Sample Category Title

Sterling Loses Ground on Just-Below Consensus Labour Market Data

Markets

Friday’s bearish engulfing pattern at record levels for the S&P 500 and Nasdaq (potential short term trend reversal) met with some more weakness in futures trading and at the opening bell, but follow-up losses remained contained to 0.11% and 0.41% respectively as some investors are still looking to buy into every minor dip. Adding evidence on the other side of the scale (room for larger correction) is the weak final hour we’ve been seeing over the last couple of sessions. The jury remains out, but we hold it on our radar as potential bigger market driver (risk sentiment) in trading days ahead. Today’s focus is on February US CPI inflation figures. Headline and core inflation are expected at 0.4% M/M and 0.3% M/M respectively with annual measures stabilizing at the top level (3.1% Y/Y) and forecast to slide to the lowest level since April 2021 for the core reading (3.7% Y/Y from 3.9% Y/Y). That’s because of relatively high comparison bases last year and probably limits scope for any upward surprises. From a (bond) market point of view, we believe that investors could be enticed to add to speculative May Fed rate cuts bets in case of a below of in-line-with consensus outcome. Such expectations re-entered markets last week after Fed Chair Powell on his second day of testimony’s before US Congress said that the Fed isn’t far from reaching the confidence level needed (on inflation) to start making monetary policy less restrictive. US Treasuries can in such scenario revisit last week’s highs (or better). The NY Fed ‘s February Survey of consumer expectations yesterday created some room to maneuver. One-year inflation expectations remained unchanged at 3%, with medium (3-yr) and long term (5-yr) expectations increased significantly: from 2.4% to 2.7% and from 2.5% to 2.9% respectively. US Treasury yields yesterday rebounded by 0.8 bps (30-yr) to 6.1 bps (2-yr). US Treasuries underperformed German Bunds (yields 2.6 bps to 4.4 bps higher), triggering a minor setback in EUR/USD (1.0926 from 1.0940). USD/JPY slightly rebounds this morning (147.50) after a BoJ-normalization induced JPY-rally. Latest rumours suggest that the board is split between March and April on ending its negative interest rate policy with Friday’s outcome of annual wage negotiations being pivotal. Sterling this morning loses ground on just-below consensus labour market data. The unemployment rate ticked up to 3.9% with average weekly earning rising by 5.6% 3M/YoY. February job growth rose by 20k following a downward revision in January. EUR/GBP moves back to 0.8550 after last week’s failed test of 0.85 support.

News & Views

The Central Bank of Argentina yesterday unexpectedly reduced its benchmark interest rate from 100 % to 80%. In January, CPI inflation was reported at 20.6% M/M and 254.2% Y/Y. Policy makers apparently see a cooling in monthly inflation, rebuilding of reserves and a rise in the parallel exchange rate of the peso as a good enough reason to ease policy already. February inflation data will be published later today (15% M/M and 282% Y/Y consensus). The move is also a bit surprising as the IMF in its latest review indicated that Argentina’s authorities agreed that the monetary policy stance needs to be tightened to support disinflation. Yesterday, the government also launched a voluntary debt swap of peso and dollar-linked debt instruments with a total value of around $65bn. Instruments maturing in 2024 can be changed for new inflation-linked instruments with maturities between 2025 and 2028 as the country tries to delay repayments on its debt.

Australian business conditions improved in February to 10 from 7. In its assessment, NAB says that the economy remained resilient in the new year and inflation is still a challenge despite slowing growth. Trading conditions and profitability pushed business conditions back above their long-run average – though conditions softened further in retail and construction, sectors that are particularly exposed to the ongoing impact of tighter monetary policy. Despite signs of resilience, NAB mentions that business confidence and forward orders both eased to remain mired at low levels. Capacity utilisation also eased. Businesses continue to report elevated rates of cost growth (both labour and materials inputs) and it appears that firms still have scope to pass some costs to consumers. Retail price growth, in particular, rose sharply to 1.4% Q/Q in a sign that further progress on inflation is unlikely to be smooth over the months ahead. Markets currently still see a first RBA rate cut in August.

