Sample Category Title

BOJ Policy Rate – USDJPY Technical Analysis

BOJ Policy Rate

The Bank of Japan is scheduled to announce its Policy Rate, Monetary Policy Statement, and BOJ Press Conference. Japan has held its interest rates at record-low levels for almost 17 years. The current interest rate is—0.10%, and according to Bloomberg analysts’ surveys, the BOJ is expected to maintain this level for the March 2024 BOJ meeting. Japan’s economy endured two decades of deflationary pressure, with the post-COVID inflation rate rising globally; Japan’s CPI Nationwide YoY, a measure of the inflation rate, crossed above the zero level in late 2021, reaching a high of 4.26% in January 2023. This was followed by a decline as the inflationary pressure eased globally. The current inflation rate in Japan stands at 2.2%, slightly above BOJ’s target of 2%. Japan’s most important union group announced stronger-than-expected annual wage deals on Friday, thus adding weight to BOJ rate hike odds.

According to the Bloomberg World Interest Rate Probability Model, it is estimated that markets have priced in a 56.1% chance of a 0.056% hike, bringing the current Implied O/N Rate up from -0.009% up to 0.047%. In another poll by Reuters, just under two-thirds of economists polled by Reuters expect the BOJ to end negative rates in April. Japan’s CPI YoY contribution breakdown shows that the decline is reflected in almost all categories, including food, fuel, and utilities, while the only noticeable increase was in the Recreation and Culture Services sector.

Source: Bloomberg Terminal

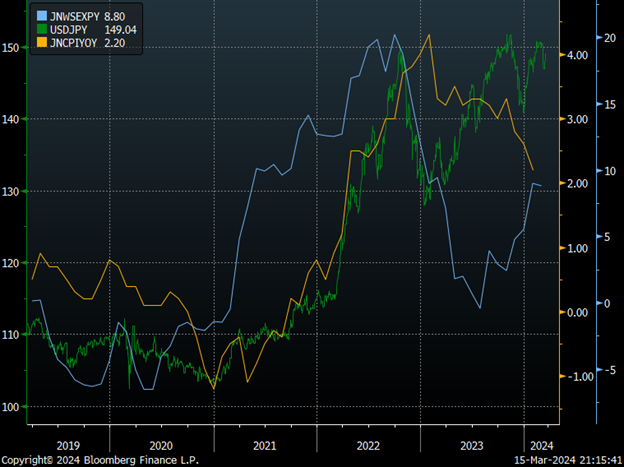

Exports mainly drive Japan’s economy, and the yen’s value against the US Dollar can significantly affect overall economic performance. The above chart shows the correlation between Japan’s export price index JNWSEXPY (Blue line) and USDJPY (Green bars), while the yellow line represents Japan’s CPI – JNCPIYOY. The recent increase in the export index is not in line with inflation and was possibly driven by a weak yen, which may be undervalued, thus less of a negative impact on Japan’s economy in case of a BOJ hike.

4 – Hour Chart

Source: Tradingview.com

- Price action was trading in an uptrend (Trendline1), followed by flag formation.

- Price broke out above the flag formation and resumed its uptrend (Trendline2), followed by a range trading pattern. Price action broke below the trading range and is currently in a pullback mode, finding resistance below the breakout level (the lower border of the trading range); the same level was a resistance in early Feb 2024. (Yellow ellipse)

- Price is trading above its fast and intermediate moving averages, EMA9, MA9, and MA21; the intersection of the three averages may represent a confluence of support if the price fails to reenter the broken trading range.

- The fast RSI is at the overbought level and in line with price action, while the smoothed RSI points down after reaching level 66, just below overbought.

