Sample Category Title

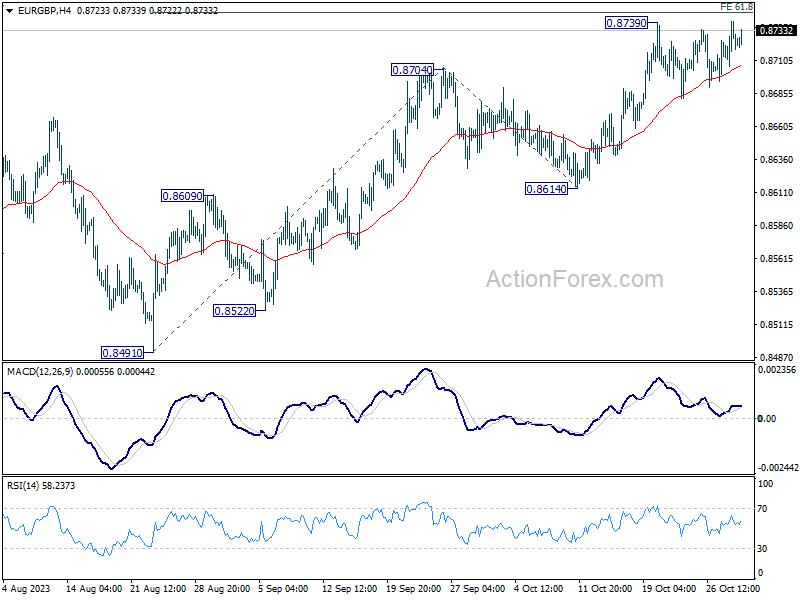

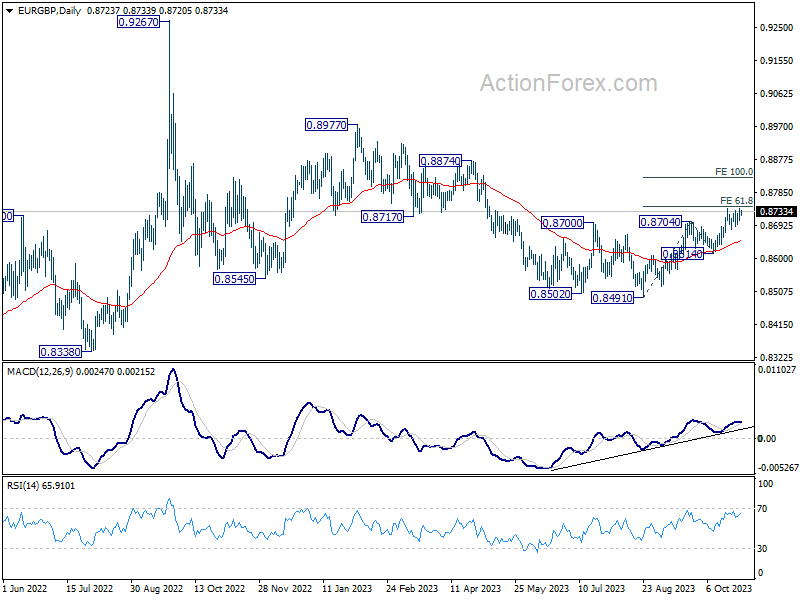

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8707; (P) 0.8724; (R1) 0.8740; More....

Intraday bias in EUR/GBP stays neutral first. In case of deeper retreat, downside should be contained by 55 D EMA (now at 0.8652). Firm break of 0.8739 will resume the whole rise from 0.8491, and target 100% projection of 0.8491 to 0.8704 from 0.8614 at 0.8827 next.

In the bigger picture, current development suggests that whole down trend from 0.9267 (2022 high) has completed with three down to to 0.8491. Rise from 0.8491 is seen as another leg inside that pattern from 0.9499 (2020 high). Further rally should be seen to 0.8977 resistance and above. This will now remain the favored case as long as 0.8614 support holds.

