Sample Category Title

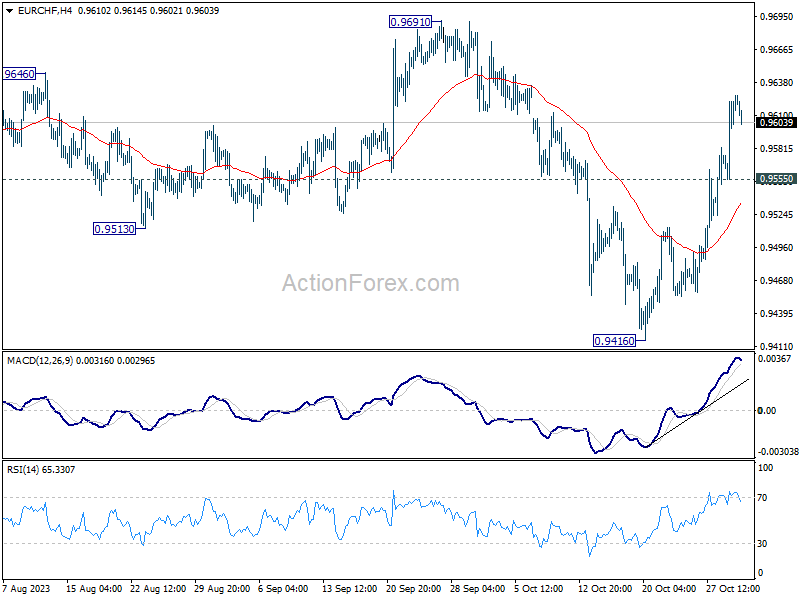

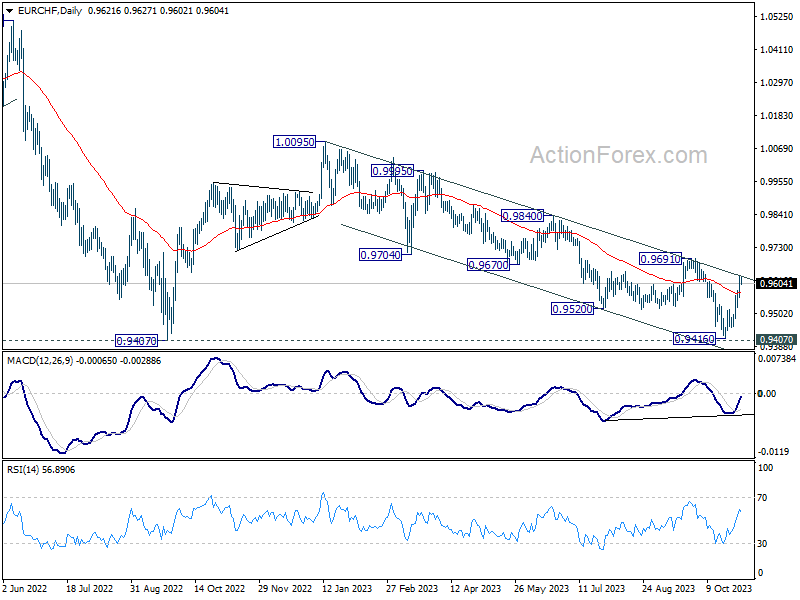

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9580; (P) 0.9605; (R1) 0.9652; More...

EUR/CHF's rebound from 0.9416 is still in progress and intraday bias stays on the upside. Further rally would be seen to 0.9691 key structural resistance. Firm break there will carry larger bullish implication. On the downside, though, below 0.9555 minor support will turn intraday bias neutral first.

In the bigger picture, down trend from 1.2004 (2018 high) is still in progress. Decisive break of 0.9407 will confirm resumption, and target 61.8% projection of 1.1149 to 0.9407 from 1.0095 at 0.9018. On the upside, break of 0.9691, however, will indicate medium term bottoming just ahead of 0.9407. Further rally could then be seen back towards 1.0095 resistance.

EUR/USD Resumes Drop, USD/JPY Extends Surge

EUR/USD is again moving lower below the 1.0615 support. USD/JPY surged and broke the 151.00 resistance zone.

Important Takeaways for EUR/USD and USD/JPY Analysis Today

- The Euro started a fresh decline below the 1.0675 support zone.

- There was a break below a key bullish trend line with support at 1.0570 on the hourly chart of EUR/USD at FXOpen.

- USD/JPY climbed higher above the 150.00 and 151.00 levels.

- There was a break above a major bearish trend line with resistance at 149.85 on the hourly chart at FXOpen.

EUR/USD Technical Analysis

On the hourly chart of EUR/USD at FXOpen, the pair remained in a bearish zone below the 1.0700 level, as mentioned in the previous analysis. The Euro declined below the 1.0615 support zone against the US Dollar.

