Sample Category Title

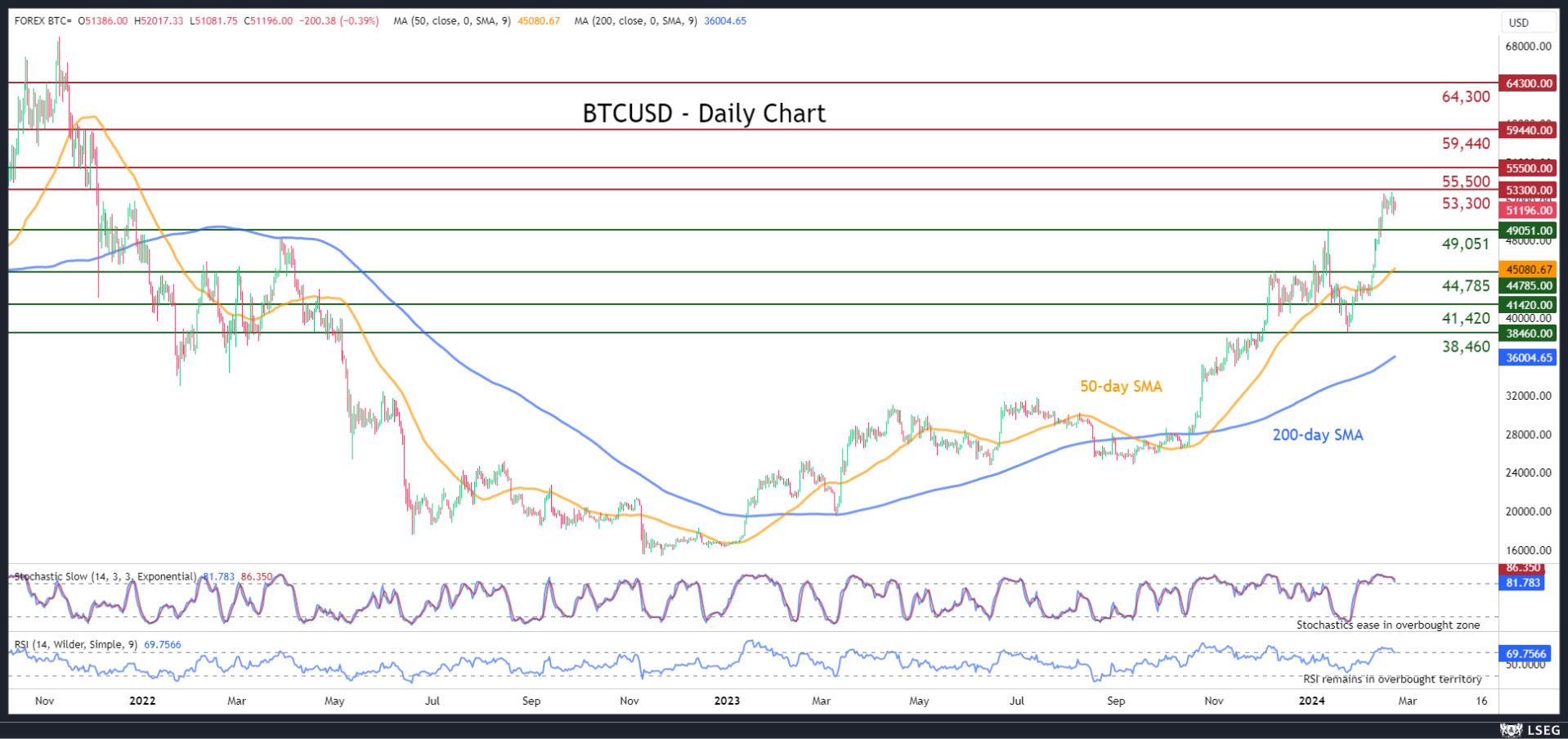

BTCUSD Consolidates Near More than 2-year High

- BTCUSD moves sideways after steep advance pauses

- Holds comfortably above 50,000 psychological mark

- Momentum indicators look overbought

BTCUSD (Bitcoin) had been in a steep advance following its break above the 50-day simple moving average (SMA) on February 7. However, the rally seems to have paused for now, with the price consolidating a tad below its more than two-year peak of 52,989.

If Bitcoin storms to fresh highs, the November 2021 support zones of 53,300 and 55,500 could now provide initial resistance. Conquering the latter, the bulls might attack 59,440, which served as both support and resistance in the November-December 2021 period. Even higher, the December 2021 resistance of 64,300 might curb further upside attempts.

On the flipside, should the tight range break to the downside, the previous peaks of 49,051 and 44,785 could act as the first lines of defence. A violation of the latter could open the door for the inside swing low of 41,420. Failing to halt there, the price may slide towards the 2024 bottom of 38,460.

In brief, BTCUSD appears to be in a consolidation phase, waiting for developments that could provide fresh directional impetus. That being said, the momentum indicators remain in their overbought zones, increasing the odds for an impending pullback.