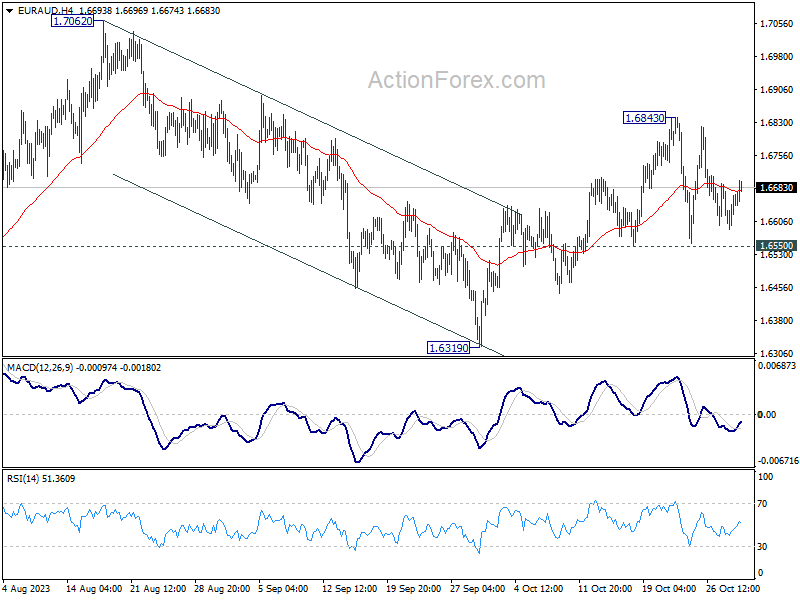

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6602; (P) 1.6643; (R1) 1.6694; More...

Range trading continues in EUR/AUD and intraday bias stays neutral at this point. Further rally is expected as long as 1.6550 support holds. Above 1.6843 will target a test on 1.7062 high. Firm break there will resume larger up trend. However, break of 1.6550 support will bring deeper fall back to 1.6319 support instead.

In the bigger picture, the strong support from medium term rising trend line indicates that rise from 1.4281 (2022 low) is still in progress. Sustained break of 1.7062 will pave the way to 61.8% retracement of 1.9799 (2020 high) to 1.4281 at 1.7691. In any case, outlook will stay bullish as long as 1.6319 support holds.

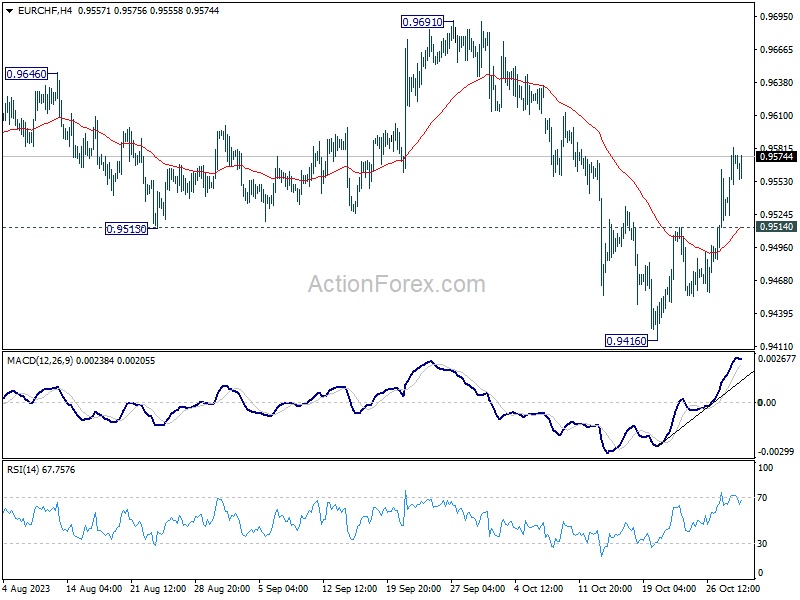

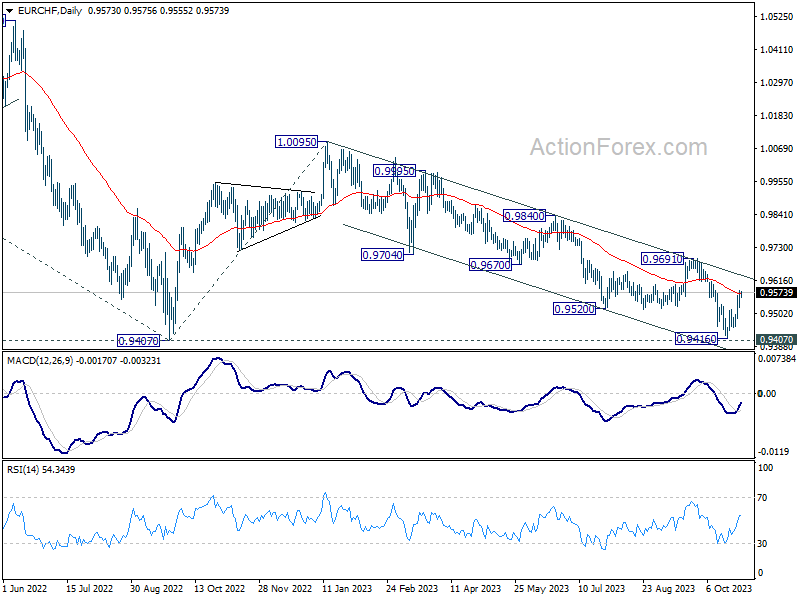

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9536; (P) 0.9560; (R1) 0.9599; More...

