Sample Category Title

USD/JPY: JPY Plummeted, Ignoring the Possibility of a More Hawkish BoJ

The price actions of the USD/JPY have reacted negatively right below the 150.70 key resistance as highlighted in our previous analysis and shed -435 pips/-2.9% to print a recent intraday low of 146.48 on 8 March.

Thereafter, the USD/JPY has drifted higher to trade back above the 148.00 psychological level in light of the “not so soft” US inflation data (CPI & PCE) for February that increases the odds that the US Federal Reserve is in no rush to cut its Fed funds rate in March and even during May’s FOMC meeting; that’s pushing backward the highly anticipated first rate cut down the calendar.

Interestingly, the Japanese side of the equation has failed to spur a renewed leg of JPY strength. Last Friday, Rengo, Japan’s largest trade union federation announced that it has secured a stronger-than-expected average employee wage increase of 5.28% in the preliminary wage negotiations result for FY 2024/2025, above last year’s increase of 3.58%, and its largest wage hike since 1991.

In recent months, Bank of Japan Governor Ueda has heavily emphasized that a sustainable wage increase is a key deciding factor for BoJ to normalize its current ultra-accommodative monetary policy.

Given the latest big jump in Japanese employees’ wages, local press Kyodo and Nikkei reported that BoJ will raise the short-term interest rate to the 0% to 0.1% range tomorrow, 19 March, at the end of its two-day monetary policy meeting, citing sources close to BoJ. The Nikkei stated that BoJ could go the extra mile tomorrow by scrapping the Yield Curve Control (YCC) program on the 10-year Japanese Government Bond (JGB) yield, that’s total removal of the limits where the 1% upper limit is being used as a “reference level” for now.

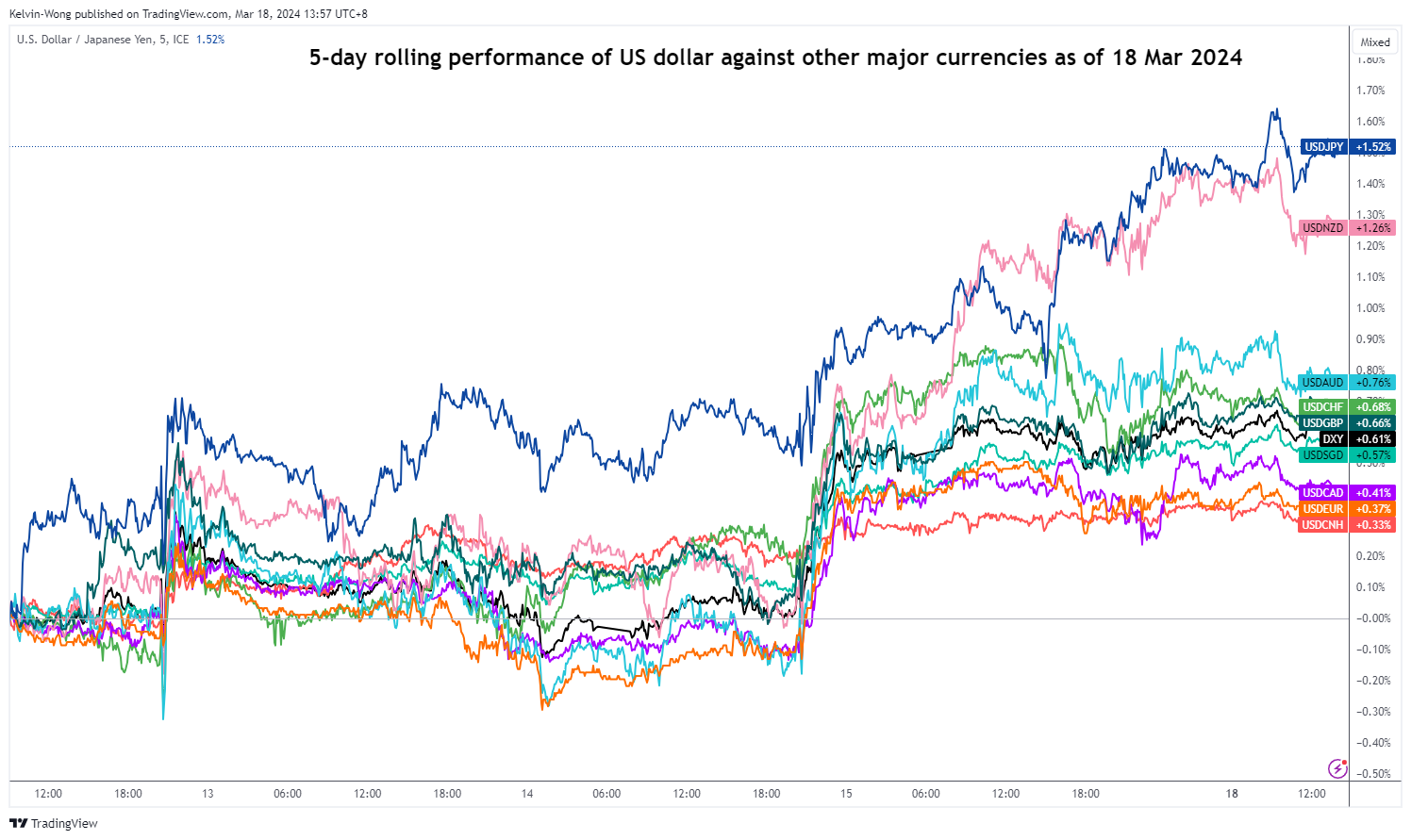

No JPY strength resurgence so far despite supporting fundamentals & news flow

Fig 1: 5-day rolling performance of USD against other major currencies as of 18 Mar 2024 (Source: TradingView, click to enlarge chart)

However, the current price action movements of USD/JPY do not seem to reflect such positive fundamentals and news flows that are supportive of JPY strength; instead, the USD/JPY has continued to extend its rally last Friday, ex-post Rengo’s wage hike results, and added +131 pips/+0.9% to print a current intraday high of 149.33 at this time of the writing.

