Sample Category Title

US Treasuries Secured Ssignificant Gains

Markets

US Treasuries secured significant gains yesterday in a three-stage rally. The US Treasury Department ignited the move with the publication of the quarterly refunding statement. The total increase of auction sizes in the November-through-January quarter was slightly smaller-than-expected, with a bigger-than-hoped-for pivot towards issuing shorter and medium term securities. Treasury plans to increase the auction sizes of the 2- and 5-yr by $3bn/month compared to August-through-October volumes, the 3-yr by $2bn/month, and the 7-yr by $1bn/month. Increases of sales of 10-yr and 30-yr securities occurs at a slower pace than in the previous quarter (single additional step-up of $2bn and $1bn respectively) with 20-yr bond volumes even unchanged. Longer term Treasuries started outperforming short-dated ones after the refunding statement with the US October manufacturing ISM extending gains. The ISM faced an unexpected setback (46.7 from 49 and vs 49 consensus), erasing previous month’s increase. Details showed a steep drop in new orders (45.5 from 49.2) and a reduction in production (50.4 from 52.5), forcing companies into lay-offs (46.8 from 51.2). Ahead of the ISM, markets ignored a decent though below-consensus October ADP employment report (113k vs 150k expected) and rising job openings (JOLTS). The Fed and chair Powell had the final say after concluding their November gathering at which the central bank kept its policy rate unchanged at 5.25%-5.50% for a second straight meeting. The statement balanced more bullish connotations to growth (“expanded at a strong pace in Q3” vs “expanding at a solid pace”) and the labour market (“moderated since earlier in the year” vs “slowed in recent months”) with the addition of tighter financial conditions. Fed chair Powell stuck to his recent mantra to proceed carefully from here. He didn’t pre-commit to the December meeting, shielding with data dependence and the publication of two additional labour market and inflation reports by the time of the convening. During the Q&A-session, he tried to divert attention from economic resilience (and related inflation risks) to the ongoing disinflationary process. In yesterday’s bullish bond momentum this was seen as evidence that the final flagged rate hike in September dots is off the table, though Powell didn’t comment on that. The longed-for Fed pivot gave Treasuries the final push in the back while lifting spirits on stock markets (up to 1.65% for Nasdaq). US yields lost 14.4 bps to 20.7 bps yesterday with the belly of the curve outperforming the wings. From a technical point of view, this calls off recent tests of cycle tops like the psychological 5% mark for the 10-yr yield. First important support stands around 4.52% (October low). The US 2-yr yield tested this reference (4.92% October low), but bounces off this morning. The (trade-weighted) greenback traded volatile but held strong yesterday despite loss of rate support (DXY unchanged close at 106.65 though softer this morning). Central bank meetings in Norway, the Czech Republic and the UK are key today. A dovish hold by the BoE and gloomy outlook risks hurting sterling.

News and views

Japanese premier Kishida has announced another round of fiscal stimulus. The package tops JPY 17tn, of which three quarters will be funded by a supplementary budget for the remainder of the FY through March 2024. Measures include temporary tax rebates and cash handouts to low-earning households as well as support for businesses to raise wages. Kishida aims to help to cushion the impact of inflation on households and companies, who have been increasingly critical of the PM’s handling of the matter. Doing so, however, risks prolonging or even intensifying rising price pressures. The Bank of Japan as recently as Tuesday took another baby step towards exiting its very easy monetary policy. But this incremental approach hurts JPY. Even with yesterday’s triple blow to the US dollar, USD/JPY continues to trade above 150. A weak JPY is another factor fueling (imported) inflation.

Governor of the Bank of Canada Macklem believes the neutral rate is rising rather than declining. Macklem told Canada’s Senate economy committee that the impact of higher budget deficits, aging societies and larger investments in renewable energy need to be considered in the matter. He added that he wasn’t “totally comfortable” with policymakers leaving the estimate for the range of the nominal neutral rate between 2-3% in the annual review back in April. If the neutral rate would indeed be higher than before, it means the current policy stance (5% policy rate), all else equal, is less restrictive than previously thought.