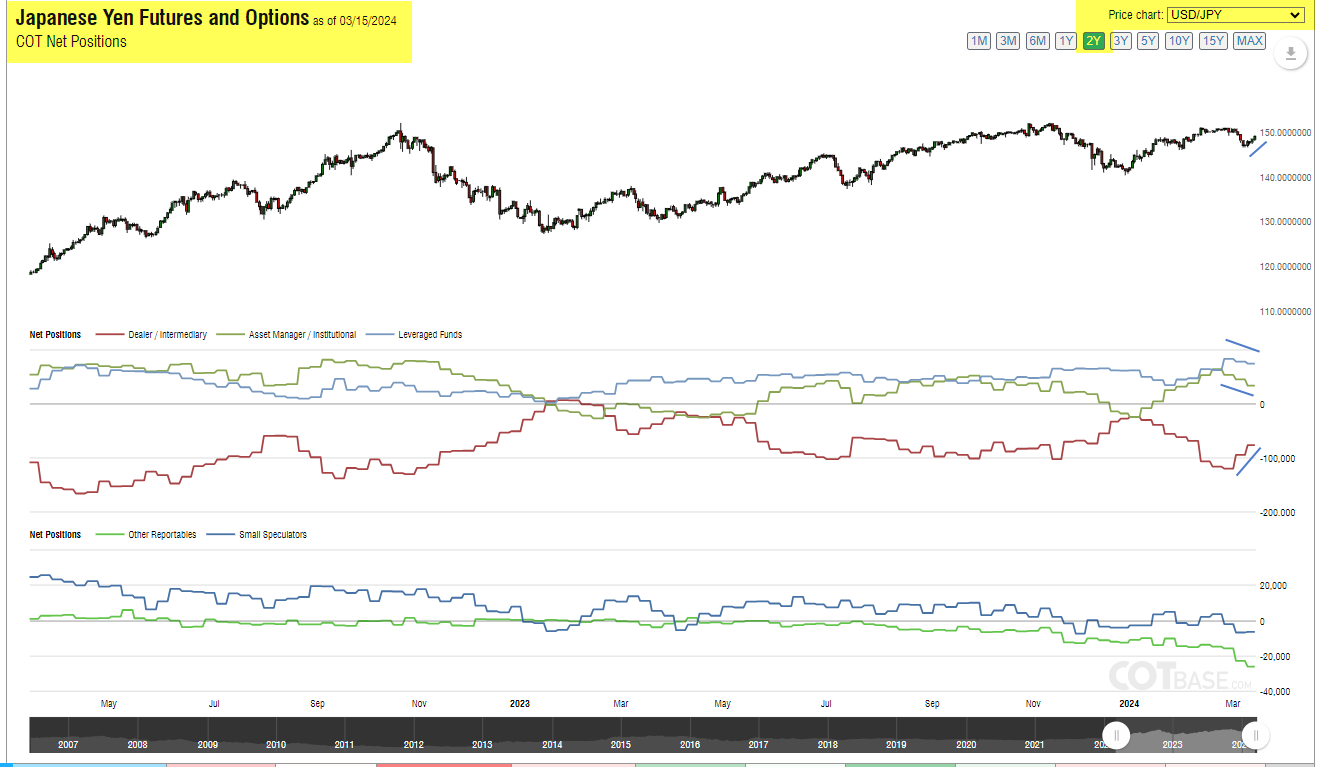

Commitment of Traders Report

Source: Cotbase.com

The COT report for the week ending on March 15th, 2024 (Includes data up to the end of day Tuesday, March 12th, 2024) reflects the three TIFF report categories, Asset Manager/Institution, Leveraged Funds, and Dealer/Intermediary, all reflect negative divergence with price action. (Image flipped to USDJPY)

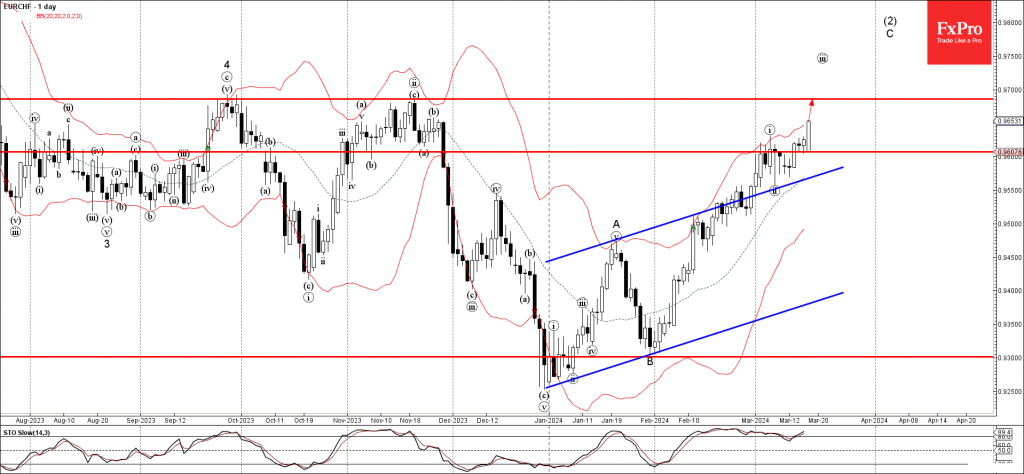

EURCHF Wave Analysis

- EURCHF under bullish pressure

- Likely to rise to resistance level 0.968

EURCHF under the bullish pressure after the pair broke the key resistance level 0.9600 (which stopped the previous impulse wave i at the start of March).

