Sample Category Title

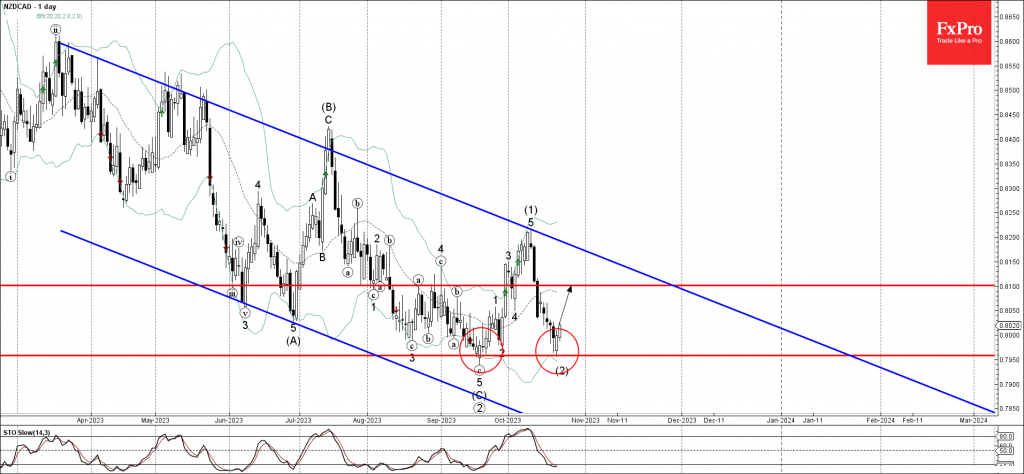

NZDCAD Wave Analysis

- NZDCAD reversed from support level 0.7960

- Likely to rise to resistance level 0.8100

NZDCAD currency pair recently reversed up with the Piercing Line from the key support level 0.7960 (which stopped the sharp downtrend in September).

The support level 0.7960 was strengthened by the nearby lower daily Bollinger Band , as can be seen below.

Given the strength of the support level 0.7960 and the oversold daily Stochastic, NZDCAD can be expected to rise further toward the next resistance level 0.8100.

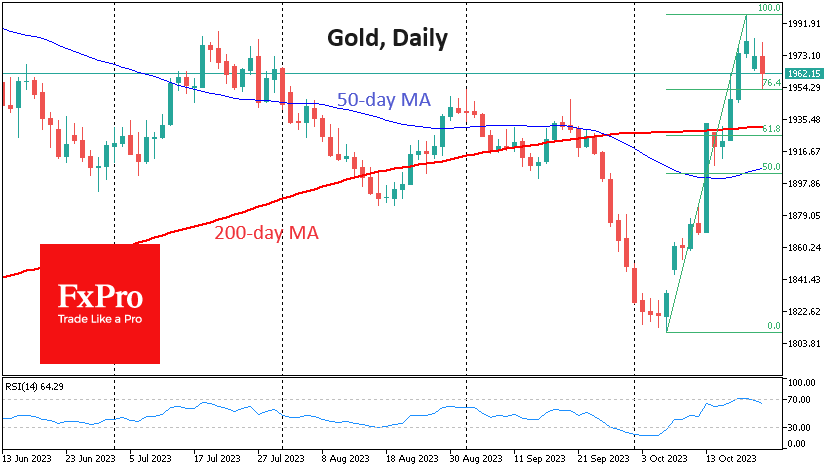

Gold Rally Runs Out of Steam

Gold is experiencing profit-taking after an impressive rally following the escalation in the Middle East.

The cost of a troy ounce of gold was down to $1955 at the peak of the European session on Tuesday, after a two-week rally from $1811 to almost $2000 since the 6th of October.

This week’s opening with a gap down was a sign that the market had built considerable profit-taking demand. The gap was closed during the day, but the decline continued Tuesday.

The market blew off steam just as the daily RSIs hit overbought levels. If this is not some short-term market noise, a full-blown correction of the latest rally would take the price to $1925, up to 61.8% of the initial advance.

Theoretically, there is a more bullish scenario for gold. According to this, today’s pullback to $1955, or 76.4%, has already removed some overbought conditions and spurred enough buying demand to increase the price.

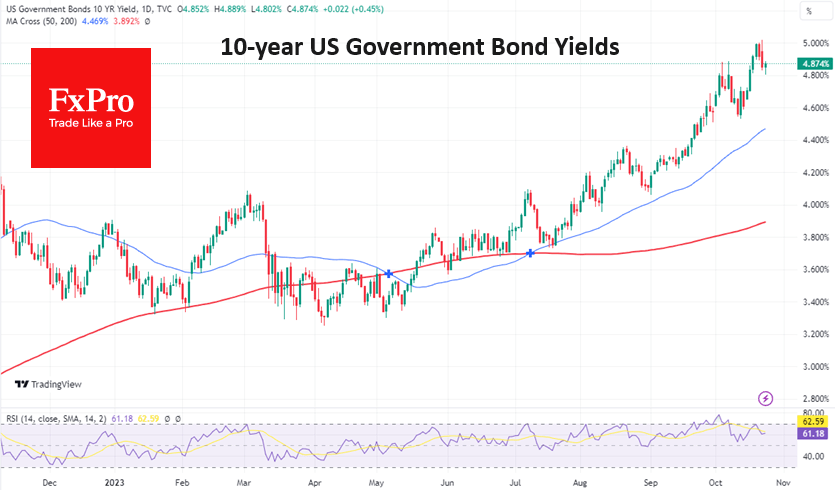

Looking at other markets, we continue to believe that the selling of gold is not yet complete. US 10-year Treasury yields approached 5% at the end of last week and briefly breached that level on Monday. But this attracted buyers into bonds, making the case for a yield top (price bottom).