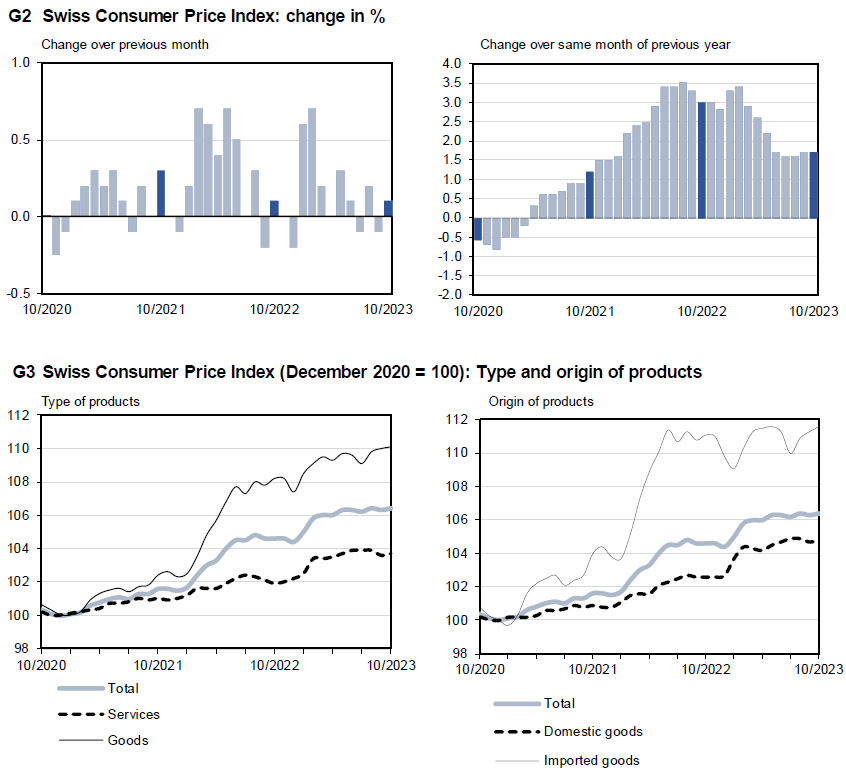

Swiss CPI unchanged at 1.7% yoy in Oct, core CPI rises to 1.5% yoy

Swiss CPI rose 0.1% mom in October, matched expectations. Core CPI (excluding fresh and seasonal products, energy and fuel) rose 0.1% mom. Domestic products prices was flat at 0.0% mom. Imported products prices rose 0.3% mom.

Annually CPI was unchanged at 1.7% yoy, matched expectations. Core CPI accelerated from 1.3% yoy to 1.5% yoy. Domestic products price growth quickened from 2.1% yoy to 2.2% yoy. Imported products price growth slowed from 0.5% yoy to 0.4% yoy.

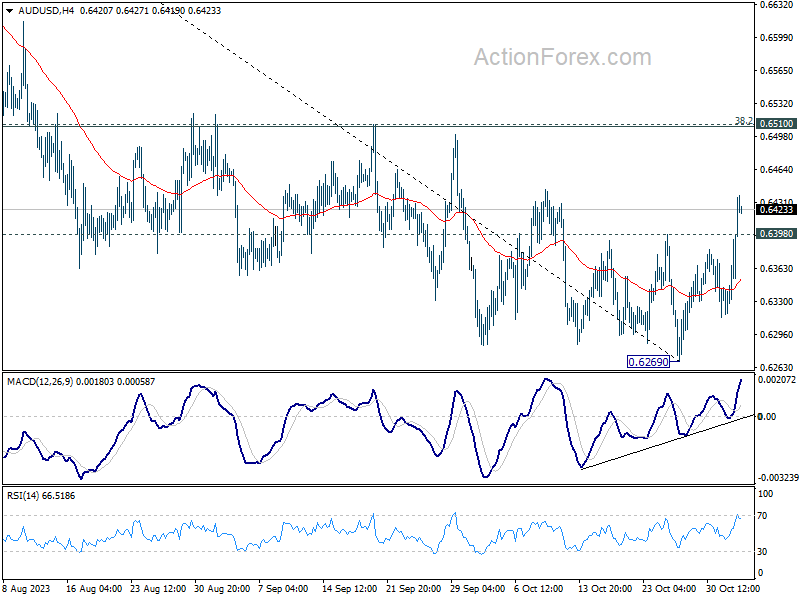

AUD/USD Daily Report

Daily Pivots: (S1) 0.6341; (P) 0.6371; (R1) 0.6423; More...

