Sample Category Title

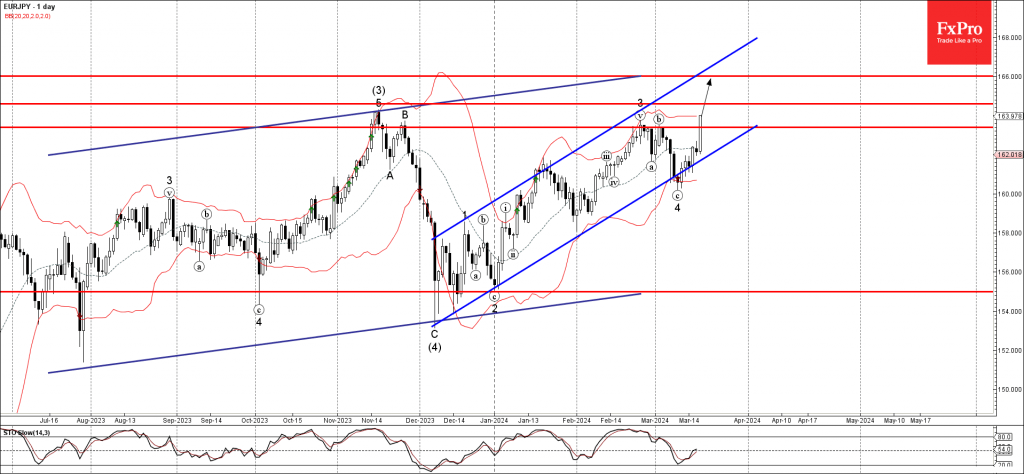

EURJPY Wave Analysis

- EURJPY broke pivotal resistance level 163.40

- Likely to rise to resistance level 164.35

EURJPY today broke above the pivotal resistance level 163.40 (which stopped the previous waves 3 and (b), as can be seen from the daily EURJPY chart below).

The breakout of the resistance level 163.40 continues the active minor impulse wave 5 of the intermediate impulse wave (5) from the start of December.

Given the clear daily uptrend, EURJPY currency pair can be expected to rise further toward the next resistance level 164.35 (top of wave (3) from November) – followed by 166.00.

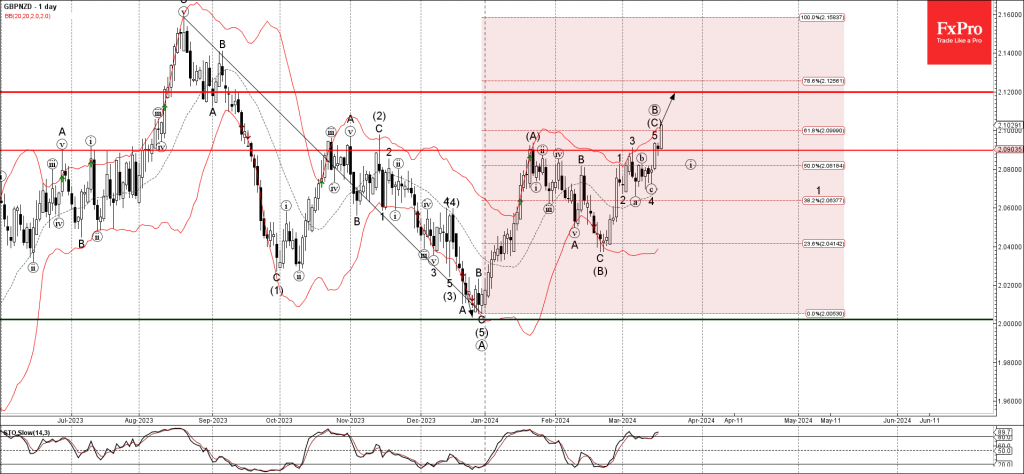

GBPNZD Wave Analysis

- GBPNZD broke resistance level 2.0895

- Likely to rise to resistance level 2.1200

GBPNZD today broke the major resistance level 2.0895 (which has been reversing the price from the end of October, as can be seen from the daily GBPNZD chart below).

The breakout of the resistance level 2.0895 coincided with the breakout of the 50% Fibonacci correction of the previous downtrend from August.

Given the strongly bullish sterling sentiment, GBPNZD currency pair can be expected to rise further toward the next resistance level 2.1200.

Sunset Market Commentary

Markets

The Bank of Japan’s first rate hike since 2007 that ended an 8-year experiment with negative rates remained talk of the town today. Ironically though, the Japanese yen nor yields profited from what is nevertheless a historical shift, quite the contrary. This morning’s policy outcome was telegraphed well in advance to markets and there’s a dovish twist to each of the separate decisions: a) the rate hike won’t be met by swift follow-through action; b) abandoning YCC is sugarcoated by a still-lofty regular bond buying scheme and a BoJ backstop to prevent yields from rising too sharply and c) ending ETF and J-REIT purchases was simply officializing what the BoJ already stopped doing since 2023. Governor Ueda during the press conference stressed the need to keep conditions accommodative. The price target is in sight but certainty of hitting it isn’t 100% yet, dixit Ueda. What the BoJ probably wanted was to keep volatility low. But trying to nip speculation for aggressive tightening in the bud backfired, forcing the yen to lose almost 1% against the dollar instead. Ueda added that if the currency impacts the outlook materially, the BoJ will consider a policy response. With USD/JPY (150.54) rapidly nearing the 2022 multi-decade high (151.95) this may be the case sooner rather than later. Japanese yields ended the day up to 2.6 bps (10-y) lower and stock markets cheered (+1%).

