Sample Category Title

Weekly Economic & Financial Commentary: FOMC Likely on Hold Until Summer

Summary

United States: The Equinox and the Struggle to Find Balance

- Spring is a time for new beginnings, and we see fresh possibility in some of this week's less-than-stellar data. It may eventually help bring the needed balance into place to get inflation closer to the FOMC's target.

- Next week: Housing Starts (Tue.), Existing Home Sales (Thu.)

International: Latin America Disinflation Is Stalling

- While nations across Latin America have made impressive progress in their battles against inflation, regional disinflation hit a few speed bumps this week that could disrupt rate cut cycles.

- Next week: Bank of Japan (Tue.), Bank of England (Thu.), Central Bank of Mexico (Thu.)

Interest Rate Watch: FOMC Likely on Hold Until Summer

- Very few observers, ourselves included, look for a policy change at next week's FOMC meeting. Indeed, recent data have reduced the odds that the Committee will cut rates at its next meeting on May 1. Accordingly, we have pushed out our expectation of the commencement of the easing cycle to June 12.

Topic of the Week: Consumer Expectations Deteriorate for Lower Income Cohorts

- Earlier this week, the New York Fed released the February update to its Survey of Consumer Expectations (SCE). The recent update depicts lower income consumers as increasingly uncertain amid broader signs of the labor market softening.

Fed to Keep Rates Unchanged for a Fifth Meeting Even as Inflation Risks Lurk

The U.S. Federal Reserve is widely expected to stand pat on the fed funds range for a fifth consecutive meeting on Wednesday. But any shift in the monetary policy statement language will be closely watched after two straight months of upside surprises on inflation.

Markets continue to expect the first interest rate cut in June in line with our expectations. But we now anticipate the Fed will be moving at a slower pace and cut rates by 75 basis points (instead of the 125 bps previously expected) this year to 4.5-4.75%, given the above-target price increases and strong growth in output and employment. Its accompanying Summary of Economic Projections will be reviewed for any changes in the expected number of rate cuts this year, and potential revisions to GDP growth, unemployment rate and inflation forecasts.

Recent comments from Fed officials have suggested they’re still committed to moving rates lower this year despite the setback in inflation. That, however, is contingent upon inflation readings easing in the months ahead. There are still three more consumer price index releases before the Fed’s June meeting. Headline inflation should follow market rent measures lower by then.

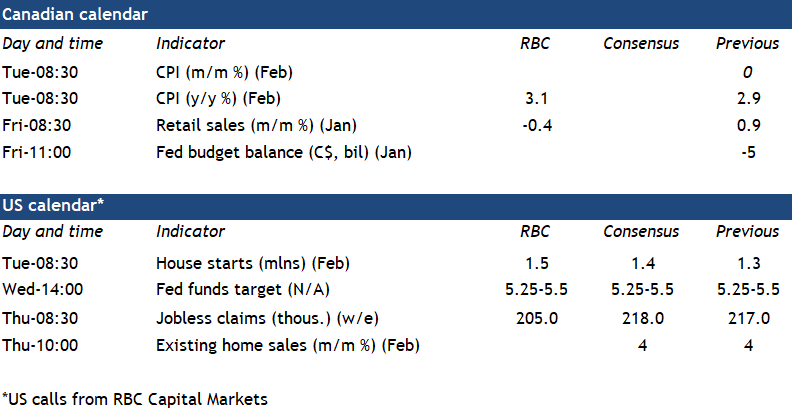

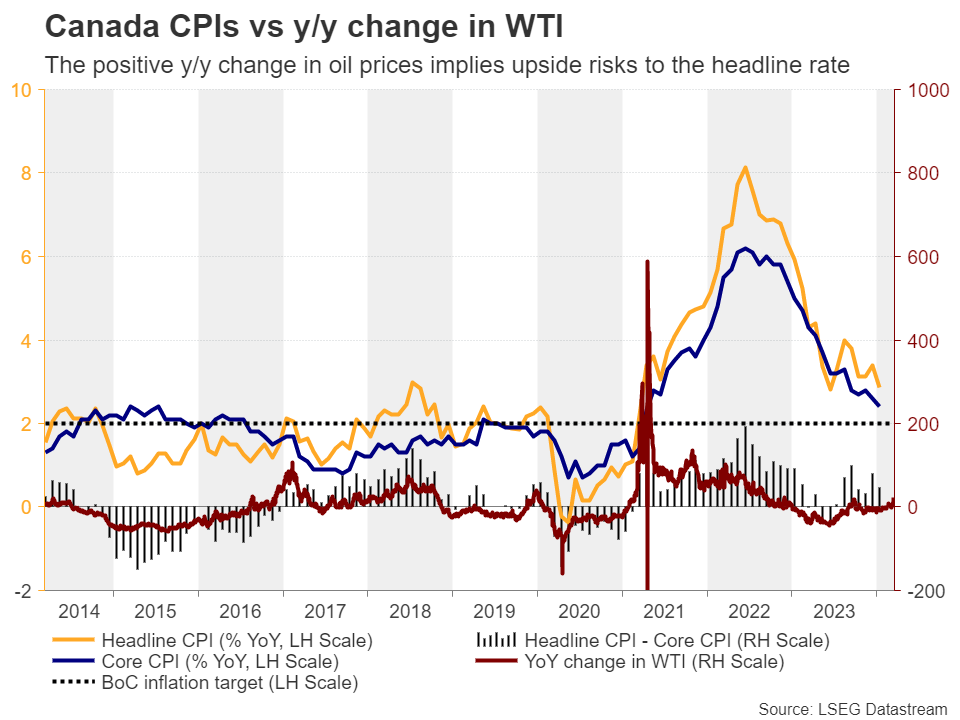

Similarly, Canada’s February CPI print on Tuesday will be watched by the Bank of Canada for more signs of improvement in price pressures. Both headline and core (ex-food and energy) inflation are expected to come in at 3.1% year-over-year with headline up from 2.9% in January on higher energy inflation. Gasoline prices rose by nearly 4% in February from a month ago. Still, a very soft economic backdrop means that price pressures in Canada are more likely to keep easing and narrowing, allowing for a first rate cut from the BoC to also come in June.

Week ahead data watch

Retail sales in Canada are expected to edge lower in January by 0.4% (nominal), consistent with Statistics Canada’s preliminary call. Gasoline prices were lower in January, but the volume is also expected to have dropped by 0.3% due to lower auto sales.

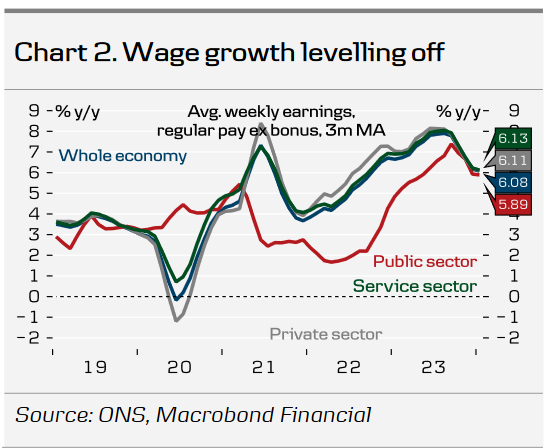

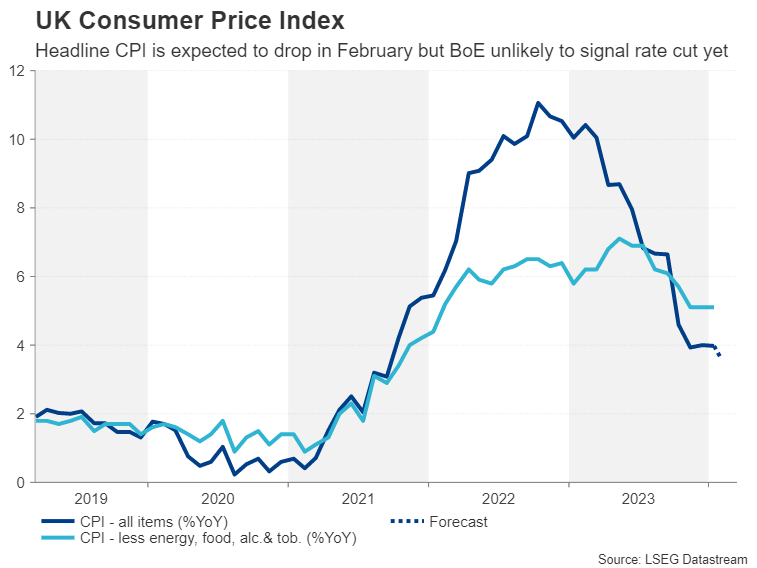

Bank of England Preview – We Still Pencil in the First Cut in June

- We expect the Bank of England (BoE) to keep the Bank Rate unchanged at 5.25% on 21 March, which is in line with consensus and current market pricing.

- Overall, we expect the MPC to repeat its previous communication relying on a data dependent approach.