AUD/USD's break of 0.6398 resistance indicates short term bottoming at 0.6398. Intraday bias is back on the upside for rebound to 0.6510 cluster resistance (38.2% retracement of 0.6894 to 0.6269 at 0.6508). Rejection by this level will retain near term bearishness or another fall through 0.6269 at a later stage. However, firm break of 0.6510 will argue that whole decline from 0.7156 might be completed with three waves down to 0.6269. Stronger rally should then be seen.

In the bigger picture, down trend from 0.8006 (2021 high) is possibly still in progress. Decisive break of 0.6169 will target 61.8% projection of 0.8006 to 0.6169 to 0.7156 at 0.6021. This will now remain the favored case as long as 0.6894, in case of strong rebound.

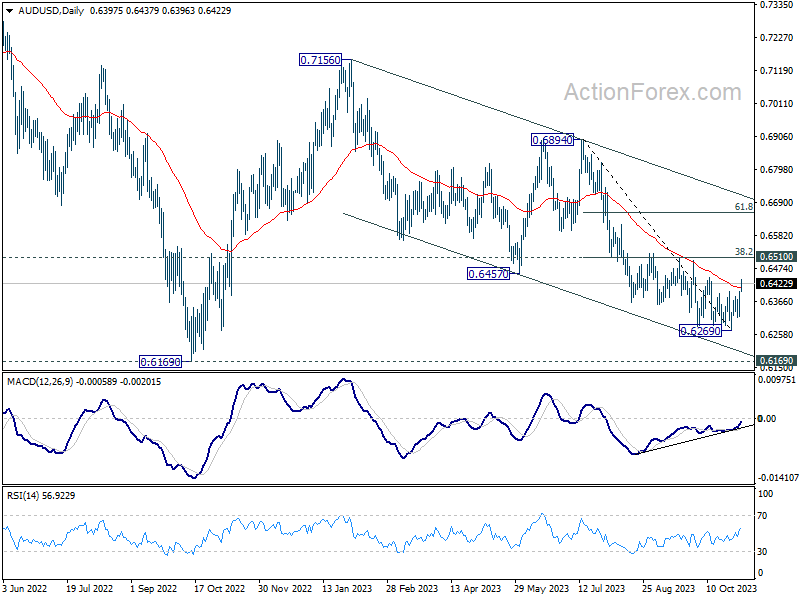

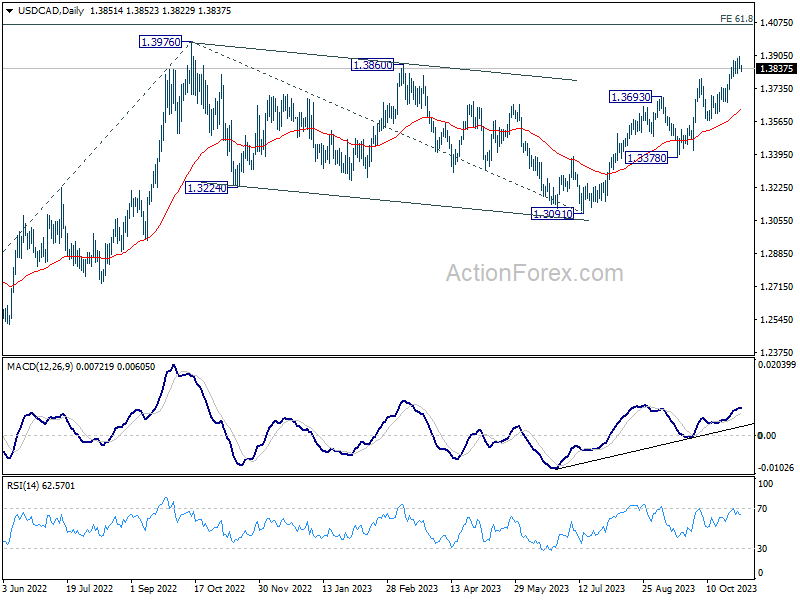

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3832; (P) 1.3865; (R1) 1.3890; More...

USD/CAD retreated quickly after edging higher to 1.3897 and intraday bias is turned neutral again. Downside of retreat should be contained by 1.3739 support to bring another rally. On the upside, above 1.3897 will target 1.3976 resistance. Decisive break there will resume larger up trend to 1.4064 projection level.

In the bigger picture, corrective pattern from 1.3976 (2022 high) should have completed with three waves down to 1.3091. Decisive break of 1.3976 high will confirm resumption of up trend from 1.2005 (2021 low). Next target will be 61.8% projection of 1.2401 to 1.3976 from 1.3091 at 1.4064. This will now remain the favored case as long as 1.3568 support holds.