Market moves outside Japan were relatively muted ahead of tomorrow’s Fed meeting. The dollar continues to trade in a sweet spot. EUR/USD hit an intraday low of 1.0835 before paring losses to 1.0864. DXY flirted with the 104 big figure. Currencies Down Under trade on the backfoot. The Reserve Bank of Australia moderated its hawkish tone and that weighed on Aussie yields and the local dollar with spill-overs to neighbouring New Zealand. Core bond yields lose a few bps in technical trading, shying away from resistance levels marked by the year-to-date highs. US rates lose up 4.3 bps, German yields drop 3.6 bps with the front-end of both curves outperforming. Oil prices extend their recent winning streak to $87.2 p/b. Economic data were largely ignored by markets. They included a better-than-expected German ZEW indicator on the expectations component hitting the highest level since before the Russian invasion. US housing data (starts and building permits) also topped forecasts.

News & Views

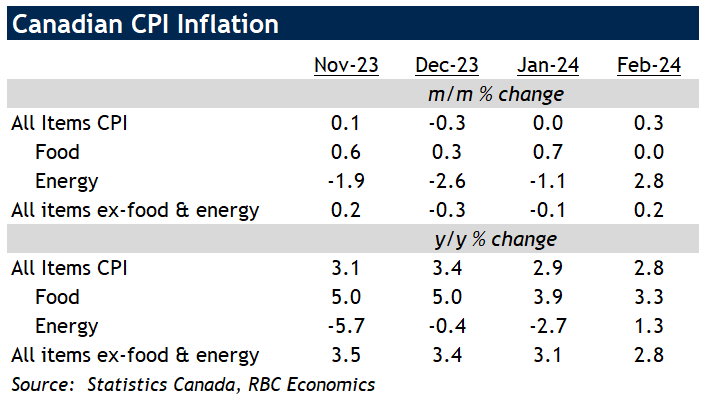

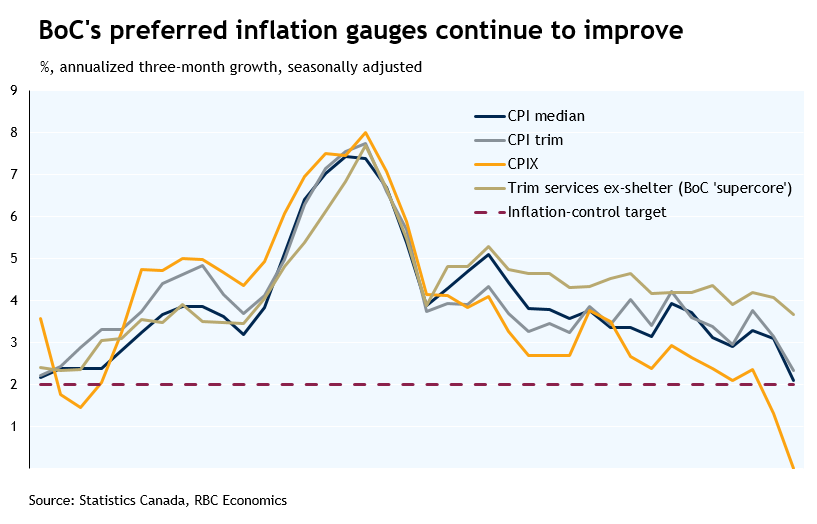

Canadian inflation accelerated “only” to 0.3% M/M from flat in January whereas consensus feared a 0.6% monthly increase. The largest contributors to the monthly increase were higher prices for travel tours and gasoline. February was the first month since October 2021 that grocery prices increased at a slower rate than headline inflation. As a consequence, the Y/Y-figure slowed from 2.9% to 2.8% (vs 3.1% forecast and matching the lowest level since March 2021). The Bank of Canada’s preferred inflation gauge, the CPI core – trimmed mean slowed from 3.4% Y/Y to 3.2% Y/Y, beating the flat expected consensus and recording the lowest level since the summer of 2021. Canadian markets reacted to the beneficial inflation print. CAD swap rates slide 5 to 12 bps with the front end of the curve outperforming. USD/CAD tests the YTD high around 1.36 on a combination of USD strength and CAD weakness. The Bank of Canada recently shifted from a tightening bias to judging how long policy rates would have to remain stable at the current level (5%). Canadian money markets attach an 80% probability to a first 25 bps rate at the June policy meeting.

