Sample Category Title

RBA stands pat, not ruling anything in or out

RBA has opted to maintain cash rate target unchanged at 4.35% today, aligning with broad market expectations. The central bank's stance reflects a cautious approach, emphasizing the prevailing uncertainty in both the global and domestic economic environments. RBA's declaration that the path of interest rates remains "uncertain" and that it is "not ruling anything in or out" underscores a flexible policy outlook, leaving the door open for rate adjustments in the future, including the possibility of further hikes.

On the inflation front, RBA acknowledges a moderating trend, consistent with its latest forecasts. This moderation is attributed primarily to slowdown in goods inflation. However, services inflation remains stubbornly high, and ism ode rating at a slower pace. Wages growth, a critical factor in the inflation equation, appears to have peaked.

Addressing the economic outlook, RBA paints a picture of significant uncertainty. Internationally, questions loom over China's economic outlook and the broader impacts of geopolitical conflicts in Ukraine and the Middle East. Domestically, uncertainties pertain to the lag effects of monetary policy adjustments, firms' pricing decisions, wages dynamics, and household consumption patterns.

(RBA) Statement by Michele Bullock, Governor: Monetary Policy Decision

At its meeting today, the Board decided to leave the cash rate target unchanged at 4.35 per cent and the interest rate paid on Exchange Settlement balances unchanged at 4.25 per cent.

Inflation continues to moderate but remains high.

Recent information suggests that inflation continues to moderate, in line with the RBA's latest forecasts. The headline monthly CPI indicator was steady at 3.4 per cent over the year to January, with momentum easing over recent months, driven by moderating goods inflation. Services inflation remains elevated, and is moderating at a more gradual pace. The data are consistent with continuing excess demand in the economy and strong domestic cost pressures, both for labour and non-labour inputs.

Higher interest rates are working to establish a more sustainable balance between aggregate demand and supply in the economy. Accordingly, conditions in the labour market continue to ease gradually, although they remain tighter than is consistent with sustained full employment and inflation at target. Wages growth picked up a little further in the December quarter, but appears to have peaked with indications it will moderate over the year ahead. Nevertheless, this level of wages growth remains consistent with the inflation target only on the assumption that productivity growth increases to around its long-run average. Inflation is still weighing on people's real incomes and household consumption growth is weak, as is dwelling investment.

The outlook remains highly uncertain.

While there are encouraging signs that inflation is moderating, the economic outlook remains uncertain. The December quarter national accounts data confirmed growth has slowed. Household consumption growth remains particularly weak amid high inflation and the rise in interest rates. After recent declines, real incomes have stabilised and are expected to grow from here, which is expected to support growth in consumption later in the year.

Meanwhile, growth in unit labour costs remains very high. It has begun to moderate slightly as measured productivity growth has picked up in the past two quarters but whether this trend will be sustained is uncertain.

The central forecasts are for inflation to return to the target range of 2–3 per cent in 2025, and to the midpoint in 2026. Services price inflation is expected to decline gradually as demand moderates and growth in labour and non-labour costs eases. Employment is expected to continue to grow moderately, and the unemployment rate and the broader underutilisation rate are expected to increase a bit further.

While there have been favourable signs on goods price inflation abroad, services price inflation has remained persistent and the same could occur in Australia. There also remains a high level of uncertainty around the outlook for the Chinese economy and the implications of the conflicts in Ukraine and the Middle East. Domestically, there are uncertainties regarding the lags in the effect of monetary policy and how firms' pricing decisions and wages will respond to the slower growth in the economy at a time of excess demand, and while the labour market remains tight. The outlook for household consumption also remains uncertain.

Returning inflation to target is the priority.

Returning inflation to target within a reasonable timeframe remains the Board's highest priority. This is consistent with the RBA's mandate for price stability and full employment. The Board needs to be confident that inflation is moving sustainably towards the target range. To date, medium-term inflation expectations have been consistent with the inflation target and it is important that this remains the case.

While recent data indicate that inflation is easing, it remains high. The Board expects that it will be some time yet before inflation is sustainably in the target range. The path of interest rates that will best ensure that inflation returns to target in a reasonable timeframe remains uncertain and the Board is not ruling anything in or out. The Board will rely upon the data and the evolving assessment of risks. The Board will continue to pay close attention to developments in the global economy, trends in domestic demand, and the outlook for inflation and the labour market. The Board remains resolute in its determination to return inflation to target.

