Sample Category Title

Fed’s Harker warns against immediate expectations for rate cuts

Philadelphia Fed President Patrick Harker did not dismiss the possibility of a rate cut as early as May meeting. But he emphasized the importance of observing "a couple more months" of economic data before making such a decision. "I think we're close," Harker stated overnight, advocating for patience by suggesting, "just give us a couple meetings."

"We may be in the position to see the rate decrease this year," he remarked. But he also tempered expectations with a reminder of the need for deliberate consideration: "But I would caution anyone from looking for it right now and right away. We have time to get this right, as we must."

Harker acknowledged the challenges inherent in the disinflation process, describing it as "bumpy and uneven at times." This acknowledgment underscores the necessity for the Fed to demand "more evidence" before altering its policy course, aiming to discern genuine economic trends from the "vagaries of monthly data."

In contemplating the initiation of policy easing, Harker advocated for a cautious approach: "let's start on a steady, slow reduction, because that to me minimizes risk."

Why September?

Absent a new inflationary shock, central banks’ next moves are likely to be down. We expect the first cut in Australia to occur after the late-September meeting. Here we explain our reasoning behind this timing.

When central banks are in data-dependent mode, financial market pricing will be data-sensitive. Turning points are always like this. The broad narrative will remain the same, but views of timing can shift suddenly. Small data surprises can matter a lot in these circumstances, even if they are mostly noise. We saw an example of this with the noise-affected January Labour Force Survey.

Absent a new inflationary shock, we can be reasonably sure that the next move is down for most central banks across advanced economies. But the question of exactly when is harder to pin down.

For Australia, we have pencilled in the first cut occurring at the late-September Board meeting, followed by another in November. Our thinking on the timing is as follows.

First, this expectation is predicated on the basis that things turn out broadly as we (and the RBA) expect. Inflation continues to decline, while growth remains soft in the first half of the year but does not fall away completely. Unemployment drifts up but does not rise precipitously.

Second, we take as given that the current stance of monetary policy is restrictive. This aligns with the RBA’s view and is supported by various indicators including credit growth and the drag from interest payments on household income. If the RBA maintained restrictive policy on an ongoing basis, growth would slow so much that inflation would undershoot the RBA target and keep falling. The decision to reduce the restrictive stance of policy – and eventually normalise to a more neutral stance – is therefore a question of when, not if.

Third, monetary policy operates with a lag, and the RBA knows this. They will not wait until inflation is already in the target range. They will start moving ahead of this point; Governor Bullock has acknowledged this in Parliamentary testimony. But as the Governor has also pointed out, they will want to wait until they are confident that inflation is declining on the desired trajectory. They want to be sure that inflation will be sustainably back inside the 2–3% target range by end-2025 and around the midpoint of the range by mid-2026.

We have landed on September as our preferred date for the first cut because some key data is released in the lead-up to that meeting. Employment and CPI inflation for the first half of 2024 will be available ahead of the August meeting, but not the crucial wages and national accounts data. These come ahead of the late-September meeting. We expect that these latter releases will show enough of a decline in input cost inflation, a turnaround in productivity and a slowing in growth in labour costs, to convince the RBA that disinflation is sustainably on track.

In the old 11-meeting timetable, it was usually assumed that the months that the RBA published a Statement on Monetary Policy (SMP) – February, May, August and November – were good months to move. In those months, the Board had new inflation data and fresh forecasts, as well as the SMP to explain the decision more expansively. But the inflation data say more about where inflation has been, not where it is going. And as the monthly inflation indicator improves, the information value of the quarterly CPI release diminishes.

Assessing the inflation outlook instead requires information about its drivers, including labour costs, productivity and the balance of demand and supply. The September meeting, along with the other non-SMP meetings, come more into play, because it is ahead of these meetings that wages and national accounts data become available. In addition, the extra value of the SMP for explaining the Board’s decisions is reduced now that the Governor will give a media conference after every meeting. Under the new operating rhythm, all meetings are in principle equally good opportunities to move.

Push and pull risks

In thinking about the risks around this view on timing, the different sources of risk are pulling in opposite directions.