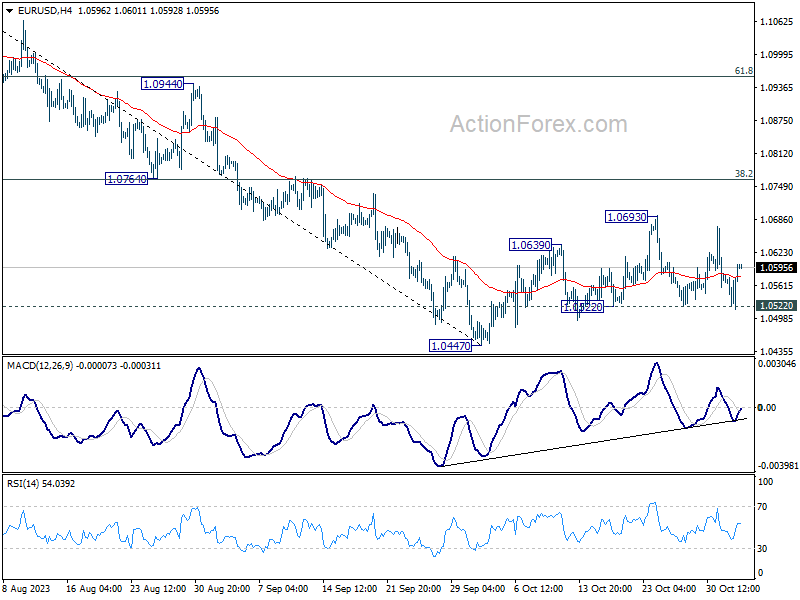

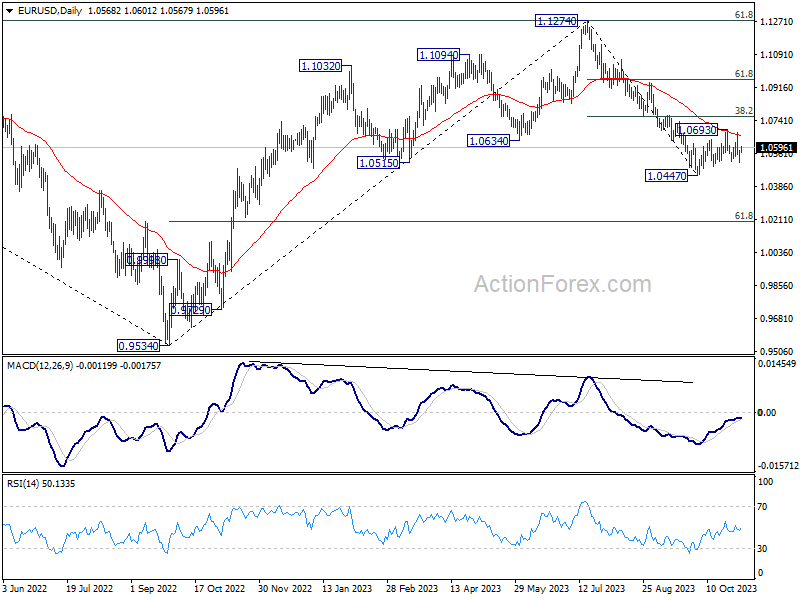

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0531; (P) 1.0556; (R1) 1.0595; More...

Intraday bias in EUR/USD stays neutral for the moment. On the downside, firm break of 1.0522 support will argue that larger fall from 1.1274 is resumed to ready. Intraday bias will be back on the downside for 1.0447 first, and then 1.0199 fibonacci level. On the other hand, strong bounce from current level, followed by break above 1.0693, will extend the rebound from 1.0447 to 1.0764 cluster resistance (38.2% retracement of 1.1274 to 1.0447 at 1.0763).

In the bigger picture, fall from 1.1274 medium term top could still be a correction to rise from 0.9534 (2022 low). But chance of a complete trend reversal is rising. In either case, current fall should target 61.8% retracement of 0.9534 to 1.1274 at 1.0199 next. For now, risk will stay on the downside as long as 55 D EMA (now at 1.0665) holds, in case of rebound.

