Sample Category Title

AUD/USD Weekly Report

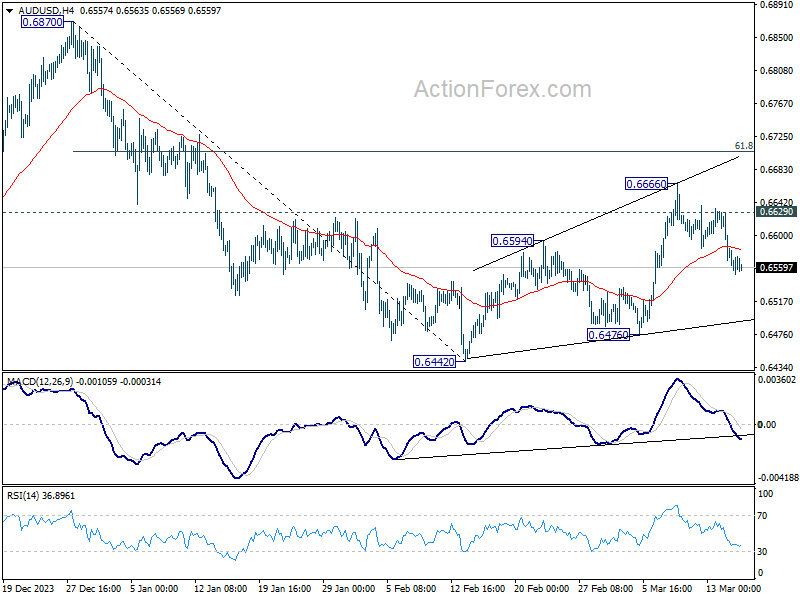

AUD/USD's fall from 0.6666 extended last week and confirm short term topping. Initial bias remains on the downside for 0.6476 support first. Break there will argue that decline from 0.6870 is ready to resume through 0.6442 low. On the upside, break of 0.6629 minor resistance will turn bias back to the upside to extend the rebound from 0.6442 instead.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which might still be in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.

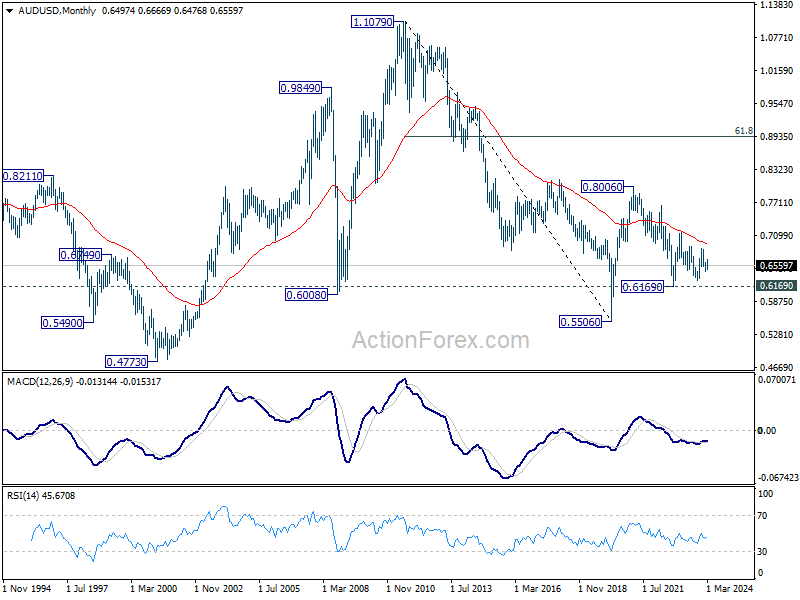

In the long term picture, the down trend from 1.1079 (2011 high) should have completed at 0.5506 (2020 low) already. It's unsure yet whether price actions from 0.5506 are developing into a corrective pattern, or trend reversal. But in either case, fall from 0.8006 is seen the second leg of the pattern. Hence, in case of deeper decline, strong support should emerge above 0.5506 to bring reversal.

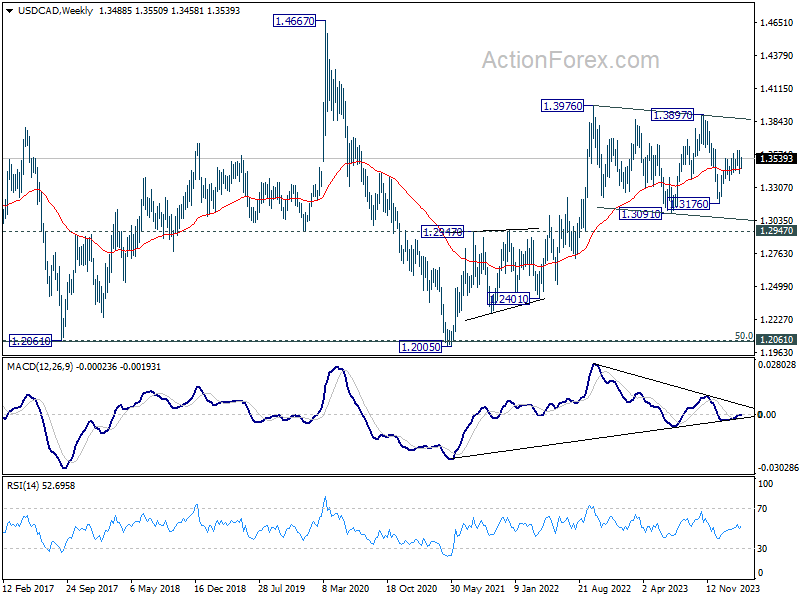

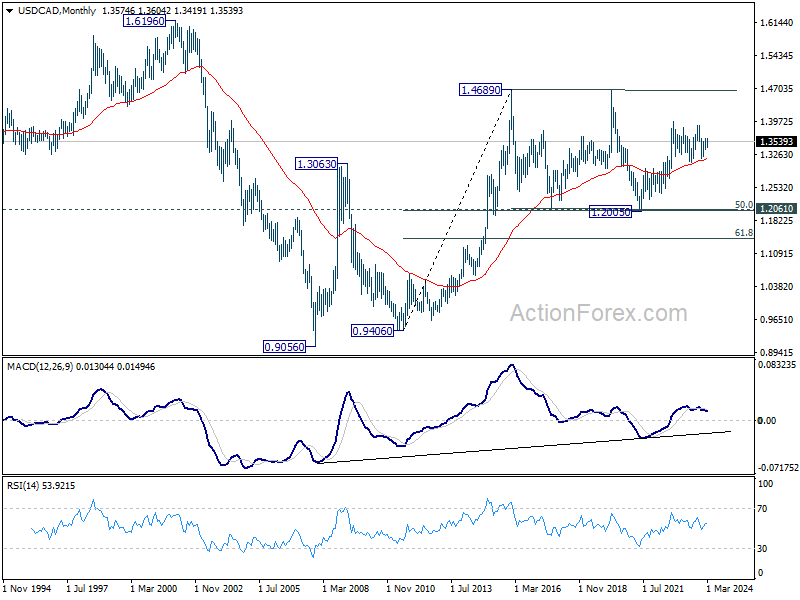

USD/CAD Weekly Outlook

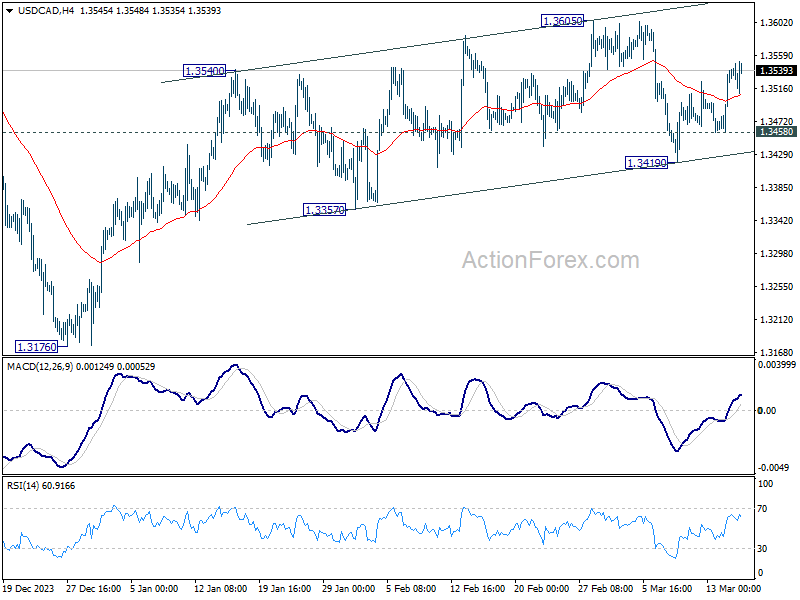

USD/CAD's rebound from 1.3419 extended higher last week and the development suggests that corrective pullback from 1.3605 has completed. Initial bias remains on the upside this week for retesting 1.3605 resistance first. Decisive break there will resume whole rally from 1.3176. On the downside, however, break of 1.3458 minor support will turn bias back to the downside or 1.3419 instead.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 at a later stage.

