Sample Category Title

Fed Review: Still on Track

- The Fed maintained monetary policy unchanged in the November meeting as widely anticipated. We still think the Fed's rate hikes are already over.

- Powell underscored, that the tightening in financial conditions needs to be persistent to influence monetary policy, but also that policy is already restrictive.

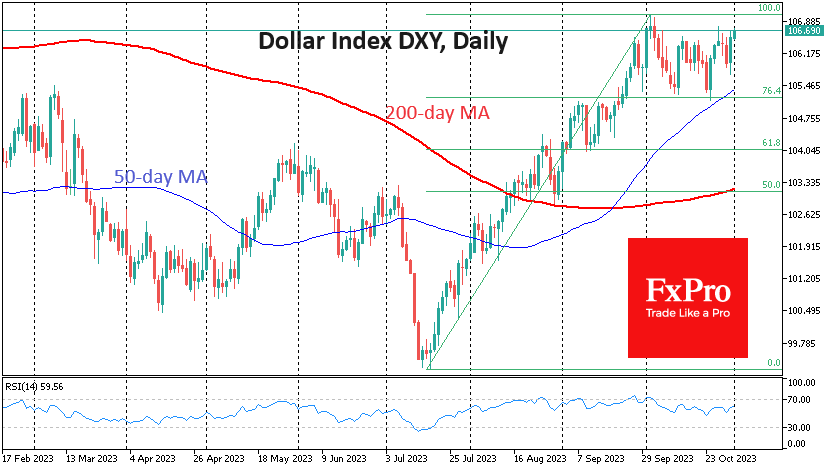

- EUR/USD rose around 50 pips, while 10y US Treasuries extended their rally with yields declining by 17bp throughout the session.

Powell delivered a balanced message with dovish undertones, as even the statement made it clear that the Fed is now closely following changes in financial conditions. Powell emphasized, that the rise in long-end yields needs to be both persistent and driven by higher term premium to influence monetary policy, but also that policy is already restrictive today.

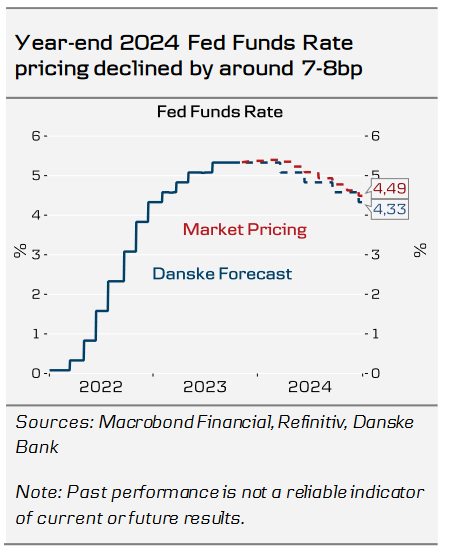

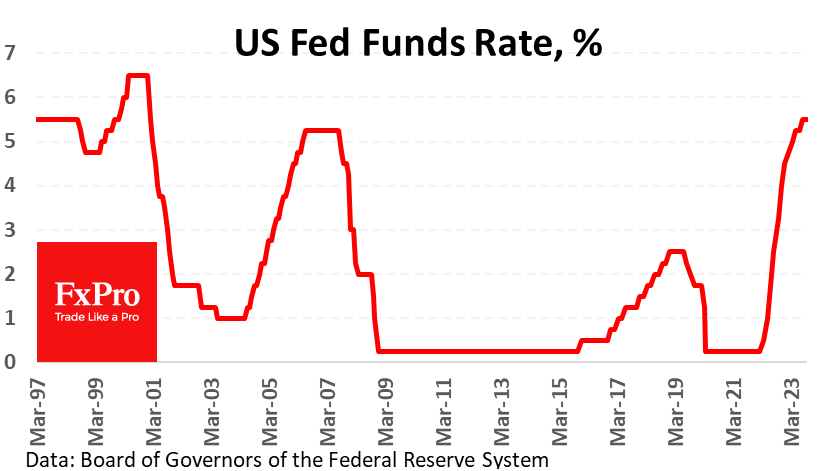

The Fed is not considering any changes to QT due to higher bond yields, as 'reserves are not even close to scarce at this point', which is in line with our thinking as well. We expect the Fed to continue QT at least into late 2024, and in any case well past the first rate cut, which we continue to pencil in for next March.