The pair even settled below the 1.0595 zone and the 50-hour simple moving average. More importantly, there was a break below a key bullish trend line with support at 1.0570. A low is formed near 1.0557 and the pair is now consolidating losses.

On the upside, the pair is now facing resistance near the 23.6% Fib retracement level of the recent decline from the 1.0675 swing high to the 1.0557 low at 1.0585.

The next key resistance is near the 50-hour simple moving average at 1.0595. The first key resistance is the 50% Fib retracement level of the recent decline from the 1.0675 swing high to the 1.0557 low at 1.0615.

A clear move above the 1.0615 level could send the pair toward the 1.0675 resistance. An upside break above 1.0675 could set the pace for another increase. In the stated case, the pair might rise toward 1.0750.

If not, the pair might resume its decline. The first major support on the EUR/USD chart is near 1.0560. The next key support is at 1.0525. If there is a downside break below 1.0525, the pair could drop toward 1.0500. The next support is near 1.0485, below which the pair could start a major decline.

USD/JPY Technical Analysis

On the hourly chart of USD/JPY at FXOpen, the pair started a strong increase from the 148.80 zone. The US Dollar gained bullish momentum above 150.00 against the Japanese Yen.

It settled above the 50-hour simple moving average and 151.00. However, the pair struggled to clear the 151.75 zone. It is now correcting gains from the 151.70 high. There was a move below the 151.50 level.

On the downside, the first major support is near the 23.6% Fib retracement level of the upward move from the 148.80 swing low to the 151.70 high. The next major support is near the 50-hour simple moving average at 150.25.

The 50% Fib retracement level of the upward move from the 148.80 swing low to the 151.70 high is also at 150.25. If there is a close below 150.25, the pair could decline steadily.

In the stated case, the pair might drop toward the 149.90 support zone. The next stop for the bears may perhaps be near the 148.80 region.

Immediate resistance on the USD/JPY chart is near the 151.70 zone. The first major resistance is near 152.00. If there is a close above the 152.00 level and the RSI stays above 50, the pair could rise toward 152.20. The next major resistance is near 154.00, above which the pair could test 155.00 in the coming days.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Don’t Expect Fed to Stop Amid Strong Growth, Higher Inflation

The US dollar was bid on Tuesday thanks to a rapid selloff in the Japanese yen, after the Bank of Japan (BoJ) announced mini policy loosening steps that didn’t find buyers. Loosening the upper limit on the 10-year JGB yield in the context of a YCC policy is not enough when considering that the BoJ should drop it altogether and for good.

But on the contrary, not only that the BoJ is not giving up on its YCC policy, but is on track to match its record annual bond purchases. Almost all the Japanese 10-year bonds are held by the BoJ – which in my opinion will become illegal one day - and the BoJ hasn’t yet moved an inch towards normalization of its rate policy whereas the major central bank rate hikes start plateauing after more than a 1.5 year of aggressive rate hikes. So, no wonder the yen got smashed yesterday. The USDJPY spiked past 151, even though the uptick in the US - Japan 10-year yield spread – which also ticked up because of a jump in the Japanese 10-year yield, didn’t attract the yen longs. The only thing that holds traders back from more aggressive selling is the fear of a direct FX intervention. If that happens, there is a good reason to buy a dip.

Zooming out of Japan, the US dollar index consolidated a touch below last month peak. The US consumer confidence index dropped to a 5-month low, but the latest wages data continued to give signs of strength. Yes strength – I am sorry. The employment cost index, a top-notch gauge of what employers spend on compensation, rose 1.1% in Q3 – slightly higher than a quarter earlier. Wages and salaries rose 4.6% - above the US headline CPI, and well above 3% as before the pandemic. And that was before the UAW reached a jaw-dropping deal with Detroit’s 3 carmakers where they nailed a 25% increase in wages and around 150% increase in compensations for the low-paid tier of temporary workers. The ADP data is expected reveal around 150K new private job additions in October, and JOLTS data is expected to show a drop in job openings. On Friday, we will have a look at the official figures. The latter won’t impact the Federal Reserve (Fed) expectations for this week’s policy decision. But any further strength in US jobs data will reinforce a potentially hawkish stance from the Fed policymakers this week.

The Fed

We know that the Fed is not done hiking the interest rates. We know that Jerome Powell won’t call the end of the policy tightening after seeing a blowout growth data – which showed that the US GDP grew almost 5% in Q3 (that’s more than China!), and inflation ticked higher because Americans kept spending. Duh! And if people kept spending their savings it was because they didn’t necessarily feel threatened to lose their jobs, or remain jobless for long. So yes, the jobs market strength is playing tricks on the Fed, and it’s clearly not loose enough. The chances are that we won’t hear anything soothingly dovish. ‘The higher yields help us do the job’ is the best it will get.