The Swiss government cut its inflation forecast for this year from 1.9% to 1.5%. The 2025 estimate is unchanged from December at 1.1%. The downgrade of the State Secretariat for Economic Affairs is mainly because of the significantly lower January CPI reading (0.2% M/M & 1.3% Y/Y) despite a boost in VAT and electricity prices. The strengthening of the Swiss franc is at play as well. Growth forecasts are unchanged at 1.1% for this year and 1.7% next year. The Swiss National Bank meets on Thursday. Consensus expects an unchanged policy rate (1.75%) with the risk that they’ll already push through or at least put forward a 25 bps rate cut. Since early February, the Swiss franc weakened from EUR/CHF 0.93 to currently 0.9640. First strong resistance stands around 0.97.

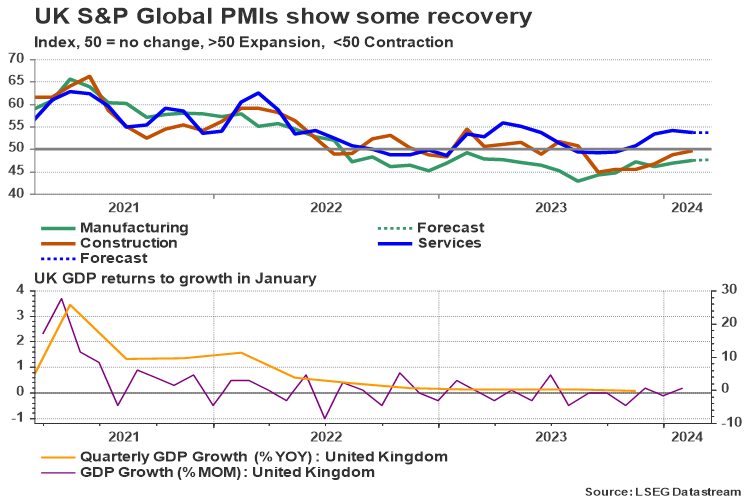

BoE Policy Meeting: Don’t Expect Fireworks

- Bank of England to retain the same policy stance

- Q2 data could be more valuable for next decision making

What happened last time

In its February policy meeting, the Bank of England (BoE) emulated the Federal Reserve by exploring rate cuts, ultimately deciding to maintain interest rates at 5.25%, their highest level in 16 years, with a 6-3 majority vote. Two policymakers voted for a rate hike but surprisingly, one policymaker raised his hand for a quarter-percentage point rate cut for the first time since the pandemic. On top of this, the central bank removed the sentence that referred to further tightening, adding to speculation that the rate hike cycle was now in the past and a new chapter of rate cuts would open in the coming months.

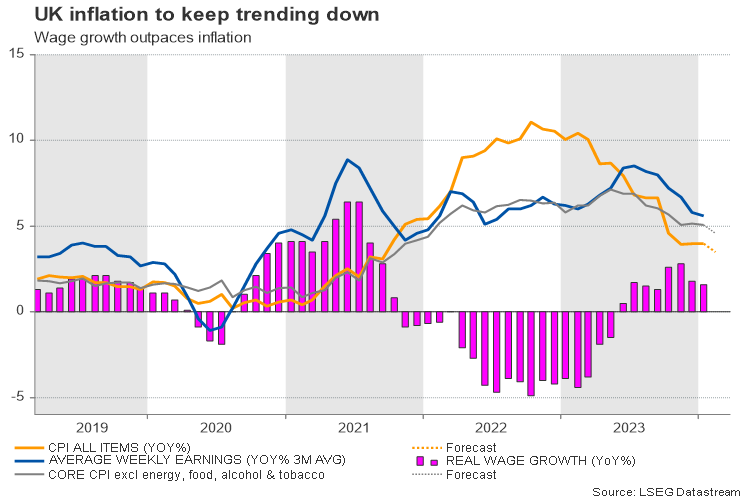

However, the central bank provided no clues about the timing of rate cuts, reiterating in the policy statement that more evidence is needed to confirm inflation is moving sustainably towards its 2.0% target. This narrative might be repeated once again when the central bank reviews its policy on Thursday. UK inflation stabilized at 4.0% y/y in January but given the recent upside surprises in the eurozone and the US CPI data, a meaningful pullback to 3.5% as analysts expect, is questionable. Besides, with the economy moving out of a mild technical recession in January on the back of growing consumption and construction, policymakers might avoid any premature rate cut signals.

Inflation expectations

Inflation expectations

The BoE economic forecasts predict a temporary slide in inflation to the 2.0% target in Q2 of this year, followed by a subsequent increase before gradually falling below that level in three years. Chancellor Jeremy Hunt did not reignite new inflation concerns nor did he spark concerns about high debt when he introduced his spring budget earlier this month. Hence, the central bank might feel more confident sticking to its current policy, especially as the continuous slowdown in wage growth keeps denting fears of a wage-price spiral.