- We expect a muted reaction in EUR/GBP with risks tilted to the topside.

We expect the Bank of England (BoE) to keep the Bank Rate unchanged at 5.25% on 21 March, which is in line with consensus and current market pricing. We expect the vote split to be 7-1-1, with the majority voting for an unchanged decision, Mann voting for a hike and Dhingra voting for a cut. Note, this meeting will include neither updated projections nor a press conference following the release of the statement.

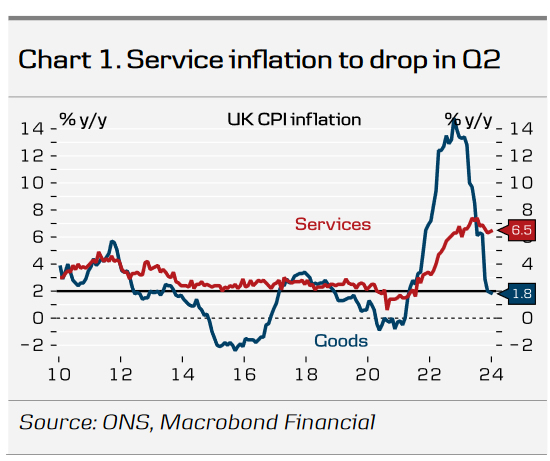

Overall, we expect the MPC to retain much of the same communication as from the February meeting, relying on a data dependent approach. Likewise, we think the BoE will be cautious in being too optimistic on the inflation outlook to prevent premature easing of financial conditions. Since the last monetary policy decision in February, data releases have overall pointed to more muted price and wage pressures. January inflation data surprised slightly to the downside and delivered a broad-based decline in inflationary momentum driven by both food and core inflation. While inflation for February is released the day before the meeting, we do not expect the print to change the outcome of this meeting. Large base effects from energy prices last spring are set to bring headline inflation back to 2% during the coming months. As previously flagged, we do not see inflation developing materially different in the UK compared to elsewhere, a call that is increasingly gaining momentum. Wage growth continues to edge lower supported by a gradually loosening of the labour market as highlighted by both the official labour market statistics and the KPMG/REC report on UK jobs. The growth backdrop remains a challenge for the MPC, with both composite and service PMIs remaining in expansionary territory pointing to a slight growth rebound in 2024 following a technical recession at the end of 2023.

Fiscal policy. The Chancellors budget included a range of easing measures including a 2pp cut to National Insurance. However, the measures are also largely set to boost the supply side, which minimises the potential upward pressure on inflation. Overall, we do not see the Spring Budget altering our long-held view of the MPC delivering its first cut in June.

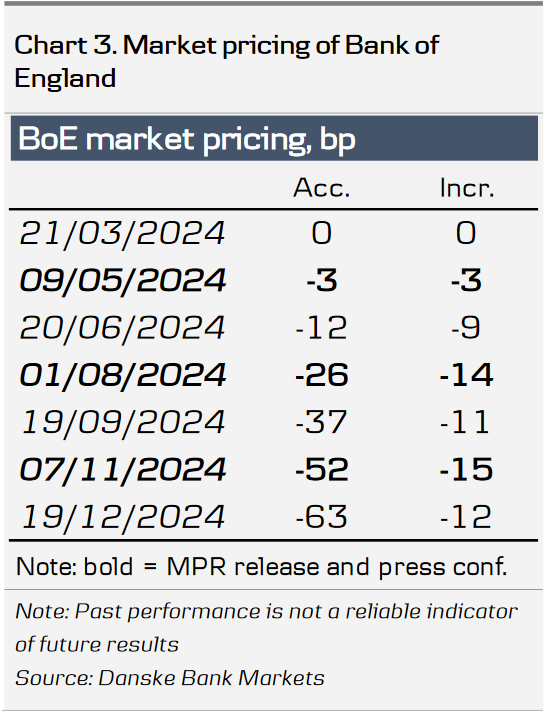

BoE call. We expect the BoE to prime markets for a rate cut at the May meeting which includes updated projections, delivering the first cut of 25bp in June. Importantly, we note that the BoE the past years traditionally has used small meetings to deliver important policy shifts: the first hike in December 2021, 50bp hike in June 2023 and unchanged decision in September 2023. We subsequently expect 25bp cuts in the following quarters, totalling 75bp of cuts for 2024. Markets are pricing 63bp for the remainder of the year with the first 25bp cut fully priced by August (chart 3).

FX. In our base case we expect a muted reaction in EUR/GBP with the MPC likely to give little away in terms of guidance. Overall, we see relative rates as a negative for GBP and see current levels as attractive levels to sell GBP. We forecast EUR/GBP towards 0.88 and stay short GBP/USD.

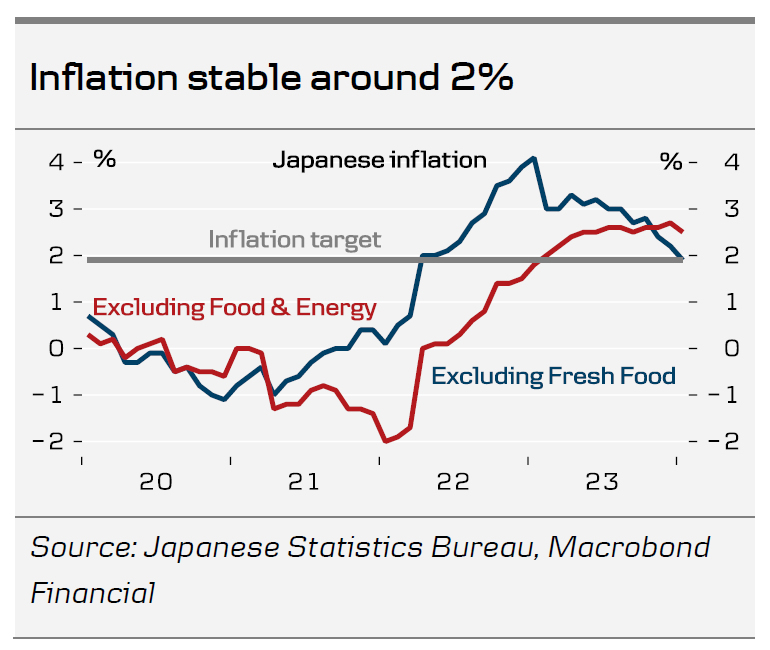

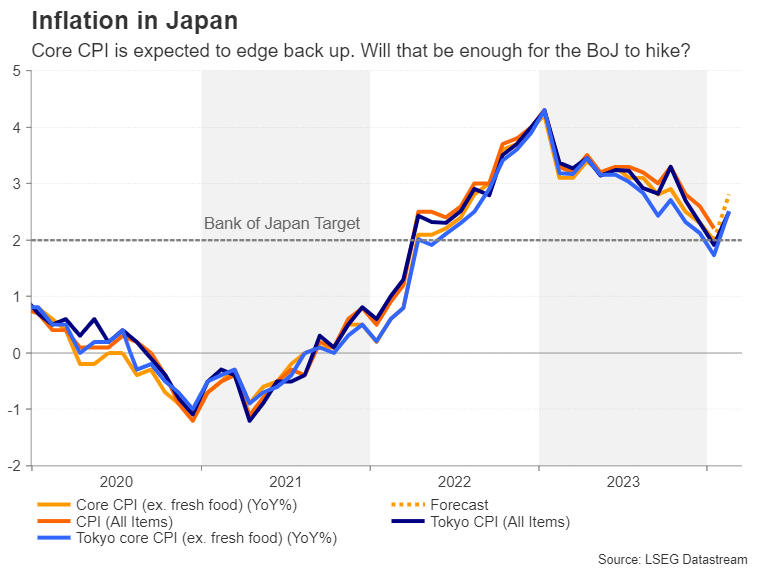

BoJ Hike in Sight – But No Reason to Rush

- The inflation target has been met for 22 consecutive months. Price pressures consistently rhymes with 2% annual inflation but the sustainability of that depends on wage increases.

- We think the BoJ is almost ready to hike the interest rate to zero and dismantle yield curve control. However, we see no reason to rush and expect them to stay on hold at the March meeting ending Tuesday, but it is admittedly a close call

- Whether the BoJ potentially exits NIRP in March or April does not alter our strategic bullish view on the JPY in 2024.