UK wages growth slows more than expected in Jan

In February, UK payrolled employment rose 20k or 0.1% mom. Median monthly pay increased by 5.5% yoy. Annual growth in median pay was highest in the other service activities sector, with an increase of 7.4% yoy, and lowest in the finance and insurance sector, with a decrease of -0.3% yoy.

In the three months to January, unemployment rate ticked up to 3.9%, above expectation of 3.8%. Average earnings including bonus rose 5.6% yoy, slowed from 5.8% yoy, below expectation of 5.7% yoy. Average earnings excluding bonus rose 6.1% yoy, down from 6.2% yoy, below expectation of 6.2% yoy.

Limited Appetite Ahead of US CPI, Bitcoin at Record

The week started with limited appetite in US stock and a fresh record for Bitcoin. Major US indices were flat on Monday’s trading session. The S&P 500 slid 0.11% as sentiment in technology stocks was mixed. Nvidia tumbled 2% yesterday, but Google gained nearly 2%. The US dollar recovered the post-US jobs data losses, the US 2-year yield stabilized near a touch above the 4.50% level and the 10-year near the 4% mark ahead of today’s all-important US CPI data.

Investors are not feeling fully comfortable into today’s US inflation print, as there are several factors warning of a second blip in US disinflation that could eventually lead to a further softening in dovish Federal Reserve (Fed) expectations. One of them is the jump in gasoline prices in February, another is the change in CPI calculation and the third is the rising inflation expectations. Released yesterday, New York Fed’s survey showed a steep rise in 3 and 5-year inflation expectations, and a steady expectation of around 3% for this year. That means that consumers who have been surveyed by New York Fed don’t expect inflation to ease much further from the actual levels. And that’s a problem because inflation tends to be self-fulfilling. In numbers, the headline inflation is expected to have steadied at 3.1% y-o-y, core inflation is expected to have eased from 3.9% to 3.7% y-o-y, but monthly headline figure could pause problem. A data set in line with expectations, or ideally lower than expected, should reinforce the Fed cut expectations for June, pull the US yields and the dollar lower. A higher-than-expected set of inflation data should soften the Fed doves’ hand and trigger a selloff in US treasuries, a rebound in US yields and the dollar. I think that there is a chance that we have a bad surprise.

For equities, volatility will certainly be on the menu of the day, as the Fed’s data-dependent approach results in an increased focus on inflation data. Bloomberg data shows that over the past six months, the S&P500 moved 0.8% up or down on average after the release of CPI data. And this number will likely go up in the run up to the first Fed rate cut.

In the meantime, Germany will release its own inflation numbers, which should print a softer yearly, and a higher monthly figure. The EURUSD retreated from post-NFP peak at yesterday’s session on expectation that the European Central Bank (ECB) will cut more than the Fed this year due to a softer economic outlook and fading pressure on wages, while yen traders are busy gathering evidence to justify a rate hike in Japan. Yesterday, the Bank of Japan (BoJ) didn’t intervene to slow the bleeding while Topix fell more than 2%. That has been perceived as a sign that the BoJ is preparing to exit the ultra-loose monetary policy. And this morning, the PPI data came in higher-than-expected to support the expectation that Japan shall move maybe in March, maybe in April, more probably in April than in March. But note that the USDJPY is higher this morning as BoJ Governor Ueda killed the bulls’ joy again, saying that the economy is recovering moderately, but that there were some weakness seen in recent data – which I interpret as ‘forget about your March hike’.

Elsewhere, Bitcoin hit a fresh record yesterday, a coin traded at $72K level. The massive inflows that have been allowed by the introduction of spot ETFs and the upcoming halving are fueling the actual rally in Bitcoin. The bulls are eyeing the $100K mark, I believe we will get there. But what will happen after is yet to be seen. Bitcoin rallies on classical demand/supply dynamics today, but the use cases have not been following the price move. On the other hand, flows point at higher Bitcoin and make Bitcoin a good diversification option as the coin is moving on its own fundamentals and not on traditional market news. Therefore, the CPI print will certainly not derail the rally.

