Sample Category Title

XTIUSD Extends Bullish Phase, but Watch for Retracement Levels Before Continuing to Buy!

- Bearish scenario: Shorts below 80.00 with TP1: 79.60, TP2: 79.30, and 78.83 with S.L. above 80.62 or at least 1% of account capital*.

- Anticipated bullish scenario: Intraday longs above 80.70 with TP: 81.50, TP2: 81.85, and TP3: 83.00, with S.L. below 80.00 or at least 1% of account capital*. Apply trailing stop.

- Bullish scenario after retracement: (After breaking bellow 80.00) Intraday longs above 78.40 with TP: 81.00, TP2: 81.50, and TP3: 82.00, with S.L. below 77.30 or at least 1% of account capital*. Apply trailing stop.

Scenario from H4 chart:

The uptrend since January broke the last relevant macro resistance (daily chart) of the October to December downtrend at 79.60, hence a retracement of at least 1/3 to 50% of the recent bullish expansion is required before a new rally confirms a macro trend change to bullish.

Under the current scenario, a retracement towards buying zones between 80.00 and the broken level at 79.60 is expected, with a possible downward extension towards 78.83, after which renew purchases aiming for the bullish average range 81.87 intraday and subsequently November resistance at 83.34, confirming the trend change.

A more extended correction towards the weekly open at 77.37 will again place the price in a buying zone to initiate the trend change rally. However, this zone acts as support, so the price must stay above it to consider the possibility of a new rise.

A decisive breakout (with a candle body) of the support at the weekly open of 77.37 will indicate renewed bearishness in the upcoming week, targeting 76.49 and 75.69.

*Uncovered POC: POC = Point of Control: It is the level or zone where the highest volume concentration occurred. If there was a bearish movement from it previously, it is considered a selling zone and forms a resistance zone. Conversely, if there was a bullish impulse previously, it is considered a buying zone, usually located at lows, forming support zones.

**Consider this risk management suggestion

**It is essential that risk management is based on capital and traded volume. Therefore, a maximum risk of 1% of capital is recommended. It is suggested to use risk management indicators such as Easy Order.

Euro Stabilizes, ECB Starts Talking Rate Cuts

The euro is steady on Friday, after sustaining sharp losses a day earlier due to the US inflation report. In the North American session, EUR/USD is trading at 1.0893, up 0.09%.

ECB members signal rate cuts coming

The European Central Bank maintained the deposit rate at 4.0% for a fourth straight time at last week’s meeting. It looks like rates have peaked but the ECB has been reluctant to signal that it is contemplating cutting rates, although the markets have priced in a first rate cut in the summer.

The ECB remains concerned about lowering rates too early and then having to zigzag on policy and raise rates if inflation starts to rise. The battle to bring eurozone inflation down to the 2% target is going well but remains unfinished, with headline inflation at 2.6% and core inflation at 3.1%.

For months, ECB policy makers have been stating that there is no rush to lower rates and warned that inflation remains a key concern. However, the winds appear to be shifting, as two ECB Governing Council members openly called for rate cuts this week.

Yammos Stournaras, head of Greece’s central bank, said that “we need to start cutting rates soon” and urged two cuts before the summer break and four during the year. Stournaras added that his stance was in line with market expectations. Olli Rehn, Governor of the Bank of Finland, said earlier on Friday that if inflation continued to drop sustainably towards the 2% target, then the ECB could slowly lower loosen policy “close to the summer”.

These comments from two senior ECB officials are a marked departure from the message the ECB has been sending and we can expect other senior officials to reiterate this dovish stance. This will likely put pressure on the euro, as lower interest rates will make the euro less attractive to investors.

EUR/USD Technical

- EUR/USD is putting pressure on resistance on 1.0907. Above, there is resistance at 1.0932

- 1.0858 and 1.0833 are providing support

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0858; (P) 1.0907; (R1) 1.0932; More...