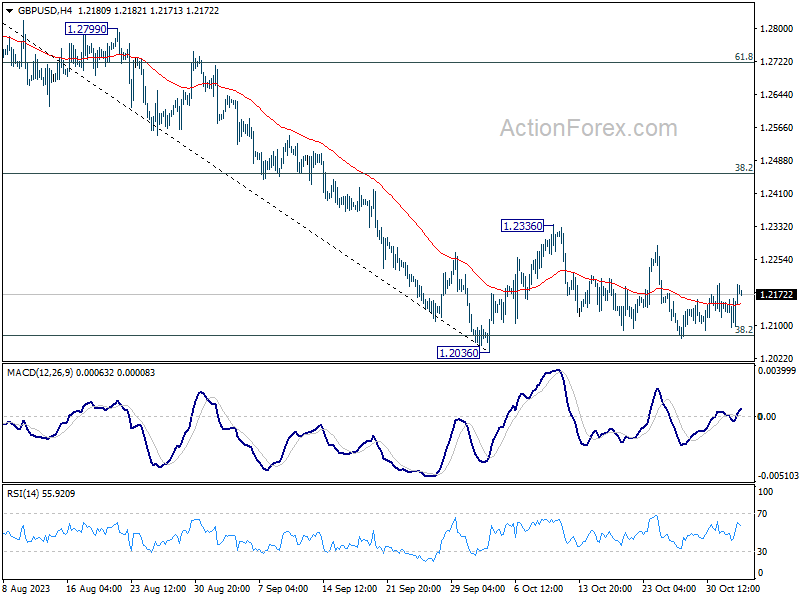

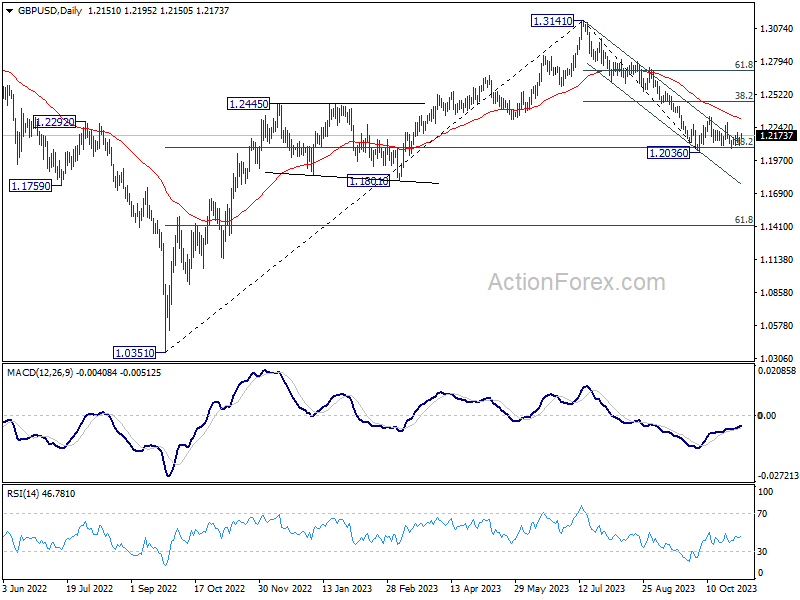

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2110; (P) 1.2137; (R1) 1.2179; More

GBP/USD is still bounded in sideway trading and intraday bias stays neutral. With 1.2336 resistance intact, downside breakout is expected. On the downside, firm break of 1.2036 will resume whole decline from 1.3141 for 1.1801 support next. However, break of 1.2336 will turn bias back to the upside for 38.2% retracement of 1.3141 to 1.2036 at 1.2458.

In the bigger picture, fall from 1.3141 medium term top could still be a correction to up trend from 1.0351 (2022 low) only. But risk of complete trend reversal is rising. Sustained break of 38.2% retracement of 1.0351 to 1.3141 at 1.2075 will pave the way to 61.8% retracement at 1.1417. For now, risk will stay on the downside as long as 55 D EMA (now at 1.2346) holds, in case of rebound.

