Sample Category Title

USD/JPY Stages More Upsides, Can Bulls Aim For 160?

Key Highlights

- USD/JPY extended gains above the 154.00 level.

- A major bullish trend line is forming with support at 153.95 on the 4-hour chart.

- EUR/USD is struggling to recover above 1.0720.

- Crude oil prices declined below the $83.50 support zone.

USD/JPY Technical Analysis

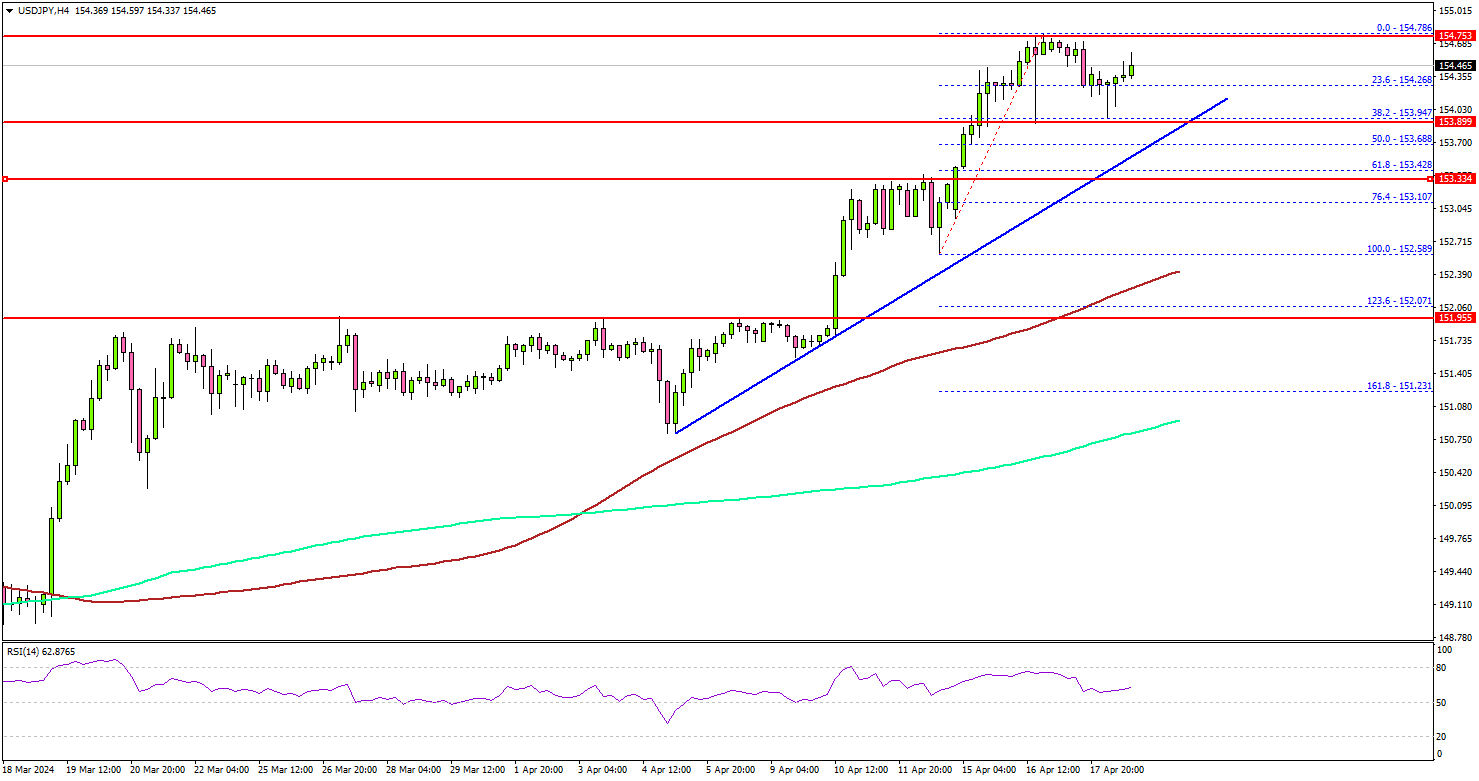

The US Dollar settled above the 150.00 level to move further into a positive zone against the Japanese Yen. USD/JPY even climbed above 154.00 and remains supported for more gains.

