Sample Category Title

UK GDP Data and Euro Area Industrial Production Figures on Today’s Menu

In focus today

In the euro area, we receive industrial production figures for January. It will be interesting to see how actual production fared in January as soft indicators have shown improvements and the global manufacturing cycle has bottomed out. Also, the ECB is set to unveil its new operational framework.

In the UK, at 8:00 CET we get the monthly GDP figures for January.

In Sweden, today's focus is on speeches from Riksbank deputy governors Flodén at 08:50 CET and Breman at 09:00 CET regarding the economic situation and current monetary policy.

Economic and market news

What happened overnight

In the US, as highly anticipated, the presidential election this year will very likely be a rematch of the 2020 election, as both President Joe Biden and former President Donald Trump secured the required number of delegates to become their parties' nominees. However, this was unofficially confirmed last week when Nikki Haley pulled out of the race.

In Japan, Reuters sources reported that the BoJ is likely to provide numerical guidance on its future bond purchases after it is soon expected to exit its long-standing yield curve control policy and negative rates. Purchases would remain close to current levels to avoid abrupt spikes in yields. Furthermore, some of the biggest Japanese companies, including Toyota, Panasonic, and Nissan, have offered their largest pay raises in decades during the annual wage negotiations. Hence, this could add support to sustainable inflation pressure.

In Europe, Governing Council member Pierre Wunsch (hawk) reiterated that the ECB may need to take a risk by implementing an interest rate cut soon, despite concerns over high wage inflation and service price increases.

What happened yesterday

In the US, February CPI came in slightly above expectations. Headline inflation was 0.44% m/m SA (consensus +0.4%) while core inflation was 0.36% m/m SA (consensus 0.36%), The details were somewhat concerning for the Fed as well - for instance non-housing services inflation, which is the key point of focus for the Fed, remained steady from January. For more details, see Global Inflation Watch, 12 March. Additionally, the NFIB's February survey showed that the small business optimism index edged down to the lowest level since May amid inflation concerns.

In Germany, the final inflation print confirmed the flash release of 2.5% y/y (0.4% m/m) increase in CPI and core CPI at 3.4% y/y. The underlying details reveal a softer inflation print than the headline figure due to package holidays and the VAT increase on food in restaurants.

In the UK, the labour report for January/February was released yesterday. Wage growth came in lower than expected across the board with average weekly earnings excl. bonus at 6.1% 3M/YoY. Similarly, the KPMG/REC report on UK jobs, which was released early Monday night showed continued broad easing in the labour market with starting salaries rising at the slowest pace for almost three years and vacancies declining rapidly. With official data still suffering from poor data quality, the BoE increasingly relies on the KPMG/REC survey as a leading indicator for wage growth and of labour market tightness.

On the geopolitical stage, President Biden announced that the US will provide a new USD 300m military aid package for Ukraine - albeit the USD 300m is merely a fraction of a USD 60bn aid package Congress has debated over the past few months. Likewise, the EU is set to agree on a new EUR 5bn military aid fund later today, reported by the Financial Times yesterday. Finally, a vessel carrying 200 tonnes of food for Gaza departed from Cyprus, which is part of a pilot project to establish a new sea route for aid to Gaza.

Equities: Global equities were higher yesterday despite a mixed US CPI report and higher yields. Looking at the sector rotation it also reveals this was not just about a very benign inflation outlook but also part of what we call the AI-frenzy with very elevated volatility in some single names. This sign of exuberance is as a standalone negative for the equity outlook. In US yesterday, Dow +0.6%, S&P 500 +1.1%, Nasdaq +1.5% and Russell 2000 -0.02%. Asian markets are mixed this morning with Japan lower and China higher. US and European futures are mostly positive.

FI: Global rates zig zagged as the immediate reaction to the US inflation release yesterday, but the market interpretation ended up being clearly to the hawkish side. The US treasury curve bear flattened as markets shaved off expectations for US rate cuts in 2024. 10Y UST yields were up 6bp, while the US breakeven inflation curve rose from the front. 10Y Bund yields rose 3bp with the Bund ASW-spread continuing to drift lower, ending the day in 30.1. The tightening of spreads was also evident in the 10Y BTP-Bund, which dropped to 127bp yesterday - the lowest since end-2021.

FX: The US CPI pushed yields higher, which in turn supported the greenback. NOK and JPY struggled vs the USD, and EUR/GBP ended the day higher amid a weak UK labour market report. NOK/SEK traded heavy and hit the lowest levels since December.

