Sample Category Title

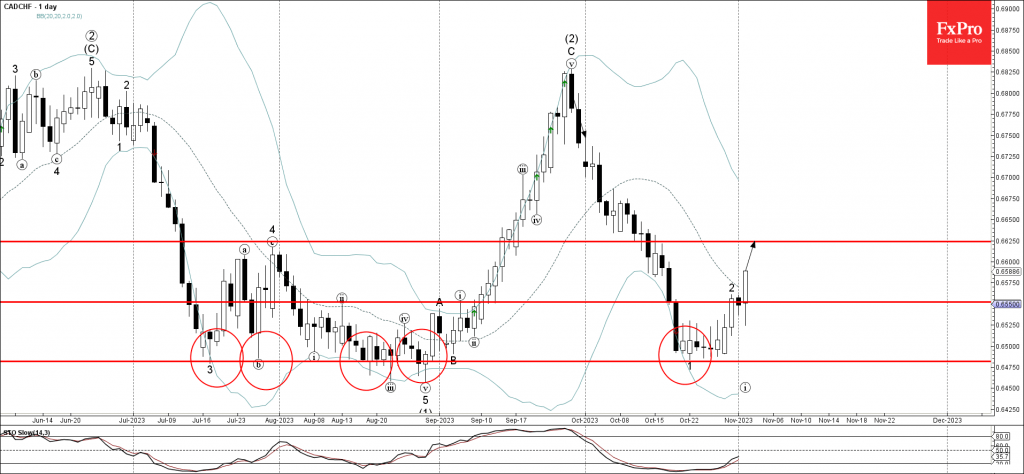

CADCHF Wave Analysis

- CADCHF broke resistance level 0.6550

- Likely to rise to resistance level 0,6625

CADCHF recently broke through the resistance level 0.6550 (which stopped the pervious minor correction 2 at the end of October, as can be seen below).

The breakout of the resistance level 0.6550 accelerated the active short-term correction 2 from the end of last month.

Given the strong Swiss franc sales and the proximity of the powerful support level 0.6480, CADCHF can be expected to rise further toward the next resistance level 0.6625.

Sunset Market Commentary

Markets

Unchanged. The Bank of England followed the European and US example and kept rates steady at 5.25%. The vote was not unanimous though, with 3 of the 9 members in favour of lifting rates 25 bps. At the heart of the decision lies a weak economy. GDP is projected to be flat in Q3 this year and to grow a negligible 0.1% in the running quarter. Both are softer than expected back in August. The BoE then expects zero growth for 2024 (with a 50% chance of a recession from Q2 on) and just 0.25% in 2025. The economy is seen in excess supply from 2024 through the end of the policy horizon (2026). Employment growth probably softened over the second half of this year and to a greater extent than thought in the summer. Based on market expectations for the policy rate to remain at the current level until Q3 2024 and then declining to 4.25% by end 2026, inflation (6.7% in September) should hit the 2% target by mid-2025 before dropping below as an increasing degree of economic slack reduces domestic inflationary pressures. Risks to the outlook remain skewed to the upside. The BoE retains the possibility of hiking further “if there were evidence of more persistent inflationary pressures”. Between the lines, however, we read a preference for keeping rates at the current level for longer over raising them once more. UK gilts hugely outperform global peers today, losing between 10.3 and 15.4 bps with money markets now convinced more than ever that tightening is over. While the BoE did have some impact, much of the losses already occurred before that in a catch-up move the US late yesterday. Sterling losses are contained. EUR/GBP bounces higher to 0.873.

Core bond yields extend yesterday’s decline. US rates ease another 0.1 (2-y)-11.4 (30-y) bps. An unexpected drop in Q3 unit labor costs (-0.8% q/q, the first decline since late 2022) amid a surge in productivity added to the move. Weekly jobless claims (217k) later topped the 210k estimate. German yields drop 2.4-8.1 bps with the long end outperforming. The 10-y yield touching 2.68% intraday effectively created the neckline of a double top technical pattern. For a second day straight, markets frontrunning the end of the tightening cycle in the advanced economies pushes equities comfortably higher. The EuroStoxx adds 1.9%, Wall Street opens about 1%+ higher. Risk on is hurting the USD. EUR/USD is testing resistance around 1.0635. DXY drops towards the 106 barrier. Even JPY is able to strengthen. USD/JPY 150 survives though.