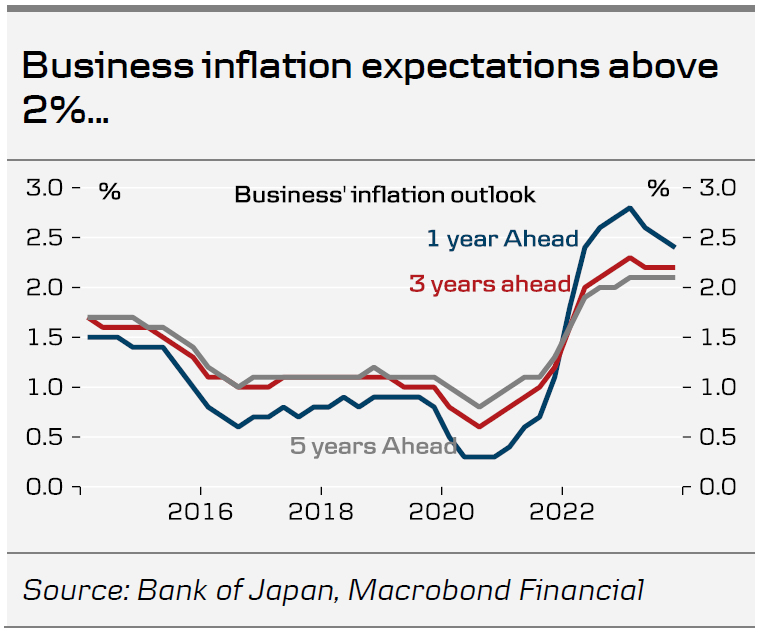

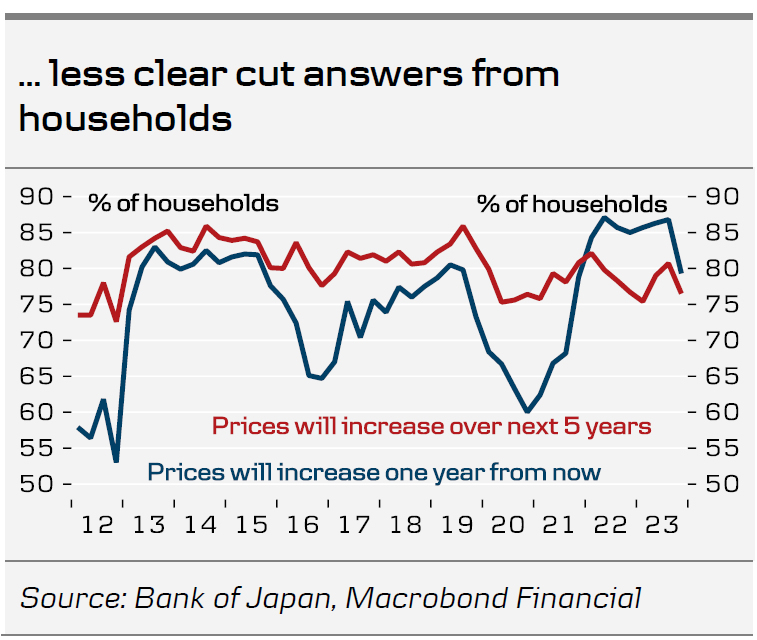

The Bank of Japan (BoJ) has met its 2% inflation target for 22 consecutive months. Their favourite inflation measure, CPI excl. fresh food, has declined steadily and stands at 2% now, as non-fresh food inflation has abated. Core price pressures rhyme with 2% inflation and have done so for a while. Businesses' inflation expectations have largely stabilised just above 2%. Households are more uncertain about the outlook for prices, though.

With this background, it could seem puzzling why Japan remains the only country in the world with a negative interest rates policy (NIRP). The reason is the absence of any significant wage-price spiral so far, which questions the longevity of Japanese inflation.

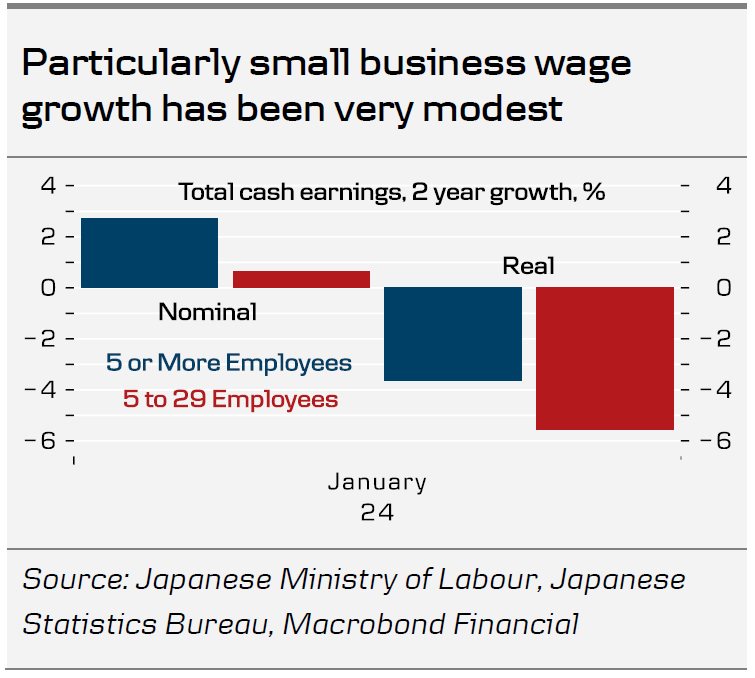

The first tally from this year's "spring wage offensive" showed that workers at major firms got a 5.28% pay increase, fairly close to the 5.85% they asked for. This is the key reason why we expect BoJ will be ready to hike its policy rate to zero in April. That said, it must remain a concern to the BoJ that wage growth is very weak among smaller businesses. Over the recent two years, wages have increased a modest 2.7% overall but only 0.7% in businesses with 5-29 employees. We will have to wait for at least the third wage tally, released in early April, to know much more about the 70% of Japanese workers who are employed in the SME segment. Only by early July, we will get the final tally and thus the full picture of the spill over to small businesses as well.

Financial markets have priced in close to 5 bps hike for the meeting ending on Tuesday, which implies a significant probability of a hike, although less than 50% as both a 10 and 20 bps hike could be in play. Thus, the March meeting is by all means live. We just do not think the BoJ has any reason to hurry. The window of opportunity to tighten policies has opened further this year as Fed cuts have been priced out of the market and a tightening move from the BoJ is now less in opposition to other global central banks than previously. It would make more sense to wait for incoming wage data ahead of the late-April meeting, which will also hold a new outlook for the economy, including the bank's first 2026 inflation forecast. By then, the quarterly Tankan report for Q1 will also be released, shedding more light on the state of the economy and businesses' price behaviour.

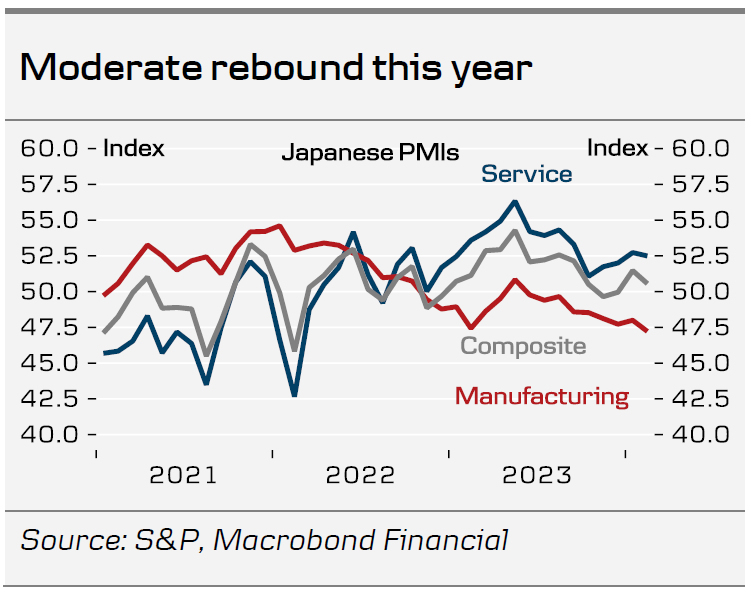

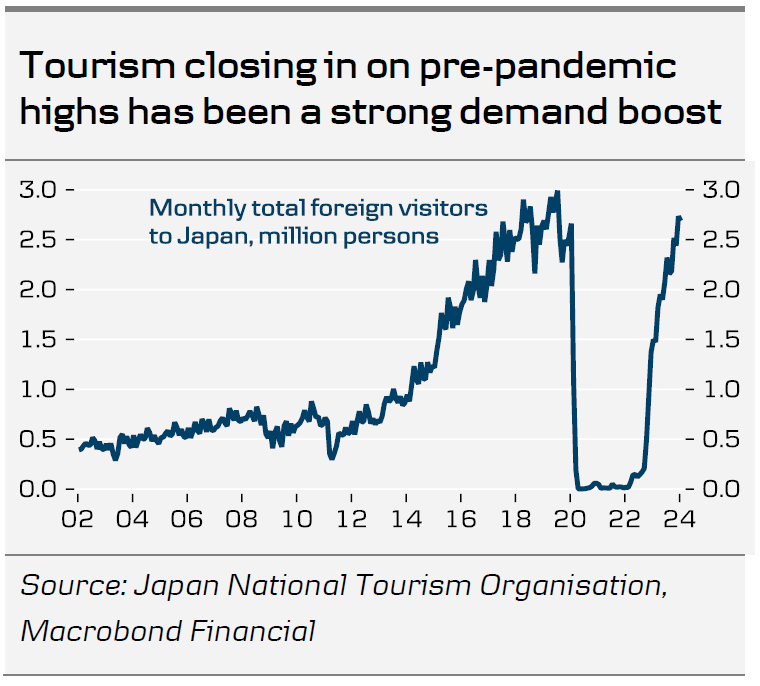

Another reason why the BoJ is perhaps in less of a hurry to exit NIRP is the recent slowdown in economic activity. Japan barely escaped technical recession in 2023H2 as Q4 growth was revised back above zero, by the slimmest possible margin, and indicators for Q1 have looked mixed. The manufacturing slowdown has worsened further, while the service sector looks quite robust, which should be seen in the light of the return of tourism. Japan has 2.7 Mio. visitors every month now, which is closing in on pre-pandemic levels. A 10 bps rate hike would be insignificant in itself, but hiking rates for the first time in 17 years and exiting NIRP will be a strong signal to markets. That is also why, the BoJ might decide to preserve the flexibility in the YCC for now, and perhaps hike rates by 20 bps. Our base case is a 10 bps hike and abolishment of YCC in April, though.

