Sample Category Title

USD/JPY Mid-Day Outlook

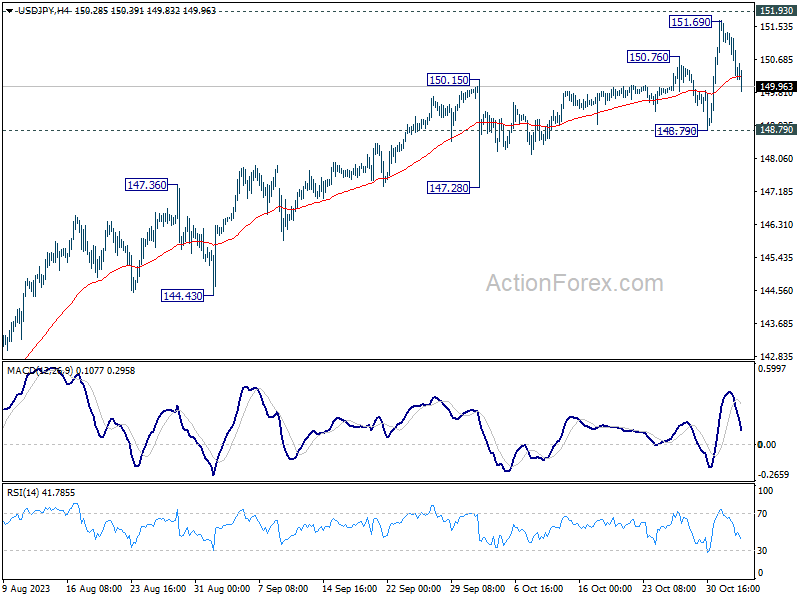

Daily Pivots: (S1) 150.50; (P) 151.10; (R1) 151.54; More...

While USD/JPY's retreat from 151.69 is steep, it's still holding above 148.79 support. Intraday bias remains neutral and some more range trading could be seen. Further rally is mildly in favor as long as 148.79 support holds. Decisive break of 151.93 will target 100% projection of 129.62 to 145.06 from 137.22 at 152.66. However, firm break of 148.79 will indicate rejection by 151.93, and bring deeper fall through 147.28 support.

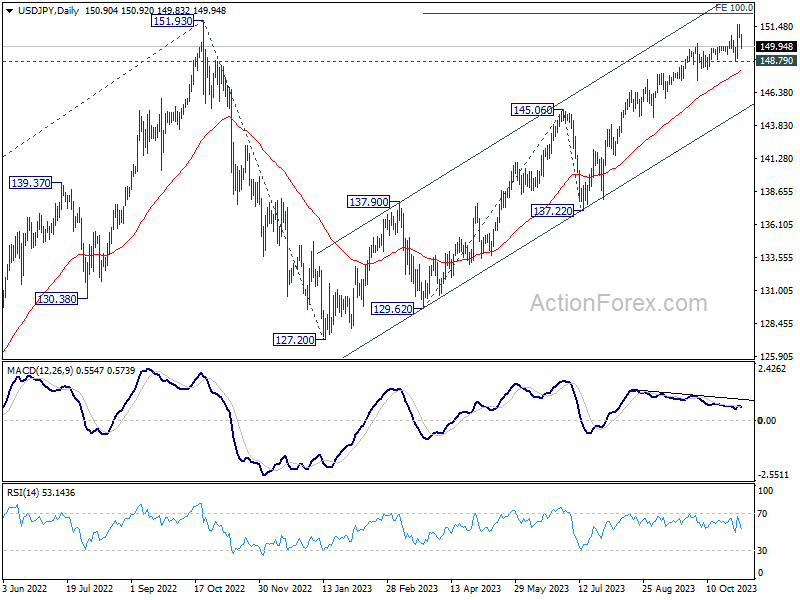

In the bigger picture, immediate focus is now on 151.93 resistance (2022 high). Rejection by 151.93, followed by sustained break of 145.06 resistance turned support will argue that rise from 127.20 has completed, and turn outlook bearish for 137.22 support and below. However, sustained break of 151.93 will confirm resumption of long term up trend. Next target will be 61.8% projection of 102.58 to 151.93 from 127.20 at 157.69.

GBP/USD Mid-Day Outlook

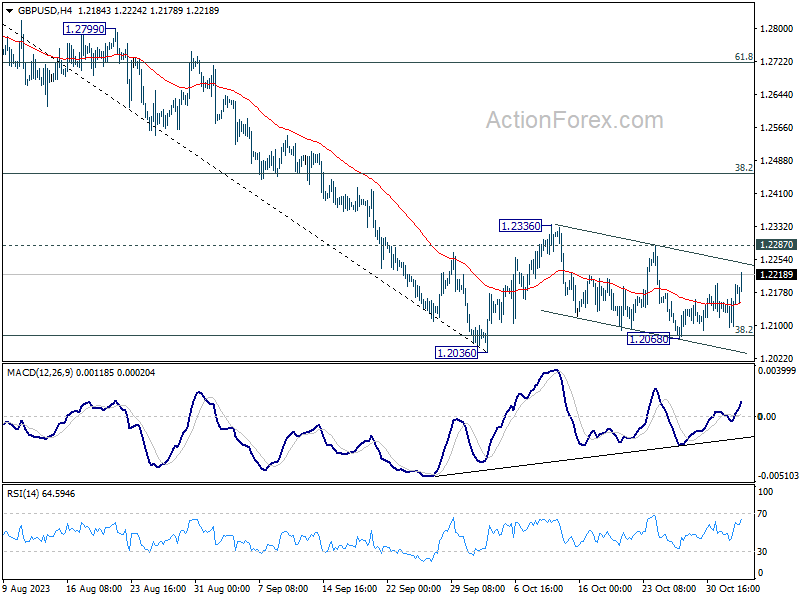

Daily Pivots: (S1) 1.2110; (P) 1.2137; (R1) 1.2179; More

GBP/USD is still bounded in established range despite today's rebound, and intraday bias stays neutral. On the upside, firm break of 1.2287 resistance will argue that rise from 1.2036 is resuming. Intraday bias will be turned back to the upside for 38.2% retracement of 1.3141 to 1.2036 at 1.2458. On the downside, decisive break of 1.2036 will resume whole decline from 1.3141 for 1.1801 support next.