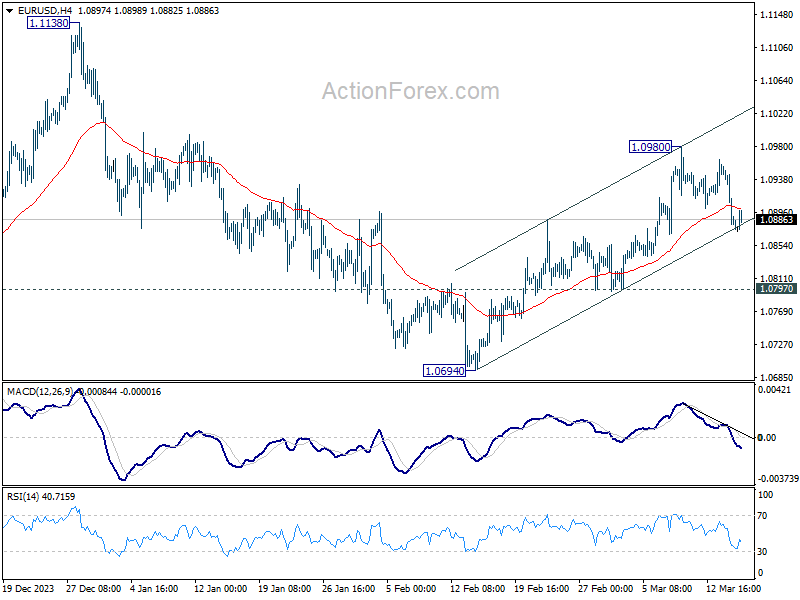

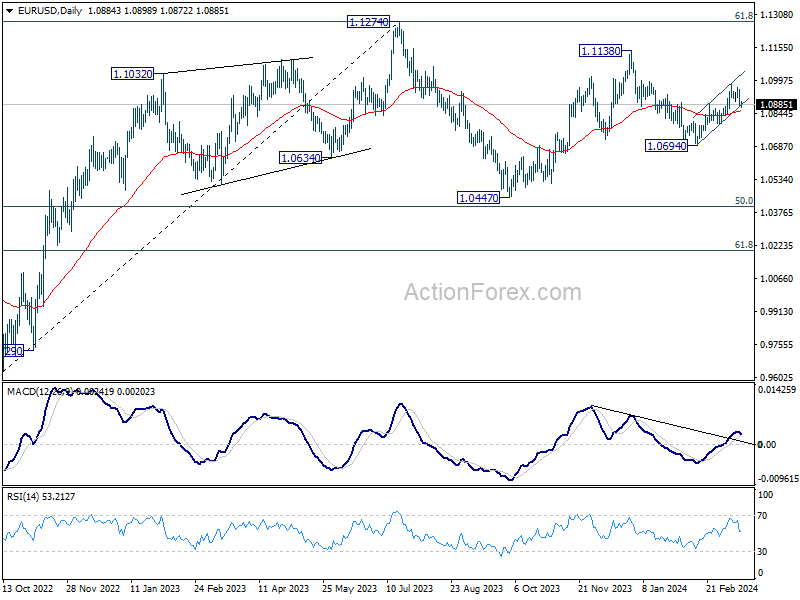

Intraday bias in EUR/USD remains mildly on the downside at this point. Fall from 1.0980 short term top would target 1.0797 support. Firm break there will argue that rebound from 1.0694 has completed and bring retest of this low. For now, risk will stay on the downside as long as 1.0980 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8795; (P) 0.8819; (R1) 0.8862; More....