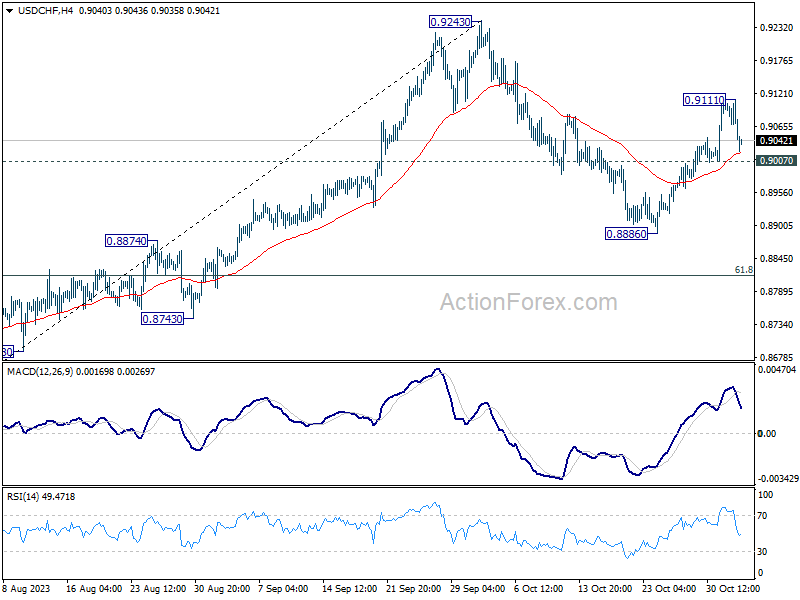

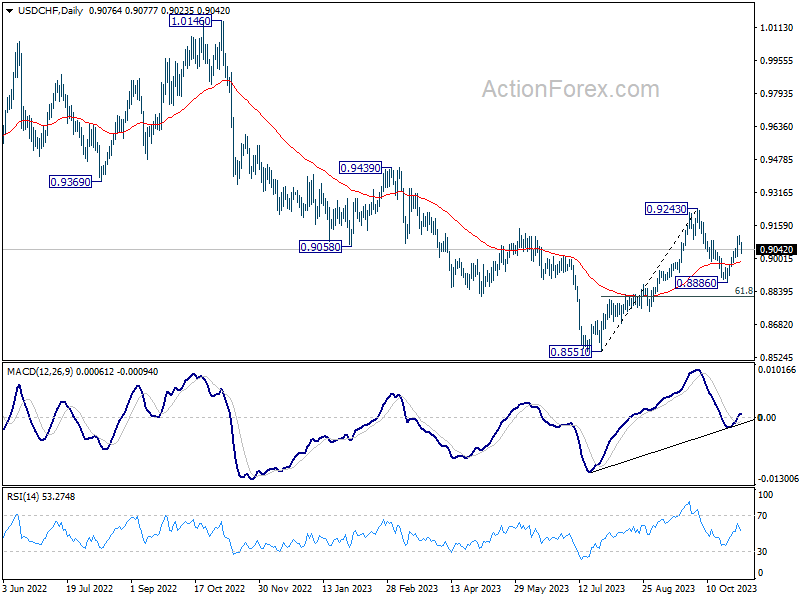

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9062; (P) 0.9087; (R1) 0.9105; More....

Intraday bias in USD/CHF is turned neutral with current retreat. For now, further rise is in favor as long as 0.9007 support holds. Above 0.9111 will resume the rebound from 0.8886 to retest 0.9243 resistance next. However, firm break of 0.9007 will turn bias to the downside for 0.8886 support instead.

In the bigger picture, outlook is mixed up by the deeper than expected pull back from 0.9243. Yet there was no follow through selling after hitting 0.8886. On the upside, break of 0.9243 resistance will revive the case of medium term bottoming at 0.8851, and turn outlook bullish. However, sustained break of 61.8% retracement of 0.8551 to 0.9243 at 0.8815 will argue that larger decline from 1.0146 is ready to resume through 0.8551 low.

AUDUSD Elliott Wave Bounce Corrective Or Simple A-B-C?

The short-term Elliott wave view in the AUDUSD suggests that the decline from the 02 February 2023 peak has ended as a diagonal structure where wave 1 ended at $0.6458 low. A bounce to $0.6899 high ended wave 2. Wave 3 ended at $0.6356 low, and wave 4 ended at $0.6511 high. Then a decline to $0.6269 low ended wave 5 thus ended wave (1). Above from there, the pair is doing a bounce in wave (2) against that cycle. And the pair soon needs to decide if it’s going to extend in 7 swings or a simple A-B-C from the lows.

So far, the rally from the lows is unfolding in 3 waves only but is expected to take the form of simple A-B-C. Whereas the first leg to $0.6283 high has ended wave ((i)). Then a pullback to $0.6313 low ended wave ((ii)). Up from there, the pair has managed to reach the extreme from the lows at $0.6427- $0.6497 area. From there, the pair is expected to make a small pullback. Then decide whether it’s going to continue higher in an impulse sequence with a shallow pullback. Or if it makes a strong pullback against the $0.6269 low then the bounce can extend in corrective 7 swings from the lows. Near-term, as long as dips remain above $0.6269 low expect the pair to continue to extend higher in the bounce. We don’t recommend buying the pair.

