Sample Category Title

February CPI: FOMC Still Searching for Confidence

Summary

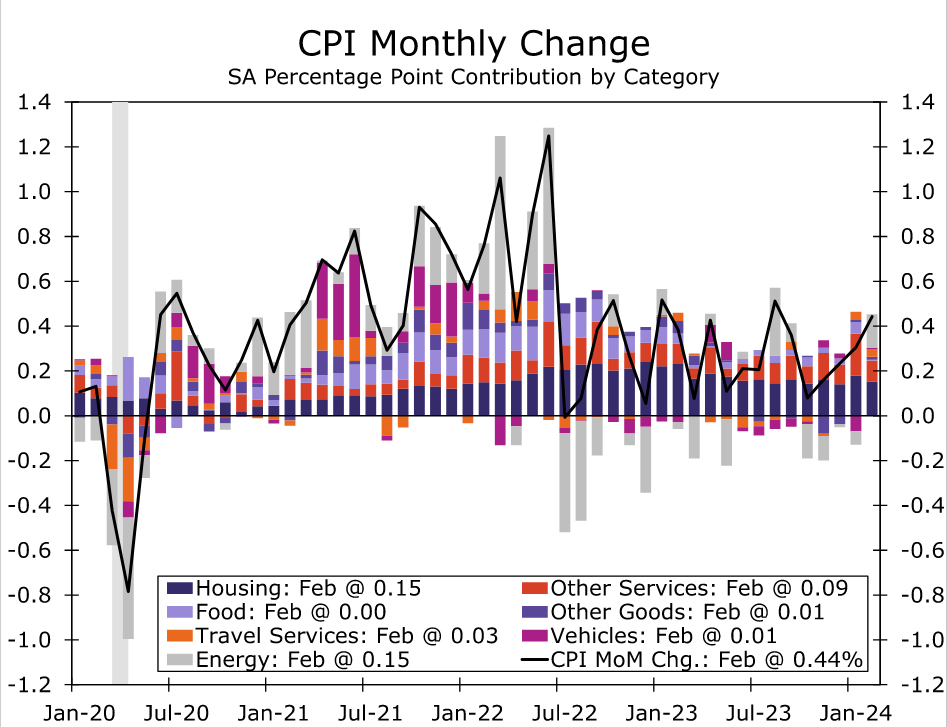

The February consumer price data came in a touch stronger than expected. The headline CPI increased 0.4% in the month, led by higher gasoline prices (+3.8%). Excluding food and energy prices, core inflation also registered 0.4%. However, the unrounded 0.36% bump in core CPI was not too far off our forecast for a 0.30% gain. Furthermore, core price growth was flattered by bigger than expected increases in volatile components such as used autos and airfares. Housing inflation cooled as owners' equivalent rent increased 0.4%, a step down from the eye-catching 0.6% jump in January.

In our view, the details of today's CPI report generally were encouraging. We expect core goods deflation to return in the coming months amid improved supply chains and less supportive seasonal factors. The much-anticipated slowdown in primary shelter inflation is ongoing. A cooling jobs market has brought about slower labor cost growth, and the widespread easing in this month's "super core" suggests services inflation may not be as sticky as some feared following last month's CPI report

That said, we doubt today's report fills the FOMC with the confidence it needs to begin cutting rates. The core CPI has risen at 4.2% annualized rate over the past three months, which is a bit higher than the 3.8% increase in core prices over the past 12 months. We expect disinflation progress to resume in the coming months for the reasons listed above, but we think the FOMC will need to see it to believe it. The first rate cut from the FOMC looks increasingly likely to occur this summer. We will be publishing our FOMC preview report and Monthly Economic Outlook in the coming days, and we will update our fed funds rate outlook in those publications.

