Sample Category Title

Sunset Market Commentary

Markets

UK labour data published this morning served as a starter before for the release the US CPI this afternoon. The data came out on the soft side of expectations. November payrolled employees declined 13k from a gain of 39k in October (and 5k expected). The series is on a downtrend, but proved quite volatile over previous months. Probably more important for markets, average weekly earnings declined more than expected both including bonusses (7.2% from 8.0%) and the ex-bonus (7.3% from 7.8%). The report overall suggests that demand pressure might gradually ease but it will take time for this to translate into a sustained cooling of inflation to 2.0%. Even so, it again was enough for markets to bring forward the pricing of BoE rate cuts. A first 25 bps BoE rate cut is now discounted for June, rather than August. UK bonds outperform Bunds and Treasuries, with yields declining 7.0/9.0 bps across the curve. The interest rate reaction also called off recent attempt of sterling to strengthen beyond the EUR/GBP 0.855 support, now nearing the 0.86 big figure. Interesting to hear the BoE assessment on Thursday.

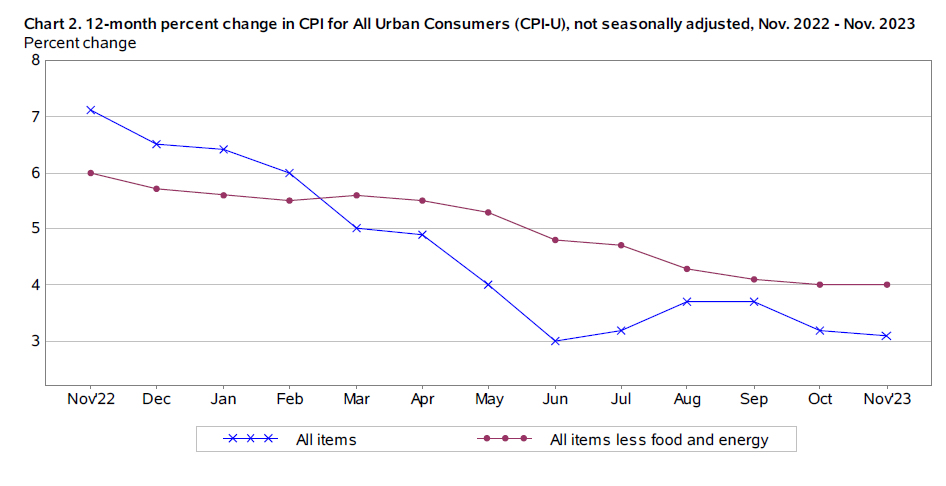

US November inflation data printed almost exact in line with expectations, with the headline at 0.1% M/M and 3.1% Y/Y and the core rising 0.3% M/M keeping the Y/Y measure unchanged at 4.0%. In a first reaction, the market briefly tried recent reaction function. No upside surprise in a first instance was seen as ‘soft’. However, markets soon understood that the report didn’t bring any new information to tomorrow’s Fed decision. US yields currently more than reverse most of the brief post-data drop with yields rising between 1.0-2.5 bps across the curve. Recent lows (in yields) will apparently stay intact going into tomorrow’s Fed decision. German Bunds still outperform with the 2-y unchanged but still declining up to 4.5 bps at the very long end (30-y). A stronger than expected ZEW economic confidence (expectations 12.8 from 9.8) as usual didn’t impress markets. Recent lows, especially for longer maturities are still quite nearby. Equities both in the US and Europe, ‘struggle’ to maintain recent gains (e.g. S&P 500 open -0.2%; EuroStoxx 50 -0.1%) still trying to sustainably break/hold above the YTD peak levels. The dollar broadly copied the reaction of yield markets, a tentative spike lower in the USD immediately after the CPI was (more than) reversed. At 103.9, DYX still trades a few ticks lower in a daily perspective. EUR/USD also is trading marginally higher (1.0785). USD/JPY trades near 145.6 (open of 146.18). Yesterday’s spike on Bloomberg comments that the BOJ likely isn’t going to phase out negative rates anytime soon was reversed intraday, but the pair rebounded post CPI.

News & Views

The European Commission released its semi-annual funding plan for the period covering January-June 2024 today. It intends to issue €75 bn of long-term EU bonds, complemented by short-term bills with the total, yearly amount within the boundaries of the yet-to-be-announced annual borrowing limit for 2024. Benchmark maturities range from 3 to 30 years, with issues through tap transactions and new lines, using auctions (seven planned) and syndications (six). The maturities for the new lines will depend on market conditions and the intention to bring liquidity to the curve where more is needed (with a tentative focus on 3y, 10y, 15y and possibly 30y for conventional lines). The EC may consider one new long dated green bond, alongside tap transactions in the first half of this year. The funds raised will be used to meet payments primarily related to NextGenerationEU and, in case of the green bond, to finance the green component of the recovery plan.

Chinese state media reported the country will step up policy adjustments to support an economic recovery next year. The media said that China plans to implement structural tax and fee cuts as well as a new round of fiscal and tax reforms with the structure of spending to be improved. It added that the country will maintain sufficient liquidity and make sure money supply matches the expected goals of economic growth. According to Reuters sources, next year’s growth goal may be set at around 5%, the same as in 2023. While that target may be achieved this year due to last year’s low-base effect (Covid lockdowns), sticking to the 5% for 2024 may prove much more difficult and could require more fiscal stimulus. The official growth target was discussed at the December 11-12 meeting by the country’s top leaders but will only be publicly announced at the opening of the annual parliament meeting, usually in March.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0744; (P) 1.0762; (R1) 1.0781; More...