Looking at the 4-hour chart, the pair surged and cleared many hurdles in the past few days. There was even a move toward the 155.00 resistance zone before the pair started a consolidation phase.

Immediate support is near the 154.20 level. The next major support is at 154.00. There is also a major bullish trend line forming with support at 153.95 on the same chart. If there is a downside break below the trend line support, the pair might test 153.20.

The main support is now forming at 152.50 and the 100 simple moving average (red, 4-hour). Any more losses might send the pair toward the 200 simple moving average (green, 4-hour) at 151.00.

On the upside, the pair is facing hurdles near 154.80. The first key resistance is near the 155.00 zone. A clear move above the 155.00 resistance could send the pair further higher. In the stated case, USD/JPY bulls could even aim for a move toward 160.00.

Looking at Oil, there was a sharp decline in prices amid the Israel-Iran war situation. There was a drop below $83.50, and the bears could aim for more downsides.

Economic Releases

- UK Retail Sales for May 2024 (YoY) - Forecast +0.1%, versus -0.4% previous.

- UK Retail Sales for May 2024 (MoM) - Forecast +0.3%, versus 0% previous.

Japan’s CPI core slows to 2.6% in Mar, CPI core-core down to 2.9%

In March, Japan observed a subtle cooling in core inflation, though levels persistently exceed BoJ's target.

Core CPI, which excludes food prices, slowed from 2.8% yoy to 2.6% yoy, slightly under the expectation of 2.7% yoy, marking a continued stretch above BoJ's 2% target for two full years.

Further detail is seen in the core-core CPI, excluding both food and energy, which decreased from 3.2% yoy to 2.9% yoy. This marks the seventh consecutive month of deceleration and brings this measure below 3% level for the first time since November 2022.

Meanwhile, headline CPI dipped slightly from 2.8% year-on-year to 2.7%, aligning with analysts' forecasts.

BoJ’s Ueda: Impact of weak Yen on inflation could lead to policy shift

During a press conference today, BoJ Governor Kazuo Ueda highlighted the potential economic repercussions of the persistently weak yen, particularly its effect on trend inflation through increased costs of imported goods.

"There's a possibility the weak yen could push up trend inflation through rises in imported goods prices," Ueda noted, indicating that such a scenario "might lead to a change in monetary policy."

At the same occasion, Finance Minister Shunichi Suzuki pointed out that exchange rates are not solely influenced by interest rate differentials. Various other factors, such as each country's current account balance, market participants' sentiment, and speculative trade, drive currency moves," Suzuki explained.

Fed’s Bostic emphasizes patience on rate cuts, open to rate hikes

Atlanta Fed President Raphael Bostic highlighted his readiness to maintain the current rate levels through the end of the year. "I'm comfortable being patient," he noted at an event overnight. "I'm of the view that things are going to be slow enough this year that we won't be in a position to reduce our rates towards ... the end of the year."

He pointed out the importance of continued job creation and wage growth that outpaces inflation as key metrics guiding his decision-making process. "If we can keep those things going, and inflation has the signs that it is moving to that target, I'm happy to just stay where we are," he explained.

However, Bostic also warned of the potential need to adjust rates upward if inflation trends unfavorably, diverging from the Fed's 2% target. "If inflation starts moving in the opposite direction away from our target, I don't think we'll have any other option but to respond to that," he stated.

"I'd have to be open to increasing rates," he added.

Fed’s Kashkari suggests rate cuts may wait until next year

Minneapolis Fed President Neel Kashkari told Fox News Channel that he wants to be "patient" regarding monetary easing. He added that the first rate cut could "potentially" be inappropriate until 2025.

"I'm in the view of, we need to wait and see, be patient as long as it takes, until we get convinced that inflation is on its way back down to 2%," he said.

Greene: BoE in trade-off territory, rate cuts not near

BoE MPC member Megan Greene said at an event overnight that rate cut is no on the immediate horizon. She characterized that BoE is in a "trade-off territory", in an environment of persistent high inflation coupled with weak growth in the UK.

