Sample Category Title

Up Go Stocks, Down Go Bonds

We knew that yesterday was going to be a good day – at least for the stock markets, given that Nvidia defied the expectations that it would - maybe – fail to deliver $20bn sales in the latest quarter. But the company announced $22bn sales. And because a potential misstep from Nvidia was seen as a major risk of a downside correction in stock markets, equity bulls broke their chains free after the blowout earnings. The star of the past two years, the most important stock on planet Earth, or the AI revolution’s mascot Nvidia ended up jumping 16% in a single session and stole the title of the biggest one day jump from Meta – which had just obtained this title after its latest quarterly report a couple of weeks ago. Nvidia added $277 billion to its market cap just yesterday. Morgan Stanley raised its price target from $750 to $795, and Bank of America raised its target from $800 to $925. Allez, let’s round it up to $1000 and see if Nvidia could hit that $1000 mark!

Euphoria and fun aside, the expectation that the narrow stock rally, mainly shouldered by tech, would broaden up has dissipated like dust in the sky in the aftermath of the first earnings season of the year. Tech, and everything related to tech is doing just fine. And the others surf on that optimism. The S&P500 rallied more than 2% and hit a fresh record yesterday and the rally is accelerating above the October 2022 to now ascending range. Nasdaq 100 soared 3% and traded close to an ATH. The Dow Jones industrial, European Stoxx 600 and Japanese Nikkei 225 traded at an ATH as well.

Investors are still wondering whether the US stocks haven’t become too expensive – because the S&P500’s PE ratio is around 23. In this context, Japanese stocks, which also benefit from the AI boom, extra-low Japanese rates, and super cheap Japanese yen trade with a PE ratio of only 16. That makes the Japanese stocks a good alternative for investors who want to increase their AI exposure and diversify geographically. Nikkei’s two heavy weights: Tokyo Electron – that makes semiconductor manufacturing equipment and Adventest – which builds chip-testing machines are both doing great.

And oh, there is also the idea that the Chinese chipmakers would be a cheap option to the US and Japanese counterparts. Yes, the Chinese chipmakers have no option but to fill in the gap from the US export ban. The Chinese companies will be constrained to buy Made-in-China chips, and the Chinese government will put all its weight to make things work – because they can’t afford to fall behind the biggest technology race of the decade. But investing in China implies taking the Chinese government risk. The question is: is growth potential in China big enough to take that risk? At this point, when the world is rushing to AI, I don’t think that the Chinese demand is necessarily needed. (Answer: not necessarily). And speaking of China – real quick – the latest data showed that new home prices dropped the most in 10 months. China’s property crisis gives no signs of improving. On the contrary.

FX and commodities

The cheery mood in the global stock markets was completely decoupled with the gloomy mood in the sovereign space. The US 2 and 10-year yields rose yesterday because some more Federal Reserve (Fed) members warned about cutting the US rates too early and too much. Yesterday’s stronger-than-expected manufacturing and housing data came as further evidence that the US economy doesn’t necessarily need rate cuts in a rush. But the US dollar appetite was nowhere to be found, the dollar index remains offered into the 100-DMA. The 3-month risk reversals of the USD against EM currencies showed that option traders are the least bullish on the US dollar against EM currencies since 2007. That’s interesting, because the US economic data continues to surprise to the upside. The Fed rate cut expectations are being scaled back, yet the dollar doesn’t gain the attraction that it deserves. That’s a good thing, mind you, to prevent the US inflation from spilling to the rest of the world, but it’s not fully rational.

Anyway, in Europe, inflation data came as no surprise while the PMI data showed that activity hit an 8-month high in February. But cracks are widening with German manufacturing falling to the lowest levels since October. Still, the German 10-year bund yield rose to 2.50% and the EURUSD shortly tested its 50-DMA – near 1.0883 – to the upside yesterday and is trying to clear its 200-DMA sustainably. The retreat in dovish European Central Bank (ECB) expectations support the euro’s rebound against the greenback, as the market pricing now suggests less than 100bp cut from the ECB this year.

In energy, US crude advanced to $79 per barrel yesterday after a lower-than-expected jump in US oil inventories last week, while nat gas futures are having a hard time rebounding after a dip to 1.55. The European nat gas futures continue to push lower as traders are selling nat gas for next winter – a sign of confidence that Europe will continue to receive the Russian gas shipments as we near the second anniversary of Russia’s invasion of Ukraine. Europe is not less shocked faced with a war on its continent but is clearly less capable of putting more restrictions on Russian energy – given the cost-of-living crisis and Germany’s descent into hell. Therefore, buying defense stocks is a better way to navigate through war in Europe than buying nat gas futures.

