Sample Category Title

Commodity Currencies at Strategic Levels. What Can Affect a Breakdown Downwards?

The decline in investor expectations regarding a change in the vector of the Fed's monetary policy contributes to the fall of not only European, but also commodity currencies. So, in recent weeks:

- AUD/USD has lost more than 200 points and is testing the extremes of 2023 near 0.6400

- USD/CAD is trading at three-year highs and has managed to strengthen by 300 points

What may affect the pricing of the main currency pairs on the market in the coming trading sessions:

- speech by the President of the Federal Reserve Bank of Chicago, Austan Goolsbee (today at 17.30 GMT+3.00)

- publication on the number of active drilling rigs from Baker Hughes (today at 20.00 GMT+3.00)

- announcement on the base lending rate from the People's Bank of China (Monday at 4.15 GMT+3.00)

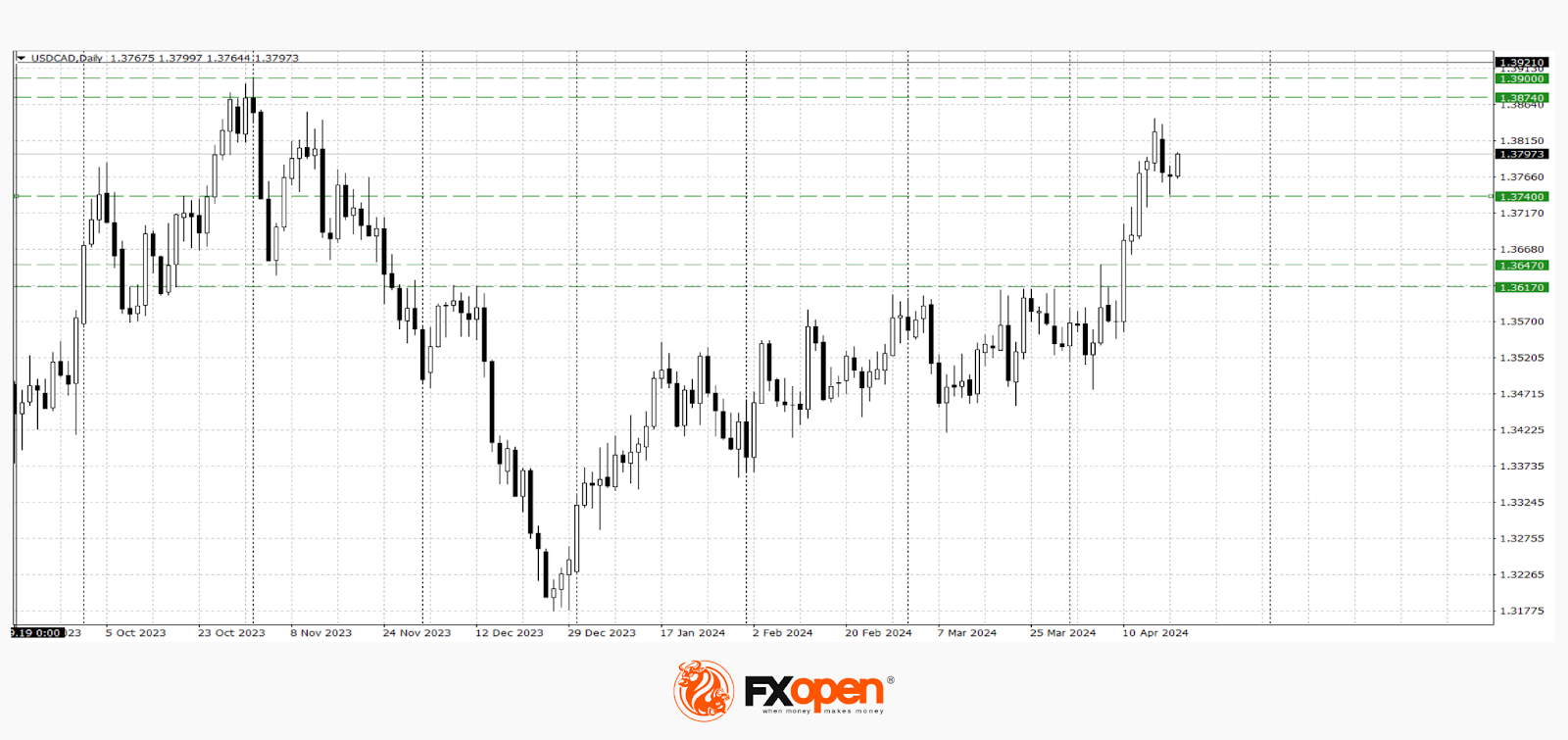

USD/CAD

The USD/CAD currency pair has come close to the important range of 1.3970-1.3800, above which the price has not risen since 2020.