Back to traditional space, your good old gold is consolidating gains near record high, as well. Any rebound in US yields on a potential CPI disappointment could trigger profit taking and a pullback at the current overbought market levels, but softer yields on a soothing CPI could encourage another test of the $2200 level.

US CPI in the Limelight

In focus today

The most important release of the day will be the US February CPI. We look for both headline and core CPI to come out at +0.3% m/m SA, slightly below consensus forecast. Markets will focus on non-housing services inflation, which surprised to the upside in January, cooling expectations of rapid rate cuts.

In Europe, we look out for the final German inflation data to dissect the large monthly increase in core inflation registered in February.

In the UK, the labour market report is published for January/February at 8:00 CET. Focus will be on developments in wage growth as this remains a key concern for the Bank of England. We expect to see the first rate cut in the UK in June.

In Denmark, the unemployment indicator for February is scheduled for release.

In Sweden, the Riksbank Board will participate in an open hearing by the Riksdag Committee on Finance today, starting at 09.00 CET.

Economic and market news

What happened overnight

In Japan, BoJ Governor Ueda was on the wire, stating that the economy is recovering moderately, while also emphasizing that some signs of weakness have been seen lately - especially in consumption and CapEx. In respect of the central bank's monetary meeting next week, Ueda highlighted that whether a positive wage-inflation cycle is ongoing will be key for their monetary policy decision. On Friday, we will get a sense of this when Japan's biggest labour union federation, Rengo, releases the first tally of pay deals. Finally, Japanese producer prices surprised to the upside, which could be another sign of underlying inflation pressures building.

What happened yesterday

In the US, data from the New York Fed showed that long-term inflation expectations climbed considerably higher. The 5Y and 3Y segments printed 2.9% (prior: 2.5%), and 2.7% (prior: 2.4%), respectively. However, one should not ring the alarm bells yet. It is notable that the 3Y January print was the lowest ever, and the current 2.7% is quite close to the pre-covid average. Moreover, this uptick follows a month where gasoline prices increased almost 5%.

Last night, President Biden presented a USD 7.3tn budget plan for 2025 in light of the upcoming presidential election. Biden's plan would boost spending, while also saving USD 3tn by raising taxes on corporations and high-income earners - for instance reversing half of Trump's 2017 cuts to corporate taxes by hiking the tax rate to 28% from 21% (35% prior to 2017). Despite the considerable tax hikes, the proposal would not have a major impact on near-term deficits, with the White House estimating that passing of the plan would see a deficit of 6.1% in 2025. This is precisely in line with the Congressional Budget Office's baseline forecast from February.

In Denmark, inflation decreased to 0.8% in February from 1.2% in January. Food prices are the key driver as the February price surge from last year rolls out of the inflation measure, with food prices declining 0.4% against an expected increase of 0.4%. In contrast to the euro area, price pressures have remained in line with 2% annual inflation in the first two months of 2024.

In Norway, February inflation figures surprised to the downside, with core inflation printing 4.9% y/y (cons: 5.3% y/y). Decomposing the figures reveals that imported inflation recovered more than we had expected, albeit this was partly offset by a moderately larger drop in food inflation. The big surprise to us was service inflation. Service prices excluding rent actually tumbled some 0.3% m/m SA, due to declines in hotel/restaurants, communication etc.

Equities: Global equities started the week lower as the AI-frenzy continued to level off. Interestingly, the crypto frenzy is continuing despite equities taking a breather. Cyclicals underperformed led by tech and industrials while energy and consumer staples outperformed. VIX crept higher and is now back above 15. In US yesterday, Dow +0.1%, S&P 500 -0.1%, Nasdaq -0.4% and Russell 2000 -0.8%. Asian markets are very mixed this morning with China continuing higher and Japan lower. European and US futures are higher.