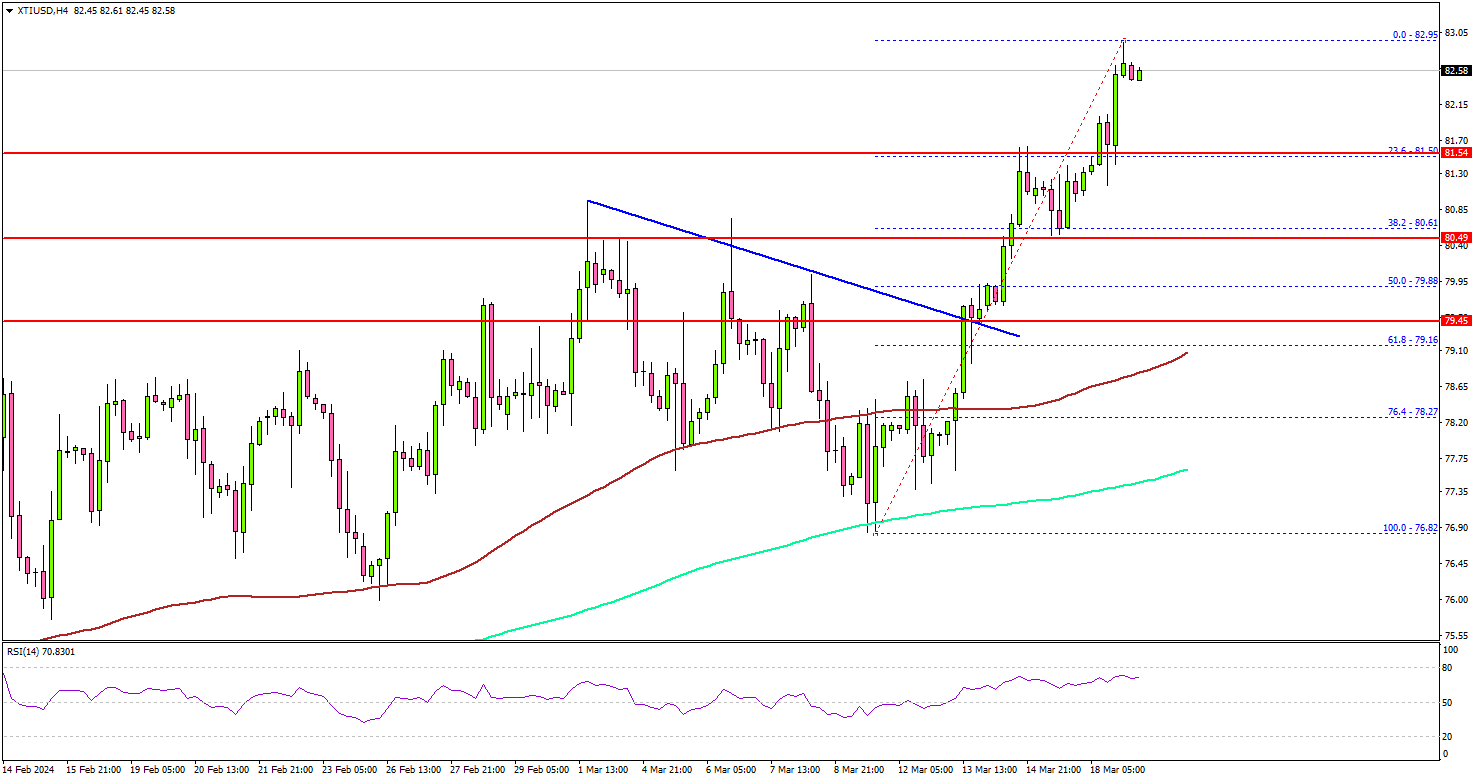

Crude Oil Price Reclaims $80, Can Bulls Push It To $85?

Key Highlights

- Crude oil bulls are eyeing an upside break above the $82.80 resistance.

- There was a break above a major bearish trend line with resistance at $79.45 on the 4-hour chart.

- Gold prices started a downside correction from the $2,195 zone.

- Bitcoin struggled above $72,000 and corrected below $70,000.

Crude Oil Price Technical Analysis

After forming a base above the $76.80 level, Crude oil prices started a fresh increase. The bulls pushed the price above the $80.00 resistance zone.

Looking at the 4-hour chart of XTI/USD, there was a break above a major bearish trend line with resistance at $79.45. The price settled above the $80.00 level, the 200 simple moving average (green, 4-hour), and the 100 simple moving average (red, 4-hour).

The price tested the $82.80 resistance and recently started a consolidation phase. The current price action suggests a high chance of more upsides above $82.80.

On the upside, the price is facing hurdles near the $82.80 level. The next major resistance is near the $83.00 zone, above which the price may perhaps accelerate higher. In the stated case, it could even visit the $85.00 resistance.

If not, the price might correct lower and test the $80.80 support. The first major support on the downside is near the $80.00 level. The next major support is at $79.40, below which the price might test the 100 simple moving average (red, 4-hour). Any more losses might send oil prices toward $78.00.