AI Surge Fuels Stock Market Gains

In focus today

The main event today will be the German Ifo print for February. The Ifo survey covers many more companies than the PMIs and it has somewhat contrasted the uptick seen in manufacturing PMIs previously. Moreover, the Ifo survey is yet to bottom out and expectations have not moved up in contrast to the ZEW.

Economic and market news

What happened overnight

Things were generally quiet overnight. In China, prices of newly built homes in tier-1 cities fell 0.7% y/y. Both Fed Governors Lisa Cook and Cristopher Waller suggested they needed more confidence that inflation was normalizing before they could cut rates, with Waller specifically noting he would need "at least another couple of months of inflation data". We expect the Fed will deliver its first cut in May.

What happened yesterday

Yesterday was a great day for stock prices as it seems that AI-optimism fuelled a market boom, after Nvidia beat quarterly earnings expectations by some margin. Tech stocks were the big winner with the Nasdaq Composite up 2.96%, but broader indices such as the MSCI world and European STOXX600 also gained, with the latter hitting an ATH driven particularly by tech stocks.

We also got a slew of data from the euro area. First, euro area composite PMIs for February drew a mixed picture with service PMIs beating expectations and manufacturing PMIs declining, especially due to a plunge in German manufacturing PMIs. The figures indicated increasing price pressure in services, which is a worrying sign for the ECB. The ECB minutes from the January meeting showed policymakers signalling patience and caution in easing too early. Final HICP inflation confirmed the flash headline inflation estimate of 2.8% y/y but suggested softer underlying inflation momentum than the flash estimate, however, this was in large part due to one-offs and tax increases.

We also got PMIs from both the UK and US, which overall were not game changers, reflected also in muted market reactions. The UK figures suggested modest growth in Q1 2024 especially due to services, while US PMIs painted a positive outlook for manufacturing which rose to 51.5, especially due to new orders (domestic and foreign), while services saw weaker incoming new business.

Equities: Global equities were markedly higher yesterday with so many interesting aspects. Nikkei 225 made the first all-time high in nearly 35 years, up almost 17% year to date. Stoxx 600 set new all-time high together with S&P500, and Nasdaq had its best session in more than a year. We make two conclusions: This is not just about seven stocks in the US. Secondly, tomorrow it has been two years since Russia invaded Ukraine, the war is still ongoing and MSCI world has returned more than 20% in the same period. Please be careful in underestimating the power of macro impact on financial markets and overestimating the impact of geopolitics. In US yesterday, Dow +1.2%, S&P 500 +2.1%, Nasdaq +3.0% and Russell 2000 +1.0%. Asian markets are mixed this morning with the Japanese market closed. US and European futures are marginally higher.

FI: 10y European yields spiked 5bp on the better-than-expected French PMI data, however it was quickly reversed following the abysmal German manufacturing PMI. Through the mid-day session with the final euro area inflation print and the ECB minutes yields gradually declined. Although none of the two inputs resulted in dovish vibes, the yield decline extended through the slightly lower than expected US PMI in the afternoon. Noteworthy, the better than anticipated jobless claims did not change markets. 10y Bunds ended 1bp lower on the day at 2.44% after breaking 2.5% through the day. The European curves bear flattened around the 10y point, with markets taking out central bank easing expectations now pointing to ECB rate cuts worth less than 100bp this year, while the long end rallied 4bp.

FX: Another good day for the SEK, which rose together with NZD and GBP, while NOK and JPY were the biggest loses. EUR/USD was on a roller coaster ride amid mixed signals from the release of flash PMIs first rising close to 1.09 before ending the day where it started just above the 1.08 level.