The breakout of the resistance level 0.9600 accelerated the C-wave of the active intermediate ABC correction (2) from the end of December.

Given the clear daily uptrend and strong Swiss franc sales, EURCHF currency pair can be expected to rise further toward the next resistance level 0.9685 (earlier monthly high from September and November).

Sunset Market Commentary

Markets

US Treasuries hold near last week’s sell-off lows in an uneventful trading session awaiting major central bank decisions. US yield currently trade up to 1.5 bps higher across the curve with both the US 2-yr and 10-yr yield testing the YTD highs at 4.74% and at 4.34%. German Bunds face some similar minor selling pressure (German yields up to 2 bps higher). Ahead of Wednesday’s FOMC meeting, the ECB holds its annual Watchers conference with a lot of prominent ECB speeches including by ECB president Lagarde. We expect Wednesday to highlight the difference between the ECB readying a June policy rate and the Fed delaying such action until September by the earliest. EUR/USD holds below 1.09 with the above scenario suggestion room for decline towards the YTD low at 1.0695. USD/JPY is heading back towards 150 (149.25) even as the BoJ could tomorrow morning conduct a first rate hike since 2007. A stronger USD and the expectation that BoJ action, if any, will be very slow and gradual holds back JPY. EUR/GBP (0.8550) is going nowhere ahead of tomorrow’s CPI inflation figures and Thursday’s BoE policy meeting. US stock markets overcome Friday’s weakness, with key indices up to 1.7% (!) higher (Nasdaq) with Apple and Alphabet driving the move on a report of AI talks.

News & Views

The EMU goods trade surplus with the rest of the world printed at €11.4bn in January compared to a deficit of €32.6bn in January last year. EMU goods exports increased by 1.3% Y/Y to €225.9bn. Imports from the rest of the world stood at €214.5 bn, a fall by 16.1% Y/Y. A breakdown by product shows that the overall surplus is mainly driven by a surplus in the chemical sector, followed by machinery and vehicles. These developments are partly offset by a deficit in the energy sector. However, as a trend the energy deficit declined throughout 2024. On a seasonally adjusted basis, the EMU surplus even hit a record high in January 2024. Over the calendar year 2023, the EMU recorded a surplus of €64bn, compared with a deficit of €335bn in 2022. The euro area exports of goods to the rest of the world stood at €2841.7bn (a decrease of 1.1% compared to 2022), while imports fell to €2777.7bn (a decrease of 13.4% compared to the year 2022). Intra-euro area trade fell to €2630.8bn in the year 2023, down by 5.1% compared to the year 2022.

The National Bank of Poland’s core inflation data showed a further decrease in February, though largely as expected. Prices excluding food and energy prices printed at 0.5% M/M and 5.4% Y/Y, compared to 0.4% M/M and 6.2% Y/Y in January. CPI excluding administered prices rose 0.3% M/M and 2.8% Y/Y (from 0.2% M/M and 3.8%Y/Y). CPI excluding most volatile items slowed to 0.2% M/M and 4.5% Y/Y (from 0.5% M/M and 5.8% Y/Y). Earlier this month, the Polish statistical office reported headline Polish CPI easing to 0.3% M/M and 2.8% Y/Y and bringing it back within the NBP target range of 2.5% +/- 1.0%. However, core inflation staying above the headline measure and uncertainty on the impact of fiscal policy/phasing out measures to cap food and energy prices, makes the majority of the MPC cautious to give guidance on any further rate cuts in the foreseeable future. Several members even see little room to cut the policy rate this year. The zloty recently ran into resistance after touching the strongest level since 2020 earlier this month. EUR/PLN trades near 4.3125, compared to a PLN YTD at EUR/PLN 4.275 last week.

