Sample Category Title

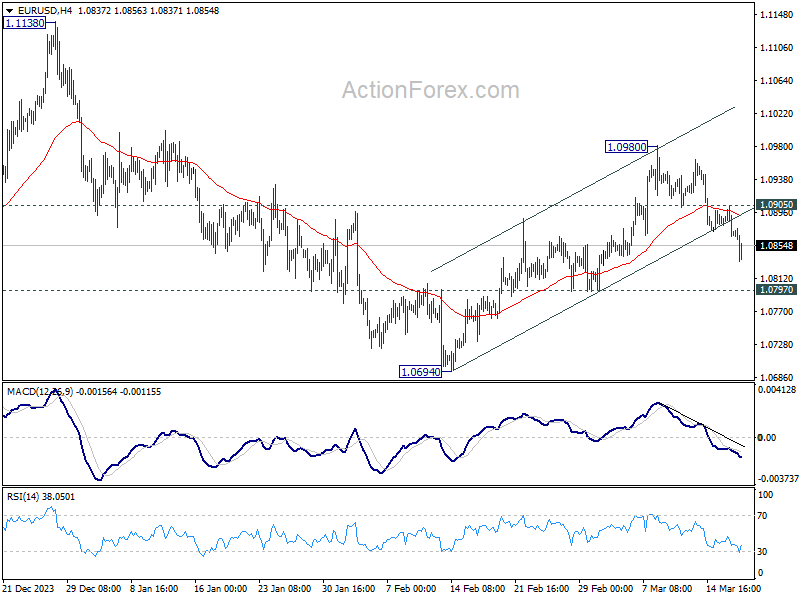

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0857; (P) 1.0881; (R1) 1.0897; More...

Intraday bias in EUR/USD remain son the downside for the moment as fall from 1.0980 is in progress. Sustained trading below 55 D EMA (now at 1.0856) will argue that rebound from 1.0694 has completed and bring retest of this low. On the upside, above 1.0905 minor resistance will turn intraday bias neutral first.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

Canada: Inflation Surprises With a Downtick in February

Headline CPI inflation moved slightly lower in February to 2.8% year-on-year (y/y), against expectations for an uptick.

Softer inflation at grocery stores was part of the story in February. Grocery price increases cooled from 3.4% y/y in January to 2.4%. This marks the first time since 2021 that grocery inflation was below headline inflation.

In February, gasoline prices flipped to and increase, up 0.8% y/y, versus a 4% y/y decline in January.

Shelter inflation continued to move higher, up 6.5% y/y in February. Rent inflation moved up to 8.2% y/y, while overall cost of owned accommodation was up 6.7% y/y.

Other areas contributing to cooler inflation were cellular and internet services. New cell phone plans were down 26.5% versus a year ago in February for the same level of service, while internet access was down 13.2% y/y.

The Bank of Canada's preferred "core" inflation measures moved lower in February to average 3.2% y/y, down from 3.4% in January.

Key Implications

February's inflation report was a little bit of good news for Canadians. After stalling through the second half of last year, that is two months of improvement on the Bank of Canada's key core inflation gauges. However, the battle isn't won yet, and we now expect the Bank of Canada will leave the overnight rate unchanged until July, as outlined in our new forecast released today.