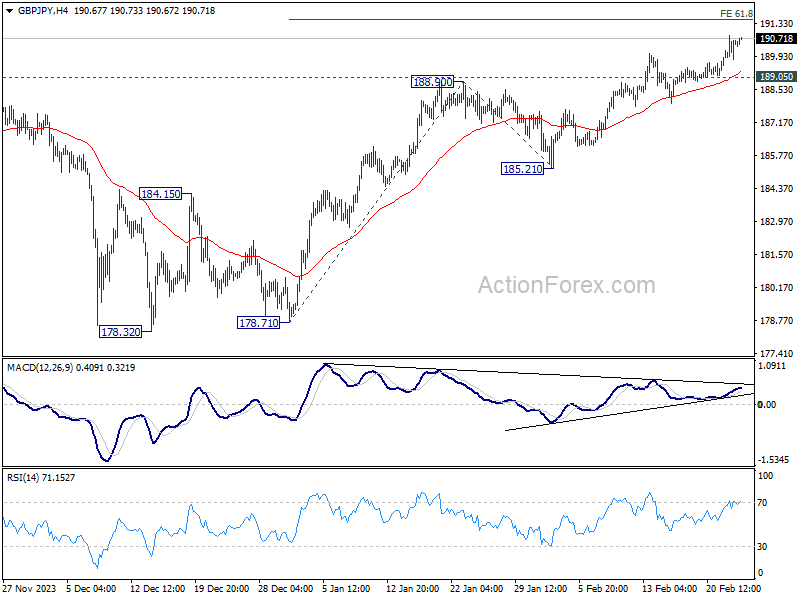

GBP/JPY Daily Outlook

Daily Pivots: (S1) 190.02; (P) 190.43; (R1) 191.00; More...

Intraday bias in GBP/JPY remains on the upside at this point. Current rally is in progress for 61.8% projection of 178.71 to 188.90 from 185.21 at 191.50. Firm break there will target 100% projection at 195.40. On the downside, below 189.05 minor support will turn intraday bias neutral and bring consolidations again, before staging another rally.

In the bigger picture, up trend from 123.94 (2020 low) in in progress. Medium term outlook will stay bullish as long as 178.32 support holds. Next target is 195.86 long term resistance (2015 high).