Interestingly, BoE governor Andrew Bailey admitted that interest rates might go down before inflation reaches the central bank’s goal. Perhaps he wanted to emphasize that sustained progress on services' costs, wage growth and labor shortages might be enough information to proceed with rate cuts. In the meantime, though, there is no guarantee that the economy will meet these conditions soon given that wage growth is still well above the inflation rate and higher than 4% observed in the US and eurozone. Upcoming wage increases in April will be closely watched for that reason, while potential spikes in raw material costs and energy prices cannot be ruled out either, given the persisting geopolitical risks in Ukraine and the Middle East.

Will the central bank call for a June rate cut?

Therefore, the rate statement might give little reason for investors to bring forward their rate cut projections from August to June. Also, if one more hawk migrates to the group of unchanged rates, shifting the voting structure to 7-2 as analysts project, that would be another indication that rate cuts are coming instead of a preference for an earlier rate reduction.

Futures markets are currently reflecting a less than 50% probability of a quarter-percentage rate cut in June and around 70% chance for a similar move in August. Perhaps investors could adjust their rate projections if inflation readings fall short of analysts’ estimates, but that would still be in line with the BoE’s forecast for a significant inflation slowdown this year. Moreover, an unexpected pullback in the flash business PMI figures due on Thursday could justify the central bank’s muted GDP growth forecast for Q1, whilst stronger-than-expected readings might question the need for a rate cut.

Thus, unless the BoE tweaks its language to support a dovish change in June, the pound could strengthen as markets would delay the possibility of rate cuts. Perhaps the second quarter data could be more vital for decision making and hence a bigger source of volatility.