You know where growth is not strong?

China is not doing brilliant and this week’s economic data in China showed that the Chinese factory sector slipped back into contraction and the Eurozone economies announced gloomy GDP updates, as well. The German economy contracted in Q3, the French and Italian economies stagnated, the overall Eurozone growth fell 0.1% on a quarterly basis.

But at least, inflation slowed. As a result of soft growth and inflation data, the EURUSD couldn’t extend gains above the 50-DMA and sank below the 1.06 level yesterday. The positive trend is losing momentum, the divergence between the strength of the US economy versus its European counterparts, and the divergence between the Fed and the European Central Bank (ECB) outlooks play in favour of a deeper depreciation in the euro against the greenback.

Crude approaching $80pb crossroads

US crude slipped below its 100-DMA yesterday as buyers became rare on news that Israel’s ground offensive is not as violent as expected. A 1.3mio barrel build in US crude inventories may have helped the bears to push the selloff below the $82pb level. Yet, oil bears will certainly hit a decent support near the $80p level because at this level, they know that Saudi has their back. And the risks of geopolitical nature remain clearly tilted to the upside. For those who bet that we will see a dip near the $80pb level, it is soon time to roll up the sleeves.

Worst since the pandemic, and yet

The S&P 500 rose on the last day of October but recorded its longest monthly slide since the pandemic. Still, the index kicks off the new month a touch above the major 38.2% retracement which should distinguish between the continuation of last year’s rally, and a slide into the medium-term bearish consolidation zone. The next direction will depend on whether the US yields will consolidate and eventually come lower, or they will continue their journey higher. In the second scenario, we will likely see major US stock indices sink into a bearish trend.

Fed in Focus

Market movers today

The key market mover today will be the FOMC meeting tonight. We expect the Fed to stay on hold in line with consensus and market expectations, and look for no further hikes at a later stage either. As higher term premiums drive the tightening in financial conditions, Fed chair Powell could take a more cautious stance in his remarks. With markets fully priced for an unchanged rate decision and no updated economic projections, all eyes will be on Powell's forward guidance. See Fed preview: Near-term bloom, long-term gloom?, 25 October. Notice that due to the shift to standard (winter) time, the rate decision tonight will be announced at 19:00 (CET) with Powell speaking at 19:30 (CET).

Ahead of the meeting we get both ISM manufacturing and the JOLTS report from the US. It will be particularly interesting to see the number of job openings after a surprising spike higher in September. It will also be worth keeping an eye on the ADP report, because markets often seem to ignore that it is not a very good indicator of where non-farm payrolls are headed.

In Sweden and Norway we will look out for PMI manufacturing data.

The 60 second overview

Europe: Eurozone inflation came in lower than expected in the preliminary data for October. Headline HICP fell 0.15% m/m on a seasonally adjusted basis, which translated into a decline in the annual inflation rate from 4.3% to 2.9% (consensus: 3.1%). Core inflation increased around 0.2% m/m for the second consecutive month, which is the lowest two-month average since the spring 2022. The disinflationary trend in the Eurozone continues, though ECB will still look for further signs of softening price pressures - especially in services, where the inflation rate rose to 0.27% m/m in October. Additionally, the first release of Q3 GDP data showed the Eurozone economy declining by 0.1% vs. +0.2% in Q2. The October PMIs indicate that the weakness has continued into Q4.

US: The Conference Board measure of US consumer confidence fell from 103 to 102.6 in October, which was slightly above consensus. The assessment of the current situation edged lower, while expectations remained subdued. The survey indicated a worsening in 6-month consumer expectations on employment, business conditions and income. The assessment of job availability (plentiful vs. not plentiful) continued to soften, though remaining high relative to the historical mean. In a separate release, the Employment Cost Index for Q3 rose 1.1% q/q (consensus 1%) with wages rising 1.2% vs. 1% in Q2. Wage growth is still well above the level consistent with the inflation target, underlining the strong labour market as the most important challenge for monetary policy to address.

China: Overnight, the Caixin manufacturing PMI for China fell from 50.6 to 49.5 in October (consensus: 50.8). This mirrors the move in the official gauge, which also fell back in contractionary territory earlier this week. The New Orders component remained weak with export orders falling for the fourth month in a row. Recent hard data for retail sales and industrial production has been better than expected, but the foundation for the economic recovery still seems fragile. Especially, as the housing crisis is still not resolved. Until it is, China will continue to rely on stimulus measures. On a separate note, the White House yesterday announced an upcoming meeting in November between Biden and Xi.