Technical analysis of USD/CAD indicates the possibility of a downward correction in the short term, since a dark clouds combination has been formed on the daily timeframe, the development of which could lead to a breakdown of yesterday’s low at 1.3740 and a further test of 1.3650-1.3620. If the upward movement resumes, the price may break through the recent high at 1.3840 and continue to rise in the direction of 1.3970-1.3880.

AUD/USD

A couple of days ago, a bullish harami combination was formed in the AUD/USD pair on the daily timeframe. This formation allowed buyers of the pair to correct to 0.6460. However, it was not possible to start a larger upward correction, and today the recent low at 0.6390 was updated. If this level becomes resistance, the price may decline to the 2023 lows at 0.6290-0.6270.

Forecast with Elliott Wave Technique Calling EURUSD to Extend Lower

Short term Elliott Wave view in EURUSD suggests that cycle from 12.28.2023 high is in progress as a zigzag Elliott Wave structure. Down from 12.28.2023 high, wave A ended at 1.0694 and rally in wave B ended at 1.098. Wave C lower is in progress as a 5 waves impulse Elliott Wave structure. Down from wave B, wave ((i)) ended at 1.072 and rally in wave ((ii)) ended at 1.0885. Pair extends lower in wave ((iii)) with internal subdivision as another 5 waves in lesser degree. Down from wave ((ii)), wave (i) ended at 1.0846 and wave (ii) ended at 1.0866.

Wave (iii) lower ended at 1.071 and rally in wave (iv) ended at 1.0756. Final wave (v) lower ended at 1.06 which completed wave ((iii)). Wave ((iv)) rally is unfolding as an expanded Flat structure. Up from wave ((iii)), wave (a) ended at 1.065 and dips in wave (b) ended at 1.06. Wave (c) higher ended at 1.069 which completed wave ((iv)). Pair then extends lower again in wave ((v)). While below 1.069, expect pair to extend lower in wave ((v)) to complete wave C of (2) before pair turns higher.

EURUSD 60 Minutes Elliott Wave Chart

EURUSD Elliott Wave Video

https://www.youtube.com/watch?v=lJnCbjidda4

Markets Thrown in Risk-off Modus on Headlines of Israeli Attack on Iran

Markets

After a brief correction Wednesday, core yields again turned north yesterday. US yields added between 6.2 bps (5-y) and 3 bps (30-y). The Philly Fed business outlook printed much strong than expected (15.5 from 3.2).Weekly jobless claims (212k) confirmed the narrative of a resilient US labour market. Fed governors turn ever more guarded on any possible rate hikes this year. Fed’s Bostic favours a scenario of 1 cut at the end of this year. Fed’s Kashkari repeated the Fed needs more confidence that inflation is declining further. It is possible to delay a rate cut to 2025. Bunds gained slightly less, between 2.8 bps (30-y) and 3.8 bps (2-y) as ECB officials try to find how much autonomous rate cuts are possible if the Fed stays on hold for longer. Equites traded mixed (EuroStoxx 50 +0.46%, Nasdaq minus 0.52%). Even so, EMU and US indices remain in a sell-on-upticks dynamics with first relevant support levels coming closer. Higher (US) yields also helped the dollar to reverse early softness. EUR/USD closed at 1.0643 (from 1.0673). USD/JPY tested multi-year peak levels in the 154.70/80 area. DXY regained the 106 barrier.

Markets this morning are thrown in risk-off modus on headlines of an Israeli attack on Iran. In a first reaction, Asian equities spiked lower, but currently are unwinding part of the initial losses. Safe haven flows propelled US Treasuries with yields briefly declining more the 10 bps, but a reversal currently limits the decline between 4.5 (2-y) and 6.5 (10-y) bps. EUR/USD briefly dropped to the 1.061 area, but the 1.06 support remains intact for now (currently 1.063). The yen briefly strengthened below USD/JPY 154, but also this move could not be sustained (154.3). Brent oil jumped from $87 p/b to temporary trade above $90 p/b, but also eases back to $88.75. Later today, the developments in the Middle East probably will continue to dominate the market dynamics as there are no important data on the agenda. The market reaction on Friday last week suggested that a reaction to attacks between Iran and Israel could stay modest as long markets don’t anticipate a large scale escalation. We assume any setback in yields to stay limited. Higher oil or commodity prices even might further raise the inflation expectations component/risk premium for yields a longer maturities. The dollar maintains a positive momentum. A break of EUR/USD below 1.06 would suggest further losses/USD gains. This morning, UK March retail sales printed slightly softer than expected (headline 0.0% M/M and 0.8% Y/Y). EUR/GBP gains a few ticks post the release (0.8565).

