Sample Category Title

Bank of England’s November Interest Rate Decision and Its Potential Impact on the Pound

The British pound faces a crucial test as the Bank of England (BoE) prepares to announce its November interest rate decision. The outcome could significantly influence the pound's value, but several factors come into play.

If all members of the Monetary Policy Committee (MPC) vote to maintain the current interest rate, and there are no substantial alterations to inflation and growth forecasts, the pound may remain relatively unaffected. This decision aligns with market expectations and is unlikely to cause significant ripples in financial markets.

However, for forward-looking observers, the key focus will be on the guidance provided in the policy statement and the forecasts outlined in the Monetary Policy Report.

Some market sentiment suggests that the BoE might aim to maintain its 'high-for-longer' message, ensuring it remains the primary takeaway from November's policy statement. Such a message could lend support to the pound.

In recent times, there have been no upward adjustments to the base rate, accompanied by indications that rate cuts are not on the immediate horizon. This message may offer some upside for GBP, especially given the already modest expectations for further tightening.

Indicative pricing only

This contrasts with previous scenarios where the euro experienced gains against the British pound. Although the euro remains at a higher level against the pound compared to the previous week, the pound's depreciation has started to stabilise.

To convey the 'higher-for-longer' message effectively, the composition of the MPC vote and the economic forecasts are critical factors.

The market anticipates a significant majority favouring the status quo, but any potential downside risk for GBP could emerge if Swati Dhingra, the most dovish member of the MPC, votes for a rate cut. This would signal a shift toward discussions about rate cuts. However, the pound's response would depend on the broader context and any accompanying discussions highlighted in the minutes.

Economic forecasts hold substantial importance as the MPC uses them to guide market interest rate expectations, which, in turn, affect borrowing costs and the exchange rate. The inflation forecast for 2025 is of particular importance. For instance, if forecasts indicate that inflation will dip below the 2.0% target by 2025, it implies that the Bank might consider interest rate cuts starting around 2024. The adjustments to these forecasts can influence expectations in the market.

As a rule of thumb, upgraded growth and inflation forecasts signal the BoE's commitment to maintaining higher rates for an extended duration. Conversely, downgrades to growth and inflation predictions can erode the strength of such guidance, potentially leading to softer pound value.

If this forecast, which currently falls below the target, experiences an upward revision, it could provide additional support for the pound. However, this might also exert downward pressure on UK bond yields and potentially lead to a weaker pound.

In the grander scheme of things, the UK's economic situation is comparatively better than what was anticipated earlier this year and more favourable than the projections for the eurozone in the near future. The latter is increasingly seen as approaching a potential recession, while the UK has managed to avert such a scenario, despite grappling with high inflation for an extended period and the economic challenges posed by the cost of living crisis during 2021 and 2022.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0531; (P) 1.0603; (R1) 1.0648; More...

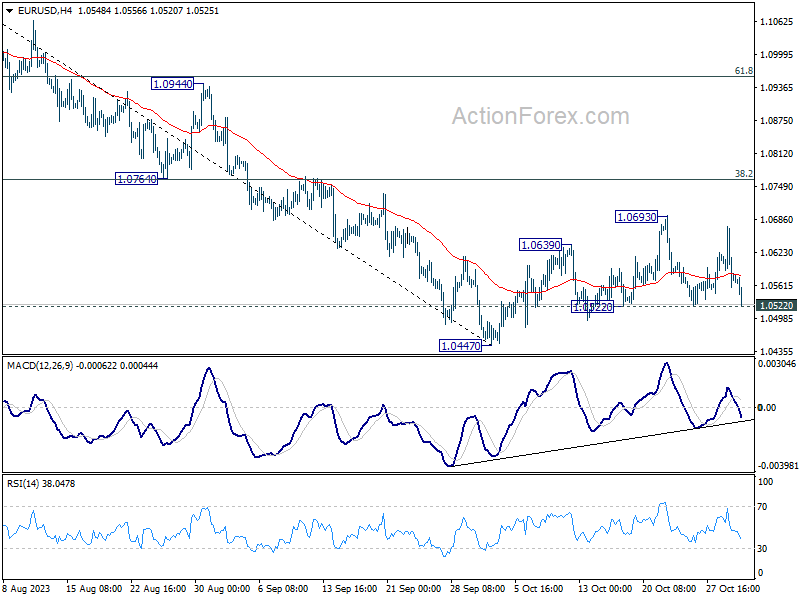

Immediate focus is now on 1.0522 support in EUR/USD. Firm break there will argue that larger fall from 1.1274 is resumed to ready. Intraday bias will be back on the downside for 1.0447 first, and then 1.0199 fibonacci level. On the other hand, strong bounce from current level, followed by break above 1.0693, will extend the rebound from 1.0447 to 1.0764 cluster resistance (38.2% retracement of 1.1274 to 1.0447 at 1.0763).