Intraday bias in EUR/CHF remains on the upside as rebound from 0.9416 is in progress. Sustained break of 55 D EMA (now at 0.9570) will bring further rise to 0.9691 key structural resistance. On the downside, though, below 0.9514 minor support will turn bias back to the downside for retesting 0.9407/16 zone.

In the bigger picture, down trend from 1.2004 (2018 high) is still in progress. Decisive break of 0.9407 will confirm resumption, and target 61.8% projection of 1.1149 to 0.9407 from 1.0095 at 0.9018. On the upside, break of 0.9691 resistance is needed to be the first sign of medium term bottoming. Otherwise, outlook will stay bearish.

Yen Falls after BoJ Decision, US Bond Investors Hopeful on Treasury’s Plan to Spend ‘Less’

The Bank of Japan (BoJ) kept interest rates unchanged, redefined the 1% limit on the 10-year JGBP yield as a loose ‘upper bound’ and scrapped its promise to keep that level intact. Alas, the move was less aggressive than expected by the market and sent the yen tumbling. Japanese policymakers’ insistence that they won’t hesitate to take additional easing measures ‘if needed’ also spoiled sentiment. The USDJPY trades just above the 150 mark this morning after the BoJ decision, although the spike in the 10-year JGB yield to almost 1% should’ve pulled the pair lower – especially after the news that the US Treasury will be borrowing less money in the last three months of this year.

The US Treasury will borrow less; the Fed is expected to announce no change – Yet

The US Treasury Department said yesterday that they are planning to borrow around $776 billion in the final quarter of the year. That’s still a historically high borrowing, but it has the merit to be below the expectation of around $800bn and it’s well below the $1 trillion that they borrowed in the July-to-September period, and which wreaked havoc in the US bond market, sending – especially the long-end of the US yield curve rallying.

Today, the Federal Reserve (Fed) starts its two-day policy meeting. Yes, the FOMC announcement on interest rates is often a big event for investors, but this time around, it won’t be the only shining star of the week. First, because we know that there won't be any rate hikes this week. The probability of no change is priced as being almost 100% sure. The Fed members will still be raising their eyebrows given the strength of the recent economic data, the uptick in inflation and global uncertainty. But they won’t necessarily be raising the rates. Therefore, what they will say they will do will matter more for the market pricing than what they will do. And the rate expectations will be played for the December and January meetings – which both hint at no rate hike either, by the way. That could change, but for now, no more rate hike is what investors are betting on.

So, in the absence of a surprise rate decision, or a surprise forward guidance about a rate decision, what will really, really matter this week for the US sovereign space and the faith of the US yields, is the US debt situation, and the Treasury Department’s quarterly announcement on details regarding the size and the maturity of the bonds that they will issue to borrow that extra $776 bn this quarter.

The composition of the US Treasury’s bond issuances will be crucial. Shifting toward shorter maturity debt could relieve the pressure on the US long-term papers but the problem with the short-term bills is that the US Treasury already sold plenty of them - they came close to their self-imposed limit of 20% last quarter- and that’s why they decided to sell more longer maturity bonds since September. The latter shift towards longer-term maturity debt explained why the long-term yields took a lift since September. Therefore, it’s not a given that the Treasury’s issuance calendar will fully calm down the bond investors’ nerves on Wednesday.

Bank of Japan Tweaks Yield Policy Again

Market movers today

Today markets will zoom in on HICP inflation data for the euro area. Country releases from yesterday were somewhat lower than expected indicating the euro area total will end up around 3% from 4.3% in September. The Spanish and German data did give some promising signs with regards to core inflation pressures in the euro area.

At the same time, we get the first GDP estimate for Q3 from Eurostat, which will likely show close to a standstill in economic activity in Q3.

In the US, the employment cost index for Q3 will hold valuable information to policy makers on price pressures. We also get Conference Board consumer confidence.

Overnight, we will look out for Chinese Caixin manufacturing PMIs. The similar official measure came in lower than expected this morning at 49.5 in October (consensus 50.2).