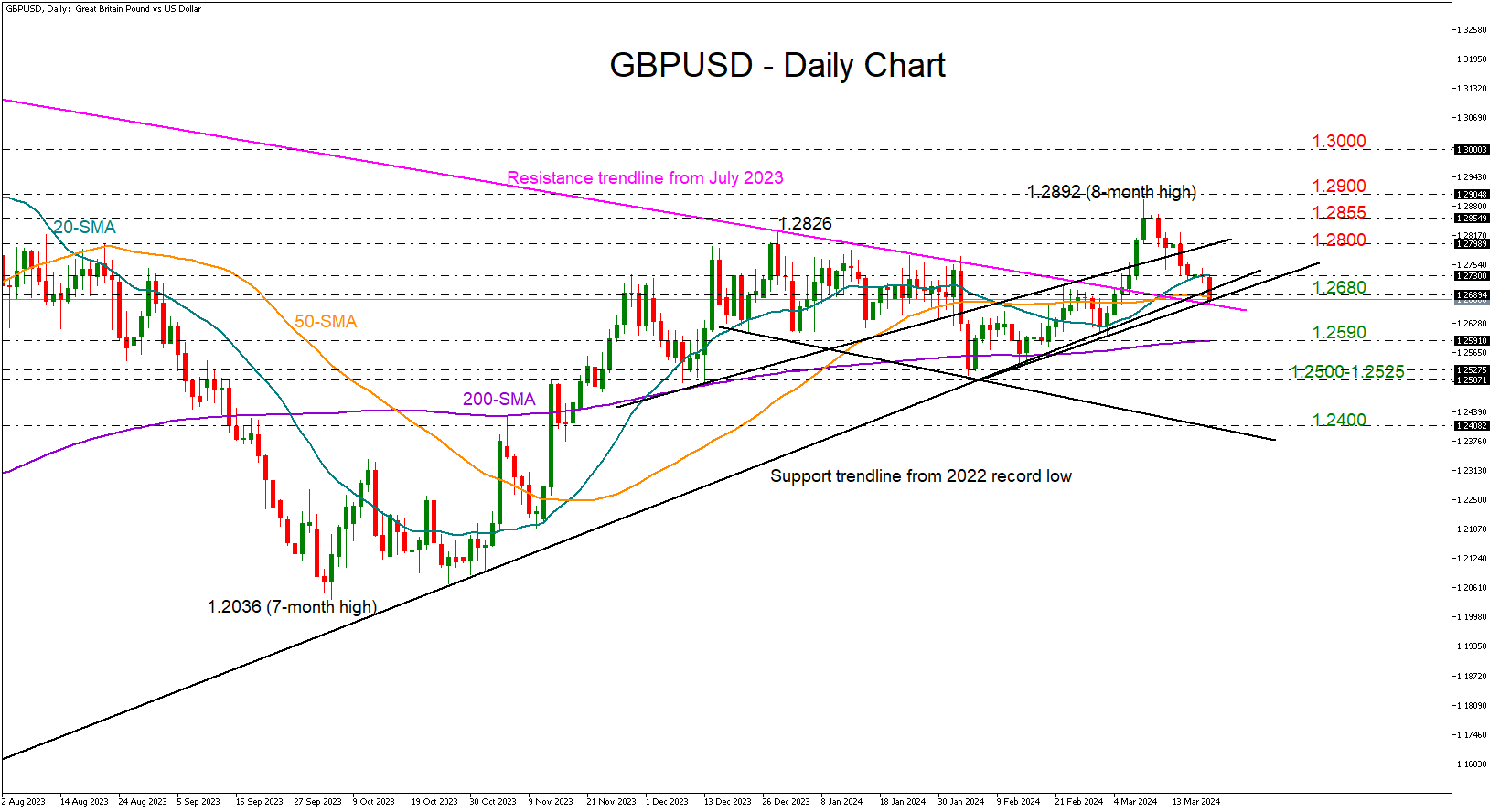

GBP/USD levels to watch

At present, GBPUSD is seeking support around the 1.2680 region following its pullback from an eight-month high of 1.2892. A close below that floor would downgrade the short-term outlook back to neutral, consequently causing a slump towards its 200-day simple moving average (SMA) at 1.2590.

On the upside, the bulls will have to crawl back above the 20-day SMA at 1.2730 in order to reach the 1.2800 round level. A move higher and above the 1.2855-1.2900 wall could see an advance towards the 1.3000 psychological level.

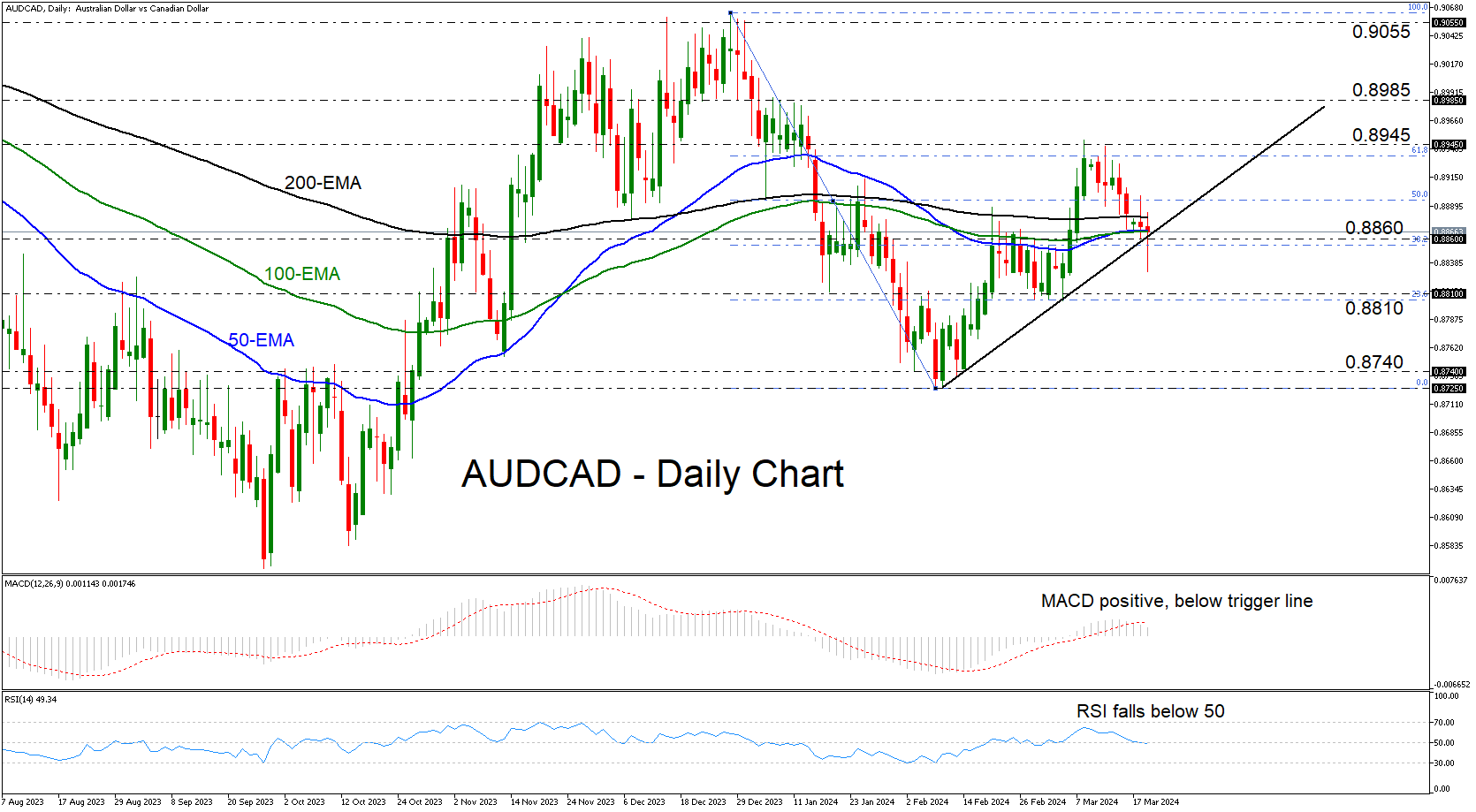

Is Upside Corrective Phase in AUDCAD Over?