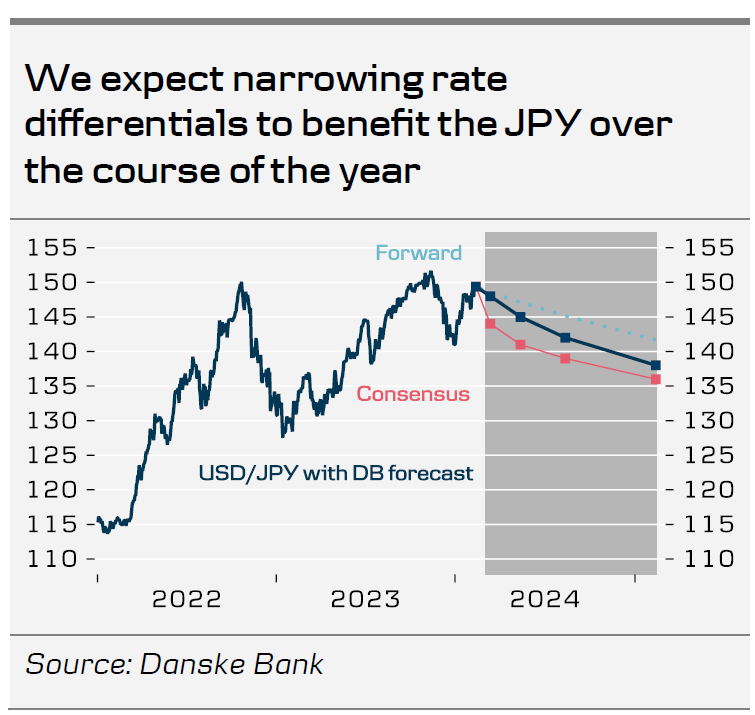

Timing of monetary policy normalization does not affect our positive stance on the JPY

Whether the BoJ potentially exits NIRP and YCC in March or April does not change our strategic bullish view on the JPY in 2024. Note that markets have seen several headlines suggesting a March BoJ move, but nothing from the more trustworthy Nikkei, which the central bank has previously used as a communication outlet.

However, near-term price action in the JPY would naturally be affected by the March meeting. Even if we are right and the BoJ does not make any changes to policy at the March meeting, it is unlikely that it will be a meeting without any notable near-term signals; for example, the BoJ could indicate an April move. We generally think that a potential hold at the March meeting would lean hawkish.

Focus will also be on whether the BoJ will offer any signals about additional changes to monetary policy during 2024. Given the uncertainty about both the domestic and global economy, we think the BoJ will refrain from delivering any pre-commitments to potential further hikes post-summer, and it will likely stay nimble and highlight uncertainties. Hence, we do not expect any major rate-hiking cycle from the BoJ during the year, and markets seem to agree as there is currently 26bp worth of rate hikes priced in for the whole year.

Therefore, the timing of the widely anticipated rate-cutting cycles from especially the Fed and the ECB could prove to be more pivotal for the JPY over the course of the year. Overall, we expect narrowing rate differentials and a global environment characterized by weaker growth and inflation impulses to favour the JPY in 2024. This has not been the case in Q1, but we still deem there are downside risks to global growth over the year. The biggest risk for our positive JPY stance is a re-acceleration in global inflation – especially in the US – which could prompt the Fed to delay rate cuts. Furthermore, a rise in energy prices would likely also leave the JPY vulnerable.

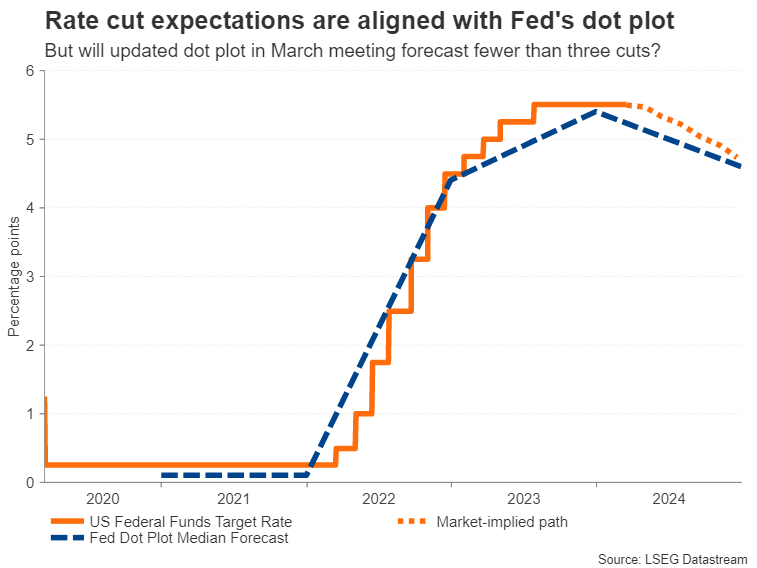

Fed preview – Taking Stock on QT and Data

- We do not expect the Fed to make monetary policy changes in its March meeting, as broadly anticipated by both markets and consensus.

- Besides the obvious focus on rate cut timing cues, we will keep an eye on the updated rate and economic projections as well as more detailed discussion on QT.

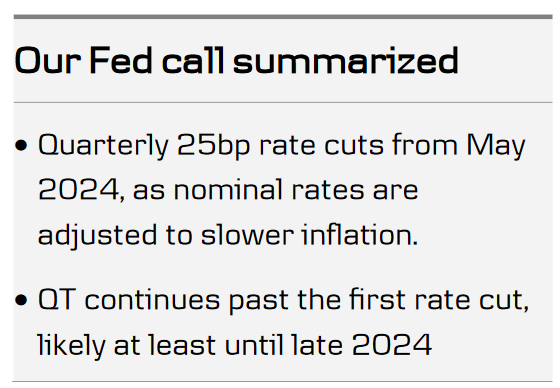

- We think the Fed will cut rates for the first time in May and start to gradually phase out QT only from September. 2024 GDP forecast is set to be revised higher, but we think 'dots' will still signal three rate cuts for this year as a whole.

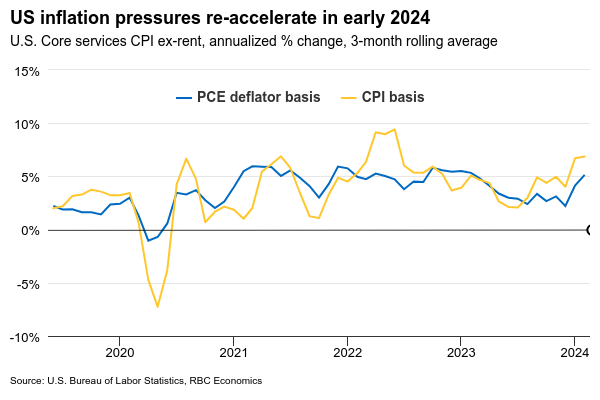

The Fed is set to balance upside surprises in recent inflation data with still cooling growth signals when it discusses monetary policy outlook for the rest of the year. Inflation data received after the January meeting has been concerning. Underlying services price pressures have remained elevated in early 2024, as we discussed in our Global Inflation Watch, 12 March, after this week's CPI release.