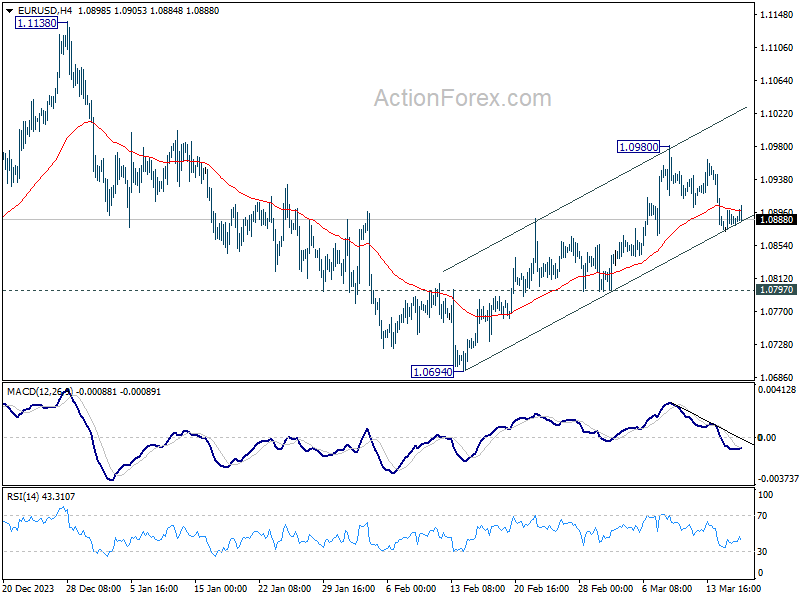

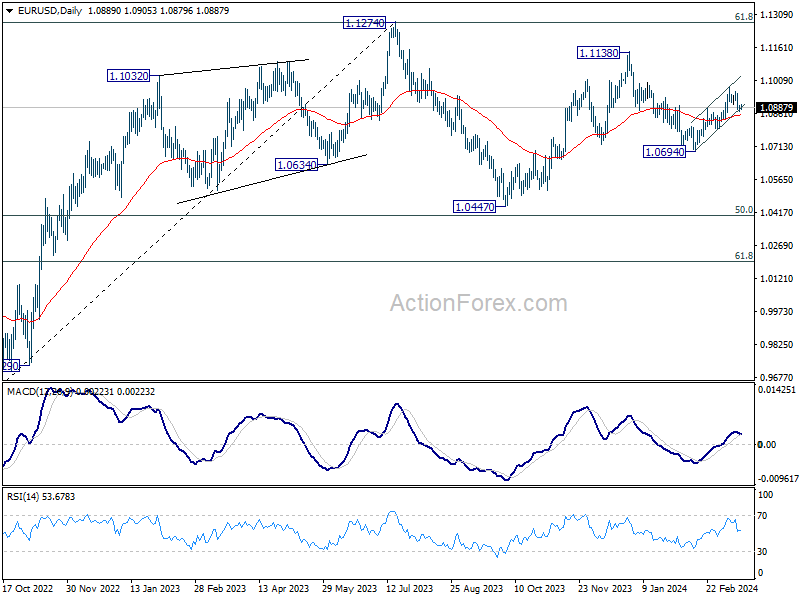

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0873; (P) 1.0887; (R1) 1.0900; More...

No change in EUR/USD and intraday bias stays on the downside. Fall from 1.0980 short term top would target 55 D EMA (now at 1.0856). Sustained break there will argue that rebound from 1.0694 has completed and bring retest of this low. For now, risk will stay on the downside as long as 1.0980 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