While we often hear that rising government bond yields are bearish for gold, it is unlikely that significant capital will buy into a falling market to avoid catching a falling knife. Signs of a bottom forming could trigger an essential shift in the overriding trade, triggering a capital flow out of gold and into bonds.

The timing of this shift is also appropriate, as it is often in October that we see a change in long-term trends with the start of a new fiscal year. A year ago, such a shift was the stock market reversal and the beginning of a weakening dollar. And now it could be the emergence of interest in beaten-down long-term US bonds to the detriment of gold and possibly equities, whose yields are now lower than most debt market securities.

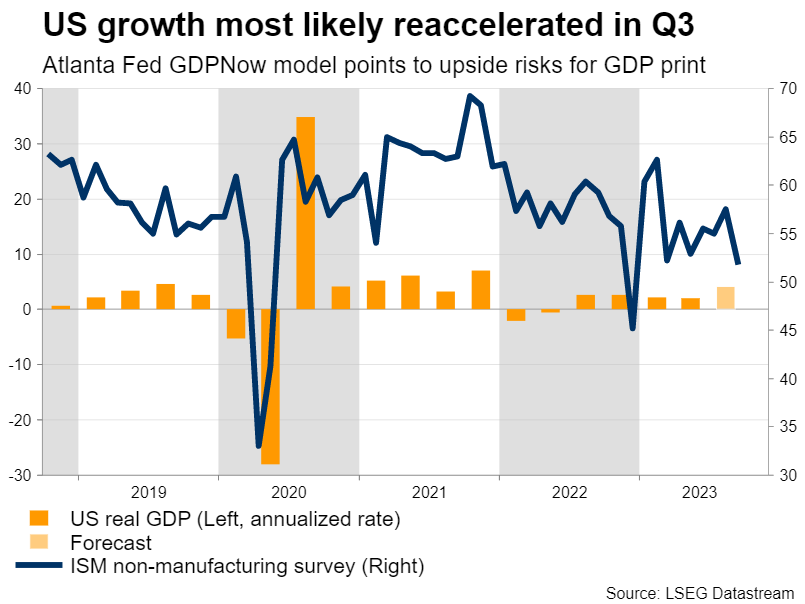

Will US GDP Stats Exceed Forecasts?

- Dollar takes a step back ahead of quarterly US GDP data

- Risks seem tilted towards stronger-than-expected report

- GDP release is scheduled for 12:30 GMT on Thursday

US economy outperforms

It's been a solid year for the American economy, which has performed well even in the face of sky-high interest rates. Economic growth seems to have accelerated over the summer as consumers continued to spend, supported by a labor market that remains exceptionally strong.

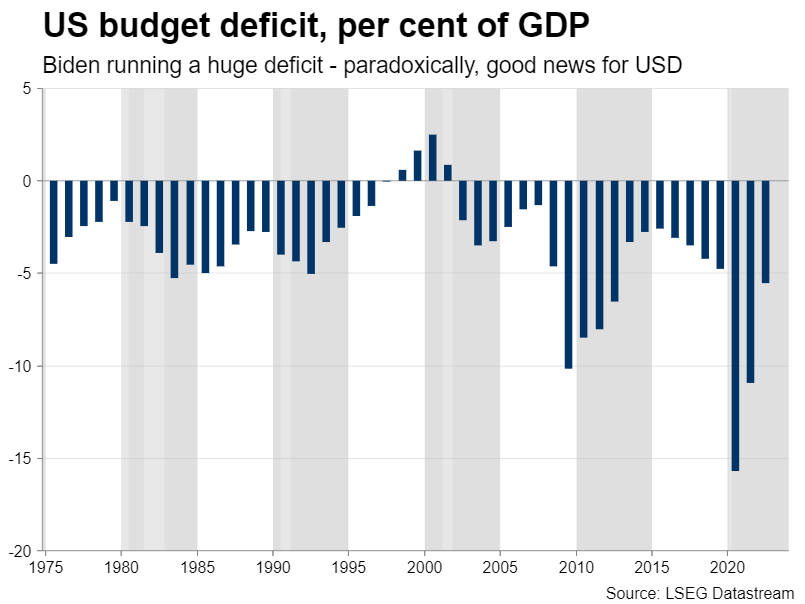

Another factor behind this resilience has been the government's heavy spending. The US government is running an enormous budget deficit, which at 5.5% of GDP is the largest deficit the country has ever run outside of recessionary periods or major wars.