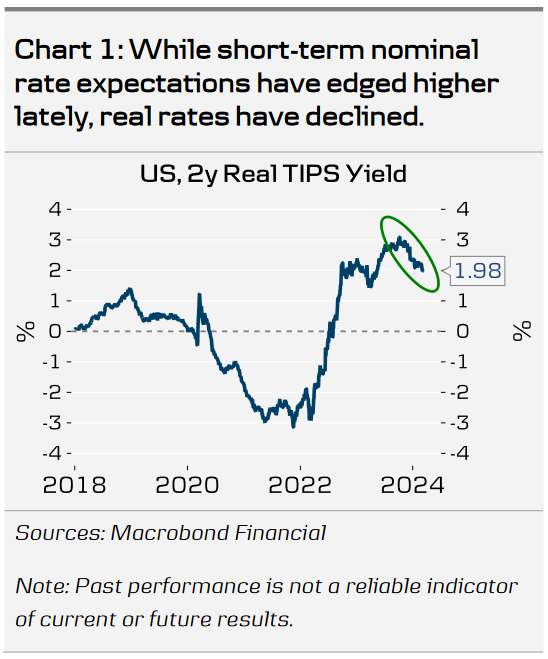

Inflation expectations have flashed warning signs as well. Even if longer-term expectations remain well anchored close to the Fed's target levels, short-term break-evens have risen over the past weeks. NY Fed's 3y survey-expectation also rose in February, albeit from a low level. While the current level of inflation expectations remains well below past years' highs, and is by no means concerning as such, rise in expected inflation pushes real interest rates lower, causing monetary policy to turn less restrictive (Chart 1).

Growth overhang from strong Q4 will likely lead to an upward revision of 2024 GDP forecast. But with recent weaker signals from ISM, hiring and retail sales, we think Powell is likely to reiterate that tight monetary policy is still expected to weigh on growth over the coming year. Inflation forecasts will likely only receive minor tweaks, and we think the widely followed median 'dot' will still point towards three rate cuts this year.

The Fed is also set to discuss the endgame for QT, but we do not expect concrete signals about phasing out the balance sheet reduction quite yet. Bank reserves stand above USD 3600bn today, or around USD 600bn higher than a year ago despite the ongoing QT. This is a result of money market funds withdrawing funds from the Fed's ON RRP facility and the Bank Term Funding Program (BTFP) introduced a year ago after the collapse of SVB. Over the next year, the remaining drawdown of ON RRP will add another USD 460bn to bank liquidity, while maturing BTFP will reduce it by USD 163bn. Treasury General Account (TGA) is currently very close to its target level (USD 768bn vs. target of USD 750bn), meaning it is unlikely to contribute to sharp swings in liquidity in 2024.

We believe the Fed will start to phase out QT by halving the pace of reductions only in September. Given the assumption above, bank liquidity would still hover roughly around $3000bn one year from today, which is most likely well above minimum ample level. In any case, we doubt the policymakers feel urgent need to communicate details about changing the pace of QT. Continuing balance sheet reduction will help maintain financial conditions restrictive even when the Fed will soon look to cut rates for the first time. We still look for total of three cuts this year, starting from May.

Markets: We expect a muted reaction

Long-end US rates will most likely react modestly to the outlined scenario for next week's

meeting, with a slight upside risk from QT communication. The pricing of rate cuts this

year has converged close to the 75bp, which we believe the dot plot will continue to signal,

and the great uncertainty still rests on whether growth and inflation data will continue

surprising to the upside in the coming months. Our 12M target for the 10-year yield remains

at 4.25%, thus close to the current level. The same goes for the USD; we do not expect a

major reaction. If anything, the USD could broadly gain strength in the G10 space if the

upside risk to long-end US yields materializes. Our EUR/USD forecast remains unchanged,

towards 1.04 on a 12M horizon.

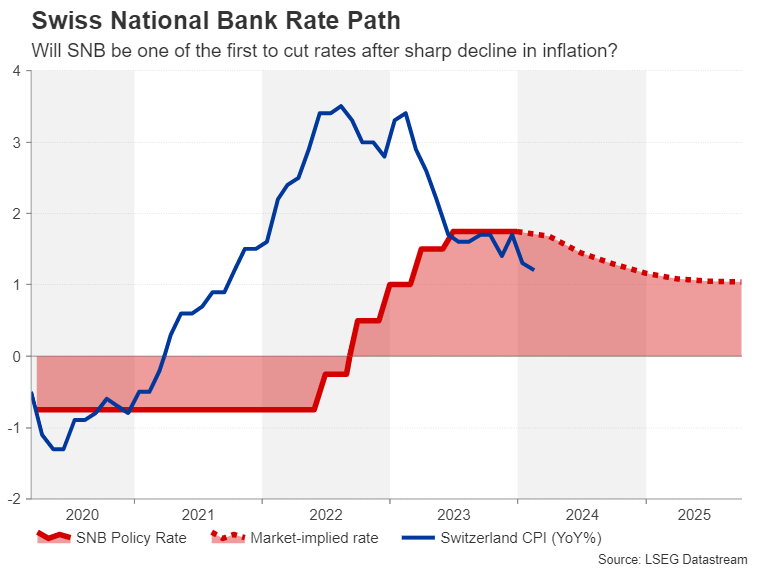

Weekly Focus – Will SNB Lead the Way in Cutting Cycle?

US inflation data was the centre of attention this week for financial markets, as price pressures remain elevated. Monthly core CPI inflation of 0.4% for the second consecutive month is too high for the Fed as strong wage growth pushes service prices higher at an annualised 7% pace. Markets zigzagged somewhat on the release but in the end the outcome was higher global yields. Producer prices and New York Fed inflation expectations added to the impression of a sustained inflation pressure in the US, with both increasing more than expected. It supported the move higher in yields and strengthened USD. On the dovish side, retail sales were weaker than expected, a challenging combination for the Fed.

With risk appetite improving through the week, prices for oil and industrial metals have also increased. Oil traded back above USD 85 per barrel in a week where an IEA report indicated an expected deficit in the oil market this year on the back of OPEC+ production cuts.

We have seen signs of global manufacturing bottoming out over the past couple of months. The data does not support any kind of boom, though, and we got some further weakening signs this week. Euro area industrial production was down 3.2% m/m in January, implying we will see no growth contribution from here until Q2 or Q3. At the same time, Asian export data, a leading indicator of global manufacturing, have been to the weak side.

In Japan, the biggest labour union federation released the first tally of this year's pay deals. This largely reflects big businesses which got 5.28%, close to what they asked for. The big question, however, remains whether this will rub sufficiently off on SMEs, where wage increases have been very modest so far. Elsewhere in Asia, the Chinese housing market continues to struggle as prices declined 1.4% y/y in February, the biggest annual drop in 13 months. The Peoples Bank of China kept rates unchanged as it likely awaits clearer signals of Fed easing.

Next week has a very busy central bank schedule. We expect no changes at the FOMC meeting but will look for clues about the timing of rate cuts and the end game for QT. We could also be in for an unusual couple of days with a Bank of Japan rate hike followed by an SNB cut two days later. While we expect the BoJ to hold the horses until April, we do expect a cut from the SNB. Both are close calls, though.

On the data front, we will start next week with key Chinese data on home and retail sales covering the first two months of the year. It will give us important information on the state of the housing crisis and the Chinese consumer. Thursday is PMI-day and it will be particularly interesting to see if the upward trend in global manufacturing PMIs continues after the recent signs of setback. In Japan we will look closely at the second wage tally at the end of the week.

Week Ahead – Five Central Banks: Who Will Hike, Who Will Not Cut?

- Fed meets on Wednesday with focus on new dot plot

- Will the Bank of Japan finally end negative rates on Tuesday?

- BoE and RBA to stick with patience, SNB might be in more of a rush to cut

- Flash PMIs plus inflation data in the UK, Japan and Canada will also be crucial

Fed decision: hoping for the best

The upcoming week will undoubtedly be one of the busiest, not to mention the most important, of the year for investors with five major central bank decisions on the way, along with a plethora of economic data. The highlight, however, looks set to be the Federal Reserve’s decision on Wednesday, as expectations of looser monetary policy in the world’s largest economy have been fuelling the incredible stock market rally of late.

Rate cut bets have swung sharply this year amid some mixed signals on the strength of the Fed’s two mandates: employment and price stability. If the overall picture could be summed up, it is that both the labour market and inflation are cooling down, but only gradually. The latest nonfarm payrolls report and CPI figures only underscored this trend.

For the Fed, although it has so far avoided the trap of pre-committing to a rate cut, the easing tendency is evident. Chair Powell told lawmakers last week that they’re “not far” from being confident that inflation is moving sustainably towards 2%. Powell’s readiness to cut is likely the reason why markets react more to soft data than upbeat ones.

However, the Fed’s projected rate cuts are based on the expectation that inflation remains in a downward trajectory despite the slowdown in the disinflation process. That trend has now started to look questionable as the latest CPI and PPI releases suggest that inflation may be flatlining before reaching the Fed’s 2% goal. This turns the spotlight on the updated FOMC dot plot, which will be the focal point of the March meeting.

There’s a possibility the median projection for 2024 will be revised from three 25-basis-point rate cuts to just two. But even if the median projection is left unrevised, if more participants see the Fed funds rate either at 4.75% or higher, that would also reflect a hawkish tilt. Yet, Powell might still attempt to strike a balanced tone in his press briefing in the event that FOMC members predict only two rate cuts, and this could limit any selloffs in stocks and other risk assets.