Equities: Equities were higher for a second day on Tuesday. No obvious drivers but for oversold conditions, yields volatility coming down and expectations for the Fed meeting tonight. S&P closed 0.7% higher and Stoxx 600 0.6%. It was an odd sector mix of real estate, banks and utilities outperforming. Again, illustrating that this was not a clear risk-on session but a rather defensive one. US futures are dipping into negative this morning.

FI: Long European bond yields ended slightly lower yesterday as Eurozone inflation came in below expectations. 10Y Bund yields was down close to 7bp in the morning, though the rally lost some steam following the release of strong ECI wage figures from the US in the afternoon. The 10Y UST yield ended the day marginally higher.

FX: Despite recovering risk sentiment (according to equities), yesterday was characterized by 'safe-have' strength within FX as USD, CHF and JPY (overnight) outperformed rest of G10. The Japanese ministry of finance is said to be "on standby" to intervene, which helped JPY to recover some lost ground over night. Scandies are still struggling, but the EUR/Scandie rallies seem to have stalled (for now) just above 11.80.

Credit: Credit markets benefitted from the betterment in overall risk sentiment, with iTraxx Xover tightening almost 15bp to 450bp and Main close to 3bp, thus closing in 85bp. Primary activity remained muted as issuers and investors were probably awaiting the release of the Eurozone CPI figures, which could provide a good window for issuers today.

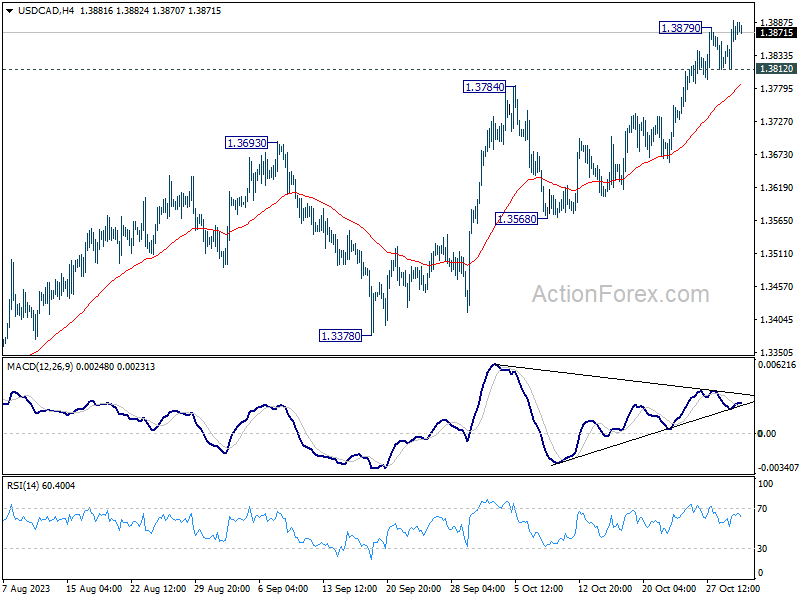

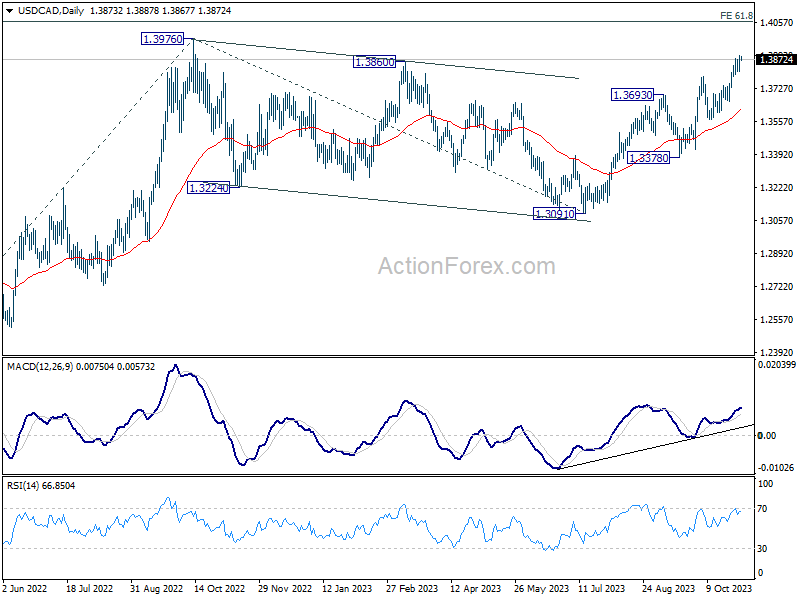

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3829; (P) 1.3860; (R1) 1.3907; More...