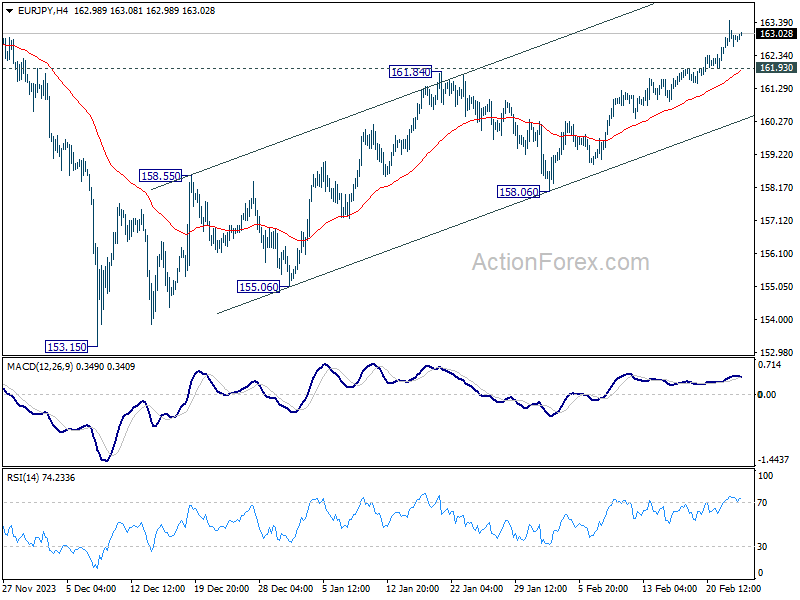

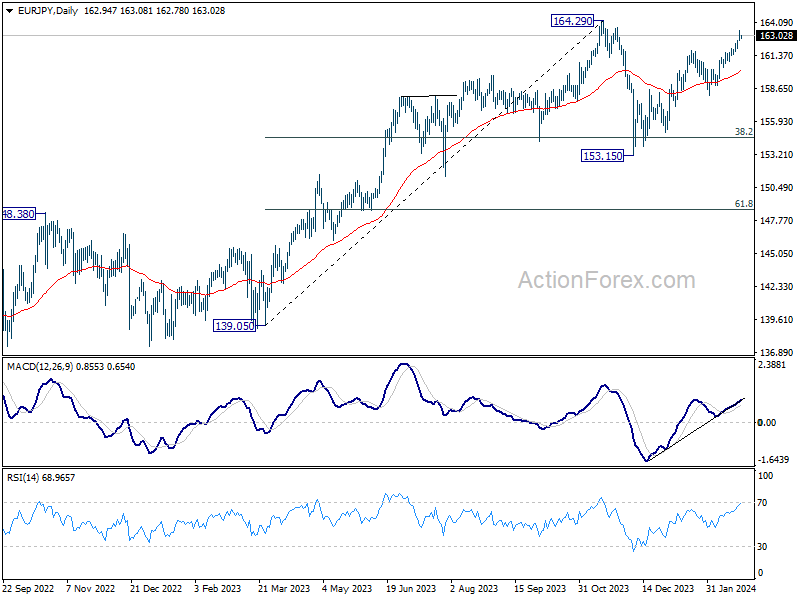

EUR/JPY Daily Outlook

Daily Pivots: (S1) 162.48; (P) 162.97; (R1) 163.44; More...

Intraday bias in EUR/JPY remains on the upside, as rise from 153.15 is in progress for retesting 164.29 high. Decisive break there will confirm larger up trend resumption. On the downside, however, below 161.93 minor support will turn intraday bias neutral and bring consolidations, before staging another rally.

In the bigger picture, price actions from 164.29 medium term top are seen as a correction to rise from 139.05 only. As long as 148.38 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) is expected to resume through 164.29 at a later stage. Next target would be 169.96 (2008 high).

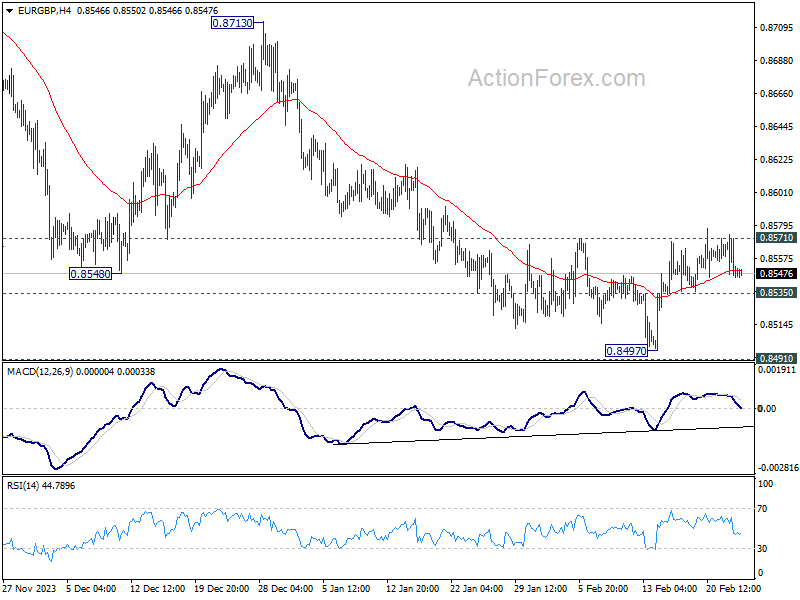

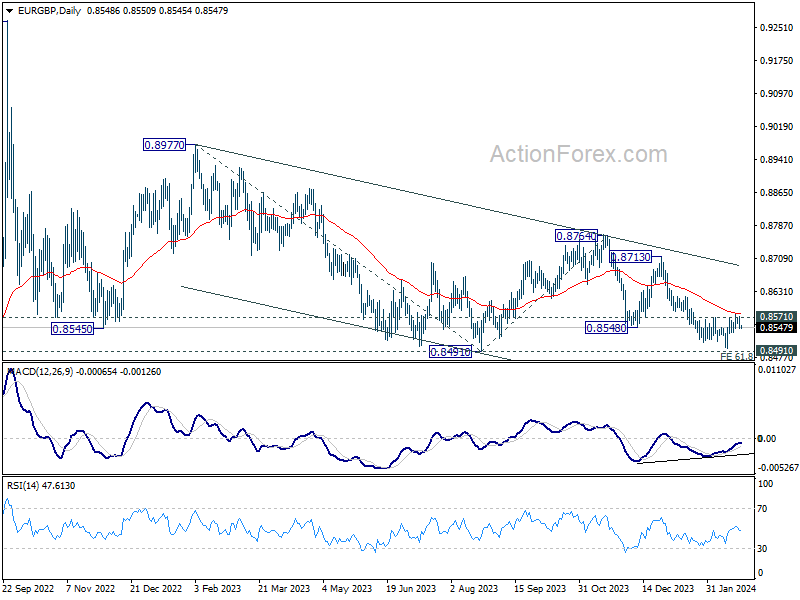

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8538; (P) 0.8556; (R1) 0.8567; More...