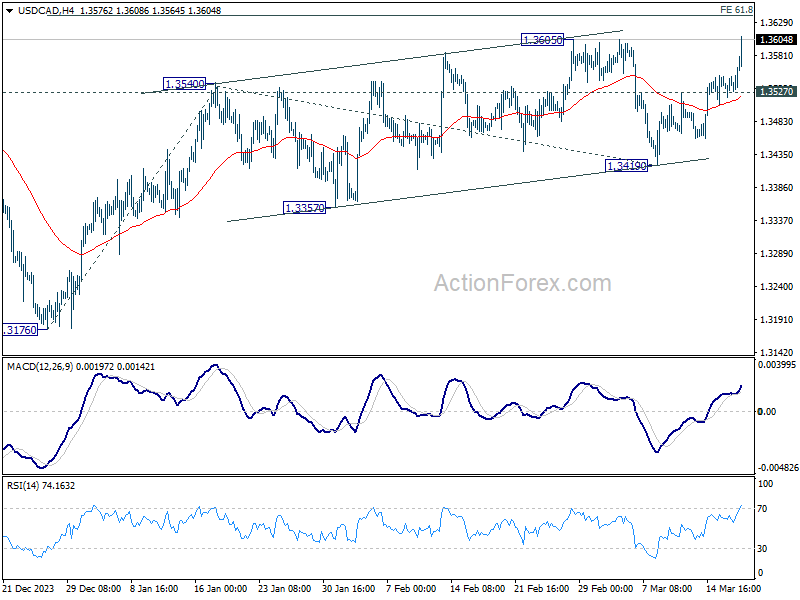

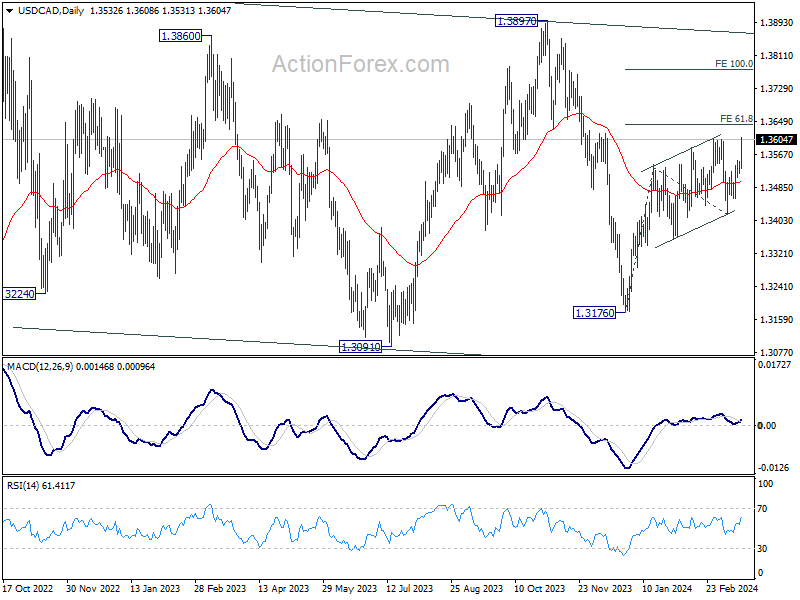

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3519; (P) 1.3536; (R1) 1.3550; More...

USD/CAD's break of 1.3605 resistance suggests that whole rise from 1.3176 is resuming. Intraday bias is back on the upside for 61.8% projection of 1.3176 to 1.3540 from 1.3419 at 1.3644 first. Decisive break there could prompt upside acceleration to 100% projection at 1.3783 next. On the downside, below 1.3527 minor support will turn intraday bias neutral first. But outlook will stay bullish as long as 1.3419 support holds.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 at a later stage.

Canadian Dollar Dives on CPI Surprise, Market Eyes Earlier BoC Rate Cut

Canadian Dollar falls sharply in early US session, triggered by an unexpected decline in Canada's headline CPI and a more significant than anticipated slowdown in core inflation measures. This trend of disinflation is likely to reassure BoC that its efforts to curb inflation are bearing fruit, possibly at a quicker pace than initially projected. The fresh data has fueled market speculation that BoC might advance its timeline for rate cuts to the second quarter of the year, rather than in the third quarter.

Meanwhile, Yen is trading as the day's weakest performer, facing steeper sell-off following BoJ's landmark decision to hike interest rates for the first time in 17 years. The market's reaction suggests a perception that, despite its symbolic significance, this rate hike could be a one-off event within the context of a broader overhaul of the monetary policy framework, rather than marking the beginning of a consistent tightening cycle. The Australian Dollar ranks as the second weakest, reflecting investor perception of a less hawkish statement from RBA than some had anticipated.

Conversely, Swiss Franc outperformed as the day's strongest currency, followed closely by Dollar and then Euro. It's important to note, however, that Franc's rise is more indicative of a recovery from key support levels against Dollar, Euro, and Sterling, rather than a signal of intrinsic strength.