News & Views

Japanese inflation eased in March. Headline prices rose 2.7%, down from 2.8% in February. The BoJ’s preferred gauge excluding fresh food came in at 2.6% vs 2.8% the month before while a measure ignoring energy prices as well eased from 3.2% to 2.9% - the first sub 3% reading since November 2022. While all gauges fell short of expectations (0.1 ppt), they remain above the 2% BoJ target for two years running. Services price growth slowed to 2.1% but should stay supported going forward on the biggest wage negotiation (>5%) outcome in decades. Coupled with the country’s weak(ening) currency – the Japanese yen recently hit a new 34-y low against the dollar – and the government’s decision to phase out utility subsidies from May (creating base effects), inflation could easily go up again in coming months. Today’s numbers aren’t going to change the BoJ’s widely expected status quo at the April 26 meeting. But upward revisions to the inflation forecast (+2% at the end of the policy horizon?!) may lay the groundwork for another rate hike later this year. The yen completely ignored the CPI outcome with geopolitical events dominating trading this morning. USD/JPY dropped to an intraday low of 153.59 after Israel retaliated for an Iranian strike last weekend in a tit-for-that response that risks escalating. The pair quickly pared losses to 154.31.

Yesterday’s European summit revealed sharp opposition against a France-led push for reforms to deepen financial market integration and central supervision. The project at stake, Capital Markets Union, mostly puts larger economies including Germany, Italy, Spain and the Netherlands against smaller countries that are wary to cede national oversight and regulatory powers to Brussels. The idea to create a CMU was already floated a decade ago but stranded quickly. Major challenges including the green transition and defense spending renewed momentum (for some at least) for an overhaul, believing that it would help tap private capital to fund the investments.

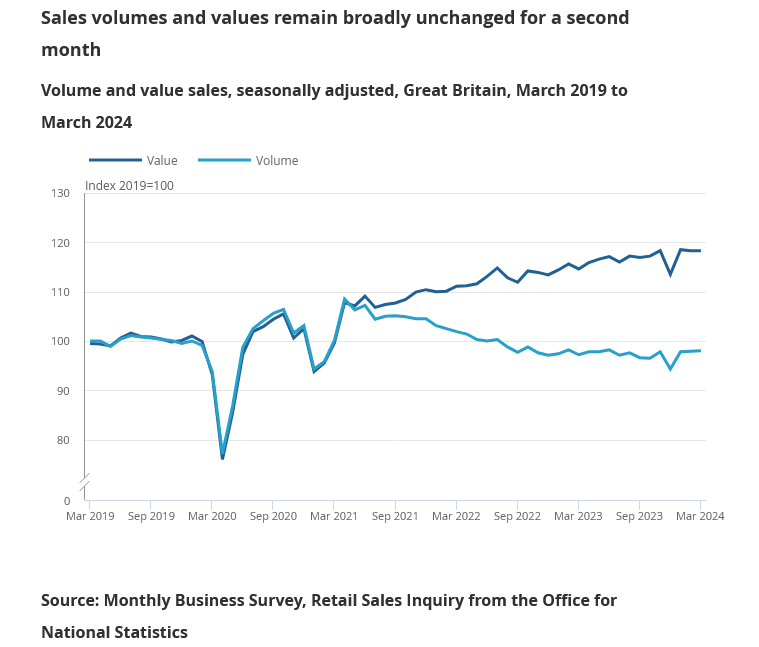

UK retail sales flat in Mar, misses expectations

In the UK, retail sales volumes was unchanged in March, falling short of the modest 0.3% mom growth anticipated by analysts. The performance within the retail sector was varied: automotive fuel and non-food store sales saw increases of 3.2% and 0.5%, respectively, which were offset by declines in food stores and non-store retailers, dropping by 0.7% and 1.5%.

On a quarterly basis, retail sales volumes rising 1.9% in the three months to March, a recovery attributed to the bounce back from particularly low sales volumes experienced during the Christmas shopping season.

