Sample Category Title

EUR/USD Mid-Day Outlook

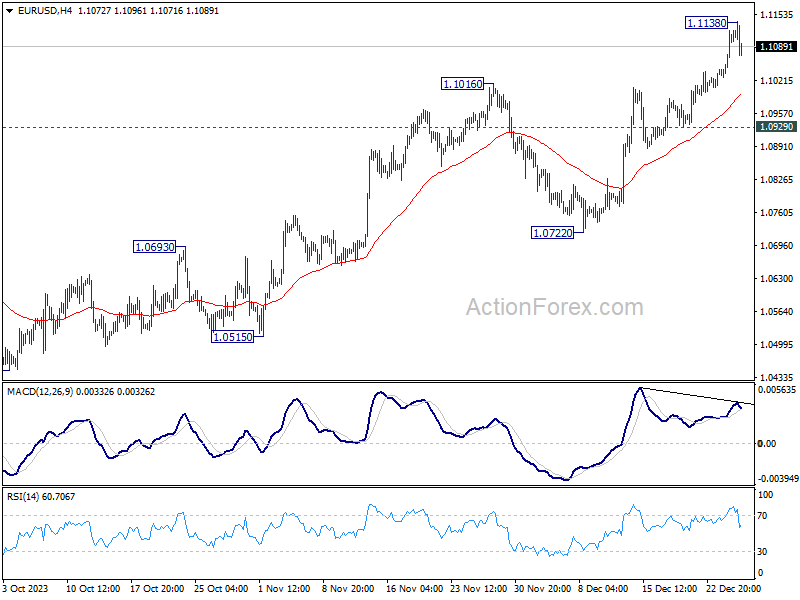

Daily Pivots: (S1) 1.1050; (P) 1.1086; (R1) 1.1144; More...

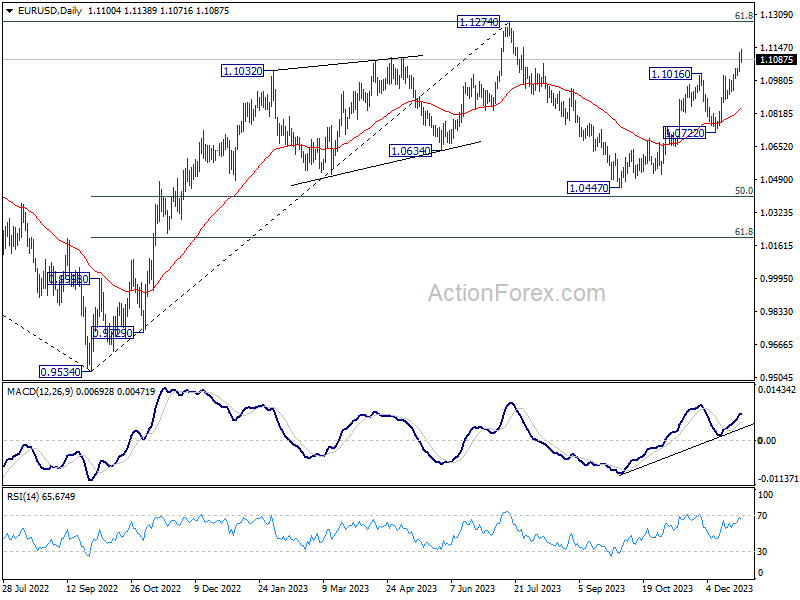

Intraday bias in EUR/USD is turned neutral first with current retreat, and some consolidations could be seen. For now, further rally is expected as long as 1.0929 support holds. Break of 1.1138 temporary top will resume the rise from 1.0447 to retest 1.1274 high. Strong resistance should be seen from there to limit upside, at least on first attempt. Meanwhile, break of 1.0929 will indicate short term topping and turn bias back to the downside for 1.0772 support.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