- AUDCAD briefly breaks below upside support line

- Oscillators suggest that momentum is turning bearish

- For the outlook to brighten, a recovery above 0.8945 may be needed

AUDCAD entered a sliding mode on March 12, after hitting resistance at 0.8945, slightly above the 61.8% Fibonacci retracement level of the December 18 – February 8 decline. Today, after the RBA softened its policy guidance, the pair fell below the upward sloping support line drawn from the low of February 9, but it rebounded back above it after Canada’s lower-than-expected CPI numbers.

Both the MACD and the RSI suggest that another round of declines may be possible soon. The former, although still positive, has fallen below its trigger line, while the latter has crossed below its 50 line, indicating bearish momentum.

If the bears are strong enough to take the pair back below the upside line and the 0.8860 area, they may drive the action towards the 0.8810 barrier, which offered support between February 28 and March 5. If that zone doesn’t hold, then a further decline could pave the way towards the 0.8740 territory, near the lows of February 13 and 14.

For the outlook to brighten again, the pair may need to climb all the way above the 0.8945 barrier. Such a move will confirm a higher high and thereby the continuation of the recovery phase that started on February 9. The next obstacle for the bulls may be at around 0.8985, the break of which could carry extensions towards the 0.9055 territory, which acted as a ceiling between December 14 and January 2.

To recap, AUDCAD has been trading in a sliding mode recently, briefly falling below an upward sloping support line today. If the bears regain control soon and push the price back below that line, this may signal the end of the upside correction that started on February 9.

Another Downside Surprise in Canadian February CPI

Canadian CPI growth was lower than expected in February, dropping to 2.8% year-over-year from 2.9% in January (expectations were for a 3.1% reading.) The downside surprise was broad-based as core CPI ex-food and energy inflation eased further to 2.8% from 3.1% in January.

Food and energy inflation were as expected - food CPI growth in February slowed further to 3.3% above last year, while energy inflation rose to 1.3% also year-over-year on higher gasoline prices.

Grocery inflation slowed to 2.4% in February with most food groups including meats, fruit and nuts seeing monthly (seasonally adjusted) price declines from January. Price growth for restaurant dining was little changed on a year-over-year basis from January, at 5.1%.

Shelter CPI growth continued to accelerate upon rising rent inflation that climbed to 7.9% in February. That was partially offset by slowing, but still-elevated price growth in mortgage interest costs (+26%) which should continue to trend lower as lending rates drop relative to a year ago.

Among other items, inflation for health care continued to trend lower to 2.7% in February, while prices for clothing and footwear (-4.2%), as well as air fares (-5.2%) both remained below where they were a year ago.

Slowing price pressures were more apparent in Bank of Canada’s aggregate core inflation measures – CPI trim (+3.2%) and CPI median (+3.1%) both eased further towards the top end of the inflation target range in Canada. The more recent three-month rolling average growth rates for those same measures averaged at 2.2% in February, or its lowest reading in three years.

Bottom Line: Building on the January CPI report that was already showing broad-based easing in price pressures in Canada, the February report today reaffirmed those trends. Different measures of core inflation all decelerated and the diffusion index that measures the scope of inflation pressures also improved. That measure however was still showing slightly broader price pressures than pre-pandemic “norms”, suggesting there’s still room for more improvement. Overall, we continue to expect a persistently soft economic backdrop to further slow inflation readings in Canada in the months ahead, allowing for the BoC to start lowering interest rates around mid-year.