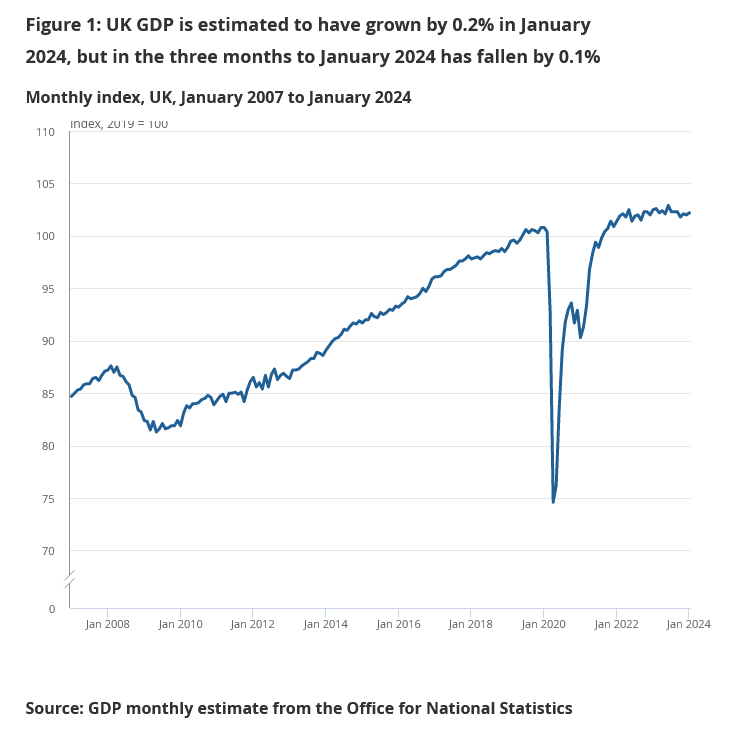

UK GDP grows 0.2% mom in Jan, matches expectations

UK GDP expanded by 0.2% mom in January, matched expectations. Services was up 0.2% mom, and was the largest contributor to growth. Production fell -0.2% mom while construction grew 1.1% mom.

In the three months to January, GDP has fallen by -0.1% 3mo3m. Services was flat. Production fell -0.2% 3mo3m. Construction fell -0.9% 3mo3m.