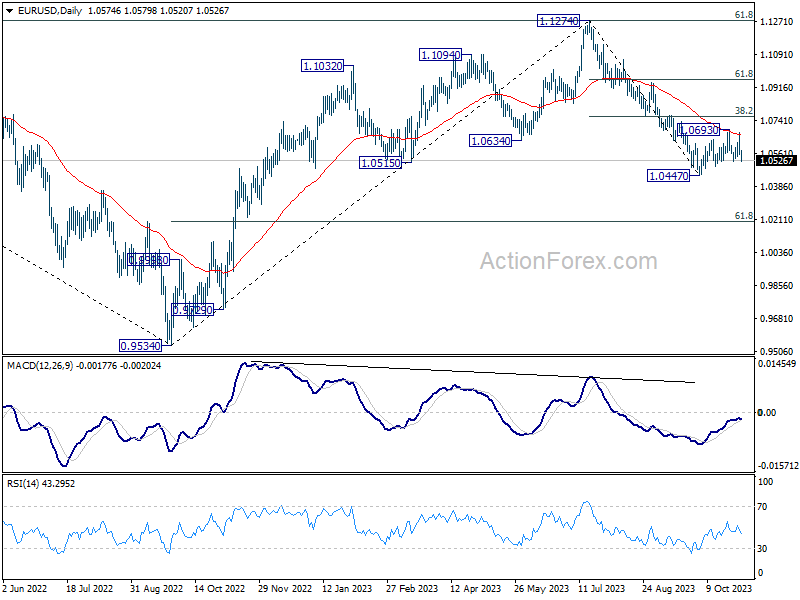

In the bigger picture, fall from 1.1274 medium term top could still be a correction to rise from 0.9534 (2022 low). But chance of a complete trend reversal is rising. In either case, current fall should target 61.8% retracement of 0.9534 to 1.1274 at 1.0199 next. For now, risk will stay on the downside as long as 55 D EMA (now at 1.0665) holds, in case of rebound.

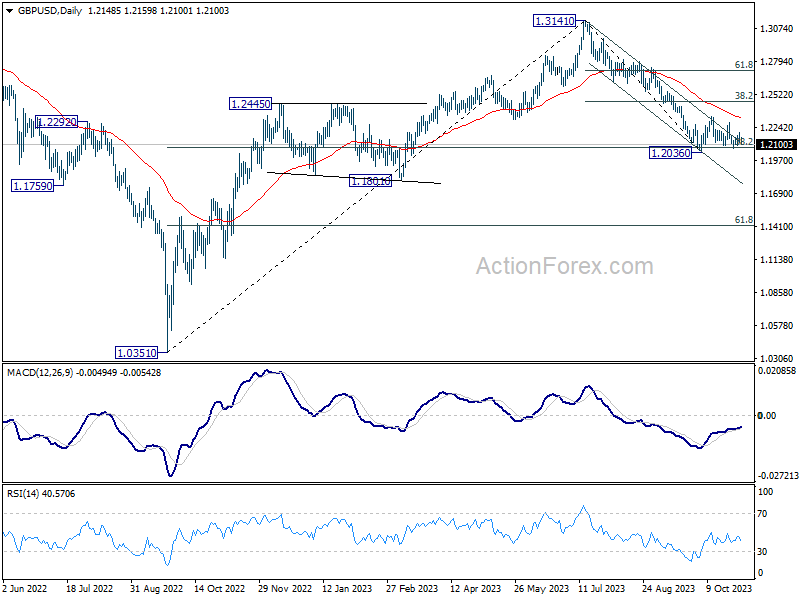

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2112; (P) 1.2157; (R1) 1.2193; More