The 60 second overview

Bank of Japan. The Bank of Japan (BoJ) tweaked its yield curve control policy (YCC) at a meeting ending this morning by redefining the 10-year rate cap as a reference rather than a rigid bound and thus also removed a pledge to defend this level with offers to buy an unlimited amount of bonds at the 1% level. A story indicating a tweak of the YCC moved USD/JPY from 149.7 to 149.0 levels already yesterday. This morning, markets sold the fact again on announcement and traded the cross back to 150. JGB yields have sold off and 10-year yields now trade 5bps closer to the rate cap at 95 bps. As we see it, this was another, likely the last, step ahead of dismantling the YCC altogether. However, the BoJ still needs confirmation that inflation has sustainably moved above the 2% target before they are ready to take bigger steps to normalisation. They are slowly recognising higher inflation is not temporary and moved their inflation forecast significantly higher, particularly for the fiscal year 2024 (starting in April) to 2.8% from 1.9% back in July.

European data softens. Inflation figures from Spain and Germany released yesterday, came in below expectations, pointing to softening inflation across the Eurozone. Seasonally adjusted German HICP fell 0.2% m/m in October, while the Spanish HICP pace halved to 0.3% from 0.6% in September. Core CPI details were also weaker in general. Meanwhile, the first release of Q3 GDP data showed Germany contracting by 0.1% q/q, highlighting the weakness of economic growth in the region. Private consumption was the main drag on growth, according to the Federal Statistics Bureau, while investments in equipment and machinery showed some improvement.

UAW strike ends. Yesterday, GM and the United Auto Workers Union (UAW) was said to have reached a tentative deal to end the six-week strike. GM has agreed to raise the hourly pay by 25% over the course of a four-year deal, which is very similar to the terms in deals struck by Ford and Stellantis last week. If ratified by the UAW, this will mark the end of the first co-ordinated strike at the three largest US car-makers.

Equities: What is a better start to the week than a Monday rebound. There were no clear drivers behind the sudden optimism, aside from S&P500 hitting correction territory on Friday. In fact, US yields even rose during the session. While the Nordic and European session was a modest one (Stoxx 600 only up 0.4%) the US bounce was forceful. Dow closed up 1.6% and S&P 500 1.2%. Cyclicals led this, with banks and communication among the better groups. The sentiment is weakening in Asia this morning after weak China PMIs and Bank of Japan abandoning yield curve control. Chinese equities almost -2% lower but Japan 0.5% higher.

FI: EGB yields fell slightly yesterday as weaker-than-expected inflation figures from Spain and Germany provided some support to the segment. However, the rally was mostly reversed in the afternoon. 10Y Bund yields ended the day down by 1bp, while 10Y BTP yields fell by 7bp. Markets are now pricing in 82bp worth of ECB cuts next year, up from 66bp before the ECB meeting last week. The long end of the UST curve was to some degree supported by the downward revision of the US Treasury's expected net borrowing until the end of the year (see FI section). The BoJs decision to soften the YCC policy has added upward pressure on long JGB yields this morning, with the 10Y tenor up by 5bp to 0.95%.

FX: EUR/USD zig-saws around 1.06 whilst USD/JPY moved back above 150 on the BoJ YCC tweak. Scandies continues to trade weaker in tandem with NOK/SEK at 1.00. Brent oil is back below USD 90/barrel after a 3% drop yesterday.

Credit: Credit spreads tightened modestly yesterday where iTraxx Xover tightened 4.8bp and Main 0.9bp. There was barely any activity in the primary market, but SEB saw solid demand for its EUR500m 5y green SNP offering, which attracted orders of more than EUR2bn.

Nordic macro

Riksbank Governor Thedeén spoke in New York last night and repeated the message that whatever the Riksbank decides at the November meeting the repo rate will remain "high for long". He expressed worries about the weak SEK and services prices making inflation "sticky". This is nothing new though. We note that the current SEK weakening in KIX terms is just about average for the 15 years during which the SEK has been depreciating between 1993 and 2022, hence 2023 is nothing special. Neither did he mention Riksbank's semi-annual business survey which suggests household-near companies are planning to slash prices. We stick to our guns of a no hike in November, for now.