Based on a 5-day rolling performance of the US dollar against other major currencies, the USD/JPY pair is the top performer so far with a gain of +1.5% (see Fig 1).

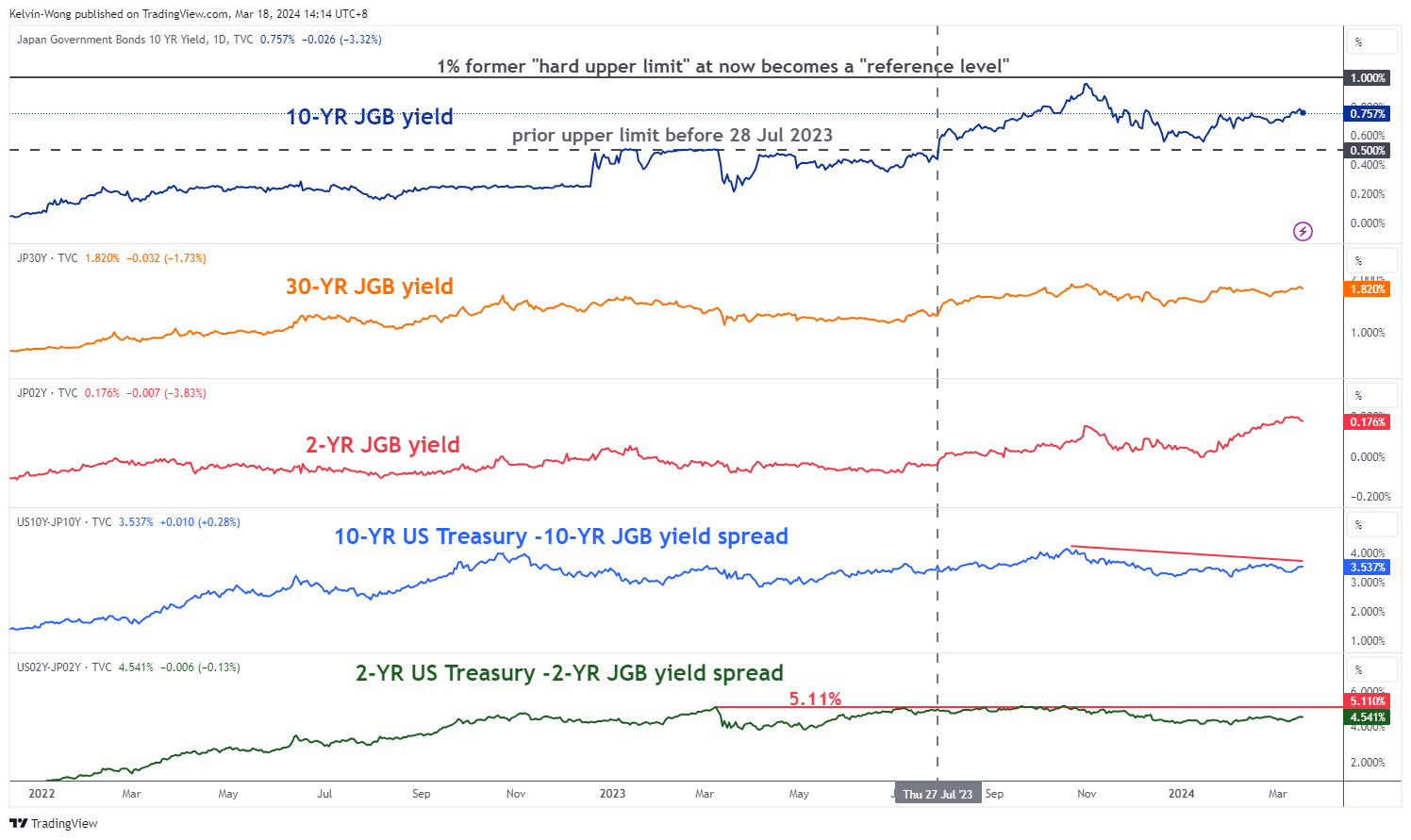

The current bout of JPY weakness may be mispriced

Fig 2: JGB yield curve spread major trends as of 18 Mar 2024 (Source: TradingView, click to enlarge chart)

Fig 3: US Treasuries/JGB yield spread medium-term trends as of 18 Mar 2024 (Source: TradingView, click to enlarge chart)

The current bear-steepening trajectory of the JGB yield curve for both the 10-year/2-year spread and 30-year/2-year spread in place since late June 2022 and most recently, both of the yield curve spreads have managed to stage a rebound from their respective ascending channel supports at 0.54% (10-year/2-year) and 1.60% (30-year/2-year) (see Fig 2).

A bear-steepening yield curve movement is being driven by the longer-end (10-year and 30-year JGB yields) that are rising at a faster pace than the lower-end (2-year JGB yield) suggests that the Japanese economy is showing no clear signs of reverting to a deflationary environment which in turn allow BoJ more room to kickstart the normalization of its ultra-accommodative monetary policy soon.

Secondly, both the long and short-end yield spread between the US Treasuries and JGBs are still capped below their respective key resistance levels; 3.8% (10-year) and 5.11% (2-year) (see Fig 3).