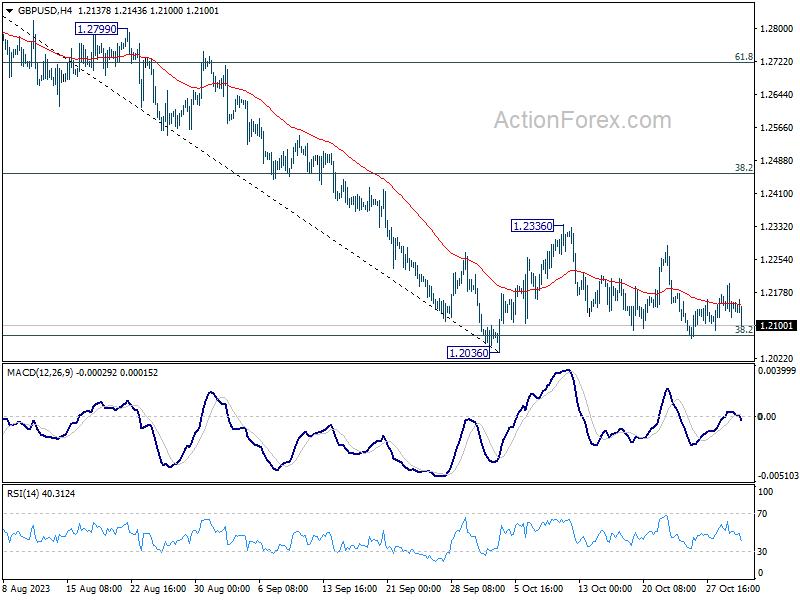

No change in GBP/USD's outlook as range trading continues. Intraday bias stays neutral first. With 1.2336 resistance intact, downside breakout is expected. On the downside, firm break of 1.2036 will resume whole decline from 1.3141 for 1.1801 support next. However, break of 1.2336 will turn bias back to the upside for 38.2% retracement of 1.3141 to 1.2036 at 1.2458.

In the bigger picture, fall from 1.3141 medium term top could still be a correction to up trend from 1.0351 (2022 low) only. But risk of complete trend reversal is rising. Sustained break of 38.2% retracement of 1.0351 to 1.3141 at 1.2075 will pave the way to 61.8% retracement at 1.1417. For now, risk will stay on the downside as long as 55 D EMA (now at 1.2346) holds, in case of rebound.

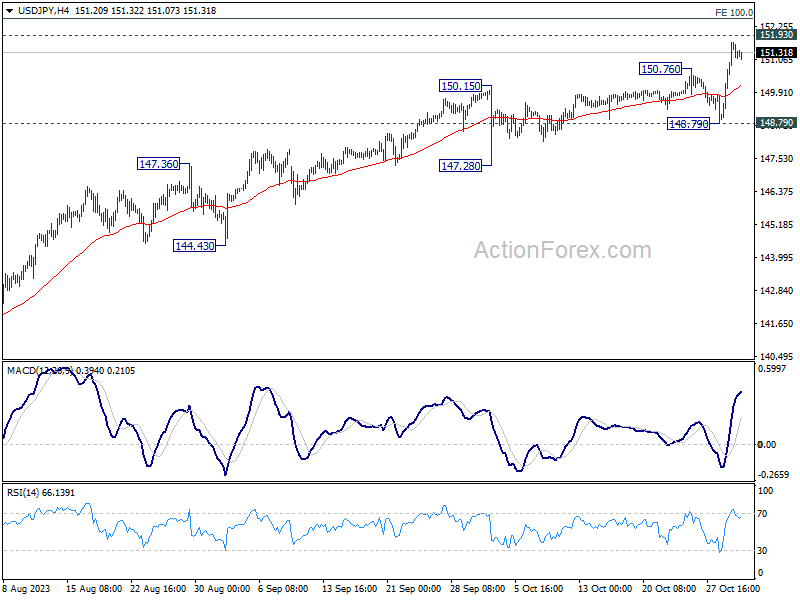

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.87; (P) 150.80; (R1) 152.56; More...

Intraday bias in USD/JPY stays on the upside despite current retreat. Further rise should be seen to 151.93 key resistance. Firm break there will target 100% projection of 129.62 to 145.06 from 137.22 at 152.66. For now, break of 148.79 support is needed to indicate short term topping. Otherwise, outlook will stay bullish in case of retreat.

In the bigger picture, immediate focus is now on 151.93 resistance (2022 high). Rejection by 151.93, followed by sustained break of 145.06 resistance turned support will argue that rise from 127.20 has completed, and turn outlook bearish for 137.22 support and below. However, sustained break of 151.93 will confirm resumption of long term up trend. Next target will be 61.8% projection of 102.58 to 151.93 from 127.20 at 157.69.

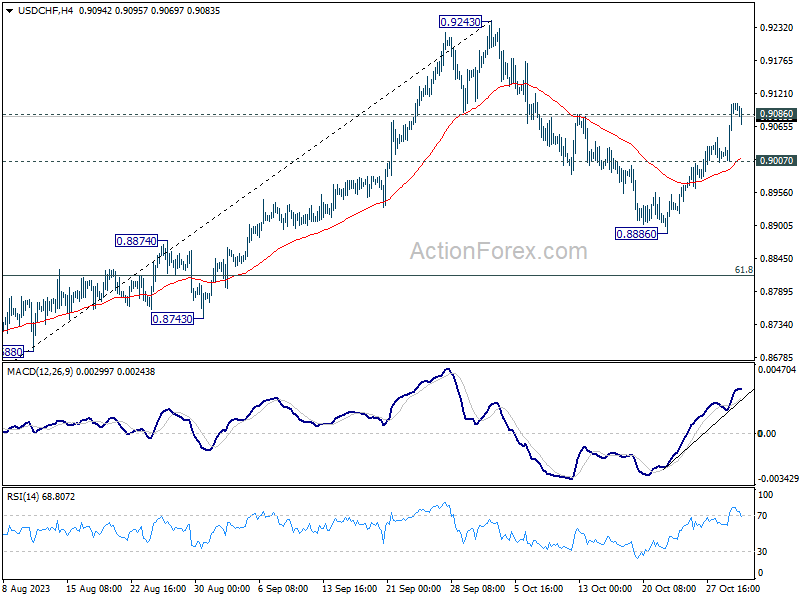

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9040; (P) 0.9074; (R1) 0.9139; More....

