Sample Category Title

NZ First Impressions: Labour Market Statistics

Unemployment rose 0.3ppts to 3.9% in the September quarter, in line with our expectations. Private sector wage growth remained high by historical norms, but shows clear signs of easing.

- Unemployment rate: 3.9% (prev: 3.6%, Westpac f/c: 3.9%, RBNZ f/c 3.8%)

- Employment change: -0.2% (prev: +1.0%, Westpac f/c: +0.4%, RBNZ f/c +0.3%)

- Labour costs (private sector): +0.9% (prev: 1.1%, Westpac f/c: 1.0%, RBNZ f/c 1.0% )

- Average hourly earnings (private sector, ordinary time): +2.0% (prev: 1.9%)

Employment fell 0.2% in the September quarter, causing annual growth to slow to 2.4 from 4.1% previously. This was a weaker outcome than suggested by the tax-based Monthly Employment Indicator (this rose 0.4% during the quarter). This might reflect genuine differences in coverage and definition between the two indicators – the MEI counts filled jobs rather than people employed and does not cover the self-employed. However, it is also possible that the unexpected weakness reflects variability in the survey sample (new respondents are rotated into the survey each quarter). On that note, also surprising was a 0.4ppts decline in the labour force participation rate to 74.0%. As a result of that decline, the estimated labour force barely grew in the September quarter despite continued strong migrant inflows and a 0.6% increase in the working age population.

But as is usually the case, differences in survey sample tend to wash out in the unemployment rate, which increased 0.3ppts to 3.9 in the September quarter – the highest reading since June quarter 2021 and an outcome that was in line with our expectations and those of the market. Also of note, a broader measure of unemployment known as the underutilisation rate – which amongst other things also captures those people that would like more work – increased by a 0.5ppts to 10.4%. So whether or not employment growth was really as soft as suggested by today’s report, it remains the case that there has been an unambiguous easing of conditions in the labour market – an outcome that was clearly foreshadowed by business survey indicators of skill shortages and labour constraints.

With the unemployment rate now well above the historic lows seen last year, wage growth is showing clear signs that it has peaked. The overall Labour Cost Index (LCI) rose 1.1% for the quarter, leaving the annual growth rate at 4.3%. However, as we expected, that result reflecting large settlements in parts of the public sector (such as healthcare), with the public sector LCI increasing 2.2% during the September quarter, lifting annual growth to 5.4%. We do not expect these settlements to continue in the future.

More importantly for the RBNZ, the LCI for the private sector increased just 0.9% in the September quarter, lowering annual growth by 0.2ppts to 4.1% (and a peak of 4.5% in the March quarter). This outcome was 0.1ppts weaker than we had expected. The unadjusted LCI – which better represents developments in take-home pay – increased 1.1%. This was the smallest increase since the December 2021 quarter, and lowered annual growth by 0.4ppts to 5.7% (thus tracking broadly in line with CPI inflation of 5.6%). Annual growth in private sector average hourly earnings, as measured by the more volatile Quarterly Employment Survey, dropped back to 7.1% from 7.7% previously.

Today’s news should leave the RBNZ comfortable with the labour market projections made in the August Monetary Policy Statement, and thus a hike in the OCR at the 29 November meeting remains very unlikely (as reflected in market pricing). Employment growth was weaker than the RBNZ had forecast – at least at face value – and the unemployment rate rose by slightly above the 3.8% figure that the RBNZ had forecast. In addition, growth in the private sector LCI was also 0.1ppts less than the RBNZ had forecast.

Looking ahead, the RBNZ is forecasting the unemployment rate to rise significantly further to 4.4% by the end of this year (data to be released in early February). Together with the outcome of the December quarter CPI (released mid-January), ongoing developments in the labour market will have a significant bearing on whether the RBNZ continues to take the view that its inflation projections remain broadly on track. More robust than expected inflation and/or labour market data would increase the likelihood that the RBNZ opts to lift the OCR at the February 2024 MPS meeting (as is Westpac’s forecast).