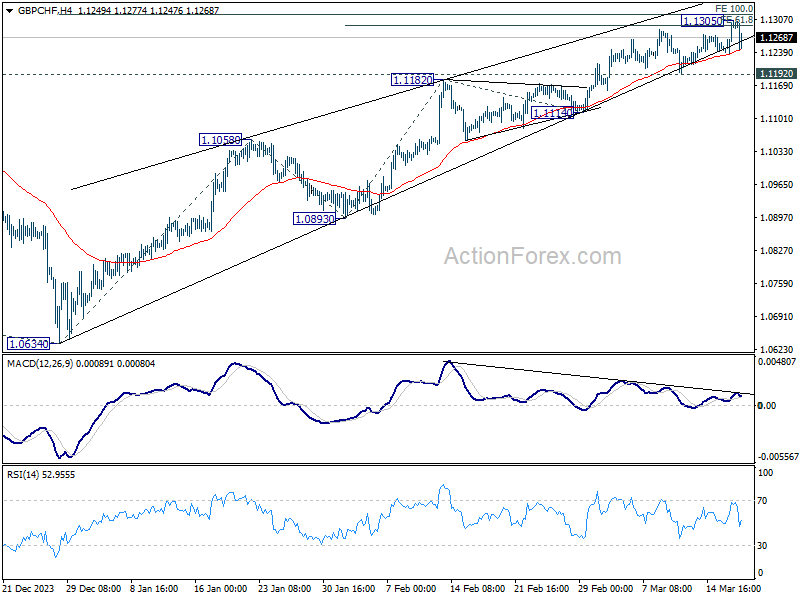

Technically, GBP/CHF retreated after hitting cluster projection zone at around 1.13 (61.8% projection of 1.0893 to 1.1182 from 1.1114 at 1.1293 and 100% projection of 1.0634 to 1.0893 from 1.1058 at 1.1317).

Considering persistent bearish divergence condition in 4H MACD, there is prospect for the cross to top at this level. Break of 1.1192 support will indicate that it has started a correction to the rally from 1.0634. Nevertheless, decisive break of this 1.13 resistance zone could prompt upside acceleration to next resistance level at 1.15.

With BoE and SNB rate decisions looming on Thursday, the direction of GBP/CHF will soon become clearer.

In Europe, at the time of writing, FTSE is down -0.18%. DAX is up 0.21%. CAC is up 0.46%. UK 10-year yield is down -0.0519 at 4.142. Germany 10-year yield is down -0.023 at 2.438. Earlier in Asia, Nikkei rose 0.66%. Hong Kong HSI fell -1.24%. China Shanghai SSE fell -0.72%. Singapore Strait Times rose 0.05%. Japan 10-year JGB yield fell -0.0315 to 0.732.

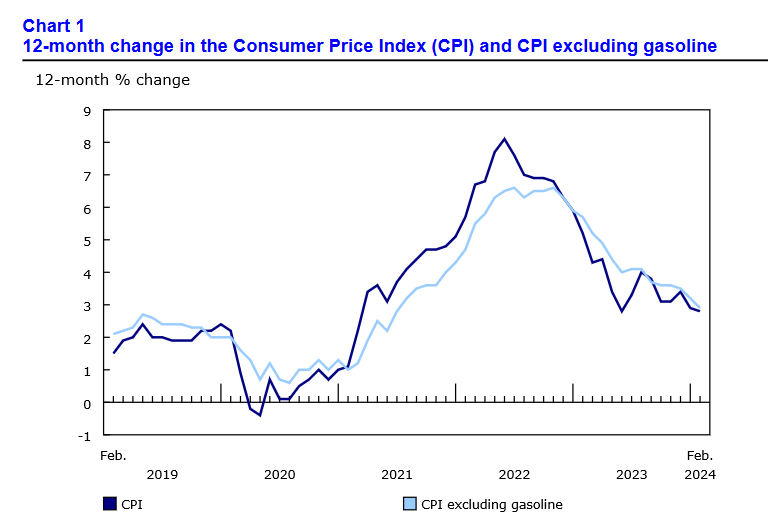

Canadian CPI cools to 2.8% yoy in Feb, below expectations

Canada's CPI decelerated in February, registering an increase of 2.8% yoy, which fell short of anticipated 3.1% yoy. This slowdown from January's 2.9% yoy offers a glimmer of relief as inflationary pressures show signs of easing. When gasoline prices are excluded, CPI was down from 3.2% yoy to 2.9% yoy. Gasoline prices themselves saw a modest uptick of 0.8% yoy, a notable recovery from -4.0% yoy decrease observed in the previous month.