In the longer term picture, price actions from 1.4689 (2016 high) are seen as a consolidation pattern, which might have completed at 1.2005. That is, up trend from 0.9506 (2007 low) is expected to resume at a later stage. This will remain the favored case as long as 1.2947 resistance turned support holds.

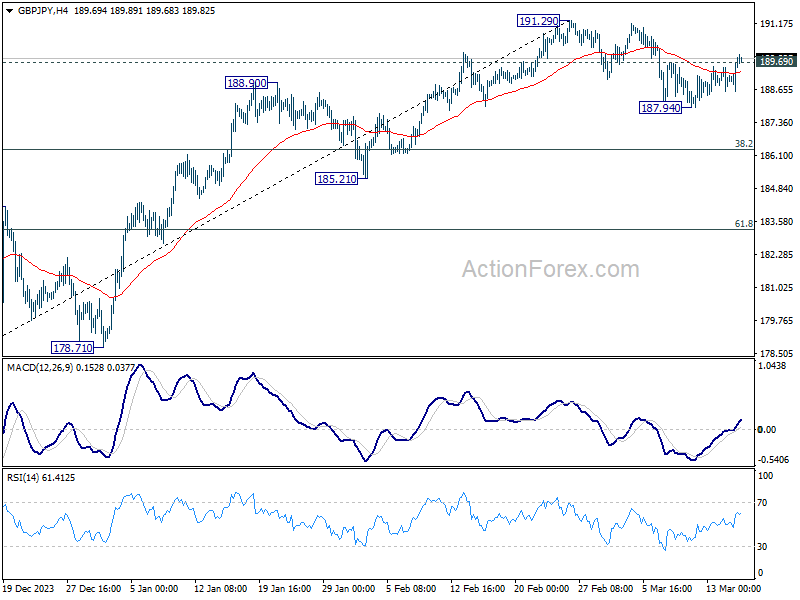

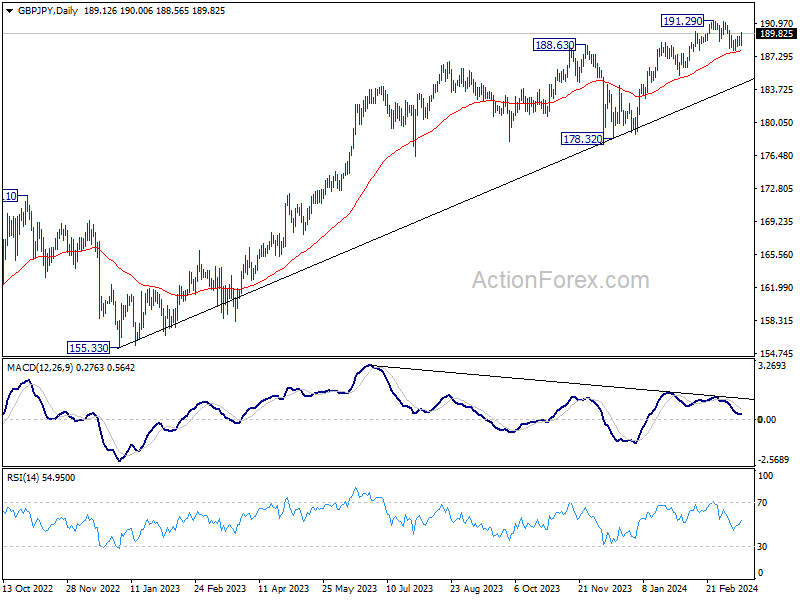

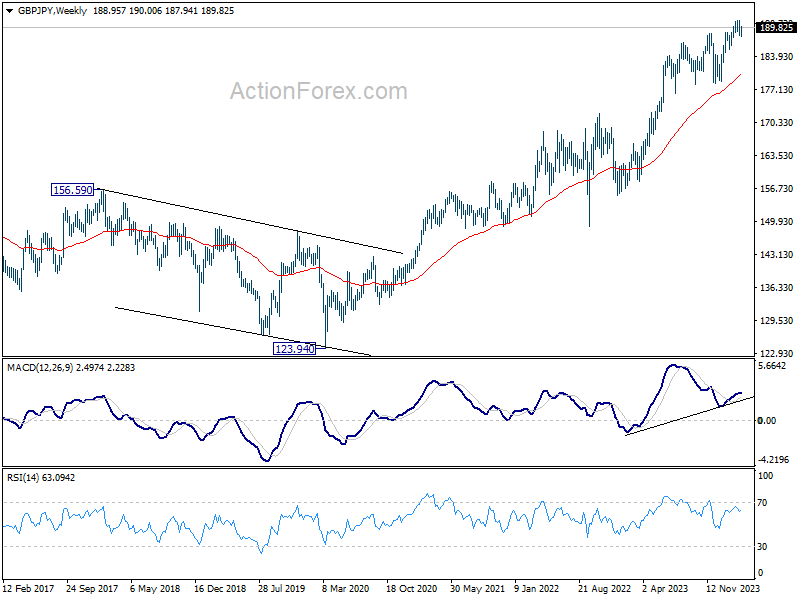

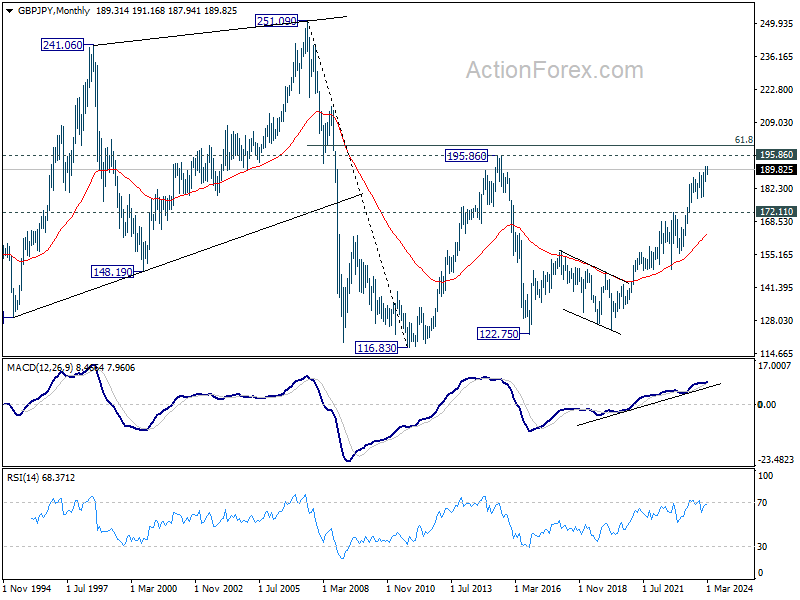

GBP/JPY Weekly Outlook

GBP/JPY's break of 189.69 minor resistance suggests that correction from 191.29 has completed at 187.94 already. Initial bias is back on the upside for retesting 191.29 high first. Decisive break there will bring larger up trend resumption. On the downside, break of 187.94 will resume the correction to 38.2% retracement of 178.32 to 191.29 at 186.33.

In the bigger picture, up trend from 123.94 (2020 low) is in progress. Medium term outlook will stay bullish as long as 178.32 support holds. Next target is 195.86 long term resistance (2015 high).

In the longer term picture, rise from 122.75 (2016 low) is seen as the third leg of the pattern from 116.83 (2011 low). Further rally will remain in favor as long as 172.11 resistance turned support holds. Break of 195.86 (2015 high) is possible. But strong resistance could be seen from 61.8% retracement of 251.09 (2007 high) to 116.83 at 199.80 to limit upside, at least on first attempt.