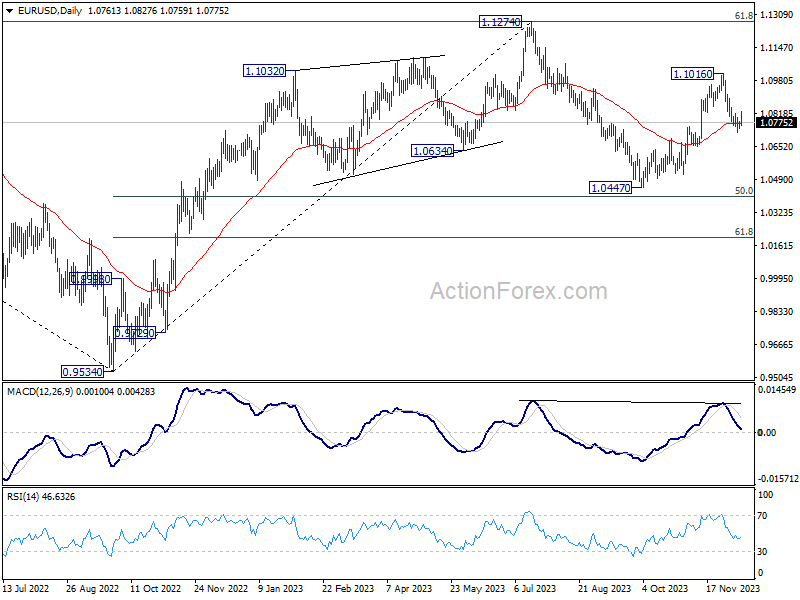

Intraday bias in EUR/USD remains neutral at this point. Further decline is expected with 1.0816 minor resistance intact. Break of 1.0722, and sustained trading below 55 D EMA (now at 1.0770) will extend the fall from 1.1016 short term top to retest 1.0447 support. However, on the upside, firm break of 1.0816 minor resistance will turn intraday bias back to the upside for stronger rebound.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 55 D EMA will argue that the third leg has already started for 1.0447 and below.

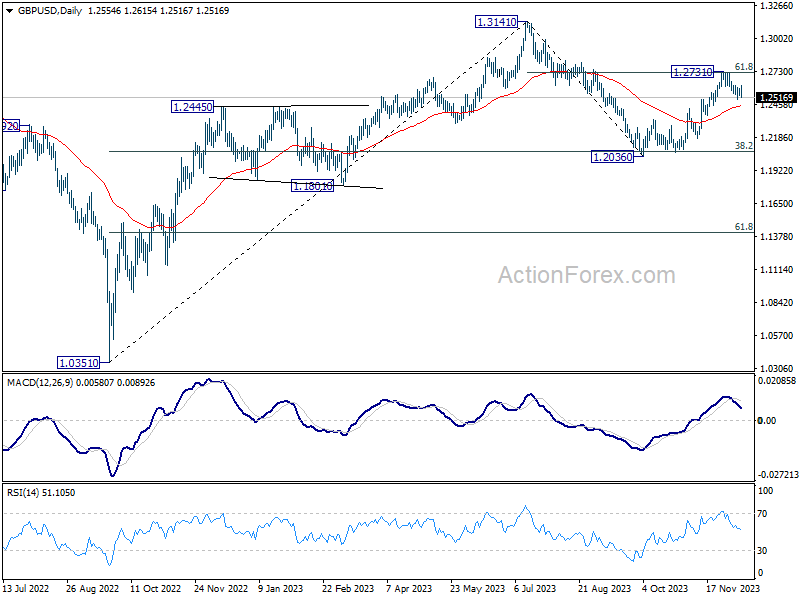

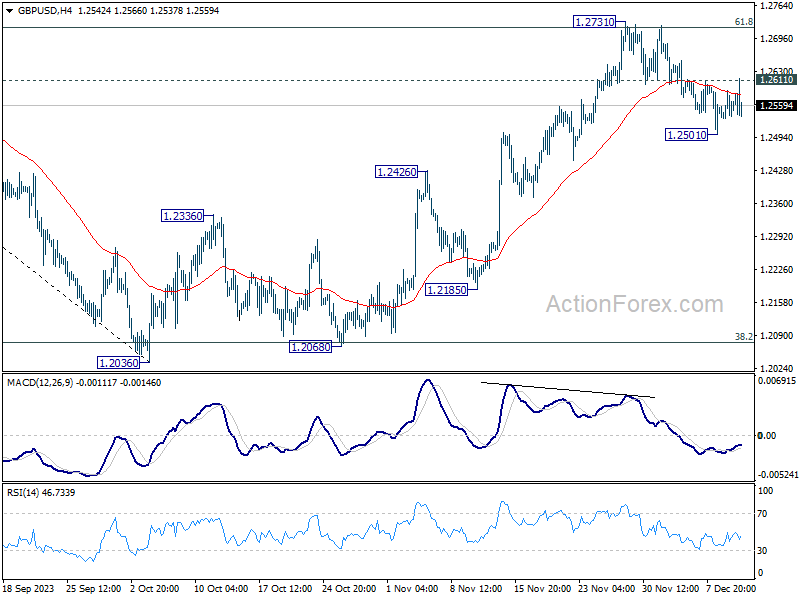

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2529; (P) 1.2560; (R1) 1.2587; More...