The more specific measures of inflation, which provide a clearer view of underlying trends, also reflected a cooling trend. CPI median, a measure that provides a middle ground by excluding extreme fluctuations, slowed from 3.3% yoy to 3.1% yoy, coming in below the expected 3.3%. Similarly, CPI trimmed, which removes the most volatile components, decreased from 3.4% yoy to 3.2% yoy. Lastly, CPI common, often regarded as a core measure that tracks common price changes across categories, decelerated from 3.4% yoy to 3.1% yoy, again missing the forecast of 3.4%.

ECB's de Guindos and de Cos eye June for rate cut

ECB Vice President Luis de Guindos emphasized the bank's expectation of having "far more data" by June, which will be crucial for evaluating the appropriateness of a rate reduction.

De Guindos also noted the current market optimism for a "soft landing" and the continued decrease in inflation. However, he warned "there could be a different situation that leads to an abrupt adjustment."

At the same event in Madrid, Governing Council member Pablo Hernandez de Cos conveyed a similar sentiment, suggesting that, based on current expectations and if macroeconomic and inflation forecasts hold, rate cuts could commence as early as June.

However, de Cos was careful to clarify that this projection does not constitute "explicit monetary policy guidance" but rather but rather "guidance that is conditioned by the evolution of data and how they can surprise us in one direction or another."

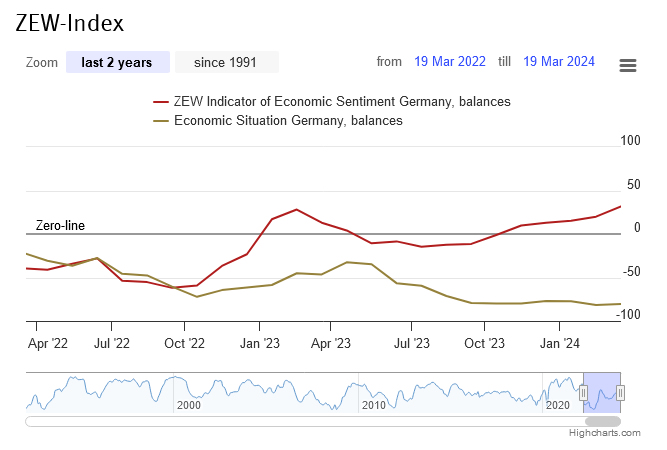

German ZEW surges to 31.7 on ECB rate cut anticipation

German ZEW Economic Sentiment rose sharply from 19.9 to 31.7 in March , well above expectation of 21.0. Current Situation Index ticked up slightly from -81.7 to -80.5, below expectation of -80.0.

Eurozone ZEW Economic Sentiment rose from 25.0 to 33.5, above expectation of 25.4. Current Situation Index fell -1.4 pts to -54.8.

ZEW President Professor Achim Wambach highlighted the "significantly improving" economic expectations for Germany. A key factor contributing to this optimism appears to be the widespread anticipation of an interest rate cut by ECB "in the next six months", as expected by over 80% of survey participants.

Additionally, Wambach pointed out that the German export sector stands to benefit from "increased economic expectations for China "and the anticipated depreciation of Dollar against Euro.

Despite these positive developments in sentiment, Wambach cautioned that the assessment of the current economic situation remains at a very low level. "This development somewhat diminishes the increased economic expectations," he added.

Swiss SECO lowers 2024 inflation forecasts sharply to 1.5%, keeps growth at 1.1%

The Swiss Federal Expert Group on Business Cycles maintained its expectation for modest GDP growth at 1.1% for 2024, with improvement to 1.7% in 2025. Uunemployment rate is projected to remain stable at 2.3% in 2024 before rising to 2.5% in 2025. Notably, inflation forecast for 2024 has been revised sharply down to 1.5% from an earlier estimate of 1.9%, and is expected to slow to 1.1% in 2025.