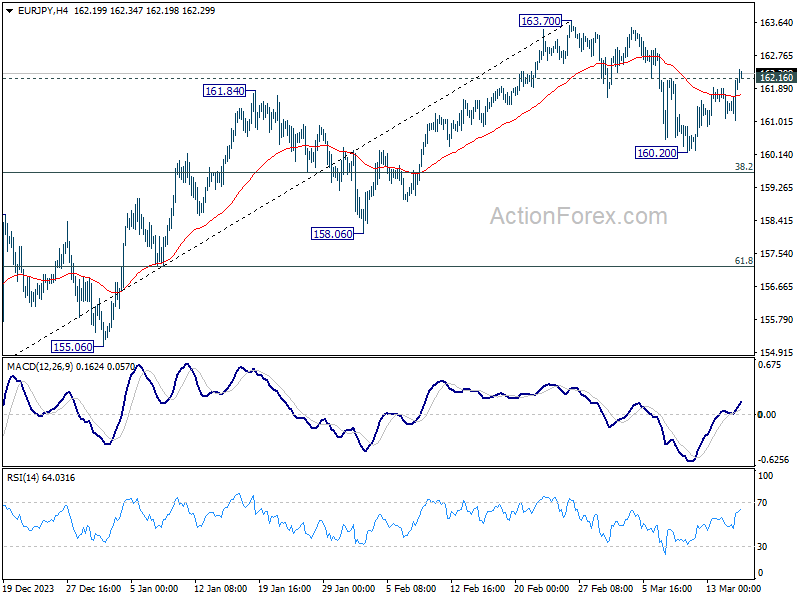

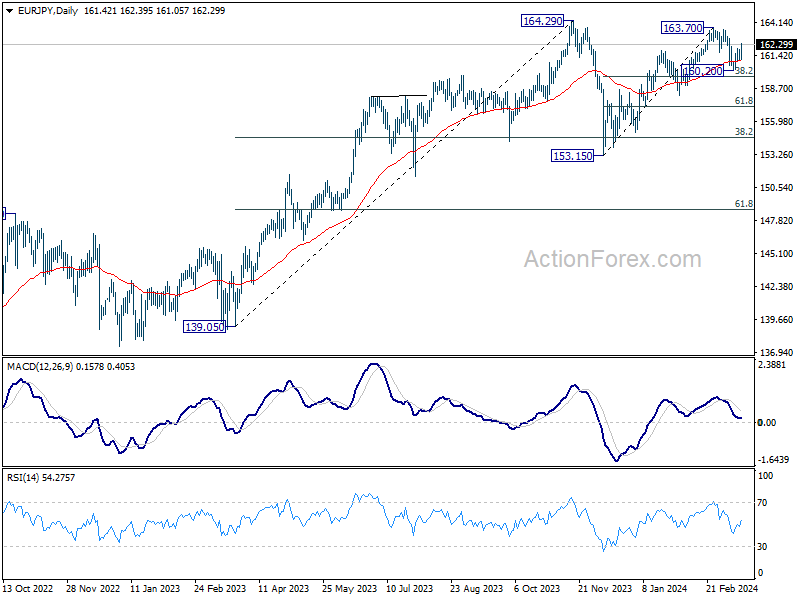

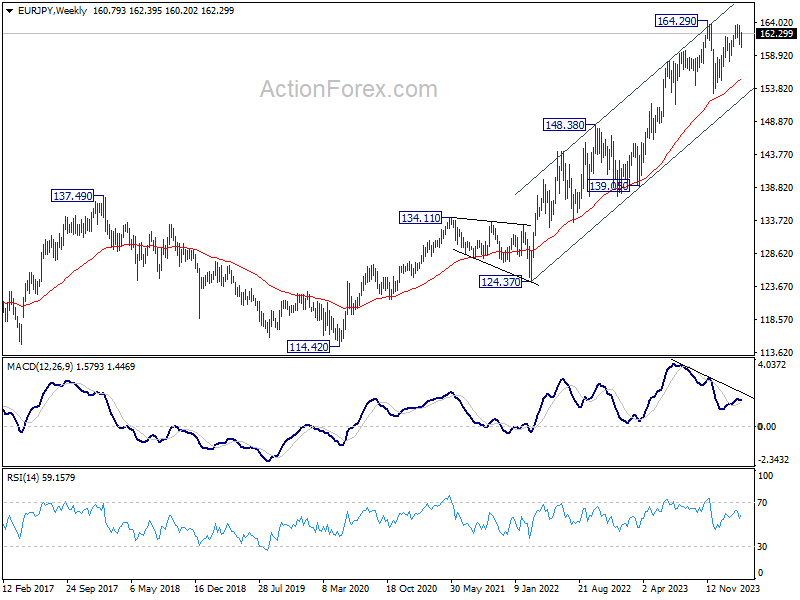

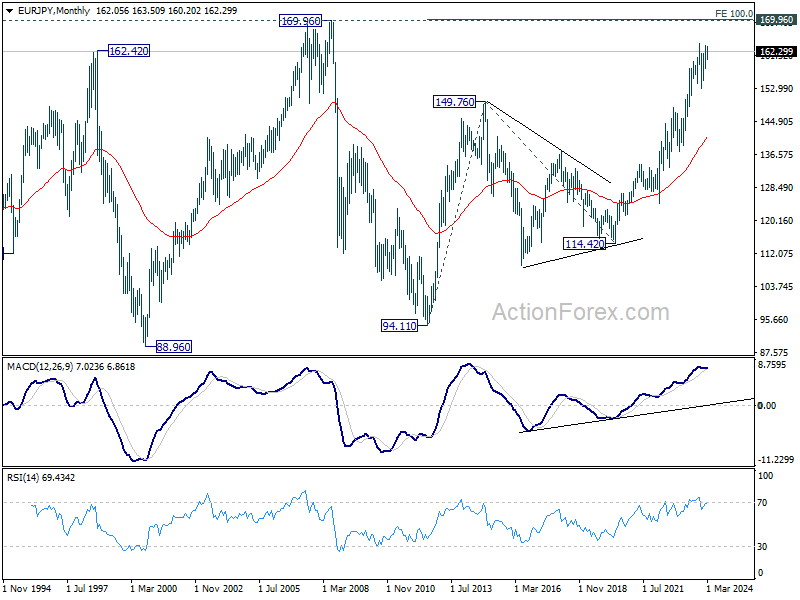

EUR/JPY Weekly Outlook

EUR/JPY's break of 162.16 minor resistance last week suggests that correction from 163.70 has completed at 160.20. Initial bias is back on the upside for retesting 163.70 resistance. Decisive break there will resume larger rally from 153.15 for 164.29 high. In case of another fall, downside should be contained by 38.2% retracement of 153.15 to 163.70 at 159.66 to bring rebound.

In the bigger picture, price actions from 164.29 medium term top are seen as a correction to rise from 139.05 which could still be extending. As long as 148.38 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) is expected to resume through 164.29 at a later stage. Next target would be 169.96 (2008 high).

In the long term picture, rise from 114.42 (2020 low) is seen as the third leg of the whole up trend from 94.11 (2012 low). Next target is 100% projection of 94.11 to 149.76 from 114.42 at 170.07 which is close to 169.96 (2008 high). This will remain the favored case as long as 148.38 resistance turned support holds.