Sunset Market Commentary

Markets

The February European headline PMI came in slightly stronger than expected, rising from 47.9 to 48.9. A deepening contraction in Germany (46.1) and sustained output fall in France (47.7) were countered by faster growth in the rest of the region. There’s a split on a sector level as well. Manufacturing unexpectedly ventured deeper in contraction territory (46.1) with Germany (42.3) in particular clipping the wings of a fragile bottoming out process. New (export) orders fell sharply, weighing on output, employment and input buying & inventories. Expectations for the year ahead remain sub-par. Services activity on the other hand stopped contracting after six months (50). Growing employment compensated a (smaller than in January) decline of new orders. The future hasn’t looked as bright in 11 months. Talking prices, manufacturing disinflation contrasts with the sharpest services output inflation since 2000 if one takes out the exceptionally strong post-Covid price dynamics. Labour market tightness and rising wages are to blame. Markets looked through the manufacturing malaise and focused on the light at the end of the services tunnel. Euro area money markets pared ECB cutting bets to less than 100 bps for this year. The German yield curve turns more inverse with changes of +2.5 bps at the front and -3.3 bps further out. ECB minutes added some substance. Judging the disinflationary process as fragile and noting only limited indications for wages to have turned a corner, policymakers agreed that it was too soon to discuss rate cuts. The risk of lowering rates too early was still seen as outweighing that of cutting too late. While the March inflation forecasts would probably be revised downwards on lower energy prices, stubborn core inflation warranted a cautious approach. US yields joined the European example for once. Lower-than-expected jobless claims (yes, again) triggered additional gains. Net daily changes vary between flat (30-y) to +2.6 bps (2-y). UK gilts outperform global peers, losing up to 2.6 bps. This is even as the services (54.3) and composite PMI (53.3) surprised to the upside to settle more comfortably above the neutral level. However, the questionnaire revealed that much of the services upturn is driven “by resurgent demand for financial services, in turn predicated on hopes of an imminent pivot to rate cutting by the Bank of England.” The latter is not at all guaranteed given the higher inflation rate - guestimated at 4% - in the sector. Manufacturing, just as in Europe, keeps struggling (47.1). The euro on the currency market sprinted towards but never really attacked the EUR/USD 1.09 big figure following the PMIs. A stronger dollar in the wake of the jobless claims wiped out almost all of the remaining EUR/USD gains (flat). The Japanese yen is nearing recent lows against the dollar again. Sterling loses out against most major peers, including the euro. EUR/GBP is testing the February top around 0.857.

News & Views

The Central Bank of the Republic of Turkey (CBRT) today kept its policy rate unchanged after rising from 8.5% in May last year to 45% in January. It was the first meeting under the new governor Fatih Karahan. The statement takes notice that due to month specific and time-dependent price and wage adjustments, the underlying trend of monthly inflation rose in January. Headline inflation in January was 6.70% M/M and 64.86% Y/Y. Core inflation printed at 70.48 % Y/Y. The CBRT sees a moderation in domestic demand, but acknowledges that stickiness in services inflation, geopolitical risks and food prices keep inflation pressures alive. The Committee signals that current level of the policy rate will be maintained (or raised if needed) until there is a significant and sustained decline in the monthly trend of inflation and until inflation expectations converge to the projected range. The CBRT also sees a real appreciation of the lira contributing to the disinflation process. The CBRT aims at inflation of 5%. In its latest projection, the bank forecasted CPI at 36.4% end this year. At EUR/TRY 33.72 the lira still trades weaker in a daily perspective, but regained some losses from early this morning.

The ECB reported a 2023 loss of €1.266 mln (break-even in 2022). The de facto loss was even bigger as the ECB used an amount of €6.620 mln of provisions for financial risk. Having raised the policy rates, interest expenses on ECB liabilities carrying a variable rate also increased while interest income on its assets did not to the same extent. The ECB said it is likely to incur losses over the next few years. The loss has no impact on its ability to conduct effective monetary policy but did result in the ECB not distributing any profits to the euro area central banks for 2023.

Canada: Retail Trade Rebounds in December, November Reading Revised Higher

Retail sales grew by 0.9% month-on-month (m/m) in December, coming in stronger than Statistics Canada's advance estimate of 0.8% m/m. In addition, November's print was revised up to a flat reading from -0.2% m/m reported earlier, making today's growth even stronger.

Adjusted for inflation, the volume of retail sales were up 0.8% in December from an upwardly revised flat reading in November (-0.2% m/m reported in the advanced estimate).

Sales at motor vehicle and parts dealers continued climb higher, registering a 1.9% m/m gain in December – the fourth consecutive month of gains.

Receipts at gasoline stations and fuel vendors were up 0.9% m/m, after a loss of 0.2% m/m in November.

Excluding sales at car dealerships and gas stations, core retail sales were up 0.5% m/m, following a upwardly revised decline of 0.4% m/m in November.

Contributors to today's gains were general merchandise stores (+2.8% m/m), food and beverage stores (+1.5% m/m), and miscellaneous store retailers (+2.1% m/m).

Receipts fell for the rest of the categories, with furniture and home furnishings stores being the biggest drag with a reading of -5.1% m/m, following an upwardly revised gain of 3.8% m/m in November.

E-commerce sales continued to report a negative reading for the second month in a row, falling 3.6% m/m after an upwardly revised loss of 1.4% m/m in November (from -1.5 m/m, reported earlier).

Statistics Canada's advance reading suggests that retail sales were down by 0.4% m/m in January (with 52.7% of companies surveyed providing responses).

Key Implications

Today's report falls in line with our expectations for a rebound in spending in Q4, which in real terms is now tracking at a 2.3% pace (annualized). Zooming in on the details, the largest driver of this holiday season's gain were auto sales, supported by pent-up demand and the recovery in auto production. Importantly, housing-related purchases remain weak, despite the recent uptick in the housing market.