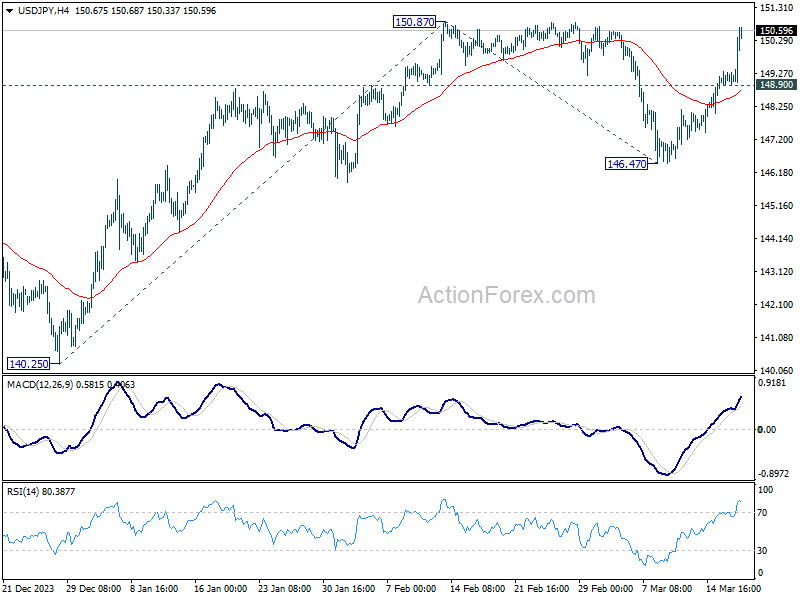

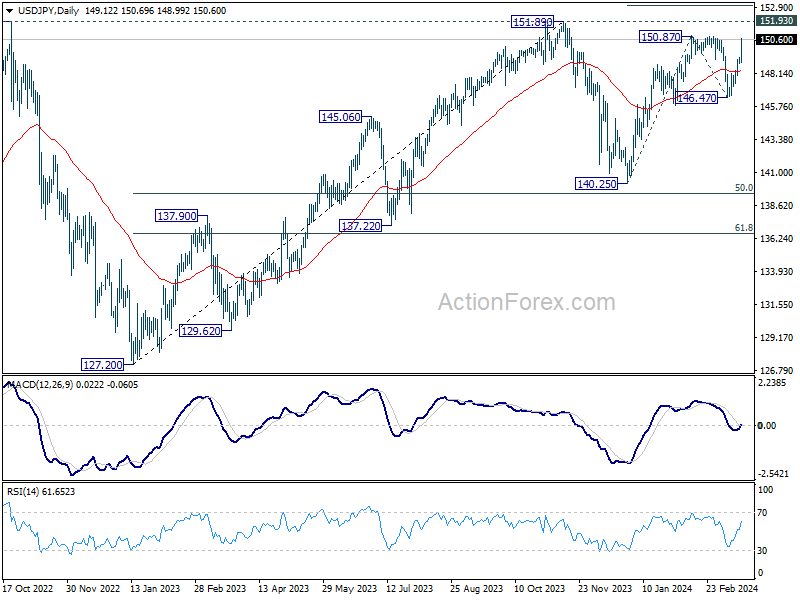

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 148.93; (P) 149.13; (R1) 149.35; More...

Intraday bias in USD/JPY remains on the upside for the moment. Firm break of 150.87/89 resistance will confirm larger up trend resumption. Next near term target will be 61.8% projection of 140.25 to 150.87 from 146.47 at 153.03. On the downside, below 148.90 minor support will delay the bullish case and turn intraday bias neutral first. But outlook will now remain bullish as long as 146.47 support holds.

In the bigger picture, correction from 151.87 (2023) high could have completed at 140.25 already. Rise from 127.20 (2023 low), as part of the long term up trend, is probably ready to resume. Decisive break of 151.93 resistance (2022 high) will confirm this bullish case. Also, this will remain the favored case as long as 140.25 support holds, in case of another fall.