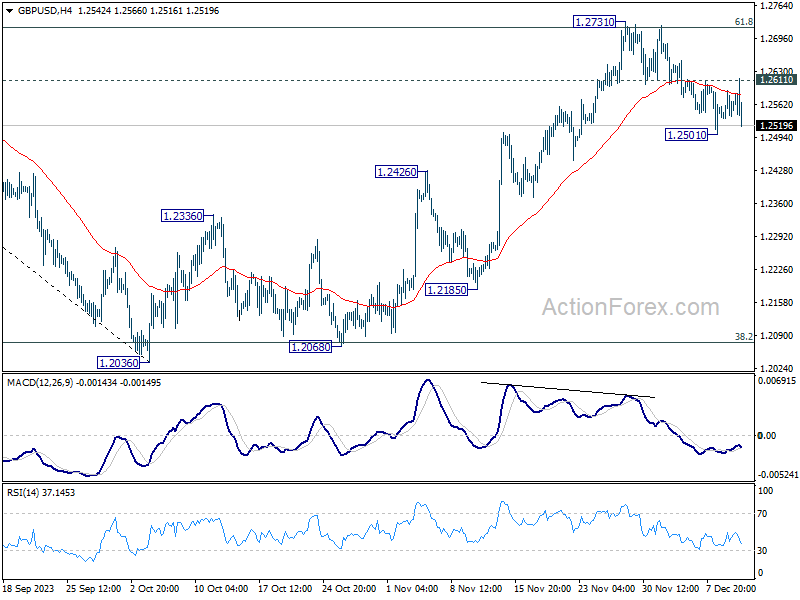

Intraday bias in GBP/USD remains neutral for the moment. Further decline remains mildly in favor with 1.2611 minor resistance intact. Below 1.2501 will resume the fall from 1.2731 short term top to to 55 D EMA (now at 1.2450). Sustained break there will bring retest of 1.2036 low. However, firm break of 1.2611 will turn bias back to the upside for retesting 1.2731 resistance.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to rise from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, that could still extend through 1.2731. But upside should be limited by 1.3141 o bring the third leg of the pattern. Meanwhile, sustained trading below 55 EMA will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again, and possibly below.

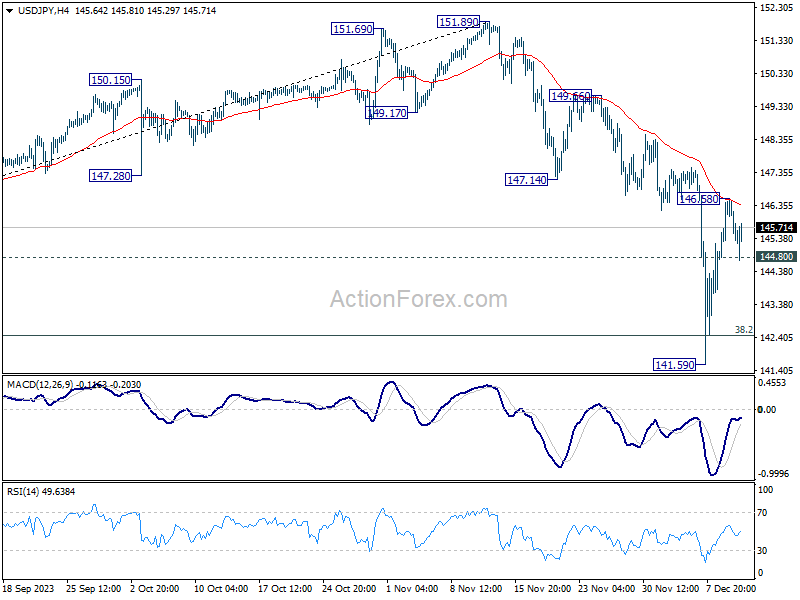

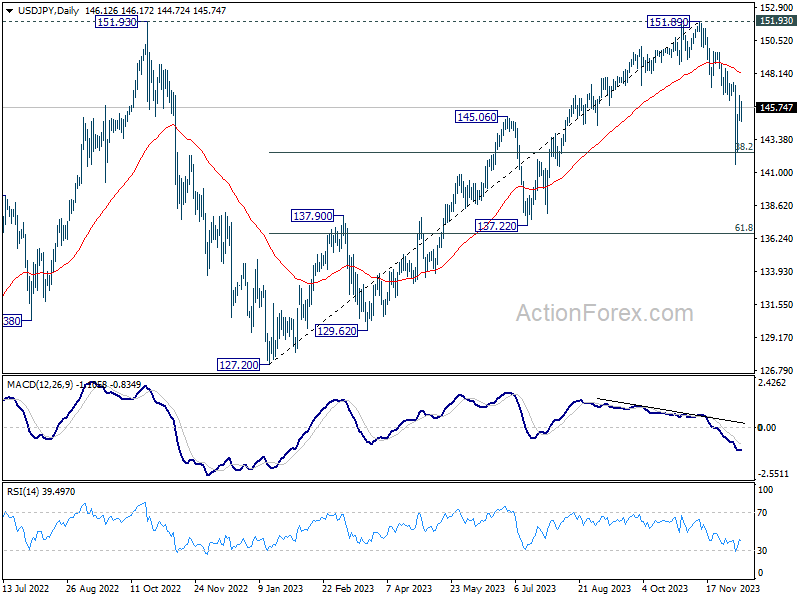

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 145.12; (P) 145.85; (R1) 146.89; More...