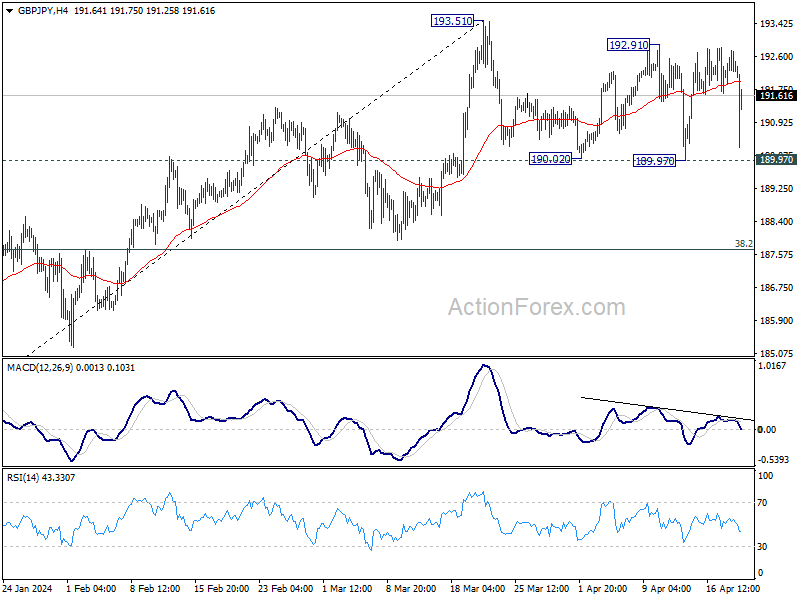

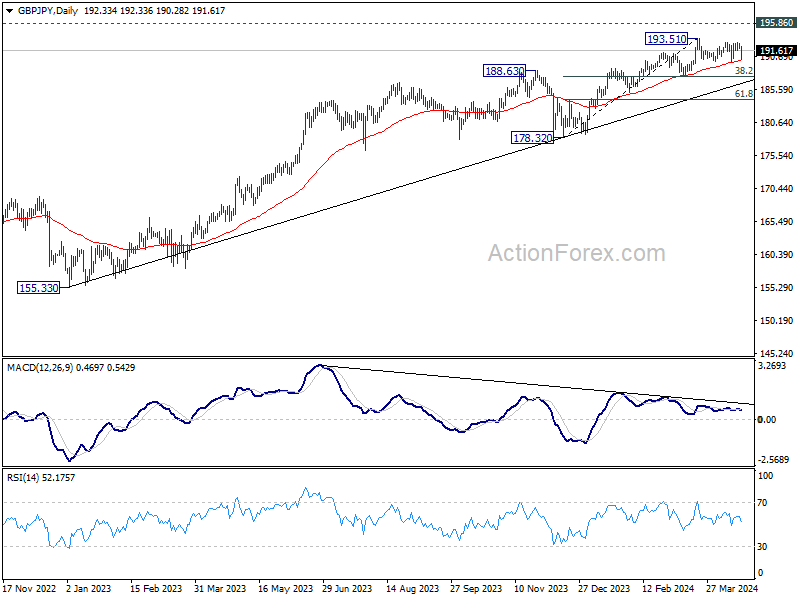

GBP/JPY Daily Outlook

Daily Pivots: (S1) 191.90; (P) 192.34; (R1) 192.77; More..

GBP/JPY is still bounded in established range despite today's volatility. Intraday bias remains neutral. On the upside, break of 193.51 will resume larger up trend to 195.86 long term resistance. Nevertheless, decisive break of 189.97 support will indicate that it's at least correcting the rise from 178.32, and target 38.2% retracement of 178.32 to 193.51 at 187.70.

In the bigger picture, current rally is part of the up trend from 123.94 (2020 low), and is in progress for 195.86 long term resistance (2015 high). Break of 187.94 support is needed to be the first sign of medium term topping. Otherwise, outlook will remain bullish in case of retreat.