Looking at Gold, the price started a downside correction below the $2,165 level and might even test the $2,120 support.

Economic Releases to Watch Today

- Canadian Consumer Price Index for Feb 2024 (MoM) – Forecast +0.6%, versus 0% previous.

- Canadian Consumer Price Index for Feb 2024 (YoY) – Forecast +3.1%, versus +2.9% previous.

AUD: Markets Prepare for RBA Rates Statement.

The Reserve Bank of Australia (RBA) is widely anticipated to maintain its current interest rates at 4.35% following its two-day meeting concluding on Tuesday. Despite holding rates steady since December, the RBA has hinted at the possibility of further rate hikes due to persistently high inflation, which has exceeded its target range of 2% to 3%. During its February meeting, some RBA members advocated for a 25 basis points increase in interest rates. While the RBA is not expected to raise rates in March, it is likely to maintain a hawkish stance due to concerns about inflation. Analysts predict that the RBA may wait until inflation moderates within its target range, which they expect to occur in the September quarter of 2024. However, the RBA's hawkishness may be constrained by a cooling Australian economy, as evidenced by sluggish GDP growth in the December quarter.

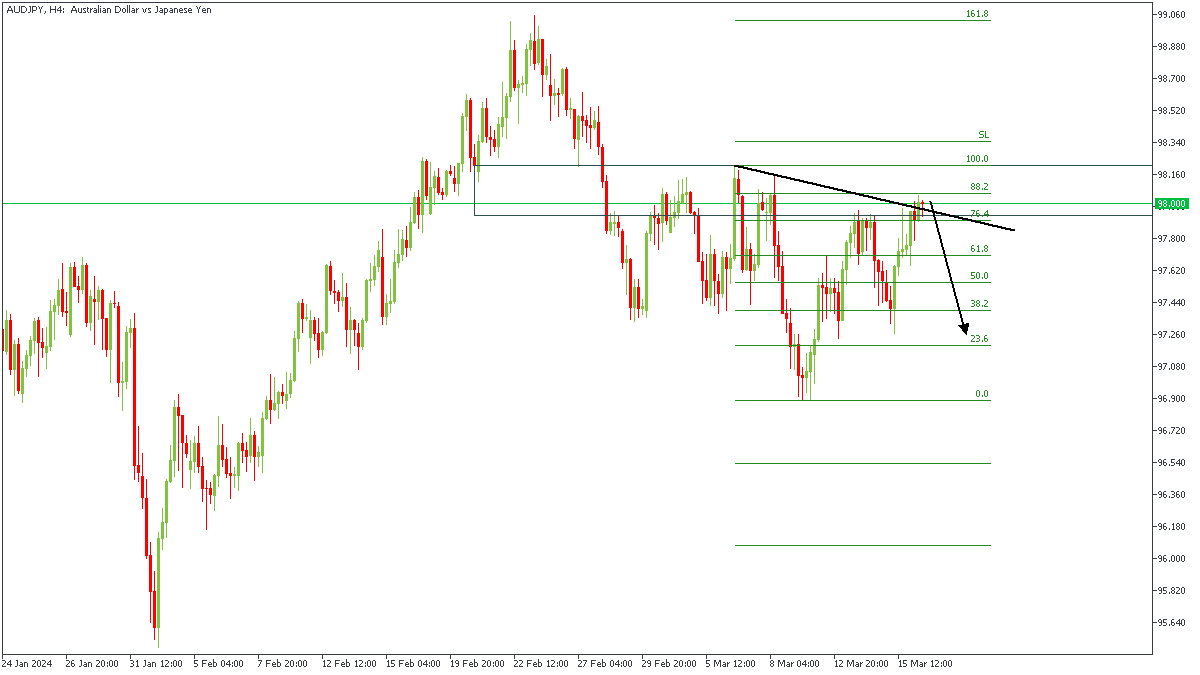

AUDJPY - H4 Timeframe

At the moment, on the H4 timeframe of AUDJPY, we see price currently riding into the trendline resistance and the 88% Fibonacci retracement level. Also, there is a pivot zone from the daily timeframe being respected by the current price action - which leads me to expect a bearish impulse from the aftermath of the rates decision.

Analyst’s Expectations:

- Direction: Bearish

- Target: 97.215

- Invalidation: 98.231

AUDNZD - D1 Timeframe

On the Daily timeframe of AUDNZD, we can see price approaching the 88% of the Fibonacci retracement level, as well as the trendline resistance. The market structure also appears clearly bearish. All of these factors point to a possible bearish impulse following the rate statement release.