A Little More Inflation Than Expected

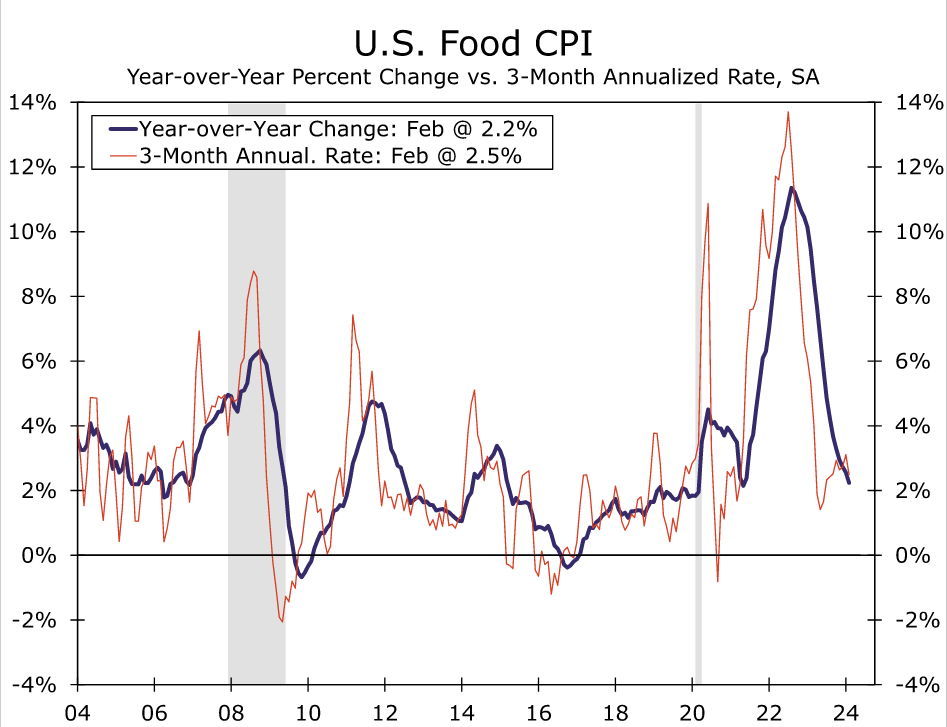

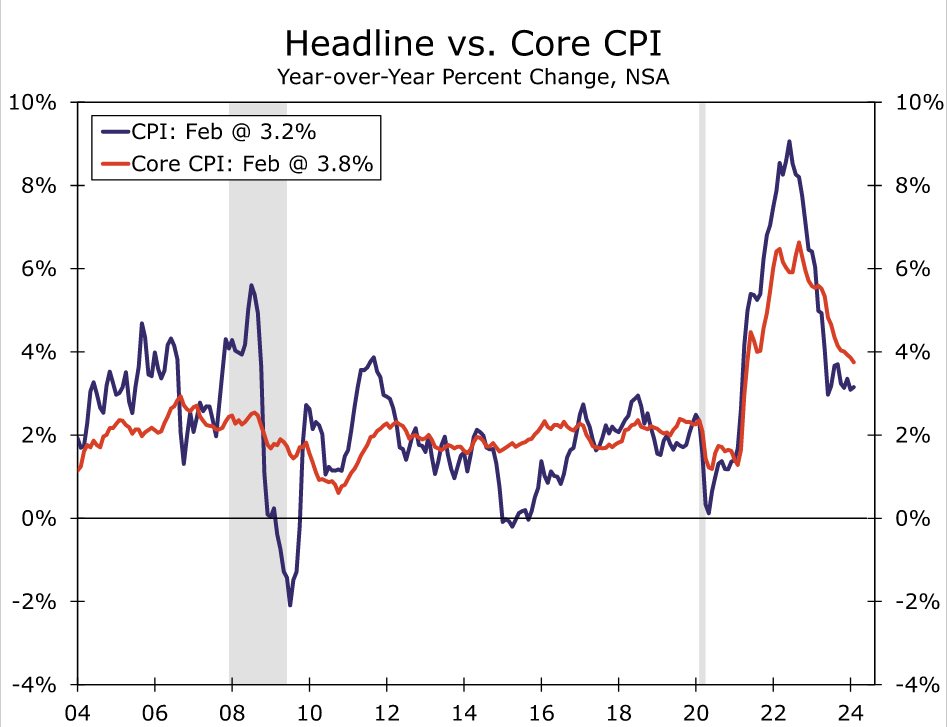

Consumer prices advanced 0.4% in February, in line with consensus expectations. The overall energy index, which accounts for a little under 7% of the CPI, increased 2.3% in February. As expected, the headline CPI was lifted by a jump in gasoline prices (+3.8%). Compared to one year ago, gasoline prices are still down 3.9%. Energy services rose a smaller 0.8%, led by utility gas service (+2.3%). Food inflation was more benign in February, with prices unchanged in the month. Grocery store prices were flat while prices at restaurants and bars increased 0.1%—the smallest monthly increase in three years. Over the past year, food inflation has cooled significantly and is now back in line with pre-pandemic norms (Figure 1).

Excluding food and energy, the gain in CPI was a touch stronger than expected. The core index advanced 0.36%, a bit above the Bloomberg consensus and our own expectation for a 0.30% gain. The somewhat firmer reading stemmed from core goods, which rose for the first time in eight months (+0.1%). As we flagged in our CPI preview, however, core goods prices looked susceptible to being bolstered by some residual seasonality in February after price increases were more dispersed throughout the calendar year the past few years. Contributing to the rise was a small rebound in prices for used vehicles, apparel and education and communication goods, which offset declines in new vehicles, motor vehicle equipment, household and recreational goods. We expect to see core goods return to deflationary territory over the next few months amid the broad improvement in supply chains and less supportive seasonal factors.