Despite current retreat, intraday bias in USD/CHF stays on the upside first. Sustained trading above 0.9086 resistance will pave the way back to 0.9342 resistance next. In any case, further rally will remain in favor as long as 0.9007 support holds. But firm break of 0.9007 will turn bias to the downside for 0.8886 support instead.

In the bigger picture, outlook is mixed up by the deeper than expected pull back from 0.9243. Yet there was no follow through selling after hitting 0.8886. On the upside, break of 0.9243 resistance will revive the case of medium term bottoming at 0.8851, and turn outlook bullish. However, sustained break of 61.8% retracement of 0.8551 to 0.9243 at 0.8815 will argue that larger decline from 1.0146 is ready to resume through 0.8551 low.

US 10-Year Yields Dip Following Treasury Auction Plan, Eyes on FOMC Decision

US 10-year yields is seeing a notable drop after Treasury unveiled its auction plan. In a closely monitored move, the department announced a USD 2B/month increase in 10-year bond sales. This increment was below market's anticipated USD 3B hike. The decision appears to bolster 10-year treasury price, subsequently pressing down 10-year yield. US stock futures echoed this positive sentiment with a rebound, though the currency market remains largely unaffected at this stage.

Attention now shifts to the impending ISM services data, but the main event on investors' radar is the Federal Open Market Committee (FOMC) rate decision. While no changes in interest rates are expected today, market participants are keen to discern the tone of the statement and Chair Jerome Powell's stance on the necessity of further tightening. Powell's views on the correlation between rising longer-term yields and the potential reduction in tightening necessities will be under scrutiny. However, it's widely believed that December's meeting, which will present new economic forecasts, holds more significance, rendering today's decision potentially uneventful.

The currency arena presents a diverse picture today. Both Aussie and Yen are witnessing upward movement, the latter buoyed by verbal interventions from Japan. Swiss Franc is also on an upward trajectory. Conversely, Euro and Sterling find themselves on the softer end of the spectrum. Dollar ranks as the third weakest performer, showing a muted reaction to the ADP private job data.

Technically, an extended recovery in NASDAQ might be seen today, subject to the outcome of FOMC. But near term outlook will stay bearish as long as 13170.39 resistance holds. Fall from 14446.55 is in favor to continue. More importantly, another decline and firm break of near term channel support could trigger downside acceleration to 61.8% retracement of 10088.82 to 14446.55 at 11753.47 next.

In Europe, at the time of writing, FTSE is up 0.29%. DAX is up 0.38%. CAC is up 0.35%. Germany 10-year yield is up 0.018 at 2.832. Earlier in Asia, Nikkei rose 2.41%. Hong Kong HSI dropped -0.06%. China Shanghai SSE rose 0.14%. Singapore Strait Times rose 0.29%. Japan 10-year JGB yield rose 0.0101 to 0.959.