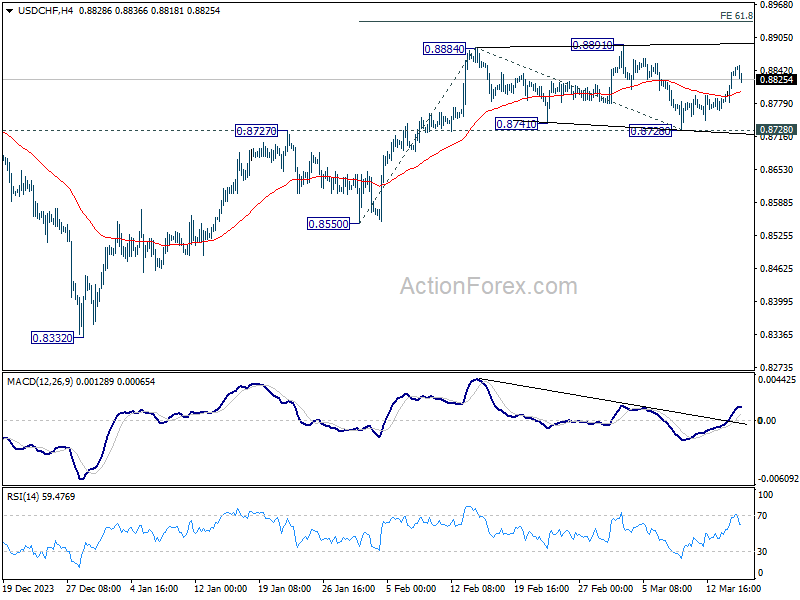

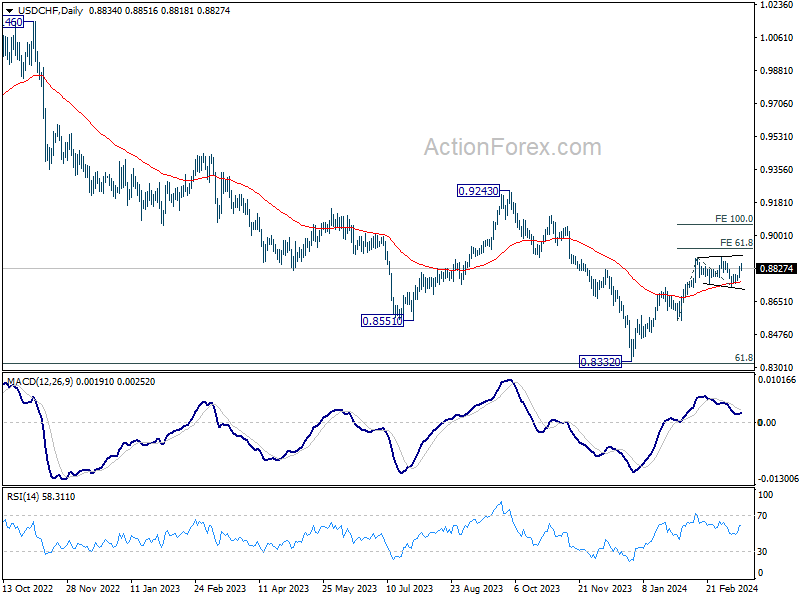

Intraday bias in USD/CHF remains mildly on the upside at this point. Consolidation from 0.8884 could have completed with three waves to 0.8728. Further rise should be seen to retest 0.8891 resistance first. Firm break there will resume whole rise from 0.8332. Next target is 61.8% projection of 0.8550 to 0.8884 from 0.8728 at 0.8934. For now, this will remain the favored case as long as 0.8728 support holds, in case of retreat.

In the bigger picture, price actions from 0.8332 medium term bottom as seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8555 support holds. But upside should be limited by 0.9243 resistance, at least on first attempt.