The risks relating to the data would, if realised, tend to pull the date of the first rate cut forward. Over the past few months, the data have tended to be softer than the RBA expected back in November. Further surprises in this direction would start to shift the inflation outlook lower. At some point, this would mean the RBA Board would reach the necessary degree of confidence about the return of inflation to target sooner. It would, however, need a material downside surprise to domestic demand that drags services inflation down faster than currently expected.

A date much sooner than September seems unlikely, however, because of the countervailing risk from the Board’s decision-making and perception of policy risk. These are considerations that would tend to push the date later.

Put simply, the RBA Board is far from being in a hurry to cut the cash rate. They do not want to risk delaying the return of inflation to target. Indeed, they would be happy to get there sooner. Even on the expected trajectory, inflation will have been above target for four years by the time it returns there. The Board is mindful that the longer inflation stays above target, the greater the risk that inflation expectations dislodge. While so far there is no evidence of this happening, it is not a risk the Board would take by moving too quickly. If expectations do shift, it could be hard to return them to target. The Board is also conscious that the peak of the cash rate has been lower here than in some peer economies. So at some level there is less work to do and less of an imperative to get on with it.

There are risks on both sides, but good reason to think these counterbalance each other. At this stage, we see the risks around the September call as balanced rather than tilted one way or another.

Beyond the first 50 (basis points)

We expect the Board to cut twice, in September and November – successive meetings under the new timetable. It is likely to wait and see the effect of these for a while before embarking on further cuts. In particular, it will want to see the effects of the tax cuts in the second half of 2024 on household spending. At this stage, though, we expect further cuts in 2025.

The closer the cash rate returns to something like neutral, the more cautious the Board is likely to be in making further moves. When you are a long way from where you need to be, rapid shifts may be called for. When you are closer to an uncertain destination, it pays to move slowly and wait for more information if possible.

Preview of RBNZ February 2024 Monetary Policy Statement

Westpac economics sees the RBNZ leaving the OCR at 5.5% at the February Monetary Policy Statement and adopting a hawkish outlook for the OCR.

Hawkish hold expected

- We expect the RBNZ will leave the OCR unchanged at 5.5% at its February policy meeting.

- The RBNZ's short term forward profile for the OCR is likely to be little changed and continue to suggest a chance of a further lift in the OCR perhaps at the May Monetary Policy Statement.

- The longer-term OCR profile may be revised up – especially if another adjustment of the neutral OCR occurs.

- More hawkish scenarios are realistic – but we see a 25bp tightening as just a 25% probability.

- Future data on non-tradables inflation, the labour market, the housing market and the Budget will be key in making the case for any further tightening – but in May, not at the current time.

- We continue to expect the OCR to remain at 5.5% until early 2025.

The RBNZ's decision and forward track.

We expect the RBNZ to leave the OCR at 5.5% at its February policy meeting and think that most interest will centre on the profile for interest rates in 2024 and beyond. A hike in the OCR is main alternative outcome with a 25% probability.

We think the RBNZ's objective will be to try to maintain the recent repricing in financial markets which has removed the expectation of rate cuts until at least the end of this year. The RBNZ will also leave open the option to tighten at the May Monetary Policy Statement, should the data warrant.

We think the RBNZ will be on edge due to some aspects of the recent data flow – even though a straight read of the entirety of that flow probably shouldn't increase concerns that inflation will move back inside the target range. Our recent "Hawks, Doves and Kiwis" note includes a number of charts that illustrate the issues discussed here. The key issues raising those concerns will be:

- the slower than expected increase in the unemployment rate (which will likely require a further adjustment of their labour market forecasts to push out the period over which the labour market adjusts).

- the higher-than-expected non-tradables inflation outcome – that comes after a string of similar disappointments on this score. If the RBNZ adjusts up its Q1 2024 non-tradables forecast to Westpac's own level (Westpac forecast +1.4% q/q, 5.6% y/y vs. RBNZ November Statement 1.0% q/q, 4.9% y/y) this will further amplify their concerns that non-tradables inflation won't subside quickly this year.