"We have to weigh the risk of doing too much against the risk of doing too little," Greene explained.

She expressed a particular concern that being too cautious could lead to more severe consequences down the line: "In my mind, doing too little is the bigger risk because you end up having to hike rates even higher in the end and could end up generating an even bigger recession," she noted.

A Lack of Shock and Awe

The United States is an outlier among advanced economies, so how much signal should policymakers elsewhere take from recent upside surprises on US inflation? Less than some people seem to think.

Perhaps the issue didn’t strike them as pertinent to a conversation with an Australian. Still, I could not help noticing that none of the offshore customers I have spoken with over the past two weeks were that shocked by the recent upside surprises on US inflation and retail sales. After all, it’s not hard to end up with high inflation when your government is running a deficit of 6% of GDP, growth is above average and the labour market is already tight. So despite the ‘shock and awe’ reaction in financial markets, perhaps people were not that surprised after all.

As discussed last week, the US fiscal and consumer situations stand in contrast to Australia. In many respects, the United States is an outlier among advanced economies.

How much signal, then, should policymakers elsewhere take from recent US inflation surprises? It does highlight that, once inflation becomes domestically focused and driven by a high level of domestic demand, it can be sticky and hard to return to target rates. This is the source of the RBA’s concern about market services inflation. While services inflation has so far declined in line with the RBA’s earlier forecasts, the RBA is mindful that progress could stall, as it seems to have done in the United States. That said, as highlighted this week by Westpac’s Head of International Economics Elliot Clarke, current high rates of services inflation in the United States have less to do with the components related to discretionary spending and more to do with slower-moving components such as insurance and medical services. Discretionary spending is high but lacks further momentum. So there are downside risks here as well as upside risks.

Another point of comparison is the role of housing-related inflation. In the US CPI, this relates only to rents, scaled up and adjusted to include imputed rents for owner-occupiers. In Australia (and Canada and New Zealand) rental inflation’s weight in the total relates only to rents actually paid by renters. The contribution of owner-occupied housing to inflation is captured by the ‘acquisitions method’ – in other words, home-building costs. These, too, have increased significantly and in Australia they continue to escalate at an above-average pace.

The question is how long housing-related inflation will stay high. Across this group of economies, we have seen surges in population growth adding to demand for rental housing. At the same time, housing construction industries remain supply constrained, with domestic supply chains an issue in some cases. There is also a question of how much of the increased demand for housing represents a longer-lasting effect of increased working from home, which has seen some households needing more space than before.

If – as is the case for Australia and Canada – the population surge is largely a catch-up from pandemic-era restrictions, it should normalise over the next year or so. Indeed, this is Westpac Economics’ projection for Australia’s population growth, returning to the pre-pandemic norm of 1½% or a little above that in 2025. The rent component of CPIs relates to the stock of all rented properties, so it is slow-moving compared with most other components of inflation. But if we are right about the population surge in Australia being mostly a post-pandemic catch-up, then the burst of rental inflation should subside over time as well. (It would normalise even faster if the construction industry found a way to recover from current supply constraints.) The drivers of US population growth are somewhat different, and a slowing is not already baked into the dynamics there. This means that a slowing in US rent growth is less assured.

The upside risks to domestic inflation in countries such as Australia and Canada should not be dismissed. Given the nature of the housing-related inflation and the state of the consumer, though, neither should they be overblown. Recall that the Australian household sector has pulled back on consumption per capita in a way not seen elsewhere. Population growth initially masked this pullback from the perspective of the business sector. More recently, surveys are suggesting that businesses are now seeing the softness in demand and reacting to it, including in their pricing strategies.

We therefore cannot rule out – as a risk scenario, not currently our central case – that the conditions for withdrawing some of the restrictive stance of monetary policy will be met in Australia and some other economies before they are met in the United States. As we have explained previously, the RBA and other central banks do not need to wait for the Federal Reserve to move before they can do so. The RBA was cutting rates in the years leading up to the pandemic while the Federal Reserve was raising them. The signal from the US experience is as an example of what could happen elsewhere, not a direct linkage between rates decisions. It is also not the only such example. For this reason, watch the outcomes in Canada and Europe, not just the United States.