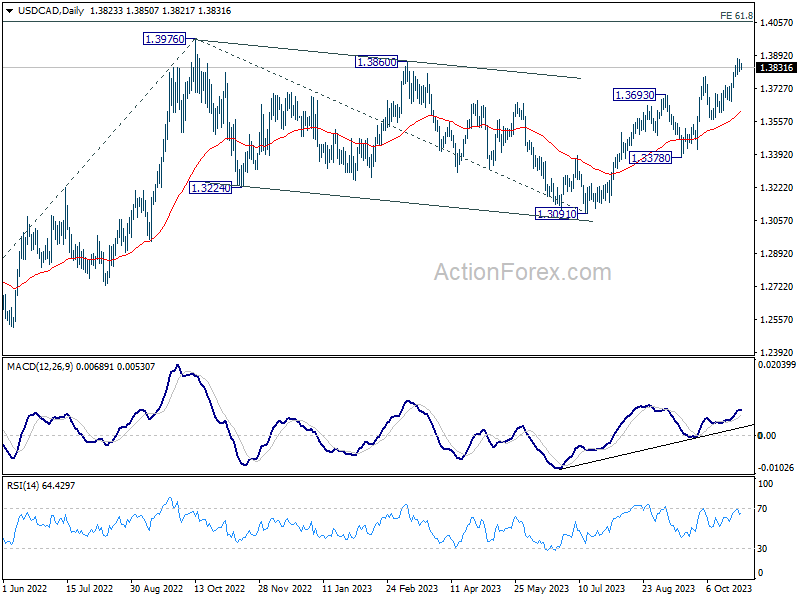

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3802; (P) 1.3838; (R1) 1.3862; More...

Intraday bias in USD/CAD is turned neutral with current retreat and some consolidations could be seen. Downside of retreat should be contained above 1.3659 support to bring another rally. On the upside, above 1.3879 will resume recent rally to retest 1.3976. Decisive break there will resume larger up trend to 1.4064 projection level.

In the bigger picture, corrective pattern from 1.3976 (2022 high) should have completed with three waves down to 1.3091. Decisive break of 1.3976 high will confirm resumption of up trend from 1.2005 (2021 low). Next target will be 61.8% projection of 1.2401 to 1.3976 from 1.3091 at 1.4064. This will now remain the favored case as long as 1.3568 support holds.