Intraday bias in EUR/GBP remains neutral at this point and outlook is unchanged. On the downside, break of 0.8535 minor support will bring retest of 0.8491/7 support zone. Firm break there will resume larger decline. However, considering bullish convergence condition in 4H MACD, sustained break of 0.8571 will confirm short term bottoming, and turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8713 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

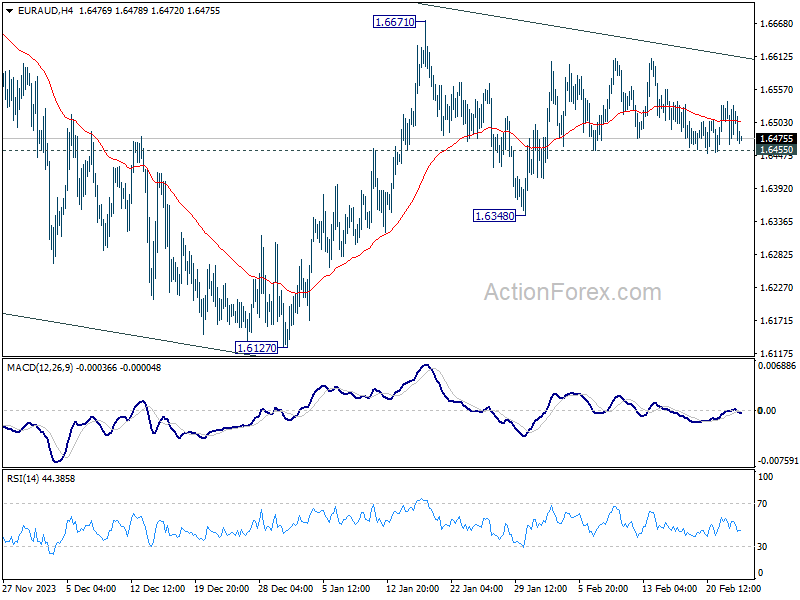

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6470; (P) 1.6504; (R1) 1.6541; More...

Intraday bias in EUR/AUD remains neutral at this point. On the upside, decisive break of 1.6671 will revive the case that whole correction from 1.7062 has completed with three waves down to 1.6127. Further rally should then be seen to 1.6844 resistance for confirmation. Nevertheless, below 1.6455 minor support will turn bias to the downside for 1.6348 and possibly below.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