CHF/JPY Technical: Potential Major Bullish Trend Exhaustion

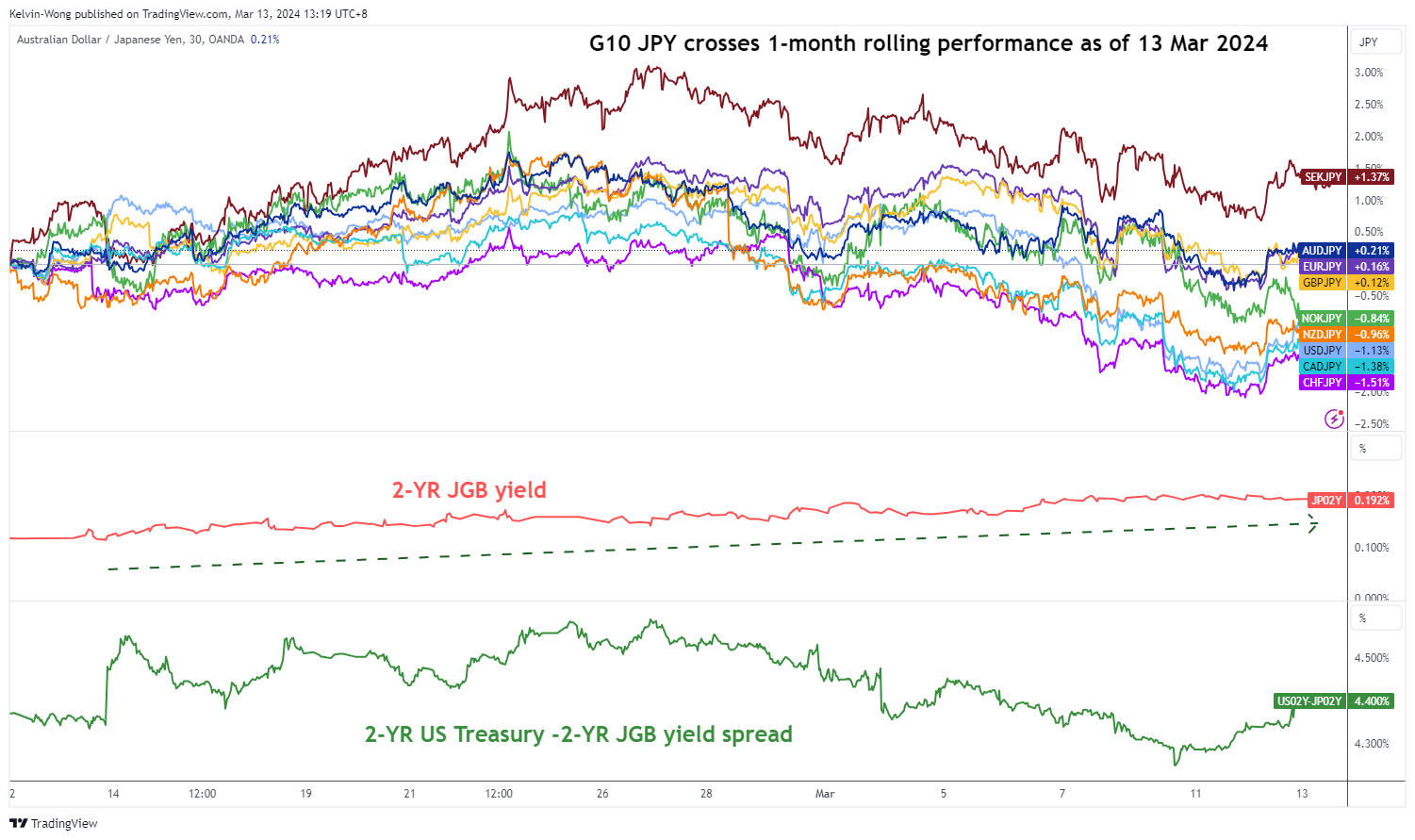

- The recent significant increase of a total of 20 bps in the 2-year JGB yield since the start of the year has come in line with the highly anticipated rosy results of the annual wage negotiations in Japan.

- In the past week, the JPY crosses have come under downside pressure as the carry trade strategy loses its appeal.

- Watch the 168.75 key short-term resistance on the CHF/JPY.

The JPY crosses have continued to face downside pressure in the recent week ahead of key related risk events such as the release of the preliminary FY 2024/2025 wage negotiation results in Japan by the latest labour union federation, Rengo on this Friday, 15 March (see Fig1).

Expectations have been optimistic as the consensus forecast is pegged at an average pay rise of 3.85% for FY 2024/2025 (above last year’s annualized gain of 3.58%), and if It turns out as expected, it will be the largest wage increase in Japan since 1993.

JPY crosses under downside pressure as carry trade strategy loses appeal

Fig 1: 1-month rolling performances of G-10 JPY crosses as of 13 Mar 2024 (Source: TradingView, click to enlarge chart)

The CHF/JPY is the worst performer among the JPY crosses as it shed -1.50% based on a one-month rolling performance basis as of today, 13 March in line with the rosy anticipated outcome of the Japanese employee’s wage negotiation results.

The primary driver of JPY strength has been the rising 2-year Japanese Government Bond (JGB) yield as it rose by a whopping 20 basis points (bps) from close to 0% at the start of January to 0.20% on 11 March as market participants have started to price in a more hawkish Bank of Japan (BoJ) going forward to either scrapped off its short-term negative interest rates policy next Tuesday, 19 March or on the 26 April monetary policy meeting.

Bearish “Ascending Wedge” detected in CHF/JPY

Fig 2: CHF/JPY major & medium-term trends as of 13 Mar 2024 (Source: TradingView, click to enlarge chart)

The major uptrend phase of CHF/JPY in place since the 13 January 2024 low of 137.44 is likely in jeopardy through the recent appearance of an impending bearish “Ascending Wedge” configuration that has taken shape from the 3 October 2023 low (see Fig 2).

The formation of the “Ascending Wedge” suggests a potential major bullish trend exhaustion condition as the magnitude of its upper boundary that connects its “higher highs” is lesser than the slope of its “lower lows” (lower boundary).

In addition, the daily RSI momentum indicator has flashed a bearish divergence condition.

Oscillating within a minor descending channel

Fig 3: CHF/JPY short-term trend as of 13 Mar 2024 (Source: TradingView, click to enlarge chart)

In the shorter term as seen on its hourly chart, the price actions of CHF/JPY have started to oscillate within a minor descending channel in place since 29 February 2024 high of 171.50.

If the 168.75 short-term pivotal resistance is not surpassed to the upside, it may see further potential weakness to expose the next intermediate support at 166.55 (close to the lower boundary of the “Ascending Wedge) in the first step (see Fig 3).

On the other hand, a clearance above 168.75 negates the bearish tone for the next near-term resistance to come in at 169.50 (also the downward-sloping 20-day moving average).

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3463; (P) 1.3495; (R1) 1.3522; More...

Intraday bias in USD/CAD remains neutral for the moment. On the downside, break of 1.3419 and sustained trading below 1.3439 support will argue that rebound from 1.3176 has completed as a corrective move to 1.3605. Near term outlook will be turned bearish for 1.3357 support first. On the upside, though, break of 1.3524 minor resistance will revive near term bullishness, and turn bias back to the upside for retesting 1.3605 resistance instead.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 at a later stage.