Market views will likely be best anchored around an expectation of no easing in 2024 by leaving the shortterm OCR forecast track unchanged from November. As noted below, a straight read of the data that has emerged since November might suggest a lower OCR track. This is because those more concerning inflation factors have been balanced to some extent by the significantly lower headline inflation outcome and much weaker GDP and economic momentum (among others – see below).

But we think the RBNZ will down-weight those more comforting factors and keep open the option of tightening in May and leave the short-term OCR forecast track unchanged. Further out, we see potential for increased in the OCR track (through 2025 and beyond) as they may further revise up their estimate for the neutral OCR (which has been revised twice in the last 6 months). The increased medium term inflation pressure coming from the required adjustments to their labour market forecasts may require an offset in terms of the length of time the OCR remains around 5.5%. This approach would be consistent with continuing with the "longer" rather than "higher" strategy in place since May 2023.

Key developments.

A straight read of the data flow since the November Statement might imply a more comforting inflation outlook – although we suspect the RBNZ will put more weight on the more concerning data points. Below, we discuss key data developments since the November MPS (arrows in brackets give our assessment of the likely first-round impact of this data on the RBNZ's assessment of the OCR):

Most important factors.

- GDP (↓↓↓): The Q3 GDP report suggested the economy was 1.8% smaller than the RBNZ forecast in November. Recent economic momentum was weaker than expected, (-1% surprise in the last six months). The RBNZ will assume that some of this surprise reflects weaker productivity growth and potential supply. But most of the more recent weakness is likely indicative of a lower output gap profile and hence less medium-term inflation pressure.

- Headline inflation and inflation expectations (↓): Annual CPI inflation was 0.3% lower than the RBNZ expected in Q4. The RBNZ will see this as helping lower inflation expectations which will dampen future inflation pressures. Lower business sector inflation expectations will have confirmed this.

- Non-tradables inflation (↑↑): Non-tradables inflation was again higher than expected by the RBNZ in Q4 (0.2ppts higher) and remained elevated at 5.9% y/y. This will be of concern as it follows a few quarters of surprises in the same direction and suggests that non-tradables inflation will only slowly fall from here.

- Labour market (↑↑): The unemployment rate rose 0.2ppts less than the RBNZ had expected in Q4 and private sector wage growth was also firmer than expected. This will likely force a further adjustment in the RBNZ's labour market forecasts following on from similar adjustments in the last few Statements.

Secondary factors.

- Migration (←→): News regarding migration is likely to have been a wash for the RBNZ. While the peak in annual migration – in October – was slightly above the RBNZ's expectations, there has been tentative evidence that the cycle has peaked. It remains to be seen how quickly the migrant inflow will ebb from here.

- Housing market (↓): Both housing turnover and house prices have been subdued in recent months and expectations of short-term house price growth have been accordingly scaled back a bit. The RBNZ should be more comfortable about this at the margin but may want to see how the market evolves in coming months to get a read on how the market will evolve over the year ahead.

- Global economy (←→): The US economy has continued to significantly outperform expectations with consensus forecasts of growth revised up accordingly. However, consensus forecasts of 2024 growth in the Asia-Pacific region – the most important region for New Zealand's exports – are unchanged from those held in November (although actions taken by Chinese authorities have slightly moderated nearterm downside risks associated with that economy). Consensus forecasts for growth in Western Europe have been revised down modestly.

- Global policy context (↓): Importantly, policy makers now seem surer that official interest rates will be reduced at some point in the coming year. This likely raises the bar a bit for the RBNZ to diverge from the general direction of the global pack – although we think the timing of any RBNZ easing will reflect domestic economic factors and not offshore central bank actions.

- Export prices (↑↑): Some key export commodity prices have shown welcome improvement over recent months, notably the price of whole milk powder which has increased 11% since the November MPS. The improved outlook will nonetheless have come as a relief to the rural sector where a paring back of spending likely contributed to the weakness of the economy in the second half of last year.

- Exchange rate (↓↓): The trade-weighted exchange rate (TWI) is currently more than 2% stronger than the RBNZ had assumed in November. An upward revision to the RBNZ's forecast will directly lower the RBNZ's forecasts of inflation in the tradables sector over the coming year.