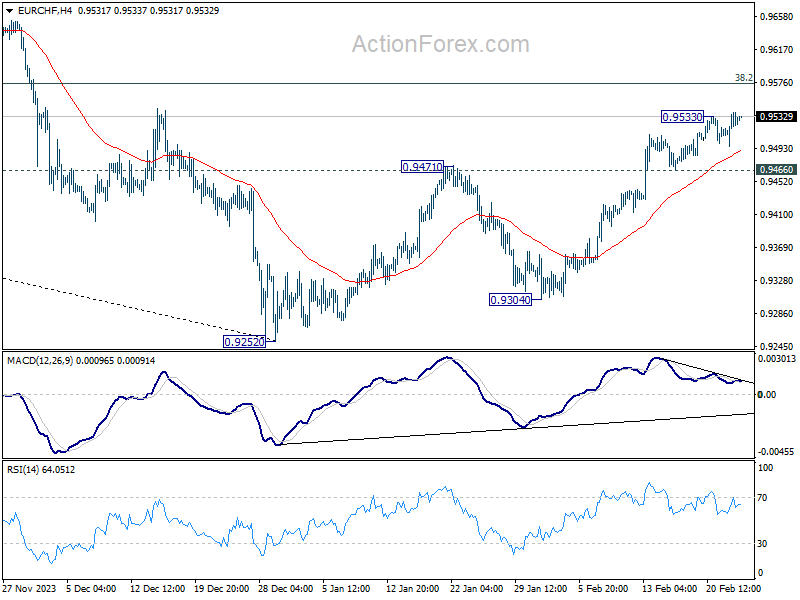

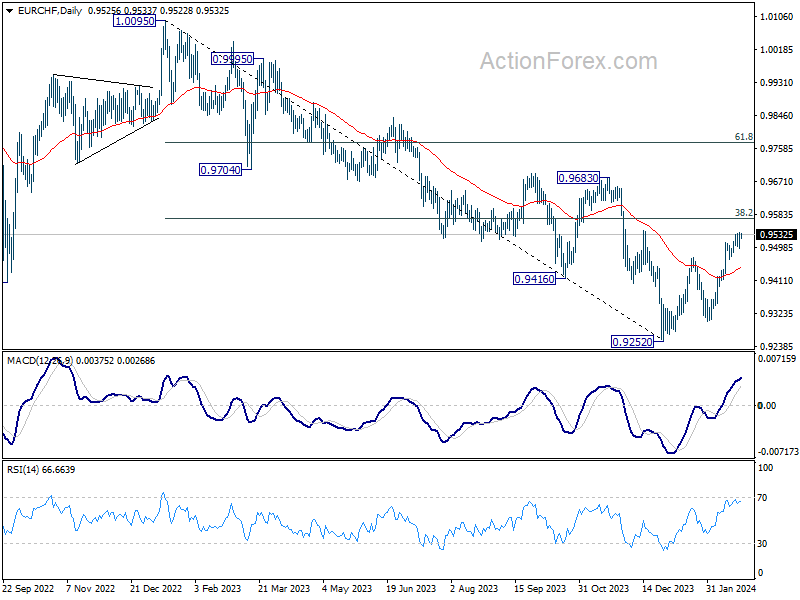

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9503; (P) 0.9521; (R1) 0.9546; More...

Intraday bias in EUR/CHF is back on the upside with breach of 0.9533 temporary top. Further rally would be seen to 0.9574 fibonacci level. Considering bearish divergence condition in 4H MACD, strong resistance could be seen there to limit upside. On the downside, break of 0.9466 support will indicate short term topping, and turn bias back to the downside.

In the bigger picture, price actions from 0.9252 are tentatively seen as a correction to the five-wave down trend from 1.0095 (2023 high). Further rise would be seen to 38.2% retracement of 1.0095 to 0.9252 at 0.9574 and possibly above. But overall medium term outlook will remain bearish as long as 0.9683 resistance holds.