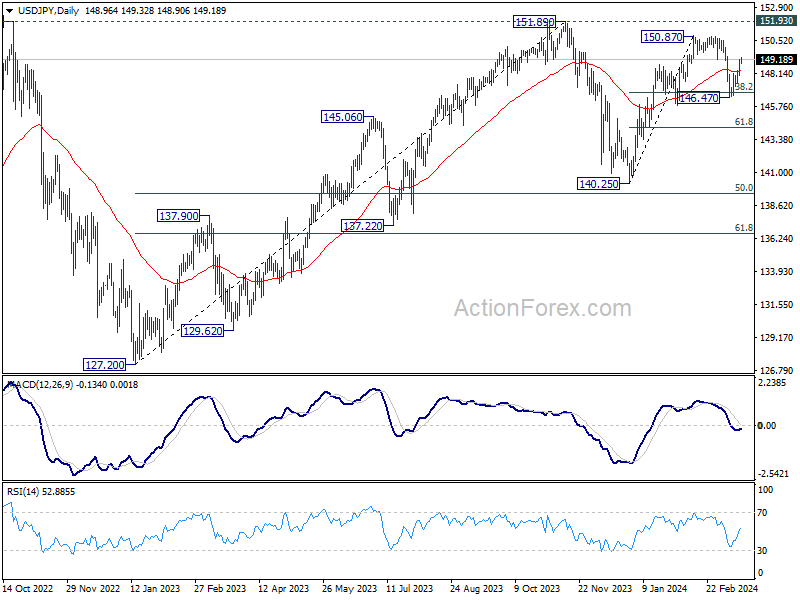

Watch the 20-day moving average of the USD/JPY

Fig 4: USD/JPY short-term trend as of 18 Mar 2024 (Source: TradingView, click to enlarge chart)

The recent two weeks of rally seen in USD/JPY from its 8 March low of 146.48 has now reached a key inflection level of 149.50 that is coincided by the 20-day moving average acting as a resistance, upper boundary of its minor ascending channel in place 8 March low, former minor swing lows of 15 February/29 February, and close to the 76.4% Fibonacci retracement of the prior minor decline from 27 February high to 8 March low (see Fig 4).

In addition, the hourly RSI momentum indicator has flashed a bearish divergence condition at its overbought region which suggests a potential easing of the recent upside momentum of USD/JPY.

If the 149.50 key short-term pivotal resistance is not surpassed to the upside, the USD/JPY may stage a potential bearish reaction to expose the near-term supports of 148.80/60 and 147.95 in the first step.

On the other hand, a clearance above 149.50 invalidates the bearish bias for a squeeze up for the next near-term resistance to come in at 150.15, and above it exposes the lower limit of a major resistance zone at 150.65/85.

Yen Surprisingly Weakens into BoJ Decision

A week packed with central bank decisions starts on a mixed note after hotter-than-expected US inflation sent the US 2-year yield around 25bp higher over the week and the 10-year yield spiked past the 4.30% mark. Stocks resisted to higher yields for the major part of the week, but the mood was not brilliant on Friday. The S&P500 fell from an ATH, as equity bulls also started feeling the heat of hawkish fears before this week’s FOMC meeting and stocks in Europe were also sold off before the weekly closing bell.

In the FX, last week saw the US dollar rebound and majors retreat against a globally stronger greenback. The EURUSD sank below 1.09, Cable fell after hitting the highest level since last summer and the USDJPY traded past the 149. While the dollar’s appreciation was easy to understand against the euro – where the European Central Bank (ECB) members sounded explicit about their intention to cut rates in June, and against sterling – where softer jobs data supported the Bank of England (BoE) doves, the persistent fall of the Japanese yen was surprising, even more so as the news that big Japanese corporation met the wages demand kept coming in throughout the week. On Friday, the country’s biggest union group announced that they secured a pay rise of nearly 5.30%. But in vain, the USDJPY kept rising. The yen bulls remain surprisingly reluctant to take action and the implied volatility in the yen markets remains surprisingly low compared to the levels we saw back in summer, when the Bank of Japan (BoJ) decided to double its target rate on JGB 10-year yield, and last December, when the BoJ was supposed to give a clearer hint on when they would exit the negative rate policy.

Some reasons for the lack of enthusiasm could be

- There are still many people – like me – thinking that there is a greater chance for the BoJ NOT to act this week but wait for the April meeting instead. If that’s the case, there is not much incentive to sell the yen at the current levels, because there is little potential for a worthy rise in the USDJPY above the 150 level.

- Even if they raised, the rate hikes in Japan will be slow and the BoJ will likely continue to buy JGBs.

- Federal Reserve (Fed) hawks weigh heavier on sentiment.

Whatever it is, the yen bulls are tired of getting disappointed by Mr. Ueda, who hinted that the bank is not in a rush to normalize.

Elsewhere

Fed expectations for this week’s meeting are mixed. We know that the Fed won’t change its interest rates this week, but the fresh forecasts and the dot plot will give a good hint on what the Fed members think about the latest economic data. The Fed members walk into this week’s meeting having seen a two-month jump in inflation, healthy jobs data, above-average economic growth and robust corporate earnings. Yes, there has been a renewed stress regarding the regional banks after the jitters around the NY Community Bancorp at the start of the year but that stress has been isolated and contained. Hence, there is a chance that the Fed members plot fewer rate cuts for this year and we see the median expectation fall to 2 rate cuts, from 3 plotted in December. If that’s the case, I would expect the US yields and the dollar extend gains and mood in equities sour and that would be such bad luck for Reddit that’s preparing to go public on March 21.

The Reserve Bank of Australia (RBA), the Bank of England (BoE) and the Swiss National Bank (SNB) will also announce their latest policy verdict this week and are expected to maintain their rates unchanged. The SNB will likely follow in the footsteps of the ECB and act in the H1. The RBA on the other hand is much more concerned by a renewed pressure on inflation and some RBA hawks even think that the bank won’t cut the rates at all this year. A hawkish stance from the RBA may not stop the AUDUSD’s selloff if the Fed sounds decidedly hawkish as well. The Aussie-dollar is better bid this morning on better-than-expected Chinese data and news that the Chinese would maintain fiscal spending to boost growth. But we shall see the pair sink below 200-DMA if dollar bulls come back in charge.