The group also outlined risks to the Swiss economy, including geopolitical tensions in the Middle East and Ukraine, which could disrupt commodity markets. Prolonged period of restrictive international monetary policy may dampen global demand, impacting Switzerland's recovery. Specific concerns were raised about Germany's industrial slowdown and China's economic cooling, which could affect Swiss foreign trade.

Conversely, there's a possibility that the recovery could outpace expectations, especially if global inflation decreases faster than anticipated, boosting consumer purchasing power and leading to quicker monetary policy easing. This scenario would likely stimulate demand further.

BoJ ends YCC and negative rates as they have fulfilled their roles

In a landmark decision that marks a significant shift in Japan's monetary policy, BoJ announced the termination of its Yield Curve Control framework and negative interest rate policy, signifying that these measures "have fulfilled their roles."

This pivotal move is underpinned by BoJ's assessment that a "virtuous cycle between wages and prices" has come in sight and that the long-standing 2% inflation target is on track to be "achieved in a sustainable and stable manner."

Setting the overnight call rate to a range of 0-0.1%, the decision was reached with a majority vote of 7-2.

BoJ will continue its purchase of JGBs at "broadly the same amount as before," ensuring a measure of stability in the bond market. This part of the decision was made with an 8-1 vote. Meanwhile, BoJ has pledged to "respond nimbly" in the event of a rapid rise in long-term interest rates

Additionally, BoJ has outlined plans to discontinue the purchase of ETFs and J-REITs, while the procurement of commercial paper and corporate bonds will be gradually reduced, aiming for discontinuation within approximately one year.

RBA stands pat, not ruling anything in or out

RBA has opted to maintain cash rate target unchanged at 4.35% today, aligning with broad market expectations. The central bank's stance reflects a cautious approach, emphasizing the prevailing uncertainty in both the global and domestic economic environments. RBA's declaration that the path of interest rates remains "uncertain" and that it is "not ruling anything in or out" underscores a flexible policy outlook, leaving the door open for rate adjustments in the future, including the possibility of further hikes.

On the inflation front, RBA acknowledges a moderating trend, consistent with its latest forecasts. This moderation is attributed primarily to slowdown in goods inflation. However, services inflation remains stubbornly high, and ism ode rating at a slower pace. Wages growth, a critical factor in the inflation equation, appears to have peaked.

Addressing the economic outlook, RBA paints a picture of significant uncertainty. Internationally, questions loom over China's economic outlook and the broader impacts of geopolitical conflicts in Ukraine and the Middle East. Domestically, uncertainties pertain to the lag effects of monetary policy adjustments, firms' pricing decisions, wages dynamics, and household consumption patterns.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3519; (P) 1.3536; (R1) 1.3550; More...

USD/CAD's break of 1.3605 resistance suggests that whole rise from 1.3176 is resuming. Intraday bias is back on the upside for 61.8% projection of 1.3176 to 1.3540 from 1.3419 at 1.3644 first. Decisive break there could prompt upside acceleration to 100% projection at 1.3783 next. On the downside, below 1.3527 minor support will turn intraday bias neutral first. But outlook will stay bullish as long as 1.3419 support holds.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 at a later stage.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 03:30 | AUD | RBA Interest Rate Decision | 4.35% | 4.35% | 4.35% | |