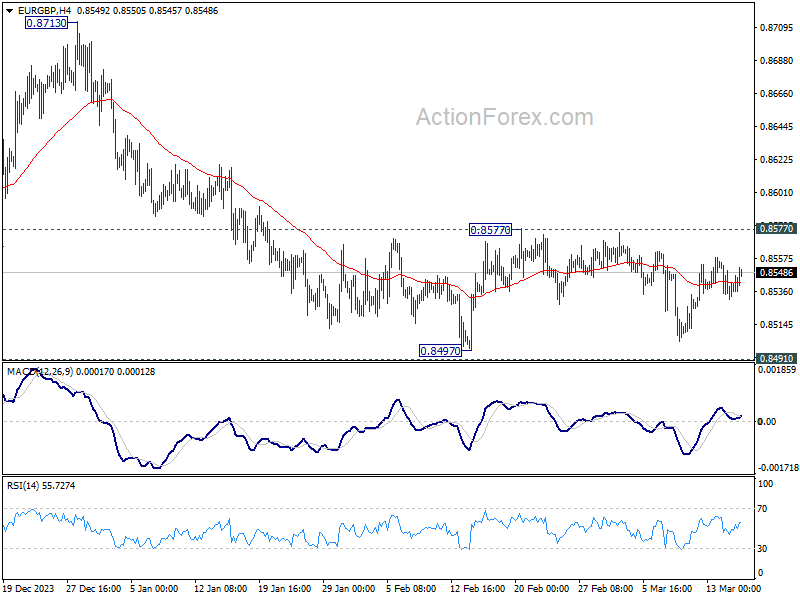

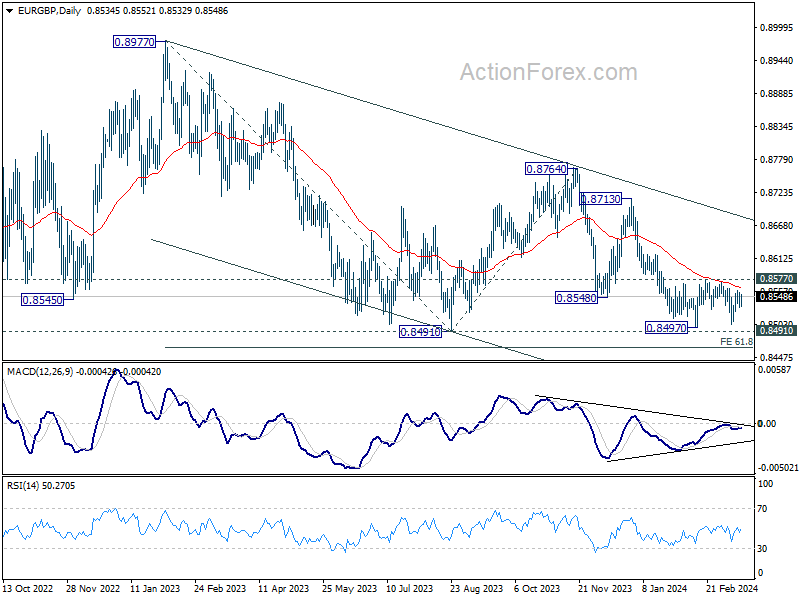

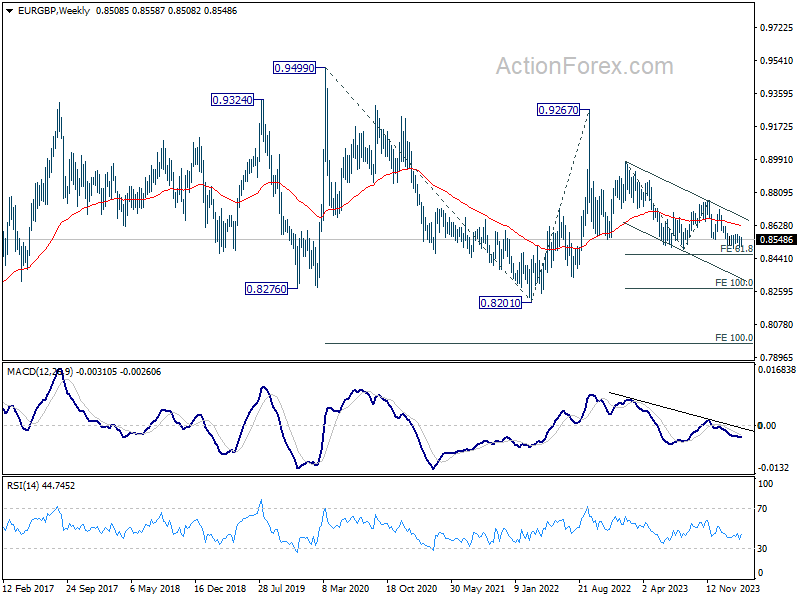

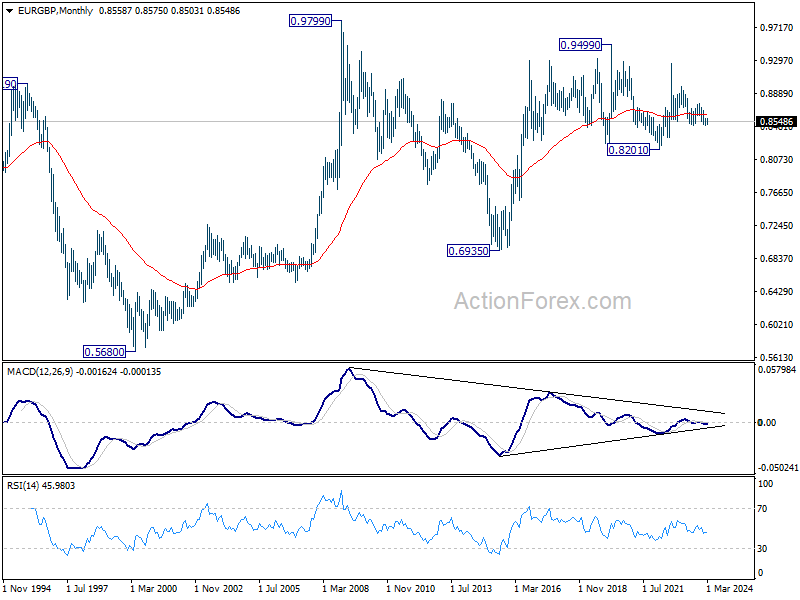

EUR/GBP Weekly Outlook

EUR/GBP was still bounded in range of 0.8497/8577 last week and outlook is unchanged. Initial bias remains neutral this week first. On the downside decisive break of 0.8491/7 support zone will confirm larger down trend resumption and target 0.8464 projection level first. However, firm break of 0.8577 will turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8713 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Fall from 0.9267 is the third leg of the pattern from 0.9499. Break of 0.8201 (2022 low) will target 100% projection of 0.9499 to 0.8201 from 0.9267 at 0.7969.

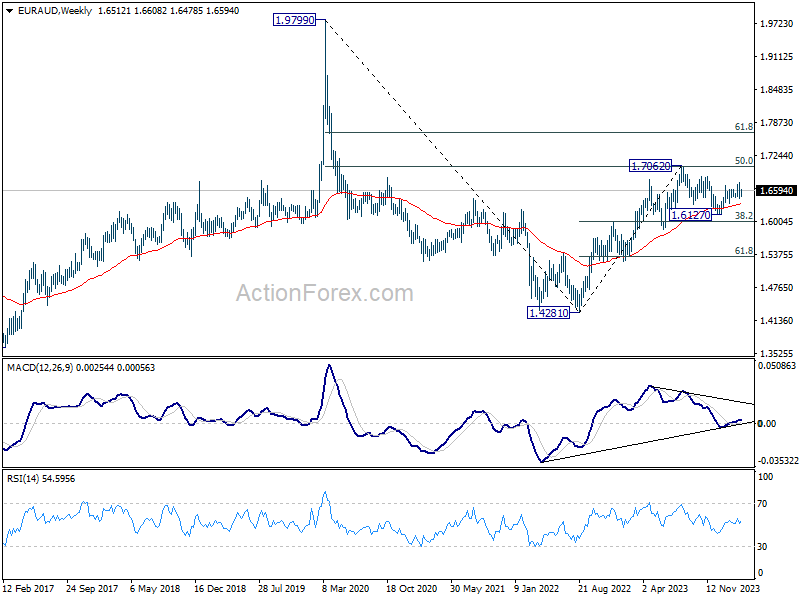

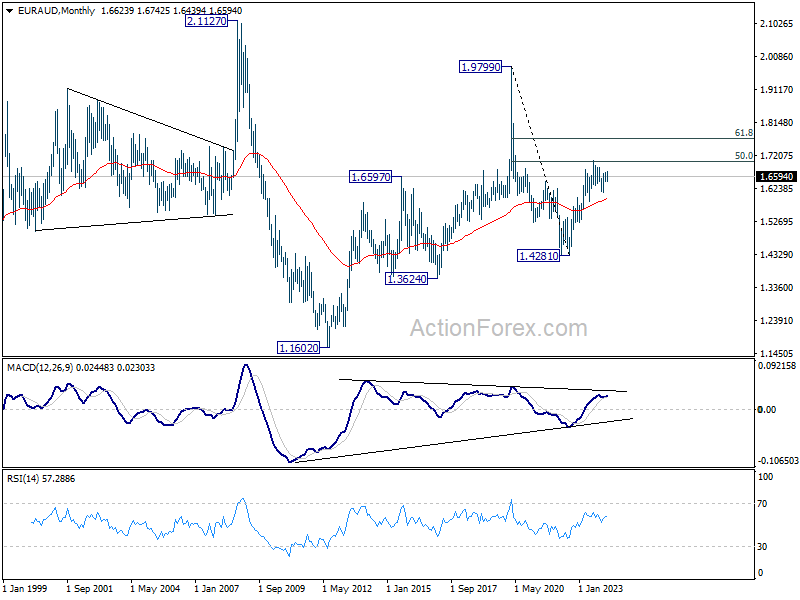

EUR/AUD Weekly Outlook

EUR/AUD recovered after drawing support from 1.6450, but upside is still capped by 1.6606 minor resistance. Initial bias stays neutral this week first. On the upside, firm break of 1.6606 will retain near term bullishness and bring retest of 1.6742. Break there will resume larger rise from 1.6127. On the downside, however, decisive break of 1.6450 support will argue that whole rebound from 1.6127 has completed with three waves up to 1.6742 already. Near term outlook will be turned bearish for 1.6127 again.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

In the longer term picture, price actions from 1.9799 (2020 high) are seen as a long term decline at the same scale as the rise from 1.1602 (2012 low). Rebound from 1.4281 is seen as the second leg. As long as 55 M EMA (now at 1.5932) holds, this second leg could still extend higher. However, sustained trading below 55 M EMA will open up the bearish case for extending the decline through 1.4281 low.