Intraday bias in USD/JPY stays neutral for the moment. On the downside, firm break of 144.80 minor support will suggest that rebound from 141.59 has completed at 146.58, after rejection by 55 4H EMA. Intraday bias will then be back on the downside for retesting 141.59 low. Overall outlook will stay bearish as long as 147.14 support turned resistance holds.

In the bigger picture, current fall from 151.89 is seen as the third leg of the corrective pattern from 151.93 (2022 high). Deeper decline would be seen through 38.2% retracement of 127.20 to 151.89 at 142.45 to 61.8% retracement at 136.63. This will now remain the favored as long as 147.14 support turned resistance holds.

US: Price Gains Across Still-Hot Service Sector Keep Upward Pressure on Core Inflation

The Consumer Price Index (CPI) rose 0.1% month-on-month (m/m) in November, a tick above the consensus forecast and a modest uptick from October. On a twelve-month basis, headline inflation slipped to 3.1% (from 3.2%).

- Energy prices were a key factor restraining the headline measure, falling 2.1% m/m. The pullback was entirely due to another drop in gasoline prices (-5.8% m/m). Food prices added upward pressure to inflation on a monthly basis (+0.2% m/m), but at 2.9% year-on-year (y/y), are no longer providing the same lift to headline inflation that they were last year.

Core inflation (excludes the direct effects of food & energy prices), rose 0.3% m/m, an acceleration from last month's 0.2% m/m gain, but in line with expectations. On a twelve-month basis, core inflation held steady at 4%.

Shelter costs remained a key factor keeping services costs elevated in November, rising 0.45% m/m, as rent of primary residence held steady at 0.5% m/m, while owners' equivalent rent accelerated to 0.5% m/m (from 0.4% in October).

- Non-housing services (aka the CPI measure of 'supercore') also accelerated in November, rising 0.5% m/m (from 0.2% m/m in October).

Core goods prices surprised to the downside, falling by 0.3% m/m – a sharper decline than October's 0.1% m/m pullback. Unlike months prior, where the declines have largely been concentrated in used vehicle prices, the pullback in November was spread across several categories including recreation commodities (-2.6% m/m), apparel (-1.3% m/m), household furnishings (-0.7% m/m), and new vehicle prices (-0.1% m/m).

Key Implications

Core inflation accelerated in November, as an uptick in both shelter costs and non-housing services (aka 'supercore') more than offset the pullback in goods prices. With both the three-and-six-month annualized rates of change (at 3.4% and 2.9%, respectively) on core running below the twelve-month change, we should see a further cooling in inflationary pressures in the months ahead. However, with price pressures on the service side of the economy remaining very sticky, the final descent to 2% is likely to come with some turbulence.

All eyes now shift to the Fed's interest rate announcement on Wednesday. While it's widely expected that FOMC will hold rates steady for the third consecutive meeting, Chair Powell is likely to push back on the recent pull-forward in rate cut expectations. With the next leg lower on inflation to evolve more slowly, and the labor market still tight by historical standards, the FOMC will likely need to keep the policy rate at today's restrictive levels through the first half of next year.

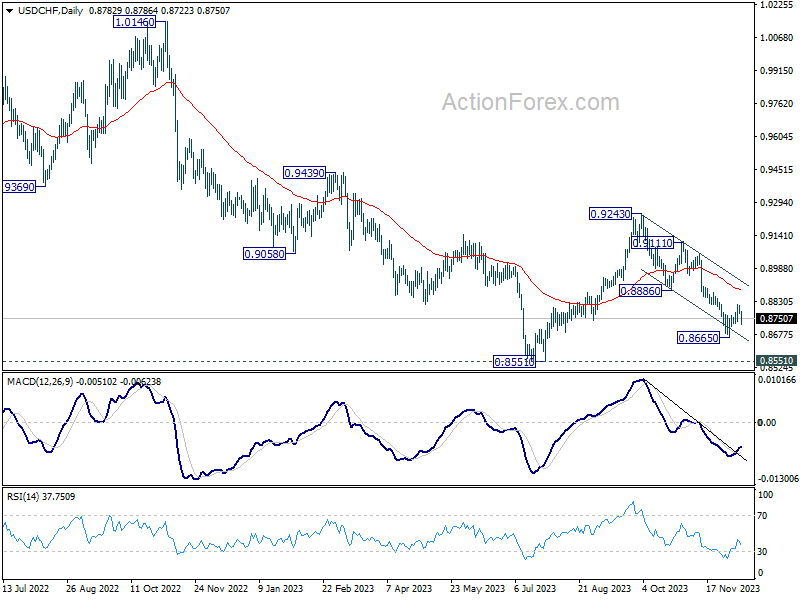

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8770; (P) 0.8793; (R1) 0.8807; More....

Intraday bias in USD/CHF stays neutral at this point. Further rise remains in favor with 0.8727 minor support intact. Above 0.8819 will resume the rebound from 0.8665 short term bottom to 0.8886 support turned resistance first. However, firm break of 0.8727 will retain near term bearishness, and turn bias back to the downside to resume the fall from 0.9243 through 0.8665.

In the bigger picture, price actions from 0.8551 are currently seen as part of a corrective pattern to the decline from 1.0146 (2022 high). Fall from 0.9243 is seen as the second leg for now. Deeper decline could be seen to 0.8551 low but strong support should be seen there to bring rebound. Meanwhile, break of 0.9111 resistance will argue that the third leg has started already, and target 0.9243 and above.