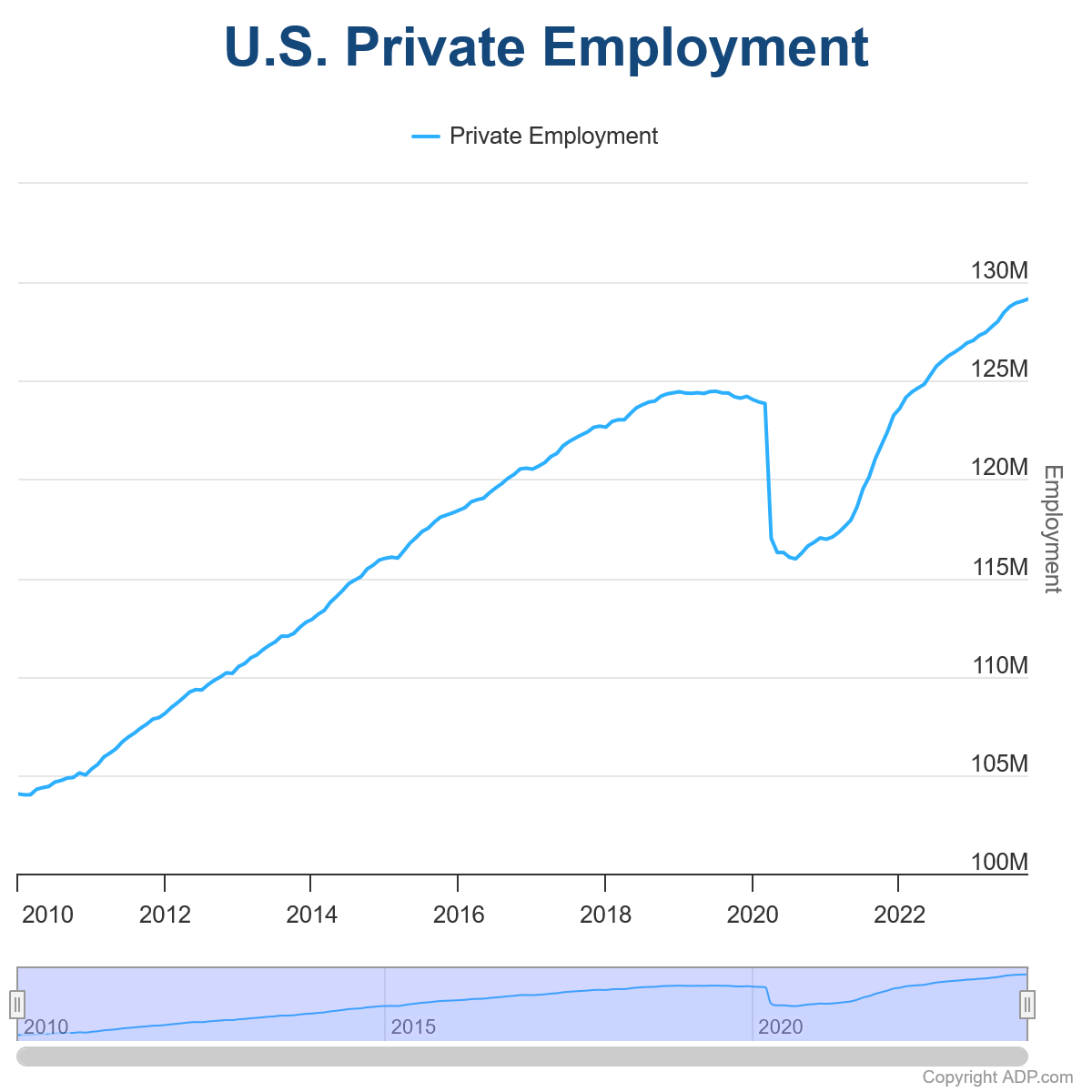

US ADP jobs grows 113k, slowing wage momentum

US ADP private sector employment gains in October fell short of expectations, with an addition of 113k jobs as opposed to the anticipated 135k. A breakdown by industry shows a modest increase of 6k in goods-producing jobs, while service sector added 107k. When considering the size of establishments, small firms contributed 19k jobs, medium-sized businesses accounted for 78k, and large enterprises added 18k.

A notable trend emerged in the wage segment. Employees who remained in their current positions reported a year-over-year pay growth of 5.7%, marking the slowest rate since October 2021. On the other hand, individuals who switched jobs experienced an 8.4% rise in wages, which is the least impressive figure since July 2021.

Nela Richardson, ADP's Chief Economist stated, "October didn't see a particular industry taking the lead in hiring. Moreover, the significant wage hikes we observed in the post-pandemic phase seem to be waning."

She further added, "The data from October offers a comprehensive view of the employment sector. Although there's a deceleration in the job market, it's still adequately robust to sustain vigorous consumer expenditure."

UK manufacturing downturn persists: PMI edges up but optimism plummets

UK PMI Manufacturing data was finalized at 44.8 in October, marking a modest improvement from September's 44.3. However, the report by S&P Global underscores some concerning aspects: declining output, a drop in new orders, and shrinking employment. Furthermore, business optimism has plunged to a ten-month low.

Rob Dobson, Director at S&P Global Market Intelligence, underscored the severity of the situation. "The UK manufacturing downturn persisted at the outset of the final quarter, exacerbating the economy's flirtation with recession," he said.

"The ongoing contraction in production for eight straight months, the longest since the 2008-09 period, is primarily due to subdued domestic and international demand, resulting in a continued downturn in new order intakes."

Dobson highlighted the skewed risks towards a negative outlook, with businesses' growing caution leading to employment cuts, reduced purchasing, and lower inventory levels.

Although there's a silver lining with a slight ease in input prices and output charges, Dobson warned that this faint inflation relief comes with an increased risk of recession, stemming from the prevailing weak demand.

Japan PMI manufacturing: Slump continues, yet optimism shines for 2024

Japan's PMI Manufacturing for October was finalized at 48.7, a slight uptick from 48.5 in September. Despite the improvement, the index languished below the critical 50 threshold for the fifth consecutive month.