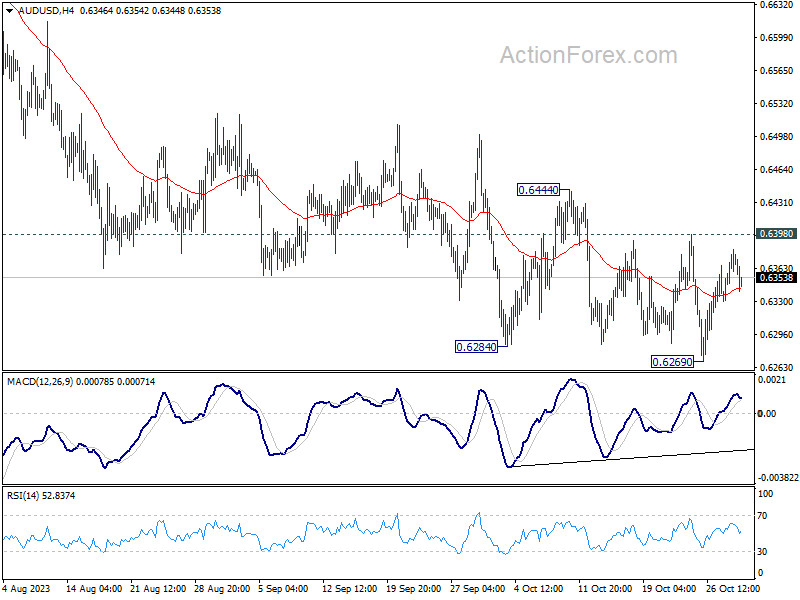

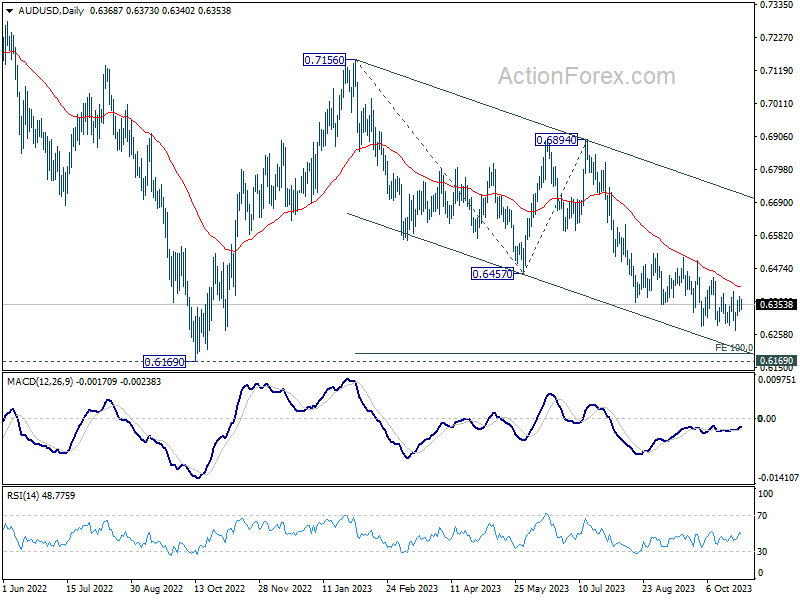

AUD/USD Daily Report

Daily Pivots: (S1) 0.6344; (P) 0.6364; (R1) 0.6395; More...

Intraday bias in AUD/USD stays neutral and outlook remains bearish with 0.6398 resistance intact. On the downside, break of 0.6269 will resume larger fall from 0.7156 to 100% projection of 0.7156 to 0.6457 from 0.6894 at 0.6195, which is close to 0.6169 medium term support.

In the bigger picture, down trend from 0.8006 (2021 high) is possibly still in progress. Decisive break of 0.6169 will target 61.8% projection of 0.8006 to 0.6169 to 0.7156 at 0.6021. This will now remain the favored case as long as 0.6894, in case of strong rebound.

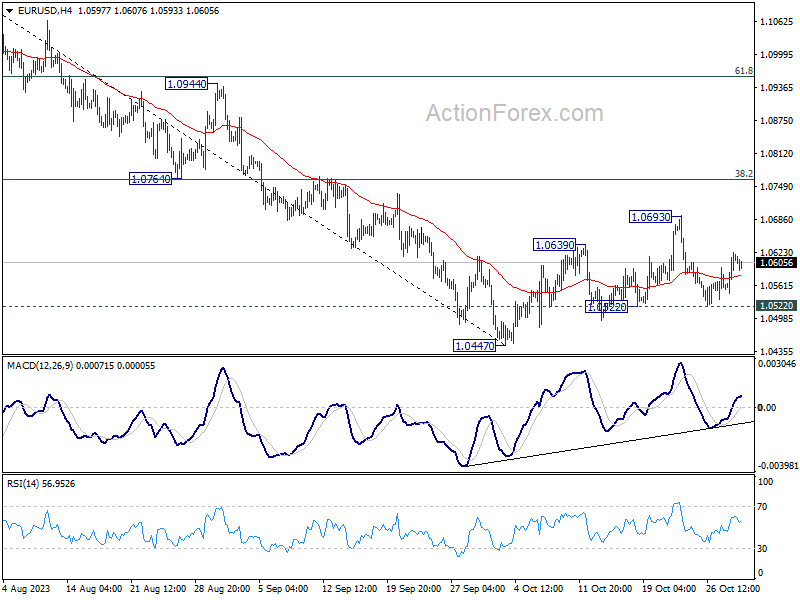

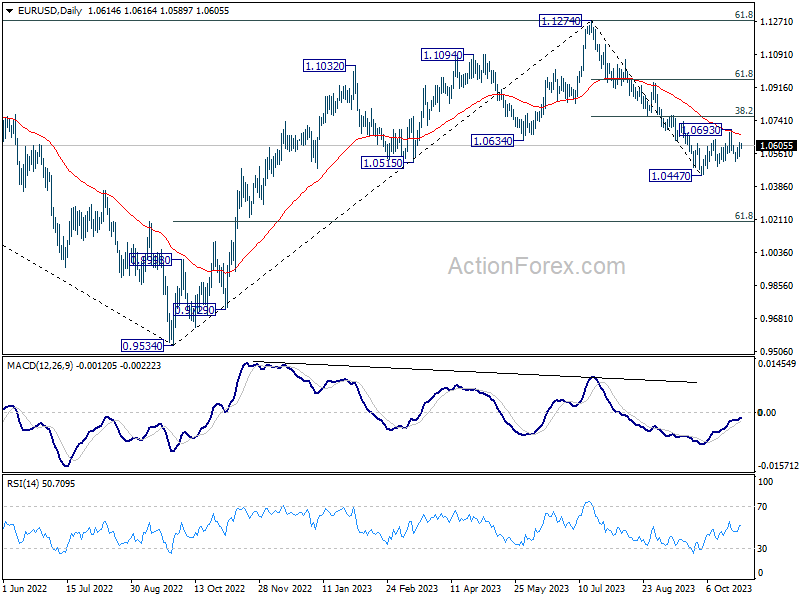

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0566; (P) 1.0596; (R1) 1.0644; More...