GBP/USD Mid-Day Outlook

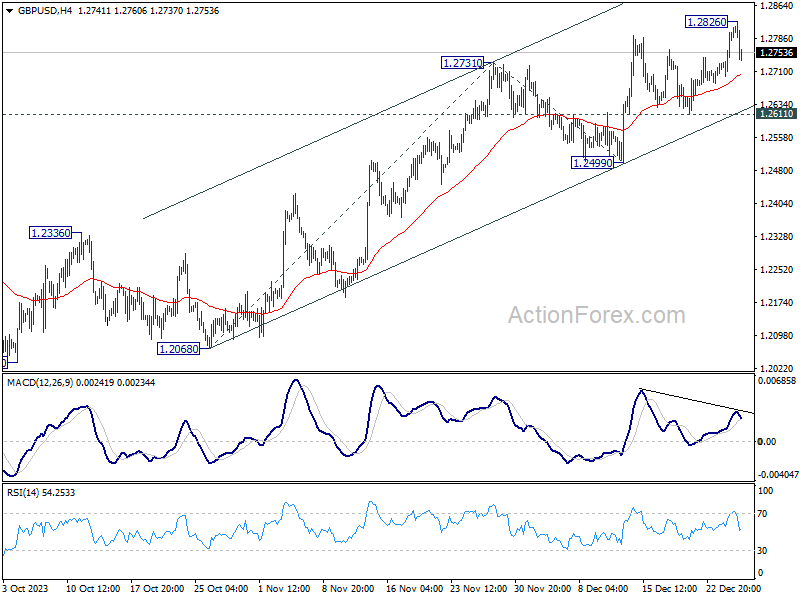

Daily Pivots: (S1) 1.2731; (P) 1.2767; (R1) 1.2835; More...

Intraday bias in GBP/USD is turned neutral again with current retreat. For now, further rise is in favor as long as 1.2611 support holds. Above 1.2826 will resume larger rise from 1.2036 to 61.8% projection of 1.2068 to 1.2731 from 1.2499 at 1.2909. Nevertheless, break of 1.2611 will indicate short term topping, and turn bias back to the downside for 1.2499 support.

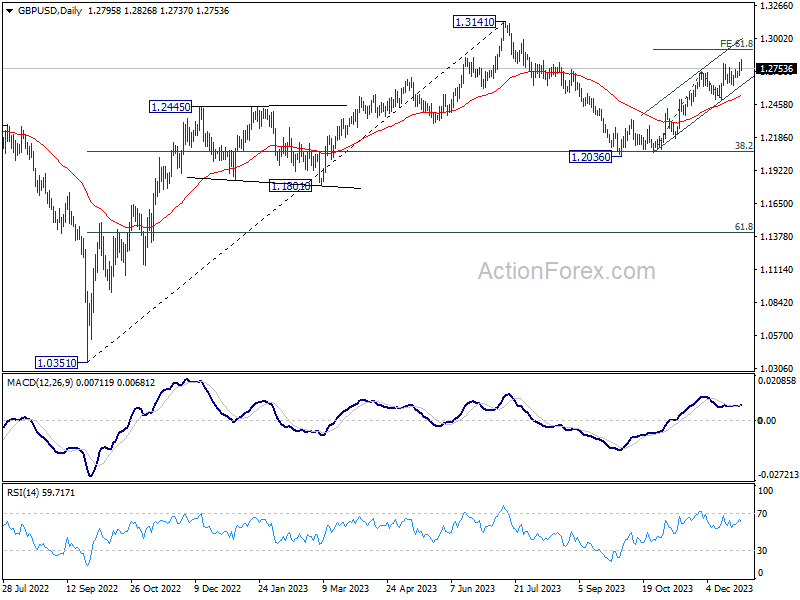

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to rise from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