FI: Yields rose from the belly of the curve as the 5y point led the sell-off amid repricing of central bank cut expectations this year. With little specific news, the 5y point in Germany rose 4bp. Markets repriced the ECB rate cut pricing 5bp lower, relative to Friday, to 98bp this year. Tomorrow, ECB is set to complete the operational framework review. Yesterday, Bloomberg sources reported that the Governing Council is favouring leaving the minimum reserve requirement at 1%. No timing has been given for a potential announcement tomorrow, albeit we know that the non-monetary policy meeting is set to start at noon CET.

FX: Wait-and-see-mode in anticipation of today's US CPI print. The USD held steady, breaking the depreciation streak while JPY continued to outperform G10 peers. EUR/GBP recovered some lost ground in anticipation of this week's UK tier 1 data releases. Scandies lost some ground in muted trading.

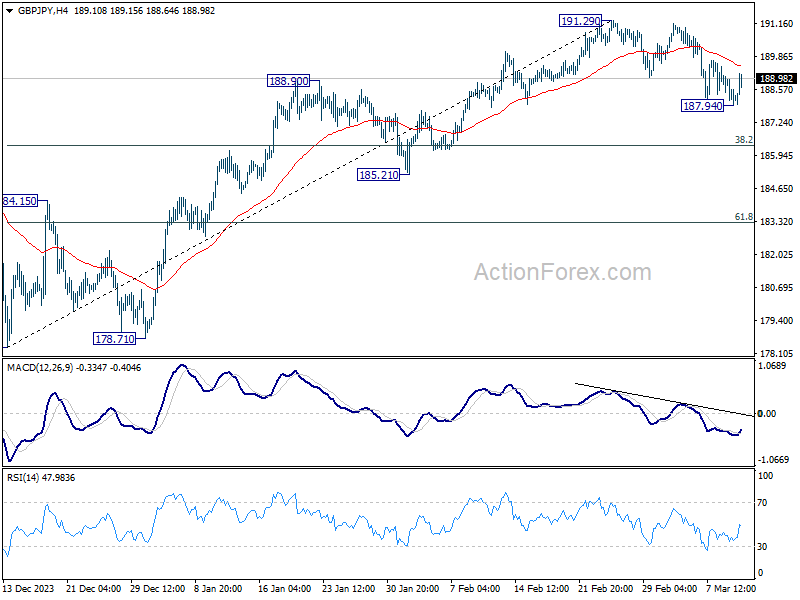

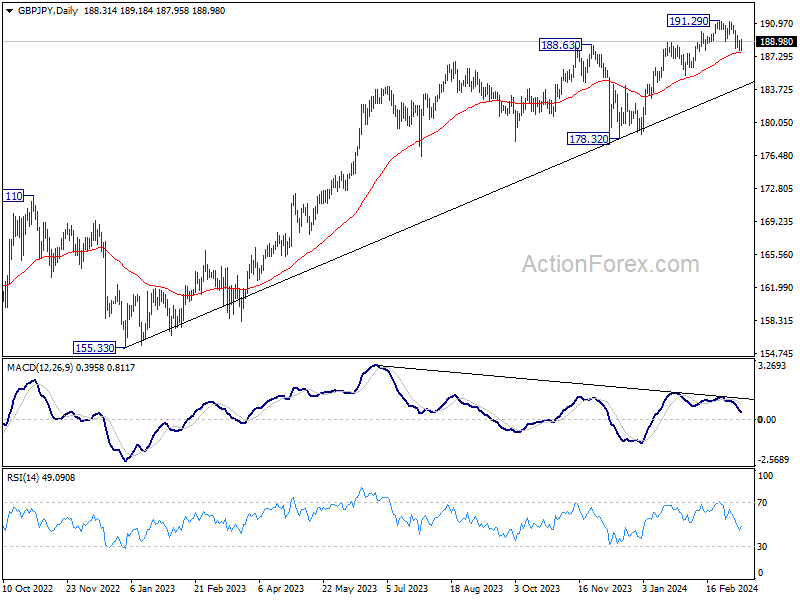

GBP/JPY Daily Outlook

Daily Pivots: (S1) 188.45; (P) 189.08; (R1) 189.78; More.....