News & Views

The Norwegian central bank unanimously decided to keep its policy rate unchanged at 4.25%. Based on the monetary policy committee’s assessment of the outlook, the policy rate will likely be raised in December even as inflation has fallen more than expected and economic activity has been somewhat lower than projected in the September Monetary Policy Report. The weaker currency poses upward inflation risks while underlying inflation needs to drop faster for the Norges Bank to hold its fire in December. If they hike, it will likely be the last move as the Committee assesses the policy rate close to the level needed to tackle inflation and with monetary policy having a tightening effect on the economy. There will likely be a need to maintain a tight stance for some time ahead to bring inflation down to the target, governor Wolden Bache admitted. NOK swap rates drop more than global peers today, losing 13 to 15 bps across the curve. The Norwegian krone suffers from the loss of rate support with EUR/NOK changing hands at 11.87, the highest level since June and compared to a YTD high of 12.11.

Swiss headline inflation rose by 0.1% M/M in October, with the Y/Y-figure stabilizing at 1.7%. Both were expected. Underlying core inflation however beat consensus rising by 0.2% M/M and 1.5% Y/Y (from 1.3% in September vs 1.4% forecast). The pick-up in core inflation was the first since February. Core CPI in between slowed from a 2.4% Y/Y-peak to a 1.3% low. The SNB meets only on a quarterly basis and kept its policy rate unchanged at 1.75% in September. More recently, SNB governor Jordan stressed that the central bank won’t hesitate to hike again if the outlook changes. Swiss money markets don’t believe that this will happen, discounting a 25 bps rate cut by March 2024 as the next move. The Swiss franc loses out against a strong euro today with EUR/CHF testing the recent highs around 0.9630.

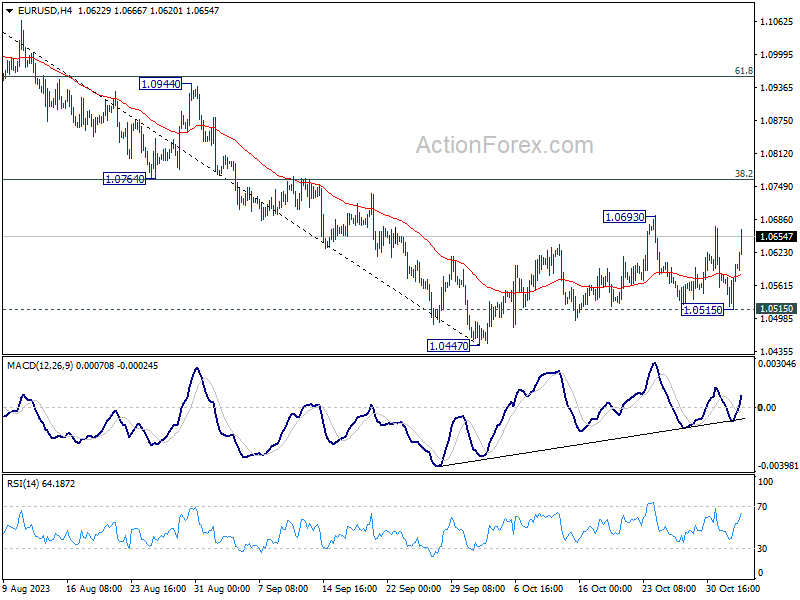

EUR/USD: Euro Regained Traction on Weaker Dollar, NFP Data Eyed for Fresh Signals

EURUSD bounced on Thursday after two-day drop was strongly rejected on signals that the US Federal Reserve kept policy unchanged and signaled that the job with rate hikes is likely done, which deflated the US dollar.

Additional pressure on greenback came from higher than expected weekly jobless claims and significant drop in unit labor cost in Q3 which indicated some weakness in labor market, though clearer picture will be seen after release of October’s NFP report on Friday.

Fresh strength probed again above pivotal Fibo barrier at 1.0638 (38.2% of 1.0945/1.0448) and cracked the base of falling daily cloud (1.0664), but faced increased headwinds, as cloud is thick and weighs heavily.

Clear break above 1.0638 and penetration of daily cloud is required to confirm initial bullish signal for attack at psychological 1.0700 barrier and avoid another bull-trap above 1.0638.

Positive momentum continues to strengthen on daily chart and MA’s (10/20/30) turned to bullish setup and underpin near-term action, which needs to hold above 1.06 zone (daily Tenkan-sen) to keep bias with bulls.

Res: 1.0664; 1.0700; 1.0736; 1.0755.

Sup: 1.0605; 1.0570; 1.0516; 1.0495.

BoE in Wait and See Mode With Wage Growth Key to Interest Rate Outlook

The Bank of England left interest rates unchanged today at 5.25%, as expected, with the vote widening slightly but remaining very close.