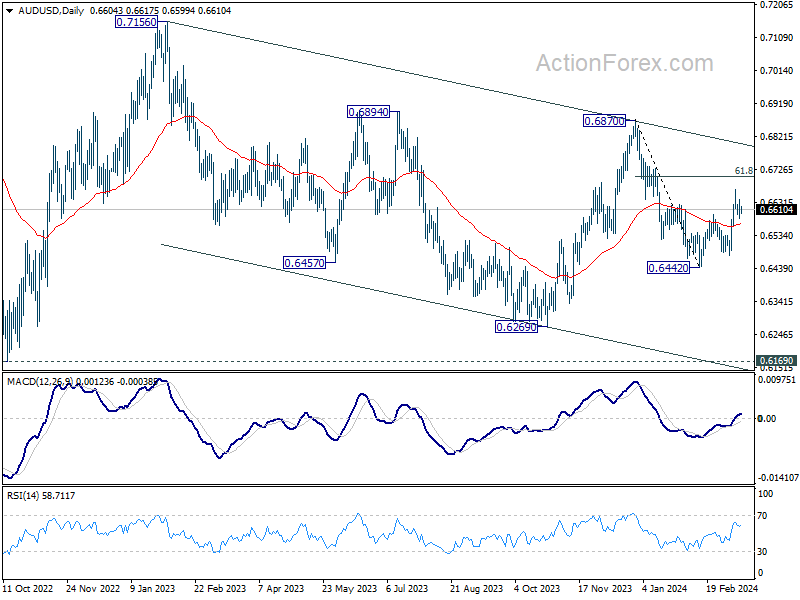

AUD/USD Daily Report

Daily Pivots: (S1) 0.6581; (P) 0.6610; (R1) 0.6635; More...

Intraday bias in AUD/USD stays neutral at this point. Another rise will be mildly in favor as long as 55 4H EMA (now at 0.6577) holds. Above 0.6666 will resume the rebound from 0.6442 to 61.8% retracement of 0.6877 to 0.6442 at 0.6707 next. Sustained trading above there will argue rise from 0.6442 is probably resuming whole rally from 0.6269. Nevertheless, sustained break of 55 4H EMA will revive near term bearishness and bring retest of 0.6442 low instead.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which might still be in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.

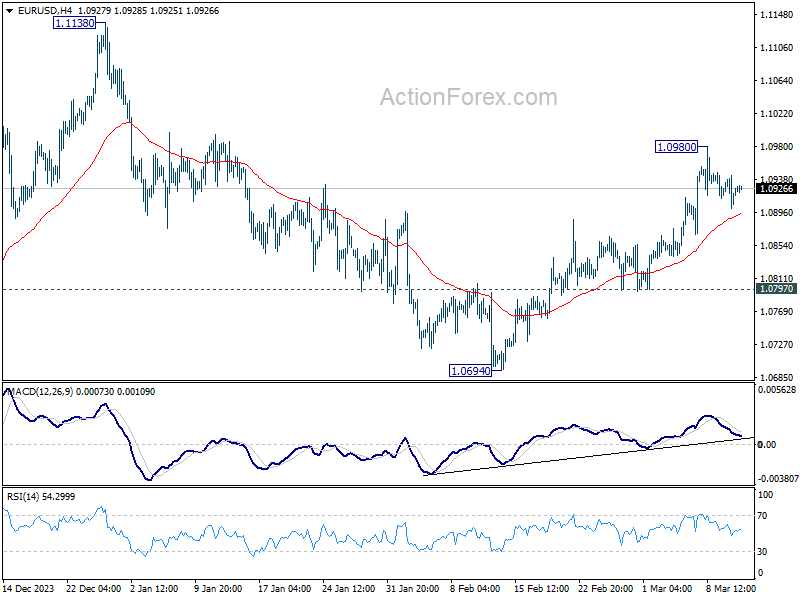

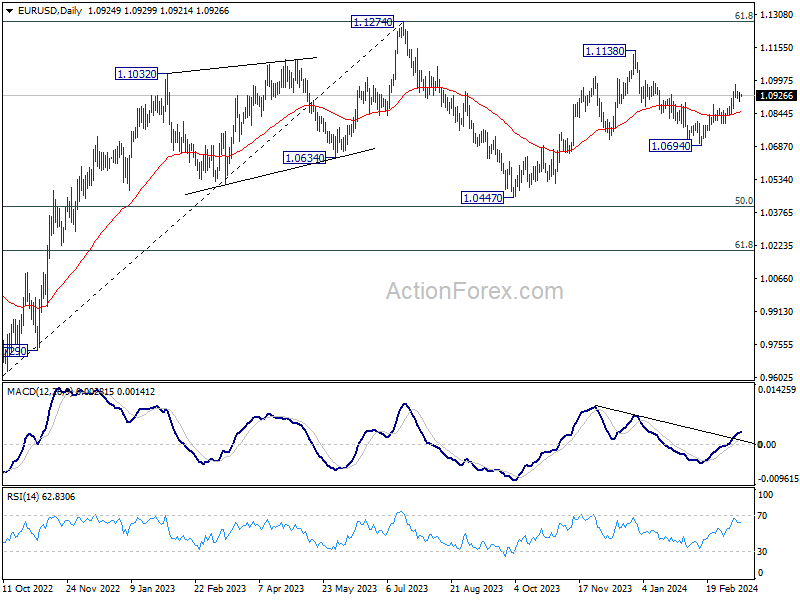

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0904; (P) 1.0924; (R1) 1.0946; More...