For the US dollar, however, the upside risks are greater than the downside risks heading into the meeting following its somewhat muted response to the recent hot price data. Traders will additionally be keeping an eye on some housing stats (building permits and housing starts on Tuesday, and existing home sales on Friday), the Philly Fed manufacturing gauge on Thursday as well as S&P Global’s flash PMI readings for March.

BoJ: time to hike?

The long-suffering yen enjoyed a much-needed lift in March amid renewed speculation that the Bank of Japan is close to ending its negative rates policy. Early indications from the spring wage negotiations point to much bigger pay deals this year than in 2023. Governor Ueda couldn’t have made it clearer that any exit from negative rates is conditional on a sustained acceleration in wage growth.

Some board members already see this criteria being met so may vote for a rate increase at Tuesday’s policy decision. However, having been patient this long, it’s unlikely that Ueda will support such a move before there’s a more complete picture about the outcome of the 2024 wage negotiations, and so April remains a more realistic timeframe for a big policy shift.

Traders seem to concur as they’ve priced in a 40% probability for a 10-bps hike in March and a 70% probability for April.

Another reason why the BoJ may prefer to wait is that the consumer price index for February is released days later on Friday. Although the annual CPI rate in Tokyo spiked higher in February, suggesting a similar move in the nationwide figures, the Bank may not want to jump the gun.

For the yen, however, the March meeting could still spur some significant gains even if no rate hike is announced. Policymakers will likely make significant tweaks to the language to possibly hint that they are close to achieving 2% inflation sustainably. They may even announce some changes to their asset purchases by ending the program for buying exchange-traded funds.

Hence, the yen could attract buyers until the April meeting. What happens after that, though, will depend on whether the BoJ will also abandon its yield curve control policy and whether a rate hike will be a one-off.

Aside from the CPI numbers, machinery orders will be watched in Japan on Monday, as well as the flash PMIs on Thursday.

UK CPI data might overshadow BoE meeting

The pound is the only major currency that is currently able to stand tall against the US dollar in terms of year-to-date performance. Much of that is to do with the expectation that the Bank of England will not be able to cut rates before August, whereas the Fed and the European Central Bank will likely cut in June. More to the point, the latest market pricing puts UK interest rates the highest in the G7 by year end, amid stickier inflation and wage pressures than in other economies.

Unsurprisingly, Bank of England officials have been less dovish than their global counterparts when it comes to rate cut talk, although they have hinted that policy might need to become less restrictive later in the year. Fortunately for the Monetary Policy Committee, there’s a raft of incoming UK data next week that should help members make up their minds.

The CPI report for February is due on Wednesday, the flash PMIs will follow on Thursday, and retail sales will wrap up the week on Friday. The inflation numbers will come just in time before the MPC votes later on Wednesday.

Both headline and core CPI were unchanged in January so policymakers will be hoping to see inflation head back down again in February. Another disappointment in CPI staying sticky, combined with a not-so-gloomy PMI survey would probably prompt the BoE to maintain its comparatively hawkish stance, boosting the pound.

However, any downside surprises in the CPI figures, especially on the back of the somewhat weaker-than-expected employment report could trigger a bit of correction in cable following its near 2% rally at the start of March.

As for Thursday’s decision, there is no press briefing nor new forecasts at the March meeting, so investors will be looking for subtle changes to the statement.

SNB might lay groundwork for a cut

The Swiss National Bank also meets on Thursday, and it too is not expected to announce any changes in borrowing costs. The Alpine nation boasts an inflation rate of just 1.2% so out of all the central banks, the SNB has the most reason to begin slashing rates imminently.

A 25-basis-point rate cut is more than fully priced in for June and this might explain why the Swiss franc is close to overtaking the yen as the worst performing currency this year. If policymakers signal that a rate cut is likely at the June meeting, the franc could extend its losses.

RBA: from a hawkish hold to a dovish hold

Kicking things off, however, is the Reserve Bank of Australia, which meets on Tuesday. The RBA has been on hold after last hiking rates back in November. Policymakers considered hiking again at both of their subsequent meetings but decided against it. At the March meeting, the decision will likely be less contentious as there’s been some further progress in bringing down inflation since the last gathering, particularly in the underlying measures.

But would that be enough for the RBA to drop its tightening bias? There’s been a notable hawkish shift in RBA policy under Governor Michelle Bullock, but in her last comments when she testified in Parliament in February, she sounded slightly more optimistic about inflation coming down. A more neutral tone on Tuesday is therefore probable and this may weigh on the local dollar.

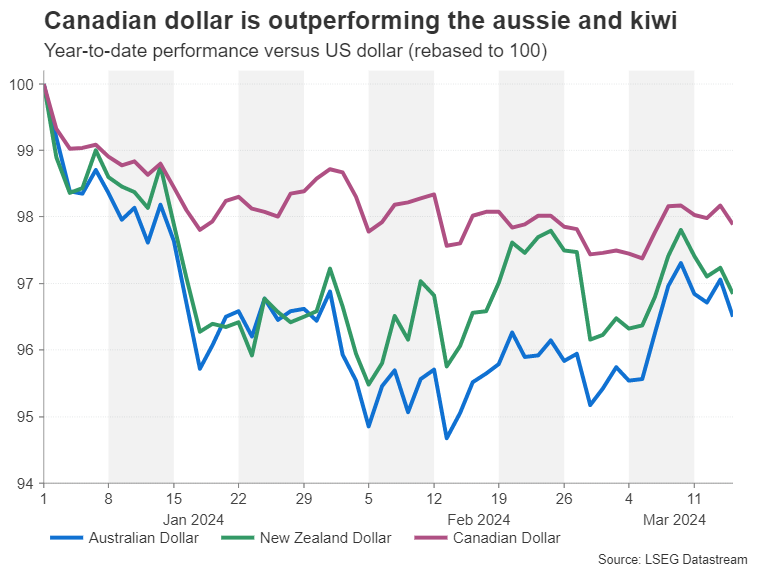

Plenty of drivers for the commodity dollars

The aussie has shed more than 3.5% so far in 2024 despite investors expecting fewer cuts by the RBA this year than other major central banks. Worries about Australia’s biggest trading partner – China – are partly to blame for this underperformance.

Aussie traders will be monitoring industrial output and retail sales numbers due in China on Monday for fresh clues on the speed of the Chinese recovery, while domestic employment figures on Thursday will also be vital.

Staying in the region, New Zealand will publish quarterly GDP estimates on Thursday, which may boost the kiwi if they show the economy returned to growth in the final quarter of 2023.

The Canadian dollar has fared somewhat better than the other commodity linked currencies, as like in the US, inflation in Canada is taking longer than anticipated to reach the 2% target. Investors have pushed out the timing of when they expect the Bank of Canada to start cutting rates, with a move not seen before the July meeting, followed by just one more cut after that.

However, headline CPI did fall back below 3.0% in January and a further decline in February might lead to rate cut bets being ratcheted up. The latest CPI release is on Tuesday, with retail sales for January coming up on Friday.

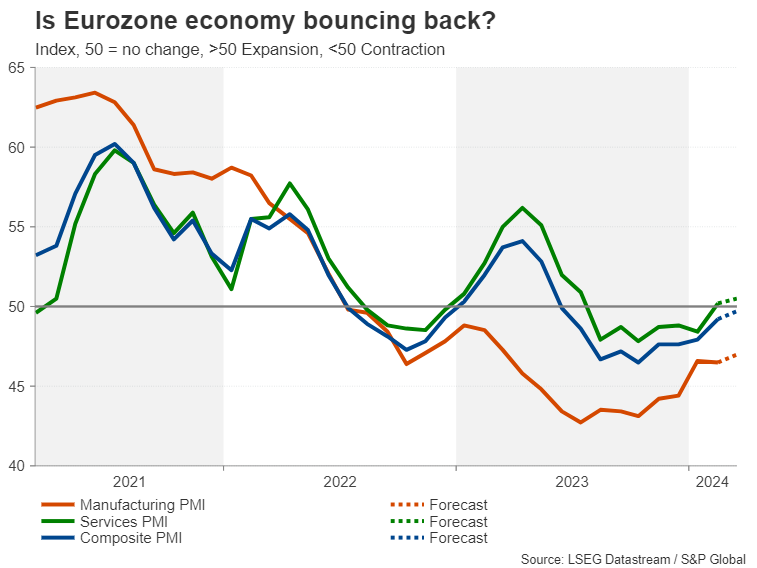

Euro eyes PMI bounce for further gains

Finally, the euro will not miss out on some attention as Thursday’s flash PMI estimates for the Eurozone could sway ECB rate cut bets. A battle is raging between the hawks and doves as to not only how soon the central bank should switch to an easing cycle, but by how much rates should be cut.

With inflationary pressures fading fast and an economy stuck in the doldrums, the ECB could yet be more aggressive than the Fed in slashing rates. However, whilst the inflation picture remains encouraging, there are signs that economic growth has started to regain some momentum. The services PMI climbed above the 50 neutral mark in February for the first time since July and is expected to improve further in March. The manufacturing sector remains in contractionary territory but there are green shoots there too.