Get Ready to Rumble – Central Bank Week is Here

In focus today

In the euro area, we will keep an eye on the final inflation data for February. The final HICP figures provide insights into the underlying inflation measures tracked by the ECB, while also revealing drivers behind the relatively strong core inflation print in February.

Overnight, the Bank of Japan concludes a two-day policy meeting, where analysts' expectations are very divided. The strong first wage tally (for more details see below) from the "spring wage offensive" we got on Friday was a key missing piece of the puzzle for the BoJ to confidently hike the policy rate out of negative territory. However, the impact on the SME segment remains uncertain. With the continued strong US inflation pressure and postponed rate cuts from the Fed, we deem a hawkish hold from the BoJ most likely. We aim for April as the right timing for a hike and abolishment of the yield curve control - for more details, see Research Japan - BoJ hike in sight - but no reason to rush Japan, 15 March.

In Australia, the Reserve Bank of Australia (RBA) will have a monetary policy meeting early tomorrow morning. In line with markets and consensus, we expect no monetary policy changes.

For the remainder of the week, major central bank decisions will be in focus. On Wednesday, we expect the FOMC to make no monetary policies changes. Thursday we will have Norges Bank (NB), Bank of England (BoE) and SNB decisions. While we expect NB and BoE to keep their policies unchanged, we expect the SNB to deliver a 25bp cut. Additionally, PMI data for various countries, including the UK, US, and euro area, will be released on Thursday.

Economic and market news

What happened overnight

In China, data overnight was slightly to the strong side with especially industrial production (IP) surprising to the upside. IP growth rose from 6.8% y/y in December to 7.0% y/y in Jan/Feb (cons: 5.3% y/y). Retail sales was broadly in line with expectations at 5.5% y/y in Jan/Feb vs expected 5.6% y/y by consensus. Housing data was positive as the level of home sales increased in Jan/Feb compared to Nov/Dec and construction starts also improved. It provides a little light in the housing crisis that the latest stimulus is starting to work and we may have seen the bottom in sales and construction. However, activity levels are still very low, and we need to see more data to make a firm conclusion on this. The market reaction was slightly positive with an 0.5% rise in offshore stocks and a small decline in USD/CNY. Financial markets have shown rising hopes that the worst of the Chinese crisis is behind us as Chinese stocks have rallied decently over the past two months and copper prices are at the highest level since April last year.

What happened on Friday and during the weekend

In the US, the University of Michigan flash consumer sentiment indicator for March was unchanged, whereas the expectations component ticked somewhat lower. While we recently have seen modest upticks in short-term market-based inflation expectations and in the NY Fed's survey, the University of Michigan inflation expectations, conversely, stayed put at previous modest levels (1y 3.9%, 5y 2.9%). This is good news for the Fed as higher inflation expectations would push real rates lower, and thus cause monetary policy to turn less restrictive. In addition, February industrial production was 0.1% m/m SA, slightly above consensus.

In Japan, as mentioned earlier, Rengo, the biggest labour union federation, released its first wage tally, which revealed a 5.28% wage increase for workers at major firms, close to their demanded 5.85%. The second tally is due this Friday. However, we will have to wait for at least the third wage tally, released in early April, to know more about the 70% of Japanese workers who are employed in the SME segment.

In Russia, the presidential election was held, and President Putin won a new six-year term.

Equities: Global equities were lower on Friday and down for the week. Normally, we would start by spending some time digesting the rotation in equities, but bond markets were more important last week; 5 out of 5 days with higher yields at the short end of the curve driven primarily by too hot inflation prints. With 20 basis points higher across the curve for the "wrong reasons" it is surprising that equities did not lose more last week. Looking forward, the biggest near-term threat to equities is more hot inflation data from the US and higher yields. Looking at the equity rotation, it is not so surprising to see energy and materials sectors doing strong with the inflationary pressure picking up. In the US on Friday, Dow -0.5%, S&P 500 -0.7%, Nasdaq -1.0% and Russell 2000 +0.4%. Asia is mostly higher this morning led by Japan (+2.5%) ahead of the interesting BoJ meeting tomorrow. European and US futures are higher this morning as well.

FI: It was a rather uneventful trading session on Friday with European bonds trading in a very tight range. 10y German yields traded within 3bp from high to low and ended the day at 2.44%. Similarly, the Bund asset swap spreads were virtually unchanged at 30bp. Seen over the week, Bund yields ended 18bp higher, and the Bund ASW tightened 3bp. We expect the Bund ASW to break through 30bp in the near term, as the current drivers (supply, lack of QE, collateral scarcity, and risk aversion) will continue.

FX: Relative monetary policy will likely drive FX markets the coming week with big central bank decisions looming. We do not expect BoJ to hike tomorrow, but it is a close call and if we are wrong JPY would likely head higher. On Thursday, we think CHF is poised to drop if we are right that the SNB will cut rates. The USD will look to see if the Fed agrees with the recent rise in US interest rates.