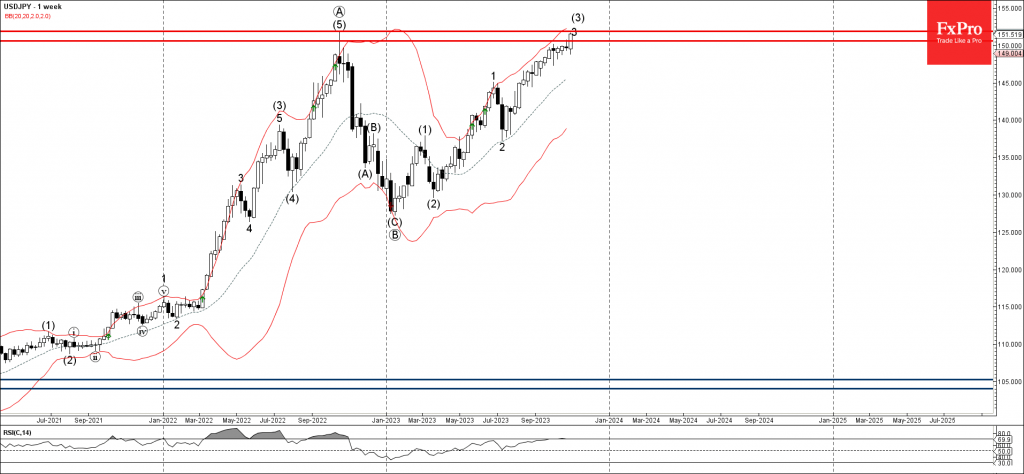

USDJPY Wave Analysis

- USDJPY broke key resistance level 150.85

- Likely to rise to resistance level 151.90

USDJPY recently broke the key resistance level 150.85 (top of the previous daily Evening Star reversal pattern from last week).

The breakout of the resistance level 150.85 accelerated the active medium-term impulse wave (3) from the March.

Given the clear weekly and daily uptrend, USDJPY can be expected to rise further toward the next resistance level 151.90 (which stopped the weekly uptrend in 2022) – from where the downward correction is likely.

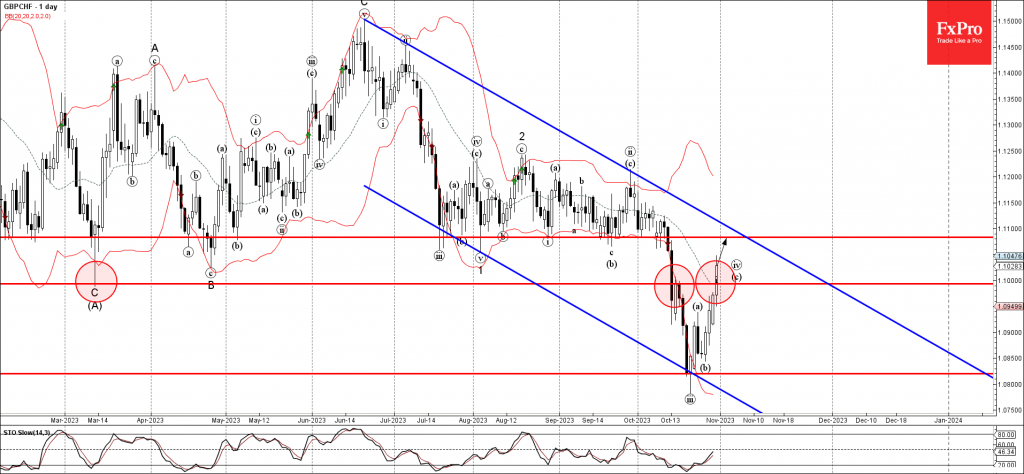

GBPCHF Wave Analysis

- GBPCHF broke key resistance level 1.1000

- Likely to rise to resistance level 1.1000

GBPCHF recently broke the key resistance level 1.1000 (top of the previous minor correction from the middle of October).