S&P Global's analysis revealed that a significant decline in output occurred due to persisting sales reductions. This challenging environment also led to the first drop in employment figures since the beginning of 2021. On the brighter side, confidence remains robust regarding a potential return to growth in 2024.

NZ employment down -0.2% in Q3, unemployment rate jumps to 3.9%

New Zealand's employment figures for Q3 came in weaker than anticipated. Employment contracted by -0.2%, sharply diverging from the forecasted growth of 0.40%.

Unemployment rate made a noticeable leap, rising from 3.6% to 3.9%, a figure that met market expectations. Additionally, both employment rate and labor force participation rate registered declines, moving from 69.8% to 69.1% and from 72.5% to 72.0% respectively.

Wage data presented a mixed picture. The all-sector wage inflation stood firm at 4.3% yoy.

The public sector experienced a particularly sharp uptick in salaries and wages, registering a 5.4% yoy increase. This significant rise is notable for being the steepest since the data series commenced in 1992, surpassing 4.2% yoy growth observed in Q2.

In contrast, the private sector saw wage cost inflation moderating to 4.1% yoy in Q3, slightly down from the 4.3% recorded in the previous quarter.

China's Caixin PMI manufacturing slips to 49.5, business optimism continues to wane

China's Caixin PMI Manufacturing index slipped from 50.6 in September to 49.5 in October, falling below market expectations set at 50.8. This marks a renewed contraction in the nation's manufacturing sector.

Wang Zhe, Senior Economist at Caixin Insight Group, highlighted several challenges facing the manufacturing industry. "Overall, manufacturers were not in high spirits in October," he said. The decline in the sector was multifaceted - supply, employment, and external demand all experienced reductions, while domestic demand saw a slower pace of expansion.

The manufacturing environment was further complicated by rising costs and output prices. This was coupled with decrease in purchases and accumulation of inventories of finished goods. Reflecting the various pressures, "business optimism continued to wane".

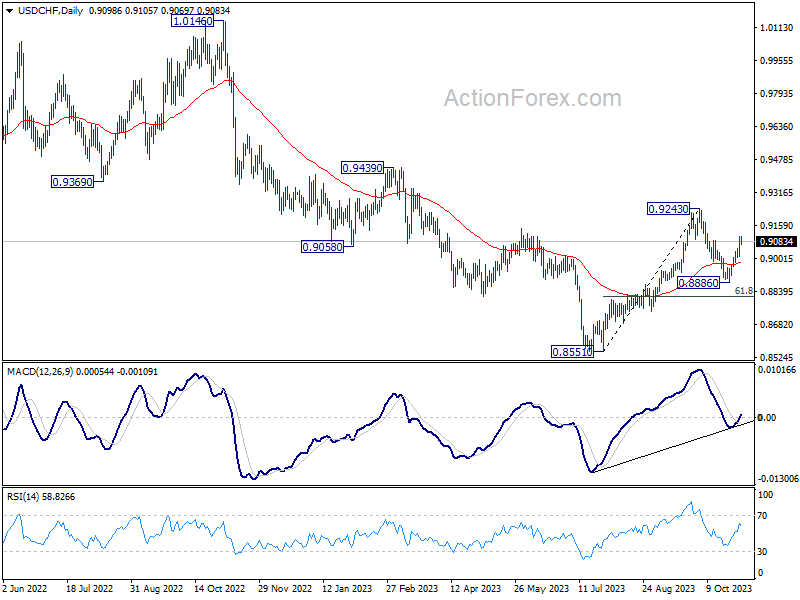

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9040; (P) 0.9074; (R1) 0.9139; More....

Despite current retreat, intraday bias in USD/CHF stays on the upside first. Sustained trading above 0.9086 resistance will pave the way back to 0.9342 resistance next. In any case, further rally will remain in favor as long as 0.9007 support holds. But firm break of 0.9007 will turn bias to the downside for 0.8886 support instead.

In the bigger picture, outlook is mixed up by the deeper than expected pull back from 0.9243. Yet there was no follow through selling after hitting 0.8886. On the upside, break of 0.9243 resistance will revive the case of medium term bottoming at 0.8851, and turn outlook bullish. However, sustained break of 61.8% retracement of 0.8551 to 0.9243 at 0.8815 will argue that larger decline from 1.0146 is ready to resume through 0.8551 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Employment Change Q3 | -0.20% | 0.40% | 1.00% | |