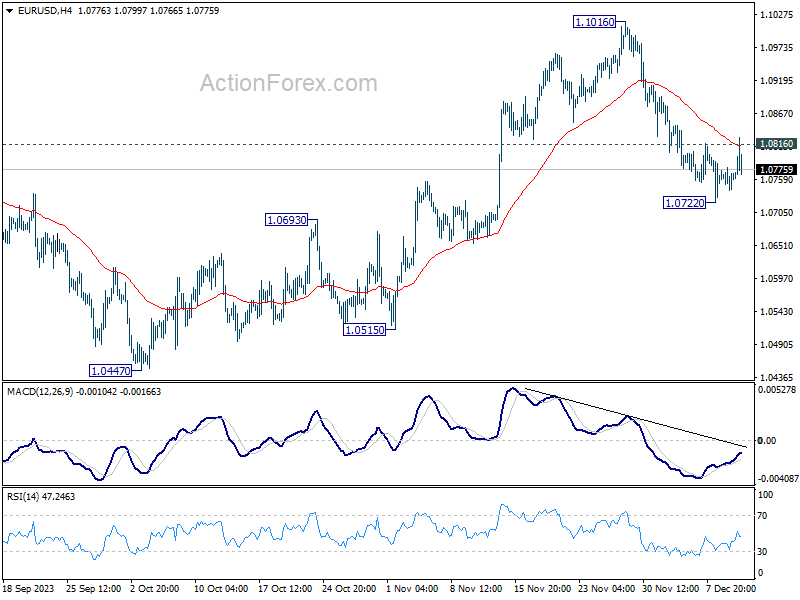

Dollar Fluctuates After US CPI, Decisive Moves Pending

In the aftermath of US CPI release, the forex markets are staying in a state of consolidation, with mixed reactions. Initially, there was an attempt to sell Dollar following the data, but this momentum quickly dissipated as the data largely aligned with market expectations. Headline CPI showed a gradual decline, albeit at a slow pace, while core CPI indicated stagnant disinflation. It may not be the right time to place significant bets on the greenback yet, especially considering FOMC rate decision and publication of new economic projections scheduled for tomorrow. The anticipation of these events has left room for potential market shifts, keeping market players cautious for now.

In terms of overall market movements, the forex markets today are somewhat mixed, indicative of a typical consolidation mode. Dollar, Australian Dollar, and Canadian Dollar are leaning towards the softer side. In contrast, Japanese Yen is showing strength, attempting a rebound from this week's pullback. Euro and Swiss Franc are also on the firmer side, while Sterling appears softer, influenced by UK job data that indicated further cooling in wage inflation.

From a technical standpoint, Dollar's rally against European majors remains a possibility, contingent on certain key levels holding in various Dollar pairs. These critical levels include 1.0816 minor resistance in EUR/USD, 1.2611 minor resistance in GBP/USD, and 0.8727 minor support in USD/CHF. Should these levels be decisively broken it could signal resurgence of broad-based Dollar weakness, or at least against Europeans.

In Europe, at the time of writing, FTSE is up 0.14%. DAX is down -0.10%. CAC is flat. Germany 10-year yield is down -0.0482 at 2.227. UK 10-year yield is down -0.099 at 3.980. Earlier in Asia, Nikkei rose 0.16%. Hong Kong HSI rose 1.07%. China Shanghai SSE rose 0.40%. Singapore Strait Times rose 0.39%. Japan 10-year JGB yield fell -0.0409 to 0.738.

US CPI ticks down to 3.1% in Nov, core CPI unchanged at 4%

The latest CPI data for US in November aligns closely with market expectations. CPI rose 0.1% mom while CPI core ex food and energy) rose 0.3% mom. Energy index down -2.3% mom, food index rose 0.2% mom.

For the 12 months period, CPI slowed from 3.2% yoy to 3.1% yoy. Core CPI was unchanged at 4.0% yoy. Energy index was down -5.4% yoy while food index was up 2.9% yoy.

German ZEW rises to 12.8 on increasing expectation of ECB rate cut

German ZEW Economic Sentiment rose slightly from 9.8 to 12.8 in December, above expectation of 8.8. Current Situation Index rose from -79.8 to -77.1, but missed expectation of -75.5.

Eurozone ZEW Economic Sentiment rose sharply from 13.8 to 23.0, well above expectation of 11.2. Current Situation Index, however, fell marginally by -0.9 pts to -62.7.

ZEW President Achim Wambach noted the slight improvement in Germany's economic outlook could be attributed to doubled expectations of interest rate cuts by ECB in the medium term. In particular, significantly more optimistic expectations are observed in the construction industry.