Analyst’s Expectations:

- Direction: Bearish

- Target: 1.06373

- Invalidation: 1.08365

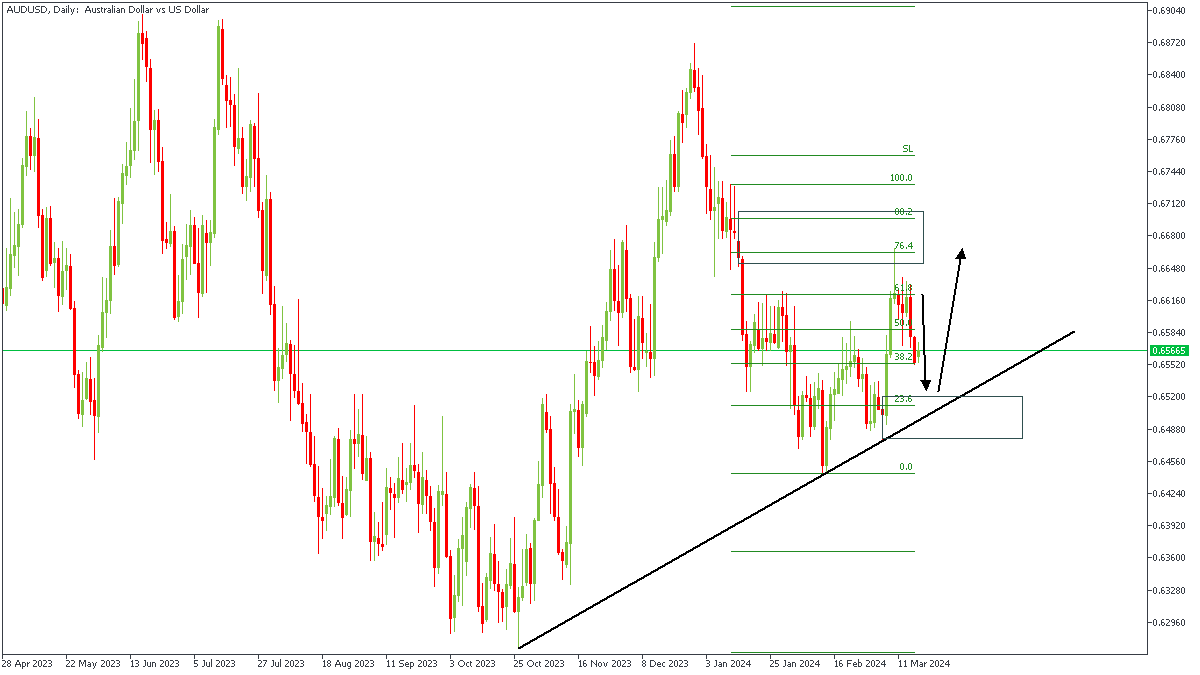

AUDUSD - D1 Timeframe

In line with the analysis last week, we’ve seen good movement from the bearish momentum on AUDUSD, but I believe we may see a change in the market direction shortly. From the chart we can see the price action currently approaching the trendline support and the demand zone. The outcome of the RBA’s rate statement could provide just the right motivation to turn the direction of the market around.

Analyst’s Expectations:

- Direction: Bullish

- Target: 0.66611

- Invalidation: 0.64779

CONCLUSION

The trading of CFDs comes at a risk. Thus, to succeed, you have to manage risks properly. To avoid costly mistakes while you look to trade these opportunities, be sure to do your due diligence and manage your risk appropriately.

BOJ Policy Rate – USDJPY Technical Analysis

BOJ Policy Rate

The Bank of Japan is scheduled to announce its Policy Rate, Monetary Policy Statement, and BOJ Press Conference. Japan has held its interest rates at record-low levels for almost 17 years. The current interest rate is—0.10%, and according to Bloomberg analysts’ surveys, the BOJ is expected to maintain this level for the March 2024 BOJ meeting. Japan’s economy endured two decades of deflationary pressure, with the post-COVID inflation rate rising globally; Japan’s CPI Nationwide YoY, a measure of the inflation rate, crossed above the zero level in late 2021, reaching a high of 4.26% in January 2023. This was followed by a decline as the inflationary pressure eased globally. The current inflation rate in Japan stands at 2.2%, slightly above BOJ’s target of 2%. Japan’s most important union group announced stronger-than-expected annual wage deals on Friday, thus adding weight to BOJ rate hike odds.

According to the Bloomberg World Interest Rate Probability Model, it is estimated that markets have priced in a 56.1% chance of a 0.056% hike, bringing the current Implied O/N Rate up from -0.009% up to 0.047%. In another poll by Reuters, just under two-thirds of economists polled by Reuters expect the BOJ to end negative rates in April. Japan’s CPI YoY contribution breakdown shows that the decline is reflected in almost all categories, including food, fuel, and utilities, while the only noticeable increase was in the Recreation and Culture Services sector.