| 21:45 | NZD | Unemployment Rate Q3 | 3.90% | 3.90% | 3.60% | |

| 21:45 | NZD | Labour Cost Index Q/Q Q3 | 0.80% | 1.00% | 1.10% | |

| 00:30 | AUD | Building Permits M/M Sep | -4.60% | 2.60% | 7.00% | 8.10% |

| 00:30 | JPY | Manufacturing PMI Oct F | 48.7 | 49 | 48.5 | |

| 01:45 | CNY | Caixin Manufacturing PMI Oct | 49.5 | 50.8 | 50.6 | |

| 08:30 | CHF | Manufacturing PMI Oct | 40.6 | 45 | 44.9 | |

| 09:30 | GBP | Manufacturing PMI Oct F | 44.8 | 45.2 | 45.2 | |

| 12:15 | USD | ADP Employment Change Oct | 113K | 135K | 89K | |

| 13:30 | CAD | Manufacturing PMI Oct | 47.5 | |||

| 13:45 | USD | Manufacturing PMI Oct F | 50 | 50 | ||

| 14:00 | USD | ISM Manufacturing PMI Oct | 49 | 49 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid Oct | 44.5 | 43.8 | ||

| 14:00 | USD | ISM Manufacturing Employment Index Oct | 51.2 | |||

| 14:00 | USD | Construction Spending M/M Sep | 0.40% | 0.50% | ||

| 14:30 | USD | Crude Oil Inventories | 1.5M | 1.4M | ||

| 18:00 | USD | Fed Interest Rate Decision | 5.50% | 5.50% | ||

| 18:30 | USD | FOMC Press Conference |

Fed Likely to Stick to (Slightly Less) Hawkish Script, Manufacturing PMI’s Remain Weak

We're seeing some trepidation in markets on Wednesday ahead of the Federal Reserve meeting later in the session and the jobs report on Friday.

The Fed meeting should be quite straightforward, with policymakers having come out in force to soothe market fears of another rate hike from the central bank, claiming recent moves in bond markets may have done some of the job for them.

This followed previous commentary that strongly hinted that another rate hike is likely, aligning with the dot plot from the September meeting, while warning that rates will stay high for a long time.

With no new forecasts due today, it's all about the tone from policymakers and Chair Jerome Powell, and with bond yields still near their recent highs, I see little chance of another shift.

I expect the Fed Funds Rate will be left unchanged at 5.25-5.5% and the corresponding commentary will be almost a carbon copy of recent statements. This isn't the time to tweak as the economic data hasn't yet justified it either way, particularly to policymakers who are not going to pivot until they're absolutely certain they've defeated inflation.

Manufacturing PMIs remain weak but signs of promise in China

We've had a selection of manufacturing PMIs this morning and, as we've come to expect, they weren't particularly surprising. The Caixin survey in China dipped back into contraction territory, in line with what we saw from the official reading yesterday, but there is some optimism that circumstances are gradually improving and will continue to do so, despite the obvious challenges.

The UK manufacturing PMI only marginally improved and less than what was expected. It remains deep into contraction territory and isn't expected to significantly improve any time soon. While far from ideal, it is only a small portion of the UK economy, with the services sector far more important to how it performs, and while that's also in contraction, it is so to a much lesser extent.

Easing geopolitical risk sees Oil further pare gains

Oil prices are rebounding today but broadly speaking we're continuing to see them drift back to levels not seen since the Hamas attack on Israel. The geopolitical risk-premium has gradually faded, with traders seemingly more hopeful that it isn't going to spread into a wider conflict and disrupt oil flows.

The economy also remains a concern, especially considering what we're seeing with bond yields and the prospect of interest rates remaining higher for longer. I'm not convinced rates will remain at or near the peak that long but with policymakers around the world insisting they will, traders are increasingly concerned about the economic cost.

Gold eases ahead of the Fed decision

Gold has pulled back a little this week but remains not far from recent highs. It's even broken $2,000 on a number of occasions in the recent sessions, albeit not significantly or for long. The risk environment hasn't improved in any significant way and yields are not far from the highs which probably explains why gold hasn't progressed either way in any significant manner.

The dollar has remained strong and will continue to be a headwind, although in this environment perhaps not to the extent is has in the past. The Fed could spring a surprise later today, although I imagine we may have to wait for the jobs numbers on Friday which will be key as a result of the incredible resilience in the labour market.

Japanese Yen Stabilizes on Intervention Threat

- Yen steadies after intervention warning

- Fed widely expected to pause at today’s meeting

The Japanese yen has steadied on Wednesday, following massive losses a day earlier. In the European session, USD/JPY is trading at 151.19, down 0.34%.

Tokyo warns of intervention after yen plunges

It was Black Tuesday for the Japanese yen, which plunged 1.78% and fell as low as 151.71, its lowest level since October 2022. The massive decline was in response to the Bank of Japan stating it would “patiently” maintain its ultra-loose policy. The BoJ kept in place its 1% upper limit on 10-year government bond yields but redefined this upper limit as a “reference” rather than a hard cap.