USD/CAD's rally resumed after brief retreat and intraday bias is back on the upside. Current rally should target retest on 1.3976. Decisive break there will resume larger up trend to 1.4064 projection level. On the downside, below 1.3812 minor support will turn intraday bias neutral again.

In the bigger picture, corrective pattern from 1.3976 (2022 high) should have completed with three waves down to 1.3091. Decisive break of 1.3976 high will confirm resumption of up trend from 1.2005 (2021 low). Next target will be 61.8% projection of 1.2401 to 1.3976 from 1.3091 at 1.4064. This will now remain the favored case as long as 1.3568 support holds.

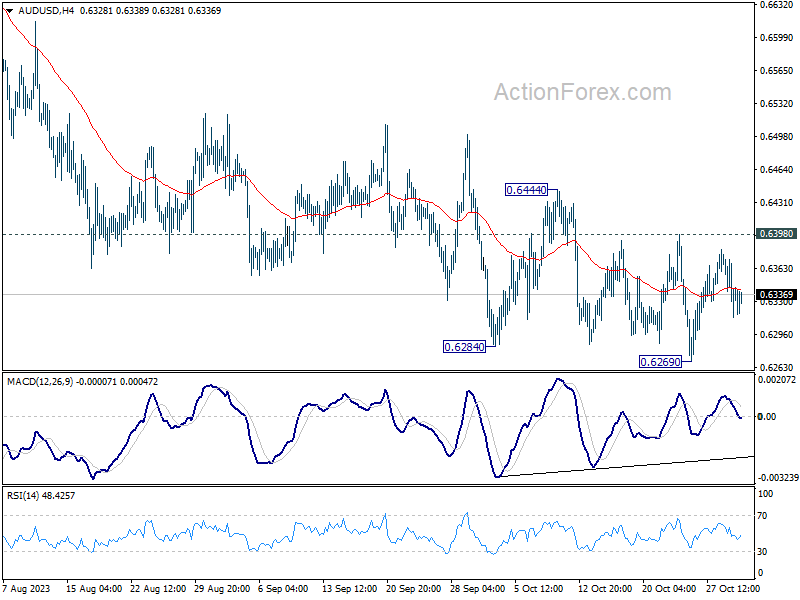

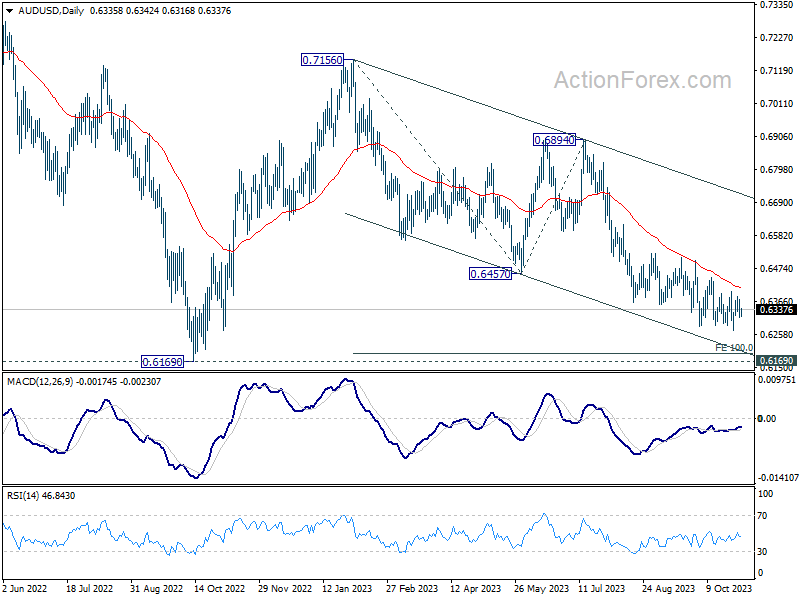

AUD/USD Daily Report

Daily Pivots: (S1) 0.6309; (P) 0.6343; (R1) 0.6372; More...

Range trading continues in AUD/USD and intraday bias stays neutral. Outlook remains bearish with 0.6398 resistance intact. On the downside, break of 0.6269 will resume larger fall from 0.7156 to 100% projection of 0.7156 to 0.6457 from 0.6894 at 0.6195, which is close to 0.6169 medium term support.

In the bigger picture, down trend from 0.8006 (2021 high) is possibly still in progress. Decisive break of 0.6169 will target 61.8% projection of 0.8006 to 0.6169 to 0.7156 at 0.6021. This will now remain the favored case as long as 0.6894, in case of strong rebound.