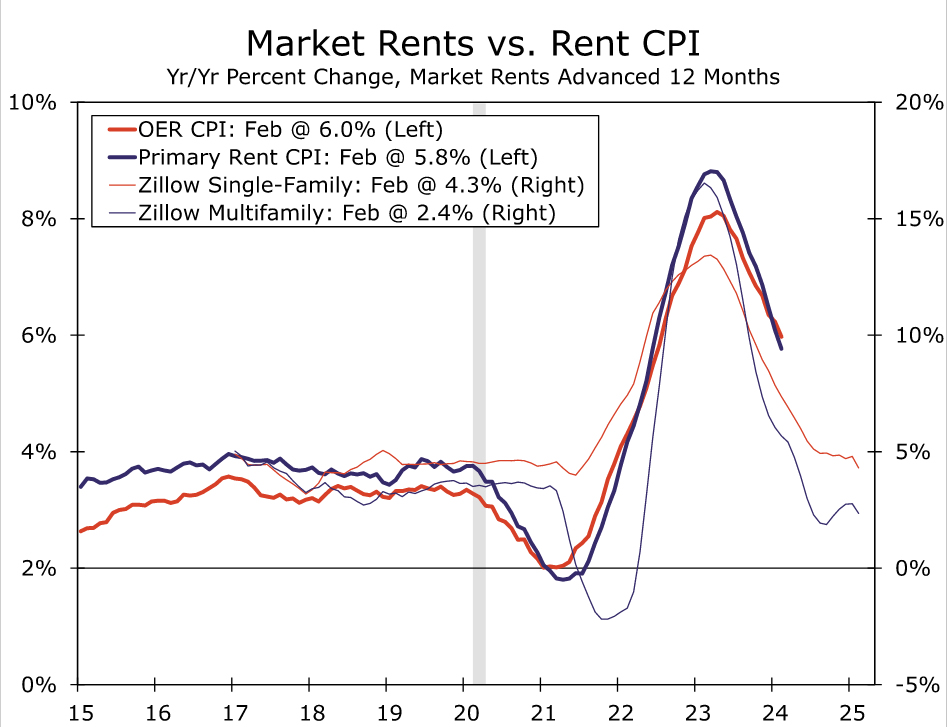

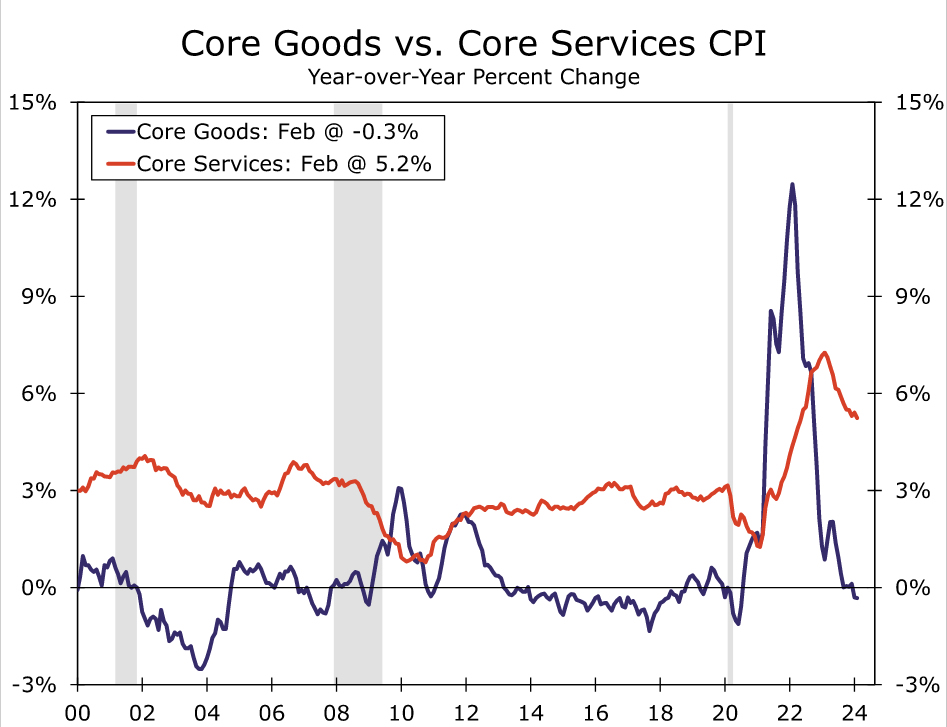

Core services, on the other hand, cooled largely as expected (Figure 3). A 0.7% jump in core services in January drove inflation's unexpected pop to start the year. In February, core services prices advanced "just" 0.5% (0.46% before rounding). After making waves in January, owners' equivalent rent growth eased in February (+0.4%). With rent of primary residences picking up in February (+0.5%), last month's eye-catching gap between the two largest components of the CPI collapsed. Through the recent monthly volatility, the trend in housing inflation remains downward. Both the year-over-year rate of OER and rent of primary residences registered the smallest increases since the summer of 2022, and a further slide appears in store with private-sector measures of rent growth having largely returned to their pre-pandemic rates (Figure 2).

Excluding primary shelter, core services also advanced at a less concerning rate in February. The CPI version of the "super core", watched by Fed officials to better gauge services inflation given the long lag in shelter inflation, advanced 0.4% after a 0.9% gain in January. The more moderate reading was helped along by a partial reversal of last month's jump in medical and personal care services, as well as smaller monthly gains in lodging away from home, motor vehicle insurance and maintenance services. The broad cooling in the CPI "super core" in February suggests services inflation is not as sticky as initially feared following January's sharp upside surprise.

On a year-ago basis, consumer prices are up 3.2%, a more palatable increase than the 6.0% increase registered this time last year but little different from the past few months (Figure 4). The recent pace of core inflation, having registered a 4.2% annualized rate over the past three months, also points to some near-term stalling in inflation's descent. However, we expect the lack of recent progress to be temporary. Price pressures across the economy continue to broadly abate. Labor costs are cooling as the jobs market softens. Consumers, while still spending, are not the price-takers they were a year or two ago as revenge spending dissipates and delinquencies creep higher. The supply chain kinks that helped drive core goods inflation to 47-year high largely have unwound, making it easier for businesses to secure product. In a separate report this morning, the February NFIB Small Business Optimism Index showed the smallest share of businesses raising prices in three years.

While a downward trend in inflation remains in place in our view, the slow progress seen over the past few months is likely to keep the Fed searching for a bit more confidence that inflation is on a sustained path back to its 2% target. The first rate cut from the FOMC looks increasingly likely to occur this summer. We will be publishing our FOMC preview report and Monthly Economic Outlook in the coming days, and we will update our fed funds rate outlook in those publications.

Sunset Market Commentary

Markets

Sticky. There’s no better way to describe today’s US CPI print. Headline and core inflation rose by 0.4% M/M in February. Both are in line with forecast, given that core CPI actually increased by 0.358% (vs 0.3% forecast). Annual readings increased for the top figure (3.2% Y/Y from 3.1% Y/Y) and fell slightly less hoped for the core gauge (3.8% Y/Y from 3.9% Y/Y). Details showed that shelter and gasoline costs were among the ones responsible for the increase with the food index being unchanged. The so-called supercore measure which filters out core services excluding shelter, rose by 0.47% M/M (4.3% Y/Y). That’s less than the extreme increase in January 0.85% M/M but still more than double the pre-pandemic average. We don’t think that today’s price figures provided the additional evidence Fed Chair Powell is looking for to give the go-ahead on a less restrictive monetary policy. Looking forward, base effects make it very likely that headline inflation will return and hold near levels around 3.5% Y/Y in coming months. Monthly CPI prints for the March – July 2023 period were either 0.1% or 0.2% with the exception of April (0.4% M/M). These low hurdles are easy to match, especially with the volatile energy component out of play. The bar for core CPI is higher, but there sticky services inflation and the delayed impact on shelter costs provide a solid “floor”. A gradual normalization of the labour market and the absence of financial shocks suggest that the Fed will only by the time of the August CPI release (September 12) at the earliest see renewed disinflationary momentum. All of a sudden, risks for next week’s FOMC meeting seem to be tilted to the hawkish side. Recall that the median outcome of the December dot plot for 2024 (4.5%-4.75% EoY policy rate) wasn’t a unanimous one. 8 out of 19 FOMC members only expected a cumulative 50 bps rate cuts over the course of this year. The probability of a May and June policy rate cut today fall to 13% and 75% respectively, with markets again more aware of the risk of a delayed start. US Treasuries spiked lower after the inflation print. US yields currently rise 4 to 5 bps across the curve. Tonight’s $39bn 10-yr Note auction will suddenly draw some more attention again… German Bunds drop in sympathy with yields up to 3 bps higher at the front end of the curve. The dollar enjoys the yield advantage with EUR/USD changing hands just above 1.09. Thinking above risk scenarios through suggests significant downside potential in the pair if the ECB sticks to its “independence” (of the Fed). Equity markets take today’s inflation numbers surprisingly positive with key US benchmarks currently up to 0.5% higher. We end with EUR/GBP which is back into familiar territory around 0.8550 after unexpectedly testing the low 0.85 area at the end of last week. Slightly disappointing UK labour market data this morning triggered the move higher.