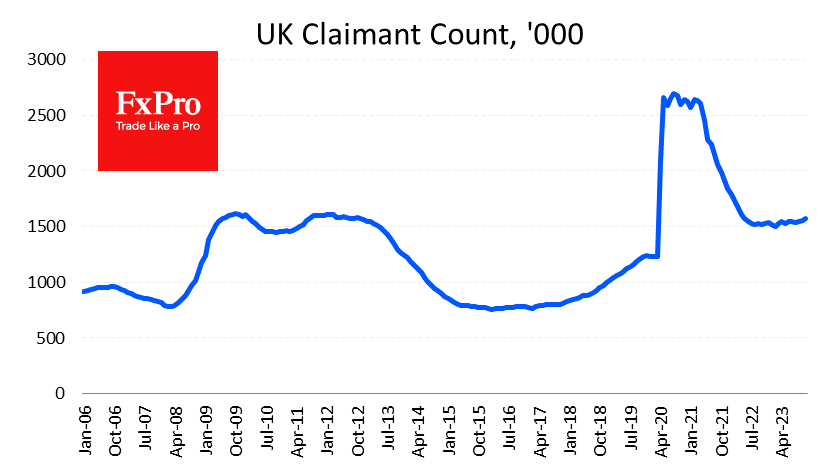

UK payrolled employment fell -13k in Nov, unemployment rate steady at 4.2% in Oct

UK payrolled employment fell slightly by -13k in November, compared with October. Comparing with November 2022, payrolled employment rose 1.1% yoy or 333k. Meanwhile monthly pay increased by 5.3% yoy, slowed from 6.2% yoy.

In the three months to October, unemployment rate was unchanged at 4.2% yoy. Average earnings (including bonus) growth slowed from 8.0% yoy to 7.2% yoy, below expectation of 7.7% yoy. Average earnings (excluding bonus) growth slowed from 7.7% yoy to 7.3% yoy, below expectation of 7.4% yoy.

Australia's Westpac consumer sentiment rose to 82.1, still far from upbeat

The latest release from Australia reveals a modest uptick in Westpac Consumer Sentiment Index, which rose by 2.7% mom to 82.1 in December. Despite this increase, Westpac's analysis describes the sentiment as "still very weak," emphasizing that "consumers remain far from upbeat."

Regarding RBA's next meeting on February 5-6, Westpac said, the "there is now a higher bar" to further tightening. It highlights the "subdued growth profile" and a "particularly weak household sector" underscored by the recent consumer sentiment results, suggesting that these factors might raise the threshold for another rate hike.

However, it's important to note the central bank's stance towards inflation. RBA has expressed a "very low tolerance for any upside surprises" in inflation rates, making the upcoming inflation data and the detailed quarterly release, due in late January, pivotal for February policy decision.

Australia's NAB business confidence and conditions decline, signaling continued soft growth

Australia NAB Business Confidence fell from -3 to -9 in November. Business Conditions fell from 13 to 9. Trading conditions fell from 19 to 13. Profitability conditions fell from 11 to 6. Employment conditions were unchanged at 8.

NAB Chief Economist Alan Oster remarked, "Both confidence and conditions declined in the month and after a period of relative stability through mid-2023 appear to be softening further." He pointed out that, excluding the pandemic period, business confidence is at its weakest since around 2012. This was a time characterized by significantly weaker conditions and slowing growth in advanced economies.

Despite these declines, Oster noted that business conditions remain above average, reflecting their strong starting point. He emphasized the importance of monitoring whether this drop in confidence continues and if a trend develops in business conditions. For the moment, these indicators suggest "ongoing soft growth in Q4".

Japan's PPI slows to weakest pace since February 2021

Japan's PPI slowed notably from 0.9% yoy to 0.3% yoy in November, but beat expectation of 0.1% yoy. That's nonetheless still the weakest pace since February 2021. November marked the 11th straight month in which the pace slowed.

Export prices was unchanged at 0.9% yoy. Import price decline slowed from -12.7% yoy to -9.7% yoy, staying negative for the eighth month.

During the month, PPI rose 0.2% mom. Import prices rose 0.7% mom. Export prices fell -0.2 %Mom.

Producer price growth stayed below the most recent consumer inflation reading for a third month. Growth in consumer prices excluding fresh food inched up to 2.9% in October.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8770; (P) 0.8793; (R1) 0.8807; More....

Intraday bias in USD/CHF stays neutral at this point. Further rise remains in favor with 0.8727 minor support intact. Above 0.8819 will resume the rebound from 0.8665 short term bottom to 0.8886 support turned resistance first. However, firm break of 0.8727 will retain near term bearishness, and turn bias back to the downside to resume the fall from 0.9243 through 0.8665.

In the bigger picture, price actions from 0.8551 are currently seen as part of a corrective pattern to the decline from 1.0146 (2022 high). Fall from 0.9243 is seen as the second leg for now. Deeper decline could be seen to 0.8551 low but strong support should be seen there to bring rebound. Meanwhile, break of 0.9111 resistance will argue that the third leg has started already, and target 0.9243 and above.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Consumer Confidence Dec | 2.70% | -2.60% | ||

| 23:50 | JPY | PPI Y/Y Nov | 0.30% | 0.10% | 0.80% | 0.90% |

| 00:30 | AUD | NAB Business Confidence Nov | -9 | -2 | -3 | |

| 00:30 | AUD | NAB Business Conditions Nov | 9 | 13 | ||

| 07:00 | GBP | Claimant Count Change Nov | 16.0K | 20.3K | 17.8K | 8.9K |

| 07:00 | GBP | ILO Unemployment Rate (3M) Oct | 4.20% | 4.20% | 4.20% | |

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Oct | 7.20% | 7.70% | 7.90% | 8.00% |