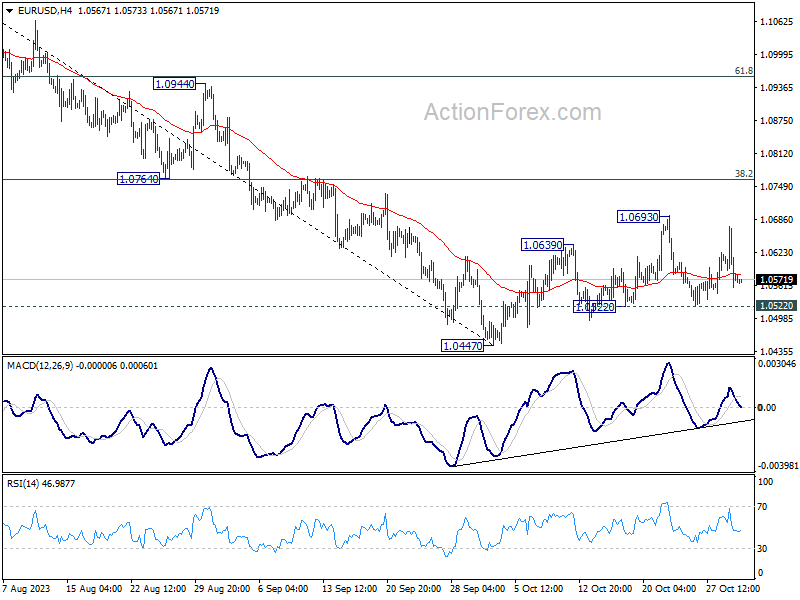

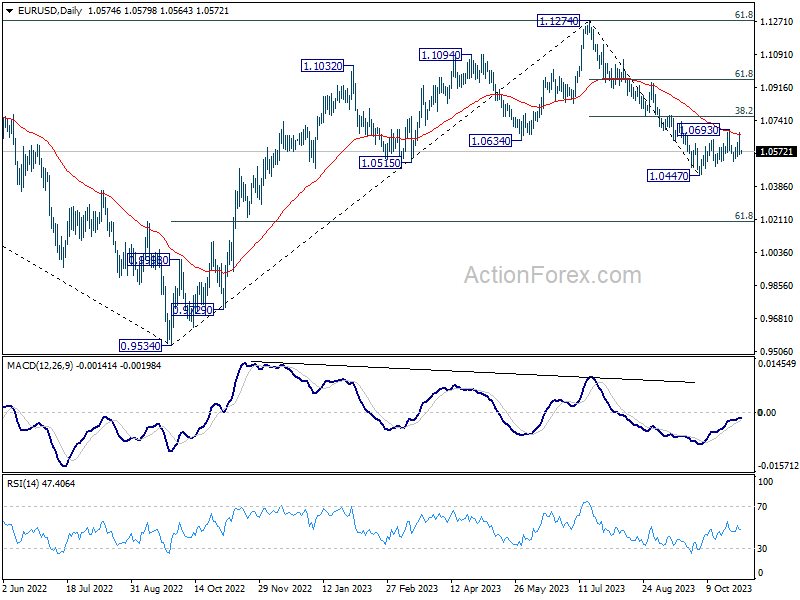

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0531; (P) 1.0603; (R1) 1.0648; More...

Intraday bias in EUR/USD remains neutral for the moment. On the downside, break of 1.0522 support will turn bias back to the downside for retesting 1.0447 low. Break there will resume larger fall from 1.1274. On the other hand, strong bounce from current level, followed by break above 1.0693, rebound from 1.0447 to 1.0764 cluster resistance (38.2% retracement of 1.1274 to 1.0447 at 1.0763).

In the bigger picture, fall from 1.1274 medium term top could still be a correction to rise from 0.9534 (2022 low). But chance of a complete trend reversal is rising. In either case, current fall should target 61.8% retracement of 0.9534 to 1.1274 at 1.0199 next. For now, risk will stay on the downside as long as 55 D EMA (now at 1.0665) holds, in case of rebound.