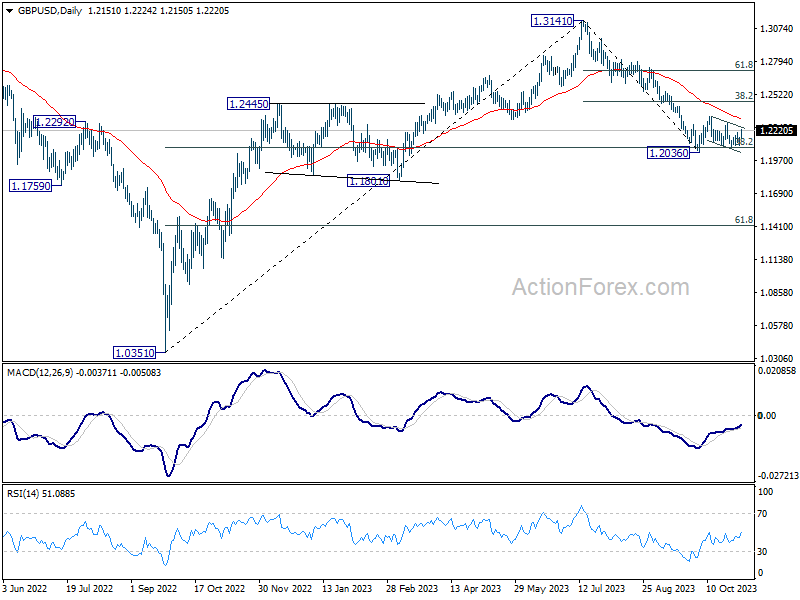

In the bigger picture, fall from 1.3141 medium term top could still be a correction to up trend from 1.0351 (2022 low) only. But risk of complete trend reversal is rising. Sustained break of 38.2% retracement of 1.0351 to 1.3141 at 1.2075 will pave the way to 61.8% retracement at 1.1417. For now, risk will stay on the downside as long as 55 D EMA (now at 1.2315) holds, in case of rebound.

Sterling Shows Mixed Response to BoE; Dollar Faces Mounting Pressure

In the wake of BoE's decision to maintain interest rates unchanged, Sterling exhibited a mixed performance, gaining against Dollar yet faltering when paired with the Euro and commodity-linked currencies. The voting pattern at the BoE leaned slightly more hawkish than anticipated, but the newly projected rate path suggests the peak in interest rates was reached already. The Dollar, on the other hand, is losing ground, exacerbated by a further dip in 10-year yield, now below 4.7% mark. This development is mirrored in US stock futures, which are signaling positive opening.

Currently, Dollar is the third weakest performer of the week, managing only marginal gains over Yen and the Swiss Franc. However, its position remains precarious. In contrast, Australian Dollar leads the pack as the week's strongest, followed by New Zealand Dollar and Euro. Canadian Dollar shows a mixed performance, while Sterling struggles to keep pace with its peers.

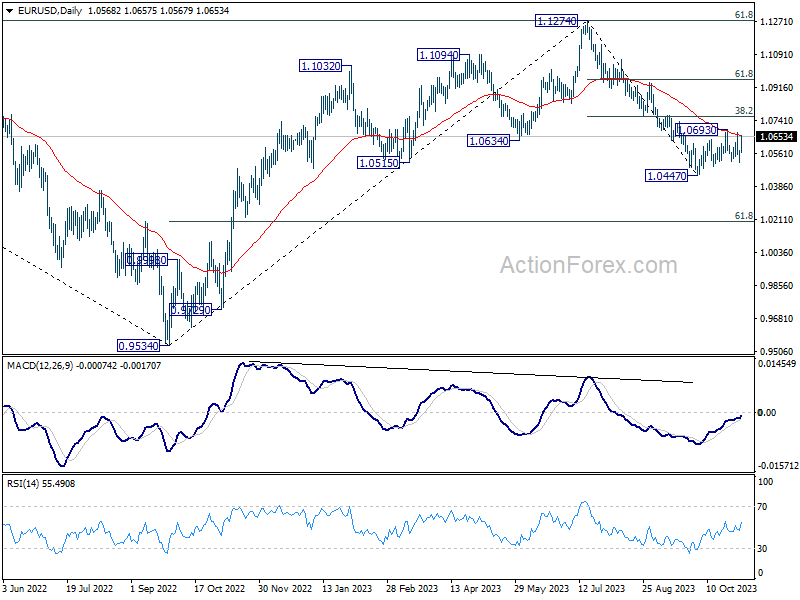

Technically, EUR/USD is back pressing 55 D EMA with today's strong bounce. Strong break of this EMA and 1.0693 resistance will carry bullish implication. Further rise should at least be seen to 1.0764 cluster resistance (38.2% retracement of 1.1274 to 1.0447 at 1.0763). However, rejection by 55 D EMA will keep near term outlook bearish for another fall through 1.0447, soon.

In Europe, at the time of writing, FTSE is up 1.24%. DAX is up 1.60%. CAC is up 1.94%. Germany 10-year yield is down -0.085 at 2.680. Earlier in Asia, Nikkei rose 1.10%. Hong Kong HSI rose 0.75%. China Shanghai SSE dropped -0.45%. Singapore Strait Times rose 0.19%. Japan 10-year JGB yield dropped -0.0433 to 0.916.

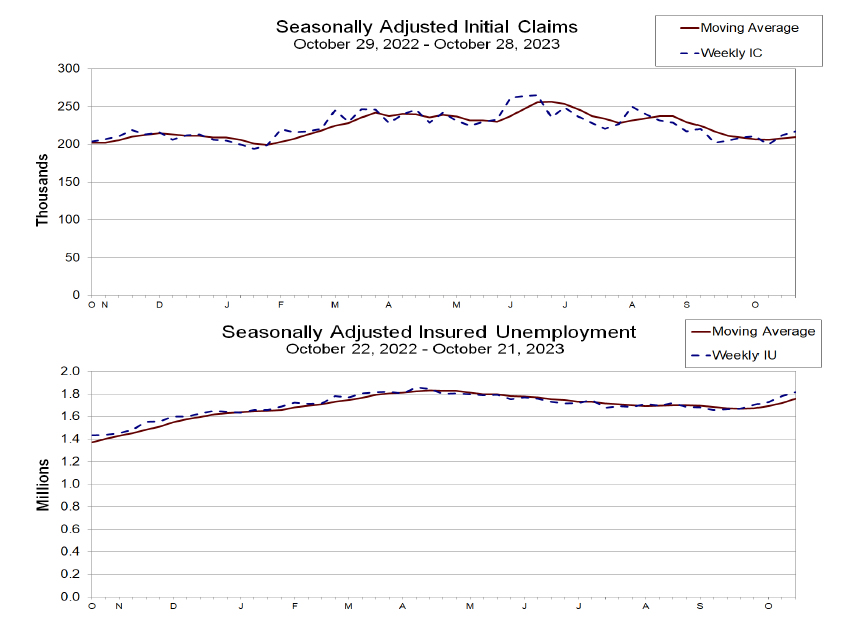

US initial jobless claims rose to 217k, above exp 210k

US initial jobless claims rose 5k to 217k in the week ending October 28, above expectation of 210k. Four-week moving average of initial claims rose 2k to 210k.