| 03:36 | JPY | BoJ Interest Rate Decision | 0.10% | 0.00% | -0.10% | |

| 04:30 | AUD | RBA Press Conference | ||||

| 04:30 | JPY | Industrial Production M/M Jan F | -6.70% | -7.50% | -7.50% | |

| 07:00 | CHF | Trade Balance (CHF) Feb | 3.66B | 3.50B | 4.74B | 4.70B |

| 08:00 | CHF | SECO Economic Forecasts | ||||

| 10:00 | EUR | Germany ZEW Economic Sentiment Mar | 31.7 | 21 | 19.9 | |

| 10:00 | EUR | Germany ZEW Current Situation Mar | -80.5 | -80 | -81.7 | |

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Mar | 33.5 | 25.4 | 25 | |

| 12:30 | CAD | CPI M/M Feb | 0.30% | 0.60% | 0.00% | |

| 12:30 | CAD | CPI Y/Y Feb | 2.80% | 3.10% | 2.90% | |

| 12:30 | CAD | CPI Median Y/Y Feb | 3.10% | 3.30% | 3.30% | |

| 12:30 | CAD | CPI Trimmed Y/Y Feb | 3.20% | 3.40% | 3.40% | |

| 12:30 | CAD | CPI Common Y/Y Feb | 3.10% | 3.40% | 3.40% | |

| 12:30 | USD | Building Permits Feb | 1.52M | 1.50M | 1.47M | |

| 12:30 | USD | Housing Starts Feb | 1.52M | 1.43M | 1.33M |

Canadian CPI cools to 2.8% yoy in Feb, below expectations

Canada's CPI decelerated in February, registering an increase of 2.8% yoy, which fell short of anticipated 3.1% yoy. This slowdown from January's 2.9% yoy offers a glimmer of relief as inflationary pressures show signs of easing. When gasoline prices are excluded, CPI was down from 3.2% yoy to 2.9% yoy. Gasoline prices themselves saw a modest uptick of 0.8% yoy, a notable recovery from -4.0% yoy decrease observed in the previous month.

The more specific measures of inflation, which provide a clearer view of underlying trends, also reflected a cooling trend. CPI median, a measure that provides a middle ground by excluding extreme fluctuations, slowed from 3.3% yoy to 3.1% yoy, coming in below the expected 3.3%. Similarly, CPI trimmed, which removes the most volatile components, decreased from 3.4% yoy to 3.2% yoy. Lastly, CPI common, often regarded as a core measure that tracks common price changes across categories, decelerated from 3.4% yoy to 3.1% yoy, again missing the forecast of 3.4%.

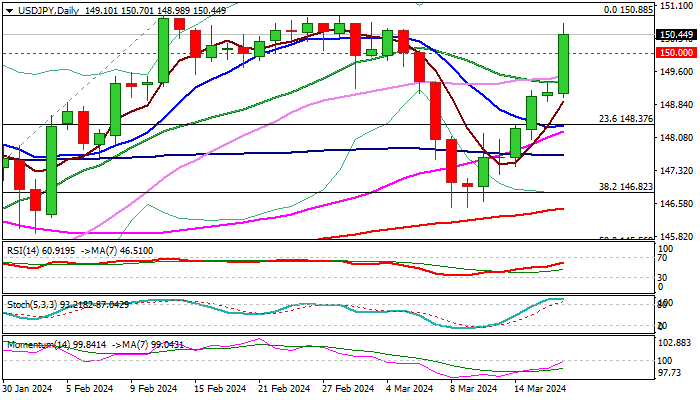

USD/JPY: Yen Loses Ground on Signs of Extended Fed/BoJ Rate Gap

USDJPY was sharply higher (up almost 1%) after BOJ’s major shift, though the message from the central bank was seen as dovish on signals that future policy tightening will be moderate, which will keep the big rate gap between the Fed and BoJ and favor the dollar.

Fresh acceleration extends recovery leg from 146.48 higher base (where a bear-trap has also formed) and returned above psychological 150 level.

Almost full retracement of 150.88/146.48 correction adds to bullish bias, with close above 150 to reinforce bullish structure for attack at 150.88 (2024 high), violation of which to expose multi-decade highs at 151.90/94.

Improved daily studies underpin the action but overbought conditions and 14-d momentum still in the negative territory warn that bulls may face increased headwinds.

Dips should ideally stay above 150 level and extended downticks should not exceed 20DMA (149.37) to keep near-term bulls in play.

Markets shift focus towards FOMC meeting on Wednesday, to get more signals about Fed’s next steps, as June rate cut is widely expected.

Res: 150.88; 151.43; 151.90; 151.94.

Sup: 150.00; 149.37; 148.92; 148.35.

ECB’s de Guindos and de Cos eye June for rate cut

ECB Vice President Luis de Guindos emphasized the bank's expectation of having "far more data" by June, which will be crucial for evaluating the appropriateness of a rate reduction.

De Guindos also noted the current market optimism for a "soft landing" and the continued decrease in inflation. However, he warned "there could be a different situation that leads to an abrupt adjustment."

At the same event in Madrid, Governing Council member Pablo Hernandez de Cos conveyed a similar sentiment, suggesting that, based on current expectations and if macroeconomic and inflation forecasts hold, rate cuts could commence as early as June.