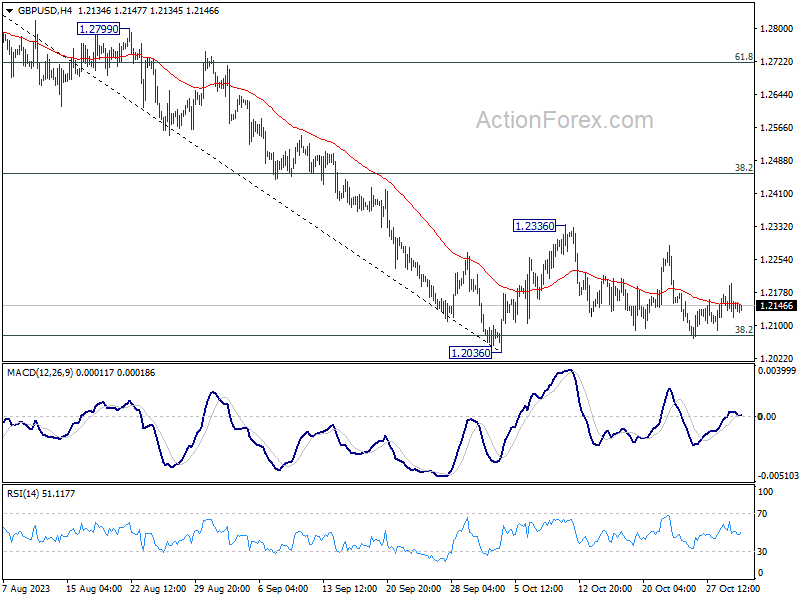

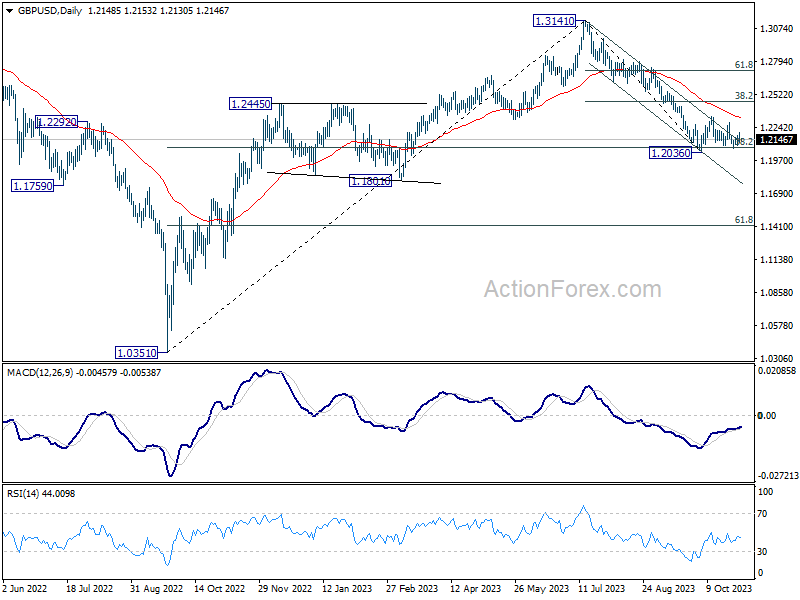

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2112; (P) 1.2157; (R1) 1.2193; More

Range trading continues in GBP/USD and intraday bias stays neutral. With 1.2336 resistance intact, downside breakout is expected. On the downside, firm break of 1.2036 will resume whole decline from 1.3141 for 1.1801 support next. However, break of 1.2336 will turn bias back to the upside for 38.2% retracement of 1.3141 to 1.2036 at 1.2458.

In the bigger picture, fall from 1.3141 medium term top could still be a correction to up trend from 1.0351 (2022 low) only. But risk of complete trend reversal is rising. Sustained break of 38.2% retracement of 1.0351 to 1.3141 at 1.2075 will pave the way to 61.8% retracement at 1.1417. For now, risk will stay on the downside as long as 55 D EMA (now at 1.2346) holds, in case of rebound.