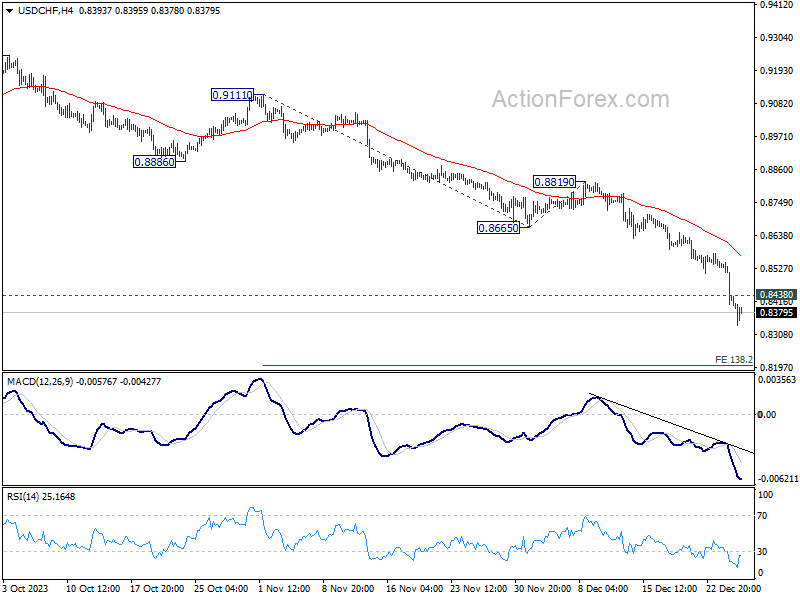

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8377; (P) 0.8463; (R1) 0.8517; More....

Intraday bias in USD/CHF remains on the downside for the moment. Current fall from 0.9243 should target 138.2% projection of 0.9111 to 0.8665 from 0.8819 at 0.8203 next. On the upside, above 0.8438 minor resistance will turn intraday bias neutral first. But outlook will stay bearish as long as 0.8665 support turned resistance holds, in case of recovery.

In the bigger picture, break of 0.8551 support indicates resumption of whole decline from 1.0146 (2022 high). Next target is 61.8% retracement of 1.0146 to 0.8551 from 0.9243 at 0.8257. Sustained break there could prompt downside acceleration to 100% projection at 0.7648. This will now remain the favored case as long as 0.8819 resistance holds.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 141.31; (P) 142.08; (R1) 142.61; More...

USD/JPY's break of 140.94 indicates resumption of fall from 151.89. Intraday bias is now on the downside. Next target is 136.63. fibonacci level. On the upside, above 142.84 minor resistance will turn intraday bias neutral gain. But recovery should be limited below 144.94 resistance to bring another decline.

In the bigger picture, fall from 151.89 is seen as the third leg of the corrective pattern from 151.93 (2022 high). Deeper decline would be seen to 61.8% retracement of 127.20 to 151.89 at 136.63, sustained break there will pave the way to 127.20 support (2022 low). This will now remain the favored as long as 146.58 resistance holds.

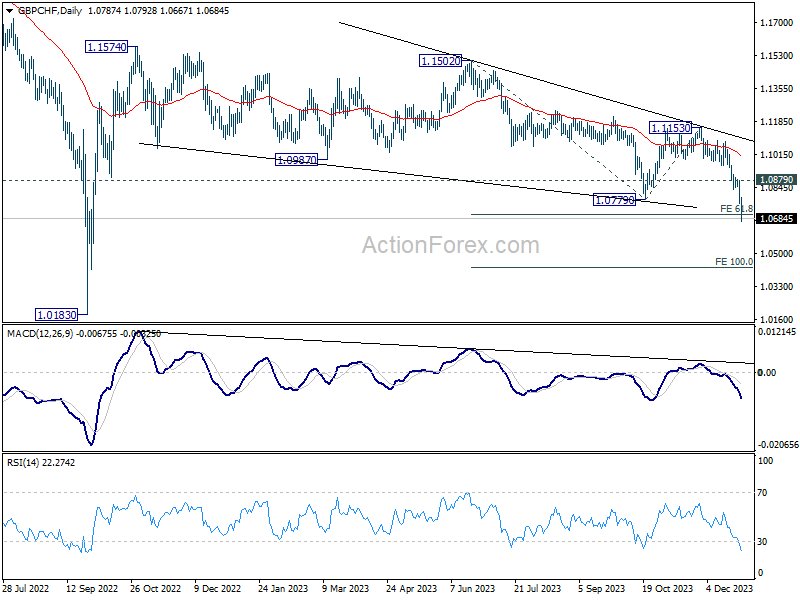

Yen and Swiss Franc Rally in Subdued Markets; Downside Acceleration in GBP/CHF

Japanese Yen and Swiss Franc are standing out with significant rallies in otherwise relatively subdued markets today. Yen resumed its near-term rise against the Dollar, reaching its highest level in five months. Simultaneously, Swiss Franc has achieved its highest level in over a decade, excluding the spike seen in 2015.