Despite a rebound, 2023 has been marked as the slowest year for holiday sales since the pandemic began. Looking ahead, we anticipate rather tepid growth in consumer spending during the first half of the year. Consumers, facing higher costs, are becoming increasingly selective in their spending habits, which by itself might have prompted the Bank of Canada to adopt a more accommodative policy earlier. However, without a clear signal from the Bank of Canada that it is willing to disregard shelter inflation, a more restrictive approach is more likely. This makes a rate cut more probable in the second quarter of 2024.

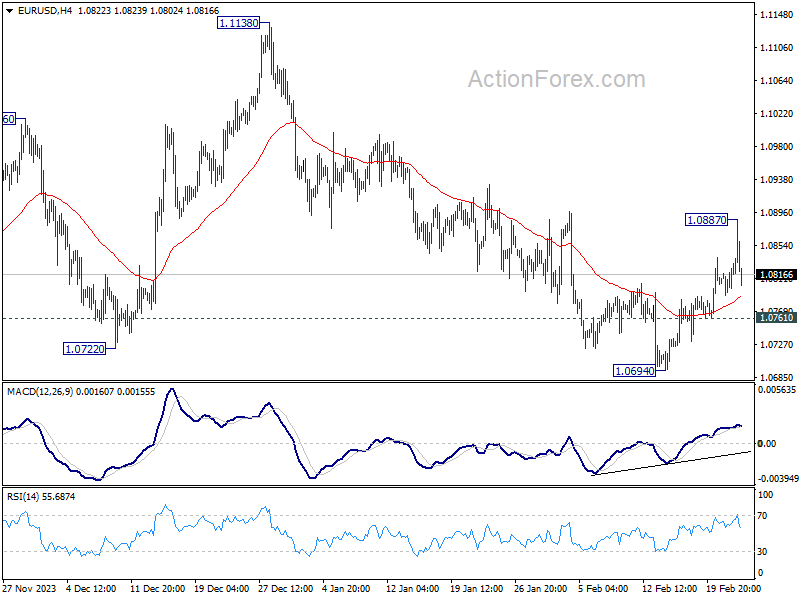

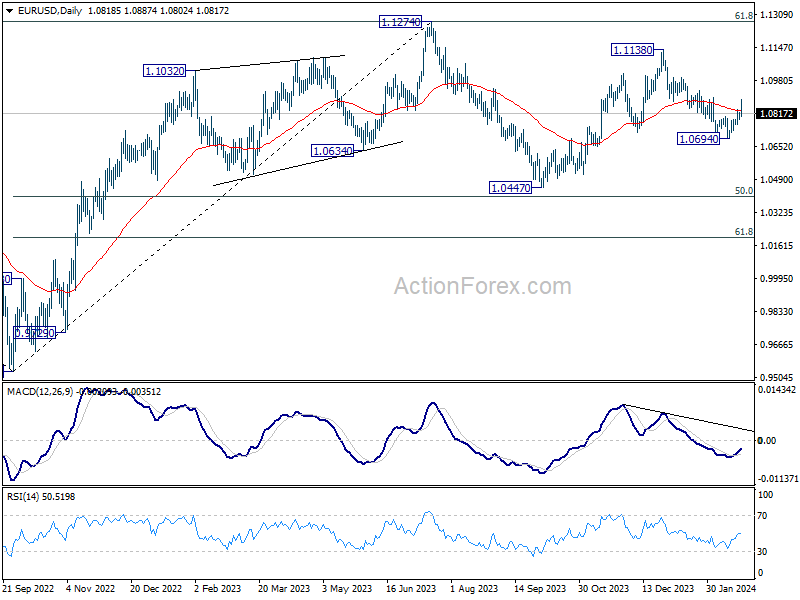

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0799; (P) 1.0811; (R1) 1.0833; More...

EUR/USD retreated after brief rise to 1.0887 and intraday bias is turned neutral first. On the upside, break of 1.0887 will affirm the case that fall from 1.1138 has completed, and target this resistance. However, break of 1.0761 will turn bias back to the downside for retesting 1.0694 support.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