Intraday bias in EUR/USD remains neutral for the moment. Further rise is in favor as long as 55 4H EMA (now at 1.0892) holds. Above 1.0980 will resume the rally from 1.0694 to retest 1.1138 high). However, sustained break of the EMA will turn bias to the downside for 1.0797 support instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

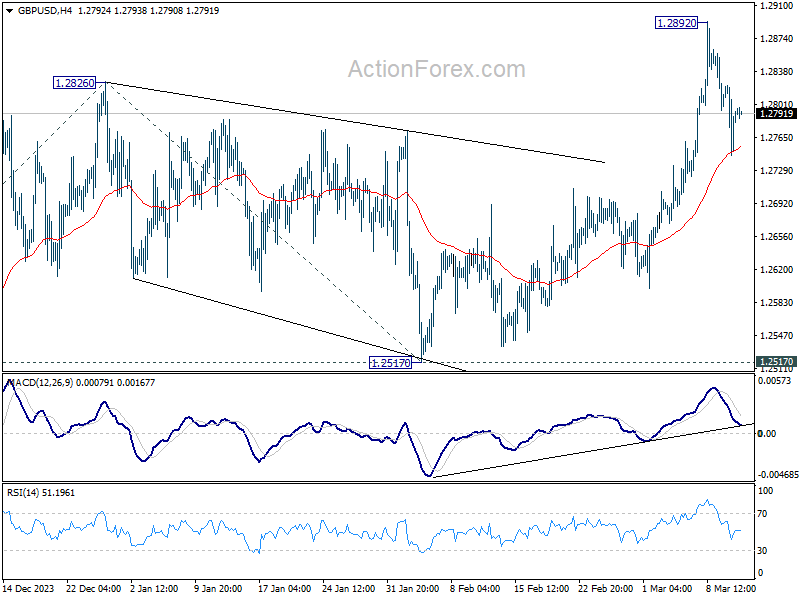

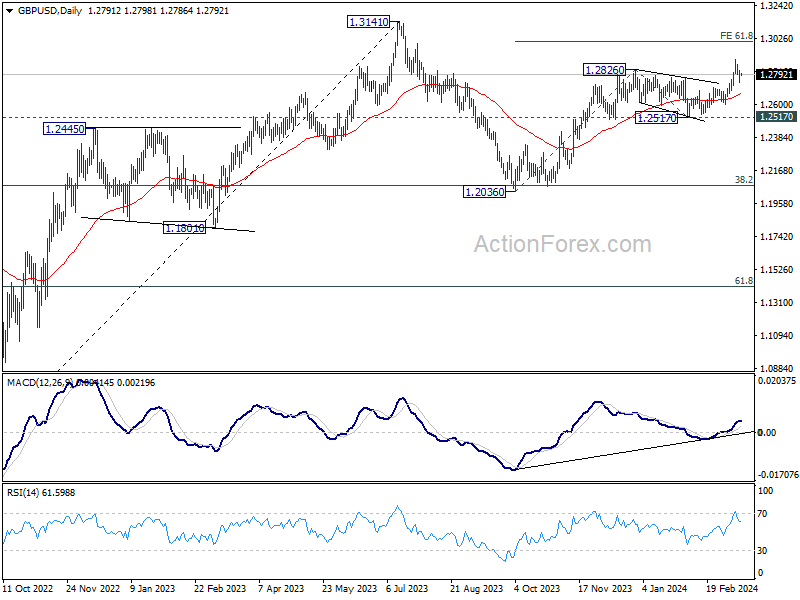

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2751; (P) 1.2788; (R1) 1.2829; More...

Intraday bias in GBP/USD remains neutral for the moment. Further rally will remain in favor as long as 55 4H EMA (now at 1.2755) holds. On the upside, above 1.2892 will resume larger rise from 1.2063 and target 61.8% projection of 1.2036 to 1.2826 from 1.2517 at 1.3005. However, sustained break of 55 4H EMA will bring deeper fall back towards 55 D EMA (now at 1.2662), and possibly further to 1.2517 structural support.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which is still in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2517 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