News & Views

The Czech statistical office yesterday reported that inflation returned to the 2% inflation target in February. This reopened the debate whether the Czech National bank (CNB) has room to step up the pace for rate cuts from current 50 bps steps. The next CNB meeting takes place on March 20. Two MPC members today advocated caution. Vice Governor Zamrazilova indicated that she will consider a quarter or a half-point rate cut at next week’s meeting. She isn’t considering ‘jumbo’ rate cuts. Ongoing price pressures in the services sector and a weak koruna warrant a cautious approach. CNB Kubicek in a separate interview with Reuters now sees inflation risks as rather balanced. He indicated likely to back a 50 bps rate cut next week. “Inflation figures speak for a faster decline (in rates). But the exchange rate has delivered part of the easing of monetary conditions.” Retail sales today also grew a faster than expected 1.0% M/M and 2.4% Y/Y in February. The koruna rebounded from EUR/CZK 25.33 to 25.26.

France remain at risk not reaching its deficit reduction target. The government last month announced €10bn of measures to reach the 2024 budget deficit target of 4.4% of GDP. According to the national audit office, the government might be too optimistic on its tax revenue assumptions as growth is only expected at 1% instead of 1.4% initially. Even this 1% growth target is considered optimistic. The country’s debt will reach 110% of GDP at the end of the year. Between 2023 and 2024, the cost of just servicing French debt will rise from €10bn to €57bn. The Cours de Comptes labels France’s public finance situation as among the worst in the euro zone.

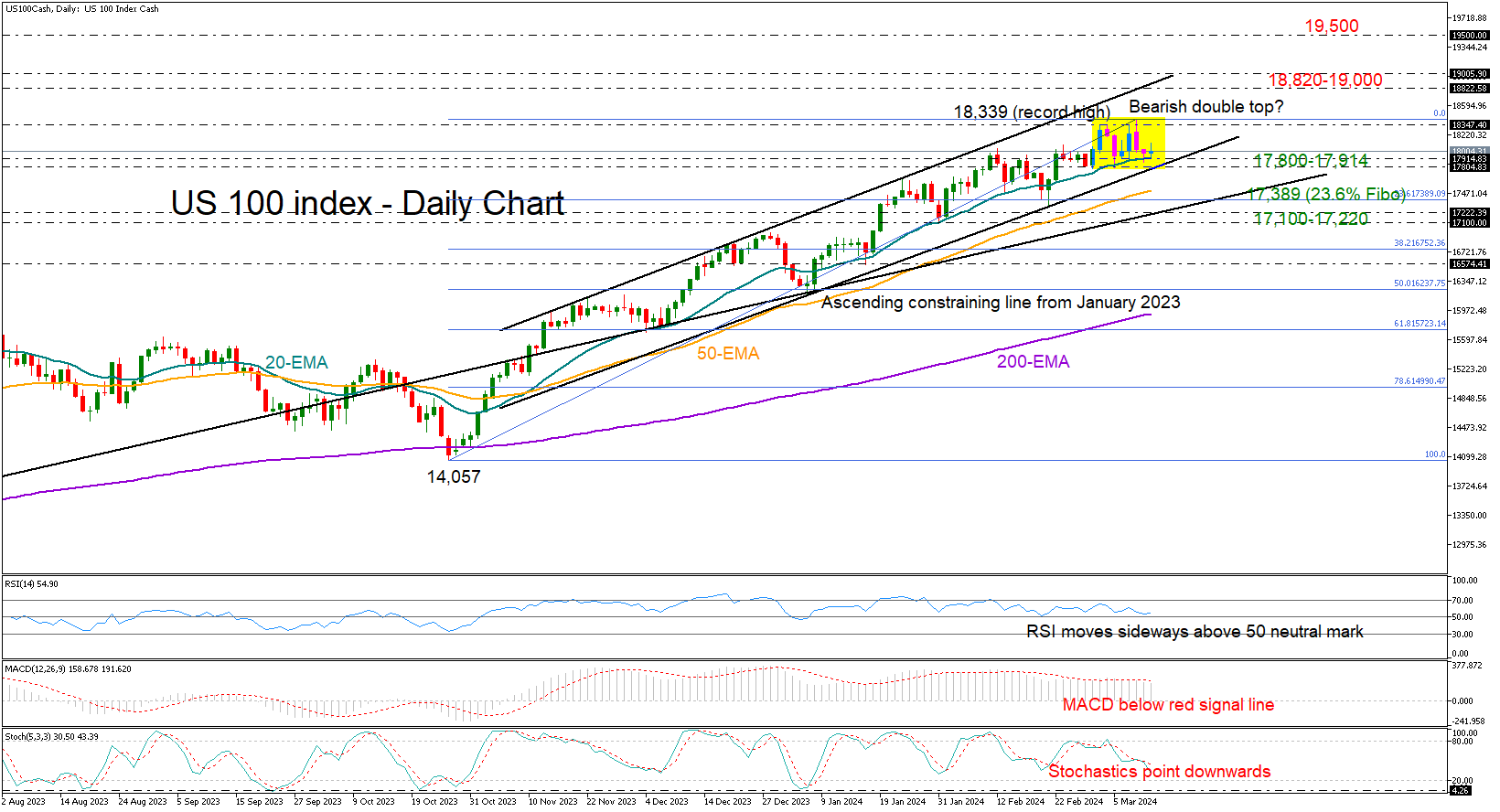

US 100 Stock Index at Risk of Double Top

- US 100 stock index forms bearish structure

- The market could balance selling forces above 17,800

The US 100 stock index (cash) seems to have formed a bearish double top pattern within a rising channel and around the peak area of 18,338.

The bears will have to successfully complete that negative pattern below the 17,800-17,914 neckline to visit the 50-day exponential moving average (EMA) and the 23.6% Fibonacci of 17,389. Slightly lower, the constraining ascending line from January 2023 might act as a safety net near 17,100, canceling an aggressive downfall towards the 38.2% Fibonacci mark of 16,752.

According to the technical signals, the bias is neutral to bearish as the RSI keeps moving sideways above its 50 neutral mark and the MACD loses steam below its red signal line along with the stochastic oscillator.

Nevertheless, as long as the price stays resilient above the 20-day EMA at 17,914, there is scope for a rebound to 18,338. An uptrend resumption above the latter could lift the index up to the resistance line from November at 18,822. The 19,000 round level and the 261.8% Fibonacci extension of the July-October 2023 downleg could be the next destination, while higher, the bulls could target the 19,500 number.