Intraday bias in EUR/USD remains neutral for the moment. On the downside, break of 1.0522 support will turn bias back to the downside for retesting 1.0447 low. Break there will resume larger fall from 1.1274. On the other hand, strong bounce from current level, followed by break above 1.0693, rebound from 1.0447 to 1.0764 cluster resistance (38.2% retracement of 1.1274 to 1.0447 at 1.0763).

In the bigger picture, fall from 1.1274 medium term top could still be a correction to rise from 0.9534 (2022 low). But chance of a complete trend reversal is rising. In either case, current fall should target 61.8% retracement of 0.9534 to 1.1274 at 1.0199 next. For now, risk will stay on the downside as long as 55 D EMA (now at 1.0665) holds, in case of rebound.

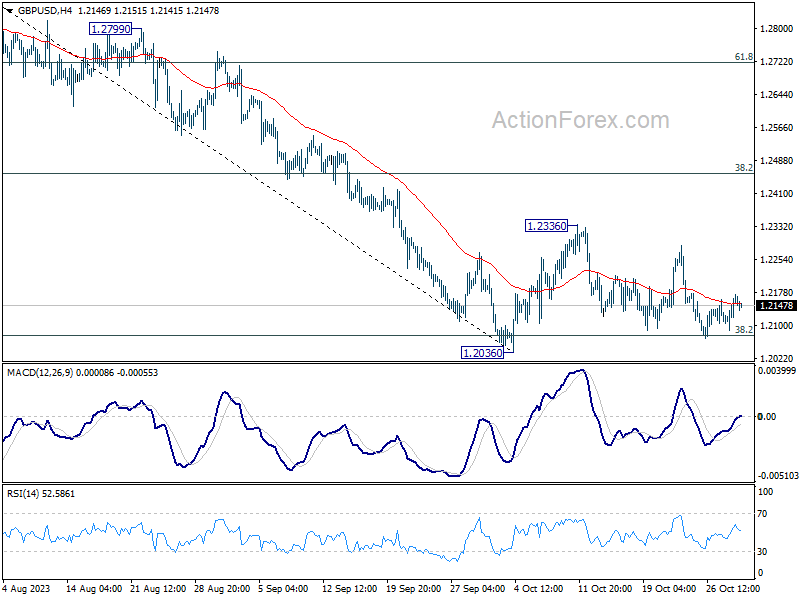

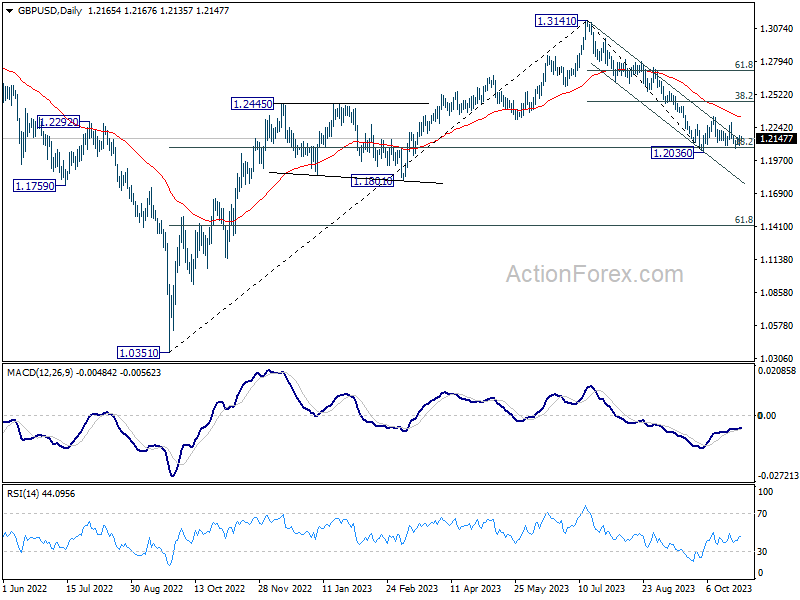

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2098; (P) 1.2130; (R1) 1.2155; More

Intraday bias in GBP/USD remains neutral at this point, as sideway trading continues. With 1.2336 resistance intact, outlook stays bearish. On the downside, firm break of 1.2036 will resume whole decline from 1.3141 for 1.1801 support next. However, break of 1.2336 will turn bias back to the upside for 38.2% retracement of 1.3141 to 1.2036 at 1.2458.