The breakout of the resistance level 1.1000 accelerated the c-wave of the active short-term ABC correction iv.

Given the strong Swiss franc sales seen across the FX markets today, GBPCHF can be expected to rise further toward the next resistance level 1.1000 (former multi-month support from July to September).

Eurozone Inflation Eases Further than Expected, US ECI a Minor Corncern, BoJ Tweak Triggers Yen Slide

Inflation in the eurozone fell below 3% in October, with energy and food prices helping to push the headline number even lower than expected. While this is undoubtedly good news, the core number is probably a more accurate reflection of where things stand and the job the ECB still has in reining in inflation in a sustainable manner.

Energy prices in particular are still volatile and base effects in the coming months will likely be less favourable. Underlying price pressures, particularly in services, still have a lot further to fall before the ECB can even consider cutting rates to support an economy that looks destined for recession.

US ECI beats expectations in a blow to the Fed

The euro initially rallied against the dollar after this morning's releases but that quickly changed following the release of the US quarterly employment cost index. While the 1.1% reading only represented a slight overshoot of the expected figure, that it's so closely monitored by the Fed will come as a setback to those hoping for rates to fall any time soon.

BoJ tweak sees yen spike above 150 against the dollar

The Bank of Japan is gradually phasing out its yield curve control policy tool, with the latest tweak allowing a little more flexibility in how far 10-year yields can trade around its 0% target. In other words, it's hoping a slow and steady abandoning of the tool will prevent unintended consequences.

While they've had some success in bond markets, the currency continues to suffer despite these tweaks ultimately being beneficial. Fighting the market at a time when other central banks are aggressively raising rates has triggered a huge depreciation in the yen forcing interventions from the Ministry of Finance.

With the yen trading back above 150 against the dollar, there'll be no shortage of speculation around the potential for another intervention. One argument against this could be that the BoJ is making moves to normalize their monetary policy approach but it's moving at such a gradual pace that the currency could suffer much more if more significant action is taken from either institution.

Oil steadies after very choppy trade over the last week

Oil prices have been relatively steady today considering how choppy they've been over the last week. While I doubt this period of volatility has passed, it is interesting crude prices have given up the bulk of their gains since Hamas attacked Israel which suggests either the geopolitical risk-premium has sharply reduced or global economic concerns have increased, perhaps a combination of the two. There's clearly still a lot of concern around events in the Middle East though and so oil prices will remain very sensitive to developments there.

Gold pushing $2,000 as yields ease

Gold is continuing to trade around $2,000, buoyed by safe-haven flows and easing shorter-term yields. While it is making brief moves above this major psychological level, it's failing to get any traction at this moment. That further reinforces how big a resistance level this is and if it can make a significant move above, it could accelerate as a result.

Sunset Market Commentary

Markets

The Bank of Japan brought the Japanese yen close towards new multidecade lows against the US dollar. USD/JPY pierced through 150 and then the 151 big figure. The couple rose to an intraday high of 151.95 in October last year before Japan turned to FX interventions. Ending the day at the current levels would nevertheless mean the strongest USD/JPY close since 1990. EUR/JPY rises beyond 160 for the first time since 2008. The yen is paying the price for the BoJ’s tedious normalization pace. It demoted the hard 1% yield cap on the 10-year tenor to merely a “reference”. It means the central bank won’t act on autopilot if yields move beyond that level. Markets are ready to test the BoJ’s resolve and sent yields in the country 1.1-5.5 bps higher. Japanese bond markets are actually an outlier compared to global peers. That makes today’s JPY move very telling. German yields ease 0.3 (2-y)-4.5 bps (30-y). European data were interesting more than they were meaningful to investors. The economy unexpectedly contracted in Q3 (-0.1% q/q). It keeps the possibility for a technical recession in 2023H2 which PMI-owner S&P Global warned for last week alive. October inflation in the bloc was softer than anticipated, with a 0.1% m/m increase leading to 2.9% y/y (from 4.3% in September). Very favourable base effects (energy-related) explain a lot of the sharp disinflation. Core CPI is much more sticky at 4.2% (from 4.5%) with services inflation even barely easing (4.6% from 4.7%). US yields fell between 4.4-9.3 bps at their lowest point of the day before suddenly spiking on an unexpected acceleration in the Employment Cost Index for Q3 (1.1%, up from 1% in Q2). Fed’s Powell has repeatedly said the ECI is one of the key indicators the central bank is watching to gauge labour market hotness and the inflation risks it poses. A batch of US housing data later showed y/y prices further bottoming out for a third month straight. Current changes in US yields vary between +0.6 bps (2-y) to -4.8 bps (30-y). Equity markets feel like rallying in Europe (SX5E +1%). US stocks erased opening losses. Aside from JPY, the US dollar also strengthens against other global peers. EUR/USD swapped gains for losses after the ECI release with the pair just holding on north of 1.06. DXY rises towards 106.54.