GBP/JPY recovered after dipping to 187.94 and intraday bias remains neutral. On the downside, below 187.94 will resume the decline from 191.29 to 38.2% retracement of 178.32 to 191.29 at 186.33. Sustained break there will raise the chance of larger scale correction and target 61.8% retracement at 183.27. On the upside, though, firm break of 55 4H EMA (now at 189.49) will retain near term bullishness and bring retest of 191.29 high.

In the bigger picture, up trend from 123.94 (2020 low) is in progress. Medium term outlook will stay bullish as long as 178.32 support holds. Next target is 195.86 long term resistance (2015 high).

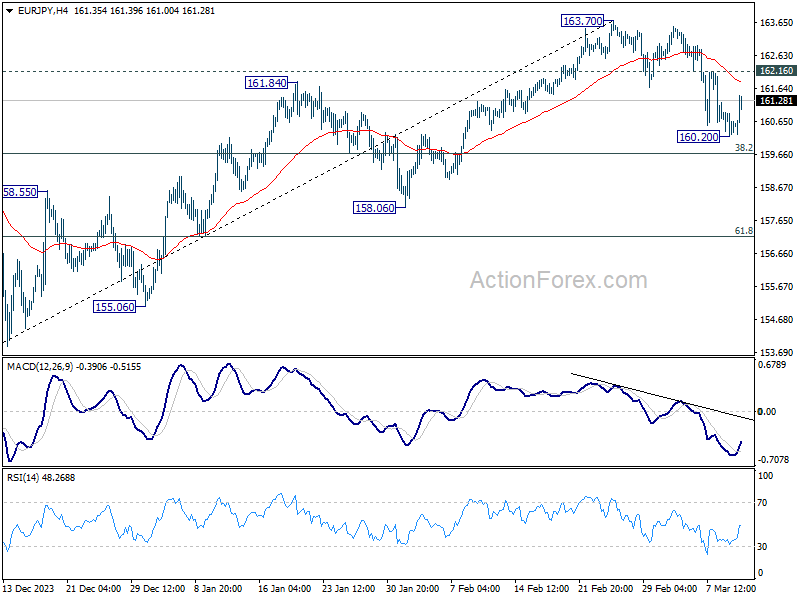

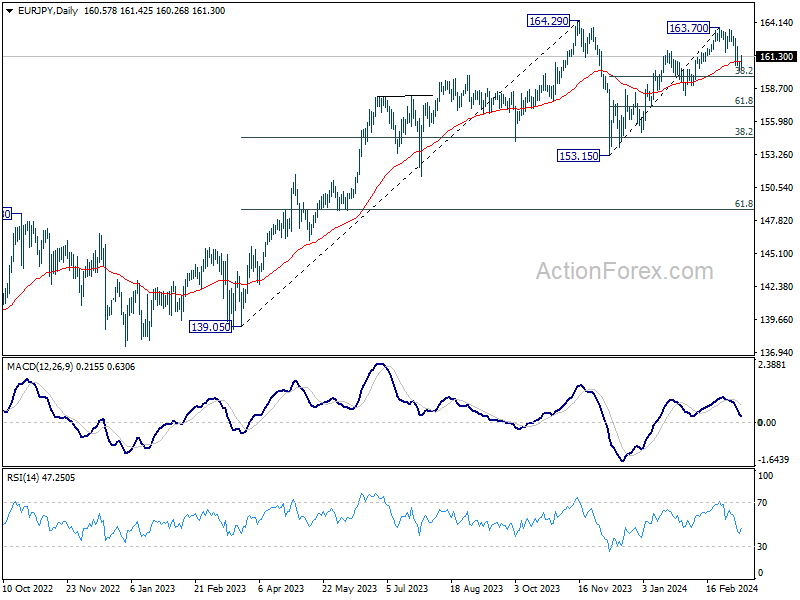

EUR/JPY Daily Outlook

Daily Pivots: (S1) 160.19; (P) 160.59; (R1) 160.96; More...