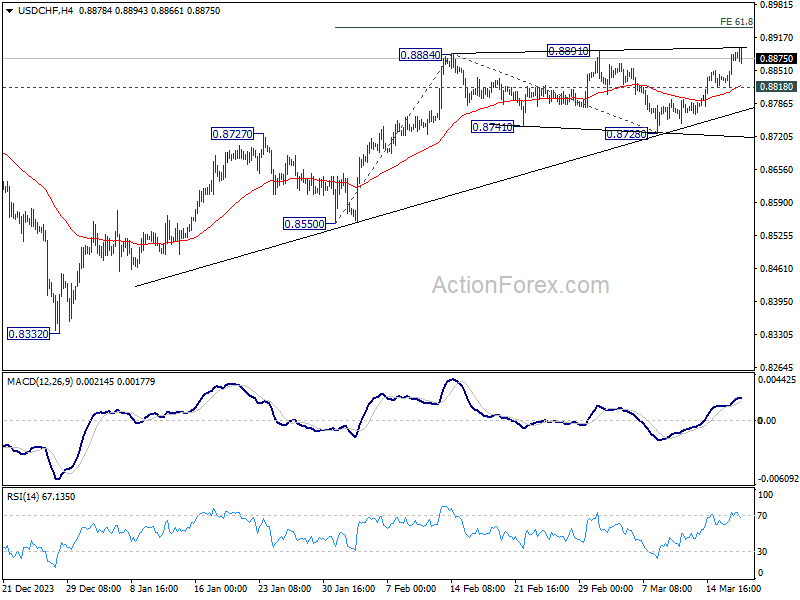

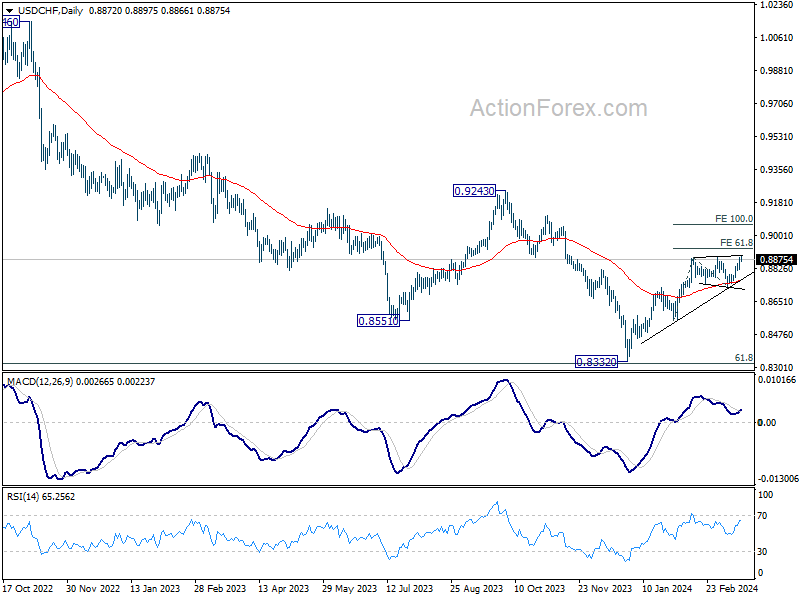

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8838; (P) 0.8863; (R1) 0.8903; More....

Intraday bias in USD/CHF remains on the upside at this point. Decisive break of 0.8891 resistance will confirm resumption of rally from 0.8332. Next target is 61.8% projection of 0.8550 to 0.8884 from 0.8728 at 0.8934. On the downside, below 0.8818 minor support will turn intraday bias neutral and bring consolidations. But outlook will stay bullish as long as as long as 0.8728 support holds, in case of retreat.

In the bigger picture, price actions from 0.8332 medium term bottom as seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8555 support holds. But upside should be limited by 0.9243 resistance, at least on first attempt.

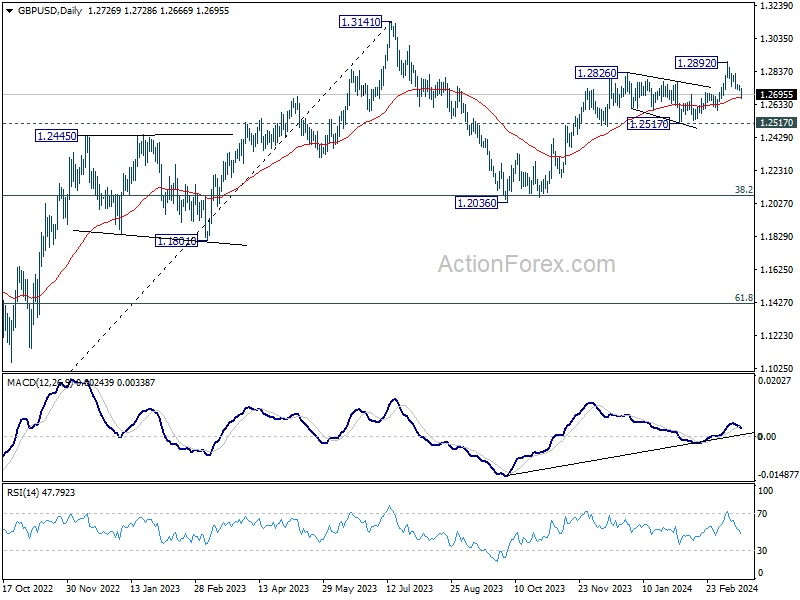

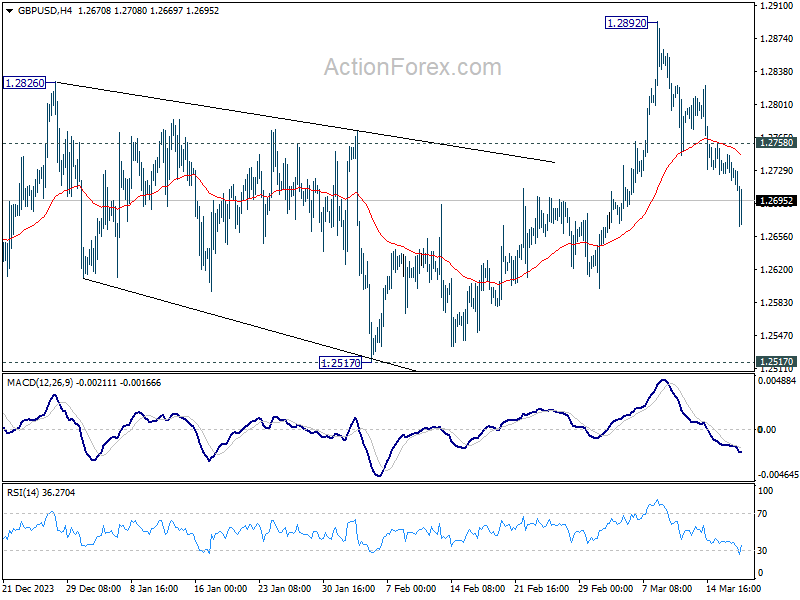

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2716; (P) 1.2731; (R1) 1.2745; More...

Intraday bias in GBP/USD remains on the downside as fall from 1.2892 is in progress. Sustained break of 55 D EMA (now at 1.2677) will target 1.2517 structural support next. On the upside, above 1.2758 minor resistance will turn intraday bias neutral first.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which is still in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2517 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.