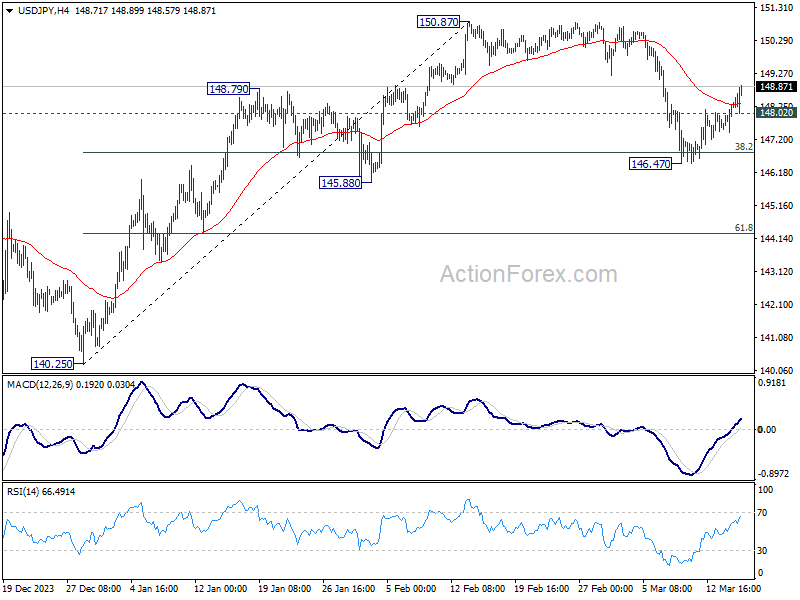

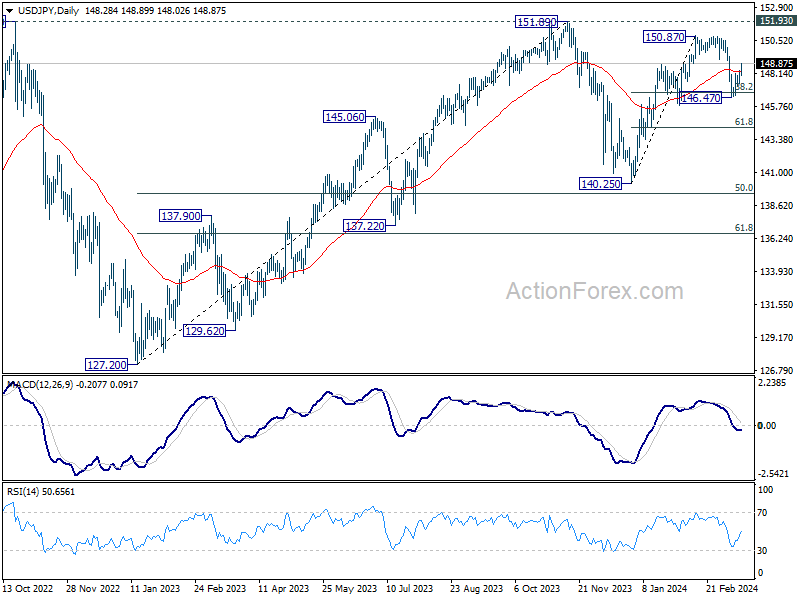

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.71; (P) 148.04; (R1) 148.63; More...

Intraday bias in USD/JPY remains on the upside for the moment. Corrective fall from 150.87 could have completed at 146.47 already, after drawing support from 38.2% retracement of 140.25 to 150.87 at 146.81. Further rise should be seen to retest 150.87 next. Nevertheless, on the downside, below 148.02 minor support will turn intraday bias neutral first.

In the bigger picture, no change in the view that price action from 151.89 (2023 high) are correction to up trend from 127.20 (2023 low). The question is whether this correction has completed at 140.25, or extending with fall from 150.87 as the third leg. Sustained break of above mentioned 146.81 fibonacci level will favor the latter case. But even so, downside should be contained by 50% retracement of 127.20 to 151.89 at 139.54.