While Dollar remains the weakest performer for the week, its selloff against currencies like the Sterling, Canadian Dollar, and Australian Dollar appears to be decelerating slightly. Euro remains firm, although it's underperforming against Yen and Franc. But the Sterling is noticeably underperforming compared to its European peers.

Technically, GBP/CHF's decline accelerates further to as low as 1.0667 so far. 61.8% projection of 1.1502 to 1.0779 from 1.1153 at 1.0706 is take out. Near term outlook will stay bearish as long as 1.0879 resistance holds. Next target is 100% projection at 1.0430.

In Europe, at the time of writing, FTSE is up 0.05%. DAX is down -0.19%. CAC is down -0.41%. Germany 10-year yield is up 0.035 at 1.931. UK 10-year yield is up 0.062 at 3.497. Earlier in Asia, Nikkei fell -0.42%. Hong Kong HSI rose 2.52%. China Shanghai SSE rose 1.38%. Singapore Strait Times rose 1.38%. Japan 10-year JGB yield fell -0.0056 to 0.593.

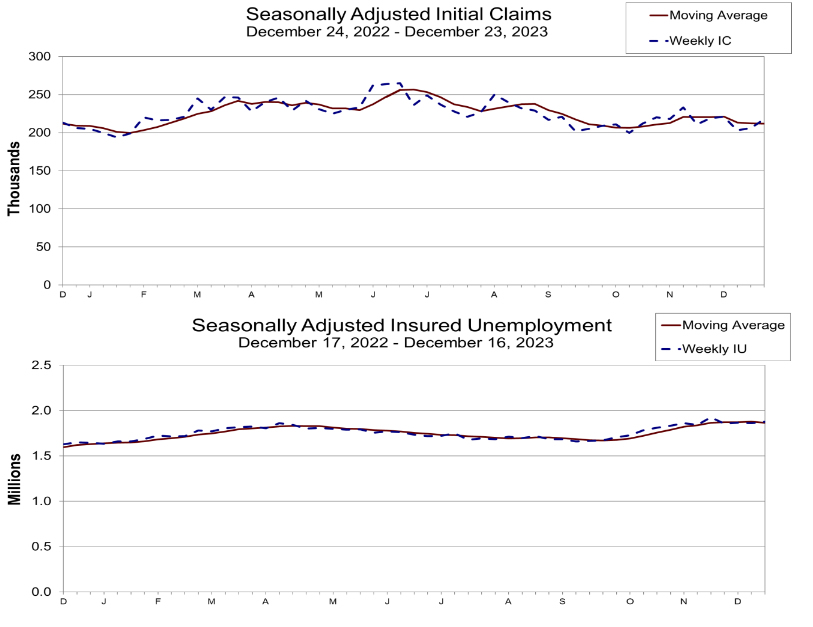

US initial jobless claims rises to 218k, vs exp 204k

US initial jobless claims rose 12k to 218k in the week ending December 23, above expectation of 204k. Four-week moving average of initial claims fell -250 to 212k.

Continuing claims rose 14k to 1875k in the week ending December 16. Four-week moving average of continuing claims fell -12.5k to 1865k.

US goods trade deficit widens slightly to USD -90.3B in Nov

US goods export fell -3.6% mom to USD 165.1B in November. Goods imports fell -2.1% mom to USD 255.4B. Goods trade deficit widened from USD -89.6B to USD -90.3B, slightly larger than expectation of USD -89.5B.

Wholesale inventories fell -0.2% mom to USD 895.7B. Retail inventories fell -0.1% mom to USD 794.9B.