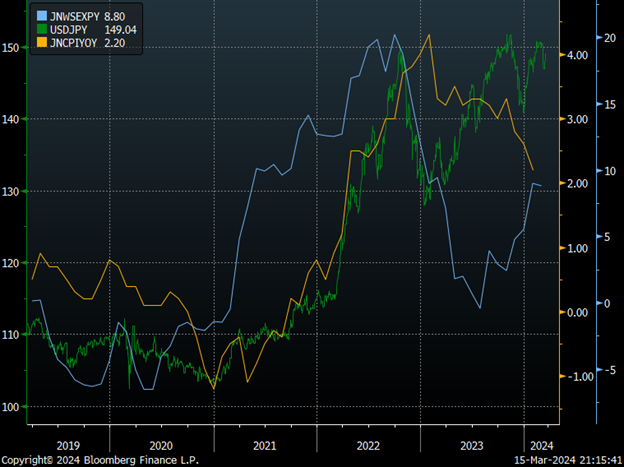

Source: Bloomberg Terminal

Exports mainly drive Japan’s economy, and the yen’s value against the US Dollar can significantly affect overall economic performance. The above chart shows the correlation between Japan’s export price index JNWSEXPY (Blue line) and USDJPY (Green bars), while the yellow line represents Japan’s CPI – JNCPIYOY. The recent increase in the export index is not in line with inflation and was possibly driven by a weak yen, which may be undervalued, thus less of a negative impact on Japan’s economy in case of a BOJ hike.

4 – Hour Chart

Source: Tradingview.com

- Price action was trading in an uptrend (Trendline1), followed by flag formation.

- Price broke out above the flag formation and resumed its uptrend (Trendline2), followed by a range trading pattern. Price action broke below the trading range and is currently in a pullback mode, finding resistance below the breakout level (the lower border of the trading range); the same level was a resistance in early Feb 2024. (Yellow ellipse)

- Price is trading above its fast and intermediate moving averages, EMA9, MA9, and MA21; the intersection of the three averages may represent a confluence of support if the price fails to reenter the broken trading range.

- The fast RSI is at the overbought level and in line with price action, while the smoothed RSI points down after reaching level 66, just below overbought.