On the macro front, Powell chose to emphasize more balanced labour markets and cooling wage growth. Despite the recent upticks in both consumer survey and market-based inflation expectations measures, Powell was optimistic that inflation expectations remain 'in a good place'. In other words, while the recent upside data surprises provided Powell an option to deliver a more hawkish message, he did not consider it necessary.

As we also discussed in our Fed preview, 25 October, Powell noted that the lags of monetary policy transmission could be longer than before, as refinancing at higher rates will push companies' net interest costs higher gradually over the coming years. Following the weaker ISM Manufacturing survey for October, Atlanta Fed's GDP nowcast declined to 1.2%, down from the previous estimate of 2.3% and 4.9% growth in Q3. While we generally avoid putting too much emphasis on a single nowcast model, Atlanta Fed's estimate foresaw the acceleration in Q3 GDP clearly before analyst consensus. Housing and business investments are already responding to higher interest rates, and we still expect private consumption to follow suit towards the winter. As we see growth risks tilted to the downside, we stick to our call that the Fed is already done with rate hikes for now.

Markets: Persistence is the key

The cautious signals from Powell accelerated the decline in long US yields, which started earlier today following the release of the less dire than expected quarterly refunding statement and disappointing ISM Manufacturing. 10Y UST yields are down 17bp for the session, while the short end of the curve is less changed. Today's massive bond market rally underlines, why Powell mentioned the persistence of the move up in long yields as a key factor in terms of evaluating the economic impact. EUR/USD edged up by approximately 50 pips and we maintain our near-term bias for higher EUR/USD on the back of a turnaround in the exceptional run of positive US economic data surprises. On the longer horizon, we forecast EUR/USD at 1.06/1.03 in 6/12M.

Fed chair Powell press conference live stream

https://www.youtube.com/watch?v=wm4McpKTA7Y

Fed keeps interest rate unchanged at 5.25-5.50%, full statement

Fed keeps interest rates unchanged at 5.25-5.50% as widely expected, by unanimous vote.

Full statement below:

Recent indicators suggest that economic activity expanded at a strong pace in the third quarter. Job gains have moderated since earlier in the year but remain strong, and the unemployment rate has remained low. Inflation remains elevated.

The U.S. banking system is sound and resilient. Tighter financial and credit conditions for households and businesses are likely to weigh on economic activity, hiring, and inflation. The extent of these effects remains uncertain. The Committee remains highly attentive to inflation risks.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. In support of these goals, the Committee decided to maintain the target range for the federal funds rate at 5-1/4 to 5-1/2 percent. The Committee will continue to assess additional information and its implications for monetary policy. In determining the extent of additional policy firming that may be appropriate to return inflation to 2 percent over time, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments. In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities, as described in its previously announced plans. The Committee is strongly committed to returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Michael S. Barr; Michelle W. Bowman; Lisa D. Cook; Austan D. Goolsbee; Patrick Harker; Philip N. Jefferson; Neel Kashkari; Adriana D. Kugler; Lorie K. Logan; and Christopher J. Waller.

(FED) Federal Reserve Issues FOMC Statement

Recent indicators suggest that economic activity expanded at a strong pace in the third quarter. Job gains have moderated since earlier in the year but remain strong, and the unemployment rate has remained low. Inflation remains elevated.