After flirting with the $1.09 level during the past week, the euro could rise further if the PMIs impress. Ahead of the PMI survey, the final CPI readings are due on Monday, while German business gauges, the ZEW and Ifo indices on Tuesday and Friday, respectively, will shed some more light on the bloc’s largest but currently the weakest economy.

RBA Could Maintain a Degree of Hawkishness

- RBA will meet on Tuesday, cash rate is expected to be kept unchanged

- Market wants a dovish show, but RBA could remain somewhat hawkish

- Aussie could benefit against the US dollar from a hawkish gathering

- Decision to be announced at 03.30 GMT, press conference one hour later

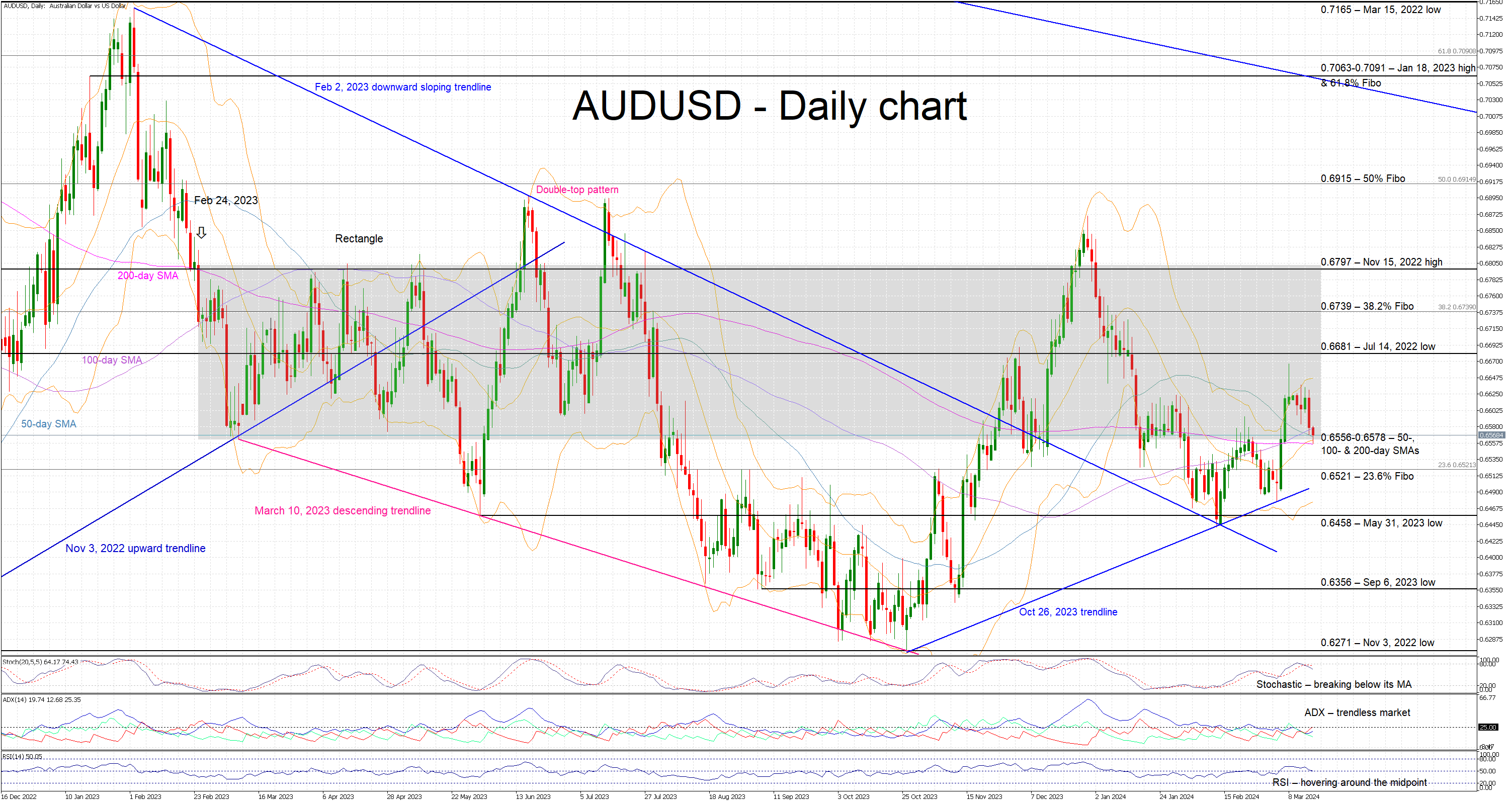

The Reserve Bank of Australia meets on Tuesday

The RBA kicks off next week’s busy central bank meetings’ schedule with its Tuesday gathering. Contrary to both the Fed and ECB being on the cusp of cutting interest rates, RBA members considered hiking rates in early February before agreeing to keep the official cash rate unchanged at 4.35%. Could this meeting bring a change in RBA’s rates outlook?

At the February 6 gathering, the main message was that progress has been made on the inflation front but the Bank needs to be confident that that this move will sustainably continue towards the target range. This gist of this message sounds familiar as it matches what we recently heard from both Fed Chairman Powell, at his double Congress testimony, and ECB President Lagarde, at the recent ECB press conference. Therefore, the key question is whether enough progress has been made since early February.

No real progress has been recorded in inflation

The monthly CPI for January came in at 3.4%, matching December’s increase, the TD-MI inflation gauge dropped to 4% in February, the lowest print since March 2022, but consumer inflation expectations over the 12 months remained at 4.5% for a third consecutive month. The wage price index for the fourth quarter of 2023 printed a tad lower but that was probably already factored in RBA’s calculations. As made evident, no major progress has been recorded on the inflation front.

In the meantime, there are conflicting messages about the growth outlook. The manufacturing sector remains under pressure, especially as China continues to experience significant growth issues despite the repeated support measures announced there, while the services sector continues to expand. This is positive from a growth perspective, but the elevated services sector inflation remains one of the main reasons why inflation is proving stickier than anticipated. The preliminary manufacturing and services PMI surveys for March will be published on Wednesday and could shed more light on the underlying economic momentum. If one adds the fact that fiscal policy is expected to loosen up during 2024, then the RBA has the option to sit back and monitor developments elsewhere.

The market accepts that the possibility of a rate move on Tuesday remains very low, with the first 25bps rate cut fully priced in by September 2024, while dismissing any chance of a rate hike. That doesn't mean that the RBA cannot maintain a degree of hawkishness at Tuesday’s meeting but being overly hawkish is probably difficult considering the rates outlook by the Fed.

Aussie gains depend on Wednesday’s Fed meeting

The aussie enjoyed a strong period against the US dollar with the pair returning inside the rectangle that has been in place since February 2023. There is a busy events’ calendar coming up with the convergence of the simple moving averages opening the door to an imminent strong move in this pair.

RBA’s meeting could boost the aussie/dollar pair higher with the July 14, 2022 low at 0.6681 possibly being the initial target, but any gains could prove short-lived as Wednesday’s Fed meeting will probably determine the short-term outlook for most dollar crosses. On the flip side, a dovish RBA gathering could open the door to a move towards the October 26, 2023 trendline, with this possible correction picking up speed if the Fed proves more hawkish than currently foreseen.

Will Canada’s CPI Data Rescue the Wounded Loonie?

- BoC sounds less dovish than expected

- Investors pencil in a first 25bps cut in July

- Canada’s CPI numbers could affect market expectations

- The data is scheduled for Tuesday at 12:30 GMT

Will the BoC cut interest rates after the Fed?

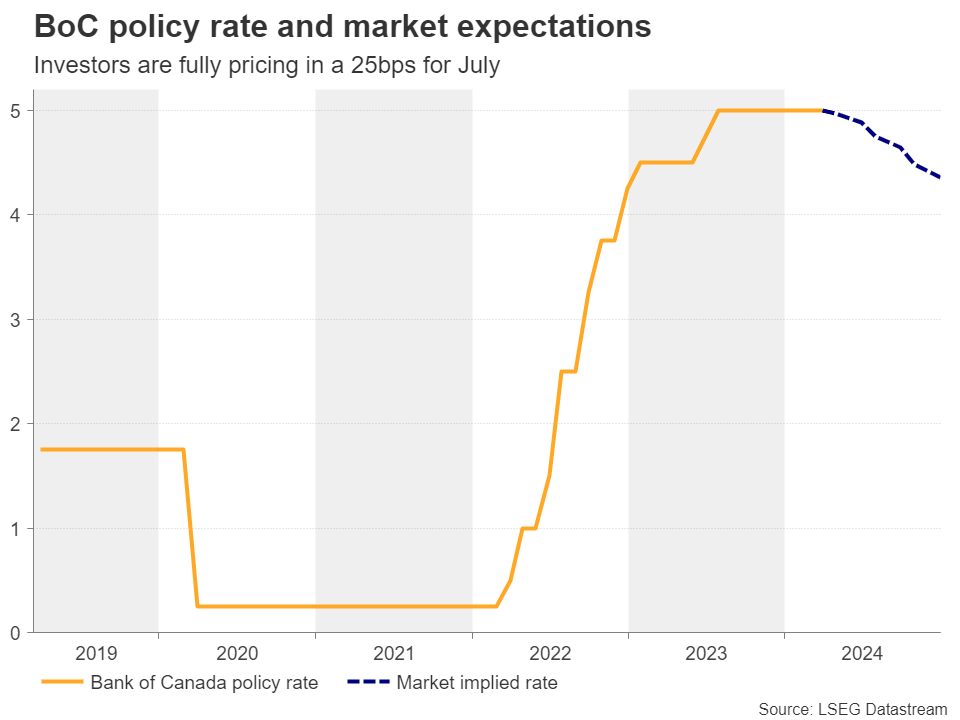

At its latest gathering on March 6, the Bank of Canada (BoC) decided to keep interest rates unchanged at 5% as expected, but the statement accompanying the decision and Governor Tiff Macklem himself signaled concerns about high underlying price pressures, with the Governor adding that more progress is needed before they start considering rate cuts.