With today’s key events (BoJ) and eco data out of the way, markets are now looking forward to tomorrow’s Fed meeting. The US Federal Reserve will skip on hiking its policy rate for a second meeting straight. Economic data since the September Fed meeting scream for the final (flagged) hike, but Fed-governors joined forces to downplay such action as the yield increase at the long end of the curve (tightening of financial conditions) substitutes for such move. We believe that Fed chair Powell will keep the option open for December (<30% market implied probability) or risk a further increase in inflation expectations which since that same Fed talk rose to match the (March) YTD high at 2.5%. The US 2-yr yield risks losing the 5% in case of a dovish skip (not our preferred scenario).

News & Views

Czech GDP unexpectedly shrank in the third quarter (-0.3% Q/Q) with y/y-comparison unchanged at -0.6% Y/Y. The supply-side breakdown suggests negative contributions coming mainly from industry, trade, transportation, accommodation and food services. Information and communication and professional, scientific, technical and administrative activities recorded positive growth. From a demand-side view, household consumptions and gross fixed capital formation weighed while exports had a positive influence. Czech employment decreased by 0.7% Q/Q, being up 0.5% Y/Y. Today’s GDP figures strengthen the case for the start of the policy rate cut cycle at Thursday’s meeting. We expect the key rate to be lowered by 25 bps to 6.75%. Czech swap rates cede up to 11.5 bps at the front end of the curve today (2y). The Czech koruna nevertheless stands its ground against the euro, trading level around EUR/CZK 24.55.

Polish inflation slowed to 0.2% M/M in October (from 0.4% in September vs 0.3% expected). In Y/Y-terms, inflation decelerated from 8.2% to 6.5% (vs 6.6% forecast). It’s the lowest level since September 2021. Fuel prices are the main culprit, crashing 4.2% M/M and 14.4% Y/Y. Food and non-alcoholic drink prices rose for the first month since May (0.4% M/M with Y/Y-growth falling from 10.4% to 7.9%. Electricity and gas prices rose marginally (0.2% M/M & 8.3% Y/Y). Polish markets didn’t respond to the near-consensus figures. Money markets expect the National Bank of Poland to proceed with another 25 bps rate cut in November.