The U.S. banking system is sound and resilient. Tighter financial and credit conditions for households and businesses are likely to weigh on economic activity, hiring, and inflation. The extent of these effects remains uncertain. The Committee remains highly attentive to inflation risks.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. In support of these goals, the Committee decided to maintain the target range for the federal funds rate at 5-1/4 to 5-1/2 percent. The Committee will continue to assess additional information and its implications for monetary policy. In determining the extent of additional policy firming that may be appropriate to return inflation to 2 percent over time, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments. In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities, as described in its previously announced plans. The Committee is strongly committed to returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Michael S. Barr; Michelle W. Bowman; Lisa D. Cook; Austan D. Goolsbee; Patrick Harker; Philip N. Jefferson; Neel Kashkari; Adriana D. Kugler; Lorie K. Logan; and Christopher J. Waller.

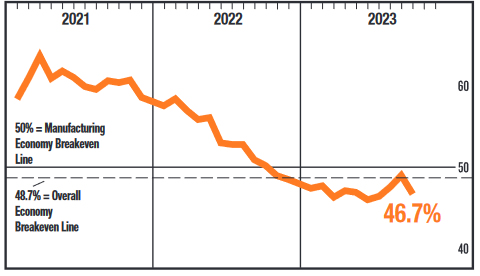

ISM Shows U.S. Manufacturing Sector Contraction Accelerated in October

The October ISM Manufacturing Index fell to 46.7, from 49.0 in September, falling short of the 49.0 markets had expected. This month's contraction was broad based with only two industries reporting growth.

The new orders sub-index pulled back 3.7 percentage points (pp) to 45.5, while new export orders remained in contraction territory (49.4) despite a month-on-month improvement. Softening demand conditions come as the employment index signaled a contraction (46.8) for the fourth time in five months.

Production was relatively unchanged from September as the index slipped 2.1 pp to 50.4. With falling new orders and stable production, the backlog of orders sub-index registered 42.2 – falling for the 13th month in a row.

The prices paid sub-index (45.1) continues to reflect softening raw materials prices.

Key Implications

October's manufacturing sector report gives back some of the upside surprises from September's release, falling back to the low ebb earlier this year. Looking at the details, broad-based weakness in the manufacturing sector persists as new orders contract, while employment growth has stalled out.

The sharp reversal in this month's report reflects a sector that continues to struggle to regain its footing after a deluge of Fed rate hikes. Amid falling demand, supply conditions have loosened considerably, and sagging raw materials prices are easing cost pressures. These factors should help mitigate the upside to consumer goods prices inflation.