AUDUSD 1-Hour Elliott Wave Chart From 11.02.2023

AUDUSD Elliott Wave Video

https://www.youtube.com/watch?v=jcDH7tRrEk8

BoE Between a Rock and a Hard Place

As widely expected, the Federal Reserve (Fed) maintained its interest rates unchanged at this week’s meeting and President Jerome Powell cited that the recent surge – especially in the long end of the US yield curve – helped tightening the financial conditions in the US. Powell repeated that the Fed is proceeding carefully but that they are ‘not confident that inflation is on path toward 2%’ target’. US policymakers redefined the US economic outlook as being ‘strong’, from being just ‘solid’.

In summary, the latest Fed decision was not dovish, unsurprisingly hawkish, and did not impact appetite in US bonds which got a boost from the Treasury’s announcement of a slightly lower-than-expected quarterly refunding auction size for the 3, 10 and 30-year maturity bonds next week. Cherry on top, the US Treasury said that they now expect one more step up in quarterly issuances for the long-term debt, whereas the expectation was multiple more step ups.

The US 10-year yield sank to 4.70% after the Fed decision and Treasury’s much-awaited issuance calendar reveal, the 30-year yield fell to 4.90%. The fact that the US will borrow slightly less than previously thought and slightly less on the long-end of the curve doesn’t mean that the fiscal outlook improved. Though lower-than-expected, the $776bn that the US Treasury is planning to borrow this quarter is a record for the last 3 months of a year. And the net interest payments on the US federal debt are rising at an eye-watering speed. In numbers, the federal debt rose more than a third since the end of 2019, and the interest expenses on that debt rose by almost 40%. That’s a detail for Janet Yellen who thinks that the surge in US yields is explained by the positive economic outlook, but the market won’t allow the Treasury to borrow like its pockets have no bottom if the Fed is not part of it.

Bad news, good news

The sharp decline in October ISM manufacturing PMI and the softer-than-expected ADP read helped boosting sentiment in US Treasuries, as they somehow softened the otherwise strong US economic outlook. The JOLTS data unexpectedly rose but no one was out looking for reasons to sell Treasuries yesterday, so that basically went unheard. The official US jobs data is due Friday and any strength in NFP, or wages could reverse the optimism that the US economic growth will… slow. And as bad news is sometimes good news for the market, the S&P500 rebounded more than 1% and closed the session at a spitting distance from the all important 200-DMA, while the rate-sensitive Nasdaq jumped almost 1.80%.

AMD, Qualcomm gain, Apple to report

On the individual level, AMD jumped almost 10% yesterday. Even though the company gave a soft guidance for Q4, they said that they expect to sell more than $2bn worth of AI chips next year. That’s a lot, that’s more than a third of the actual revenue they make. Qualcomm jumped nearly 4% in afterhours trading, as the world’s largest seller of smartphone chips gave a better-than-expected prediction for this quarter, saying that the inventory glut in mobile-phone industry may be receding.

Today, Apple will post its Q3 earnings, after the bell. We have reservations regarding the results as the iPhone15 sales are not as brilliant as investors hoped they would be, and Huawei is apparently eating Apple’s market share in China. Apple’s overall revenue is seen down by around 3%. Ouch. The good news is that the morose expectations could be easier to beat. Otherwise, we could see Apple tank below the $170 per share, into the bearish consolidation zone, and become vulnerable to deeper losses.

BoE not to raise rates, but its inflation tolerance

The Bank of England (BoE) is the next major central bank to announce its rate decision today, and the Brits are not expected to raise the interest rates at today’s MPC meeting, but they are expected to increase their tolerance faced with above 2% inflation, instead. That’s not good for central bank credibility, even less so when the BoE’s credibility is not at its best since the start of this tightening cycle. If investors sense that the BoE will let inflation run hot, by lack of choice, sterling could take a significant hit.

Gold and Oil

Appetite in gold eases as Israelian attacks are perceived as being less aggressive than what they could be. De-pricing of Mid-East risks could send the price of an ounce to, or below the 200-DMA, near the $1933 level. Upside risks prevail, but fresh news should gradually lose their shocker impact and the $2000 per ounce level will likely attract top sellers more than anything else.