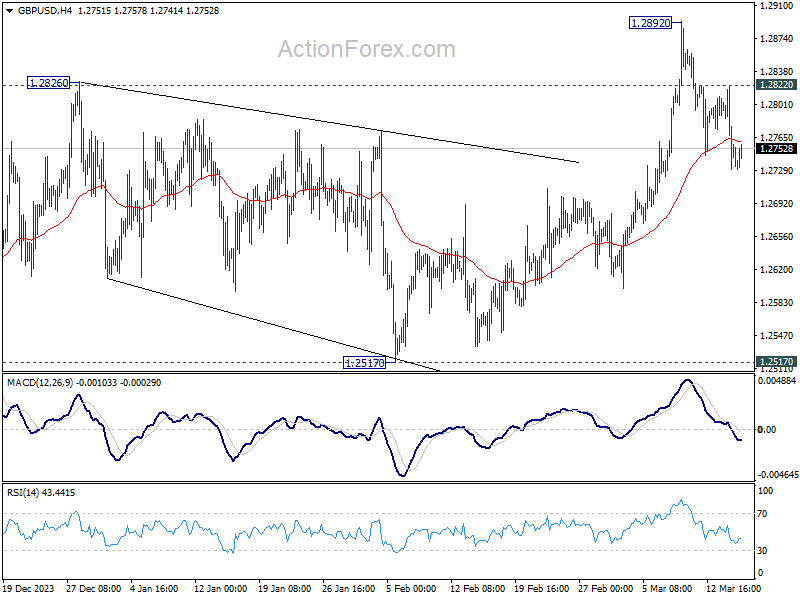

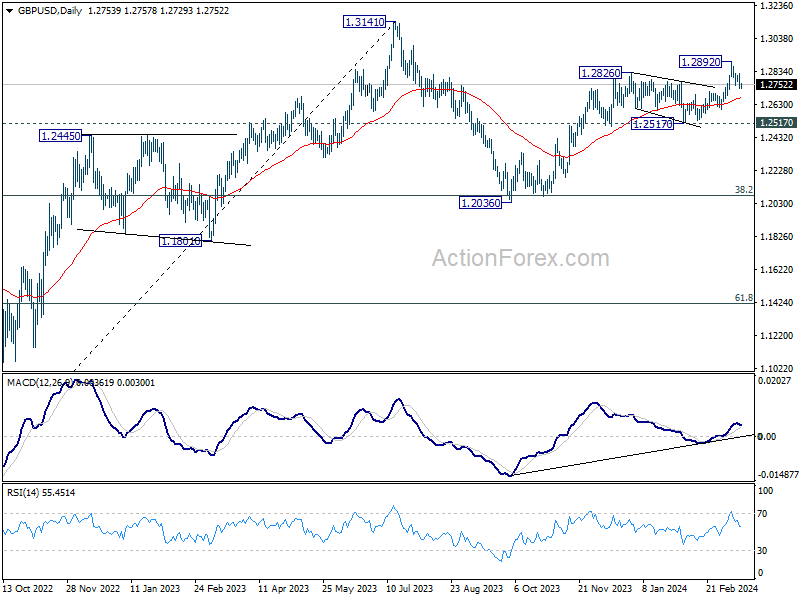

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2715; (P) 1.2769; (R1) 1.2807; More...

Intraday bias in GBP/USD remains mildly on the downside at this point. Fall from 1.2892 short term top would target 55 D EMA (now at 1.2673). Sustained break there will target 1.2517 structural support next. For now, risk will stay mildly on the downside as long as 1.2822 minor resistance holds, in case of recovery.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which is still in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2517 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

Yen Retreats Further as Dollar Sees Caution Among Traders

Yen's pull back continues today despite more positive news on wages negotiations in Japan. Remarkably, the currency has undone its gains from last week against all major counterparts, barring the even more beleaguered New Zealand Dollar. Expectations are still leaning towards an imminent interest rate hike by BoJ; however, speculation is rife that the central bank may postpone this move to April to coincide with the release of new economic projections.

Dollar remains the strongest currency for the week, although it has started to lose some momentum. Traders seem to be adopting a more cautious stance in anticipation of next week's FOMC meeting and the forthcoming economic projections. The financial markets are bracing for a significant week ahead, with several other major central banks, including BoJ, RBA, SNB, and BoE, all scheduled to announce their monetary policy decisions. In light of these upcoming events, it is unsurprising that traders are hesitant to place substantial bets during the last trading session of the week.