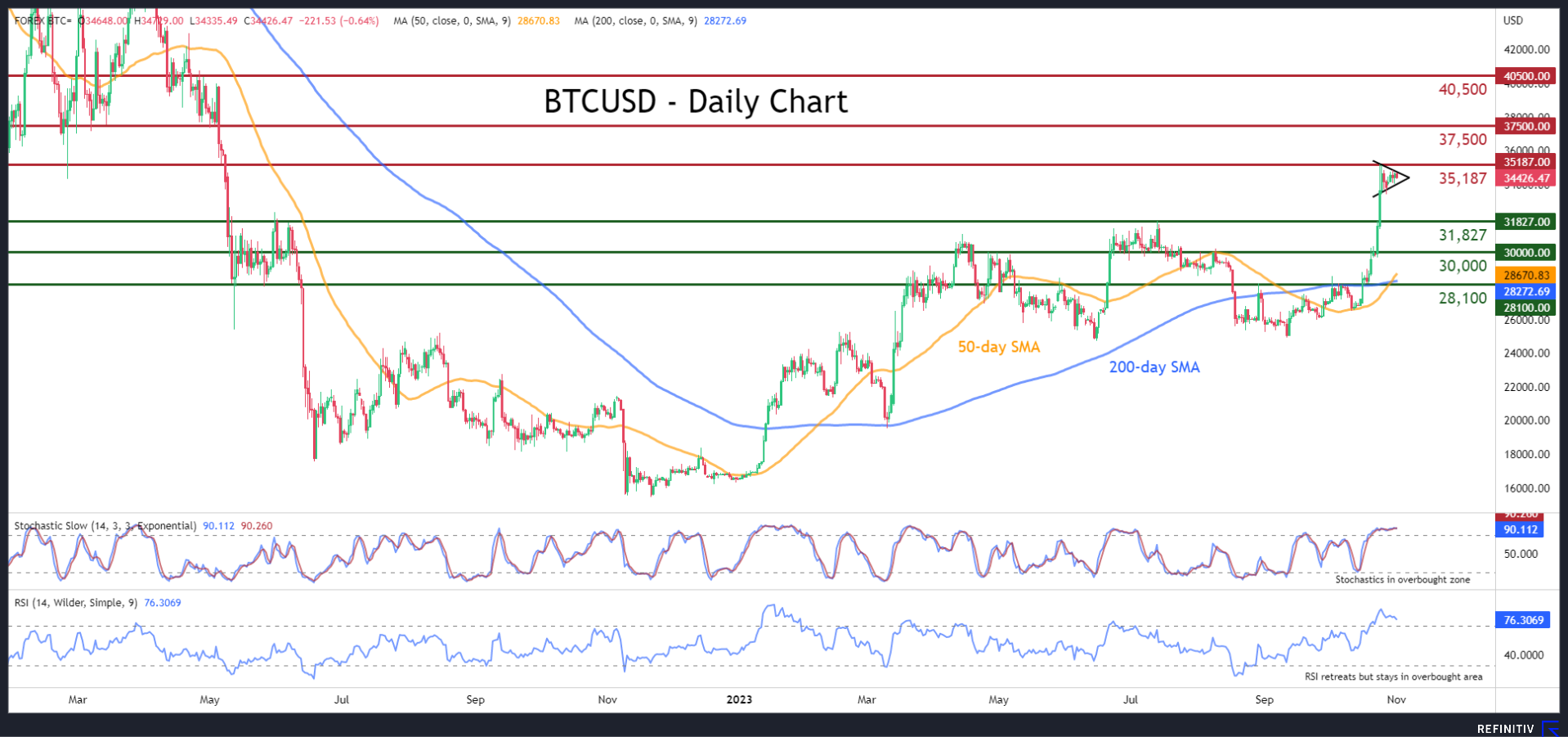

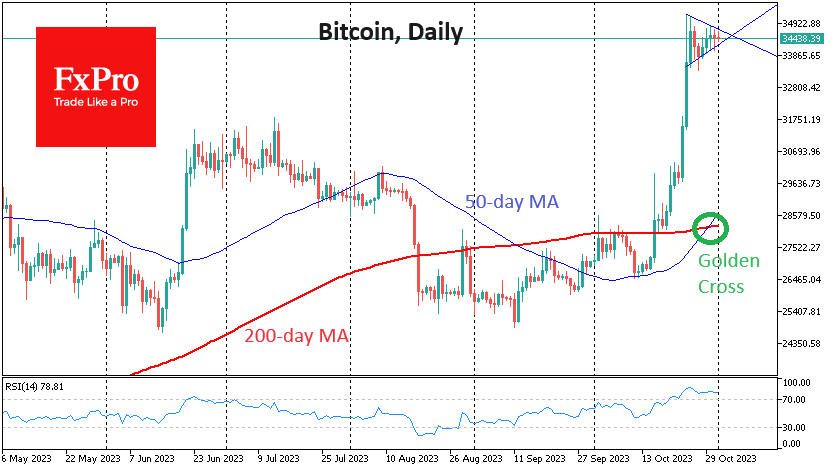

BTCUSD Consolidates Below its 18-month Peak

- BTCUSD surged above 35,000 to its highest since May 2022

- Has been flat since then, forming a pennant pattern

- Momentum indicators remain within overbought territories

BTCUSD (Bitcoin) has experienced a massive rally driven by speculation around the approval of spot-Bitcoin ETFs, which sent the price to a fresh 18-month high of 35,187. However, the leading cryptocurrency has been trading sideways in the past seven days, with the formation of a pennant hinting at an impending breakout.