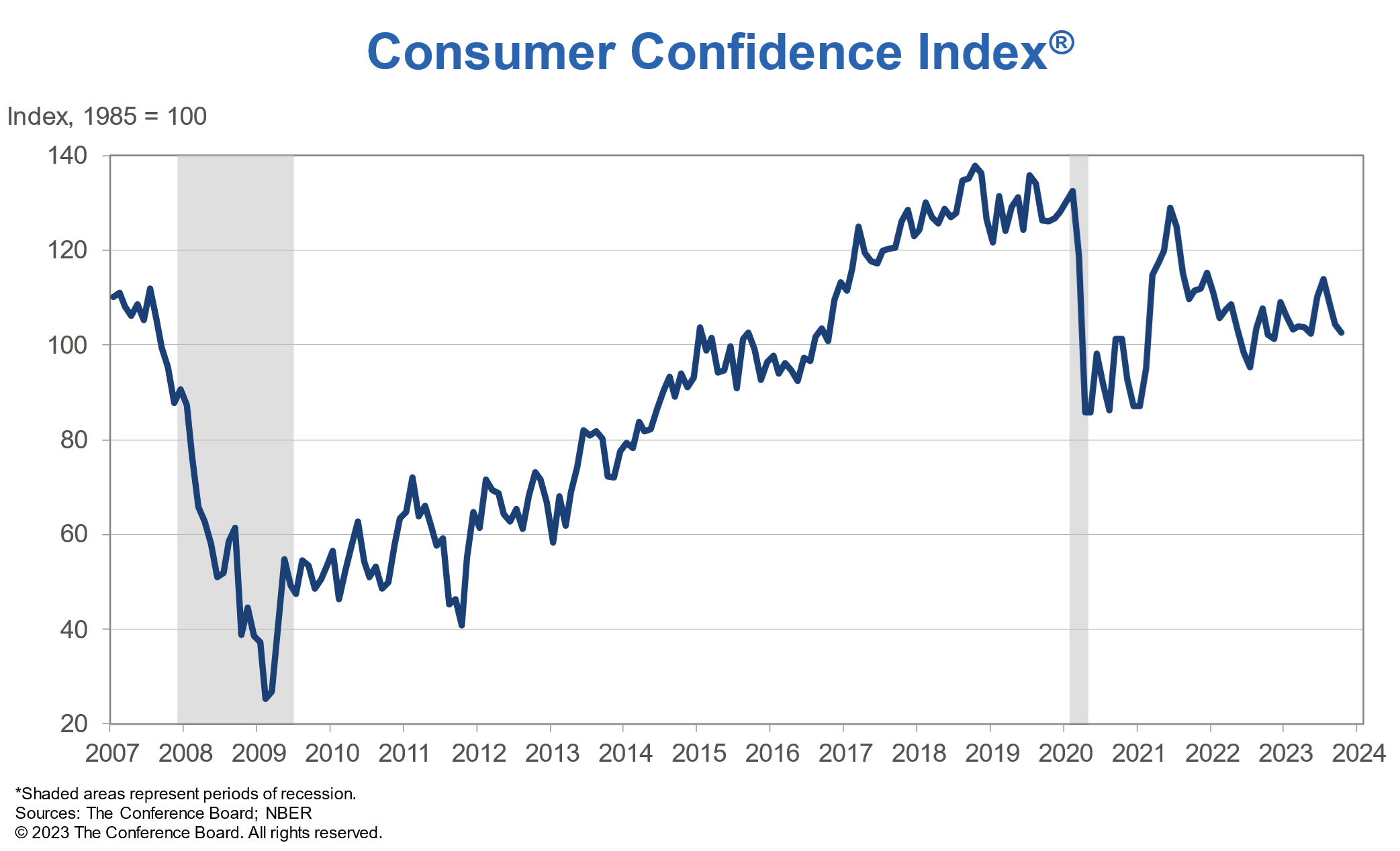

US consumer confidence fell to 102.6, third month of decline

Conference Board's Consumer Confidence Index in the US recorded a dip in October 2023, falling from 104.3 to 102.6, though it managed to beat the anticipated 100.4. This decline marks the third consecutive month where consumer confidence has waned. Breaking it down further, Present Situation Index saw a decrease from 146.2 to 143.1, while Expectations Index also experienced a slight drop, moving from 76.4 to 75.6.

Dana Peterson, Chief Economist at Conference Board, highlighted, "Consumer confidence fell again in October 2023, marking three consecutive months of decline." This drop in confidence reflects concerns in both the present economic conditions and future expectations.