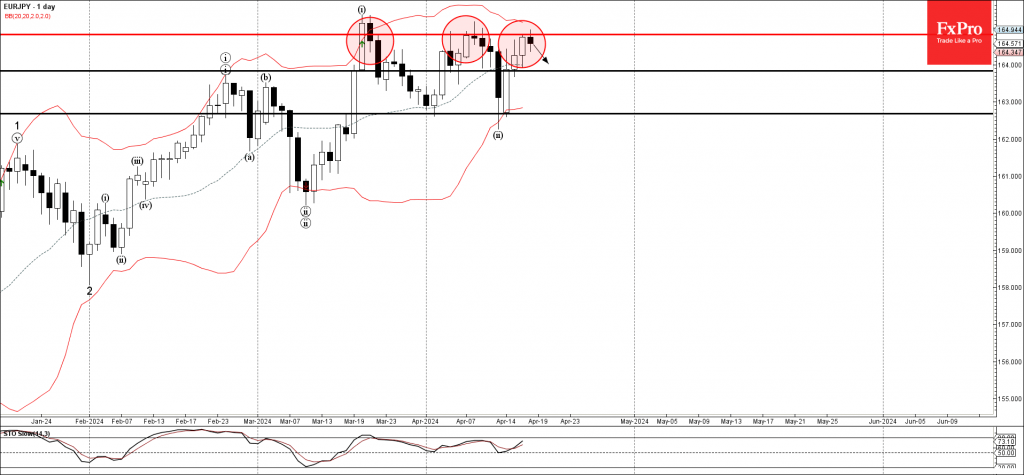

EURJPY Wave Analysis

- EURJPY reversed from resistance level 164.00

- Likely to fall to support level 163.85

EURJPY currency pair recently reversed down from the pivotal resistance level 164.00, which has been reversing the price from last month.

The resistance level 164.00 was strengthened by the nearby upper daily Bollinger Band, as you can see below.

Given the strength of the aforementioned resistance level 164.00 and the bearish euro sentiment seen today, EURJPY can be expected to fall further to the next round support level 163.85.

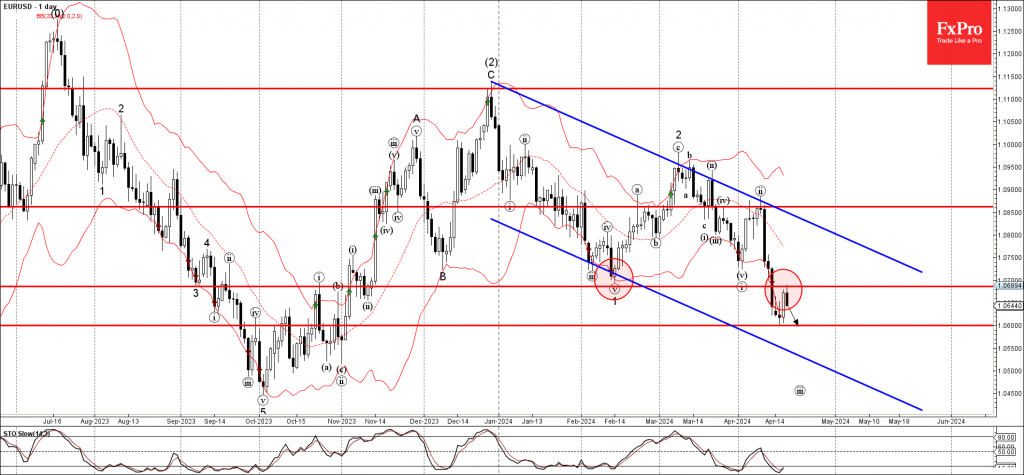

EURUSD Wave Analysis

- EURUSD reversed from resistance level 1.0685

- Likely to fall to support level 1.0600

EURUSD currency pair recently reversed down from the resistance level 1.0685, former multi-month support from February, acting as the support after it was broken.

The downward reversal from this resistance level 1.0685 continues the active minor impulse wave 3 of the higher impulse wave (3) from December.

Given the multi-month downtrend, EURUSD can be expected to fall further to the next round support level 1.0600.