In summary, the uptrend in the US 100 stock index has started to show some cracks, though traders may not engage in selling activities unless the price tumbles below 17,800. Futures markets were pointing to a soft positive open on Wall Street at the time of writing.

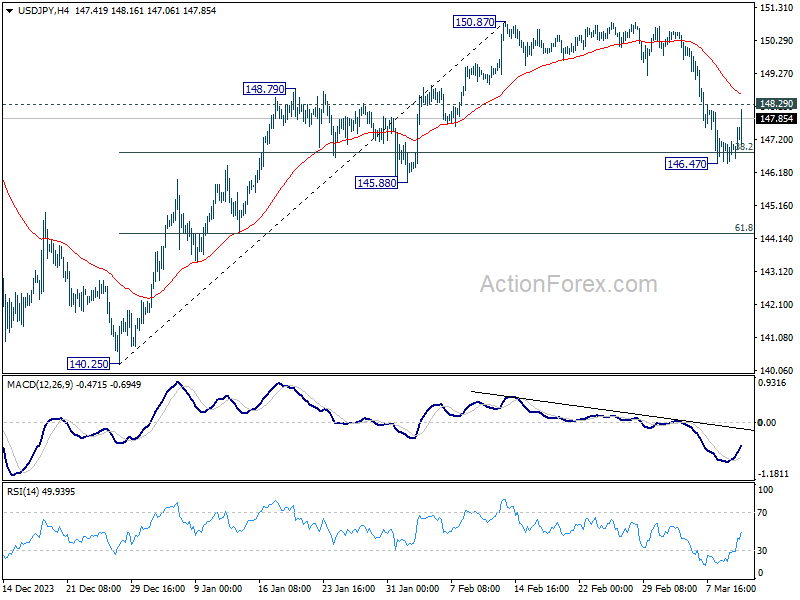

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 146.57; (P) 146.87; (R1) 147.25; More...

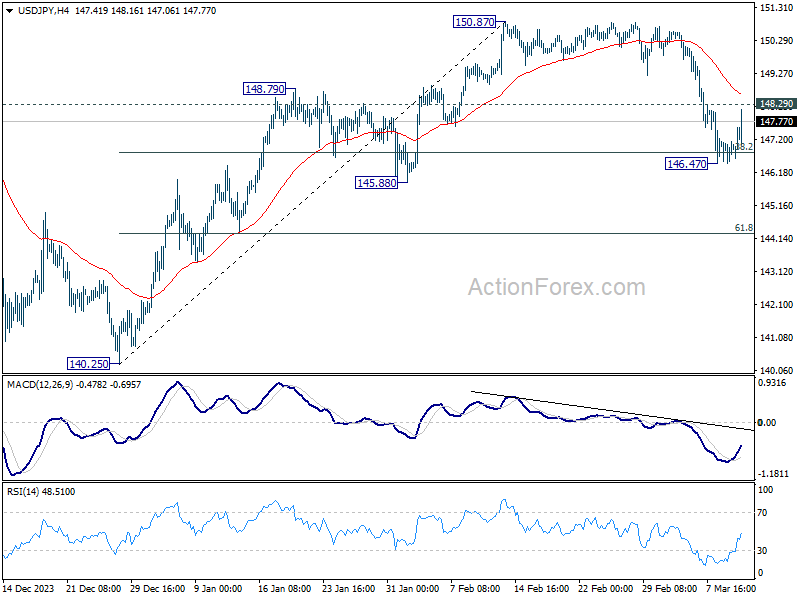

Intraday bias in USD/JPY remains neutral at this point. On the downside, sustained break of 38.2% retracement of 140.25 to 150.87 at 146.81 will argue that fall from 150.87 is reversing the whole rally from 140.25. In this case, deeper decline would be seen to 61.8% retracement at 144.30 and below. Nevertheless, strong support from 146.81, followed by break of 148.29 minor resistance resistance, will argue that fall from 150.87 is merely a correction, which has completed already. Retest of 150.87 should be seen next.

In the bigger picture, no change in the view that price action from 151.89 (2023 high) are correction to up trend from 127.20 (2023 low). The question is whether this correction has completed at 140.25, or extending with fall from 150.87 as the third leg. Sustained break of above mentioned 146.81 fibonacci level will favor the latter case. But even so, downside should be contained by 50% retracement of 127.20 to 151.89 at 139.54.

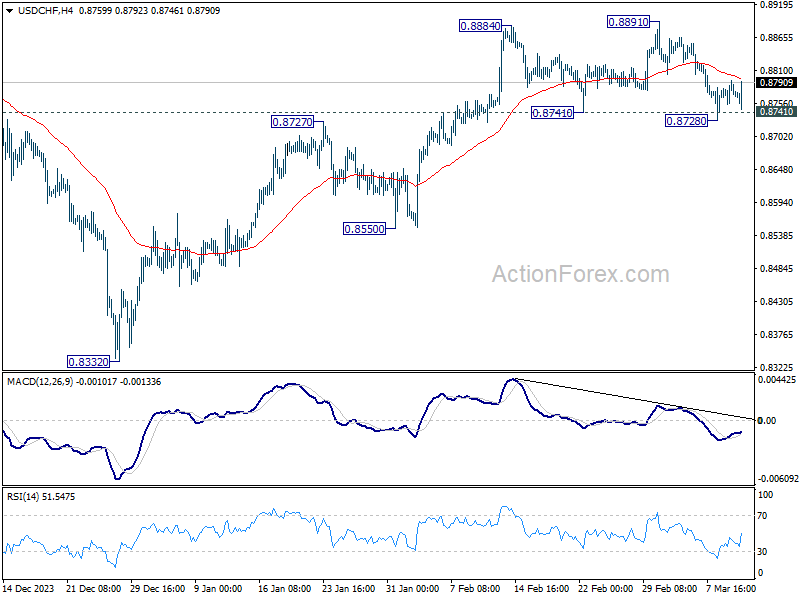

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8754; (P) 0.8775; (R1) 0.8794; More....