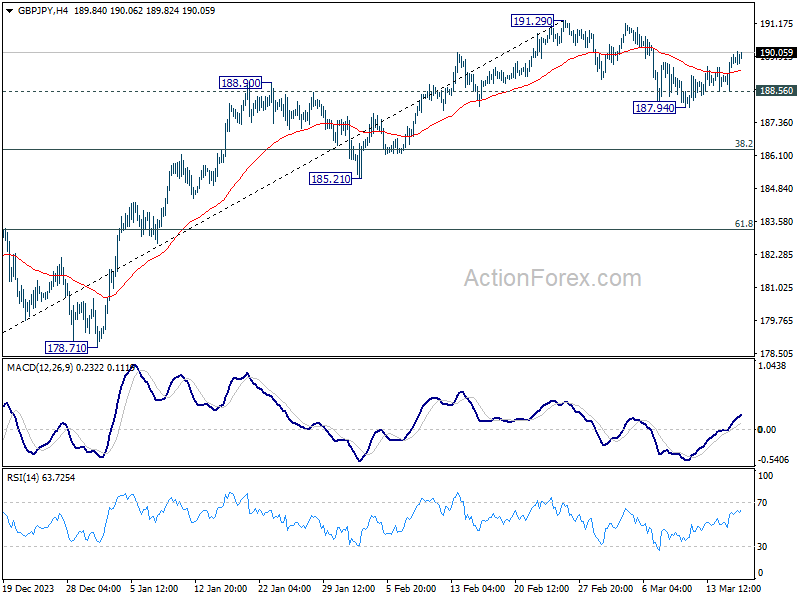

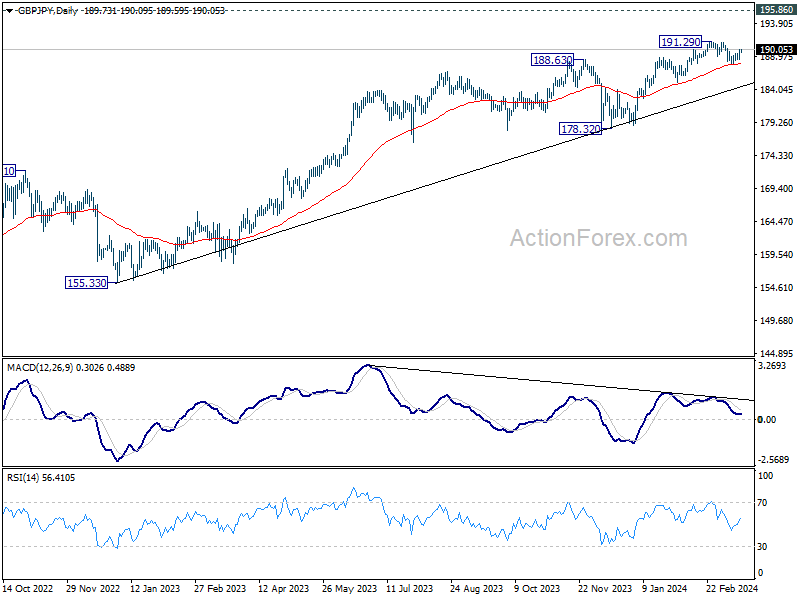

GBP/JPY Daily Outlook

Daily Pivots: (S1) 188.94; (P) 189.49; (R1) 190.38; More.....

Intraday bias in GBP/JPY remains on the upside at this point. Correction from 191.29 should have completed at 187.94 already. Further rise should be seen to retest 191.29 high first. Decisive break there will bring larger up trend resumption. On the downside, below 188.56 minor support will turn bias back to the downside to resume the correction instead.

In the bigger picture, up trend from 123.94 (2020 low) is in progress. Medium term outlook will stay bullish as long as 178.32 support holds. Next target is 195.86 long term resistance (2015 high).