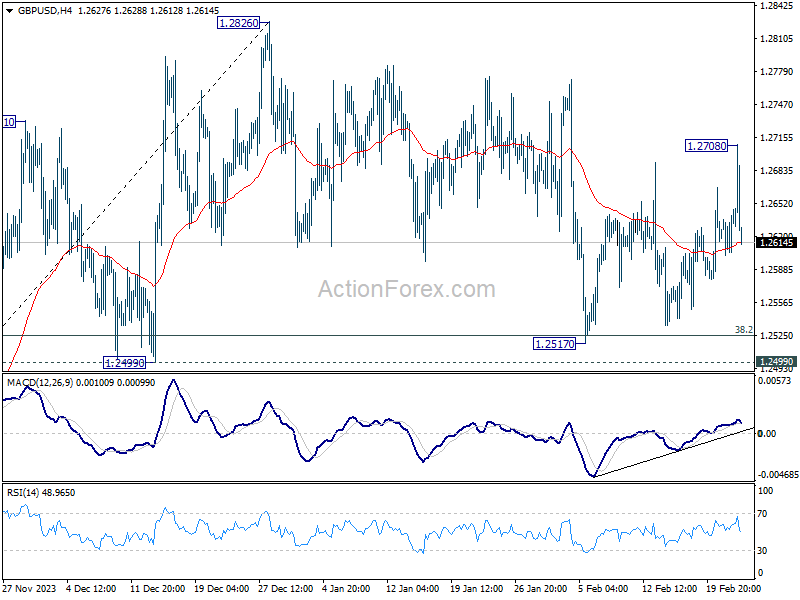

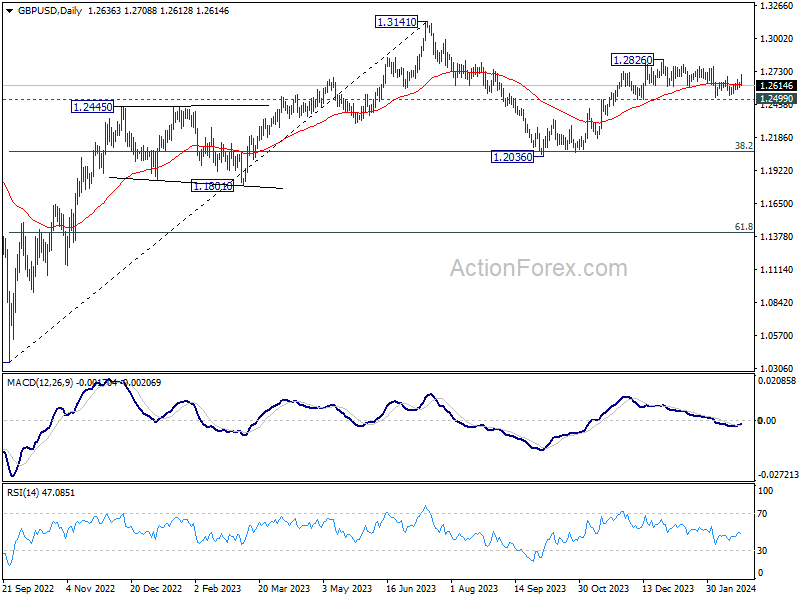

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2613; (P) 1.2628; (R1) 1.2652; More...

Despite spiking higher to 1.2708, GBP/USD quickly retreated. Intraday bias remains neutral first. On the upside, break of 1.2708 resistance will indicate that correction from 1.2826 has completed. Intraday bias will be back on the upside for retesting 1.2826. Nevertheless, decisive break of 1.2499 will argue that whole rise from 1.2036 has completed and turn near term outlook bearish.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which could be still in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

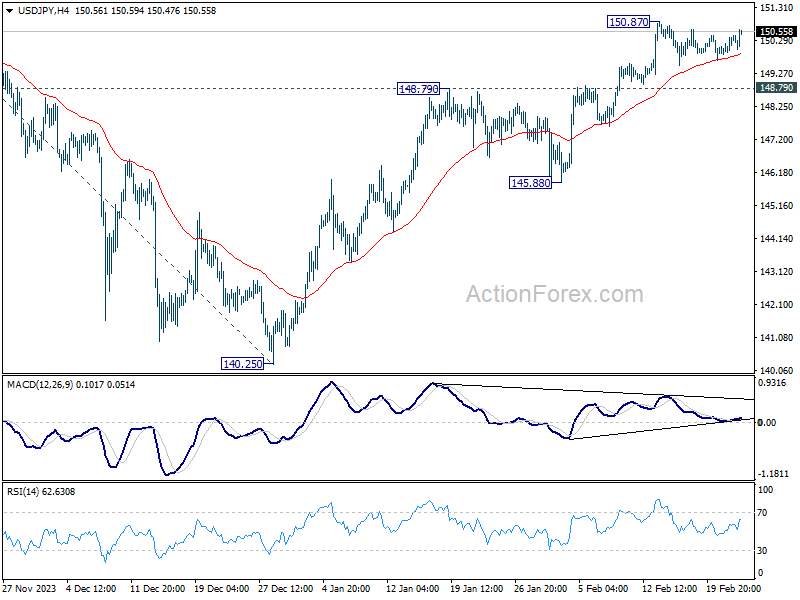

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.96; (P) 150.18; (R1) 150.50; More...

USD/JPY is still bounded in consolidation from 150.87 and intraday bias remains neutral. Another retreat cannot be ruled out, but downside should be contained by 148.79 resistance turned support to bring rise resumption. Above 150.87 will resume the rally from 140.25 to 151.89/93 key resistance zone. Decisive break there will confirm larger up trend resumption of 155.50 projection level next. However, firm break of 148.79 will turn bias to the downside for 145.88 support.