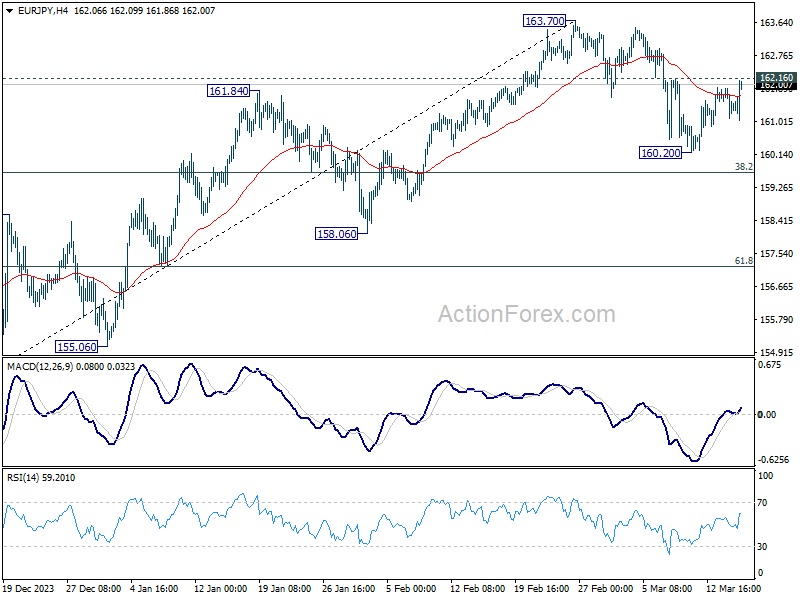

Technically, EUR/JPY is now eyeing 162.16 minor resistance with current rebound. Firm break there will argue that corrective fall from 163.70 has completed at 160.20 already, and stronger rise would be seen back to retest 163.70 resistance. However, it is crucial to bear in mind the considerable market risk posed by the upcoming BoJ rate decision next Tuesday, which could overturn all the technical development. So, any bounce could be short lived until 163.70 is firmly taken out with power.

In Europe, at the time of writing, FTSE is up 0.13%. DAX is up 0.41%. CAC is up 0.50%. UK 10-year yield is up 0.024 at 4.216. Germany 10-year yield is up 0.0177 at 2.445. Earlier in Asia, Nikkei fell -0.26%. Hong Kong HSI fell -1.42%. China Shanghai SSE rose 0.54%. Singapore Strait Times fell -0.42%. Japan 10-year JGB yield rose 0.0174 to 0.793.

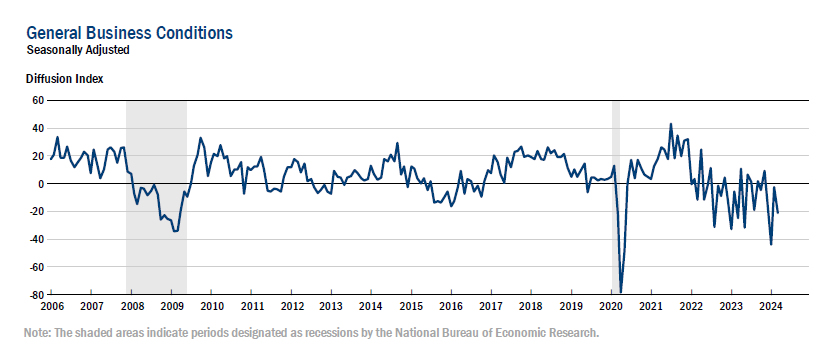

US Empire state manufacturing dives to -20.9, activity falls significantly

US Empire State Manufacturing Index fell sharply from -2.4 to -20.9 in March, well below expectation of -6.5. Looking at some details, new orders fell from -6.3 to -17.2. Shipments fell from 2.8 to -6.9. Prices paid fell from 33.0 to -28.7. Prices received ticked up from 17.0 to 17.8. Number of employments fell from -0.2 to -7.1. Average workweek fell from -4.7 to -10.4.

Richard Deitz, Economic Research Advisor at the New York Fed said: "Manufacturing activity fell significantly in New York State in March, with a decline in new orders pointing to softening demand. Labor market conditions remained weak as both employment and hours worked decreased."

Japan's Shunto negotiations yield 5.28% pay rise, a 33-Year High

Japan's annual labor negotiations, known colloquially as "Shunto" or the "spring wage offensive," have culminated in a remarkable outcome this year, with major firms agreeing to a pay increase of 5.28%—the highest in 33 years.

This significant hike, announced by the country's largest trade union group Rengo, surpasses the previous year's increase of 3.80%. With wage talks for smaller companies anticipated to wrap up by the end of March, this development is a critical one in the context of monetary policy considerations by BoJ.

This wage growth is likely to be viewed positively by BoJ officials, who are widely expected to be on the verge of ending the long-standing negative interest rate policy. However, the exact timing of such a policy shift, whether it could be announced as soon as next week's meeting or delayed until April, remains a matter of speculation.

A recent Reuters poll conducted between March 11 and 14 showed that out of 34 economists surveyed, only 12 anticipate a rate hike in the upcoming week. The majority, 21 out of 34, foresee such a move in April.

Those in favor of an April decision point to BoJ's access to more comprehensive information by then, including results from Tankan survey, insights from branch managers, and a new set of economic projections.

Yet, history has shown that BoJ has a penchant for surprising the markets. This unpredictability serves as a reminder to never rule out the possibility of a sooner move.