The BoJ tweak is apparently an attempt to abandon its yield control curve (YCC) policy without too much fanfare. The move clearly didn’t impress investors as the yen took a tumble. The Japanese currency has stabilized today, courtesy of jawboning from Masota Kanda, the top currency official at the Ministry of Finance (MoF).

Kanda said that the MoF is on “standby”, the same type of language he used a year ago when the MoF intervened on the currency markets, and warned that he was “very concerned about one-sided, sudden moves in currencies”. Kanda wouldn’t say what he would do but he accused speculators of being responsible for the yen’s recent moves. Today’s verbal intervention may have halted the yen’s slide for now, but with the US/Japan rate differential continuing to widen and I would expect the downswing to continue, absent an intervention on the currency markets.

The Federal Reserve winds up its two-day meeting today and the markets have fully priced in rate pause, which would keep the benchmark rate at 5.25%-5.50%. That doesn’t mean that the meeting is without significance. Investors will be looking for signals as to what the Fed plans to do next. Fed Chair Powell has been hawkish about inflation and I wouldn’t be surprised if he reiterated the same message at today’s meeting.

USD/JPY Technical

- There is resistance at 151.97 and 152.85

- USD/JPY is testing support at 150.51. Below, there is support at 150.51

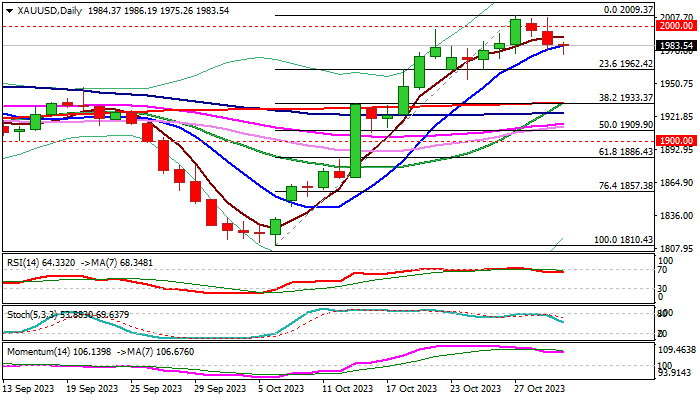

XAU/USD: Gold Consolidating After Failure at $2000 Barrier

Gold remains at the back foot for the third consecutive day, following another failure to sustain gains above psychological $2000 level.

Yellow metal ‘s price hit new multi-month high at $2009 last Friday, but subsequent return below $2000 points to persisting headwinds at this zone.

Gold rallied strongly in October (up 7.3%) driven by strong safe-haven demand after the conflict in Middle East started, adding to already fragile geopolitical situation and prompting investors out of riskier assets.

Dips were so far shallow and contained by rising daily Tenkan-sen / broken Fibo 61.8% of $2080/$1810 downtrend ($1983/77 respectively), with ability to hold above these levels to signal limited consolidation ahead of fresh attempt higher.

Deeper pullback, however, should find firm ground at $1960/50 zone to mark a healthy correction and keep larger bulls unharmed.

Daily studies remain bullish, with current pullback so far seen as technical correction, sparked by overbought conditions.

US Federal Reserve ends its policy meeting today and the decision is expected to strongly influence metal’s price.

Wide expectations that the central bank will keep the policy unchanged would offer fresh support to gold, though, investors will be also looking for the Fed’s assessment of the US economy, which would provide more clues about central bank’s action in the near future.

Bullish bias expected above $1962/53 (Fibo 23.6% of $1810/$2009/Oct 24 trough) while break lower would put bulls on hold and risk attack at lower pivot at $1933 (200DMA / Fibo 38.2%).

Conversely, sustained break of $2000 zone would generate initial signal of bullish continuation and expose targets at $2009, $2048 and $2080.

Res: 1990; 2000; 2009; 2021.

Sup: 1975; 1962; 1953; 1933.

US ADP jobs grows 113k, slowing wage momentum

US ADP private sector employment gains in October fell short of expectations, with an addition of 113k jobs as opposed to the anticipated 135k. A breakdown by industry shows a modest increase of 6k in goods-producing jobs, while service sector added 107k. When considering the size of establishments, small firms contributed 19k jobs, medium-sized businesses accounted for 78k, and large enterprises added 18k.

A notable trend emerged in the wage segment. Employees who remained in their current positions reported a year-over-year pay growth of 5.7%, marking the slowest rate since October 2021. On the other hand, individuals who switched jobs experienced an 8.4% rise in wages, which is the least impressive figure since July 2021.

Nela Richardson, ADP's Chief Economist stated, "October didn't see a particular industry taking the lead in hiring. Moreover, the significant wage hikes we observed in the post-pandemic phase seem to be waning."

She further added, "The data from October offers a comprehensive view of the employment sector. Although there's a deceleration in the job market, it's still adequately robust to sustain vigorous consumer expenditure."