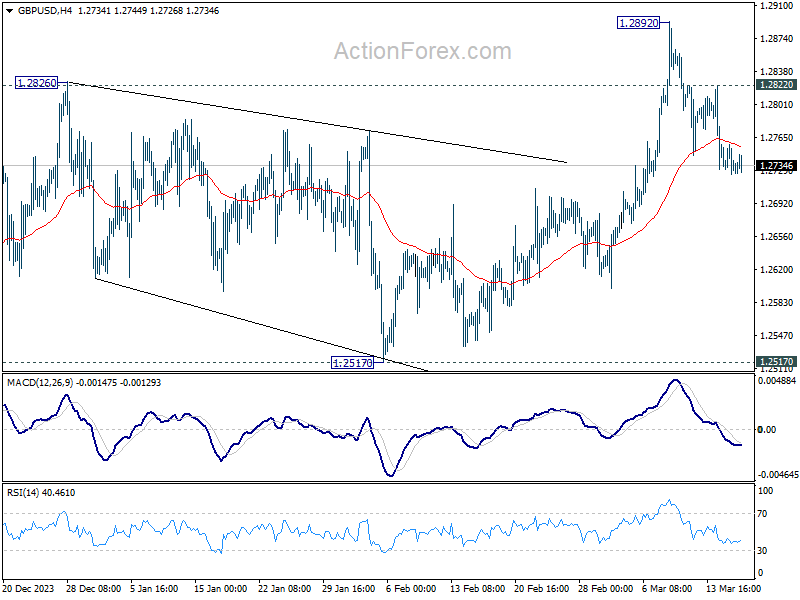

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2721; (P) 1.2741; (R1) 1.2755; More...

No change in GBP/USD's outlook as fall from 1.2892 short term top is in progress. Deeper decline would be seen to 55 D EMA (now at 1.2673). Firm break there will target .2517 structural support. For now, risk will stay mildly on the downside as long as 1.2822 minor resistance holds, in case of recovery.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which is still in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2517 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

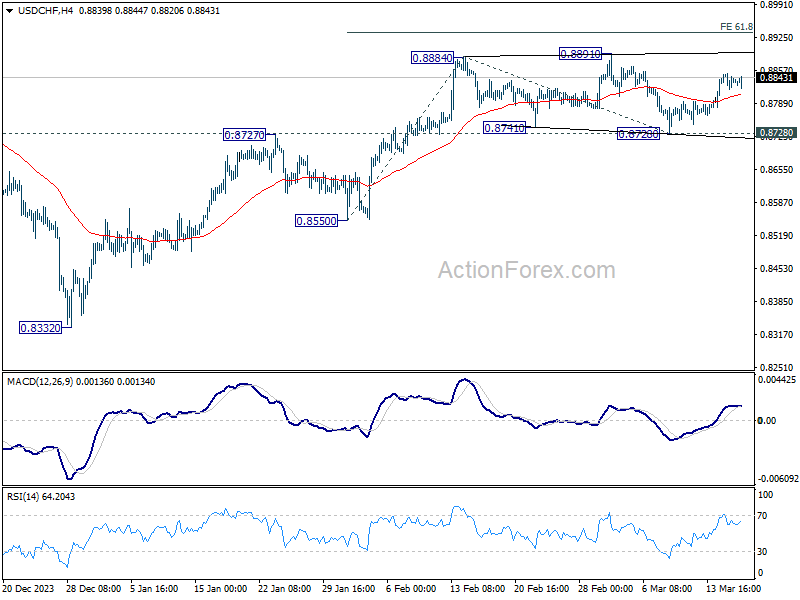

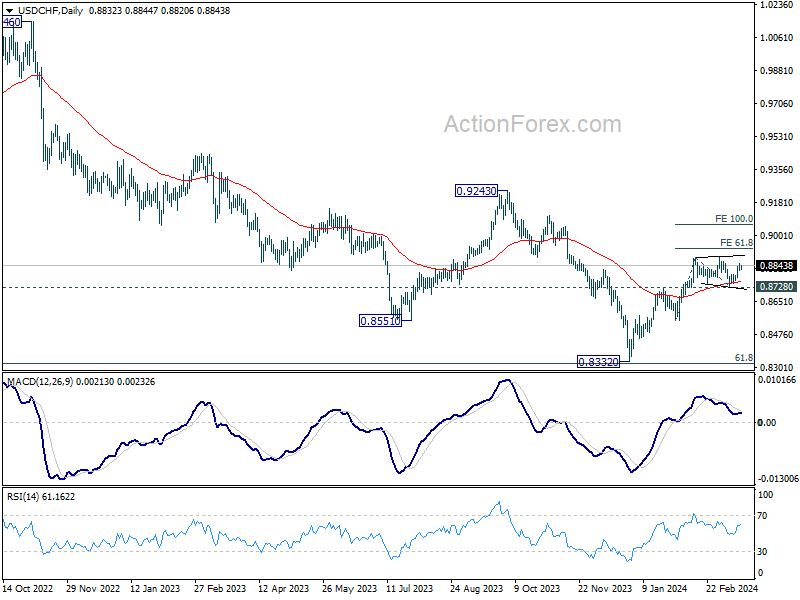

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8818; (P) 0.8836; (R1) 0.8852; More....