The fact that the vote remains close highlights how uncertain the outlook remains in the view of the MPC and how, as Bailey reaffirmed in the press conference after, the risks to inflation are still to the upside.

That said, based on its forecasts, which show inflation falling below 2% over the forecast period, a rate cut is seemingly the more likely next move. Of course, these forecasts are always subject to change and often are, especially in such a challenging and uncertain environment.

Still, it looks clear at this point that the BoE is, like many of its peers, done with the tightening cycle and it's now a case of how long it remains at the peak. Of course, that's also extremely important at a time when rates are restrictive, and potentially significantly so.

The BoE is persisting with the language of "sufficiently restrictive for sufficiently long" which isn't as helpful as they may think. But it does come across softer than some of its peers which may again suggest it's not as confident that rates will stay at the peak as long as others. Or perhaps I'm just reading too much into these statements like everyone else.

A final point that was very evident in the press conference is how taken aback the MPC has been by wage growth and what that means for inflation and interest rates. Measures of wage growth may therefore become the key data release going forward as other areas of the economy cool but this remains stubbornly high. Lower wage growth may well be what tips the balance of the forecasts in favour of earlier rate cuts.

The pound has been quite choppy across the initial announcement and new projections, and then throughout the press conference but nothing has significantly changed which suggests today has largely unfolded as expected. There remains considerable uncertainty and the data over the coming months could clear things up. Until then, the BoE, like its peers is in wait-and-see mode.

Franc May Continue to Strengthen amid Low Inflation

Today it became known about the level of inflation in Switzerland. Compared to the US, UK, and other countries, Switzerland can boast of a CPI of only 0.1%. The minimal increase in prices is due to an increase in fuel costs due to the rise in oil prices in the second half of the year. Thus, the country’s economy provides more arguments in favor of the protected harbor status.

On October 5, we wrote that the Swiss franc was near an important resistance, forming an AB double top. After this, the rate fell by 2.5% to form the October low, and now the chart provides a new piece of information for analysis, in particular about the 0.909 level, which acts as an important resistance.

The USD/CHF price has interacted with it before (as shown by the arrows), but note:

→ the level was able to stop the sharp increase on October 31;

→ did not allow the price to reach the upper boundary of the ascending channel (shown in blue);

→ the price only briefly stayed higher. The bulls were unable to gain a foothold above 0.909, and the rate fell to the lower border of the channel.

On November 2-3, rebounds form from the lower border of the channel, which looks like a logical development of the situation, but the progress of the rebounds has not approached 50% of the decline from the November highs, so this can hardly be considered a successful resumption of the bullish trend. But the bears seem determined to firmly seize the initiative, given the strength and confidence of the Swiss economy and the CHF's ability to be protected from inflation.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Bitcoin Updates Its Maximum for the Year

The cryptocurrency market showed a correlation with the stock market, gaining bullish momentum amid softening rhetoric from the Federal Reserve.

The price of the main cryptocurrency reached USD 35,900 for the first time in 18 months.

Wherein:

→ the positivity is also due to expectations that the US Securities and Exchange Commission will approve a Bitcoin ETF. According to analysts at Bernstein (an asset management firm), this could happen by the first quarter of 2024.

→ according to the same analysts, the price of Bitcoin could reach USD 150k by 2025;

→ Jurrien Timmer, director of global macroeconomics at Fidelity, called bitcoin a commodity currency or exponential gold that aims to be a store of value and a hedge against monetary depreciation.

Are the bullish sentiments that strong?

The chart provides information to help maintain an unbiased view of the market:

→ the price of BTC/USD is slightly above the upper border of the ascending channel. And this is a sign of overbought;

→ the price dynamics of BTC/USD forms a divergence with the RSI indicator, which is also in the overbought zone — which ultimately indicates the market’s vulnerability to a rollback;

→ the price is above the psychological level of 35,000 – and an analysis of the past behavior of the bitcoin price relative to round levels shows that false punctures are a common practice;

→ BTC/USD price has moved out of the consolidation zone (shown by the green triangle), but a breakout of the consolidation zone could be followed by a ton of buyers — and it is possible that they will find themselves locked in losses if a pullback does occur. A price return to the green triangle area will motivate them to close positions, thereby exerting even more selling pressure.

While ETF approval seems imminent and could attract significant capital to the bitcoin market over the long term, technically, the BTC/USD price could pull back from overbought territory.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

British Pound Gets Lift from Fed and BoE Pauses

- British pound posts sharp gains

- BoE and Fed pause for second straight time

The British pound has posted strong gains on Thursday. In the European session, GBP/USD is trading at 1.2216, up 0.54%.