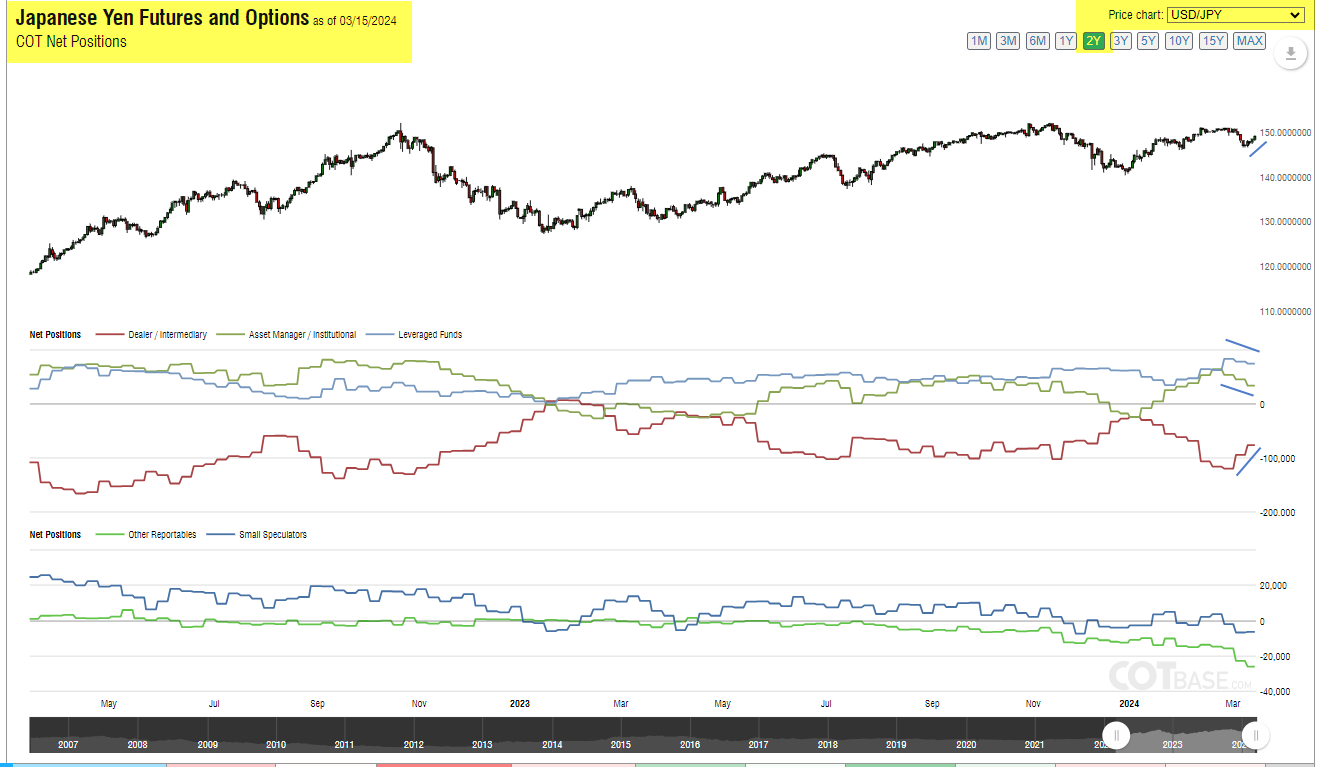

Commitment of Traders Report

Source: Cotbase.com

The COT report for the week ending on March 15th, 2024 (Includes data up to the end of day Tuesday, March 12th, 2024) reflects the three TIFF report categories, Asset Manager/Institution, Leveraged Funds, and Dealer/Intermediary, all reflect negative divergence with price action. (Image flipped to USDJPY)

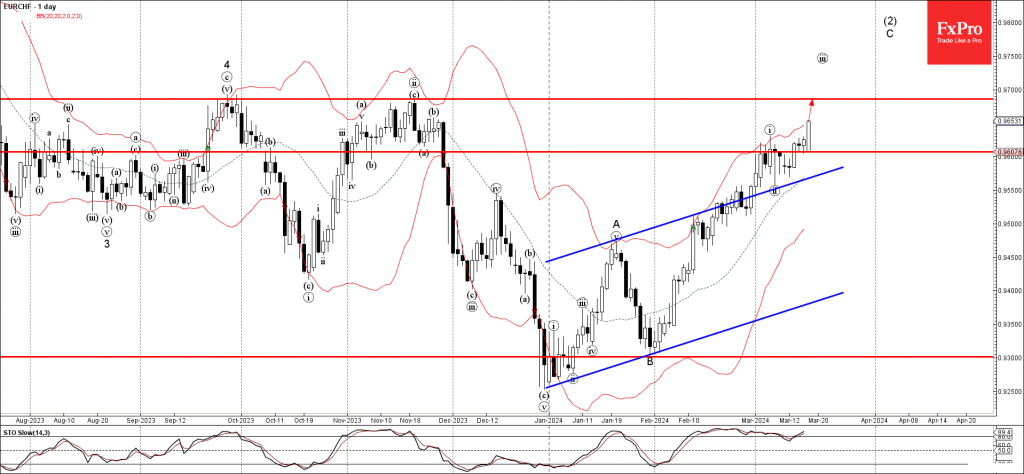

EURCHF Wave Analysis

- EURCHF under bullish pressure

- Likely to rise to resistance level 0.968

EURCHF under the bullish pressure after the pair broke the key resistance level 0.9600 (which stopped the previous impulse wave i at the start of March).

The breakout of the resistance level 0.9600 accelerated the C-wave of the active intermediate ABC correction (2) from the end of December.

Given the clear daily uptrend and strong Swiss franc sales, EURCHF currency pair can be expected to rise further toward the next resistance level 0.9685 (earlier monthly high from September and November).

Sunset Market Commentary

Markets

US Treasuries hold near last week’s sell-off lows in an uneventful trading session awaiting major central bank decisions. US yield currently trade up to 1.5 bps higher across the curve with both the US 2-yr and 10-yr yield testing the YTD highs at 4.74% and at 4.34%. German Bunds face some similar minor selling pressure (German yields up to 2 bps higher). Ahead of Wednesday’s FOMC meeting, the ECB holds its annual Watchers conference with a lot of prominent ECB speeches including by ECB president Lagarde. We expect Wednesday to highlight the difference between the ECB readying a June policy rate and the Fed delaying such action until September by the earliest. EUR/USD holds below 1.09 with the above scenario suggestion room for decline towards the YTD low at 1.0695. USD/JPY is heading back towards 150 (149.25) even as the BoJ could tomorrow morning conduct a first rate hike since 2007. A stronger USD and the expectation that BoJ action, if any, will be very slow and gradual holds back JPY. EUR/GBP (0.8550) is going nowhere ahead of tomorrow’s CPI inflation figures and Thursday’s BoE policy meeting. US stock markets overcome Friday’s weakness, with key indices up to 1.7% (!) higher (Nasdaq) with Apple and Alphabet driving the move on a report of AI talks.