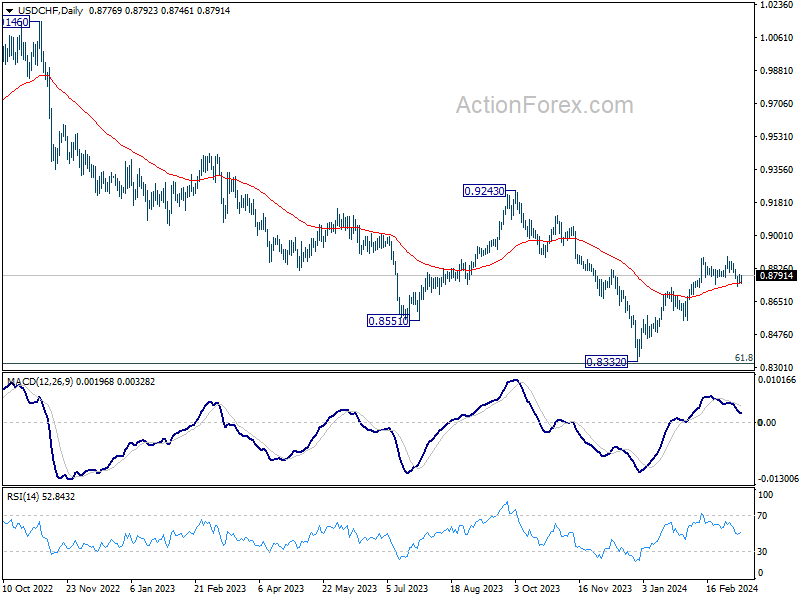

Intraday bias in USD/CHF remains neutral at this point, and outlook is unchanged. On the downside, sustained break of 0.8741 will argue that the whole rebound from 0.8332 might have completed, and bring deeper fall to 0.8550 support. Nevertheless, strong bounce from current level will retain near term bullishness. Further break of 0.8891 will resume the rise from 0.8332.

In the bigger picture, price actions from 0.8332 medium term bottom as seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8555 support holds. But upside should be limited by 0.9243 resistance, at least on first attempt.

EUR/USD Mid-Day Outlook

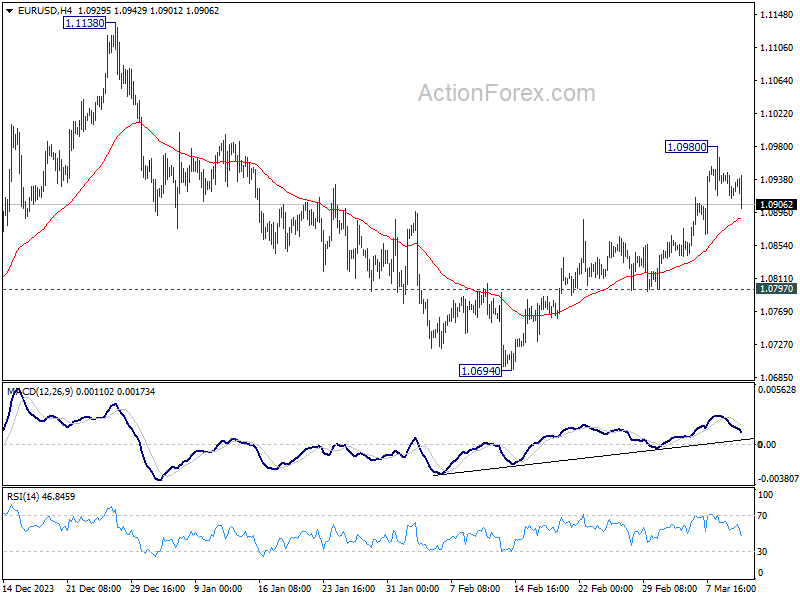

Daily Pivots: (S1) 1.0911; (P) 1.0929; (R1) 1.0944; More...

EUR/USD's retreat from 1.0980 extends slightly lower today but intraday bias stays neutral first. Further rise would remain in favor as long as 1.0797 support holds. Fall from 1.1138 could have completed at 1.0694, as a correction to rise from 1.0447. Above 1.0980 will resume the rise from 1.0694 to retest 1.1138 high.

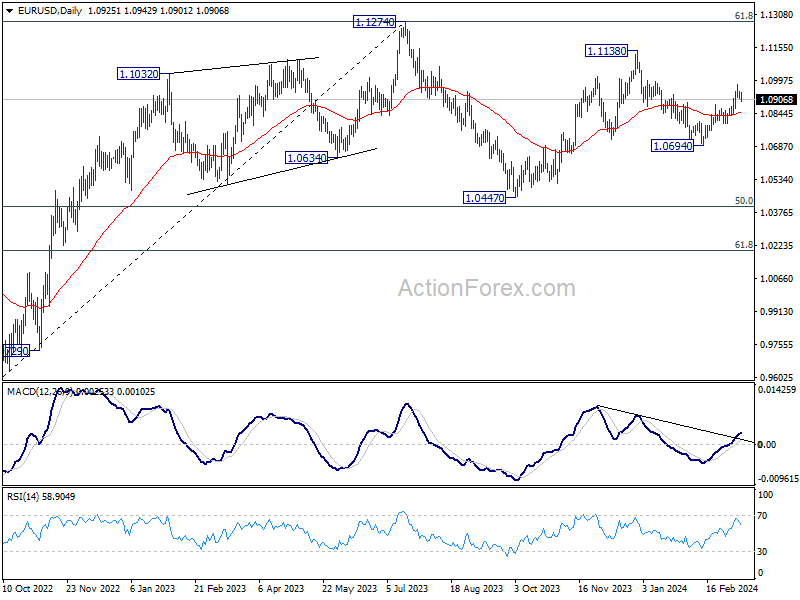

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

US: Core Inflationary Pressures Were (Again) Hotter Than Expected in February

The Consumer Price Index (CPI) rose 0.4% month-on-month (m/m) in February, in line with the consensus forecast. On a twelve-month basis, CPI inched up to 3.2% (from 3.1% in January).

- Energy prices rose 2.3% m/m, largely driven by an uptick in gasoline prices (+3.8% m/m). Conversely, food prices were flat on the month.

Excluding food & energy, core prices rose 0.4% m/m, matching January's gain and coming in a tick above the consensus forecast. The twelve-month change fell 0.1 percentage points to 3.8%.