Continuing claims rose 35k to 1818k in the week ending October 21. Four-week moving average of continuing claims rose 37k to 1758k.

BoE stands pat, adopts lower rate path for economic forecasts

BoE held its Bank Rate steady at 5.25%, aligning with broad market anticipations. The decision came with a 6-3 split, with Megan Greene, Jonathan Haskel, and Catherine Mann opting for a 25 basis points increase. The bank emphasized the necessity of maintaining a restrictive monetary stance for an extended period to steer inflation back to its target. They also signaled that should more enduring inflation signs surface, the option for further rate hikes is still on the table.

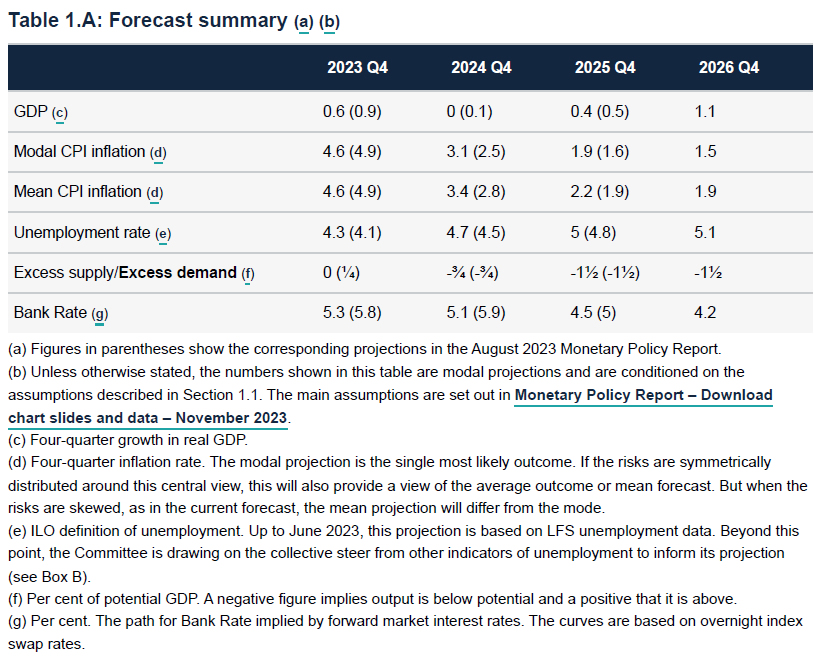

Four-quarter GDP growth:

- Lowered from 0.9% to 0.6% in Q4 2023.

- Lowered from 0.1% to 0.0% in Q4 2024.

- Lowered from 0.5% to 0.4% in Q4 2025.

- At 1.1% in Q4 2026 (new).

Modal CPI inflation:

- Lowered from 4.9% to 4.6% in Q4 2023.

- Raised from 2.5% to 3.1% in Q4 2024.

- Raised from 1.6% to 1.9% in Q4 2025.

- Slow to 1.5% in Q4 2026. (new).

These projections are based on a market-implied path for the Bank Rate that hovers around 5.25% until Q3 2024, and then gradually decreases to 4.25% by the end of 2026.

This represents a lower trajectory compared to the projections in August, which anticipated a Bank Rate of 5.8% by the end of 2023, 5.9% by the end of 2024, and 5% by the end of 2025.

Eurozone PMI manufacturing finalized at 43.1, woes deepen

Eurozone's PMI Manufacturing reading for October was finalized at 43.1, a slight decline from September's 43.4.

A closer look at individual countries, notably, Germany, Europe's largest economy, posted a five-month high, though it still lurks in the downturn territory with a reading of 40.8. France hits a 41-month low at 42.8.

Amidst the broader decline, Greece displayed resilience with a two-month high of 50.8. In contrast, countries such as Ireland, Spain, and Italy presented figures pointing towards continued economic pressure with readings of 48.2, 45.1, and 44.9, respectively.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, likened the ongoing trend in Eurozone manufacturing to a "bumpy sleigh ride." While the slight stability in recent PMI figures might hint at approaching the low point of this downturn, the critical indicators like the new orders index remain in the red.

The stagnation of these vital indices, as history suggests, could potentially set the stage for a recovery. However, de la Rubia anticipates this turnaround to materialize in the first half of the upcoming year.

Furthermore, he pointed out the synchronized decline among the eurozone nations. With key players like France, Italy, Spain, and Germany showcasing dipping PMIs, it's evident that a sectoral contraction might be imminent for these nations in the current quarter.

Swiss CPI unchanged at 1.7% yoy in Oct, core CPI rises to 1.5% yoy

Swiss CPI rose 0.1% mom in October, matched expectations. Core CPI (excluding fresh and seasonal products, energy and fuel) rose 0.1% mom. Domestic products prices was flat at 0.0% mom. Imported products prices rose 0.3% mom.

Annually CPI was unchanged at 1.7% yoy, matched expectations. Core CPI accelerated from 1.3% yoy to 1.5% yoy. Domestic products price growth quickened from 2.1% yoy to 2.2% yoy. Imported products price growth slowed from 0.5% yoy to 0.4% yoy.

Australia's trade surplus narrows sharply to AUD 6.79B in Sep

Australia's economic outlook has taken a concerning turn as the trade surplus for September contracted significantly, recording its lowest monthly surplus since March 2021. The data released indicates a shrinkage from prior month's AUD 10.16B to AUD 6.79B, falling short of the anticipated AUD 9.58B surplus. This sharp decline in trade surplus is fueling concerns that the Australian economy may have slipped into recession in the third quarter.

The primary factor contributing to the reduced surplus is a noticeable -1.4% yoy drop in goods exports, which totaled AUD 45.62B. This decline was primarily driven by a substantial -39.2% reduction in the shipment of metals and non-monetary gold, a critical export commodity for the Australian economy.