News & Views

The EMU goods trade surplus with the rest of the world printed at €11.4bn in January compared to a deficit of €32.6bn in January last year. EMU goods exports increased by 1.3% Y/Y to €225.9bn. Imports from the rest of the world stood at €214.5 bn, a fall by 16.1% Y/Y. A breakdown by product shows that the overall surplus is mainly driven by a surplus in the chemical sector, followed by machinery and vehicles. These developments are partly offset by a deficit in the energy sector. However, as a trend the energy deficit declined throughout 2024. On a seasonally adjusted basis, the EMU surplus even hit a record high in January 2024. Over the calendar year 2023, the EMU recorded a surplus of €64bn, compared with a deficit of €335bn in 2022. The euro area exports of goods to the rest of the world stood at €2841.7bn (a decrease of 1.1% compared to 2022), while imports fell to €2777.7bn (a decrease of 13.4% compared to the year 2022). Intra-euro area trade fell to €2630.8bn in the year 2023, down by 5.1% compared to the year 2022.

The National Bank of Poland’s core inflation data showed a further decrease in February, though largely as expected. Prices excluding food and energy prices printed at 0.5% M/M and 5.4% Y/Y, compared to 0.4% M/M and 6.2% Y/Y in January. CPI excluding administered prices rose 0.3% M/M and 2.8% Y/Y (from 0.2% M/M and 3.8%Y/Y). CPI excluding most volatile items slowed to 0.2% M/M and 4.5% Y/Y (from 0.5% M/M and 5.8% Y/Y). Earlier this month, the Polish statistical office reported headline Polish CPI easing to 0.3% M/M and 2.8% Y/Y and bringing it back within the NBP target range of 2.5% +/- 1.0%. However, core inflation staying above the headline measure and uncertainty on the impact of fiscal policy/phasing out measures to cap food and energy prices, makes the majority of the MPC cautious to give guidance on any further rate cuts in the foreseeable future. Several members even see little room to cut the policy rate this year. The zloty recently ran into resistance after touching the strongest level since 2020 earlier this month. EUR/PLN trades near 4.3125, compared to a PLN YTD at EUR/PLN 4.275 last week.

