airport,m even though the causes were unknown.

The missile launches are continuation of hostilities following last Saturday when Iran targeted Israel with over 300 drones and missiles, a majority of which were intercepted by Israel and its allies.

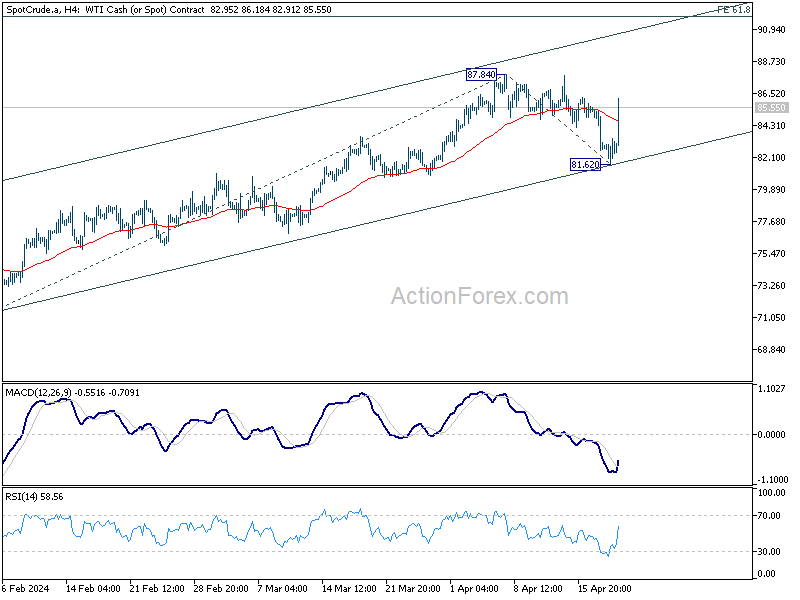

WTI oil's strong rebound today suggests that corrective pullback from 87.84 has completed at 81.62 already. Further rise would be seen to retest 87.84 resistance first. Decisive break there will resume whole rally from 67.79 and target 61.8% projection of 71.32 to 87.84 from 81.62 at 91.82 next.

Also, note that rise from 67.79 is seen as the third leg of the pattern from 63.67 (2023 low). Hence, break of 95.50 is possible in the medium term, depending on whether WTI could sustain its upside momentum.

BoJ's Ueda: Impact of weak Yen on inflation could lead to policy shift

During a press conference today, BoJ Governor Kazuo Ueda highlighted the potential economic repercussions of the persistently weak yen, particularly its effect on trend inflation through increased costs of imported goods.

"There's a possibility the weak yen could push up trend inflation through rises in imported goods prices," Ueda noted, indicating that such a scenario "might lead to a change in monetary policy."

At the same occasion, Finance Minister Shunichi Suzuki pointed out that exchange rates are not solely influenced by interest rate differentials. Various other factors, such as each country's current account balance, market participants' sentiment, and speculative trade, drive currency moves," Suzuki explained.

Japan's CPI core slows to 2.6% in Mar, CPI core-core down to 2.9%

In March, Japan observed a subtle cooling in core inflation, though levels persistently exceed BoJ's target.

Core CPI, which excludes food prices, slowed from 2.8% yoy to 2.6% yoy, slightly under the expectation of 2.7% yoy, marking a continued stretch above BoJ's 2% target for two full years.

Further detail is seen in the core-core CPI, excluding both food and energy, which decreased from 3.2% yoy to 2.9% yoy. This marks the seventh consecutive month of deceleration and brings this measure below 3% level for the first time since November 2022.

Meanwhile, headline CPI dipped slightly from 2.8% year-on-year to 2.7%, aligning with analysts' forecasts.

Fed's Bostic emphasizes patience on rate cuts, open to rate hikes

Atlanta Fed President Raphael Bostic highlighted his readiness to maintain the current rate levels through the end of the year. "I'm comfortable being patient," he noted at an event overnight. "I'm of the view that things are going to be slow enough this year that we won't be in a position to reduce our rates towards ... the end of the year."

He pointed out the importance of continued job creation and wage growth that outpaces inflation as key metrics guiding his decision-making process. "If we can keep those things going, and inflation has the signs that it is moving to that target, I'm happy to just stay where we are," he explained.

However, Bostic also warned of the potential need to adjust rates upward if inflation trends unfavorably, diverging from the Fed's 2% target. "If inflation starts moving in the opposite direction away from our target, I don't think we'll have any other option but to respond to that," he stated.

"I'd have to be open to increasing rates," he added.

Fed's Kashkari suggests rate cuts may wait until next year

Minneapolis Fed President Neel Kashkari told Fox News Channel that he wants to be "patient" regarding monetary easing. He added that the first rate cut could "potentially" be inappropriate until 2025.

"I'm in the view of, we need to wait and see, be patient as long as it takes, until we get convinced that inflation is on its way back down to 2%," he said.

Greene: BoE in trade-off territory, rate cuts not near

BoE MPC member Megan Greene said at an event overnight that rate cut is no on the immediate horizon. She characterized that BoE is in a "trade-off territory", in an environment of persistent high inflation coupled with weak growth in the UK.

"We have to weigh the risk of doing too much against the risk of doing too little," Greene explained.

She expressed a particular concern that being too cautious could lead to more severe consequences down the line: "In my mind, doing too little is the bigger risk because you end up having to hike rates even higher in the end and could end up generating an even bigger recession," she noted.

Looking ahead

UK retail sales and Germany PPI are the only economic data releases today.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6406; (P) 0.6432; (R1) 0.6446; More...

Intraday bias in AUD/USD is back on the downside a recent decline resumes through 0.6388 temporary low. Sustained break of 61.8% projection of 0.6870 to 0.6442 from 0.6643 at 0.6378 will extend the fall from 0.6870 to 100% projection at 0.6215. On the upside, break of 0.6455 resistance will turn intraday bias neutral again first.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which is still in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | National CPI Y/Y Mar | 2.70% | 2.70% | 2.80% | |

| 23:30 | JPY | National CPI core Y/Y Mar | 2.60% | 2.70% | 2.80% | |

| 23:30 | JPY | National CPI core-core Y/Y Mar | 2.90% | 3.20% | ||

| 06:00 | GBP | Retail Sales M/M Mar | 0.30% | 0.00% | ||

| 06:00 | EUR | Germany PPI M/M Mar | 0.00% | -0.40% | ||

| 06:00 | EUR | Germany PPI Y/Y Mar | -4.10% |

Oil and safe havens rally amid new Middle East conflict

Oil prices surges sharply in Asian session and there was a significant influx into safe-haven assets such as Gold, Dollar, Swiss Franc, and Japanese Yen.

This market reaction was triggered by escalating tensions in the Middle East, following a report by ABC News on a retaliatory missile strike by Israel against Iran. Meanwhile, Iran's Fars news agency also reported that explosions were heard near the Isfahan airport,m even though the causes were unknown.

The missile launches are continuation of hostilities following last Saturday when Iran targeted Israel with over 300 drones and missiles, a majority of which were intercepted by Israel and its allies.

WTI oil's strong rebound today suggests that corrective pullback from 87.84 has completed at 81.62 already. Further rise would be seen to retest 87.84 resistance first. Decisive break there will resume whole rally from 67.79 and target 61.8% projection of 71.32 to 87.84 from 81.62 at 91.82 next.

Also, note that rise from 67.79 is seen as the third leg of the pattern from 63.67 (2023 low). Hence, break of 95.50 is possible in the medium term, depending on whether WTI could sustain its upside momentum.