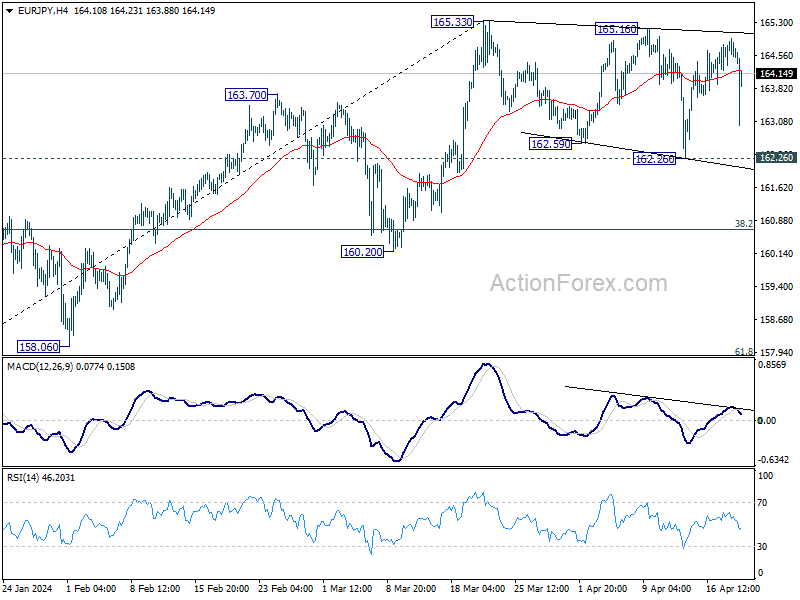

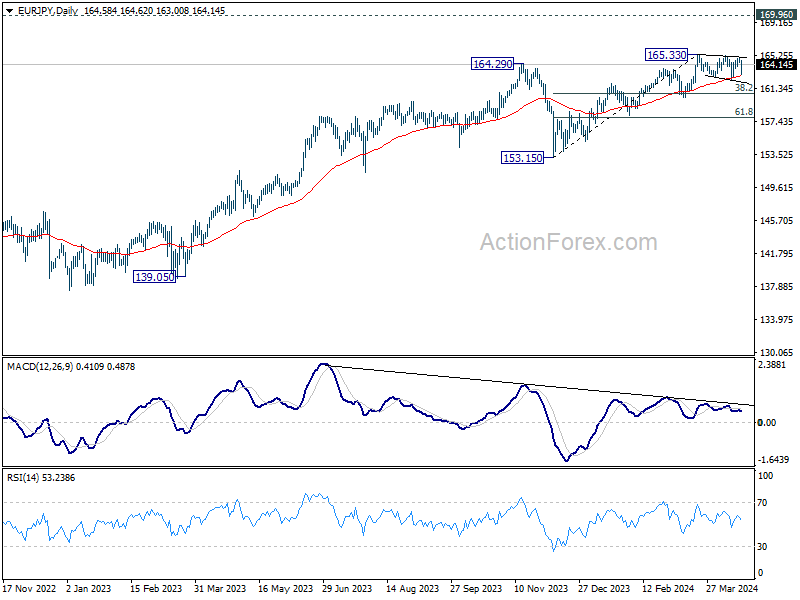

EUR/JPY Daily Outlook

Daily Pivots: (S1) 164.32; (P) 164.64; (R1) 164.91; More...

Range trading continues in EUR/JPY despite huge volatility. Intraday bias remains neutral first. On the upside, firm break of 165.33 will resume larger up trend towards 169.96 key resistance next. However, decisive break of 162.26 support will argue that it's at least correcting the rise from 153.15, and target 38.2% retracement of 153.15 to 165.33 at 160.67.

In the bigger picture, current rally is part of the up trend from 114.42 (2020 low), which is still in progress. Next target is 169.96 (2008 high). Break of 160.20 support is needed to be the first sign of medium term topping. Otherwise, outlook will stay bullish in case of retreat.