However, de Cos was careful to clarify that this projection does not constitute "explicit monetary policy guidance" but rather but rather "guidance that is conditioned by the evolution of data and how they can surprise us in one direction or another."

German ZEW surges to 31.7 on ECB rate cut anticipation

German ZEW Economic Sentiment rose sharply from 19.9 to 31.7 in March , well above expectation of 21.0. Current Situation Index ticked up slightly from -81.7 to -80.5, below expectation of -80.0.

Eurozone ZEW Economic Sentiment rose from 25.0 to 33.5, above expectation of 25.4. Current Situation Index fell -1.4 pts to -54.8.

ZEW President Professor Achim Wambach highlighted the "significantly improving" economic expectations for Germany. A key factor contributing to this optimism appears to be the widespread anticipation of an interest rate cut by ECB "in the next six months", as expected by over 80% of survey participants.

Additionally, Wambach pointed out that the German export sector stands to benefit from "increased economic expectations for China "and the anticipated depreciation of Dollar against Euro.

Despite these positive developments in sentiment, Wambach cautioned that the assessment of the current economic situation remains at a very low level. "This development somewhat diminishes the increased economic expectations," he added.

Aussie Slides After RBA’s Pause

The Australian dollar is sharply lower on Tuesday. In the European session, AUD/USD is trading at 0.6507, down 0.80%. The Aussie is on a nasty slide and has declined by 1.7% since March 13.

RBA removes tightening bias

The Reserve Bank of Australia maintained the cash rate at 4.35% for a fourth straight time at today’s meeting. A pause was widely expected, which left the focus on the rate statement and Governor Bullock’s follow-up press conference.

The RBA statement noted that the “Board is not ruling anything in or out”, which was a change from the February statement which said “a further increase in interest rates cannot be ruled out”. The markets jumped on this slight variance, taking it as a signal that the RBA had removed its hiking bias. The Australian dollar has responded with sharp losses in the aftermath of the meeting.

The statement said that “encouraging signs that inflation is moderating”, but the RBA remains concerned that inflation still remains high and is worried about the uncertain economic outlook, both domestically and abroad. Household consumption remains weak and growth has slowed, and China’s economy remains a major concern.

The bottom line? Inflation is still too high and the RBA won’t be rushed into lowering rates until it sees a further drop in inflation. At her press conference, Governor Bullock tried to downplay the change in language in the statement, but the markets viewed this as a significant step towards trimming rates later this year.

In the US, it’s an unusually quiet week, with no tier-1 events on the data calendar. Investors will be focused on the Federal Reserve’s rate announcement on Wednesday. The Fed is virtually certain to maintain the benchmark rate of 5%-5.25%, and will be combing the rate statement for any insights about a date for an initial rate cut.

AUD/USD Technical

- AUD/USD has pushed below support at 0.6528 and is putting pressure on support at 0.6497