- Fiscal settings (←→): If the RBNZ takes the HYEFU forecasts at face value, the cumulative negative fiscal impulse over the forecast period is fractionally smaller than was depicted in the PREFU. However, the RBNZ will likely defer any strong judgment on the implications of fiscal policy for the economic outlook until the Government has published its Budget Policy Statement (27 March) and Budget 2024 (30 May).

The communications objective.

We think the RBNZ is likely to be happy with current market pricing. They will likely have been very uncomfortable with market views of near term easing that were held in December and January. Similarly, we suspect they were also not as hawkish as market views a week or so ago. We think the RBNZ will want to allow the option to tighten in May should data support that view. We don't think the RBNZ will want to see markets price in rate cuts for at least 6 months.

We think the RBNZ will want to encourage markets to maintain current short-term pricing (i.e. a 50/50 chance of a hike at the May Statement) and drive home the view that the OCR is not moving lower in 2024. This will ensure retail lending rates don't fall and will prepare markets for a hike should data in the next few months suggest reduced confidence that inflation will decline to 2% in the second half of 2025.

Scenarios.

We see three main scenarios:

- Baseline case (65% probability) the OCR is unchanged and the RBNZ retains a similar short term OCR track to November (peak OCR in Q3 – maybe bought forward to Q2 - at around 5.69%). Longer term OCR expectations could be revised up if the RBNZ makes another adjustment to its neutral OCR estimate or if the RBNZ sees increased medium term inflation risks from the slowly adjusting labour market. The RBNZ could hike at the May MPS should core inflation pressures not significantly abate (Q1 CPI due 17 April), if the labour market doesn't sufficiently adjust (Q1 data due 1 May) or if the government's fiscal stance appears insufficient to ameliorate inflation concerns (Budget 24 will be released after the MPS but we expect the RBNZ will have the key data before then).

- Hawkish case (25%) the OCR is hiked to 5.75% and the forecast track is revised up to convey a risk of a further rate hike in 2024. Easing might be pushed out to mid-2025. This would be linked to risks of housing strength, a slower rise in the unemployment rate from here and an ongoing sluggish response of core inflation to tighter monetary conditions.

- Dovish case (10%) the OCR remains at 5.5%. The OCR track is revised down slightly to be like that in the August MPS (i.e., around a one-third chance of a hike this year), but the OCR remains at 5.5% until early 2025. Upside risks to the OCR might be mentioned but be of a much lower profile – the core message would be one of OCR stability through 2024).

Our OCR view for 2024.

We expect the OCR to remain unchanged over 2024. There are certainly risks of another move higher – most likely around the middle of the year once further data on the extent of labour market adjustment, core inflation pressures, migration and housing market pressures and the fiscal stance become much clearer. But, more likely, as the year proceeds it will become more apparent that inflation is on the right track, implying the current level of the OCR is the right one, given sufficient time.

NZ First Impressions: Retail trade, December Quarter 2023

Retail spending was much weaker than expected in the December quarter, highlighting weak household spending appetites in the face of high inflation and high borrowing costs.

December quarter real retail sales (volumes): -1.9% (Prev: -0.8%)

Westpac f/c: -0.6%, Market: -0.2%

December quarter nominal sales level: -1.5% (Prev: 0.8%)

Annual changes (September 2023 vs September 2022)

- Nominal sales: -0.4%

- Volume of goods sold: -4.1%

Retail spending has been much weaker than expected.

Overall spending levels were down 1.9% in the December quarter. And updated estimates of spending in the September quarter now show a 0.8% drop (earlier estimates suggested that spending had been flat over the September quarter).

Today’s result was below market forecasts for a 0.2% decline, and even weaker than our bottom of market forecast for a 0.6% fall.

Weakness in spending has been widespread. Notably, there have been continued declines in spending in interest rate sensitive areas, such as spending on household durables like furnishings and appliances. We’ve also seen continued falls in spending in the hospitality sector.

What does this tell us about the strength of spending?