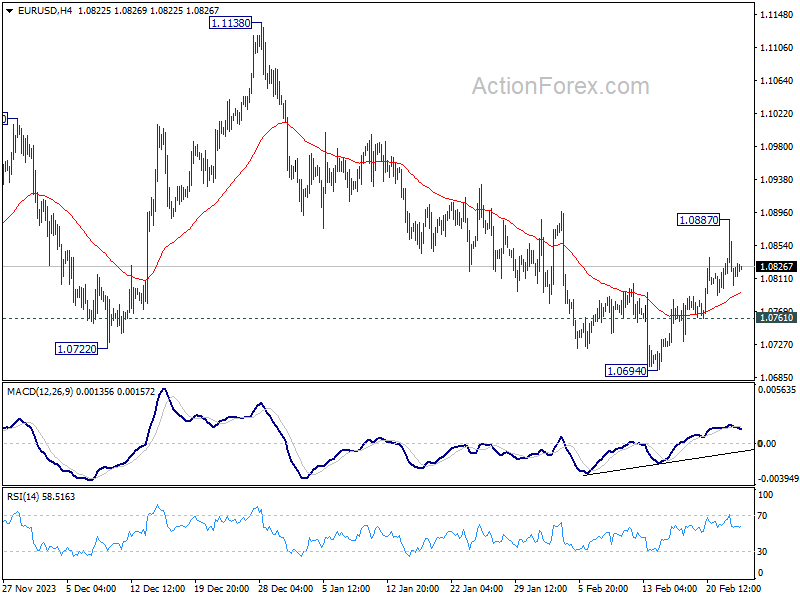

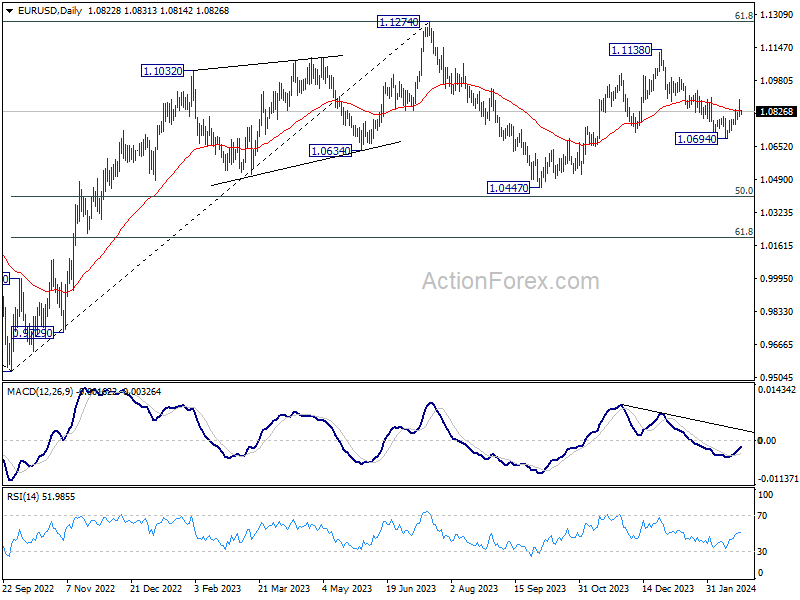

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0788; (P) 1.0838; (R1) 1.0872; More...

Intraday bias in EUR/USD remains neutral for the moment. On the upside, break of 1.0887 will affirm the case that fall from 1.1138 has completed, and target this resistance. However, break of 1.0761 will turn bias back to the downside for retesting 1.0694 support.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

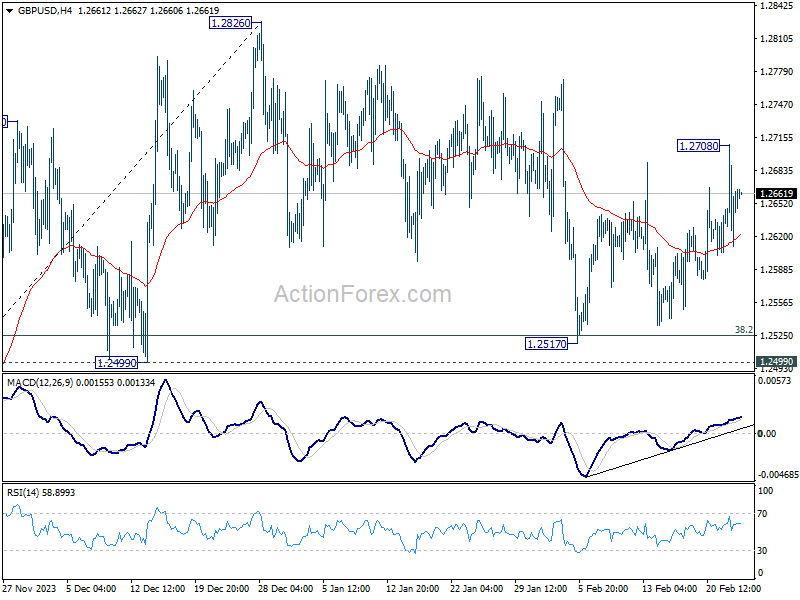

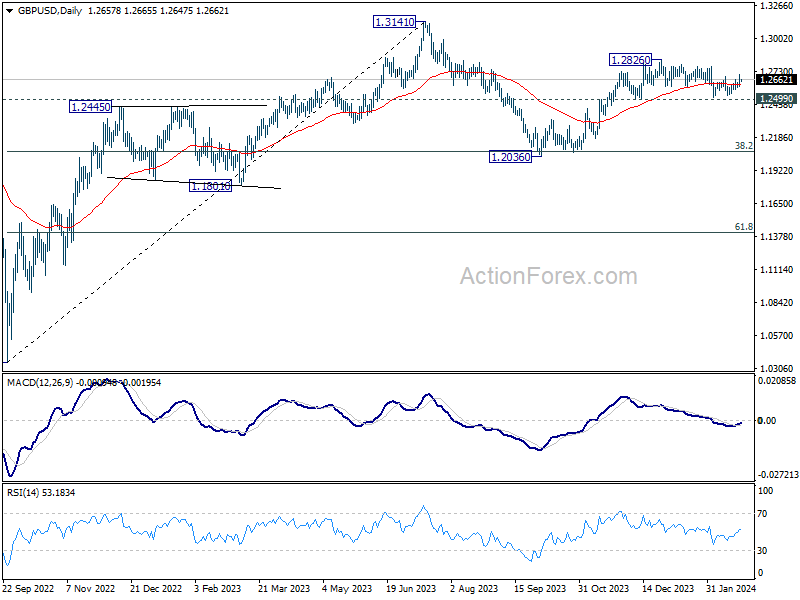

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2612; (P) 1.2661; (R1) 1.2710; More...