Bank of England pauses

The Bank of England voted to maintain interest rates at 5.25% at today’s meeting. The pauses follow 14 straight rate increases in the current tightening cycle which began in December 2021. The move indicates that the MPC is sticking to the “Table Mountain” approach, which is essentially a “higher for longer” stance that keeps rates at elevated levels until the BoE is confident that inflation will fall back to the 2% target.

The MPC vote was 6-3, with the majority favoring a pause and three members voting to hike rates by a quarter-point. At the September meeting, the vote to pause was 5-4. The division within the MPC indicates that members remain divided over policy, which will make it difficult for Governor Bailey to present a clear path moving forward.

The BoE revised inflation projections slightly higher and the statement noted that the BoE stood ready to raise rates if it sees “more persistent inflationary pressures”. The markets are hoping that the back-to-back pauses mark the end of the current rate-tightening cycle, but rate cuts aren’t expected until late in 2024. Governor Bailey said after the meeting that higher interest rates had pushed inflation lower but it was “much too early to be thinking about rate cuts.”

US dollar dips after Fed pause

The Federal Reserve held rates for a second straight time on Wednesday. The Fed reiterated that rate hikes remained on the table, but acknowledged that “tighter financial and credit conditions” were weighing on inflation. This was likely a reference to the recent rise in US Treasuries, which has increased borrowing costs and could push inflation lower without the Fed having to raise rates.

If Powell was trying to sound hawkish, the markets weren’t buying it. Future markets have priced in another pause in December and expectations are that the Fed is done with hiking, despite Powell’s assertion to the contrary. The US dollar is down against all of the majors and US stock markets were strongly higher on Wednesday.

GBP/USD Technical

- GBP/USD is testing resistance at 1.2175. Above, there is resistance at 1.2251

- There is support at 1.2068 and 1.2032

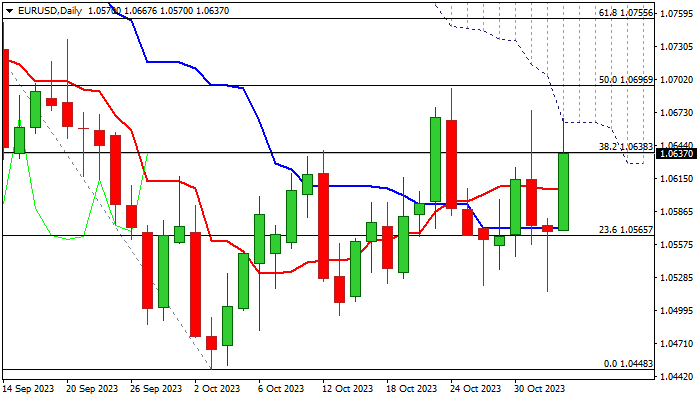

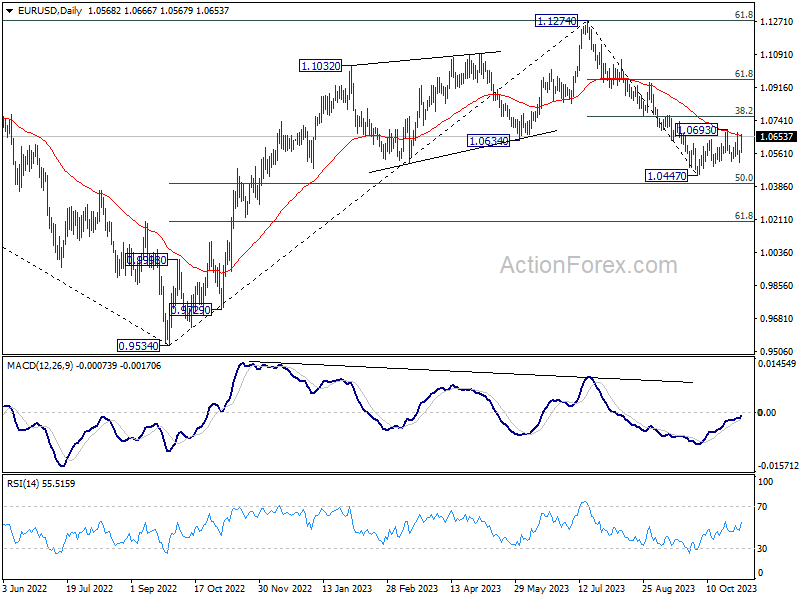

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0531; (P) 1.0556; (R1) 1.0595; More...