Today’s report highlights the significant impact that price increases and higher borrowing costs are having on spending appetites. Nominal spending levels were down 0.4% over the past year. But with strong price growth, the amount of goods that households are actually taking home has dropped 4% over the past year. And it’s been falling for two years now as strong financial pressures have squeezed households’ spending power.

Notably, those declines have come at the same time as population growth has been surging. In per capita terms, the volume of goods that households are taking home has fallen 6.7% over the past year.

With interest rates at high levels and inflation still strong, we expect continued weakness in spending over 2024.

Implications for GDP growth

Today’s result was weaker than expected. We’re currently forecasting a modest 0.1% rise in December quarter GDP. We’ll review that number over the coming weeks as more data comes to hand.

EUR/USD – A Bullish Breakout or Just Further Consolidation?

- Eurozone sees marginal improvement in surveys

- US services cool in February

- EURUSD breaks through descending channel

The PMI surveys have certainly made it an eventful day in the markets, albeit one that doesn’t necessarily provide more clarity on interest rate movements in the coming months.

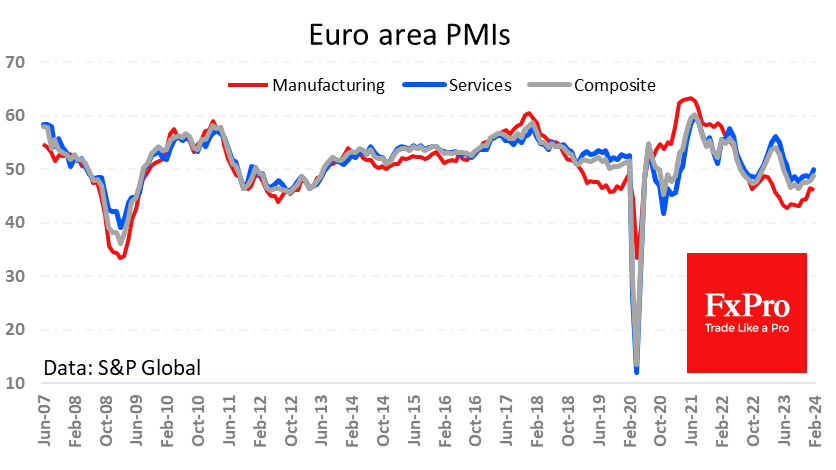

The eurozone PMIs displayed some improvement on the services side, with the survey moving out of contraction territory for the first time in six months. Manufacturing on the other hand reversed some of the recent progress and remained deep in contraction.

Economic resilience, even strength, in the US has proven to be a burden rather than a benefit as its cast doubt over whether the Federal Reserve should commence cutting interest rates soon.

Today’s surveys may help to alleviate some of those concerns, with the services PMI slipping back from last month to 51.3.

How bullish is this week’s breakout?

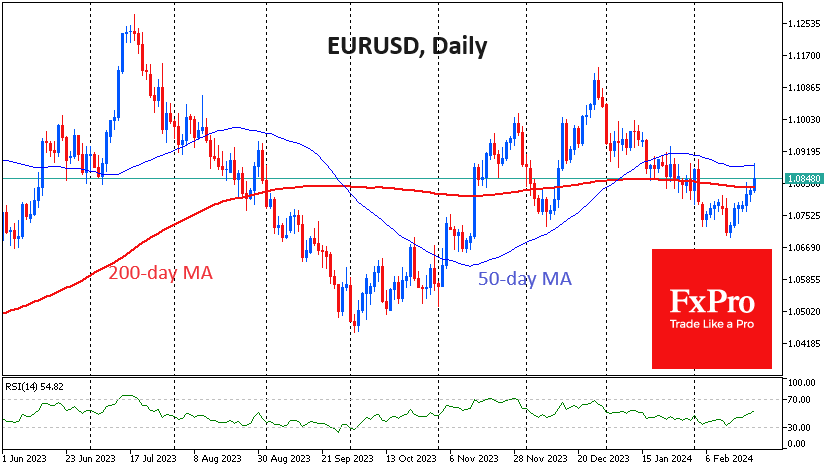

EURUSD broke higher earlier in the week after bouncing off the 61.8% Fibonacci retracement level the week prior.