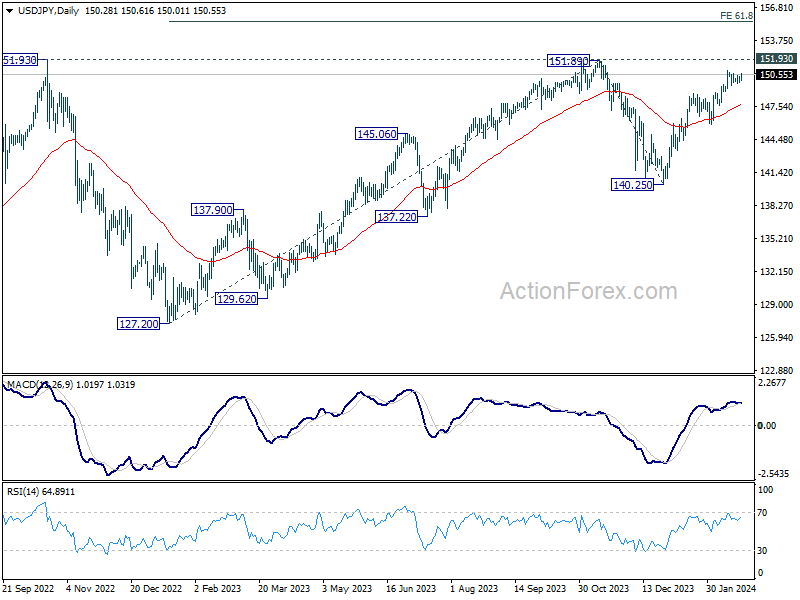

In the bigger picture, fall from 151.89 is seen as a correction to the rally from 127.20, which might have completed at 140.25 already. Firm break of 151.89/93 resistance zone will confirm up trend resumption, and next target will be 61.8% projection of 127.20 to 151.89 from 140.25 at 155.50. This will now remain the favored case as long as 140.25 support holds.

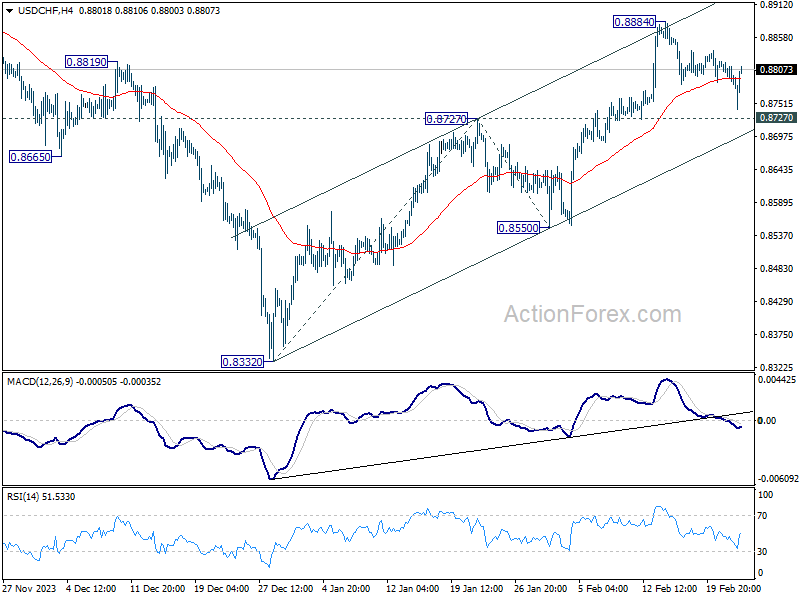

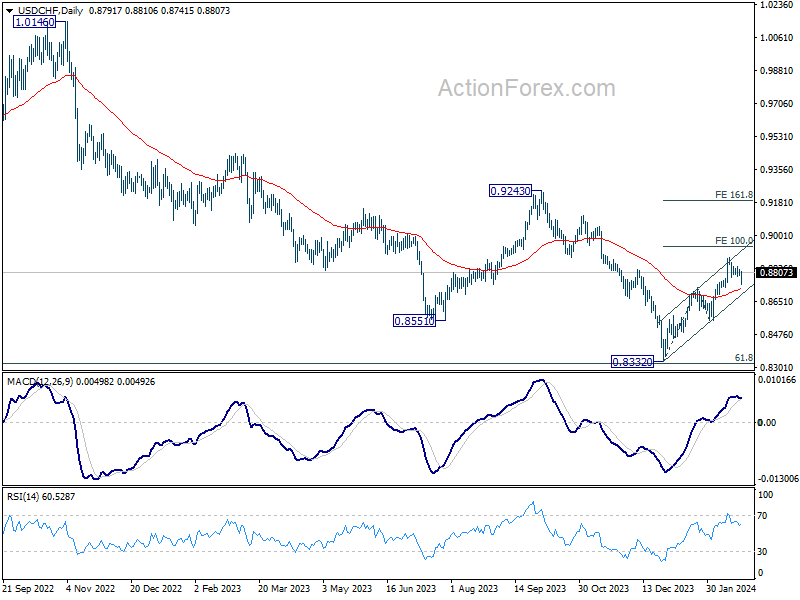

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8783; (P) 0.8802; (R1) 0.8816; More....

Despite earlier dip, USD/CHF recovered ahead of 0.8727 resistance turned support. Intraday bias remains neutral and further rally is still expected. On the upside, break of 0.8885 will resume the rise from 0.8332 and target and 100% projection of 0.8332 to 0.8727 from 0.8550 at 0.8954. However, sustained break of 0.8727 will dampen this bullish view, and turn bias back to the downside for 0.8550 support instead.

In the bigger picture, a medium term bottom should be formed at 0.8332, on bullish convergence condition in W MACD, just ahead of 0.8317 long term fibonacci support. It's still early to decide if the larger down trend from 1.0146 (2022 high) is reversing. But further rise should be seen to 0.9243 resistance even as a correction.

Yen Falters in Risk-On Environment, Dollar Seeks Comeback With Surging Yields

Global financial markets are currently basking in a robust wave of risk-on sentiment, evidenced by Japan's Nikkei and Europe's Stoxx 600 indices reaching new record highs. The optimism is further bolstered by promising US futures, with the technology sector leading the charge, significantly propelled by Nvidia's impressive results. This surge in tech enthusiasm is largely fueled by the ongoing artificial intelligence boom, which seems poised to captivate market sentiment for the foreseeable future.