ECB's Holzmann cautions against expectations of 2024 rate cuts

ECB Governing Council member Robert Holzmann emphasized there should be no presumption of rate reductions in the coming year.

Holzmann stated, "Even if the ECB is past an unprecedented series of ten consecutive rate increases, there is also for the year 2024 no guarantee of rate reductions."

Further reinforcing this cautious approach, Holzmann remarked on the current status of inflation and the ECB's policy measures, "Monetary policy normalization is already showing its impact on slowing inflation, but it would still be premature to think about rate cuts."

Japan's industrial production down -0.9% mom, continues to seesaw indecisively

Japan's industrial production fell -0.9% mom in November, marking the first decrease in three months. This drop, however, was less severe than the expected -1.6% mom decline. A notable factor in the contraction was -2.5% mom fall in motor vehicle production. Among the 15 sectors surveyed, 11 reported decreased production, while four sectors experienced increases.

Index of industrial shipments also dropped by -1.3% mom, aligning with overall decline in industrial production. Conversely, Index of inventories saw a marginal increase of 0.1% mom.

The Ministry of Economy, Trade and Industry maintained its assessment of industrial output as "fluctuating indecisively." Looking ahead, manufacturers expect a rebound in output by 6.0% mom in December, followed by -7.2% mom decrease in January 2023.

An METI official said, "We'll continue to monitor the impact of the global economic downturn and rising prices".

In separate release, retail sales data painted a more positive picture. Sales in November rose 5.3% yoy, exceeding forecast of 5.0% yoy, and marked the 21st consecutive month of expansion since March 2022. On a month-on-month basis, retail sales grew 1.0%, following 1.7% growth in October.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 141.31; (P) 142.08; (R1) 142.61; More...

USD/JPY's break of 140.94 indicates resumption of fall from 151.89. Intraday bias is now on the downside. Next target is 136.63. fibonacci level. On the upside, above 142.84 minor resistance will turn intraday bias neutral gain. But recovery should be limited below 144.94 resistance to bring another decline.

In the bigger picture, fall from 151.89 is seen as the third leg of the corrective pattern from 151.93 (2022 high). Deeper decline would be seen to 61.8% retracement of 127.20 to 151.89 at 136.63, sustained break there will pave the way to 127.20 support (2022 low). This will now remain the favored as long as 146.58 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Industrial Production M/M Nov P | -0.90% | -1.60% | 1.30% | |

| 23:50 | JPY | Retail Trade Y/Y Nov | 5.30% | 5.00% | 4.20% | 4.10% |

| 13:30 | USD | Initial Jobless Claims (Dec 22) | 218K | 204K | 205K | 206K |

| 13:30 | USD | Goods Trade Balance (USD) Nov P | -90.3B | -89.5B | -89.6B | |

| 13:30 | USD | Wholesale Inventories Nov P | -0.20% | -0.20% | -0.40% | |

| 15:00 | USD | Pending Home Sales M/M Nov | 1.10% | -1.50% | ||

| 15:30 | USD | Natural Gas Storage | -80B | -87B | ||

| 15:30 | USD | Crude Oil Inventories | -2.7M | 2.9M |

US initial jobless claims rises to 218k, vs exp 204k

US initial jobless claims rose 12k to 218k in the week ending December 23, above expectation of 204k. Four-week moving average of initial claims fell -250 to 212k.

Continuing claims rose 14k to 1875k in the week ending December 16. Four-week moving average of continuing claims fell -12.5k to 1865k.

US goods trade deficit widens slightly to USD -90.3B in Nov

US goods export fell -3.6% mom to USD 165.1B in November. Goods imports fell -2.1% mom to USD 255.4B. Goods trade deficit widened from USD -89.6B to USD -90.3B, slightly larger than expectation of USD -89.5B.

Wholesale inventories fell -0.2% mom to USD 895.7B. Retail inventories fell -0.1% mom to USD 794.9B.

AUD/USD Eyes Chinese PMIs

- China releases PMIs on Saturday

The Australian dollar has edged lower on Thursday. In the European session, AUD/USD is trading at 0.6833, down 0.21%. Earlier today, the Aussie climbed as high as 0.6871, its highest level since July.