In the bigger picture, fall from 1.3141 medium term top could still be a correction to up trend from 1.0351 (2022 low) only. But risk of complete trend reversal is rising. Sustained break of 38.2% retracement of 1.0351 to 1.3141 at 1.2075 will pave the way to 61.8% retracement at 1.1417. For now, risk will stay on the downside as long as 55 D EMA (now at 1.2346) holds, in case of rebound.

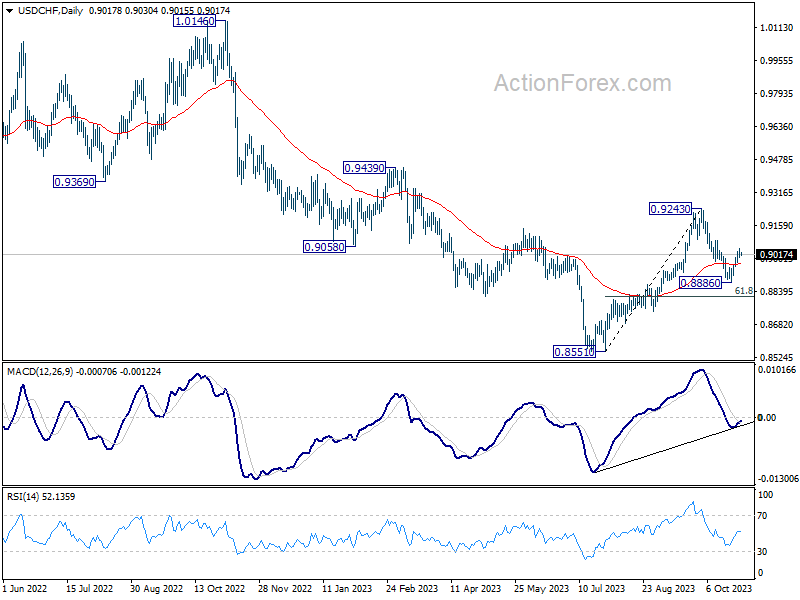

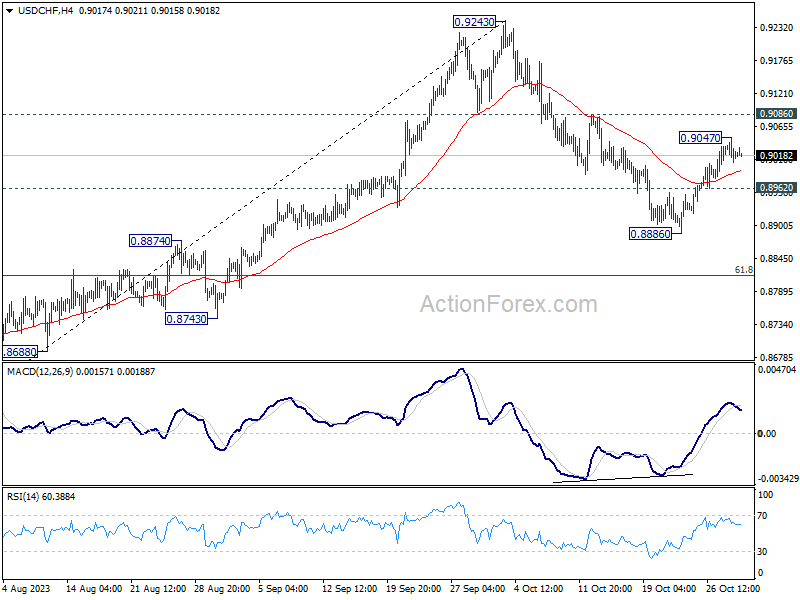

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8991; (P) 0.9014; (R1) 0.9048; More....

Intraday bias in USD/CHF is turned neutral with 4H MACD crossed below signal line. On the upside, above 0.9047 will resume the rebound from 0.8886 to 0.9086 resistance. Sustained break there will pave the way back to 0.9342 resistance next. On the downside, however, below 0.8962 minor support will turn bias back to the downside for 0.8886 and possibly below.

In the bigger picture, outlook is mixed up by the deeper than expected pull back from 0.9243. Yet there was no follow through selling after hitting 0.8886. On the upside, break of 0.9243 resistance will revive the case of medium term bottoming at 0.8851, and turn outlook bullish. However, sustained break of 61.8% retracement of 0.8551 to 0.9243 at 0.8815 will argue that larger decline from 1.0146 is ready to resume through 0.8551 low.