EUR/USD is still capped below 1.0693 resistance despite current rebound. Intraday bias stays neutral first. On the upside, break of 1.0693 will extend the rebound from 1.0447 to 1.0764 cluster resistance (38.2% retracement of 1.1274 to 1.0447 at 1.0763). However, break of 1.0515 will indicate that larger fall from 1.1274 is ready to resume through 1.0447 to 1.0199 fibonacci level.

In the bigger picture, fall from 1.1274 medium term top could be viewed part of a correction to rise from 0.9534 (2022 low). An interim bounce from current level, as the second leg of the pattern, cannot be ruled out. But upside should be limited well below 1.1274 resistance to start the third level. The pattern would likely at least have a take on 61.8% retracement of 0.9534 to 1.1274 at 1.0199 before completion.

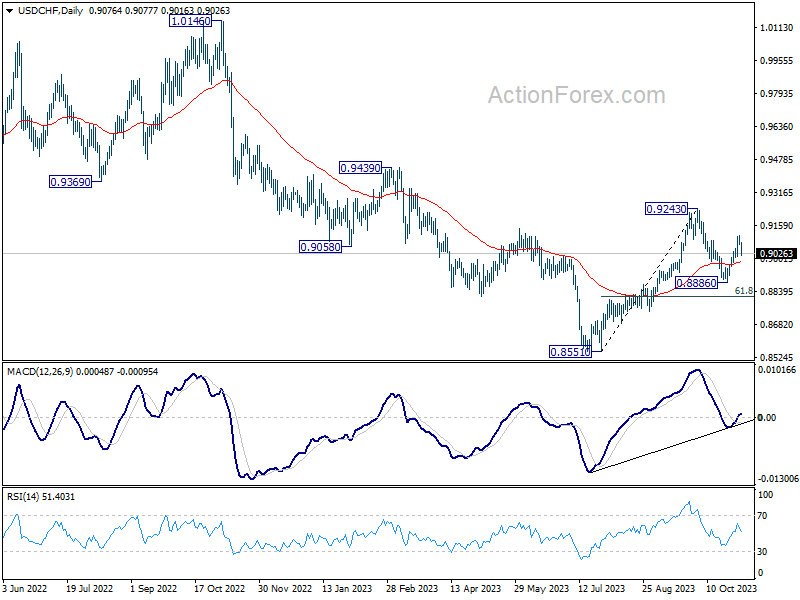

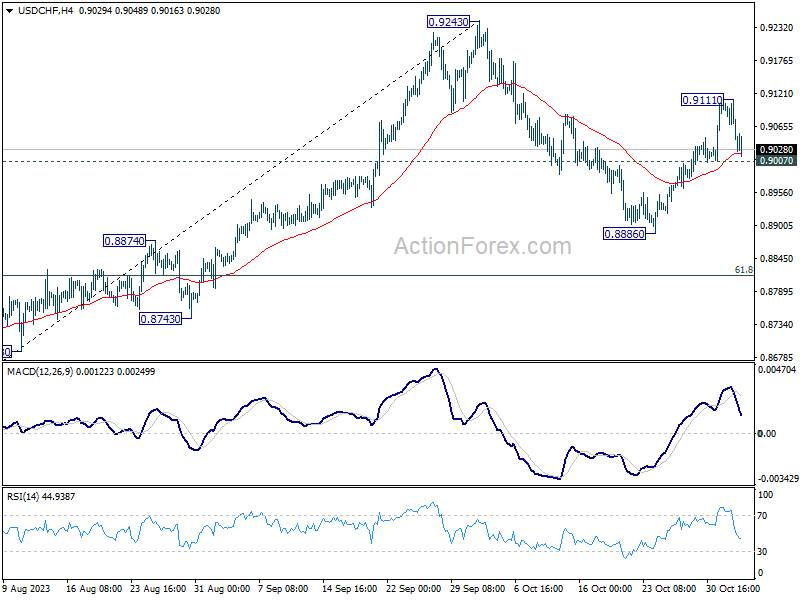

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9062; (P) 0.9087; (R1) 0.9105; More....

Intraday bias in USD/CHF stays neutral first, and further rise remains mildly in favor as long as 0.9007 support holds. Above 0.9111 will resume the rebound from 0.8886 to retest 0.9243 resistance next. However, firm break of 0.9007 will turn bias to the downside for 0.8886 support instead.

In the bigger picture, outlook is mixed up by the deeper than expected pull back from 0.9243. Yet there was no follow through selling after hitting 0.8886. On the upside, break of 0.9243 resistance will revive the case of medium term bottoming at 0.8851, and turn outlook bullish. However, sustained break of 61.8% retracement of 0.8551 to 0.9243 at 0.8815 will argue that larger decline from 1.0146 is ready to resume through 0.8551 low.