Intraday bias in EUR/JPY is turned neutral again with current recovery. On the downside, below 160.20 will resume the fall from 163.70 to 38.2% retracement of 153.15 to 163.70 at 159.66. Sustained break there will indicate that fall from 163.70 is reversing whole rise from 153.13, and target 61.8% retracement at 157.18. On the upside, though, above 162.16 minor resistance will retain near term bullishness, and bring retest of 163.70.

In the bigger picture, price actions from 164.29 medium term top are seen as a correction to rise from 139.05 which could still be extending. As long as 148.38 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) is expected to resume through 164.29 at a later stage. Next target would be 169.96 (2008 high).

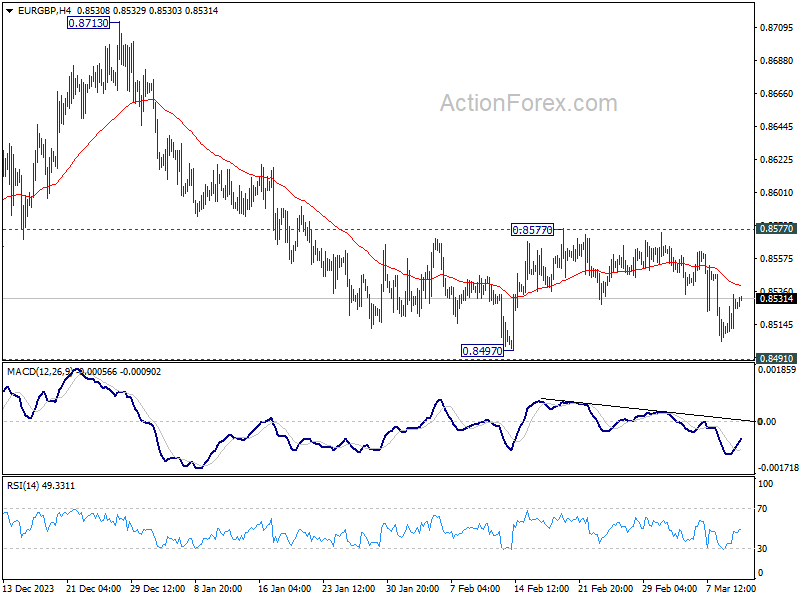

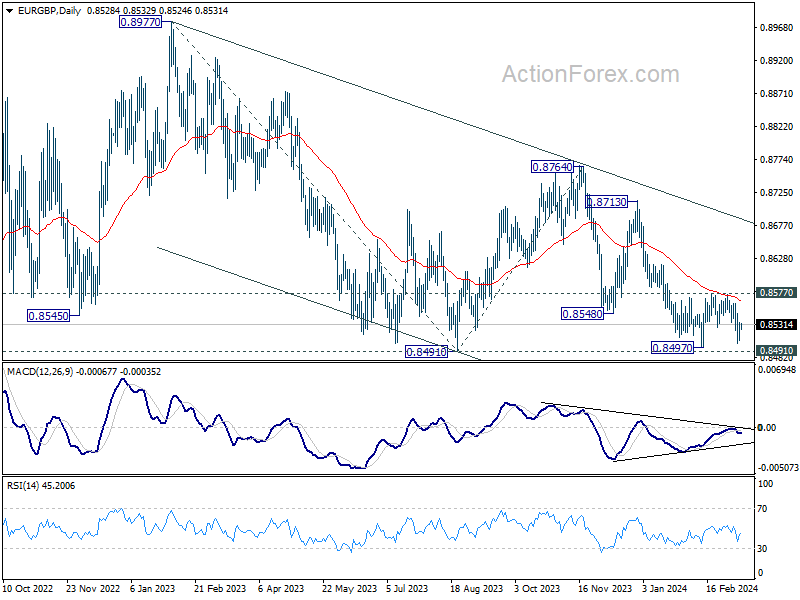

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8510; (P) 0.8522; (R1) 0.8540; More...