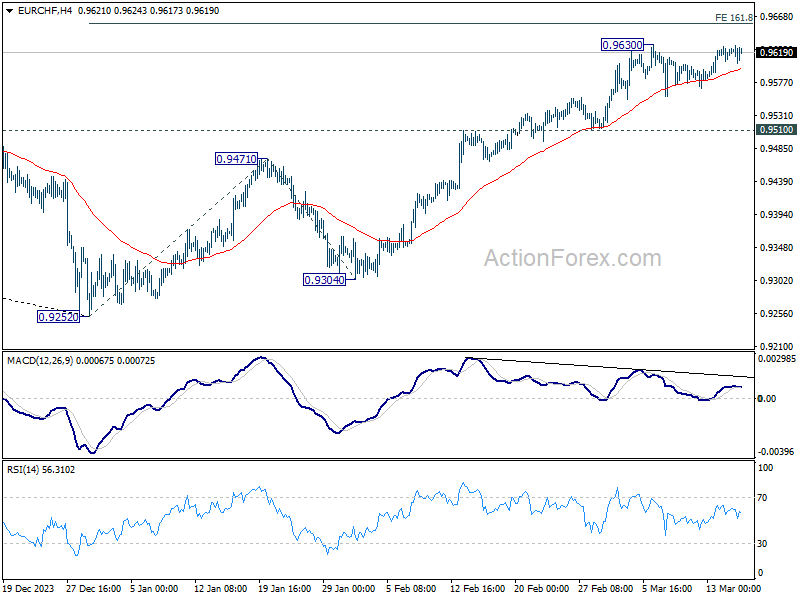

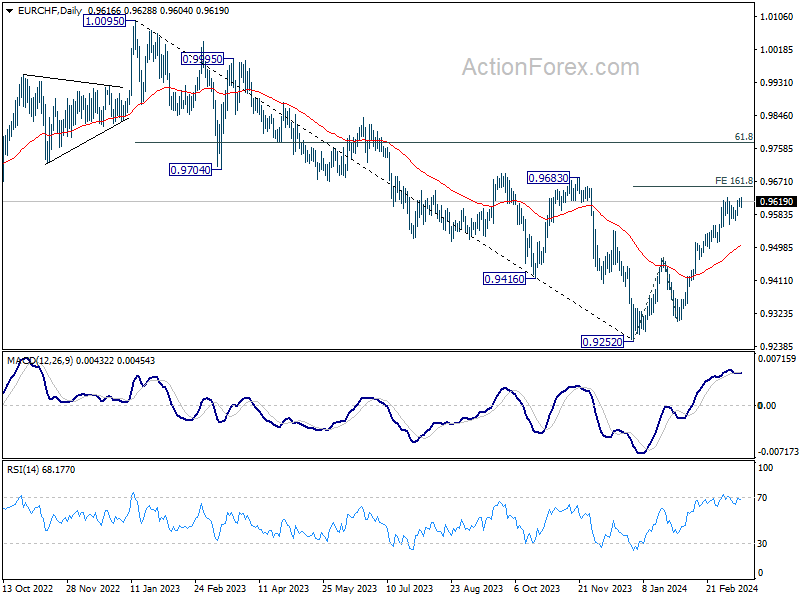

EUR/CHF Weekly Outlook

EUR/CHF stayed in consolidation below 0.9630 last week and outlook is unchanged. Initial bias remains neutral this week first. Another dip cannot be ruled out, but outlook will stay bullish as long as 0.9510 support holds. On the upside, break of 0.9630 will resume the rise from 0.9252 and target 161.8% projection of 0.9252 to 0.9471 from 0.9304 at 0.9658 next. However, considering bearish divergence condition in 4H MACD, firm break of 0.9510 will turn bias back to the downside for deeper fall.

In the bigger picture, as long as 0.9683 resistance holds, rebound from 0.9252 are seen as a corrective move only. Larger down trend is expected to resume through 0.9252 after the correction completes. However, firm break of 0.9683 and sustained trading above 55 W EMA (now at 0.9620) will argue that 0.9252 is already a medium term bottom. Stronger rise would then be seen 61.8% retracement of 1.0095 to 0.9252 at 0.9773 and above.

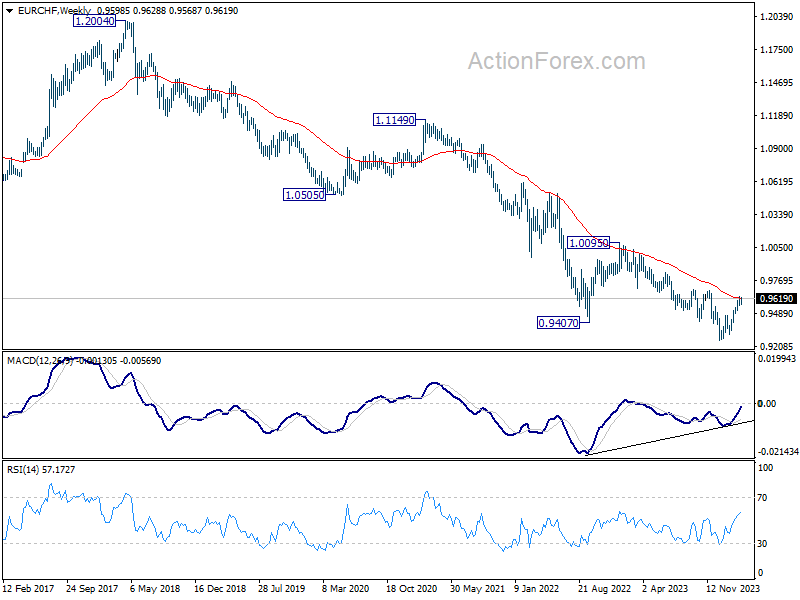

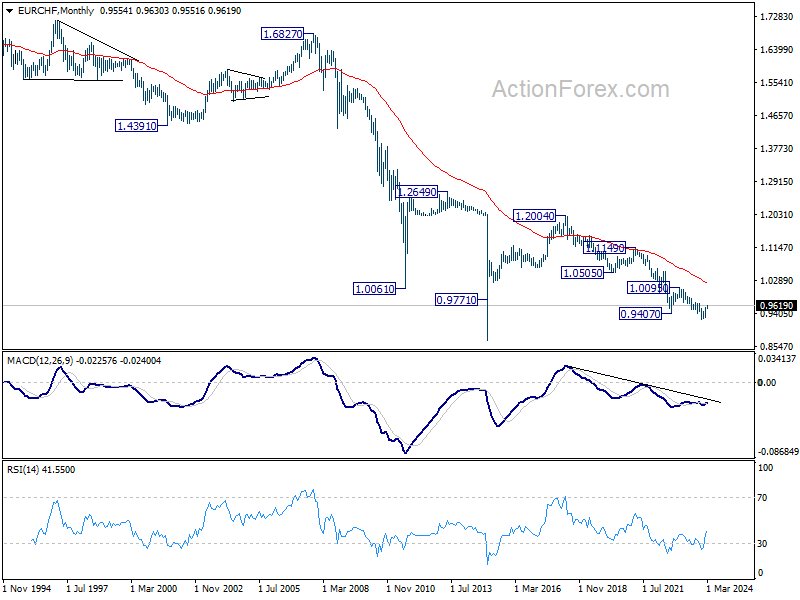

In the long term picture, fall from 1.2004 (2018 high) is part of the multi-decade down trend. Firm break of 1.0095 resistance is needed to be the first sign of long term bottoming. Otherwise, outlook will remain bearish.

Summary 3/18 – 3/22

Monday, Mar 18, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 21:30 | NZD | Business NZ PSI Feb | 52.1 | |

| 23:50 | JPY | Machinery Orders M/M Jan | -0.70% | 2.70% |

| 02:00 | CNY | Industrial Production Y/Y Feb | 5.30% | 6.80% |

| 02:00 | CNY | Retail Sales Y/Y Feb | 5.60% | 7.40% |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Feb | 3.20% | 3.00% |

| 10:00 | EUR | Eurozone Trade Balance (EUR) Jan | 14.2B | 13.0B |

| 10:00 | EUR | Eurozone CPI Y/Y Feb F | 2.60% | 2.60% |

| 10:00 | EUR | Eurozone CPI Core Y/Y Feb F | 3.10% | 3.10% |

| 12:30 | CAD | Raw Material Price Index Feb | 1.20% | |

| 12:30 | CAD | Industrial Product Price M/M Feb | -0.10% | |

| 14:00 | USD | NAHB Housing Index Mar | 48 | 48 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 21:30 | NZD | Business NZ PSI Feb | |

| Forecast: | Previous: 52.1 | ||

| 23:50 | JPY | Machinery Orders M/M Jan | |

| Forecast: -0.70% | Previous: 2.70% | ||

| 02:00 | CNY | Industrial Production Y/Y Feb | |

| Forecast: 5.30% | Previous: 6.80% | ||

| 02:00 | CNY | Retail Sales Y/Y Feb | |

| Forecast: 5.60% | Previous: 7.40% | ||

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Feb | |

| Forecast: 3.20% | Previous: 3.00% | ||

| 10:00 | EUR | Eurozone Trade Balance (EUR) Jan | |

| Forecast: 14.2B | Previous: 13.0B | ||

| 10:00 | EUR | Eurozone CPI Y/Y Feb F | |

| Forecast: 2.60% | Previous: 2.60% | ||

| 10:00 | EUR | Eurozone CPI Core Y/Y Feb F | |

| Forecast: 3.10% | Previous: 3.10% | ||

| 12:30 | CAD | Raw Material Price Index Feb | |

| Forecast: | Previous: 1.20% | ||

| 12:30 | CAD | Industrial Product Price M/M Feb | |

| Forecast: | Previous: -0.10% | ||

| 14:00 | USD | NAHB Housing Index Mar | |

| Forecast: 48 | Previous: 48 | ||

Tuesday, Mar 19, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| JPY | BoJ Interest Rate Decision | -0.10% | -0.10% | |