Prices for core services rose 0.5% m/m – a deceleration from last month's gain of 0.7%. The pullback was related to some easing in both shelter costs (0.4% m/m from 0.6% m/m in January) and non-housing services (up 0.5% m/m from 0.8% m/m in January). However, the three-and-six-month annualized rates of change on non-housing services remain hot at 6.4% and 5.8%, respectively.

Core goods prices unexpectedly ticked higher last month, rising 0.1% m/m. Used vehicle prices (+0.5% m/m) and apparel (+0.6% m/m) both rebounded after having recorded declines in months' prior.

Key Implications

That makes two consecutive months of stronger than expected readings on core inflation. The upward surprise was the result of a modest gain in goods prices – snapping eight prior months of declines – and a still hot reading on non-housing service inflation. As a result, both the three-and-six month annualized readings on core ticked higher in February, rising to 4.2% (from 4.0%) and 3.9% (from 3.6%), respectively.

For a Fed that has become increasingly data dependent, this morning's numbers are unlikely to give policymakers much further conviction that inflation remains on a sustained downward path to 2%. With the economy still strong, Fed officials can afford to keep rates elevated into the summer and continue to wait for further signs of cooling on the inflation front before dialing back the policy rate.

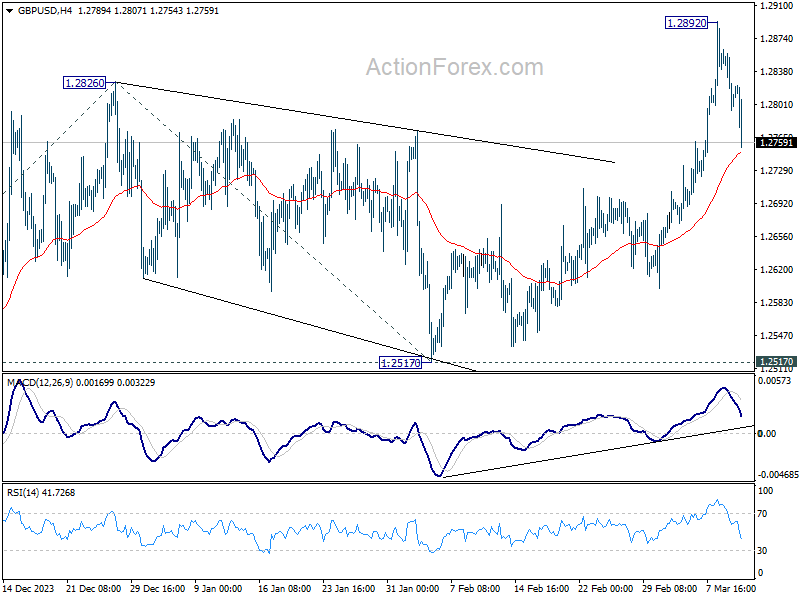

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2784; (P) 1.2825; (R1) 1.2855; More...

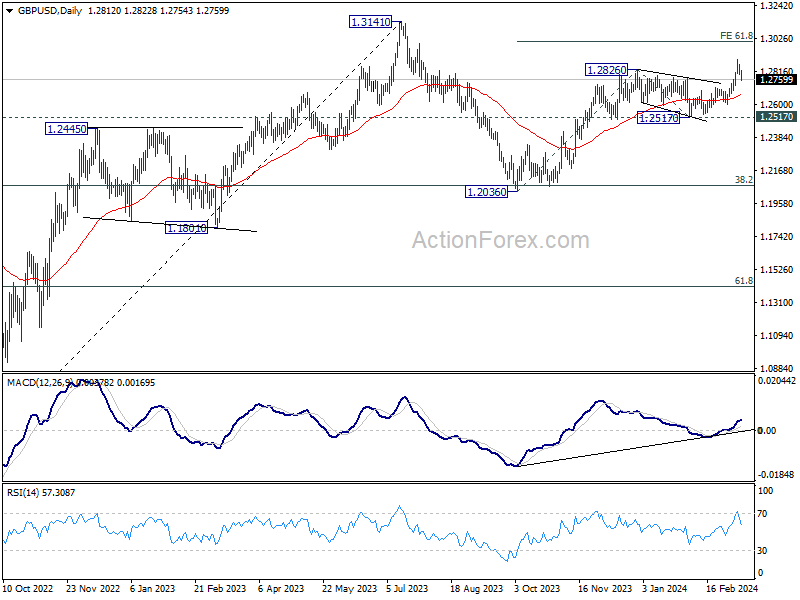

GBP/USD's retreat from 1.2892 extends lower today. But still, further rally will remain in favor as long as 55 4H EMA (now at 1.2746) holds. On the upside, above 1.2892 will resume larger rise from 1.2063 and target 61.8% projection of 1.2036 to 1.2826 from 1.2517 at 1.3005. However, sustained break of 55 4H EMA will bring deeper fall back towards 55 D EMA (now at 1.2662), and possibly further to 1.2517 structural support.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which is still in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2517 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

Dollar Hesitates after Stronger than Expected CPI, Sterling Lower on Job Data

Dollar saw only a temporary uplift from stronger-than-expected CPI figures from the US. The greenback reverted to pre-release levels, while stock futures rebounded. Traders appeared to be refraining from taking decisive bets. This reaction suggests that the inflation data, despite being higher than anticipated, may not be sufficiently influential to deter Fed from cutting interest rate in June. The core inflation rate's modest cooling, alongside perceptions of energy driven headline inflation rise as "transitory," has seemingly tempered immediate concerns over persistent inflationary pressures.

In the UK, Pound faced slight selling pressure following reports of weaker-than-expected wage growth and a slight uptick in the unemployment rate. This economic backdrop is unlikely to prompt BoE to delay its anticipated interest rate cut beyond August. However, the lackluster progress on the wages front does not necessitate an accelerated policy easing from BoE either. With the central bank not under immediate pressure to adjust its policy stance, it will continue its patient approach and wait for more data first.

Across the currency spectrum, Yen emerged as the day's weakest, with enthusiasm regarding next week's potential BoJ rate hike cooled. Sterling is the second weakest followed by Dollar. Australian Dollar is now the strongest, followed by Swiss Franc and New Zealand Dollar. Euro and Canadian are mixed.