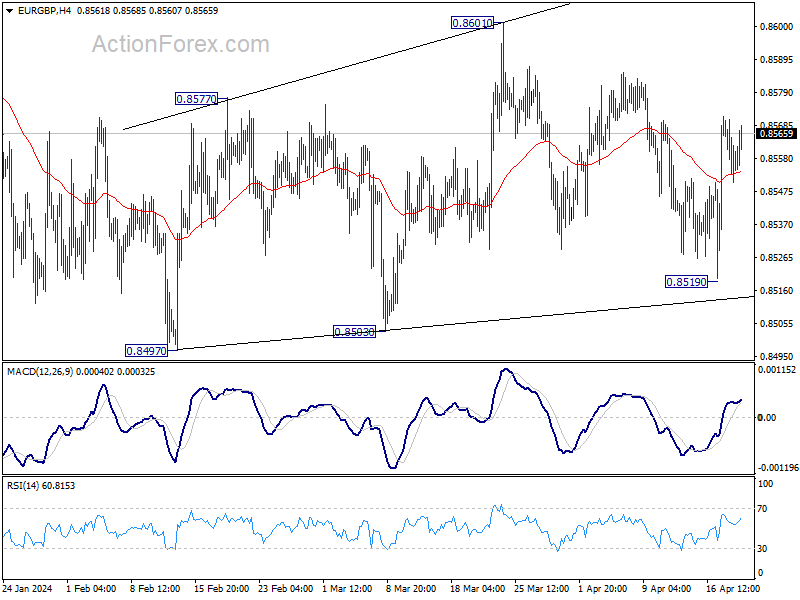

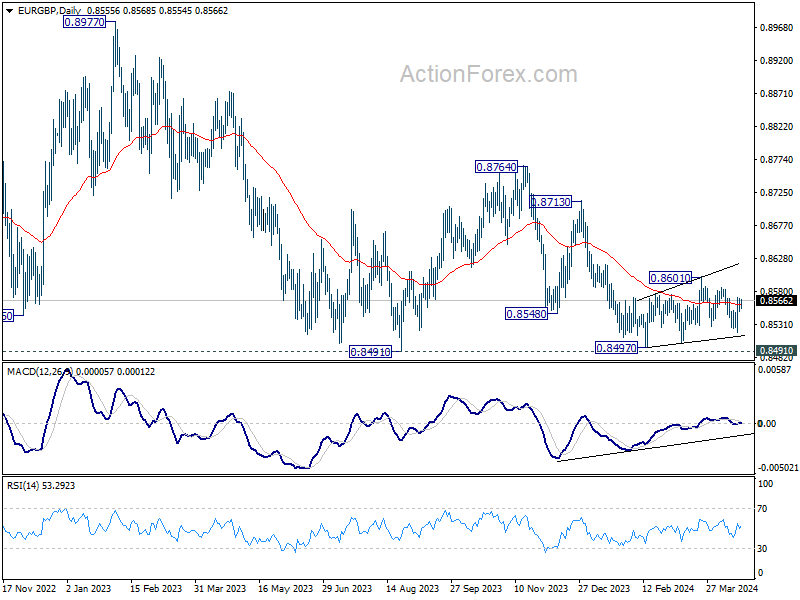

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8549; (P) 0.8560; (R1) 0.8570; More...

Outlook in EUR/GBP remains unchanged as range trading continues. Intraday bias stays neutral at this point. On the downside, firm break of 0.8529 support will argue that the corrective recovery from 0.8497 has completed at 0.8601. Intraday bias will be back on the downside for retesting 0.8497 low next. On the upside, break of 0.8601 will resume the rebound instead.

In the bigger picture, there is no clear sign that down trend from 0.9267 has completed, despite loss of downside momentum as seen in D MACD. As long as 0.8601 resistance holds, the down trend will remain in favor to resume through 0.8491 low at la later stage.

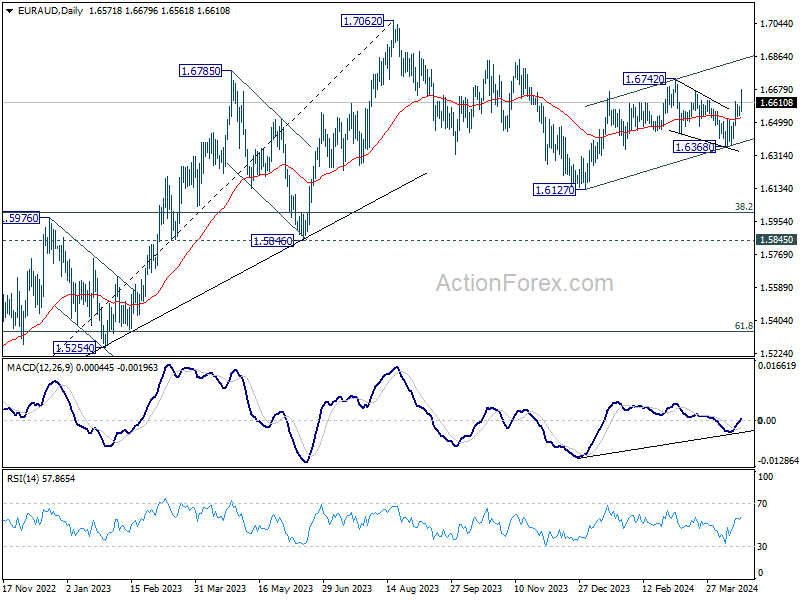

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6542; (P) 1.6573; (R1) 1.6607; More...

EUR/AUD's rally from 1.6368 resumed after brief consolidations. Breach of 1.6677 resistance argues that fall from 1.6742 has completed as a three-wave corrective move to 1.6368. Intraday bias is back on the upside for retesting 1.6742. On the downside, below 1.6534 support will turn intraday bias neutral again first.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). In case of another fall, Strong support is expected around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound. Break of 1.7062 is in favor as a later stage.