No change in USD/CHF's outlook and intraday bias stays mildly on the upside. As noted before, consolidation from 0.8884 should have completed with three waves to 0.8728. Further rally should be seen to retest 0.8891 resistance first. Firm break there will resume whole rally from 0.8332. Next target is 61.8% projection of 0.8550 to 0.8884 from 0.8728 at 0.8934. For now, this will remain the favored case as long as 0.8728 support holds, in case of retreat.

In the bigger picture, price actions from 0.8332 medium term bottom as seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8555 support holds. But upside should be limited by 0.9243 resistance, at least on first attempt.

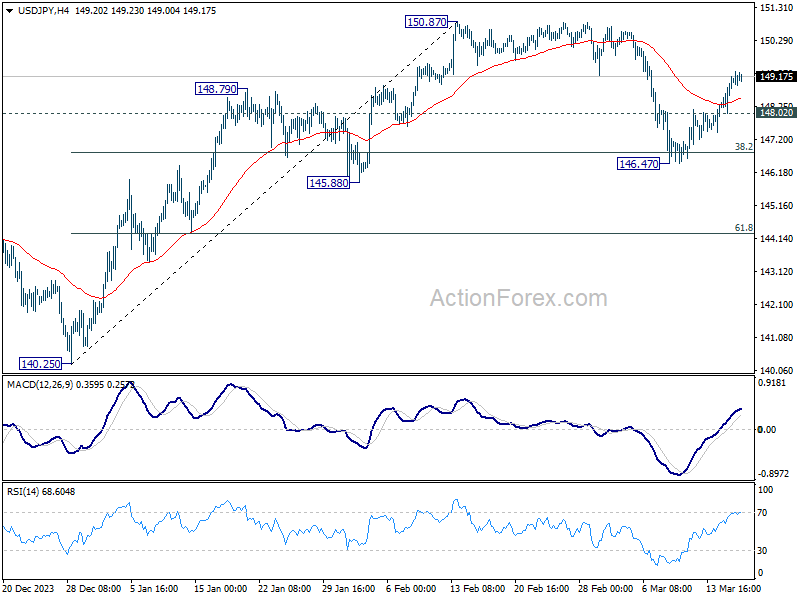

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 148.34; (P) 148.75; (R1) 149.47; More...

USD/JPY's rebound from 146.47 is still in progress and intraday bias stays on the upside. Corrective fall from 150.87 should have completed at 146.47, after drawing support from 38.2% retracement of 140.25 to 150.87 at 146.81. Further rally should be seen to 150.87/89 key resistance zone. Nevertheless, on the downside, below 148.02 minor support will turn intraday bias neutral first.

In the bigger picture, no change in the view that price action from 151.89 (2023 high) are correction to up trend from 127.20 (2023 low). The question is whether this correction has completed at 140.25, or extending with fall from 150.87 as the third leg. Sustained break of above mentioned 146.81 fibonacci level will favor the latter case. But even so, downside should be contained by 50% retracement of 127.20 to 151.89 at 139.54

Yen on the Brink as Markets Await BoJ

Yen's continued weakness persists in today's subdued market, despite growing expectations for a BoJ rate hike in the upcoming Asian session—a move anticipated to conclude its longstanding negative rates policy. Although the anticipated adjustment from -0.10% to 0.00% may seem minor, its symbolic significance for the Japanese economy is profound, as it heralds a new era of monetary policy.

Recent reports underscore the momentum building towards this policy shift. A Reuters article highlighted a source's comments on the robust wage increases by large enterprises, setting a positive precedent for smaller companies. Recent wages increase is seen as a catalyst for boosting consumption, stimulating demand and prices, suggesting BoJ might not need to defer action until April.

Conversations with CEOs, as reported by Bloomberg TV, reveal a readiness for an interest rate hike, regardless of whether it occurs in March or April, signifying a widespread acceptance of the impending policy change. Retailers also anticipate benefits from a stronger Yen, viewing it as a vital step towards normalizing inflation and the broader economy.

Yet, predicting BoJ's moves remains challenging, with the central bank known for its unpredictability. Thus, any surprises in the upcoming announcement would align with its historical pattern of unexpected decisions.