One of the primary worries for consumers remains the rising prices, particularly noticeable in groceries and gasoline. These increasing costs continue to be a major concern, influencing overall consumer sentiment.

In addition to economic factors, political uncertainty and escalating interest rates have also contributed to the decline in confidence. Furthermore, increasing tensions and unrest in the Middle East have heightened worries around war and conflicts, adding another layer of apprehension among consumers.

Doves Firmly in Control of BoE Meeting

- The Bank of England meets as geopolitical developments affect market sentiment

- Another pause is priced in but Wednesday’s Fed gathering could unsettle expectations

- The statement is set for Thursday 12:00 GMT; press conference 30 minutes later

- Calendar also includes the final Manufacturing and Services PMI prints

Data since September have been on the weak side

With the focus lately turned elsewhere, it has been a quiet month for the ΒοΕ, especially as its members continued to be less active when compared to their Fed and ECB counterparts. This comes after a difficult September BoE meeting, considering the 5-4 split vote in favour of a rate pause. Developments since then have been mixed as the late September upside surprise in the final GDP figure for the second quarter of 2023 was not followed by a plethora of stronger prints in other data releases.

More specifically, the property sector is a headache for the BoE as the various house price indices continue to show a contraction in prices. In addition, mortgage approvals remain in a downward trend and net lending is almost stagnant and potentially preparing for the first negative month-on-month print since August 2021. Also, retail sales continue to exhibit negative annual growth rates as consumer confidence shows further signs of deterioration.

Crucially, inflation edged higher in September but the same is not expected for October. This next inflation report will be released on November 15, and because of base effects, a strong deceleration in the annual figure is forecast. Governor Bailey has already been on the wires talking about this expectation, thus sending a strong signal to the hawks regarding Thursday’s meeting.

Will it be an easier meeting for Governor Bailey?

Therefore, the decision seems easier this time around with the market assigning only a 2% probability for a 25bps rate move on Thursday. Having said that, the focus will be on the voting pattern and the overall rhetoric. In terms of the former, a 6-3 voting result in favour of another rate pause is expected; thus, we are in for a surprise if the four hawks that supported a rate hike in September do not shift their votes.

Additionally, the market will also be looking for the “further tightening in monetary policy would be required if there were evidence of more persistent inflationary pressures” comment that appeared in the last statement, in order to gauge if the BoE decided to tone down its hawkishness. To be fair, the overall BoE meeting is bound to be affected by what the Fed announces the previous night (Wednesday). If the Fed opts for a hawkish stance, there could be some inclination by Bailey et al to follow suit, without shocking the market. Such an outcome could result in the rate cut expectations, currently priced by mid-2024, to be pushed slightly out.

Quarterly forecasts on the menu as well

The meeting also entails the quarterly Monetary policy Report, which includes the Bank’s quarterly forecasts. The last set of these projections at the August meeting showed inflation dropping to 1.7% by end-2025 but with risks skewed towards a stronger figure. A confirmation of these forecasts and/or an even weaker outlook in the examined horizon could put to bed the prospects of further rate hikes and bring forward expectations for the first rate cut.