Given that the short-term oscillators are suggesting an overstretched advance, the price could reverse lower towards the previous resistance of 31,827, which also held strong in June 2022. A violation of that zone could shift the spotlight to the 30,000 psychological mark. Failing to halt there, the king of cryptos could descend towards the 28,100 hurdle.

On the flipside, if the pennant pattern breaks to the upside, the bulls could aim for the 18-month high of 35,187. Even higher, the inside swing low of $37,500 registered in May 2022 could prove to be a tough obstacle for the price to overcome. Further upside attempts may then cease around 40,500, which acted as both support and resistance in the first half of 2022.

Overall, BTCUSD has been trading within a range in the past week, but its technical setup is warning of a potential spike. Can the recent completion of a golden cross between 50- and 200-day simple moving averages (SMAs) propel the price deeper into overbought territories?

US ISM manufacturing plummets to 46.7, longest contraction streak since Great Recession

In an alarming development for the US economy, ISM Manufacturing PMI for October has nosedived to 46.7, a stark contrast from last month's 49.0 and shattering expectations which had anticipated it to remain steady. This marks the twelfth month in a row where the PMI has stayed below the critical 50-point mark, signaling a contraction in manufacturing activity. This persistent downturn is reminiscent of the distressing times during the 2007-2009 Great Recession.

Digging deeper into the data, new orders saw a decrease, moving from 49.2 to 45.5. This now marks the 14th month where new orders have contracted. Production levels, too, experienced a decline, sliding from 52.5 to a borderline 50.4. Employment metrics were not immune either, plummeting from 51.2 to 46.8. However, there was a minor uptick in prices, which moved from 43.8 to 45.1.

The ISM's statement offered some insight into the broader implications of this data. They pointed out, "The correlation between the Manufacturing PMI and the entirety of the US economy suggests that the October reading of 46.7 percent equates to a decrease of minus-0.7 percent in real GDP, when viewed on an annualized basis."

Fed Needs to be Seriously Hawkish to Avoid More Hikes

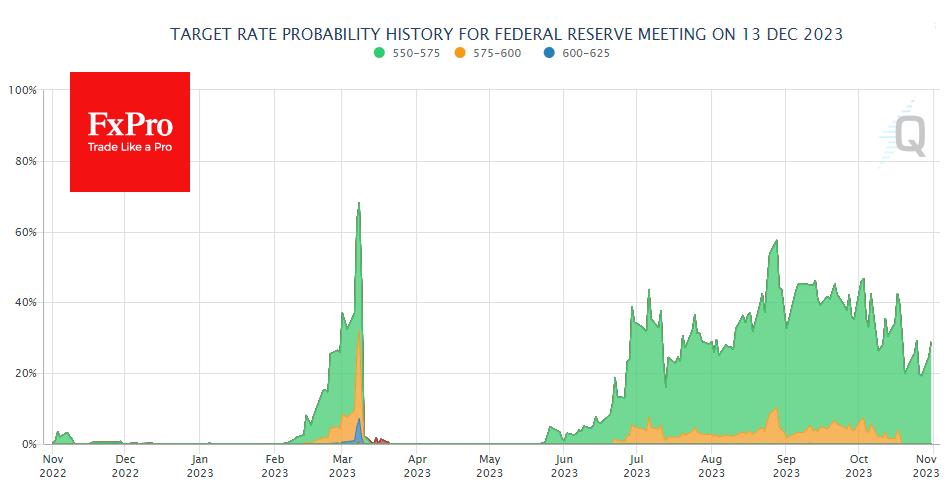

The rate decision and the Fed’s comments promise to be the highlight in a week full of releases. The market is in no doubt that the pause in policy tightening is here to stay, with interest rate futures pricing in a near 100% probability of a hike. Comments from Fed officials in recent weeks have removed all intrigue, showing a consensus for keeping policy on hold to gather more data.