On the import side, there was a 7.5% yoy increase to AUD 38.84B. This surge in imports is attributed to a 23.3% jump in import of capital goods. Additionally, there was a noticeable spike in the demand for recreational items.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2110; (P) 1.2137; (R1) 1.2179; More

GBP/USD is still bounded in established range despite today's rebound, and intraday bias stays neutral. On the upside, firm break of 1.2287 resistance will argue that rise from 1.2036 is resuming. Intraday bias will be turned back to the upside for 38.2% retracement of 1.3141 to 1.2036 at 1.2458. On the downside, decisive break of 1.2036 will resume whole decline from 1.3141 for 1.1801 support next.

In the bigger picture, fall from 1.3141 medium term top could still be a correction to up trend from 1.0351 (2022 low) only. But risk of complete trend reversal is rising. Sustained break of 38.2% retracement of 1.0351 to 1.3141 at 1.2075 will pave the way to 61.8% retracement at 1.1417. For now, risk will stay on the downside as long as 55 D EMA (now at 1.2315) holds, in case of rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Monetary Base Y/Y Oct | 9.00% | 5.90% | 5.60% | |

| 00:30 | AUD | Goods Trade Balance (AUD) Sep | 6.79B | 9.58B | 9.64B | 10.16B |

| 07:30 | CHF | CPI M/M Oct | 0.10% | 0.10% | -0.10% | |

| 07:30 | CHF | CPI Y/Y Oct | 1.70% | 1.70% | 1.70% | |

| 08:45 | EUR | Italy Manufacturing PMI Oct | 44.9 | 46.5 | 46.8 | |

| 08:50 | EUR | France Manufacturing PMI Oct F | 42.8 | 42.6 | 42.6 | |

| 08:55 | EUR | Germany Manufacturing PMI Oct F | 40.8 | 40.7 | 40.7 | |

| 08:55 | EUR | Germany Unemployment Change Oct | 30K | 15K | 10K | |

| 08:55 | EUR | Germany Unemployment Rate Oct | 5.80% | 5.80% | 5.70% | |

| 09:00 | EUR | Eurozone Manufacturing PMI Oct F | 43.1 | 43 | 43 | |

| 11:30 | USD | Challenger Job Cuts Y/Y Oct | 8.80% | 58.20% | ||

| 12:00 | GBP | BoE Interest Rate Decision | 5.25% | 5.25% | 5.25% | |

| 12:00 | GBP | MPC Official Bank Rate Votes | 3--0--6 | 2--0--7 | 4--0--5 | |

| 12:30 | USD | Initial Jobless Claims (Oct 27) | 217K | 210K | 210K | 212K |

| 12:30 | USD | Nonfarm Productivity Q3 P | 4.70% | 4.00% | 3.50% | |

| 12:30 | USD | Unit Labor Costs Q3 P | -0.80% | 1.10% | 2.20% | |

| 14:30 | USD | Natural Gas Storage | 81B | 74B |

US initial jobless claims rose to 217k, above exp 210k

US initial jobless claims rose 5k to 217k in the week ending October 28, above expectation of 210k. Four-week moving average of initial claims rose 2k to 210k.

Continuing claims rose 35k to 1818k in the week ending October 21. Four-week moving average of continuing claims rose 37k to 1758k.

BoE stands pat, adopts lower rate path for economic forecasts

BoE held its Bank Rate steady at 5.25%, aligning with broad market anticipations. The decision came with a 6-3 split, with Megan Greene, Jonathan Haskel, and Catherine Mann opting for a 25 basis points increase. The bank emphasized the necessity of maintaining a restrictive monetary stance for an extended period to steer inflation back to its target. They also signaled that should more enduring inflation signs surface, the option for further rate hikes is still on the table.

Four-quarter GDP growth:

- Lowered from 0.9% to 0.6% in Q4 2023.

- Lowered from 0.1% to 0.0% in Q4 2024.

- Lowered from 0.5% to 0.4% in Q4 2025.

- At 1.1% in Q4 2026 (new).

Modal CPI inflation:

- Lowered from 4.9% to 4.6% in Q4 2023.

- Raised from 2.5% to 3.1% in Q4 2024.

- Raised from 1.6% to 1.9% in Q4 2025.

- Slow to 1.5% in Q4 2026. (new).

These projections are based on a market-implied path for the Bank Rate that hovers around 5.25% until Q3 2024, and then gradually decreases to 4.25% by the end of 2026.

This represents a lower trajectory compared to the projections in August, which anticipated a Bank Rate of 5.8% by the end of 2023, 5.9% by the end of 2024, and 5% by the end of 2025.

(BOE) Bank rate maintained at 5.25%

Monetary Policy Summary, November 2023

The Bank of England's Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. At its meeting ending on 1 November 2023, the MPC voted by a majority of 6–3 to maintain Bank Rate at 5.25%. Three members preferred to increase Bank Rate by 0.25 percentage points, to 5.5%.

The Committee's updated projections for activity and inflation are set out in the accompanying November Monetary Policy Report. These are conditioned on a market-implied path for Bank Rate that remains around 5¼% until 2024 Q3 and then declines gradually to 4¼% by the end of 2026, a lower profile than underpinned the August projections.

Since the MPC's previous meeting, long-term government bond yields have increased across advanced economies. GDP growth has been stronger than expected in the United States. Underlying inflationary pressures in advanced economies remain elevated. Following events in the Middle East, the oil futures curve has risen somewhat while gas futures prices are little changed.

UK GDP is expected to have been flat in 2023 Q3, weaker than projected in the August Report. Some business surveys are pointing to a slight contraction of output in Q4 but others are less pessimistic. GDP is expected to grow by 0.1% in Q4, also weaker than projected previously.

The MPC continues to consider a wide range of data to inform its view on developments in labour market activity, rather than focusing on a single indicator. The increasing uncertainties surrounding the Labour Force Survey underline the importance of this approach. Against a backdrop of subdued economic activity, employment growth is likely to have softened over the second half of 2023, and to a greater extent than projected in the August Report. Falling vacancies and surveys indicating an easing of recruitment difficulties also point to a loosening in the labour market. Contacts of the Bank's Agents have similarly reported an easing in hiring constraints, although persistent skills shortages remain in some sectors.

Pay growth has remained high across a range of indicators, although the recent rise in the annual rate of growth of private sector regular average weekly earnings has not been apparent in other series. There remains uncertainty about the near-term path of pay, but wage growth is nonetheless projected to decline in coming quarters from these elevated levels.