No change in EUR/GBP's outlook as range trading continues. Intraday bias stays neutral for the moment. On the downside decisive break of 0.8491/7 support zone will confirm larger down trend resumption and target 0.8464 projection level first. Nevertheless, firm break of 0.8577 will turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8713 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

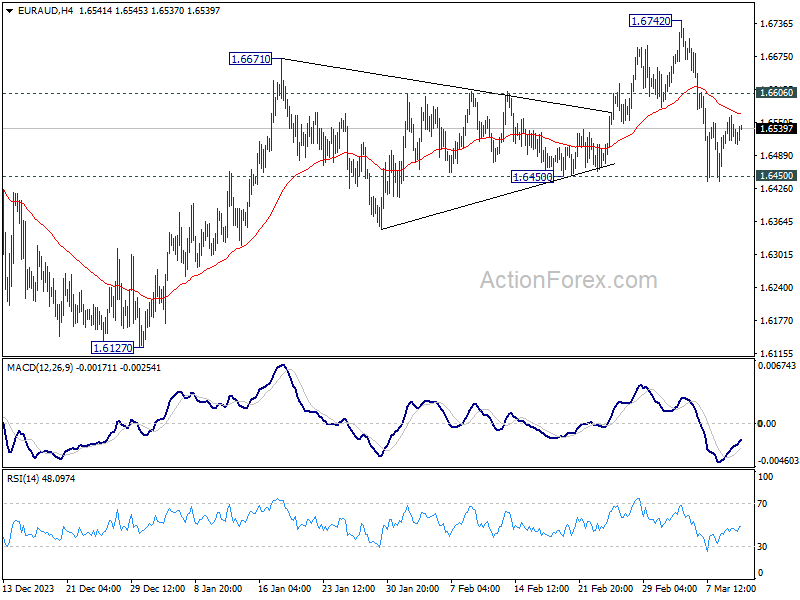

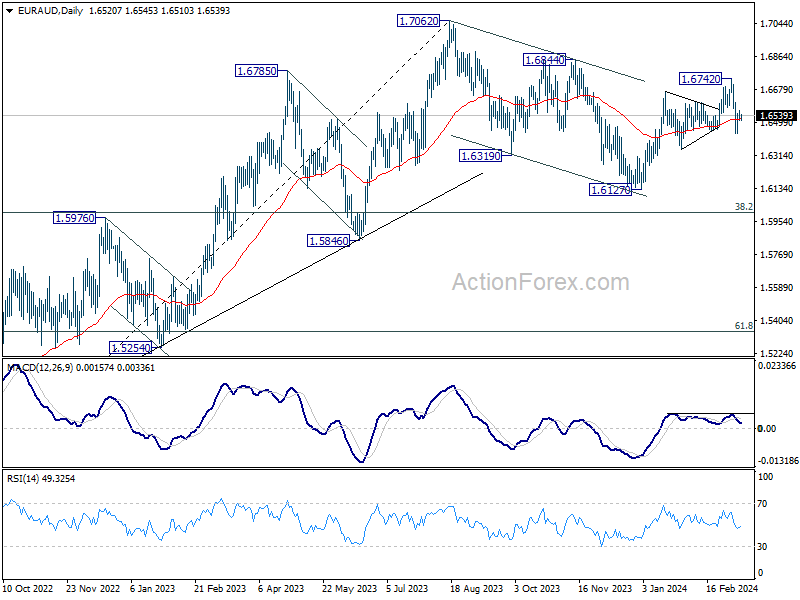

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6491; (P) 1.6528; (R1) 1.6558; More...