EURUSD Daily

Source – OANDA

The break above the descending channel could be a very bullish signal, particularly coming so soon after the Fib bounce. The only issue may be that the pair has been largely rangebound for some time.

While this may suggest it’s gathering some upside momentum, it’s too early to say where that will take it and whether 1.10 or the late December highs will be breached.

Fed’s Jefferson anticipates monetary easing later this year, cautiosly optimistic on inflation progress

Fed Vice Chair Philip Jefferson's speech today offered insights into the monetary policy outlook and identified key risks in the coming months. He suggested that, assuming the economy develops as anticipated, "it will likely be appropriate to begin dialing back our policy restraint later this year."

He highlighted three principal risks that warrant close monitoring. First, consumer spending could be "more resilient" than expected, which could inadvertently halt progress on inflation. Second, the possibility of employment weakening as the factors currently bolstering economic growth begin to wane. Jefferson addressed geopolitical risks, specifically the possibility of escalating conflicts in the Middle East and their broader impact on commodity prices, such as oil, and global financial markets.

Overall, Jefferson remained "cautiously optimistic" on the progress on inflation, and emphasized the importance of considering the "totality of incoming data" in shaping Fed's policy decisions.

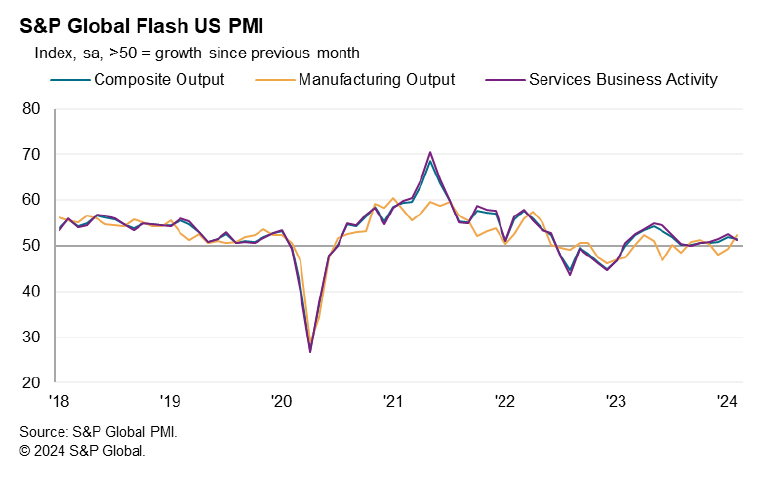

US PMI composite falls to 51.4, sustained expansion and subdued price pressures

US PMI Manufacturing jumped from 51.5 to 50.7 in February, a 17-month high. PMI Services fell from 52.5 to 51.3. PMI Composite also fell from 52.0 to 51.4.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said:

"The early PMI data for February indicate that the US economy continued to expand midway through the first quarter, pointing to annualized GDP growth in the region of 2%. Although service sector growth cooled slightly, manufacturing staged a welcome return to growth, with factory output growing at the fastest rate for ten months.

"Better weather conditions compared to January trumped shipping concerns, helping drive an overall improvement in supplier delivery times, which in turn facilitated higher factory production. Signs of inventory reduction policies becoming less widespread also helped boost production and sustain high levels of business confidence in the outlook for the year ahead among manufacturers.

"Service sector growth has slipped slightly, however, as has confidence in the year-ahead outlook among service providers, in part reflecting some pull back in the extent to which interest rates are expected to fall in 2024. It is nevertheless welcome news that both manufacturing and services are expanding again for the first time in three months.

"The sustained expansion is being accompanied by subdued price pressures. Although up slightly in February, the survey's gauge of selling prices for goods and services continues to run at a level consistent with the Fed hitting its 2% inflation target, and a further fall in cost growth to the lowest since October 2020 hints at price pressures remaining subdued in the coming months."