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Oct | 7.30% | 7.40% | 7.70% | |

| 10:00 | EUR | Germany ZEW Economic Sentiment Dec | 12.8 | 8.8 | 9.8 | |

| 10:00 | EUR | Germany ZEW Current Situation Dec | -77.1 | -75.5 | -79.8 | |

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Dec | 23 | 11.2 | 13.8 | |

| 11:00 | USD | NFIB Business Optimism Index Nov | 90.6 | 90.7 | 90.7 | |

| 13:30 | USD | CPI M/M Nov | 0.10% | 0.10% | 0.00% | |

| 13:30 | USD | CPI Y/Y Nov | 3.10% | 3.10% | 3.20% | |

| 13:30 | USD | CPI Core M/M Nov | 0.30% | 0.30% | 0.20% | |

| 13:30 | USD | CPI Core Y/Y Nov | 4.00% | 4.00% | 4.00% |

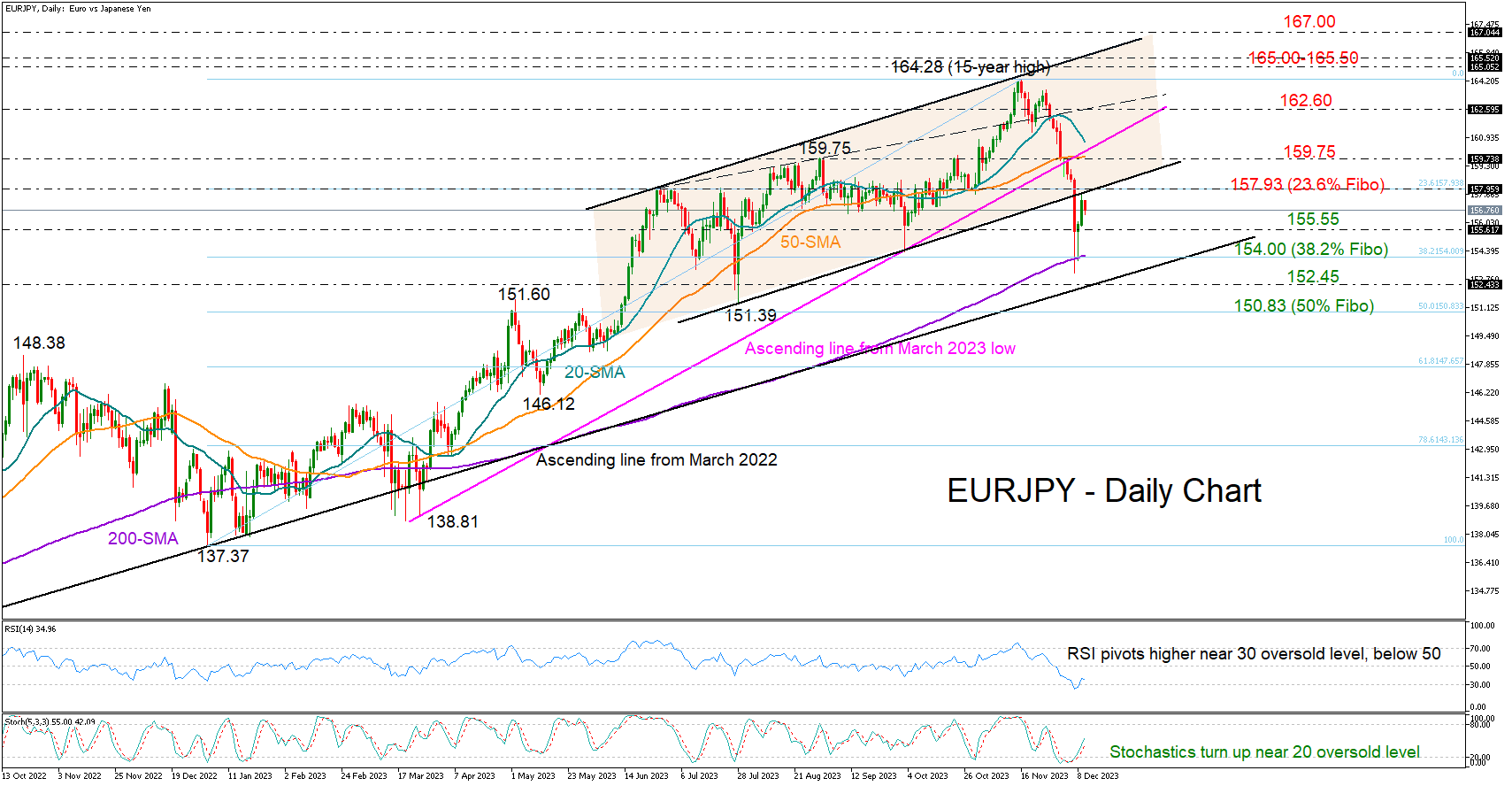

EURJPY Rotates Higher, But Trend Risks Remain

- EURJPY pauses sharp downfall near 200-day SMA

- Oversold, but trend signals remain discouraging

EURJPY turned oversold near its 200-day simple moving average (SMA) after a heavy bearish storm squeezed the pair from fifteen-year highs to a four-month low of 153.00 last week.

The latest freefall in the price has breached the June-November bullish channel, charting a new lower low in the short-term picture. Hence, traders may stay cautious, although the RSI and the stochastic oscillators have changed direction to the upside, backing the latest upturn in the price.

The pair faced difficulty in re-entering the broken upward-sloping channel on Monday at 157.93. That is where the 23.6% Fibonacci mark of the 2023 uptrend is also positioned. Therefore, a close above that bar could be important for a continuation towards the 50-day SMA at 159.75. The 20-day SMA is within breathing distance and if it proves easy to pierce through, the recovery could next take a breather around the short-term constraining line from June at 162.60 before reaching November’s highs.