Twelve-month CPI inflation fell to 6.7% both in September and 2023 Q3, below expectations in the August Report. This downside news largely reflects lower-than-expected core goods price inflation. At close to 7%, services inflation has been only slightly weaker than expected in August. CPI inflation remains well above the 2% target, but is expected to continue to fall sharply, to 4¾% in 2023 Q4, 4½% in 2024 Q1 and 3¾% in 2024 Q2. This decline is expected to be accounted for by lower energy, core goods and food price inflation and, beyond January, by some fall in services inflation.

In the MPC's latest most likely, or modal, projection conditioned on the market-implied path for Bank Rate, CPI inflation returns to the 2% target by the end of 2025. It then falls below the target thereafter, as an increasing degree of economic slack reduces domestic inflationary pressures.

The Committee continues to judge that the risks to its modal inflation projection are skewed to the upside. Second-round effects in domestic prices and wages are expected to take longer to unwind than they did to emerge. There are also upside risks to inflation from energy prices given events in the Middle East. Taking account of this skew, the mean projection for CPI inflation is 2.2% and 1.9% at the two and three-year horizons respectively. Conditioned on the alternative assumption of constant interest rates at 5.25%, which is a higher profile than the market curve beyond the second half of 2024, mean CPI inflation returns to target in two years' time and falls to 1.6% at the three-year horizon.

The MPC's remit is clear that the inflation target applies at all times, reflecting the primacy of price stability in the UK monetary policy framework. The framework recognises that there will be occasions when inflation will depart from the target as a result of shocks and disturbances. Monetary policy will ensure that CPI inflation returns to the 2% target sustainably in the medium term.

Since the MPC's previous decision, there has been little news in key indicators of UK inflation persistence. There have continued to be signs of some impact of tighter monetary policy on the labour market and on momentum in the real economy more generally. Given the significant increase in Bank Rate since the start of this tightening cycle, the current monetary policy stance is restrictive. At this meeting, the Committee voted to maintain Bank Rate at 5.25%.

The MPC will continue to monitor closely indications of persistent inflationary pressures and resilience in the economy as a whole, including a range of measures of the underlying tightness of labour market conditions, wage growth and services price inflation. Monetary policy will need to be sufficiently restrictive for sufficiently long to return inflation to the 2% target sustainably in the medium term, in line with the Committee's remit. The MPC's latest projections indicate that monetary policy is likely to need to be restrictive for an extended period of time. Further tightening in monetary policy would be required if there were evidence of more persistent inflationary pressures.

Minutes of the Monetary Policy Committee meeting ending on 1 November 2023

1: Before turning to its immediate policy decision, the Committee discussed: the international economy; monetary and financial conditions; demand and output; and supply, costs and prices. The latest data on these topics were set out in the accompanying November 2023 Monetary Policy Report.

2: The Committee discussed the global economic outlook. Consumer price inflation had generally been easing in advanced economies, but remained elevated. There were upside risks to inflation from energy prices given events in the Middle East. Global growth had remained subdued over the course of 2023 and, in aggregate, had evolved largely as had been expected in the August Monetary Policy Report. Within that, in 2023 Q3, GDP growth in the United States and China had been stronger than expected while euro-area growth had been weaker. Bank staff judged that output was currently above potential in the United States and could remain so for some time, although the extent to which recent strength in activity had also reflected stronger supply was uncertain. In contrast, a sustained period of excess supply was expected in the euro area. In part, that reflected the greater exposure of Europe to the global energy price shock, which had contributed to a more significant trade-off between the outlooks for inflation and growth.

3: Market expectations for the paths of policy rates suggested that interest rates were at or near their peaks in the United Kingdom, the United States and the euro area. Monetary policymakers in each jurisdiction had described the stance of monetary policy as restrictive. Market participants had reported an increasing conviction that UK policy rates would remain 'higher-for-longer' and the median respondent to the Bank's latest Market Participants Survey expected Bank Rate to remain at 5.25% until the second half of 2024, before declining gradually. The sensitivity of interest rates over the year ahead to economic data outturns appeared to have diminished, with more variation in expected rates at the two and three-year horizons.

4: The Committee discussed movements in longer-term advanced economy government bond yields, which had risen materially since the MPC's September meeting, with the largest moves seen in the United States. In part, that was likely to reflect market expectations that global policy rates would remain higher for longer during the current cycle. It was also possible that market perceptions of the equilibrium real interest rate had risen in recent years. Models used by Bank staff suggested that a rise in term premia, the additional compensation that investors required to hold longer-term bonds, had contributed to the most recent rise in longer-term global yields. That might have reflected increased uncertainty around the economic outlook and interest rates, as well as an evolving assessment of the balance of supply and demand in government bond markets. It remained the case, however, that changes in term premia had accounted for only a small proportion of the overall rise in longer-term advanced economy government bond yields over the past two years, relative to the contribution from the rise in expected policy rates.

5: The Committee discussed the recent weakening in UK GDP growth, in the context of the significant tightening of monetary policy since the end of 2021, continued weakness in potential supply growth and an unwinding of previous fiscal support. Quarterly GDP was expected to have been flat in 2023 Q3. Some business surveys of current output and orders were pointing to a fall in GDP in Q4, although other more forward-looking indicators were less pessimistic about growth prospects.

6: There had been increasing signs of some impact of tighter monetary policy on momentum in the real economy. This was perhaps clearest in weaker housing investment, for which the impact of tighter policy was likely to have come through most quickly. Contacts of the Bank's Agents were reporting that higher financing costs, along with greater economic uncertainty, had also been inhibiting business investment, although companies with strong cash positions were continuing to invest. The tightening in monetary policy would take time to feed through to consumer spending fully and was taking effect against the backdrop of a broader recovery in real incomes. There had, however, been declines recently in retail sales volumes, consumer services output and consumer confidence.

7: The slowdown in GDP growth had been feeding into a softening of labour demand. A decline in response rates had resulted in the ONS temporarily ceasing to publish Labour Force Survey estimates of employment, unemployment and inactivity from the June data. Nevertheless, the collective steer from a broad range of indicators, which had tracked the underlying trends in official estimates of labour market activity in the past, pointed to employment being broadly flat in the second half of 2023. There was a narrower set of indicators available to monitor developments in the split of non-employment between unemployment and inactivity. The number of vacancies had continued to decline and indicators of recruitment difficulties had eased, consistent with the labour market loosening further. The labour market had nevertheless remained relatively tight.