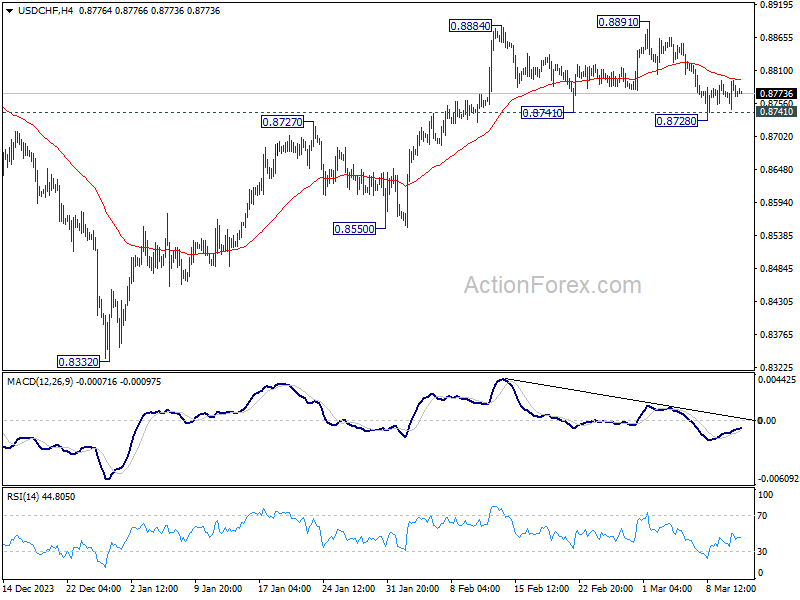

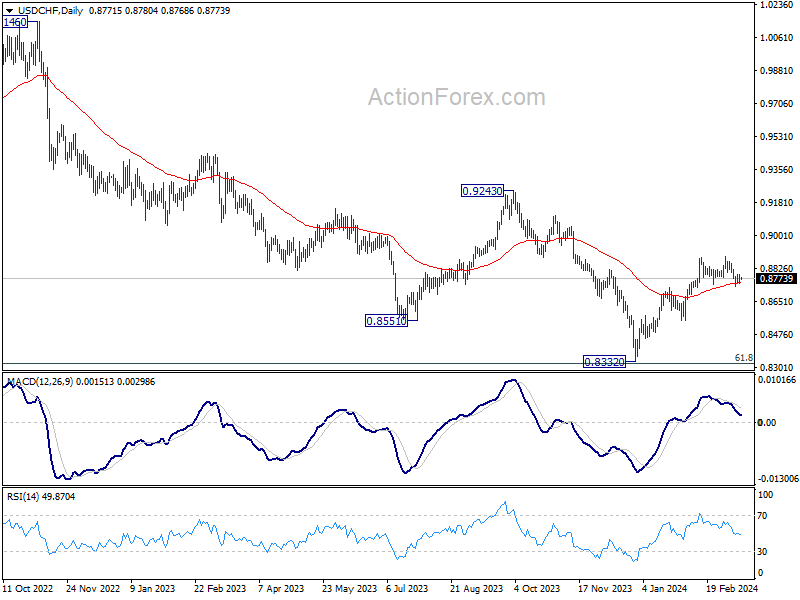

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8748; (P) 0.8772; (R1) 0.8796; More....

USD/CHF is staying in tight range above 0.8728 and intraday bias stays neutral. On the downside, sustained break of 0.8741 will argue that the whole rebound from 0.8332 might have completed, and bring deeper fall to 0.8550 support. Nevertheless, strong bounce from current level will retain near term bullishness. Further break of 0.8891 will resume the rise from 0.8332.

In the bigger picture, price actions from 0.8332 medium term bottom as seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8555 support holds. But upside should be limited by 0.9243 resistance, at least on first attempt.