US crude rebounded near the $80pb yesterday, as the decline toward the psychological $80pb level brought in dip buyers. We could reasonably expect the US crude to correct toward $85pb as geopolitical tensions loom, and supply remains at jeopardy.

Bond Markets Rally

Market movers today

We have more central bank meetings on the menu today. We expect Norges Bank to leave rates unchanged at 4.25%. All eyes will instead be on what signals the bank puts out about its December meeting. See RTM Norway - Norges Bank on hold; to keep a data-dependent tightening bias, 27 October.

We also expect no changes from the Bank of England. We see them sticking to their guidance emphasising the "higher for longer" approach, like the ECB. See Bank of England Preview - Soft data warrants the BoE to stay on hold, 27 October.

On the data front, we will look out for the German unemployment rate, which has been climbing slowly higher this year.

In the US, we will keep an eye on Q3 unit labour cost data to gauge cost pressures at a business level. We also get initial jobless claims.

In Denmark, FX reserve figures are released by Nationalbanken. We do not think they have been active in the market in October, as EUR/DKK has traded quite close to the central rate.

The 60 second overview

Fed on hold. The FOMC decided, as expected, to keep the Fed Funds target range unchanged at 5.25-5.50% at yesterday's meeting. Powell struck a rather balanced tone at the press conference, emphasising that the FOMC sees progress but is not yet convinced that financial conditions are sufficiently restrictive. The FOMC is closely following the move up in long rates, though the impact of growth remains to be seen. Looking ahead, December is still 'live', though Powell hinted that the September median expectation of one more hike this year could be less accurate today. US inflation has moderated, but, as Powell put it, 'a few months of good data is only the beginning of the Fed building confidence that inflation is moving sustainably down'. We stick to our call that the last rate hike was delivered in July. The Fed signaled no plans to make changes to QT, which we expect to run at least into late 2024 and in any case well past the first rate cut. See US Research - Fed review: Still on Track, 1 November.

Bond markets rally. Several additional factors provided tailwinds to bonds yesterday. The US Quarterly Refunding Statement showed that the US Treasury expects to slow the pace of issuance in the long end of the curve in December and January. Additionally, total issuance at next week's refunding auction will be slightly smaller than expected at USD112bn. The decline in yields gained further traction in the afternoon following the release of significantly weaker than expected Manufacturing ISM figures for October. Labour market data was mixed with ADP lower than expected at 89.000 in October (consensus 150.000), while job openings remained elevated at ˜9.5mn in September.

Equities: Equities continued higher for a third day in a row. A lot of moving pieces but an unsurprising Fed meeting, weak macro data and lower Treasury borrowing than expected sent yields substantially lower and equities higher. As it was a yield driven session, cyclical growth and quality stocks were in favour, including big tech, consumer discretionary or real estate. The Nordic session was also a quality oriented one, but with a defensive tilt with especially health care at the top. This summarized to S&P 500 a full 1.1% higher, Stoxx 600 0.6% and small caps yet again underperforming. As yields are continuing lower this morning, US futures indicate another opening in green.

FI: EGB yields fell yesterday with USTs as US economic data surprised to the downside, Powell struck a dovish tone and the US Treasury issuance outlook was less bad than expected. 10Y Bund yields ended the day down 4bp, while the 10Y BTP-Bund spread tightened a few basis points. The 5Y5Y EUR Inflation Swap rate declined by 3bp to 2.47% - the lowest level seen since mid-June. 10Y UST yields ended the session down by 18bp.

FX: As per our expectations, Powell was interpreted as dovish by markets and US yields declined sharply. The USD gave back some of its gains from earlier in the session and EUR/USD ended up basically unchanged on the day. A rather uneventful day for Scandies whereas the JPY recovered some of the previously lost ground vs the USD. The GBP held steady in anticipation of today's BoE meeting.

Credit: Credit markets saw their fourth consecutive day of tightening, which has resulted in total tightening of 30bp for Xover, which currently trades at 430bp, and 6bp for Main, which is now at 83.6bp.

Nordic Macro

We expect Norges Bank to stay on hold at 4.25% today. All eyes will be on what signals the bank puts out about its December meeting. Lower inflation numbers must be weighed against a weaker NOK, and Norges Bank must stress that risks are tilted to both sides and that the December decision obviously will be data-dependent.