8: The Committee discussed the degree of persistence in wages and domestic prices. The recent rise in the annual rate of growth of private sector regular average weekly earnings had not been apparent in other indicators of pay, but there was a common signal that wage growth had remained elevated at around 7%. At the same time, annual services CPI inflation had yet to recede meaningfully, with declines in headline inflation having instead been accounted for by lower energy, food and core goods price inflation. The recent persistence in CPI inflation had in part reflected second-round effects, including through companies' price-setting behaviour. In its November Monetary Report projections, the MPC also judged that more of the recent unexpected strength in pay had been associated with a higher medium-term unemployment rate, owing to more persistent labour market frictions and a resistance to past losses in real income. To the extent that higher unemployment had reflected such supply-related factors, it would imply less easing in the labour market and hence weigh less on pay growth.

The immediate policy decision

9: The MPC sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment.

10: The Committee agreed that there had been little news in key indicators of UK inflation persistence since the MPC's previous decision. Past increases in Bank Rate had weighed increasingly on the economy with the impact of tighter monetary policy likely to materialise earlier in demand and labour market tightness than in wage growth and services CPI inflation.

11: UK GDP was expected to have been unchanged in 2023 Q3, and to grow by 0.1% in Q4. In the MPC's November Monetary Policy Report projections, GDP was expected to be broadly flat over the first half of the forecast period and growth was projected to remain well below historical averages in the medium term, a weaker profile than in the August Report.

12: Against this backdrop of subdued economic activity, and based on a range of indicators, employment growth was likely to have softened. Falling vacancies and surveys indicating an easing of recruitment difficulties also pointed to a loosening in the labour market.

13: Pay growth had remained high across a range of indicators, although the recent rise in the annual rate of growth of private sector regular average weekly earnings (AWE) had not been apparent in other series. There remained uncertainty about the near-term path of pay. The MPC judged in its November Report projections that more of the recent unexpected strength in pay had been associated with a higher medium-term equilibrium unemployment rate, and therefore greater persistence in wage and price inflation.

14: Twelve-month CPI inflation remained well above the 2% target. Inflation had fallen to 6.7% both in September and 2023 Q3, below expectations in the August Report. The downside news had largely reflected lower-than-expected core goods price inflation. At close to 7%, services CPI inflation was only slightly weaker than had been expected in August.

15: In the MPC's latest most likely, or modal, projections, conditioned on the market-implied path for Bank Rate, CPI inflation was expected to return to the 2% target by the end of 2025. It was then projected to fall below the target thereafter, as an increasing degree of economic slack was expected to reduce domestic inflationary pressures.

16: The Committee continued to judge that the risks around the modal inflation projection were skewed to the upside. Second-round effects in domestic prices and wages were expected to take longer to unwind than they had done to emerge. There were also upside risks to inflation from energy prices given events in the Middle East. Taking account of this skew, the mean projection for CPI inflation was 2.2% and 1.9% at the two and three-year horizons respectively.

17: The MPC also considered its projections conditioned on the alternative assumption of constant interest rates at 5.25% over the forecast period, which was a higher profile than the market curve beyond the second half of 2024. Under this alternative assumption, mean CPI inflation was expected to return to the 2% target in two years' time, three quarters earlier than when conditioned on the market-implied path for interest rates.

18: The MPC's remit was clear that the inflation target applied at all times, reflecting the primacy of price stability in the UK monetary policy framework. The framework recognised that there would be occasions when inflation would depart from the target as a result of shocks and disturbances. Monetary policy would ensure that CPI inflation returned to the 2% target sustainably in the medium term. Monetary policy was also acting to ensure that longer-term inflation expectations were anchored at the 2% target.

19: Given the significant increase in Bank Rate since the start of this tightening cycle, the current monetary policy stance was restrictive. The decision whether to increase or to maintain Bank Rate at this meeting was again finely balanced between the risks of not tightening policy enough when underlying inflationary pressures could prove more persistent, and the risks of tightening policy too much given the impact of policy that was still to come through.

20: Six members judged that maintaining Bank Rate at 5.25% was warranted at this meeting. There had been little news in UK economic data since the previous meeting. GDP growth had weakened and the labour market had continued to loosen. CPI inflation was expected to decline significantly in coming quarters, and the acceleration in AWE, while noteworthy, was not reflected in a broader range of wage growth measures. For most members within this group, the MPC's latest projections indicated that a restrictive monetary policy stance was likely to be warranted for an extended period of time to bring inflation sustainably back to the 2% target. A further rise in Bank Rate remained a possibility. For one member, the risks of overtightening policy had continued to build. Lags in the effects of monetary policy meant that sizeable impacts from past rate increases were still to come through.

21: Three members preferred a 0.25 percentage point increase in Bank Rate, to 5.5%, at this meeting. Although there was some weakening in economic activity, real household incomes had continued to rise, and forward-looking indicators of output had remained positive. The labour market was still relatively tight, consistent with a rise in the medium-term equilibrium rate of unemployment and strong labour demand, and the pace of loosening had been slow. Measures of wage growth and services inflation had remained elevated. These members continued to judge that there was evidence of more persistent inflationary pressures. An increase in Bank Rate at this meeting was necessary to address the risks of more deeply embedded inflation persistence and bring inflation back to target sustainably in the medium term.

22: The MPC would continue to monitor closely indications of persistent inflationary pressures and resilience in the economy as a whole, including a range of measures of the underlying tightness of labour market conditions, wage growth and services price inflation. Monetary policy would need to be sufficiently restrictive for sufficiently long to return inflation to the 2% target sustainably in the medium term, in line with the Committee's remit. The MPC's latest projections indicated that monetary policy was likely to need to be restrictive for an extended period of time. Further tightening in monetary policy would be required if there were evidence of more persistent inflationary pressures.

23: The Chair invited the Committee to vote on the proposition that:

- Bank Rate should be maintained at 5.25%.

24: Six members (Andrew Bailey, Sarah Breeden, Ben Broadbent, Swati Dhingra, Huw Pill and Dave Ramsden) voted in favour of the proposition. Three members (Megan Greene, Jonathan Haskel and Catherine L Mann) voted against the proposition, preferring to increase Bank Rate by 0.25 percentage points, to 5.5%.

Operational considerations

25: On 25 September, the Bank of England had completed the final gilt sales auction of the October 2022 to September 2023 annual programme to meet the MPC's decision to reduce the stock of UK government bond purchases held for monetary policy purposes by £80 billion over that period.

26: At its September 2023 meeting, the MPC had voted to reduce the stock of UK government bond purchases held for monetary policy purposes by £100 billion over the 12-month period from October 2023 to September 2024. The first auction of that annual programme had taken place on 2 October 2023.

27: On 1 November, the total stock of assets held for monetary policy purposes was £751 billion, comprising £750 billion of UK government bond purchases and £0.6 billion of sterling non‐financial investment‐grade corporate bond purchases.