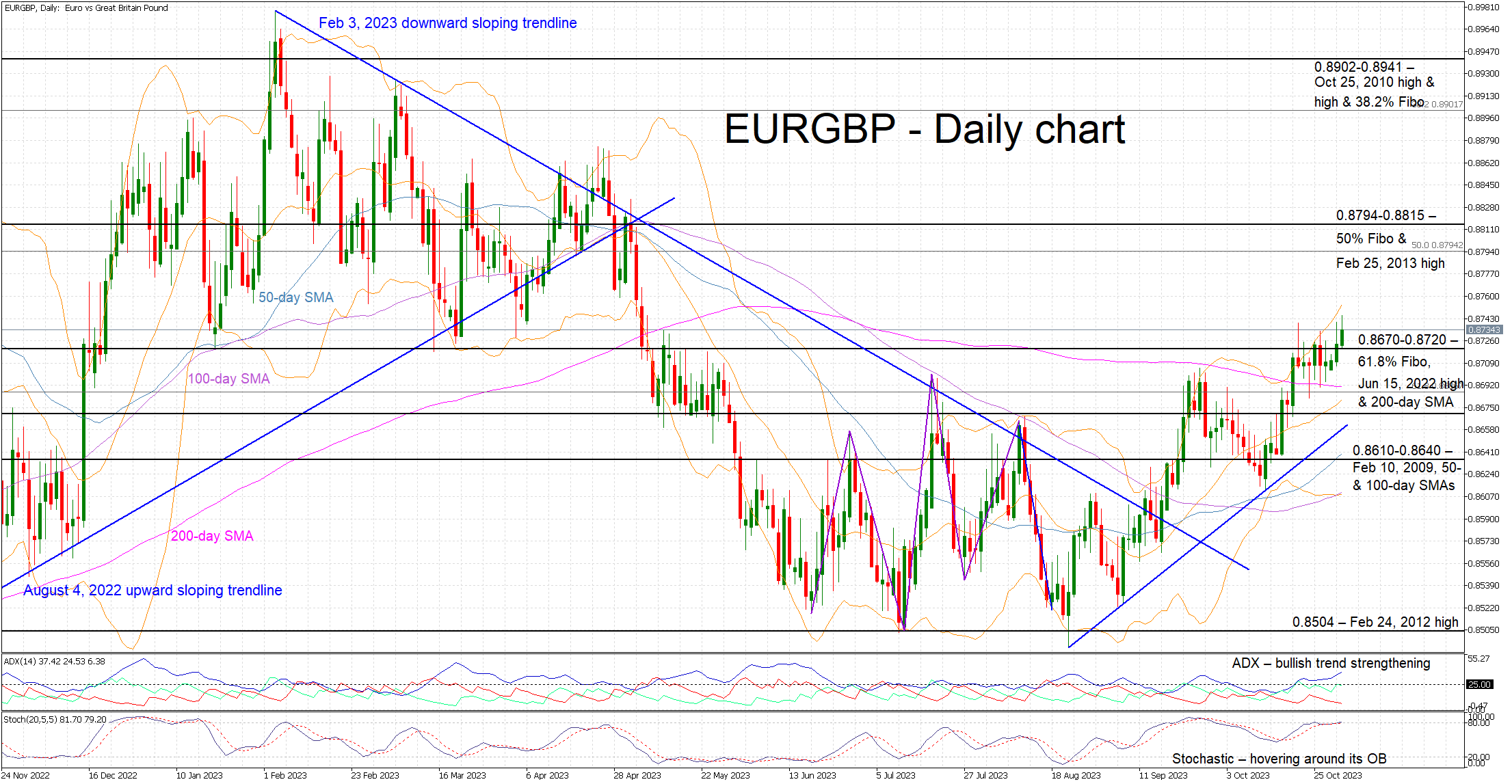

The pound is on the backfoot since August

The euro-pound pair has been experiencing an aggressive uptrend since the August lows as the euro bulls are trying to recover part of their sizeable losses that occurred during 2023. This move is somewhat surprising considering the ECB’s change of stance and the weak data releases seen in the euro area lately. Therefore, the pound could benefit from this week’s events. A hawkish BoE and/or a tighter voting result could allow the euro-pound pair to move lower, potentially overcoming the support set by the busy 0.8670-0.8720 area. On the flip side, a dovish meeting would keep the door open for the euro bulls to plot a course towards the 0.8794-0.8815 range.

Canada’s Economy Recorded No Growth in August, Likely Stalled in September

Canadian economic growth came in flat on a month-on-month (m/m) basis in August, below Statistics Canada's advanced estimate and market expectations of a mild 0.1% m/m gain. The flash estimate for September points to another month of zero growth.

August's reading was mixed, with output expanding in 8 of 20 industries. Goods producing industries (-0.2% m/m) lagged the 0.1% m/m gain in the services sector.