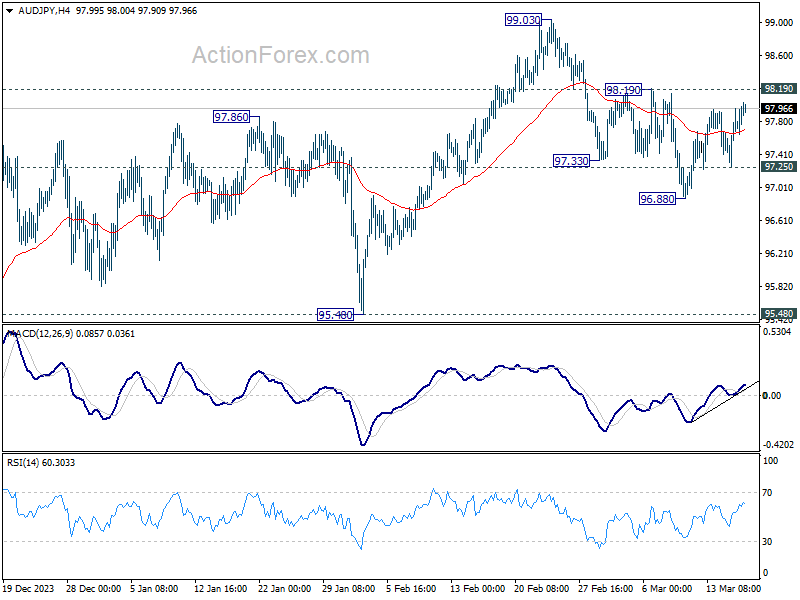

In the broader currency markets, Australian Dollar is the relatively stronger performer of the day, with New Zealand Dollar and Euro also showing mild strength. Dollar lags behind, positioned just ahead of Yen, followed closely by Swiss Franc. Sterling and the Canadian Dollar find themselves in a middle ground.

Technically, a main question is whether AUD/JPY's correction from 99.03 has completed with three waves down to 96.88 already. Decisive break of 98.19 will affirm this bullish case, and target 99.03 high next. However, break of 97.25 will indicate that fall from 99.03 is resuming through 96.88, towards 95.48 key support level. With BoJ and RBA poised to announce their rate decisions shortly, clarity on this technical query is imminent.

In Europe, at the time of writing, FTSE is up 0.19%. DAX is up 0.14%. CAC is up 0.05%. UK 10-year yield is down -0.0025 at 4.200. Germany 10-year yield is up 0.029 at 2.472. Earlier in Asia, Nikkei rose 2.67%. Hong Kong HSI rose 0.10%. China Shanghai SSE rose 0.99%. Singapore Strait Times fell -0.03%. Japan 10-year JGB yield fell -0.030 to 0.763.

Eurozone CPI finalized at 2.6% in Feb, core CPI at 3.1%

Eurozone CPI was finalized at 2.6% yoy in February, down from 2.8% yoy in January. CPI core (excluding energy, food, alcohol & tobacco) was finalized at 3.1% yoy, down from prior month's 3.3% yoy.

The highest contribution to the annual Eurozone inflation rate came from services (+1.73 percentage points, pp), followed by food, alcohol & tobacco (+0.79 pp), non-energy industrial goods (+0.42 pp) and energy (-0.36 pp).

EU CPI was finalized at 2.8% yoy. The lowest annual rates were registered in Latvia, Denmark (both 0.6%) and Italy (0.8%). The highest annual rates were recorded in Romania (7.1%), Croatia (4.8%) and Estonia (4.4%). Compared with January, annual inflation fell in twenty Member States, remained stable in five and rose in two.

NZ BNZ services rises to 53.0, signs of early and strong growth emerge

New Zealand's BusinessNZ Performance of Services Index climbed from 52.2 to 53.0 in February, marking its highest point since March 2023.

A closer examination of the index's components reveals a generally positive picture. Activity and sales maintained steady pace, inching slightly up from 53.0 to 53.1. Employment saw modest increase, moving closer to the expansionary threshold by rising from 48.3 to 49.1. Notably, new orders and business surged significantly from 52.4 to 56.0, the highest level recorded since December 2022.

The feedback from businesses highlighted persistent concerns, with the proportion of negative comments standing at 57.3% in February, a slight improvement from December's 58.7% but an increase from January's 53.0%. Businesses continue to identify the cost of living as the primary factor influencing activity, alongside the difficulties posed by the overall economic conditions.