28: The following members of the Committee were present:

- Andrew Bailey, Chair

- Sarah Breeden

- Ben Broadbent

- Swati Dhingra

- Megan Greene

- Jonathan Haskel

- Catherine L Mann

- Huw Pill

- Dave Ramsden

Sarah Breeden was present as an observer before becoming a member on 1 November.

Sam Beckett was present as the Treasury representative.

Ben Bernanke was present as an observer.

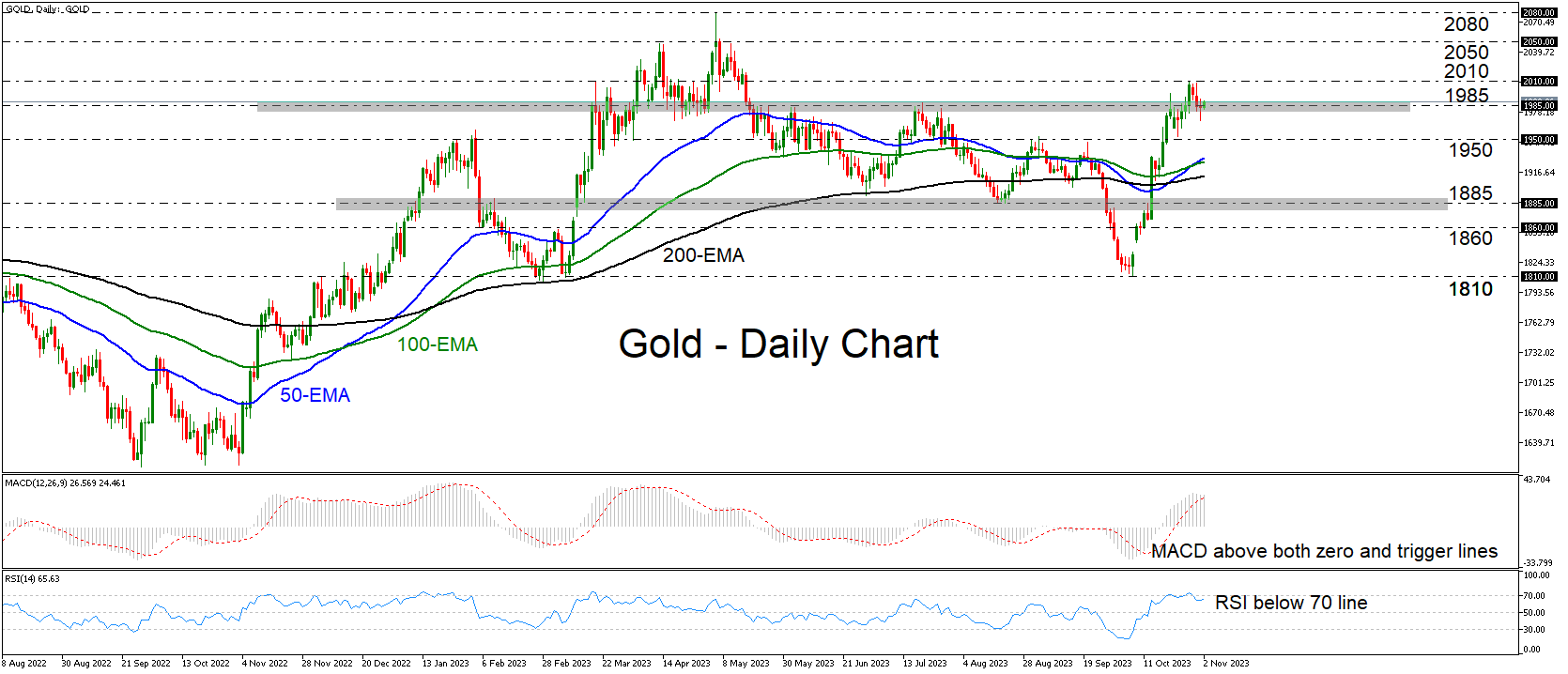

Gold Trades Near Key Barrier of 1,985

- Gold pulls back to rest near 1,985 key zone

- Daily oscillators detect slowing upside momentum

- A break lower could signal the metal’s return within a broader range

Gold has been in a retreat mode since October 30, after hitting resistance near the 2,010 zone. The metal has seen massive gains due to concerns surrounding the conflict in the Middle East, but the current retreat has brought it back near the 1,985 barrier, which acted as the upper bound of the sideways range that contained most of the price action from January 12 until October 27.

The MACD lies above both its zero and trigger lines, but shows signs of topping, while the RSI exited its above-70 zone, and it is now hovering slightly below 70. Both indicators suggest that the geopolitics-related rally is losing momentum and that some further retreat may be possible in the days to come.

A clear close below 1,985 could confirm gold’s return within the aforementioned sideways range and may allow declines towards the 1,950 barrier, marked by the inside swing highs of September 1 and 20. If the bears are not willing to stop there, then a break lower could pave the way towards the lower bound of the range at around 1,885.

On the upside, a rebound and a break above 2010 could signal that the bias remains bullish and that the current retreat was just a breather before the next leg north. The precious metal could next meet resistance at the high of May 10 at around 2,050, the break of which could put the record peak of a around 2,080 on the bulls’ radar.

To recap, gold pulled back this week and is now trading near the key barrier of 1,985. A clear close below it could signal the metal’s return within a longer-term sideways range, while a rebound may confirm that the broader bias remains bullish.