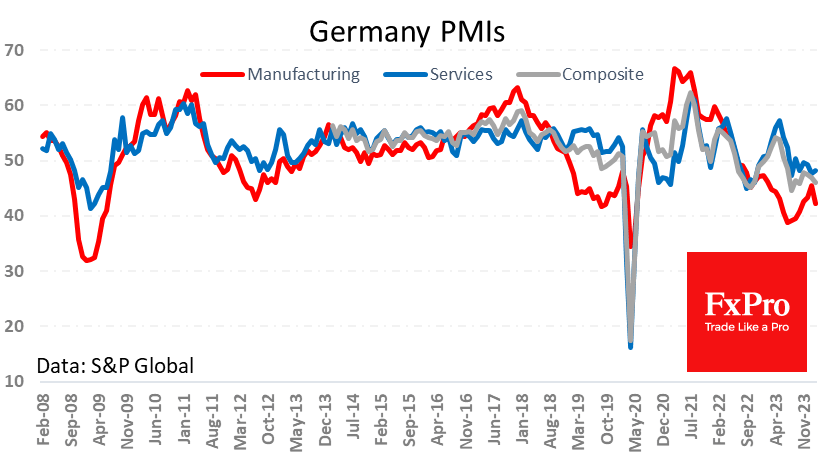

Disappointing German Manufacturing Halted Euro’s Flight

Mixed PMI data from various Euro area countries led to a surge in volatility for European currency pairs on Thursday morning.

Preliminary estimates for France surprised with their strength. The manufacturing PMI jumped from 43.1 to 46.8 (43.5 expected). The services index rose from 45.4 to 48.0 (45.7 expected). These figures came well above expectations, boosting risk appetite and supporting buying in both the single currency and equities.

However, the EURUSD’s rise to 1.0887 was rudely halted by the release of the exact figures for Germany, where the manufacturing index fell to 42.3 from 45.5 (expected 46.1). The services index rose to 48.2 from 47.7 (48.0 was expected).

For the euro area, the manufacturing index fell from 46.6 to 46.1, against expectations for a rise to 47.0. The services sector reached the critical milestone of 50.0. Readings below this level indicate a month-on-month contraction, and the overall composite PMI for the euro area remained in contractionary territory for the seventh consecutive month. However, it has risen to 48.9, the highest level since June last year.

The EURUSD rose for the seventh consecutive session. The bulls tested the 200-day average earlier in the week, and the pair traded above this important trend indicator on Thursday morning. For much of last month, the pair was bought on dips below this line, and clearly, they did not want to stay away from it for long in February. The ability to attract buyers from these levels could set up a sustained uptrend.

However, the course of trading suggests that it will be a very bumpy and uneven road. On Thursday, in addition to the disappointment of the weak German data, the 50-day moving average acted as resistance. This dynamic suggests that we may see an intense tug-of-war in the coming days before the bulls can mount an offensive.

Fundamental pressures on the dollar against the euro include expectations that the Fed will start cutting rates much sooner than the ECB.