NZ BNZ manufacturing climbs to 49.3, a glimmer of hope in ongoing recession

New Zealand BusinessNZ Performance of Manufacturing Index rose from 47.5 to 49.3 , marking the highest point in a year. However, the sub-50 reading indicates that the sector remains in contraction for the twelfth consecutive month.

A closer examination of the components reveals a mixed bag of progress and setbacks. Production saw a significant leap from 42.9 to 49.1, reaching its peak since January 2023. Contrarily, employment edged down to the breakeven point of 50.0 from 51.3. New orders continued to struggle, remaining unchanged at 47.8 and indicating contraction for the ninth month in a row, reflecting the ongoing difficulty in securing new business. Finished stocks and deliveries both saw improvements, with deliveries crossing into expansion territory at 51.4, the highest since March 2023.

Despite these developments, the sector's sentiment remains cautious, with 62% of comments being negative in February, marginally less pessimistic than January's 63.2% but more so than December's 61%. The primary concerns among respondents were a lack of orders, both domestically and internationally, and a general slowdown in the economy.

Stephen Toplis, BNZ's Head of Research acknowledged that while New Zealand's manufacturing sector "is still in recession", the latest PMI data signals "there is light at the end of the tunnel". The proximity of the PMI to the "breakeven" threshold and the positive differential between new orders and inventory suggest an upcoming increase in production.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2715; (P) 1.2769; (R1) 1.2807; More...

Intraday bias in GBP/USD remains mildly on the downside at this point. Fall from 1.2892 short term top would target 55 D EMA (now at 1.2673). Sustained break there will target 1.2517 structural support next. For now, risk will stay mildly on the downside as long as 1.2822 minor resistance holds, in case of recovery.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which is still in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2517 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ PMI Feb | 49.3 | 47.3 | 47.5 | |

| 04:30 | JPY | Tertiary Industry Index M/M Jan | 0.30% | 0.10% | 0.70% | |

| 09:30 | GBP | Consumer Inflation Expectations | 3.00% | 3.30% | ||

| 10:00 | EUR | Italy Retail Sales M/M Jan | -0.10% | 0.20% | -0.10% | -0.20% |

| 12:15 | CAD | Housing Starts Y/Y Feb | 253K | 227K | 224K | 223K |

| 12:30 | CAD | Wholesale Sales M/M Jan | 0.10% | -0.60% | 0.30% | |

| 12:30 | USD | NY Empire State Manufacturing Index Mar | -20.9 | -6.5 | -2.4 | |

| 12:30 | USD | Import Price Index M/M Feb | 0.30% | 0.20% | 0.80% | |

| 13:15 | USD | Industrial Production M/M Feb | 0.00% | -0.10% | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Mar P | 77.3 | 76.9 |

US Empire state manufacturing dives to -20.9, activity falls significantly

US Empire State Manufacturing Index fell sharply from -2.4 to -20.9 in March, well below expectation of -6.5. Looking at some details, new orders fell from -6.3 to -17.2. Shipments fell from 2.8 to -6.9. Prices paid fell from 33.0 to -28.7. Prices received ticked up from 17.0 to 17.8. Number of employments fell from -0.2 to -7.1. Average workweek fell from -4.7 to -10.4.

Richard Deitz, Economic Research Advisor at the New York Fed said: "Manufacturing activity fell significantly in New York State in March, with a decline in new orders pointing to softening demand. Labor market conditions remained weak as both employment and hours worked decreased."