- There is resistance at 0.6584 and 0.6615

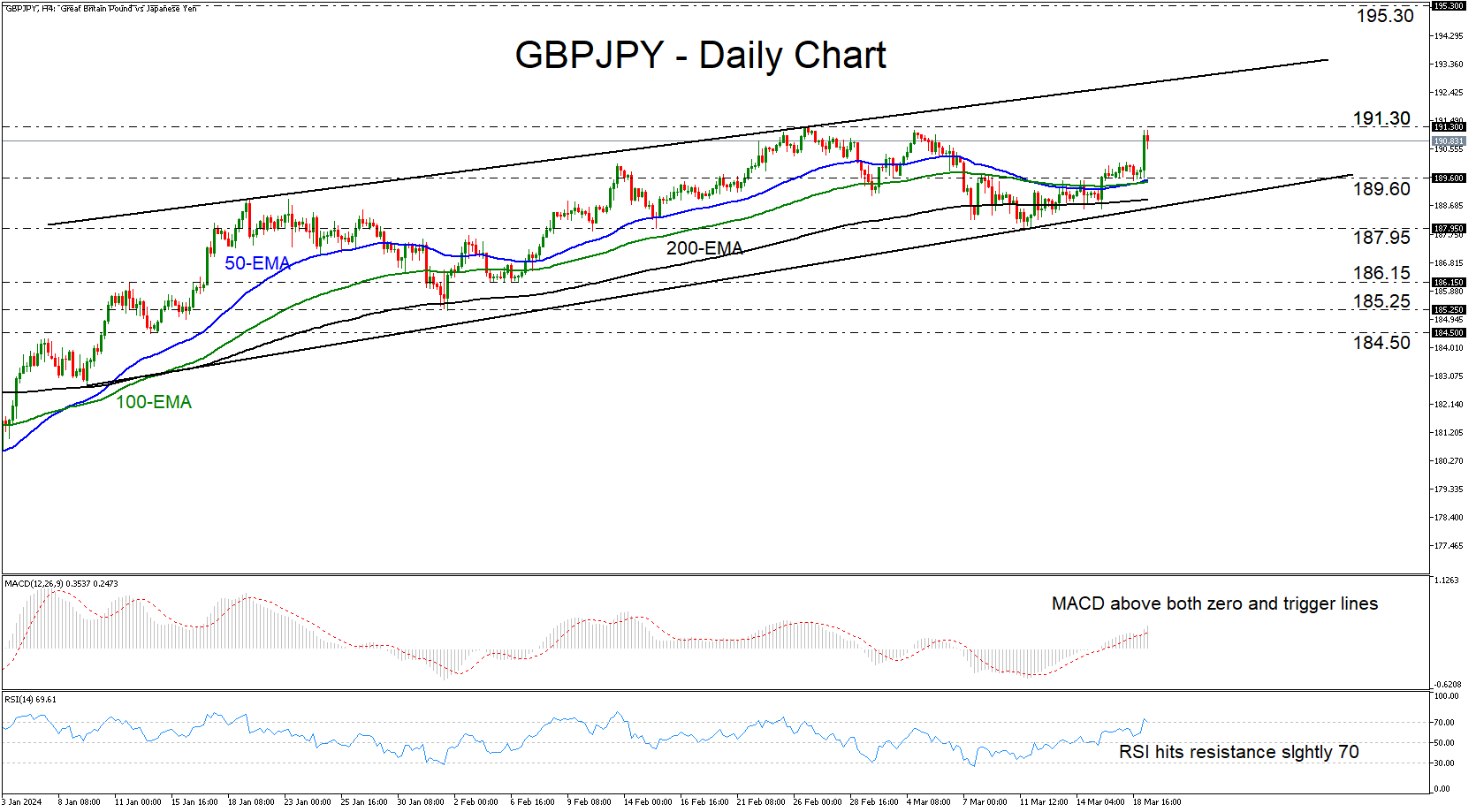

Will GBPJPY Enter Territories Last Seen in 2015?

- GBPJPY trades higher and hits resistance near 191.30

- Remains in uptrend despite BoJ decision

- MACD and RSI detect positive momentum

- For the outlook to change, a dip below 187.95 may be needed

GBPJPY traded higher yesterday, but hit resistance near the 191.30 barrier today, marked by the high of February 26, and pulled back somewhat. Even after the BoJ took interest rates out of negative territory and abandoned yield curve control, the pair remains in an uptrend as denoted by the upward sloping trendline drawn from the low of January 9.

The short-term oscillators detect positive momentum corroborating the bullish outlook. The MACD is running above both its zero and trigger lines, while the RSI is lying within its above-70 zone, although it ticked down today. This means that some further retreat may be on the cards before the next leg north.

The bulls could take charge again from near the 189.60 zone, which coincides with the 50- and 100-period exponential moving averages (EMAs), and they may drive the action above 191.30, entering territories last tested in August 2015. The next resistance obstacle may be the upward sloping resistance line drawn from the high of January 19, but if traders are willing to overcome that line as well, they could take the pair all the way up to the 195.30 area, which acted as a ceiling during the whole summer of 2015.

For the near-term picture to shift to bearish, a decisive dip below 187.95 may be needed. Such a move will take GBPJPY below all the plotted moving averages and below the uptrend line taken from the low of January 9. The bears may then get encouraged to dive towards the 186.15 zone that offered support between February 5 and 7.

To sum up, GBPJPY remains in an uptrend despite the BoJ hiking interest rates and abandoning yield curve control. A break above 191.30 will confirm a higher high and take the pair into territories last tested in 2015.