Range trading continues in EUR/AUD and intraday bias remains neutral. On the downside, decisive break of 1.6450 support will argue that whole rebound from 1.6127 has completed with three waves up to 1.6742 already. Near term outlook will be turned bearish for 1.6127 again, to extend the whole corrective pattern from 1.7062. Nevertheless, strong rebound from current level, followed by break of 1.6606 minor resistance, will retain near term bullishness and bring retest of 1.6742.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

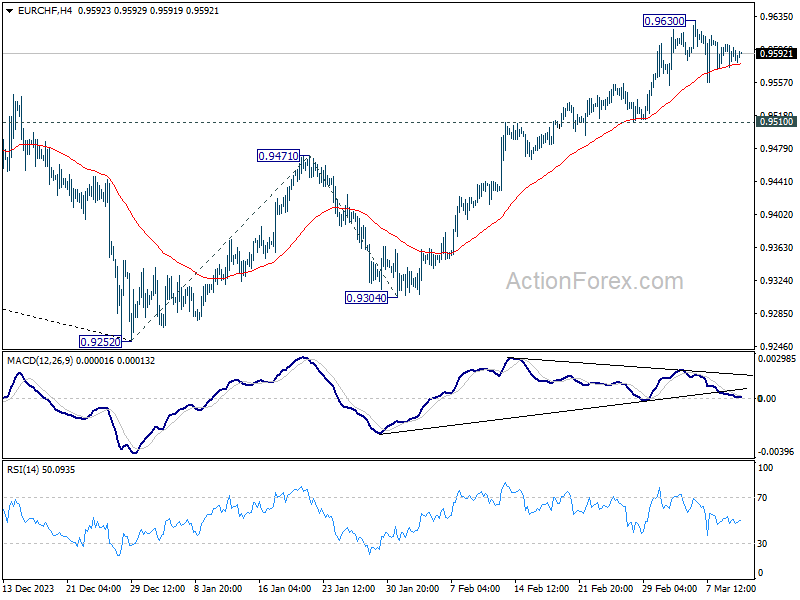

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9575; (P) 0.9589; (R1) 0.9602; More...

EUR/CHF's consolidation continues below 0.9630 temporary top and intraday bias remains neutral. As long as 0.9510 support holds, further rally is still expected. On the upside, break of 0.9630 will resume the rise from 0.9252 and target 161.8% projection of 0.9252 to 0.9471 from 0.9304 at 0.9658 next. However, considering bearish divergence condition in 4H MACD, firm break of 0.9510 will turn bias back to the downside for deeper fall.

In the bigger picture, as long as 0.9683 resistance holds, rebound from 0.9252 are seen as a corrective move only. Larger down trend is expected to resume through 0.9252 after the correction completes. However, firm break of 0.9683 and sustained trading above 55 W EMA (now at 0.9620) will argue that 0.9252 is already a medium term bottom. Stronger rise would then be seen 61.8% retracement of 1.0095 to 0.9252 at 0.9773 and above.

GBPJPY Should Resuming to the Upside After a Corrective Pause

GBPJPY has ended a cycle from 14.12.2023 low. Up from 14.12.2024 low, wave (1) ended at 191.32 and pullback in wave (2) is in progress. The pair resumes lower in wave ((i)) with internal subdivision as 5 waves. Down from wave (1), wave (i) ended at 190.34 and wave (ii) pullback ended at 190.99. Pair resumes lower in wave (iii) towards 189.34 and bounce in wave (iv) ended at 190.03. Final leg wave (v) ended at 189.02 which completed wave ((i)) in higher degree. Pullback in wave ((ii)) higher did a zigzag Elliott Wave structure ending at 191.18 high.

Down from wave ((ii)), wave (i) ended at 189.84 and wave (ii) pullback ended at 190.68. Pair resumes lower in wave (iii) towards 188.23 and bounce in wave (iv) ended at 188.79. Last wave (v) ended at 188.22 which completed wave ((iii)) in higher degree. Rally from 188.22 low ended at 189.72 and also wave ((iv)) correction. Currently, we are expecting to complete an ending diagonal as wave ((v)) and also wave A where market should reacgt higher in 3, 7 or 11 swings correction as wave B before resuming to the downside in wave C to finish the correction in wave (2) lower.

GBPJPY 60 Minutes Elliott Wave Chart