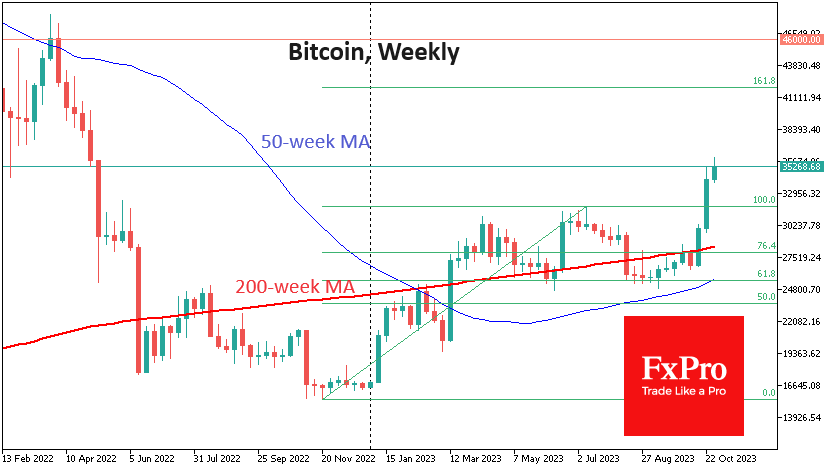

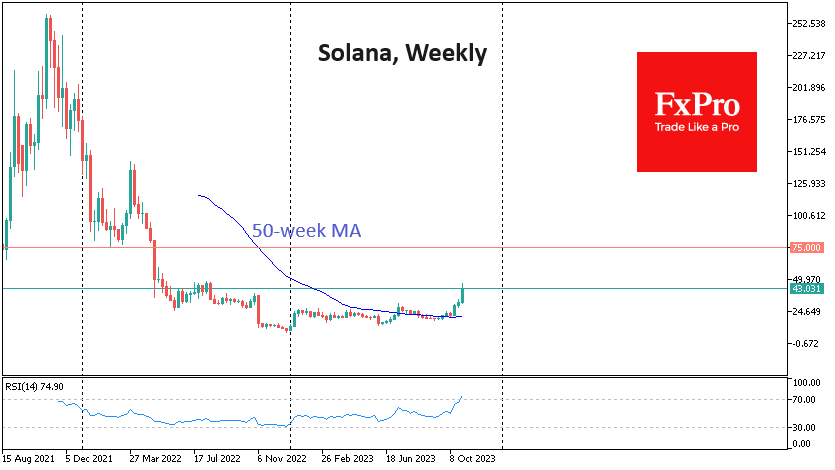

Solana Races Towards the Sun, Bitcoin Reaches New Heights

Market picture

The cryptocurrency market rose on Wednesday, gaining fresh buying impulse after the Fed’s comments. Total market cap exceeded $1.30 trillion (+2.6% in 24 hours) and reached $1.32 trillion at the start of the day. Bitcoin surpassed $35K (+2.2%), and demand spread to leading altcoins such as XRP (+4%) or Solana (+10%).

Bitcoin broke the upper boundary of the week-long consolidation, climbing to $36K early on Thursday before retreating to $35.1K by the European session. Technically, the recent jump is a confirmation of the bullish bias. Bitcoin may not face significant resistance until $41K, but the maximum target for this momentum is $46K, where there was the last reversal.

Solana has gained up to 50% over the last three days. It has already surpassed its Fibonacci upside target of 161.8% of the original jump from 12 to 26 October. This coin’s price is at its highest since August last year, although it is still 85% below its peak of precisely two years ago. There is no technical resistance between $48 and $75, but it already looks locally overheated.

News background

According to CoinDesk, several of the world’s largest market makers could provide liquidity for BlackRock’s bitcoin ETF if regulators approve the product. Jane Street, Virtu Financial, Jump Trading and Hudson River Trading have already talked with BlackRock, which recently updated its filing with the SEC to launch the ETF.

October was probably SkyBridge Capital’s best month ever, said hedge fund founder Anthony Scaramucci. Bitcoin had an impressive month, he said. The fund also holds a lot of Solana, up 70% for the month.

Tether, the issuer of the USDT stablecoin, reported reserves for the third quarter of the year. According to the report, the financial giant’s excess reserves totalled $3.2 billion.

The TON blockchain set a new world record during public testing, completing nearly 105,000 transactions per second (TPS). This figure exceeds all confirmed results of other blockchains and the maximum speed of the centralised payment systems Visa and Mastercard. The previous holder of the fastest blockchain title was Solana.

Eurozone PMI manufacturing finalized at 43.1, woes deepen

Eurozone's PMI Manufacturing reading for October was finalized at 43.1, a slight decline from September's 43.4.

A closer look at individual countries, notably, Germany, Europe's largest economy, posted a five-month high, though it still lurks in the downturn territory with a reading of 40.8. France hits a 41-month low at 42.8.

Amidst the broader decline, Greece displayed resilience with a two-month high of 50.8. In contrast, countries such as Ireland, Spain, and Italy presented figures pointing towards continued economic pressure with readings of 48.2, 45.1, and 44.9, respectively.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, likened the ongoing trend in Eurozone manufacturing to a "bumpy sleigh ride." While the slight stability in recent PMI figures might hint at approaching the low point of this downturn, the critical indicators like the new orders index remain in the red.

The stagnation of these vital indices, as history suggests, could potentially set the stage for a recovery. However, de la Rubia anticipates this turnaround to materialize in the first half of the upcoming year.

Furthermore, he pointed out the synchronized decline among the eurozone nations. With key players like France, Italy, Spain, and Germany showcasing dipping PMIs, it's evident that a sectoral contraction might be imminent for these nations in the current quarter.

EUR/GBP Technical: Medium-Term Bullish Basing as BoE Looms

- Three key technical developments have suggested that the EUR/GBP cross pair has formed a potential medium-term bullish basing configuration since 23 August 2023

- Watch the key short-term support at 0.8680.

- Immediate resistances stand at 0.8750 and 0.8820.

The price actions of the EUR/GBP cross pair have started to trace out a medium-term bullish basing configuration since 23 August 2023 as we await the latest Bank of England (BoE) monetary policy decision later today.

Clearance above 200-day moving average

Fig 1: EUR/GBP medium-term trend as of 2 Nov 2023 (Source: TradingView, click to enlarge chart)

There are three key positive technical developments that have taken form. Firstly, the bullish basing formation has taken shape after a recent retest (23 August 2023) on the major ascending trendline from the 7 March 2022 low of 0.8203.

Secondly, recent price actions have surpassed the key 200-day moving average with a retest and rebound from it during yesterday’s US session (1 November) ex-post FOMC.

Thirdly, the 20 and 50-day moving averages have started to slope upwards with price actions above the 50-day moving average that indicate a potential medium-term uptrend phase is in motion.

Oscillation within a minor ascending channel

Fig 2: EUR/GBP minor short-term trend as of 2 Nov 2023 (Source: TradingView, click to enlarge chart)

In the short-term as seen in the 1-hour chart, the EUR/GBP has evolved into an impulsive up move sequence within a minor ascending channel in place since the 6 September 2023 low.

Watch the 0.8680 key short-term pivotal support (lower boundary of the ascending channel & 20-day moving average) for a potential push-up to retest the 31 October minor swing high area of 0.8750 before the intermediate resistance at 0.8820 (upper boundary of the ascending channel, 2/3May 2023 swing high & Fibonacci extension).

However, a break below 0.8680 negates the bullish tone for a pull-back toward the next intermediate support at 0.8640 (50-day moving average).