Risk appetite rise boosts Aussie

The US dollar has hit rough times and the Australian dollar has taken full advantage, surging 7.8% since November 1st. The US dollar has fallen sharply against the other major currencies over the past two months, as the markets expect the Federal Reserve to cut interest rates up to six times next year. Fed members have cautioned that the market is getting ahead of itself but don’t expect markets to dampen expectations after Fed Chair Powell pencilled in three rate cuts in 2024 at the December meeting.

There are no Australian events this week but the risk-on mood in the financial markets has boosted the Australian dollar, which is headed for a third straight winning week. Investors will be keeping an eye on Chinese PMIs which will be released on Saturday. China’s recovery has been patchy and the slowdown has resulted in deflation in the world’s number two economy. The manufacturing sector has been mired in contraction for most of this year and non-manufacturing expansion has been steadily falling and has stagnated over the past two months.

The PMI releases could have a strong impact on the direction of the Australian dollar early next week, as China is Australia’s largest export market. If the PMIs are stronger than expected, the Aussie could get a lift. Conversely, a weak PMI report would likely weigh on the Australian dollar.

The US labour market has remained strong despite the Federal Reserve’s steep rate-tightening cycle. Unemployment claims will be released later today, with a market consensus of 205,000, compared to last week’s reading of 210,000. The Fed is under pressure to lower interest rates early in 2024 but the robust labour market is complicating such a move, as jobs remain plentiful and workers are spending which is helping keep inflation high.

AUD/USD Technical

- AUD/USD tested resistance at 0.6853 earlier. Next, there is resistance at 0.6906

- 0.6772 and 0.6719 are providing support

ECB’s Holzmann cautions against expectations of 2024 rate cuts

ECB Governing Council member Robert Holzmann emphasized there should be no presumption of rate reductions in the coming year.

Holzmann stated, "Even if the ECB is past an unprecedented series of ten consecutive rate increases, there is also for the year 2024 no guarantee of rate reductions."

Further reinforcing this cautious approach, Holzmann remarked on the current status of inflation and the ECB's policy measures, "Monetary policy normalization is already showing its impact on slowing inflation, but it would still be premature to think about rate cuts."

Japanese Yen Keeps on Rolling

- Japanese retail sales climb but industrial production declines

- Japanese gain rises sharply

The Japanese yen has posted sharp gains on Thursday. In the European session, USD/JPY is trading at 140.66, down 0.82%.

Japanese retail sales beat forecast

Japanese releases were a mixed bag today. Retail sales impressed with a gain of 5.3% y/y in November, following a downwardly revised 4.1% gain in October and beating the market consensus of 5.0%. Monthly, retail sales climbed 1%, rebounding from a 1.6% decline in October.

The news was not as cheery on the manufacturing front, as Industrial Production declined by 0.9% m/m in November, compared to a 1.3% gain in October. Still, this was above the market consensus of -1.6%.

The mixed data is indicative of an uneven recovery. Consumer spending is solid and the service sector is expanding, while manufacturing is mired in a slump.

There has been feverish speculation that the Bank of Japan will exit its ultra-loose policy, but the BoJ will want to see stronger growth before making any dramatic shifts, which could include lifting rates into positive territory. The markets have circled January and April has strong possibilities for a move, but I would lean towards April, as the annual wage negotiations in March will help determine if inflation is sustainable. Let’s not forget that the BoJ has caught the markets off guard in the past with changes to policy and a move at the January meeting cannot be completely discounted.

In the US, the Federal Reserve has all but declared that the rate-tightening cycle is over. Fed Chair Jerome Powell has jumped on the rate-cutting bandwagon and has signalled that the Fed expects to trim rates three times in 2024. The markets are more bullish and have priced in six rates, starting as early as March. This has led some Fed members to caution that the markets are getting ahead of themselves and that rate cuts are not necessarily imminent..

USD/JPY Technical

- USD/JPY has pushed below support at 141.38 and is testing support at 140.78. The next support level is 140.01

- There is resistance at 142.08 and 142.61