| 03:30 | AUD | RBA Interest Rate Decision | 4.35% | 4.35% |

| 04:30 | AUD | RBA Press Conference | ||

| 04:30 | JPY | Industrial Production M/M Jan F | -7.50% | -7.50% |

| 07:00 | CHF | Trade Balance (CHF) Feb | 3.50B | 4.74B |

| 08:00 | CHF | SECO Economic Forecasts | ||

| 10:00 | EUR | Germany ZEW Economic Sentiment Mar | 21 | 19.9 |

| 10:00 | EUR | Germany ZEW Current Situation Mar | -80 | -81.7 |

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Mar | 25.4 | 25 |

| 12:30 | CAD | CPI M/M Feb | 0.60% | 0.00% |

| 12:30 | CAD | CPI Y/Y Feb | 3.10% | 2.90% |

| 12:30 | CAD | CPI Median Y/Y Feb | 3.40% | 3.30% |

| 12:30 | CAD | CPI Trimmed Y/Y Feb | 3.50% | 3.40% |

| 12:30 | CAD | CPI Common Y/Y Feb | 3.60% | 3.40% |

| 12:30 | USD | Building Permits Feb | 1.50M | 1.47M |

| 12:30 | USD | Housing Starts Feb | 1.43M | 1.33M |

| 20:00 | NZD | Westpac Consumer Survey Q1 | 88.9 | |

| 21:45 | NZD | Current Account (NZD) Q4 | -7.80B | -11.47B |

| GMT | Ccy | Events | |

|---|---|---|---|

| JPY | BoJ Interest Rate Decision | ||

| Forecast: -0.10% | Previous: -0.10% | ||

| 03:30 | AUD | RBA Interest Rate Decision | |

| Forecast: 4.35% | Previous: 4.35% | ||

| 04:30 | AUD | RBA Press Conference | |

| Forecast: | Previous: | ||

| 04:30 | JPY | Industrial Production M/M Jan F | |

| Forecast: -7.50% | Previous: -7.50% | ||

| 07:00 | CHF | Trade Balance (CHF) Feb | |

| Forecast: 3.50B | Previous: 4.74B | ||

| 08:00 | CHF | SECO Economic Forecasts | |

| Forecast: | Previous: | ||

| 10:00 | EUR | Germany ZEW Economic Sentiment Mar | |

| Forecast: 21 | Previous: 19.9 | ||

| 10:00 | EUR | Germany ZEW Current Situation Mar | |

| Forecast: -80 | Previous: -81.7 | ||

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Mar | |

| Forecast: 25.4 | Previous: 25 | ||

| 12:30 | CAD | CPI M/M Feb | |

| Forecast: 0.60% | Previous: 0.00% | ||

| 12:30 | CAD | CPI Y/Y Feb | |

| Forecast: 3.10% | Previous: 2.90% | ||

| 12:30 | CAD | CPI Median Y/Y Feb | |

| Forecast: 3.40% | Previous: 3.30% | ||

| 12:30 | CAD | CPI Trimmed Y/Y Feb | |

| Forecast: 3.50% | Previous: 3.40% | ||

| 12:30 | CAD | CPI Common Y/Y Feb | |

| Forecast: 3.60% | Previous: 3.40% | ||

| 12:30 | USD | Building Permits Feb | |

| Forecast: 1.50M | Previous: 1.47M | ||

| 12:30 | USD | Housing Starts Feb | |

| Forecast: 1.43M | Previous: 1.33M | ||

| 20:00 | NZD | Westpac Consumer Survey Q1 | |

| Forecast: | Previous: 88.9 | ||

| 21:45 | NZD | Current Account (NZD) Q4 | |

| Forecast: -7.80B | Previous: -11.47B | ||

Wednesday, Mar 20, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 07:00 | EUR | Germany PPI M/M Feb | -0.20% | 0.20% |

| 07:00 | EUR | Germany PPI Y/Y Feb | -4.40% | |

| 07:00 | GBP | CPI M/M Feb | 0.70% | -0.60% |

| 07:00 | GBP | CPI Y/Y Feb | 3.50% | 4.00% |

| 07:00 | GBP | Core CPI Y/Y Feb | 4.60% | 5.10% |

| 07:00 | GBP | RPI M/M Feb | 0.80% | -0.30% |

| 07:00 | GBP | RPI Y/Y Feb | 4.50% | 4.90% |

| 07:00 | GBP | PPI Input M/M Feb | 0.20% | -0.80% |

| 07:00 | GBP | PPI Input Y/Y Feb | -3.30% | |

| 07:00 | GBP | PPI Output M/M Feb | 0.10% | -0.20% |

| 07:00 | GBP | PPI Output Y/Y Feb | -0.60% | |

| 07:00 | GBP | PPI Core Output Y/Y Feb | -0.40% | |

| 07:00 | GBP | PPI Core Output M/M Feb | 0.20% | |

| 09:00 | EUR | Italy Industrial Output M/M Jan | 0.10% | 1.10% |

| 14:30 | USD | Crude Oil Inventories | -1.5M | |

| 15:00 | EUR | Eurozone Consumer Confidence Mar P | -15 | -16 |

| 17:30 | CAD | BoC Summary of Deliberations | ||

| 18:00 | USD | Fed Interest Rate Decision | 5.50% | 5.50% |

| 18:30 | USD | FOMC Press Conference | ||

| 21:45 | NZD | GDP Q/Q Q4 | 0.00% | -0.30% |

| 22:00 | AUD | Manufacturing PMI Mar P | 47.8 | |

| 22:00 | AUD | Services PMI Mar P | 53.1 | |

| 23:50 | JPY | Trade Balance (JPY) Feb | -0.85T | 0.24T |

| GMT | Ccy | Events | |

|---|---|---|---|

| 07:00 | EUR | Germany PPI M/M Feb | |

| Forecast: -0.20% | Previous: 0.20% | ||

| 07:00 | EUR | Germany PPI Y/Y Feb | |

| Forecast: | Previous: -4.40% | ||

| 07:00 | GBP | CPI M/M Feb | |

| Forecast: 0.70% | Previous: -0.60% | ||

| 07:00 | GBP | CPI Y/Y Feb | |

| Forecast: 3.50% | Previous: 4.00% | ||

| 07:00 | GBP | Core CPI Y/Y Feb | |

| Forecast: 4.60% | Previous: 5.10% | ||

| 07:00 | GBP | RPI M/M Feb | |

| Forecast: 0.80% | Previous: -0.30% | ||

| 07:00 | GBP | RPI Y/Y Feb | |

| Forecast: 4.50% | Previous: 4.90% | ||

| 07:00 | GBP | PPI Input M/M Feb | |

| Forecast: 0.20% | Previous: -0.80% | ||

| 07:00 | GBP | PPI Input Y/Y Feb | |

| Forecast: | Previous: -3.30% | ||

| 07:00 | GBP | PPI Output M/M Feb | |

| Forecast: 0.10% | Previous: -0.20% | ||

| 07:00 | GBP | PPI Output Y/Y Feb | |

| Forecast: | Previous: -0.60% | ||

| 07:00 | GBP | PPI Core Output Y/Y Feb | |

| Forecast: | Previous: -0.40% | ||

| 07:00 | GBP | PPI Core Output M/M Feb | |

| Forecast: | Previous: 0.20% | ||

| 09:00 | EUR | Italy Industrial Output M/M Jan | |

| Forecast: 0.10% | Previous: 1.10% | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: -1.5M | ||

| 15:00 | EUR | Eurozone Consumer Confidence Mar P | |

| Forecast: -15 | Previous: -16 | ||

| 17:30 | CAD | BoC Summary of Deliberations | |

| Forecast: | Previous: | ||

| 18:00 | USD | Fed Interest Rate Decision | |

| Forecast: 5.50% | Previous: 5.50% | ||

| 18:30 | USD | FOMC Press Conference | |

| Forecast: | Previous: | ||

| 21:45 | NZD | GDP Q/Q Q4 | |

| Forecast: 0.00% | Previous: -0.30% | ||

| 22:00 | AUD | Manufacturing PMI Mar P | |

| Forecast: | Previous: 47.8 | ||

| 22:00 | AUD | Services PMI Mar P | |

| Forecast: | Previous: 53.1 | ||

| 23:50 | JPY | Trade Balance (JPY) Feb | |

| Forecast: -0.85T | Previous: 0.24T | ||

Thursday, Mar 21, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Mar P | 47.5 | 47.2 |