In the currency markets, Japanese Yen emerges as the most significant underperformer, embodying the broad risk-on sentiment that typically sees investors moving away from safe-haven assets. Swiss Franc also finds itself on the weaker side, echoing a similar sentiment. However, development in other currencies are less clear.

While Dollar experienced some pressure earlier in the day, it's is attempting a rebound in early US session, buoyed by rally in Treasury yields. Euro found support from improvement in PMI data, particularly with France showing robust performance that helped counterbalance weak Germany's. Accounts from the European Central Bank (ECB) meeting revealed policymakers' apprehensions regarding premature policy easing. However, this has not translated into sustained momentum for the common currency.

As it stands, New Zealand and Australian Dollar lead as the frontrunners in the currency markets, benefiting from the risk-on environment. Euro follows, while the Sterling lags behind alongside Swiss Franc. Yet, the dynamic nature of the markets suggests that these positions could shift by the end of US session.

In Europe, at the time of writing, FTSE is up 0.25%. DAX is up 1.55%. CAC is up 1.09%. UK 10-year yield is down -0.0060 at 4.105. Germany 10-year yield is down -0.002 at 2.446. Earlier in Asia, Nikkei rose 2.19%. Hong Kong HSI rose 1.45%. China Shanghai SSE rose 1.27%. Singapore Strait Times rose 0.18%. Japan 10-year JGB yield fell -0.0045 to 0.721.

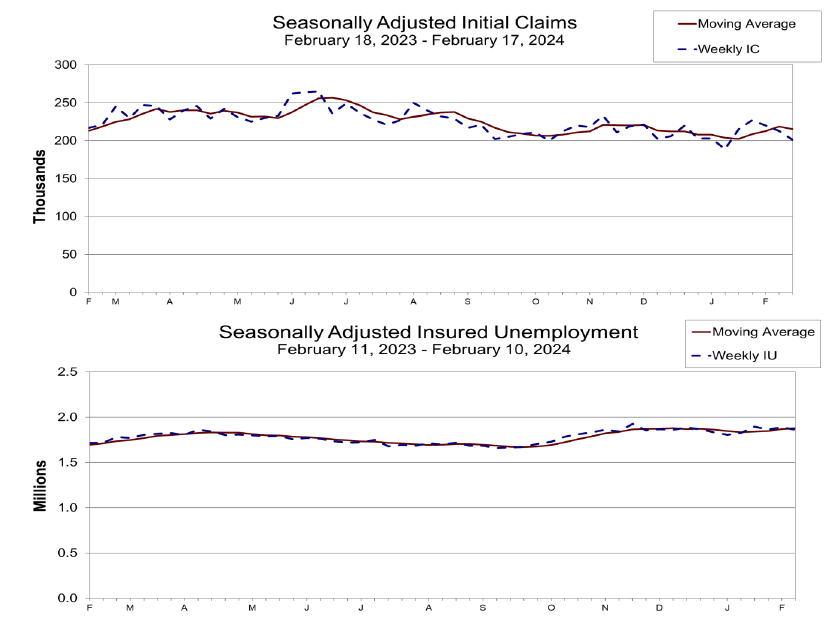

US initial jobless claims falls to 201k

US initial jobless claims fell -12k to 201k in the week ending February 17, below expectation of 217k. Four-week moving average of initial claims fell -3.5k to 215k.

Continuing claims fell -27k to 1862k in the week ending February 10. Four-week moving average of continuing claims rose 8.5k to 1878k, highest since December 11, 2021.

Canada's retail sales rises 0.9% mom in Dec, slightly above expectation

Canada's retail sales rose 0.9% mom to CAD 67.3B in December, slightly above expectation of 0.8% mom. Sales were up in five of nine subsectors and were led by increases at motor vehicle and parts dealers (+1.9%). In volume terms, retail sales increased 0.8% in December.

Retail sales were up 1.0% in Q4, marking a second consecutive quarterly increase. In volume terms, retail sales increased 1.3% in the quarter.

Advance estimate suggests that sales decreased -0.4% mom in January.

ECB minutes reveal consensus on prematurity of rate cut discussions

Accounts of ECB's January 24-25 meeting showed that reveal a cautious stance among its members towards the idea of interest rate cuts. Officials reached a "broad consensus" on the notion that discussing rate cuts at this juncture was "premature" with many members emphasizing "risk management considerations" as a foundation for this perspective. The "risk of cutting policy rates too early was still seen as outweighing that of cutting rates too late", the minuted noted.

Members also emphasized the "high reputational costs" that could arise from having to reverse policy direction should economic conditions improve unexpectedly, wage growth pick up pace, or if new inflationary pressures were to surface. Such a scenario, they argued, could undermine the credibility of ECB's policy framework and its commitment to price stability.

Furthermore, the discussion acknowledged that while financial markets have already begun to anticipate rate cuts in 2024, leading to a somewhat "loosening of both financial and financing conditions," this anticipation could be deemed "premature." There was a concern that acting on market expectations too soon could inadvertently "derail or delay" the efforts to steer inflation back to its target level in a timely manner.

Eurozone CPI finalized at 2.8% in Jan, core at 3.3%

Eurozone PMI was finalized at 2.8% yoy in January, down from December's 2.9% yoy. Core CPI was finalized at 3.3% yoy, down from prior month's 3.4% yoy. The highest contribution to came from services (+1.73 percentage points, pp), followed by food, alcohol & tobacco (+1.13 pp), non-energy industrial goods (+0.53 pp) and energy (-0.62 pp).