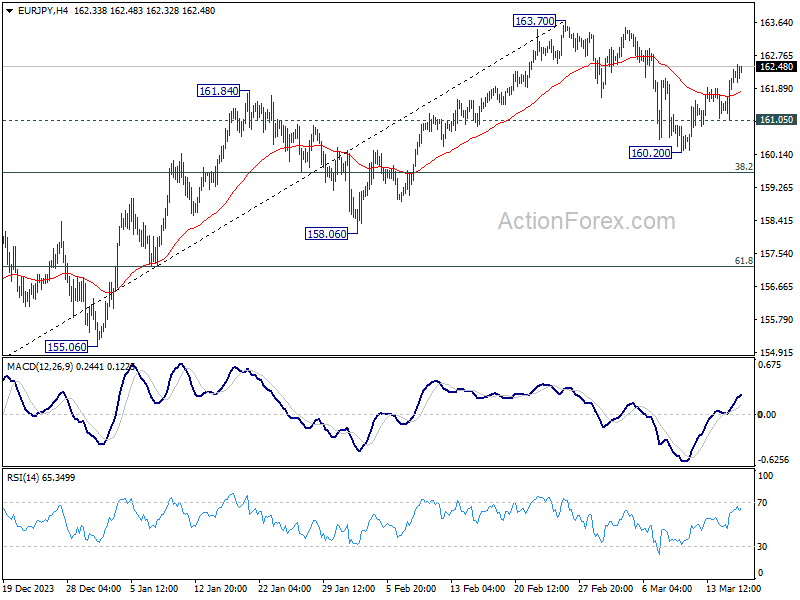

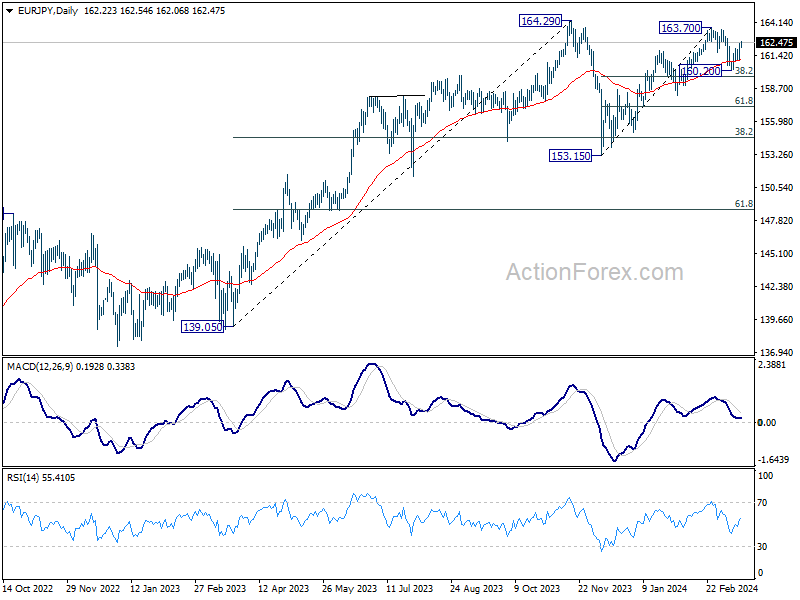

EUR/JPY Daily Outlook

Daily Pivots: (S1) 161.40; (P) 161.90; (R1) 162.74; More...

Intraday bias in EUR/JPY remains on the upside for the moment. Correction from 163.70 should have completed at 160.20. Further rally would be seen to retest 163.70 first. Decisive break there will resume larger rally from 153.15 for 164.29 high. On the downside, below 161.05 minor support will turn bias back to the downside to resume the correction from 163.70.

In the bigger picture, price actions from 164.29 medium term top are seen as a correction to rise from 139.05 which could still be extending. As long as 148.38 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) is expected to resume through 164.29 at a later stage. Next target would be 169.96 (2008 high).

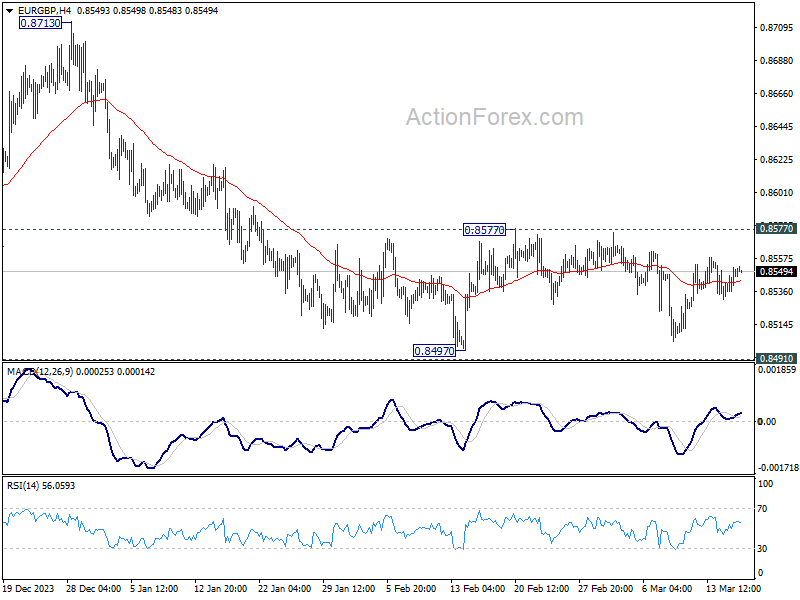

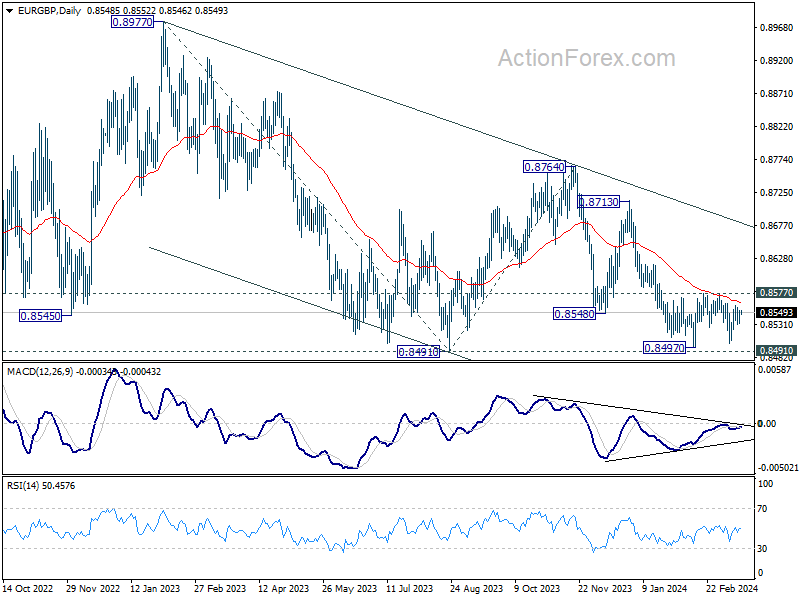

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8536; (P) 0.8544; (R1) 0.8558; More...

Range trading continues in EUR/GBP and intraday bias remains neutral. On the downside decisive break of 0.8491/7 support zone will confirm larger down trend resumption and target 0.8464 projection level first. However, firm break of 0.8577 will turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8713 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