Intraday bias in GBP/USD remains neutral for the moment. On the upside, break of 1.2708 resistance will indicate that correction from 1.2826 has completed. Intraday bias will be back on the upside for retesting 1.2826. Nevertheless, decisive break of 1.2499 will argue that whole rise from 1.2036 has completed and turn near term outlook bearish.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which could be still in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

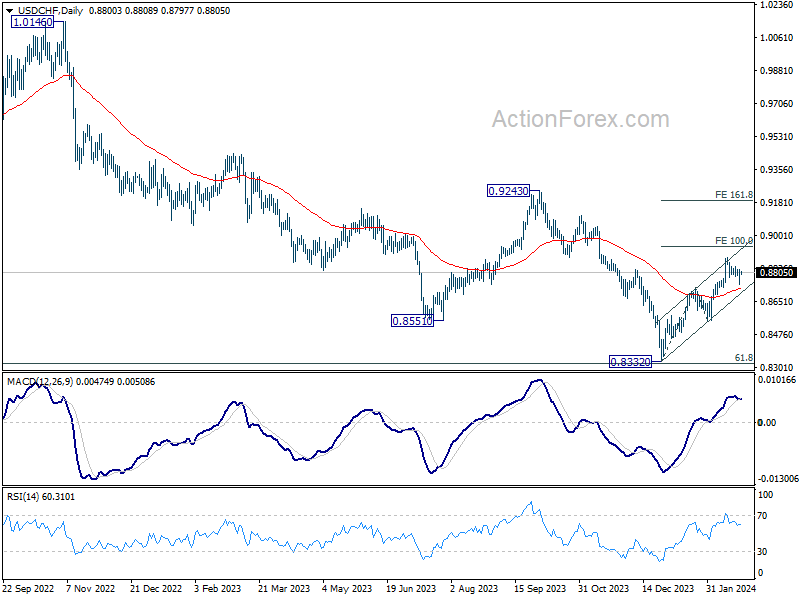

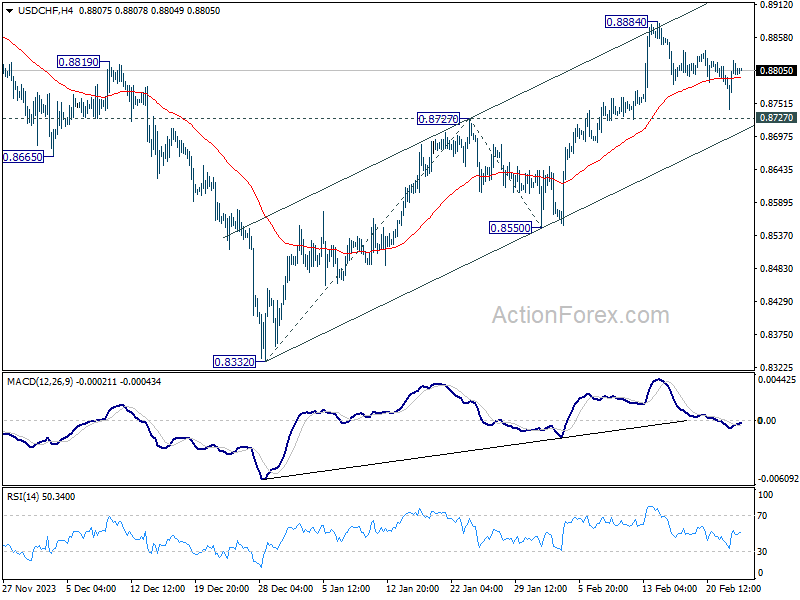

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8756; (P) 0.8789; (R1) 0.8835; More....

USD/CHF is still extending the consolidation from 0.8884 and intraday bias remains neutral. With 0.8727 resistance turned support intact, further rally is expected. On the upside, break of 0.8885 will resume the rise from 0.8332 and target and 100% projection of 0.8332 to 0.8727 from 0.8550 at 0.8954. However, sustained break of 0.8727 will dampen this bullish view, and turn bias back to the downside for 0.8550 support instead.

In the bigger picture, a medium term bottom should be formed at 0.8332, on bullish convergence condition in W MACD, just ahead of 0.8317 long term fibonacci support. It's still early to decide if the larger down trend from 1.0146 (2022 high) is reversing. But further rise should be seen to 0.9243 resistance even as a correction.