| 00:30 | AUD | Employment Change Feb | 40.2K | 0.5K |

| 00:30 | AUD | Unemployment Rate Feb | 4.00% | 4.10% |

| 07:00 | GBP | Public Sector Net Borrowing (GBP) Feb | 5.2B | -17.6B |

| 08:15 | EUR | France Manufacturing PMI Mar P | 47.3 | 47.1 |

| 08:15 | EUR | France Services PMI Mar P | 48.6 | 48.4 |

| 08:30 | EUR | Germany Manufacturing PMI Mar P | 43.5 | 42.5 |

| 08:30 | EUR | Germany Services PMI Mar P | 48.9 | 48.3 |

| 08:30 | CHF | SNB Interest Rate Decision | 1.75% | |

| 09:00 | CHF | SNB Press Conference | ||

| 09:00 | EUR | Eurozone Current Account (EUR) Jan | 32.3B | 31.9B |

| 09:00 | EUR | ECB Economic Bulletin | ||

| 09:00 | EUR | Eurozone Manufacturing PMI Mar P | 47.0 | 46.5 |

| 09:00 | EUR | Eurozone Services PMI Mar P | 50.5 | 50.2 |

| 09:30 | GBP | Manufacturing PMI Mar P | 47.8 | 47.5 |

| 09:30 | GBP | Services PMI Mar P | 53.8 | 53.8 |

| 12:00 | GBP | BoE Interest Rate Decision | 5.25% | 5.25% |

| 12:00 | GBP | MPC Official Bank Rate Votes | 0--1--8 | 2--1--6 |

| 12:30 | CAD | New Housing Price Index M/M Feb | 0.10% | -0.10% |

| 12:30 | USD | Initial Jobless Claims (Mar 15) | 210K | 209K |

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Mar | 0.2 | 5.2 |

| 12:30 | USD | Current Account (USD) Q4 | -209B | -200B |

| 13:45 | USD | Manufacturing PMI Mar P | 51.9 | 52.2 |

| 13:45 | USD | Services PMI Mar P | 52 | 52.3 |

| 14:00 | USD | Existing Home Sales Feb | 3.94M | 4.00M |

| 14:30 | USD | EIA Natural Gas Storage Change (Mar 15) | -9B | |

| 21:45 | NZD | Trade Balance (MZD) Feb | -976M | |

| 23:30 | JPY | National CPI Y/Y Feb | 2.20% | |

| 23:30 | JPY | National CPI ex Fresh Food Y/Y Feb | 2.80% | 2.00% |

| 23:30 | JPY | National CPI ex Food Energy Y/Y Feb | 3.50% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Mar P | |

| Forecast: 47.5 | Previous: 47.2 | ||

| 00:30 | AUD | Employment Change Feb | |

| Forecast: 40.2K | Previous: 0.5K | ||

| 00:30 | AUD | Unemployment Rate Feb | |

| Forecast: 4.00% | Previous: 4.10% | ||

| 07:00 | GBP | Public Sector Net Borrowing (GBP) Feb | |

| Forecast: 5.2B | Previous: -17.6B | ||

| 08:15 | EUR | France Manufacturing PMI Mar P | |

| Forecast: 47.3 | Previous: 47.1 | ||

| 08:15 | EUR | France Services PMI Mar P | |

| Forecast: 48.6 | Previous: 48.4 | ||

| 08:30 | EUR | Germany Manufacturing PMI Mar P | |

| Forecast: 43.5 | Previous: 42.5 | ||

| 08:30 | EUR | Germany Services PMI Mar P | |

| Forecast: 48.9 | Previous: 48.3 | ||

| 08:30 | CHF | SNB Interest Rate Decision | |

| Forecast: | Previous: 1.75% | ||

| 09:00 | CHF | SNB Press Conference | |

| Forecast: | Previous: | ||

| 09:00 | EUR | Eurozone Current Account (EUR) Jan | |

| Forecast: 32.3B | Previous: 31.9B | ||

| 09:00 | EUR | ECB Economic Bulletin | |

| Forecast: | Previous: | ||

| 09:00 | EUR | Eurozone Manufacturing PMI Mar P | |

| Forecast: 47.0 | Previous: 46.5 | ||

| 09:00 | EUR | Eurozone Services PMI Mar P | |

| Forecast: 50.5 | Previous: 50.2 | ||

| 09:30 | GBP | Manufacturing PMI Mar P | |

| Forecast: 47.8 | Previous: 47.5 | ||

| 09:30 | GBP | Services PMI Mar P | |

| Forecast: 53.8 | Previous: 53.8 | ||

| 12:00 | GBP | BoE Interest Rate Decision | |

| Forecast: 5.25% | Previous: 5.25% | ||

| 12:00 | GBP | MPC Official Bank Rate Votes | |

| Forecast: 0--1--8 | Previous: 2--1--6 | ||

| 12:30 | CAD | New Housing Price Index M/M Feb | |

| Forecast: 0.10% | Previous: -0.10% | ||

| 12:30 | USD | Initial Jobless Claims (Mar 15) | |

| Forecast: 210K | Previous: 209K | ||

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Mar | |

| Forecast: 0.2 | Previous: 5.2 | ||

| 12:30 | USD | Current Account (USD) Q4 | |

| Forecast: -209B | Previous: -200B | ||

| 13:45 | USD | Manufacturing PMI Mar P | |

| Forecast: 51.9 | Previous: 52.2 | ||

| 13:45 | USD | Services PMI Mar P | |

| Forecast: 52 | Previous: 52.3 | ||

| 14:00 | USD | Existing Home Sales Feb | |

| Forecast: 3.94M | Previous: 4.00M | ||

| 14:30 | USD | EIA Natural Gas Storage Change (Mar 15) | |

| Forecast: | Previous: -9B | ||

| 21:45 | NZD | Trade Balance (MZD) Feb | |

| Forecast: | Previous: -976M | ||

| 23:30 | JPY | National CPI Y/Y Feb | |

| Forecast: | Previous: 2.20% | ||

| 23:30 | JPY | National CPI ex Fresh Food Y/Y Feb | |

| Forecast: 2.80% | Previous: 2.00% | ||

| 23:30 | JPY | National CPI ex Food Energy Y/Y Feb | |

| Forecast: | Previous: 3.50% | ||

Friday, Mar 22, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:01 | GBP | GfK Consumer Confidence Mar | -20 | -21 |

| 07:00 | GBP | Retail Sales M/M Feb | -0.30% | 3.40% |

| 09:00 | EUR | Germany IFO Business Climate Mar | 86.2 | 85.5 |

| 09:00 | EUR | Germany IFO Current Assessment Mar | 86.9 | |

| 09:00 | EUR | Germany IFO Expectations Mar | 84.1 | |

| 12:30 | CAD | Retail Sales M/M Jan | -0.40% | 0.90% |

| 12:30 | CAD | Retail Sales ex Autos M/M Jan | -0.50% | 0.60% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:01 | GBP | GfK Consumer Confidence Mar | |

| Forecast: -20 | Previous: -21 | ||

| 07:00 | GBP | Retail Sales M/M Feb | |

| Forecast: -0.30% | Previous: 3.40% | ||

| 09:00 | EUR | Germany IFO Business Climate Mar | |

| Forecast: 86.2 | Previous: 85.5 | ||

| 09:00 | EUR | Germany IFO Current Assessment Mar | |

| Forecast: | Previous: 86.9 | ||

| 09:00 | EUR | Germany IFO Expectations Mar | |

| Forecast: | Previous: 84.1 | ||

| 12:30 | CAD | Retail Sales M/M Jan | |

| Forecast: -0.40% | Previous: 0.90% | ||

| 12:30 | CAD | Retail Sales ex Autos M/M Jan | |

| Forecast: -0.50% | Previous: 0.60% | ||

The Weekly Bottom Line: Sticky Prices Could Delay Rate Cuts

U.S. Highlights

- February’s Consumer Price Index report showed that inflation came in higher-than-expected for a second consecutive month – a development which is likely to be on the Fed’s agenda at their two-day meeting next week.

- Spending in the retail sector disappointed expectations, despite some recovery from last month’s notable decline.

- With inflation top of mind, U.S. small businesses were also feeling less optimistic in February.

Canadian Highlights

- Canadian bond yields climbed this week, reflecting developments south of the border and domestic inflationary concerns.

- Canadian households saw a sizeable increase in net worth in the fourth quarter of 2023, fueled by financial market gains and restrained liability growth. Anticipated wealth gains in Q1 may prove to be a tailwind for consumer spending.

- Quebec’s budget highlighted fiscal challenges with rising debt levels, while the upcoming federal update in April is likely to see upward revisions to government revenues but offers limited fiscal leeway.