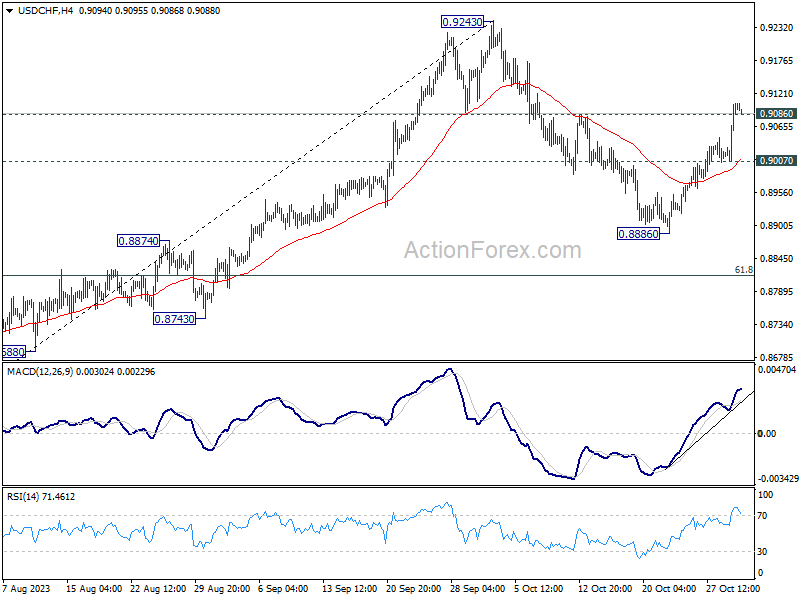

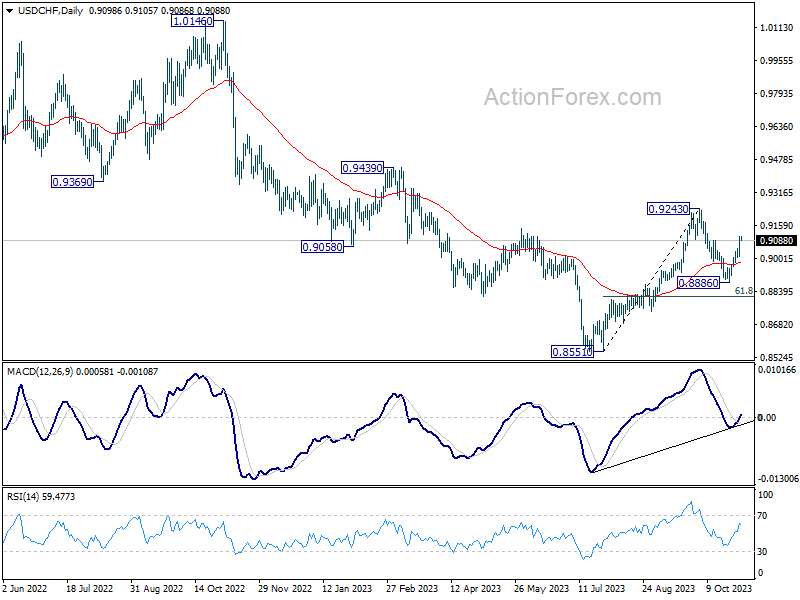

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9040; (P) 0.9074; (R1) 0.9139; More....

Intraday bias in USD/CHF stays on the upside at this point. Sustained trading above 0.9086 resistance will pave the way back to 0.9342 resistance next. On the downside, below 0.9007 minor support will turn intraday bias neutral first.

In the bigger picture, outlook is mixed up by the deeper than expected pull back from 0.9243. Yet there was no follow through selling after hitting 0.8886. On the upside, break of 0.9243 resistance will revive the case of medium term bottoming at 0.8851, and turn outlook bullish. However, sustained break of 61.8% retracement of 0.8551 to 0.9243 at 0.8815 will argue that larger decline from 1.0146 is ready to resume through 0.8551 low.

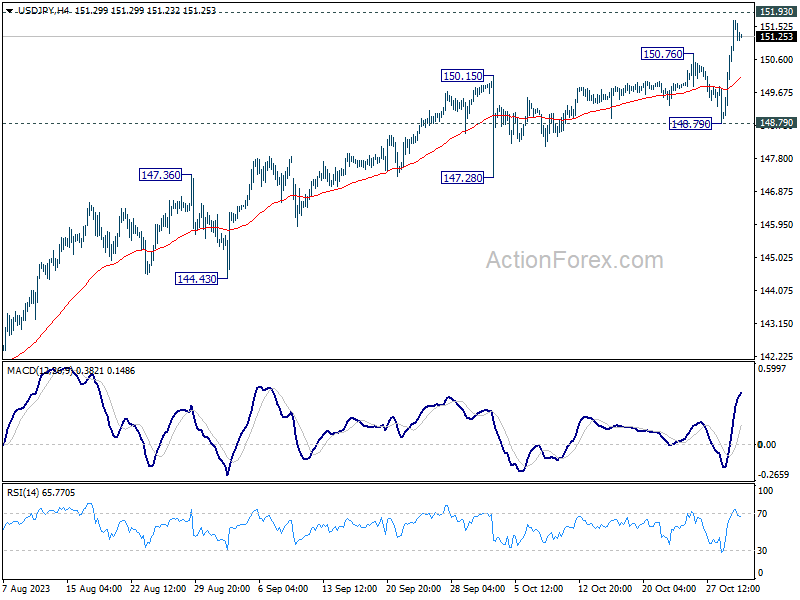

USD/JPY Daily Outlook

Daily Pivots: (S1) 149.87; (P) 150.80; (R1) 152.56; More...

Intraday bias in USD/JPY remains on the upside for 151.93 key resistance. Firm break there will target 100% projection of 129.62 to 145.06 from 137.22 at 152.66. For now, break of 148.79 support is needed to indicate short term topping. Otherwise, outlook will stay bullish in case of retreat.

In the bigger picture, immediate focus is now on 151.93 resistance (2022 high). Rejection by 151.93, followed by sustained break of 145.06 resistance turned support will argue that rise from 127.20 has completed, and turn outlook bearish for 137.22 support and below. However, sustained break of 151.93 will confirm resumption of long term up trend. Next target will be 61.8% projection of 102.58 to 151.93 from 127.20 at 157.69.