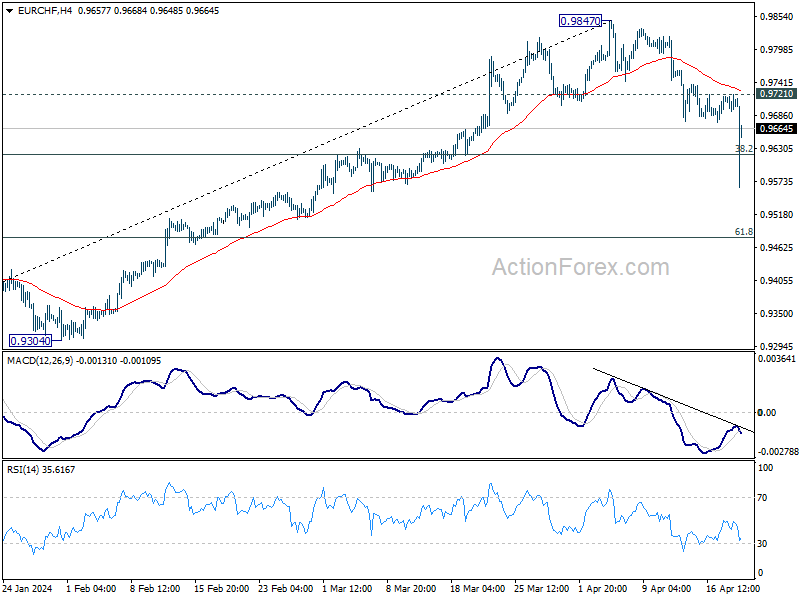

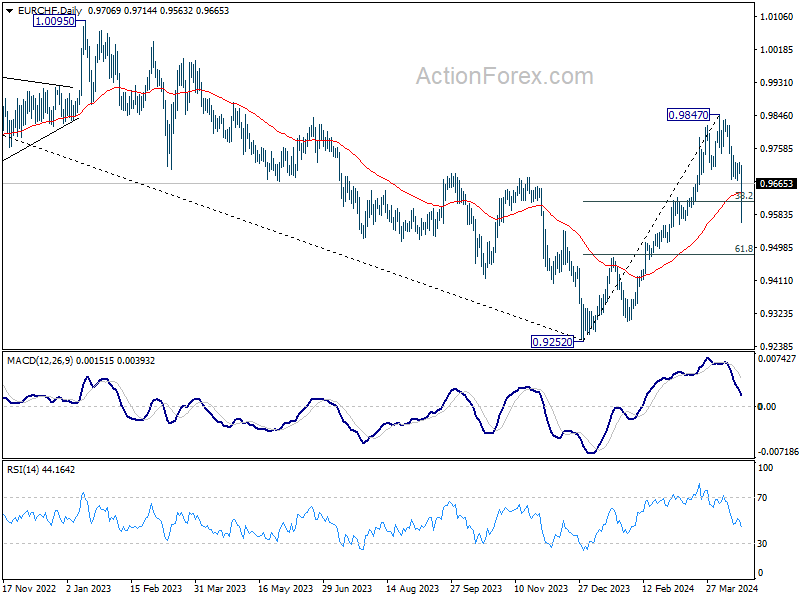

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9690; (P) 0.9713; (R1) 0.9732; More...

Intraday bias in EUR/CHF is back on the downside as fall from 0.9847 resumed. Sustained break of 38.2% retracement of 0.9252 to 0.9847 at 0.9620 will bring deeper fall to 61.8% retracement at 0.9479. On the upside, though, break of 0.9721 minor resistance will turn bias back to the upside for retesting 0.9847.

In the bigger picture, a medium term bottom should be in place at 0.9252 already, on bullish convergence condition in W MACD. Rise from there now target 38.2% retracement of 1.2004 (2018 high) to 0.9252 (2023 low) at 1.0303, even as a correction to the down trend from 1.2004. This will remain the favored case as long as 55 D EMA (now at 0.9639) holds.

Cliff Notes: Seeking Clarity on Labour Market Conditions

Key insights from the week that was.

In Australia, the March Labour Force Survey provided some much-needed clarity on labour market conditions after an incredibly volatile opening to the year. Following an upwardly revised gain of nearly 118,000 in February, employment fell only modestly in March, down by just 6,600. On a quarter-average basis, employment’s momentum was strong in Q1 at 2.7%yr but consistent with a trend softening from 2023’s 3.0%yr. At the same time, the declines in average hours worked per employee have become less severe, H2 2023’s correction of 2.7% followed by a more modest 0.4% fall in Q1 2024 (both in quarter-average terms). Consequently, the net effect on total hours worked, or total labour usage, was flat in the opening months of this year.