U.S. – Sticky Prices Could Delay Rate Cuts

The key data among this week’s releases was the consumer price inflation numbers. While the headline monthly figure was in line with expectations, the details could give the Fed more to discuss in their upcoming policy meeting next week. Markets took the report in stride, with Treasury yields up a bit and the major stock indices closing the day higher after the release.

Delving into the details, the CPI report showed that both monthly and annual headline inflation accelerated in February, largely reflecting a rise in gasoline and shelter prices. This was also accompanied by higher-than-expected figures for both monthly and annual core inflation. Notably, the prices for core goods unexpectedly ticked higher in February after eight consecutive months of price declines. Back-to-back months of stronger than expected readings on core inflation point to an uneven road ahead as the Fed attempts to steer inflation back to target.

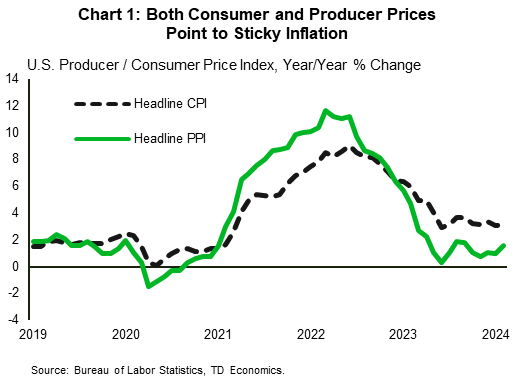

Price pressures further up the supply chain were also a little hotter than expected in February. The Producer Price Index (PPI) also came in above expectations. Both the monthly and annual headline PPI numbers accelerated relative to January. As such, both the consumer and producer price reports suggest that inflationary pressures remain sticky (Chart 1).

Adding to the subjects that the Fed will likely be mulling over during their meeting, is the 0.6% m/m gain in February’s retail sales after a sizeable pullback in January. On the upside, while retail sales growth flipped back to positive territory, it was lower than market expectations (0.8%). What’s more, the control group category, which factors into the calculation of personal consumption expenditure, was flat on the month relative to expectations for growth. Overall, the data suggests that consumers still have the ability to spend, despite challenges to their balance sheet, such as higher prices.

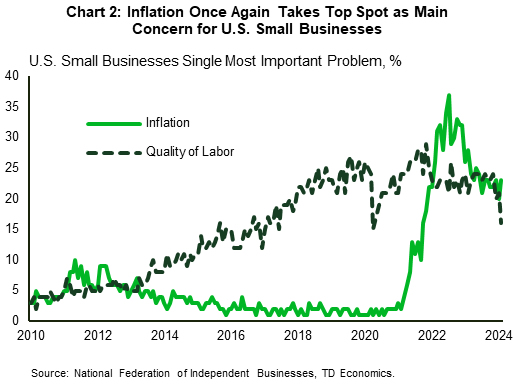

Inflation was also high on the list of concerns for America’s small businesses. A net 23% of respondents to the NFIB’s small business survey noted that inflation was their single most important business problem, up three points from the previous reading (Chart 2). Overall, small businesses were less optimistic in February, with the optimism index dropping to a nine-month low of 89.4. This was lower than market expectations for a slight improvement and notably below the series’ 50-year average of 98. On the upside, small businesses are having an easier time attracting and retaining employees, such that the net percentage of firms who increased compensation or are planning to do so in the near-term both fell over the month.

The key takeaway from this week’s releases is that while the labor market is normalizing as indicated by responses from the small business sector, consumers still have spending power and inflationary pressures have not fully abated. The combination suggests that the Fed is likely to remain cautious with respect to rate cuts, erring on the side of leaving rates higher for longer rather than take the risk of re-igniting price pressures by cutting prematurely.

Canada – Wealth Boost May Cheer Some Consumers

This week saw a quieter pace in economic data, leaving financial market sentiment largely influenced by developments south of the border. There, expectations for higher rates firmed in light of more persistent inflationary pressures and sustained consumer activity, nudging the Canadian government’s 5-year rate benchmark up by more than 20 basis points. Initially buoyed by the International Energy Agency’s revised oil demand growth estimates for 2024, the S&P TSX index reached its highest level since April 2022 but retreated later, closing 0.6% higher for the week.

Sparse though it was, the week brought forward several second-tier data releases. The national balance sheet and financial flow accounts for Q4 2023 showed that Canadian household net worth grew by $290 billion, offsetting the previous quarter's decline. This uptick nudged wealth growth back into positive territory for Q4, edging the year-end balance closer to its 2021 zenith. Gains in the financial markets and subdued liabilities growth delivered a boost to Canadian households' wealth.

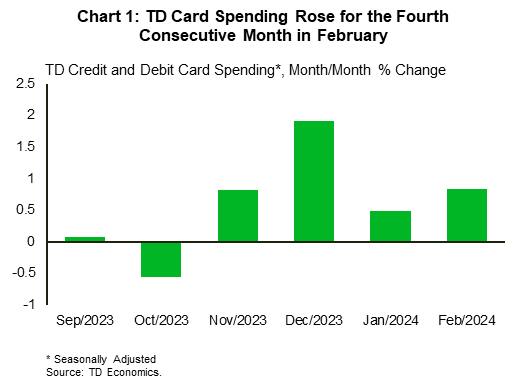

The apparent rebound in household wealth towards 2023’s end could be behind a renewed consumer momentum in recent months. The concept of "the wealth effect", though theoretical in classical economics, tangibly influences sentiment. This means an upgrade in consumer spending might be in the books. So far in the first quarter equity prices remain on an upswing. In addition, we expect home prices to turn positive this quarter, supporting wealth gains. Today's report on housing starts suggests that February's sizeable increase in starts was at least partially driven by a rebound in housing market activity and rising home prices. Furthermore, our internal spending data shows a fourth consecutive month of spending increases in February (Chart 1). This suggests Q1 may prove relatively buoyant for consumer spending.

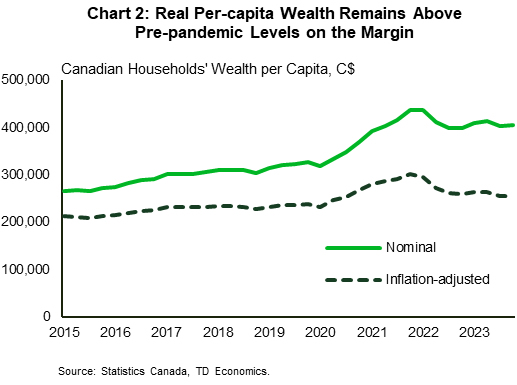

The potential wealth effect on consumer spending, however, likely remains confined to a fraction of Canadian families. Adjusted for inflation and population growth, households' wealth is back to late 2020 levels and is only around 7% higher than the 2019 level (Chart 2). Compare this to the peak in Q4 2021, when this measure was 26% higher. Since then, real spending per capita contracted in five out eight last quarters. As more Canadians renew their mortgages at higher rates, the economy braces for a period of below-trend growth amid rising debt servicing costs.

Weak revenue growth and debt servicing costs were top of mind for Quebec's fiscal authorities as they prepared the province's budget. Expectations for the fiscal outlook have dimmed, with an anticipated rise in the debt-to-GDP ratio to 40% by FY2025/26 due to increased spending and tepid revenue growth. The Government of Canada is also preparing for its April 16th Budget, where we expect upward revisions to nominal GDP forecasts to boost government revenues, but offer limited fiscal leeway. Major new expenditures are unlikely, with nationwide pharmacare likely being the most heavily discussed item. After all, the government seems to be attuned to the need of striking the right balance between cost and effectiveness, while ‘creating the conditions’ for interest rates to fall.

Weekly Economic & Financial Commentary: FOMC Likely on Hold Until Summer

Summary

United States: The Equinox and the Struggle to Find Balance

- Spring is a time for new beginnings, and we see fresh possibility in some of this week's less-than-stellar data. It may eventually help bring the needed balance into place to get inflation closer to the FOMC's target.

- Next week: Housing Starts (Tue.), Existing Home Sales (Thu.)

International: Latin America Disinflation Is Stalling

- While nations across Latin America have made impressive progress in their battles against inflation, regional disinflation hit a few speed bumps this week that could disrupt rate cut cycles.

- Next week: Bank of Japan (Tue.), Bank of England (Thu.), Central Bank of Mexico (Thu.)

Interest Rate Watch: FOMC Likely on Hold Until Summer

- Very few observers, ourselves included, look for a policy change at next week's FOMC meeting. Indeed, recent data have reduced the odds that the Committee will cut rates at its next meeting on May 1. Accordingly, we have pushed out our expectation of the commencement of the easing cycle to June 12.

Topic of the Week: Consumer Expectations Deteriorate for Lower Income Cohorts

- Earlier this week, the New York Fed released the February update to its Survey of Consumer Expectations (SCE). The recent update depicts lower income consumers as increasingly uncertain amid broader signs of the labor market softening.