This, combined with data releases after the decision, convinced investors to push back their rate cut bets. Although they are assigning a 20% chance for a quarter-reduction at the upcoming meeting on April 10, they are fully pricing in such a move for July, while the total number of basis points worth of rate reductions for the whole year stands at 65, interestingly less than the 75bps currently projected for the Fed.

Jobs report corroborate BoC’s less dovish stance

Just two days after the last meeting, the employment report for February revealed that the unemployment rate ticked up to 5.8% from 5.7%. but that the economy added more jobs than in January, confounding expectations of a slowdown. Coming on top of the better-than-expected GDP data for Q4, the jobs report added to speculation that the BoC could wait for a while longer before lowering borrowing costs.

Will inflation prove to be stickier than expected?

With all that in mind, loonie traders are now likely to shift their attention to Tuesday’s CPI numbers for February as they try to get a clearer picture of when policymakers are likely to hit the cut button. According to the Ivey PMI for the month, prices eased in February, suggesting that after January’s slowdown, at least the core CPI metrics may continue to drift south. That said, with the y/y change in oil prices turning positive lately, the headline CPI rate may prove to be stickier, as was the case with US inflation.

Although analysts at the National Bank of Canada (NBC) said recently that the central bank will soon need to cut interest rates due to weak private domestic demand and flat private-sector employment, a potential rebound in the headline CPI rate back above 3%, which is the upper bound of the BoC’s 1-3% target range, could add to speculation that officials could remain sidelined for a while longer.

Can the loonie stage a strong comeback?

The Canadian dollar could benefit if inflation proves to be hotter than expected, but calling a long-lasting uptrend against its neighboring US dollar would still be premature. The Fed will announce its monetary policy decision on Wednesday, and an upwardly revised dot-plot could add fresh fuel to the greenback’s engines.

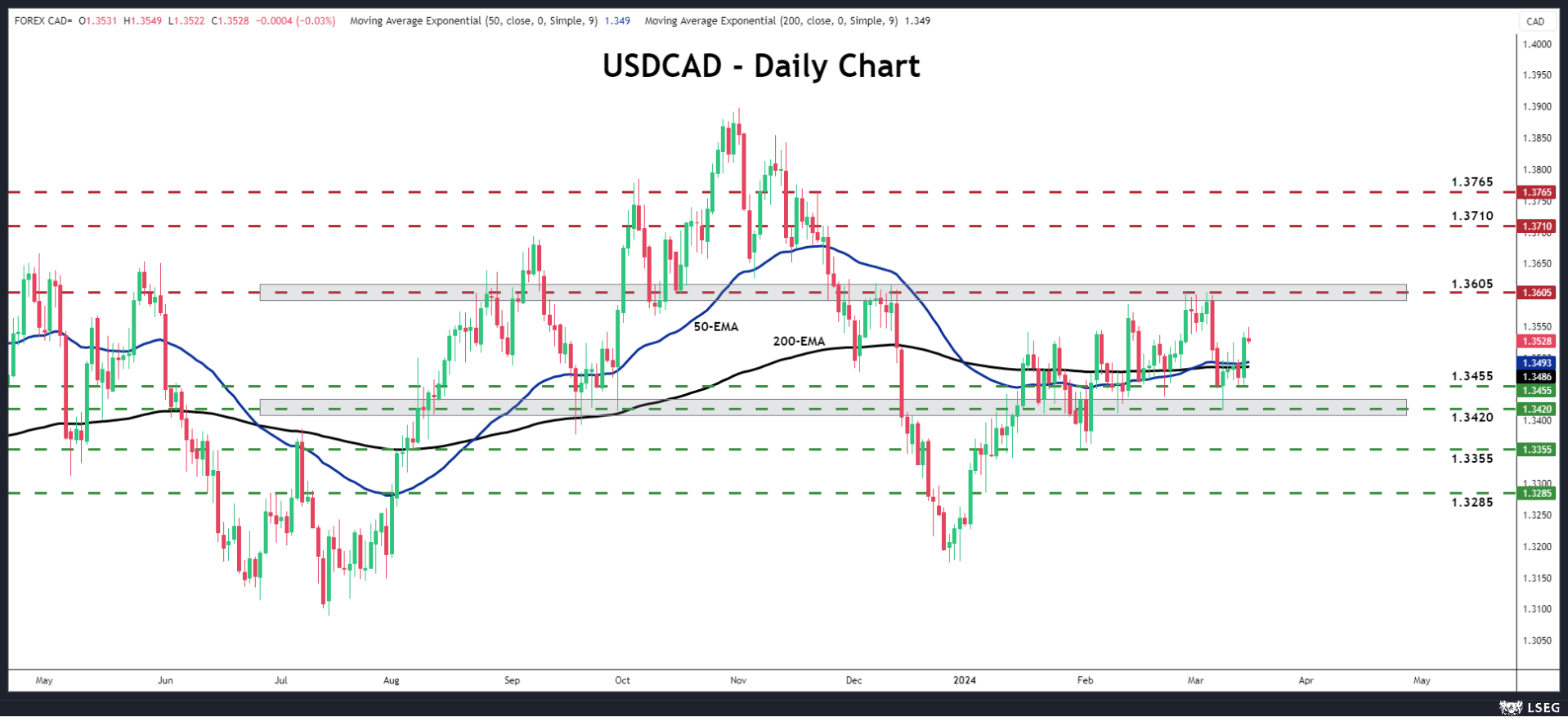

From a technical standpoint, dollar/loonie has been in an uptrend since December 27. However, despite the latest leg north, the overall picture suggests that the trend has been losing steam lately. Hotter than expected inflation could result in a pullback but the bulls may be tempted to buy again from near the 1.3455 zone and aim for the 1.3605 area which offered resistance between February 28 and March 5.

For the outlook of this pair to change to bearish, a decisive dip below 1.3420 may be needed. Such a move may encourage the sellers to push the action down to the low of January 31, at around 1.3355.

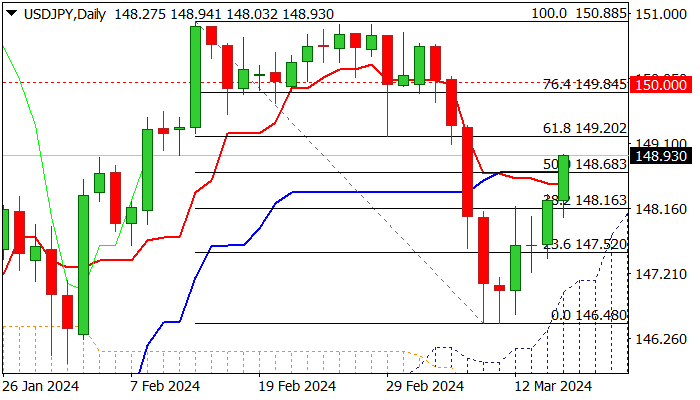

USD/JPY: Stands at the Front Foot Ahead of BoJ and Fed Policy Meetings

USDJPY has so far retraced over 50% of the recent 150.88/146.48 drop, in steep recovery that extends into fifth straight day.

Fresh strength emerged from profit-taking after the pair was sharply down on growing speculations that the BoJ would start tightening its monetary policy this month, with significant interest rate gap between two central banks, working in favor of dollar.

Near-term action was also supported by rising and thickening daily cloud which contained pullback and continued to underpin recovery, though technical studies are still mixed and lack firm direction signal.

All eyes are on next week’s policy meetings of BoJ and Fed, with Bank of Japan widely expected to end its ultra-low policy phase, while the US central bank is likely to remain on hold, but markets will be looking for fresh signals about the timing of the first rate cut.

Res: 149.20; 149.40; 150.00; 150.88.

Sup: 148.68; 148.16; 147.87; 147.11.