Technically, as USD/JPY stabilized around 38.2% retracement of 140.25 to 150.87 at 146.81 focus is now on the strength of the rebound from 146.47. Decisive break of 148.29 minor resistance will argue fall from 150.87 has completed after defending 146.81. That would retain near term bullish in the pair for rising through 150.87 at a later stage.

In Europe, at the time of writing, FTSE is up 1.23%. DAX is up 0.56%. CAC is up 0.23%. UK 10-year yield is down -0.0563 at 4.009. Germany 10-year yield is up 0.002 at 2.308. Earlier in Asian, Nikkei fell -0.06%. Hong Kong HSI rose 3.05%. China Shanghai SSE fell -0.41%. Singapore Strait Times rose 0.10%. Japan 10-year JGB yield rose 0.0014 to 0.768.

US CPI rises to 3.2% yoy in Feb, CPI core down to 3.7% yoy, both above expectations

US CPI rose 0.4% mom in February, matched expectations. CPI core (ex-food and energy) rose 0.4% mom, above expectation of 0.3% mom. Food index was unchanged whole energy index rose 2.3% mom.

Over the 12-month period, headline CPI accelerated from 3.1% yoy to 3.2% yoy, above expectation of 3.1% yoy. CPI core slowed from 3.9% yoy to 3.8% yoy, above expectation of 3.7% yoy. Energy index was down -1.9% yoy while good index was up 2.2% yoy.

UK wages growth slows more than expected in Jan

In February, UK payrolled employment rose 20k or 0.1% mom. Median monthly pay increased by 5.5% yoy. Annual growth in median pay was highest in the other service activities sector, with an increase of 7.4% yoy, and lowest in the finance and insurance sector, with a decrease of -0.3% yoy.

In the three months to January, unemployment rate ticked up to 3.9%, above expectation of 3.8%. Average earnings including bonus rose 5.6% yoy, slowed from 5.8% yoy, below expectation of 5.7% yoy. Average earnings excluding bonus rose 6.1% yoy, down from 6.2% yoy, below expectation of 6.2% yoy.

BoJ's Ueda: Economy recovering gradually despite some signs of weakness

In a parliamentary address today, BoJ Governor Kazuo Ueda noted that Japan's economy is "still recovering gradually", despite acknowledging some recent "signs of weakness".

Ueda highlighted a concerning trend of weakening consumption in food and daily necessities amid rising prices. However, he also pointed out a silver lining with moderate improvements in household spending, fueled by expectations of wage increases.

The anticipation around a rate hike by BoJ has garnered significant attention recently, with Ueda reiterating the bank's focus on the emergence of a "positive wage-inflation cycle." This perspective is crucial for determining the viability of reaching BoJ's inflation targets sustainably and stably.

"Various data have come out since January and we'll likely have additional data come out this week. We will look comprehensively at such data, and make an appropriate monetary policy decision," he said.

Australia NAB business confidence falls to 0, cost pressures clearly remain elevated

Australia's NAB Business Confidence ticked down from 1 to 0 in February. Business Conditions rose from 7 to 10. Trading conditions rose form 9 to 14. Profitability conditions rose from 6 to 9. Employment conditions rose from 5 to 6.

Cost pressures remain a significant concern. Labor (2.0% in quarterly equivalent terms) and purchase cost (1.8%) growth stayed constant. Product price growth rose from 1.1% to 1.3% while retail price growth surged from 0.9% to 1.4%.

Alan Oster, NAB's Chief Economist, pointed out that cost pressures "clearly remain elevated", and there's scope for firms to pass this through to output prices."

He emphasized the role of global supply improvements in driving the progress on disinflation so far, cautioning that future advancements is "unlikely to be linear."

According to Oster, the path to returning inflation within RBA's target band by 2025 is fraught with uncertainties. He predicts a "cautious approach" from RBA, with interest rates to be "on hold for most of this year."

RBA's Hunter: Data broadly in line with expectations

RBA Assistant Governor Sarah Hunter noted that the incoming data were "broadly in line with what we were anticipating." Nevertheless, she emphasized that the central bank is "monitoring and looking" and will be updating the economic forecasts in May.

Hunter also touched on the challenges posed by interest rate hikes, particularly for households finding such adjustments difficult. However, she emphasized that "inflation is the single biggest drag", highlighting RBA's primary focus on managing inflation to ensure economic stability and growth.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2784; (P) 1.2825; (R1) 1.2855; More...

GBP/USD's retreat from 1.2892 extends lower today. But still, further rally will remain in favor as long as 55 4H EMA (now at 1.2746) holds. On the upside, above 1.2892 will resume larger rise from 1.2063 and target 61.8% projection of 1.2036 to 1.2826 from 1.2517 at 1.3005. However, sustained break of 55 4H EMA will bring deeper fall back towards 55 D EMA (now at 1.2662), and possibly further to 1.2517 structural support.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which is still in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2517 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | PPI Y/Y Feb | 0.60% | 0.50% | 0.20% | |

| 23:50 | JPY | BSI Large Manufacturing Index Q1 | -6.7 | 6.2 | 5.7 | |

| 00:30 | AUD | NAB Business Confidence Feb | 0 | 1 | ||

| 00:30 | AUD | NAB Business Conditions Feb | 10 | 6 | ||

| 07:00 | EUR | Germany CPI M/M Feb F | 0.40% | 0.40% | 0.40% | |

| 07:00 | EUR | Germany CPI Y/Y Feb F | 2.50% | 2.50% | 2.50% | |

| 07:00 | GBP | Claimant Count Change Feb | 16.8K | 20.3K | 14.1K | 3.1K |

| 07:00 | GBP | ILO Unemployment Rate (3M) Jan | 3.90% | 3.80% | 3.80% | |

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Jan | 5.60% | 5.70% | 5.80% | |

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Jan | 6.10% | 6.20% | 6.20% | |

| 10:00 | USD | NFIB Business Optimism Index Feb | 89.4 | 90.7 | 89.9 | |

| 12:30 | USD | CPI M/M Feb | 0.40% | 0.40% | 0.30% | |

| 12:30 | USD | CPI Y/Y Feb | 3.20% | 3.10% | 3.10% | |

| 12:30 | USD | CPI Core M/M Feb | 0.40% | 0.30% | 0.40% | |

| 12:30 | USD | CPI Core Y/Y Feb | 3.80% | 3.70% | 3.90% |