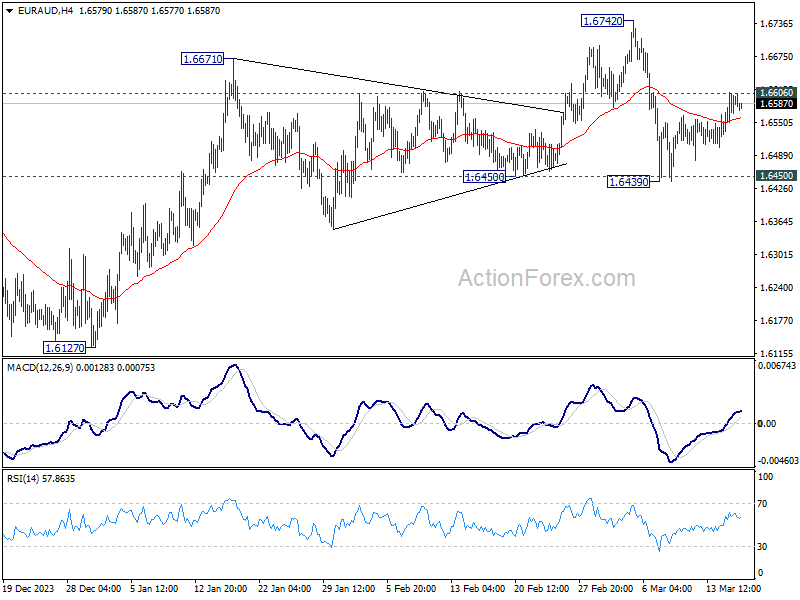

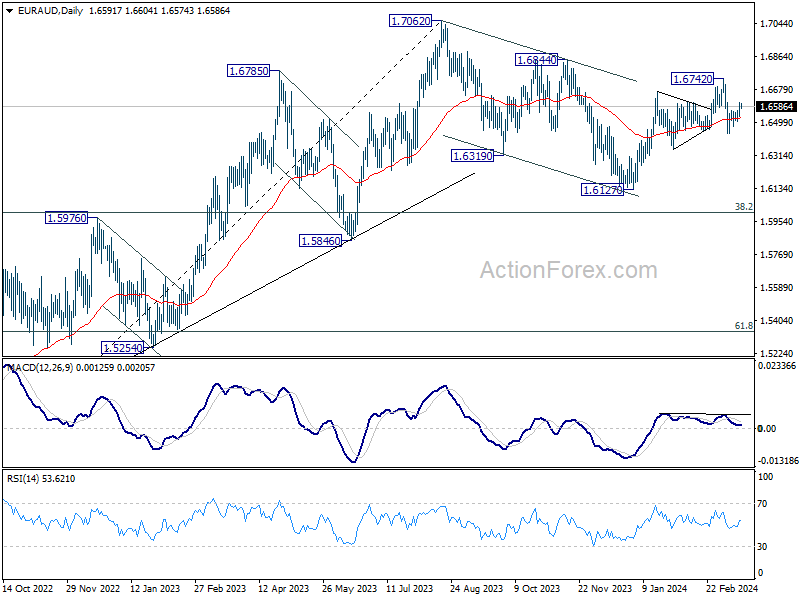

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6542; (P) 1.6576; (R1) 1.6631; More...

Intraday bias in EUR/AUD stays neutral at this point. On the upside, firm break of 1.6606 will retain near term bullishness and bring retest of 1.6742. Break there will resume larger rise from 1.6127. On the downside, however, decisive break of 1.6450 support will argue that whole rebound from 1.6127 has completed with three waves up to 1.6742 already. Near term outlook will be turned bearish for 1.6127 again.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

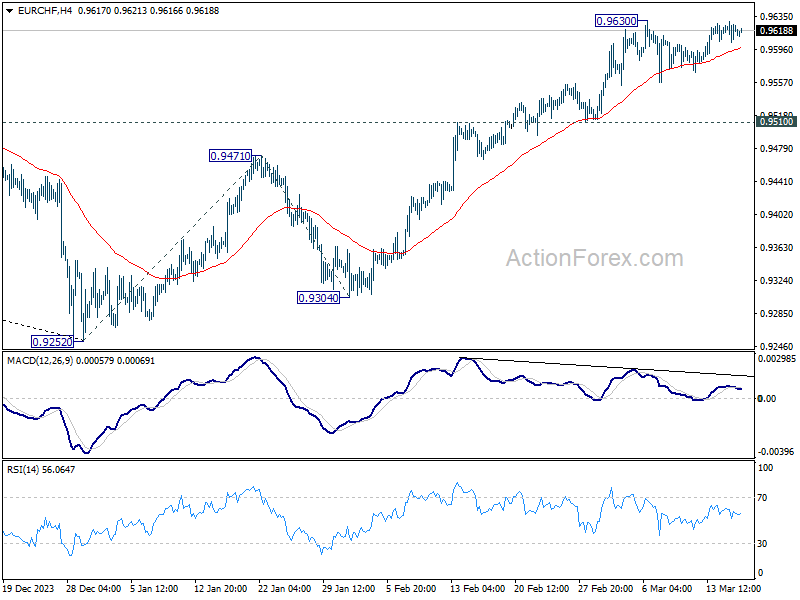

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9606; (P) 0.9619; (R1) 0.9631; More...

Range trading continues in EUR/CHF and intraday bias stays neutral. Another dip cannot be ruled out, but outlook will stay bullish as long as 0.9510 support holds. On the upside, break of 0.9630 will resume the rise from 0.9252 and target 161.8% projection of 0.9252 to 0.9471 from 0.9304 at 0.9658 next. However, considering bearish divergence condition in 4H MACD, firm break of 0.9510 will turn bias back to the downside for deeper fall.

In the bigger picture, as long as 0.9683 resistance holds, rebound from 0.9252 are seen as a corrective move only. Larger down trend is expected to resume through 0.9252 after the correction completes. However, firm break of 0.9683 and sustained trading above 55 W EMA (now at 0.9620) will argue that 0.9252 is already a medium term bottom. Stronger rise would then be seen 61.8% retracement of 1.0095 to 0.9252 at 0.9773 and above.