BNZ's Head of Research Stephen Toplis said that "when we combine the PMI and PSI together to get an indicator of activity, there is a strong suggestion of growth returning later this year. The turnaround occurs a little stronger and earlier than we are forecasting but, whatever the case, it is a heartening sign".

China's industrial production expand 7% yoy, retail sales up 5.5% yoy

China's industrial production grew 7.0% yoy in the January-February period, above expectation of 5.3% yoy. During the same period, retail sales rose 5.5% yoy, below expectation 5.6% yoy.

Fixed asset investment rose 4.2% yoy, above expectation of 3.2% yoy. Investment into real estate fell by -9% yoy. Investment in infrastructure rose by 6.3% yoy while that in manufacturing increased by 9.4% yoy.

"The economy kept rebounding and improving in January and February with various policies taking effect. But we also need to see that the external environment is increasingly complex, grim and uncertain, and the problem of insufficient domestic demand still remains. The foundation for the economy's rebound needs to be further solidified," NBS said.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 148.34; (P) 148.75; (R1) 149.47; More...

USD/JPY's rebound from 146.47 is still in progress and intraday bias stays on the upside. Corrective fall from 150.87 should have completed at 146.47, after drawing support from 38.2% retracement of 140.25 to 150.87 at 146.81. Further rally should be seen to 150.87/89 key resistance zone. Nevertheless, on the downside, below 148.02 minor support will turn intraday bias neutral first.

In the bigger picture, no change in the view that price action from 151.89 (2023 high) are correction to up trend from 127.20 (2023 low). The question is whether this correction has completed at 140.25, or extending with fall from 150.87 as the third leg. Sustained break of above mentioned 146.81 fibonacci level will favor the latter case. But even so, downside should be contained by 50% retracement of 127.20 to 151.89 at 139.54

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ PSI Feb | 53 | 52.1 | 52.2 | |

| 23:50 | JPY | Machinery Orders M/M Jan | -1.70% | -0.70% | 2.70% | |

| 02:00 | CNY | Industrial Production Y/Y Feb | 7.00% | 5.30% | 6.80% | |

| 02:00 | CNY | Retail Sales Y/Y Feb | 5.50% | 5.60% | 7.40% | |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Feb | 4.20% | 3.20% | 3.00% | |

| 10:00 | EUR | Eurozone Trade Balance (EUR) Jan | 14.2B | 13.0B | ||

| 10:00 | EUR | Eurozone CPI Y/Y Feb F | 2.60% | 2.60% | ||

| 10:00 | EUR | Eurozone CPI Core Y/Y Feb F | 3.10% | 3.10% | ||

| 12:30 | CAD | Industrial Product Price M/M Feb | 0.00% | -0.10% | ||

| 12:30 | CAD | Raw Material Price Index Feb | 0.80% | 1.20% | ||

| 14:00 | USD | NAHB Housing Index Mar | 48 | 48 |

USD/JPY in Holding Pattern Ahead of Key BoJ Meeting

The Japanese yen is showing limited movement to start off the week. In the European session, USD/JPY is trading is almost unchanged at 149.07.

Will the BoJ raise rates on Tuesday?

The Bank of Japan will make its rate announcement on Tuesday and there is a strong possibility that the BoJ will lift interest rates out of negative territory. This would mark a sea-change in policy as the last rate hike occurred in 2007.

Japan is experiencing inflation after years of deflation, and speculation has been rising that the BoJ will pivot after years of an ultra-accommodative monetary policy. Governor Ueda has repeatedly stressed that the BoJ will not tighten until wage growth rises, as that would be evidence that inflation is sustainable.

The annual wage negotiations indicate a massive victory for workers, with wages set to rise as much as 5.2%. This could well be the signal that Ueda needs to hit the rate-hike trigger. The key question is whether the BoJ will raise rates on Tuesday or wait until April, which would provide the central bank with more data before making such a critical decision.

It’s a close call as to whether the BoJ will make the move on Tuesday or wait until April. Goldman Sachs is expecting that the BoJ will raise rates and also abolish its yield curve control policy which it uses to target interest rates levels.

If the BoJ raises rates, the yen will likely move higher. Even if the central bank stands pat, with expectations of a possible move at a fever pitch, we can expect volatility from the yen after the meeting.

Hold tight for what should be a busy Tuesday.

USD/JPY Technical

- USD/JPY put pressure on resistance at 149.47 earlier. Above, there is resistance at 149.88

- 148.75 and 148.34 are providing support