The unemployment rate ticked up slightly from 3.7% in February to 3.8% in March, its three-month average of 3.9% virtually unchanged from Q4 2023. With labour demand’s softness largely presenting in average hours, underemployment continued to rise (albeit slightly) in the opening quarter, from 6.5% in December to 6.6% in March on a quarter-average basis. The stronger-than-expected degree of resilience suggested by these figures are broadly mirrored by other measures of spare capacity, including hours-based underutilisation, youth unemployment, vacancies-to-unemployment and indicators from business surveys.

On balance, this update presents a slightly better read on the underlying state of labour market conditions in Q1 2024. On average, outcomes over the past three months are still consistent with a trend softening in the labour market, just not to the extent observed over the second half of 2023. The extent to which labour demand will continue to cool near-term, however, critically depends on the interplay between headcount and average hours. We continue to expect some softness to present via the latter, but given recent data, prospects of material economy-wide declines in employment seem increasingly unlikely at this stage; that, of course, being one of the key goals of the RBA in its current policy cycle.

In New Zealand, the Q1 CPI came in between Westpac and the RBNZ’s expectations, rising 0.6% in the quarter and 4.0%yr. The detail suggests imported inflation is easing, but domestic inflation pressures continue to show strength. This poses a considerable challenge for the RBNZ as they seek to bring inflation back to the mid-point of the target range. Next week sees the release of Australia’s Q1 CPI. We expect a 0.8% rise in the quarter, but base effects will see the annual rate fall to 3.5%yr. Our preview is available at Westpac IQ. Chief Economist Luci Ellis this week also discussed the implications of global inflation developments for Australia and the RBA.

Over in the UK meanwhile, the annual CPI nudged down to 3.2%yr in March, mostly due to food prices. BoE Governor Andrew Bailey remains confident that inflation will fall sharply in April because of energy prices, putting the inflation target in sight and allowing the central bank to consider cutting rates. However, services inflation remains persistent, contributing 92% of total inflation over the year.

Strong wages gains continue to pressure services inflation, boosting consumer spending capacity and raising firms’ production costs, which they aim to pass on. Wage growth has eased from a high of 8% in the middle of 2023, but has held above 6% the last three months. Decision Maker Panel’s wage expectations for the year ahead continue to edge lower, but at 4.7% is still strong. Persistence in wage and services inflation will continue to cast doubts over whether the BoE will easily meet their 2% medium-term objective and consequently how far policy can be eased. Still, the first cut is in sight and welcome as the UK economy stagnates.

In Europe, services inflation also remains sticky, but goods disinflation is increasingly taking the pressure off the ECB, headline inflation now 2.4%yr and core 2.9%yr. Labour market momentum has also eased, pointing to an increasingly benign balance of risks for wage and services inflation. This puts the European Central Bank in a comfortable position to begin easing in June, although they are also likely to proceed cautiously.

Across the pond, headline US retail sales rose 0.7%mth in March, and the control group, which feeds into GDP calculations, gained 1.1%mth. This result follows a soft January/ February and may have been inflated somewhat by sales promotions. However, holding real GDP growth materially above trend in Q1, it reinforces the market’s current concerns over inflation’s persistence.

While only a qualitative guide, the FOMC’s April Beige Book depicted a much softer economy. Overall, “economic activity expanded slightly” over the 3 months to April, with 10 of the 12 districts experiencing “slight or modest economic growth”. “Consumer spending barely increased overall” and consumers’ price sensitivity was called out. Employment “rose at a slight pace overall”, and the labour market was seen as coming into balance. Wage growth was regarded as benign, annual wage growth having “recently returned to their historical averages”. This guidance points to a continued deceleration in inflation and restraint by consumers in the months ahead.

How much further progress is necessary for the FOMC to be comfortable easing policy remains an open question. At 2.5% and 2.8%, February’s annual headline and core PCE inflation was very similar to Europe’s CPI momentum at March, 2.4% and 2.9% for headline and core. But the US’ CPI measure has shown greater persistence January through March, primarily as a result of capacity constraints (e.g. rents) and the lagged secondary influence of prior goods inflation (e.g. motor vehicle insurance). Next week’s US GDP and March PCE reports are eagerly awaited.

Finally, back in Asia, China’s Q1 GDP highlighted the benefit of reform, with high-tech manufacturing and infrastructure investment driving a 6% annualised GDP gain in the quarter, even as the property sector continued to contract and consumer demand remained fragile. Authorities 5.0% target for 2024 is now within sight, only requiring annualised growth between 4% and 5% Q2 to Q4. Sentiment in China’s economy is unlikely to improve quickly, as property and financial sector risks remain front of mind. However, we expect the economy’s momentum to persist and authorities aims to be achieved, or modestly excee.