All the intrigue and potential for market movement is focused on sentiment about the path forward. According to the latest data, markets are pricing in a 27% probability of a December hike, which was as low as 20% recently.

Meanwhile, the US economy continues to churn out much stronger-than-expected numbers and gain momentum. Just look at the GDP growth rate of almost 4.9% in the last quarter; before the pandemic, we last saw this in 2014. What a stark contrast to expectations of a recession!

In such an environment, Fed chief Jerome Powell has little choice but to continue threatening the markets with a willingness to raise interest rates even further if inflation picks up. And these potential threats, it seems to me, should be open enough to reach markets that do not believe in further hikes and are pricing in a first cut as early as next summer.

These are perfectly reasonable predictions, but they require a sharp cooling soon to materialise. And that requires scaring the markets beyond belief. If Powell can convince the markets at the press conference that he is not bluffing when he threatens another hike, that will be the best news for the dollar.

The US dollar was in a slow but steady rally until early October. The dollar index paused while awaiting critical economic data and central bank decisions. This situation paved the way for movement in both directions.

Therefore, in the event of a real threat of a rate hike, the US dollar rally may get a second wind, and we will see both the initial strong momentum and the subsequent smooth rise on the renewed carry trade.

Tighter monetary policy will also be good news for the US bond market, in our view. It has recently suffered from falling bond prices (rising yields) for long-term bonds. However, raising short-term rates will increase the odds of an economic slowdown by lowering long-term rates, which means higher bond prices. And that’s what the Fed and the Treasury need right now.

The main question, in our view, is whether Powell will be able to convince the Fed that his threats are serious (if they are, of course), given that the credibility of the Fed chairman’s words has been undermined by his rhetoric being too hawkish in 2018 and too soft in 2021. In the former case, he promised more rate hikes when the market was already signalling that it was coming apart at the seams.

The collapse in equities and the turmoil in the interbank lending market forced a change of course. The more recent episode of “transitory inflation” is perhaps something everyone remembers. This is why the Fed now finds it challenging to manage market expectations and must do more than it could with greater credibility.

Seasonality on Bitcoin’s Side in November

Market picture

October was the second best-performance month for Bitcoin this year after January. BTC soared 27% to highs over the past year and a half above $34K.

Regarding seasonality, November is considered a moderately successful month for BTC. Over the past 12 years, Bitcoin has ended the month on seven occasions with an average gain of 24%. In cases of decline, the average drop was 17%.

The “Golden Cross” on Bitcoin’s daily timeframes was formed at the end of October thanks to the price rally in the second half of the month. But this event did not trigger further buying. The same was true with the “Death Cross” in September, which came the day after the local price bottom.

After crossing the $34K mark, the early phase of the bull market began, according to Look Into Bitcoin. Pointsville founder Gabor Gurbach cited the increased presence of institutionalisation as the main driver of further growth.

News background

Trader Rekt Capital is not so optimistic. After halving, he expects consolidation in the range of $24K-$30K and only later an exit on the parabolic growth to the six-digit marks.

Billionaire Stanley Drakenmiller called Bitcoin “gold for the young.” He said that while he regrets not owning BTC, he prefers investing in gold.

It is the 15th anniversary of the Bitcoin white paper. On 31 October 2008, a person (or group of people) under Satoshi Nakamoto’s pseudonym published the Bitcoin white paper. The nine-page technical document described the principle of operation of the peer-to-peer payment system, which later revolutionised the world of financial technology.

Crypto exchange Bittrex has received court approval for a revised bankruptcy plan and winding down operations in the US. Bittrex Global continues to operate outside of the US.

Attackers hacked a popular Telegram bot to track transactions on the decentralised exchange Uniswap. Against this background, the price of the native token UNIBOT fell by more than 40%.