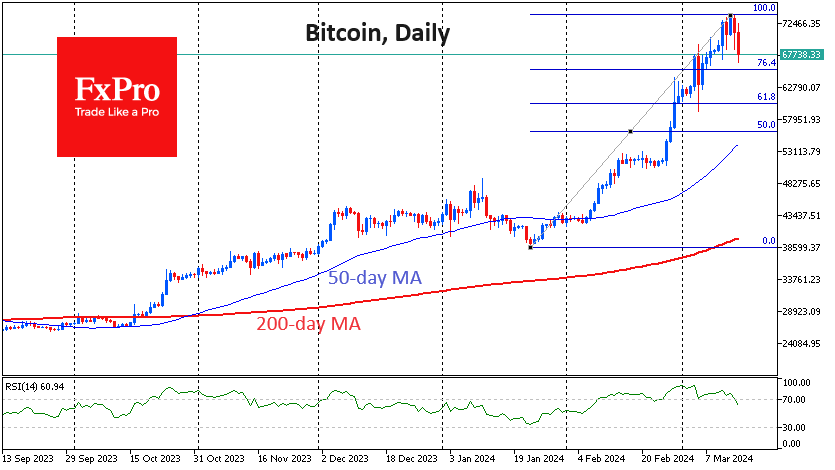

Bitcoin Could Correct to $60K

Market picture

The cryptocurrency market is under pressure, losing 6% of its capitalisation in the last 24 hours to $2.6 trillion.

Bitcoin is losing almost 7% in 24 hours, at one point wiping out last week’s gains and falling to $66.7K. We note that the current area of active buying is below last week’s selling levels. Obviously, new historical highs are a trigger for selling. Some players are taking profits, which raises the question of whether there will be enough hot buyers at current levels or whether the majority will prefer to wait for a deeper correction.

In a corrective scenario, the $65.0-65.5K and $60.0-60.5K areas are of particular interest, as they contain important round levels (significant for retail) and the 76.4% and 61.8% Fibonacci retracement lines.

As a result of another recalculation, the difficulty of mining the first cryptocurrency increased by 5.79%. The indicator updated the historical maximum at 83.95T. The average hash rate for the period since the previous change in value was 600.72 EH/s.

News background

The addition of spot bitcoin ETFs to the list of instruments by major platforms and the approval of options based on them will be “powerful catalysts” for demand by the end of the year, notes Bloomberg. The ETFs are not yet available to clients of registered investment advisor platforms with $7-10 trillion in assets, but that could happen within the next few months.

Fees in EIP-4844-implemented layer-2 networks saw a several-fold decline after the Dencun upgrade in the Ethereum mainnet. Gas fees in the Base protocol dropped from $0.7 to $0.0024. In Optimism, transaction fees dropped from $0.66 to $0.0055, and in zkSync – from $0.32 to $0.097.

QCP Capital predicts that Ethereum will fall after the Dencun upgrade. Appetite for ETH-focused instruments in the futures and options markets has declined, suggesting a deterioration in the altcoin’s medium-term prospects.

MicroStrategy launches its second round of Bitcoin fundraising. The company will raise $500 million through the issuance of convertible notes due in 2030. The offering will be subject to “market and other conditions”. MicroStrategy previously held an $800 million bond sale in early March.

NZ Dollar Extends Losses after Mfg. PMI Contraction

The New Zealand dollar continues to lose ground and has dropped more than 1% since Wednesday. In the European session, NZD/USD is trading at 0.6094, down 0.59%.

NZ Manufacturing PMI declines for 12th straight month

New Zealand’s manufacturing industry marked an unhappy anniversary on Friday as the sector contracted for a twelfth straight month (a PMI reading below 50 indicates contraction and above 50 indicates expansion). There was a silver lining as the BusinessNZ Manufacturing PMI improved in February for a second straight month, rising from 47.5 in January to 49.3 and beating the market estimate of 48.1.

This marked the highest level since February 2023 and raises hopes for manufacturers that there is light at the end of the tunnel. The slowdown in the New Zealand economy has dampened manufacturing activity and manufacturers reported weak demand both domestic and offshore in the February report.

It will be a busy start to next week with the release on Monday of New Zealand Services PMI and Chinese retail sales and industrial production. New Zealand’s services sector is showing signs of expansion and jumped to 52.1 in January, up from 48.8 in December. The uptrend is expected to continue in February, with a forecast of 52.9.

Chinese data often has a strong impact on the movement of the New Zealand dollar, as China is New Zealand’s largest export market. China’s retail sales is expected to fall to 5.2% y/y in January, down from 7.4% in December. Industrial production is also projected to de-accelerate to 5% in January, compared to 7.4% in December. If these key releases are weaker than expected, the New Zealand dollar could have a rough start to the week.

NZD/USD Technical

- NZD/USD has pushed below support at 0.6110 and tested support at 0.6090 earlier. Below, there is support at 0.6057

- There is resistance at 0.6143 and 0.6163