On the goods side, mining, quarrying, and oil and gas extraction led the charge with growth of 1.2% m/m in August. The oil and gas subsector was up for a seventh time in eight months (+1.0% m/m). Offsetting this gain was a third consecutive monthly contraction in the manufacturing sector (-0.6%).

On the services side, wholesale trade advanced a healthy 2.3% m/m with the machinery, equipment and supplies subsector contributing most (+5.1% m/m). However a 2.2% slide in food services and drinking places pulled the accommodation and food services sector down 1.8% in August. Transportation and warehousing advanced by 0.8% m/m, led by water transportation (+4.2%) that recouped losses in July on the back of the BC Port Strike.

The advanced reading of flat growth in September was driven by declines in mining, quarrying, and oil and gas extraction and utilities, but was partially offset by increases in the construction and public sectors.

Key Implications

No real tricks in this GDP report, but it isn't a treat either. "Essentially flat" is the theme for the third quarter, as growth in July, August and September are hovering around the zero growth line. Taken altogether, this presents a modest downside risk to the Bank of Canada's recently revised 0.8% annualized growth forecast for the third quarter this year.

Higher interest rates are certainly doing their part to tamp down excess demand, and we continue to expect below-trend growth for the next couple of quarters. After holding the policy rate at 5.00% last week, the Bank of Canada (BoC) should feel confident that their rate hikes are working to pull the economy back into balance. That said, they have voiced their need to remain vigilant, especially as core inflation remains at uncomfortable levels. Employment and wages data later this week will be on watch, as this segment of the economy continues to show relative strength.

Aftermath of BoJ’s Policy Statement

The Bank of Japan (BoJ) recently concluded its October monetary policy review meeting, deciding not to make any adjustments to its current policy settings. This means the interest rate remains at -10bps, and the 10-year JGB yield target remains at 0%. A noteworthy change in the BoJ's approach is the redefinition of the 1.0% 10-year JGB yield cap, now regarded as a reference rather than a strict limit.

The central bank also plans to be more adaptable in managing market operations, determining offer rates for fixed-rate JGB buying operations individually, taking into account various market factors. Furthermore, the BoJ emphasizes the need for strengthening wages and prices within a virtuous economic cycle. It reiterates its dedication to ongoing monetary easing under YCC, aiming to boost economic activity and facilitate wage growth.

This decision underscores the high level of uncertainty currently prevailing in the economy and financial markets. The BoJ's announcement, made just a few hours ago, reflects its commitment to maintaining a flexible and supportive monetary policy as it navigates the challenges presented by today's economic landscape.

AUDJPY - H4 Timeframe

The AUDJPY chart above shows price approaching a key level at the 76% of the Fibonacci retracement, alongside the presence of a drop-base-drop supply zone. The head-and-shoulder pattern and the trendline resistance serve as additional confirmations for the bearish sentiment.

Analyst’s Expectations:

- Direction: Bearish

- Target: 95.189

- Invalidation: 96.341

CADJPY - H4 Timeframe

CADJPY is currently at a rally-base-drop supply zone, with the confluence of the resistance trendline, and the 100-day moving average resistance. Based on this, I will uphold a bearish sentiment since the supply zone also overlaps a resistance pivot zone.

Analyst’s Expectations:

- Direction: Bearish

- Target: 108.082

- Invalidation: 109.168

NZDJPY - H4 Timeframe

On the 4-Hour chart of NZDJPY, we can see price resting at the 200-day moving average, with further confluence from the trendline resistance, rally-base-drop supply zone, as well as the bearish array of the moving averages.

Analyst’s Expectations:

- Direction: Bearish

- Target: 87.388

- Invalidation: 88.559

CONCLUSION

The trading of CFDs comes at a risk. Thus, to succeed, you have to manage risks properly. To avoid costly mistakes while you look to trade these opportunities, be sure to do your due diligence and manage your risk appropriately.