EU CPI was finalized at 3.1% yoy. The lowest annual rates were registered in Denmark, Italy (both 0.9%), Latvia, Lithuania and Finland (all 1.1%). The highest annual rates were recorded in Romania (7.3%), Estonia (5.0%) and Croatia (4.8%). Compared with December, annual inflation fell in fifteen Member States, remained stable in one and rose in eleven.

Eurozone PMI composite rises to 48.9, a step towards recovery amid German drag

Eurozone PMI Manufacturing dipped further from 46.6 to 46.1 in February, undershooting expectations of a 47.1 reading and signaling continued contraction. Conversely, PMI Services climbed from 48.4 to neutral mark of 50.0, surpassing the forecast of 48.7 and reaching a 7-month high. This uplift in services contributed to PMI Composite's rise from 47.9 to 48.9, marking an 8-month peak yet still indicating slight overall economic contraction.

Norman Liebke, Economist at Hamburg Commercial Bank, cited a "glimmer of hope" as Eurozone edges closer to recovery, particularly within the services sector. Despite the manufacturing downturn, Liebke reaffirms an annual growth forecast of 0.8% for 2024.

ECB is likely to find the latest PMI figures concerning, especially with output prices increasing for the fourth consecutive month, largely driven by labor-intensive services sector grappling with rising wages. ECB is anticipated to make its first interest rate cut in June according to Liebke's forecast.

The disparity in economic performance between Germany and France is striking. Germany, Europe's largest economy, appears to be a significant "drag" on the broader Eurozone growth, with its manufacturing sector facing pronounced challenges. In contrast, France is experiencing a more robust recovery across both services and manufacturing.

Germany's PMI readings for February further underscore its economic difficulties, with PMI Manufacturing plummeting to a 4-month low of 42.3, PMI Services rising from 48.2 and Composite PMI also hitting a 4-month low at 46.1.

On the other hand, France's economic indicators offer more positive news, with PMI Manufacturing surging to an 11-month high of 46.8, Services PMI rising to an 8-month high at 48.0, and PMI Composite reaching a 9-month high at 47.7.

UK PMI composite rises to 53.3, growth accelerates as inflation concerns loom

UK's PMI Manufacturing edged up from 47.0 to 47.1, aligning with expectations, while PMI Services was steady at 54.3, just shy of the anticipated 54.4. PMI Composite index rose from 52.9 to 53.3, underscoring a period of accelerated economic growth and marking the highest reading in nine months.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, emphasized the significance, noting that recent uptick is part of a consistent pattern of improvement over the "four straight months". Williamson's analysis suggests that the economy is expanding at a quarterly rate of 0.2-0.3% in Q1 2024, signaling that UK's recessionary phase may have concluded.

Williamson highlighted supply chain disruptions, particularly those related to Red Sea shipping, have led to the most significant delays observed in over 18 months. These disruptions have escalated shipping costs, contributing to a notable increase in selling prices for goods—the largest monthly rise seen in nine months.

Moreover, service sector inflation has edged higher due to increased wage costs and the indirect effects of rising goods prices. The survey data suggest consumer price inflation may hover around 4% in the coming months, doubling BoE's target rate.

Given these dynamics—accelerating growth coupled with rising prices—February's PMI data suggests that BoE are "increasingly likely to err on the side of caution" towards reducing interest rates.

Japan's PMI composite drops to 50.3, from recovery to stagnation

Japan's PMI Manufacturing dipped further to 47.2 from 48.0, marking the ninth consecutive month of sector contraction and hitting the lowest point since August 2020. PMI Services also declined, albeit more moderate, falling from 53.1 to 52.5. Consequently, Composite PMI, which combines both manufacturing and service sectors, decreased from 51.5 to a near-stagnation point of 50.3.

Usamah Bhatti, Economist at S&P Global Market Intelligence, commented on the recent data, noting that the slight improvement observed at the beginning of the year has "all but evaporate[d]" in February. He described the month's growth as "only fractional," attributing it to "softer upturn in services activity" that was insufficient to counterbalance the "steepest contraction in manufacturing output for a year."

Australia's Composite PMI climbs to 51.8, diminishing prospects for near-term RBA rate cut

Australia's PMI Manufacturing fell sharply from 50.1 to 47.7 in February, with Manufacturing Output marking a 45-month low at 45.0. In stark contrast, PMI Services surged to a 10-month high of 52.8, propelling the Composite PMI to 51.8, the first time it has breached the 50-mark threshold since last June.

Warren Hogan, Chief Economic Advisor at Judo Bank, said the PMI results "weaken the case for monetary policy easing any time soon". Improvement in activity indicators and modest rise in price indexes suggest that "risks to monetary policy remain even balanced".

Hogan's analysis also points to an economy that is gaining momentum, expanding at more vigorous pace in 2024 compared to the latter half of 2023. He posits that continuous improvements could herald stronger economic growth this year than the last, hinting that "soft landing is behind us".

Furthermore, Composite Employment Index reached its highest level since last September, indicating "rising labour demand and employment growth" in the overall economy. This is accompanied by intensifying price pressures, with Composite Output Price Index's climb to its highest point since last September 2023, indicating that domestic inflation could be hovering between 4% and 5%. Hogan cautions that the recent trend of disinflation "may well have run its course."