Otherwise, the pair could enter a consolidation phase. The 155.55 region and the 200-day SMA, which intersects the 38.2% Fibonacci of 154.00, could keep the bears in control. If the outlook deteriorates below the ascending line from March 2022 at 152.45, selling pressures could drive the pair towards the 50% Fibonacci of 150.83.

All in all, the latest sell-off in EURJPY raised concerns about a bearish trend reversal. Downside risks could ease if the price manages to bounce back above 157.93.

US CPI ticks down to 3.1% in Nov, core CPI unchanged at 4%

The latest CPI data for US in November aligns closely with market expectations. CPI rose 0.1% mom while CPI core ex food and energy) rose 0.3% mom. Energy index down -2.3% mom, food index rose 0.2% mom.

For the 12 months period, CPI slowed from 3.2% yoy to 3.1% yoy. Core CPI was unchanged at 4.0% yoy. Energy index was down -5.4% yoy while food index was up 2.9% yoy.

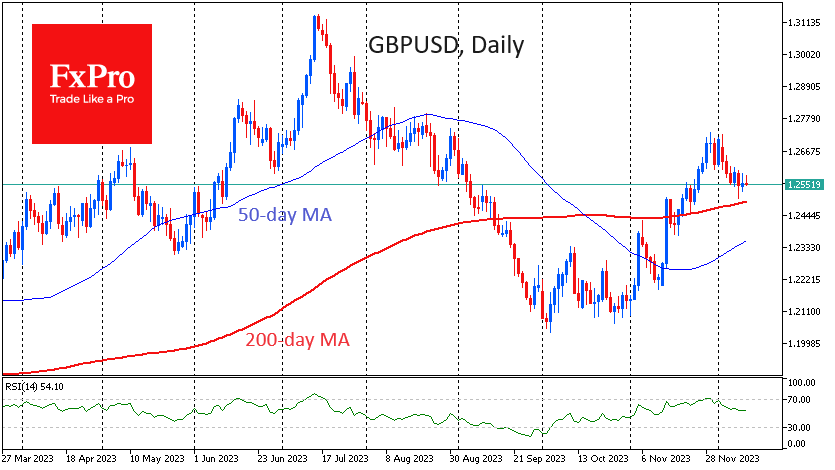

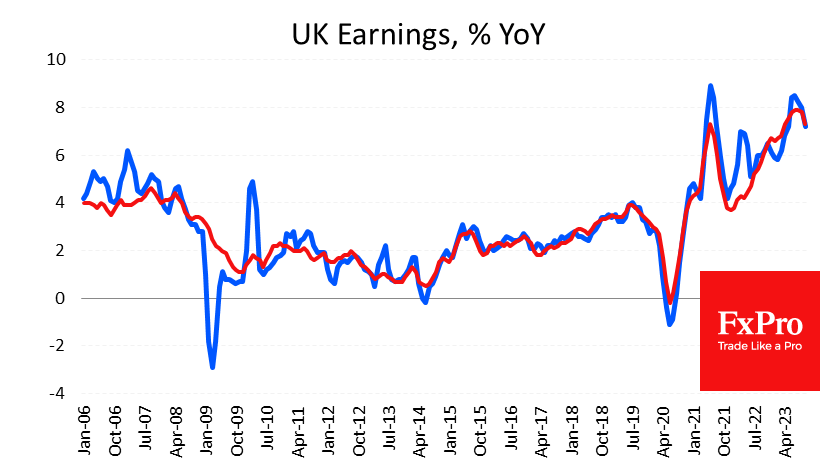

Is UK Labour Market Cool Enough for BoE?

The UK labour market is cooling, showing an increase in claims from claimants. In addition, wage growth is slowing. The data provided further evidence that the UK economy has moved into a new phase of the economic cycle, although the inflation genie remains at large.

In November, the number of people receiving benefits rose by 16K to 1575K – the highest since April 2022. The UK labour market is cutting jobs more actively, a reversal after a plateau between September last year and February this year.

Meanwhile, wages continue to contribute to inflation, adding 7.2% in the August-October period to the same period a year earlier. The rate of wage growth is down 1.3 percentage points from a peak of 8.5% four months ago, although it remains notably above the consumer inflation rate of 4.6% y/y.

On the one hand, the Bank of England has seen slowing inflation and there are growing signs of a cooling labour market, supporting the sentiment that it will reach a plateau and that the next move after a prolonged pause will be lower.

On the other hand, both price and wage growth rates have been held at elevated levels for an extended period (3 years for wages and over two years for inflation), working to raise inflation expectations and making returning to the norm more difficult.

And this divergence creates intrigue ahead of the Bank of England’s looming meeting on Thursday. If the Bank of England acts based on hard data, it should remain in inflation-suppressing mode, warning it is ready to raise rates to bring inflation back on target more quickly.

However, major peers – the ECB and the Fed – are signalling that they are done with hikes and have moved into a ‘wait-and-see’ mode, and the Bank of England may announce the same shift in two days.

The GBP/USD pair retreated towards 1.25 at the end of last week, approaching its 200-day average from above. This week, the battle for the long-term trend has every chance of intensifying, and a bull or bear victory could signal a lasting signal of further Pound movement. A consolidation under 1.25 opens a quick path to 1.22 or even 1.2060. The ability to hold above due to a strong economy or a hawkish stance from the Central Bank will kick-start a growth momentum with a quick update to 1.27 and the potential to rise above 1.30 before the end of Q1.