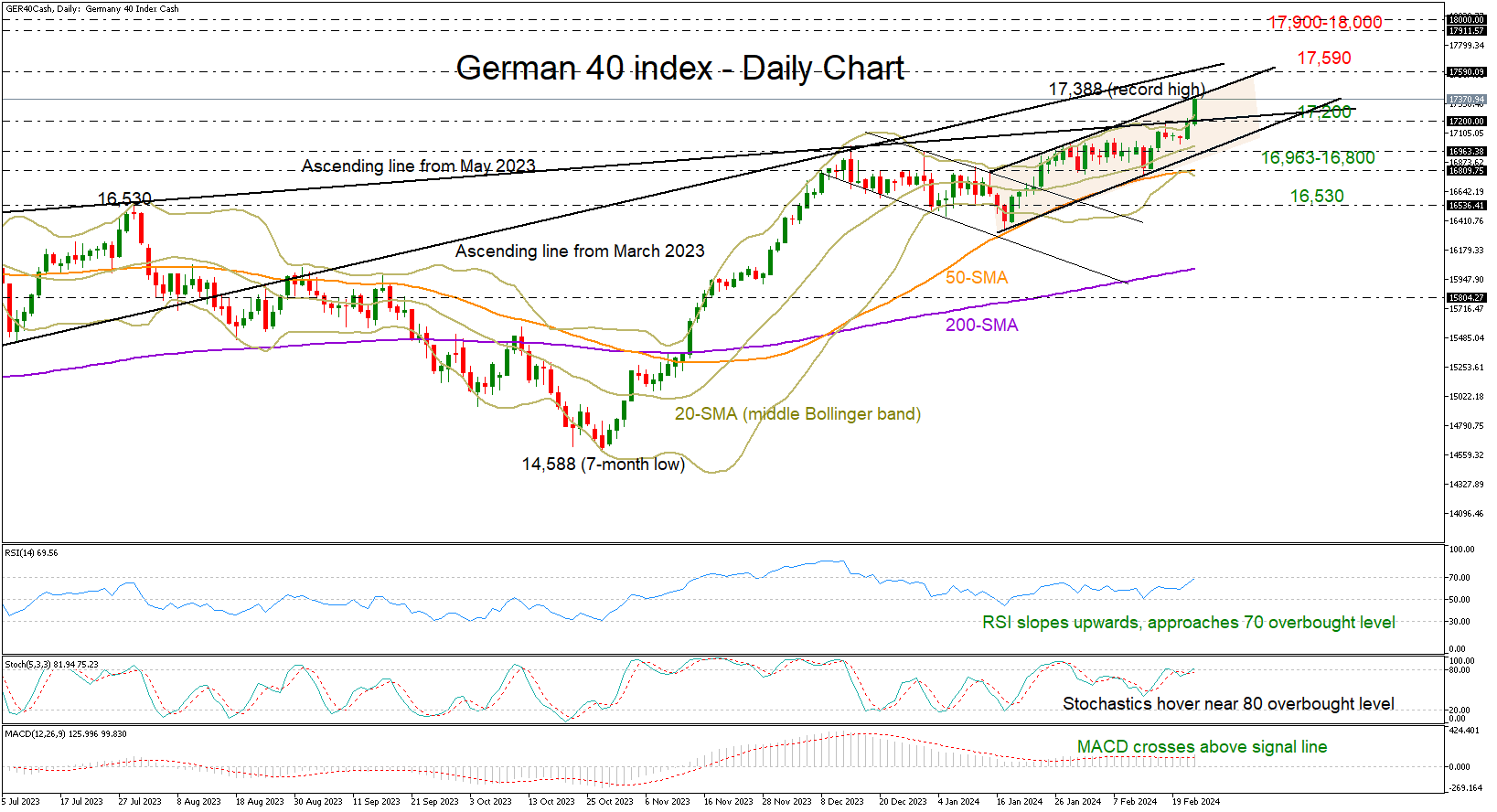

GER 40 Index Back at Record Highs

- The German 40 index hits a record high within bullish formation

- Might be sailing within overbought waters, but there is still some bullish power

Despite the disappointing manufacturing PMI data, the German 40 index (cash) managed to spike to a record high of 17,388 on Thursday, rising above the important resistance line which has been blocking the bulls during 2023.

The index has been resilient above its short-term simple moving averages (SMAs) over the past month, but with the price set to close comfortably above the upper Bollinger band and trading around the upper edge of a short-term bullish channel, a downside correction cannot be excluded. Still, the RSI and the stochastic oscillator have not confirmed overbought conditions yet, suggesting that the bulls might stay in play for a bit longer before the next bearish wave takes place.

On the upside, the 161.8% Fibonacci extension of the previous downleg at 17,410 is within breathing distance, while slightly higher, the ascending trendline from March 2023 at 17,590 could be another tough barrier. Surpassing the latter, the door could open for the 17,900-18,000 territory.

Alternatively, a negative reversal could initially halt near the 17,200 constraining zone. If the bears claim that region, the price could slide to stabilize around the channel’s lower band at 16,963 or near the 50-day SMA at 16,800. If selling tendencies intensify from there, the index may head down to meet July’s high of 16,530.

Overall, the German 40 index has restored its bullish trajectory, and only a drop below 16,960 would downgrade the outlook back to neutral.