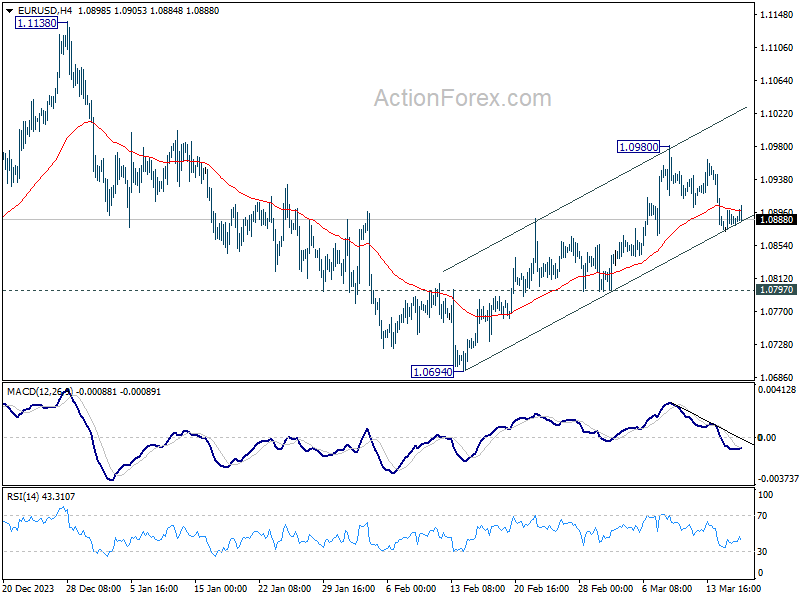

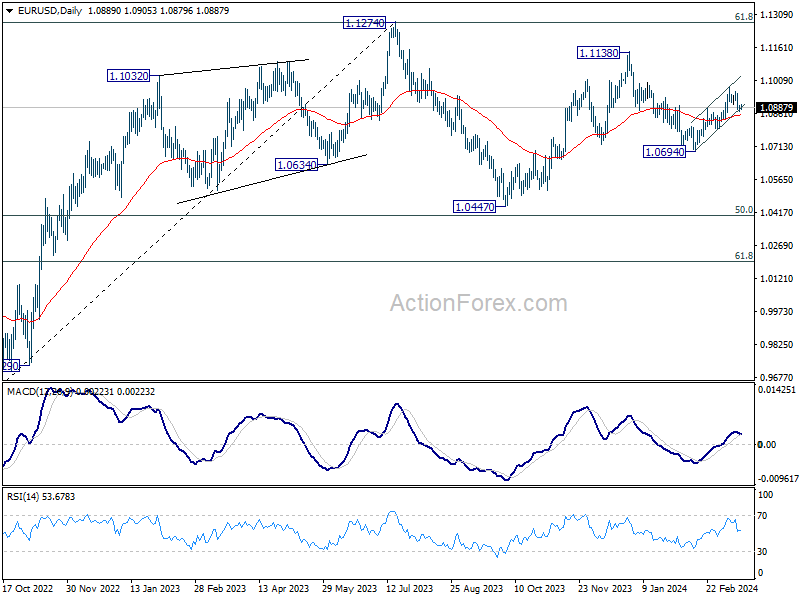

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0873; (P) 1.0887; (R1) 1.0900; More...

No change in EUR/USD and intraday bias stays on the downside. Fall from 1.0980 short term top would target 55 D EMA (now at 1.0856). Sustained break there will argue that rebound from 1.0694 has completed and bring retest of this low. For now, risk will stay on the downside as long as 1.0980 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

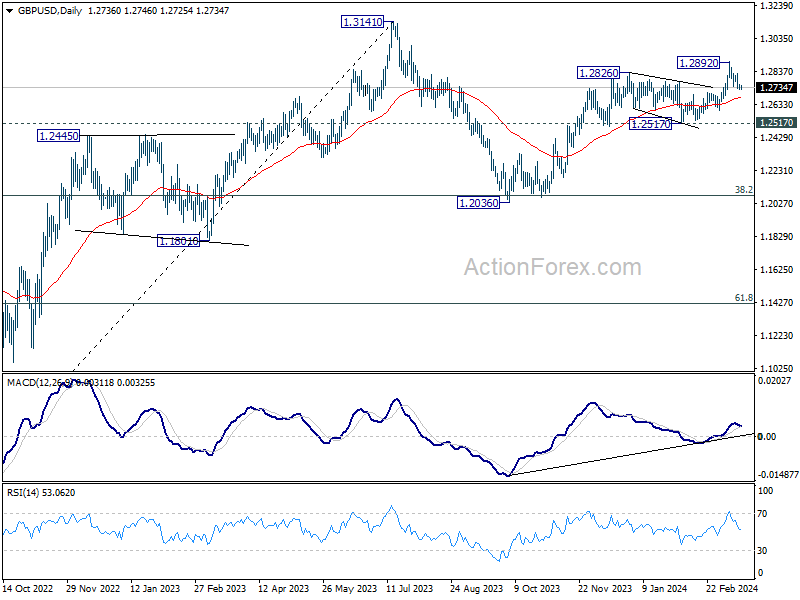

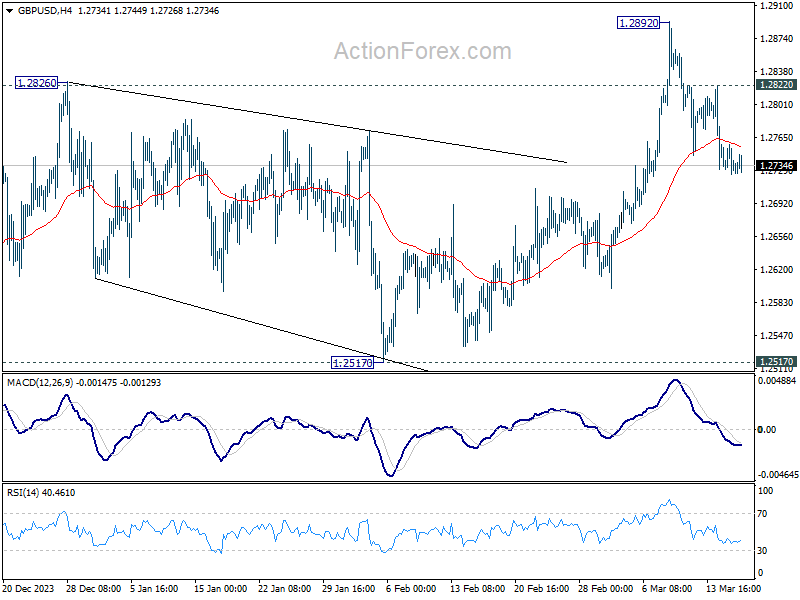

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2721; (P) 1.2741; (R1) 1.2755; More...

No change in GBP/USD's outlook as fall from 1.2892 short term top is in progress. Deeper decline would be seen to 55 D EMA (now at 1.2673). Firm break there will target .2517 structural support. For now, risk will stay mildly on the downside as long as 1.2822 minor resistance holds, in case of recovery.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which is still in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2517 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.