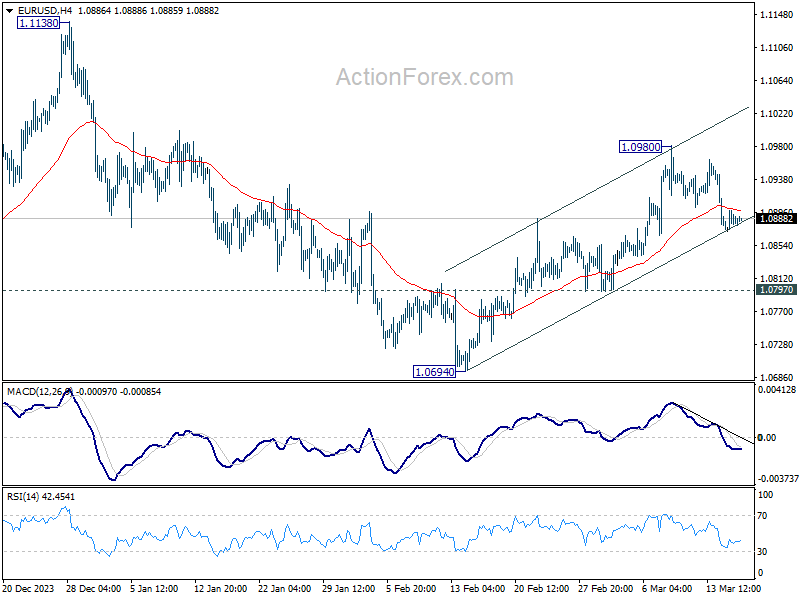

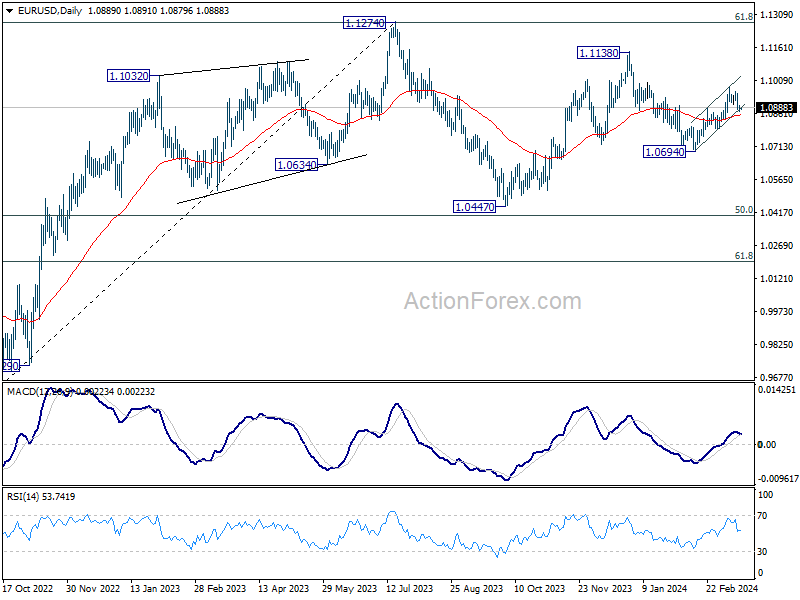

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0873; (P) 1.0887; (R1) 1.0900; More...

Intraday bias in EUR/USD remains on the downside for the moment. Fall from 1.0980 short term top would target 55 D EMA (now at 1.0856). Sustained break there will argue that rebound from 1.0694 has completed and bring retest of this low. For now, risk will stay on the downside as long as 1.0980 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

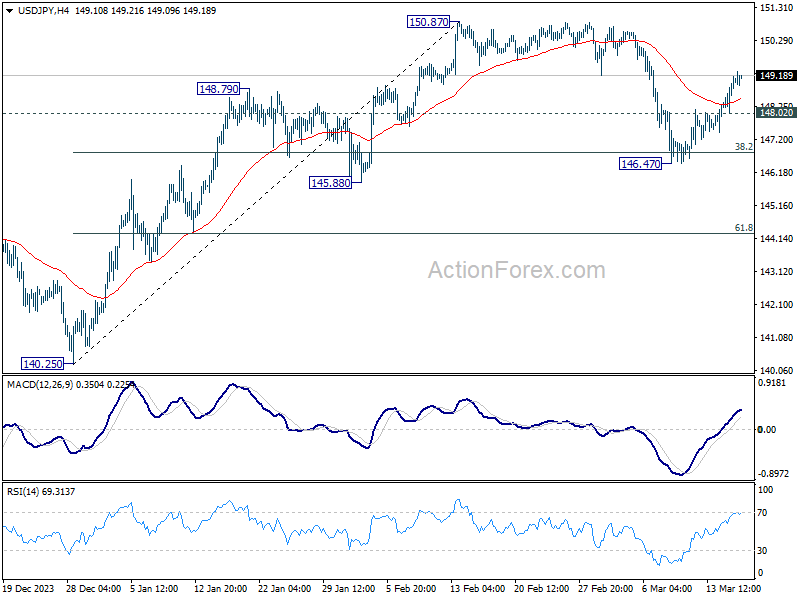

USD/JPY Daily Outlook

Daily Pivots: (S1) 148.34; (P) 148.75; (R1) 149.47; More...

Intraday bias in USD/JPY remains on the upside for the moment. Corrective fall from 150.87 should have completed at 146.47, after drawing support from 38.2% retracement of 140.25 to 150.87 at 146.81. Further rally should be seen to 150.87/89 key resistance zone. Nevertheless, on the downside, below 148.02 minor support will turn intraday bias neutral first.

In the bigger picture, no change in the view that price action from 151.89 (2023 high) are correction to up trend from 127.20 (2023 low). The question is whether this correction has completed at 140.25, or extending with fall from 150.87 as the third leg. Sustained break of above mentioned 146.81 fibonacci level will favor the latter case. But even so, downside should be contained by 50% retracement of 127.20 to 151.89 at 139.54