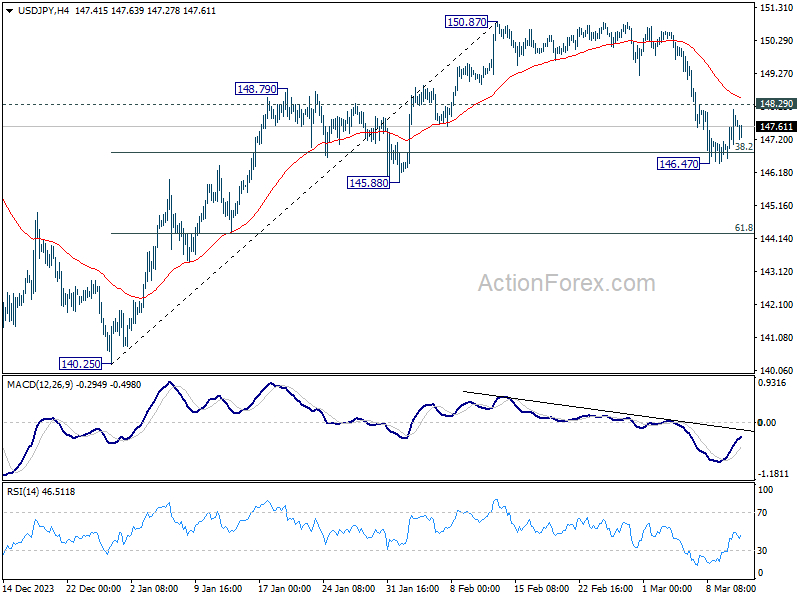

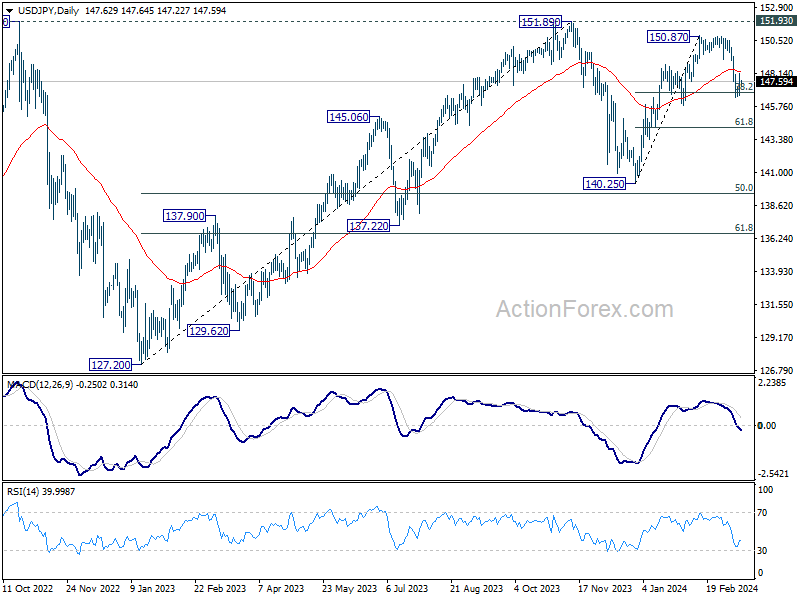

USD/JPY Daily Outlook

Daily Pivots: (S1) 146.85; (P) 147.44; (R1) 148.27; More...

Intraday bias in USD/JPY remains neutral for the moment, and outlook is unchanged. On the downside, sustained break of 38.2% retracement of 140.25 to 150.87 at 146.81 will argue that fall from 150.87 is reversing the whole rally from 140.25. In this case, deeper decline would be seen to 61.8% retracement at 144.30 and below. Nevertheless, strong support from 146.81, followed by break of 148.29 minor resistance resistance, will argue that fall from 150.87 is merely a correction, which has completed already. Retest of 150.87 should be seen next.

In the bigger picture, no change in the view that price action from 151.89 (2023 high) are correction to up trend from 127.20 (2023 low). The question is whether this correction has completed at 140.25, or extending with fall from 150.87 as the third leg. Sustained break of above mentioned 146.81 fibonacci level will favor the latter case. But even so, downside should be contained by 50% retracement of 127.20 to 151.89 at 139.54.

Yen Slightly Firmer on Wage Growth Prospects, Dollar Rally Capped

In today's subdued Asian session, the currency markets saw minimal movement, with most major pairs and crosses gyrating within yesterday's range. Japanese Yen managed to carve out modest gain, buoyed by optimistic remarks and tangible actions related to wage growth within the country. Chief Cabinet Secretary Yoshimasa Hayashi's commentary on seeing "strong momentum" for wage increases provides a beacon of hope for substantial wage growth, particularly among small and mid-sized firms—a crucial component for a balanced economic uplift.

This sentiment is further reinforced by landmark wage agreements by stalwarts of Japan's industrial sector, including Toyota Motor which agreed to raise workers' wages by the largest rate in 25 years. Meanwhile, Panasonic and Nissan committed to meet union demands in full.

Despite these positive developments, BoJ's stance on interest rate adjustments remains cautiously in the balance. Reports suggest that while a decision on hiking interest rates next week is nearing, it has not been conclusively reached.

Dollar's performance is mixed, failing to capitalize significantly on the post-CPI rebound. While, recovery in 10-year yield provided some support, the greenback's advances were capped by robust risk-on sentiment, evidenced by a new record close for S&P 500. The market's expectations for a Fed rate hike in June have moderated slightly from 72% to 66%, according to Fed funds futures, yet the anticipation of such a move remains a cornerstone of current market projections.

Overall in the markets, , Sterling is currently as the week's weakest link, with investors keenly awaiting today's UK GDP data for directional cues. Yen and Kiwi are the next weakest. On the other hand, Dollar is the strongest followed by Swiss Franc and Canadian. Euro and Aussie are mixed in the middle. But still, it's emphasized that all major pairs and crosses are stuck inside last week's range, suggesting that consolidative trading is still in progress.

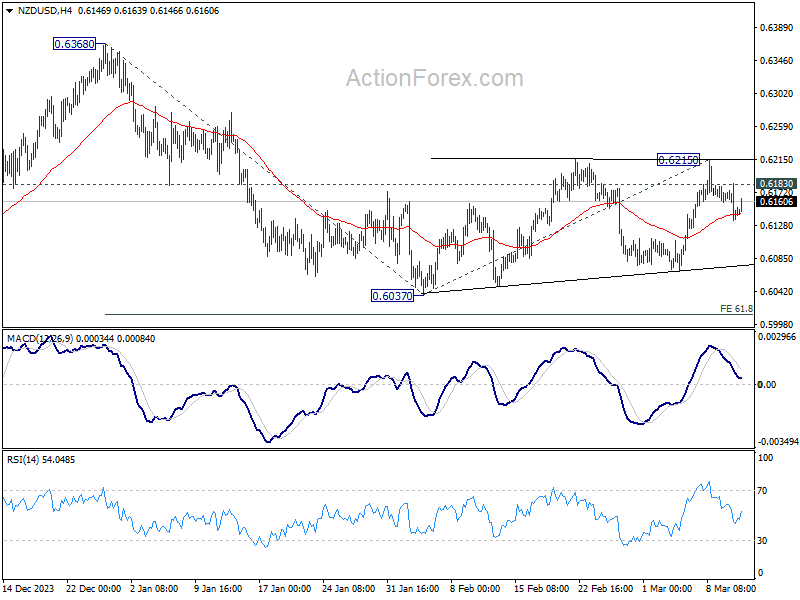

Technically, NZD/USD recovered mildly after hitting 55 4H EMA (now at 0.6143). But risk is mildly on the downside as long as 0.6183 minor resistance holds. Sustained break of the EMA will argue that corrective pattern from 0.6037 has completed with three waves to 0.6215. In this case, fall from 0.6368 would be ready to resume through 0.6037. If realized, the next down move in NZD/USD would likely be accompanied by AUD/USD's fall towards 0.6442 support.