New Zealand's trade deficit widens, exports falls -7.1% yoy and imports down -20% yoy

New Zealand's trade activity in January showed notable downturn, with goods exports dropping by -7.1% yoy to NZD 4.9B and goods imports declining by a substantial -20.0% yoy to NZD 5.9B. This resulted in trade deficit of NZD -976m, significantly larger than the anticipated NZD -200m.

A closer examination of the data reveals Australia as the leading contributor to the monthly fall in New Zealand's exports, with a -17% decrease amounting to NZD -112m. Not far behind, Japan saw a dramatic -34% reduction in its exports from New Zealand, translating to NZD -105m. Conversely, EU was a rare bright spot, where New Zealand's exports actually increased by 5.8%, or NZD 15m. Other major trading partners like China and the USA also experienced declines in exports from New Zealand, by -2.8% (NZD -42m) and -5.6% (NZD -31m), respectively.

On the import side, EU recorded the most significant monthly drop, with imports falling by -33% to NZD -386m. South Korea followed closely with a -34% decrease, equating to NZD -286m. Other notable decreases in imports came from China (NZD -84m, -5.4%), Australia (NZD -57m, -9.2%), and the USA (NZD -30m, -5.6%).

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8783; (P) 0.8802; (R1) 0.8816; More....

Despite earlier dip, USD/CHF recovered ahead of 0.8727 resistance turned support. Intraday bias remains neutral and further rally is still expected. On the upside, break of 0.8885 will resume the rise from 0.8332 and target and 100% projection of 0.8332 to 0.8727 from 0.8550 at 0.8954. However, sustained break of 0.8727 will dampen this bullish view, and turn bias back to the downside for 0.8550 support instead.

In the bigger picture, a medium term bottom should be formed at 0.8332, on bullish convergence condition in W MACD, just ahead of 0.8317 long term fibonacci support. It's still early to decide if the larger down trend from 1.0146 (2022 high) is reversing. But further rise should be seen to 0.9243 resistance even as a correction.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Trade Balance (NZD) Jan | -976M | -200M | -323M | -368M |

| 22:00 | AUD | Manufacturing PMI Feb P | 47.7 | 50.1 | ||

| 22:00 | AUD | Services PMI Feb P | 52.8 | 49.1 | ||

| 00:30 | JPY | Manufacturing PMI Feb P | 47.2 | 48.2 | 48 | |

| 00:30 | JPY | Services PMI Feb P | 52.5 | 53.1 | ||

| 08:15 | EUR | France Manufacturing PMI Feb P | 46.8 | 44 | 43.1 | |

| 08:15 | EUR | France Services PMI Feb P | 48 | 45.6 | 45.4 | |

| 08:30 | EUR | Germany Manufacturing PMI Feb P | 42.3 | 46.1 | 45.5 | |

| 08:30 | EUR | Germany Services PMI Feb P | 48.2 | 48 | 47.7 | |

| 09:00 | EUR | Eurozone Manufacturing PMI Feb P | 46.1 | 47.1 | 46.6 | |

| 09:00 | EUR | Eurozone Services PMI Feb P | 50 | 48.7 | 48.4 | |

| 09:30 | GBP | Manufacturing PMI Feb P | 47.1 | 47.1 | 47 | |

| 09:30 | GBP | Services PMI Feb P | 54.3 | 54.4 | 54.3 | |

| 10:00 | EUR | Eurozone CPI Y/Y Jan F | 2.80% | 2.80% | 2.80% | |

| 10:00 | EUR | Eurozone CPI Core Y/Y Jan F | 3.30% | 3.30% | 3.30% | |

| 12:30 | EUR | ECB Meeting Accounts | ||||

| 13:30 | CAD | Retail Sales M/M Dec | 0.90% | 0.80% | -0.20% | |

| 13:30 | CAD | Retail Sales ex Autos M/M Dec | 0.60% | 0.70% | -0.50% | |

| 13:30 | USD | Initial Jobless Claims (Feb 16) | 201K | 217K | 212K | 213K |

| 14:45 | USD | Manufacturing PMI Feb P | 50.2 | 50.7 | ||

| 14:45 | USD | Services PMI Feb P | 52 | 52.5 | ||

| 15:00 | USD | Existing Home Sales Jan | 3.95M | 3.78M | ||

| 15:30 | USD | Natural Gas Storage | -59B | -49B | ||

| 16:00 | USD | Crude Oil Inventories | 3.9M | 12.0M |

US initial jobless claims falls to 201k

US initial jobless claims fell -12k to 201k in the week ending February 17, below expectation of 217k. Four-week moving average of initial claims fell -3.5k to 215k.

Continuing claims fell -27k to 1862k in the week ending February 10. Four-week moving average of continuing claims rose 8.5k to 1878k, highest since December 11, 2021.

Canada’s retail sales rises 0.9% mom in Dec, slightly above expectation

Canada's retail sales rose 0.9% mom to CAD 67.3B in December, slightly above expectation of 0.8% mom. Sales were up in five of nine subsectors and were led by increases at motor vehicle and parts dealers (+1.9%). In volume terms, retail sales increased 0.8% in December.

Retail sales were up 1.0% in Q4, marking a second consecutive quarterly increase. In volume terms, retail sales increased 1.3% in the quarter.

Advance estimate suggests that sales decreased -0.4% mom in January