In Asia, at the time of writing, Nikkei is down -0.17%. Hong Kong HSI is up 0.50%. China Shanghai SSE is down -0.07%. Singapore Strait Times is up 0.54%. 10-year JGB yield is down -0.0044 at 0.764. Overnight, DOW rose 0.61%. S&P 500 rose 1.12%. NASDAQ rose 1.54%. 10-year yield rose 0.051 to 4.155.

BoE's Bailey surge in unemployment unnecessary on tackling inflation

BoE Governor Andrew Bailey expressed a more positive stance on the UK's inflation scenario compared to a year ago, particularly regarding the potential for "second round effects" to drive further price surges.

At a panel discussion at the Bank of Italy Symposium, he noted there is "very limited evidence so far" that an uptick in unemployment is a prerequisite for reigning in inflationary pressures.

Bailey highlighted the UK's labor market status, pointing out that the country is near or at full employment. "It doesn't get a lot of comment, but we have seen very limited evidence so far of an increase in unemployment as a sort of necessary condition of reducing inflation," he added.

ECB's Villeroy sees broad agreement for Spring rate cut

In an interview with Le Figaro, ECB Governing Council member Francois Villeroy de Galhau revealed a "very broad agreement" within the council to initiate rate cuts in spring, with lasts until end of June.

Villeroy, who also serves as Governor of Bank of France, expressed optimism that "we're winning the battle against inflation". The bank lowered core inflation forecast for 2024 from 2.8% to 2.4%. This revision aligns with more moderate wage increases, with average salaries expected to rise by 3.2%, down from the previously predicted 4.1%.

On the growth front, Bank of France downgraded its 2024 growth projections slightly from 0.9% to 0.8%, with expectations for an acceleration to 1.5% in 2025 and 1.7% in 2026. Villeroy confidently stated, "France will avoid recession."

ECB's Wunsch: We have to make a bet at some point

ECB Governing Council member Pierre Wunsch emphasized the need for proactive stance on interest rates, acting on the fact that "inflation has gone down, is moving in the right direction".

Speaking at a news conference for the Belgian national bank's annual report, Wunsch candidly expressed that ECB is nearing a point where it must "make a bet" on cutting interest rates.

However, he was quick to temper expectations, noting that any decision to cut rates would be made carefully, with a keen eye on the persisting challenges of "service inflation and wage developments", which are "still running at levels that are ultimately not compatible with our objective"

Despite these concerns, Wunsch indicated that ECB would not delay rate cuts until wage growth falls to 3%.

Looking ahead

UK will release GDP, production and trade balance in European session. Eurozone will release industrial production. North America calendar is empty.

USD/JPY Daily Outlook

Daily Pivots: (S1) 146.85; (P) 147.44; (R1) 148.27; More...

Intraday bias in USD/JPY remains neutral for the moment, and outlook is unchanged. On the downside, sustained break of 38.2% retracement of 140.25 to 150.87 at 146.81 will argue that fall from 150.87 is reversing the whole rally from 140.25. In this case, deeper decline would be seen to 61.8% retracement at 144.30 and below. Nevertheless, strong support from 146.81, followed by break of 148.29 minor resistance resistance, will argue that fall from 150.87 is merely a correction, which has completed already. Retest of 150.87 should be seen next.

In the bigger picture, no change in the view that price action from 151.89 (2023 high) are correction to up trend from 127.20 (2023 low). The question is whether this correction has completed at 140.25, or extending with fall from 150.87 as the third leg. Sustained break of above mentioned 146.81 fibonacci level will favor the latter case. But even so, downside should be contained by 50% retracement of 127.20 to 151.89 at 139.54.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 07:00 | GBP | GDP M/M Jan | 0.20% | -0.10% | ||

| 07:00 | GBP | Manufacturing Production M/M Jan | 0.00% | 0.80% | ||

| 07:00 | GBP | Manufacturing Production Y/Y Jan | 2.00% | 2.30% | ||

| 07:00 | GBP | Industrial Production M/M Jan | 0.00% | 0.60% | ||

| 07:00 | GBP | Industrial Production Y/Y Jan | 0.70% | 0.60% | ||

| 07:00 | GBP | Goods Trade Balance (GBP) Jan | -15.0B | -14.0B | ||

| 10:00 | EUR | Eurozone Industrial Production M/M Jan | -1.00% | 2.60% | ||

| 13:00 | GBP | NIESR GDP Estimate (3M) Feb | -0.10% | |||

| 14:30 | USD | Crude Oil Inventories | 0.9M | 1.4M |