This tremendous spending has helped safeguard economic growth, but it has also sent borrowing costs spiraling higher. Yields on longer-dated US government bonds briefly topped 5% for the first time since 2007, as the Treasury continues to flood markets with newly-issued debt to fund its budget shortfalls.

Even though it appears fiscally irresponsible, this situation has been a blessing for the dollar. The US currently enjoys the strongest growth among the G10 nations and offers the highest real yields, making the dollar more attractive both from an economic and an interest rate perspective.

Positive GDP surprise?

Turning to the upcoming dataset, GDP growth is anticipated to have reached an annualized pace of 4.2% in the third quarter, which is double the 2.1% achieved in the second quarter. Such an acceleration would be impressive, and there is even some scope for an upside surprise.

The Atlanta Fed has a model that estimates GDP in real time and it currently points to a growth rate of 5.4% for the third quarter, far higher than the official forecasts by economists. This model has a solid track record, so if there is any surprise in this dataset, it is more likely to be positive rather than a disappointment.

A GDP report that exceeds estimates could light another fire under US yields and in the process, help the dollar resume its uptrend. Looking at the euro/dollar chart, the first major obstacle for sellers to overcome might be near 1.0500. On the flipside, a disappointment in this data could bring the recent high of 1.0695 back into play.

Beyond the GDP stats, there are several other US releases that could also impact markets this week. Durable goods orders for September will be released on Thursday as well, while on Friday, the core PCE price index will hit the markets alongside personal consumption and income numbers for the same month. The core PCE index will be closely scrutinized by Fed officials and investors to get a sense of whether inflation continues to cool, as forecasts suggest.

Dollar remains attractive

All told, the US dollar seems like the most attractive major currency at this stage. It enjoys the strongest economic growth among the developed economies and also offers the highest real interest rates, a combination that is music to the ears of investors.

At the same time, there's no real alternative in the FX market. The euro has been plagued by recession concerns, the yen has been crippled by interest rate differentials as the Bank of Japan refuses to raise rates, and the problems in China are dimming the outlook for commodity currencies like the Australian or New Zealand dollars.

Now to be clear, the US faces several risks as well. Consumer savings from the pandemic have already run out and with student debt repayments resuming too, this could dampen spending and growth next year. But even if the American economy loses steam, it would still be in better shape than other regions.

Therefore, it seems like there's no credible alternative to the dollar for now. That's particularly true when considering the dollar's safe-haven qualities as well, which might come into play if the global economy continues to struggle.

Sunset Market Commentary

Markets

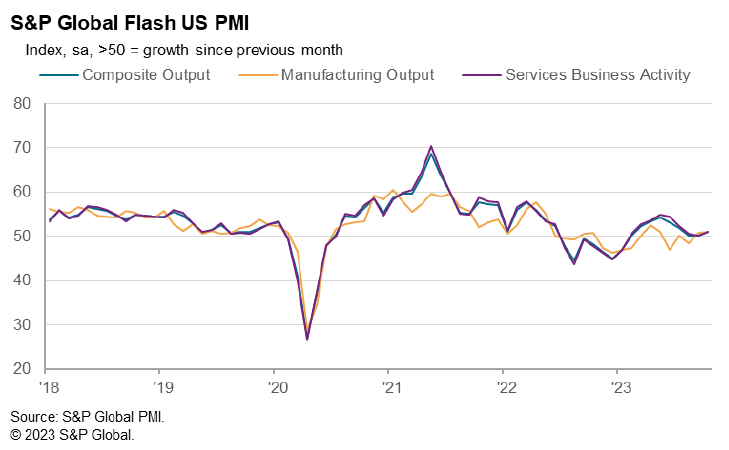

Softer-than-expected European October PMIs were a perfect excuse for core bonds to build on yesterday’s remarkable intraday U-turn. In a Germany-led decline, the composite figure dropped from 47.2 to 46.5, more than offsetting the September uptick . Both manufacturing (43.0 from 43.4) and services (47.8 from 48.7) are in contraction territory at the start of 2023Q4. PMI owner S&P Global called the situation moving from bad to worse, expecting a recession with back-to-back negative quarterly growth in Q3 and Q4. New orders continue to drop at one the quickest paces since 2009 in manufacturing and January 2021 in services. In response to the activity slowdown and accelerated depletion of backlogs, the private sector shed personnel for the first time since January 2021 even as the service sector’s gauge still printed slightly above the neutral 50 barrier. Input costs fell across the private economy but cost inflation in the services sector remains higher than at any time in the pre-pandemic period since 2008 with wages often cited as a key driver. Prices charged (output inflation) rose at a marginally weaker rate in October than in September at the lowest since February 2021. The PMI publication coincided with the ECB’s Q3 lending survey, which showed credit standards having tightened further across all loan categories and loan demand retreating strongly. It all but cements the ECB’s expected rate pause at Thursday’s meeting. Lagarde in a call on Monday with high-ranked European officials said the economy faces stagnation for the next few quarters while adding that the fight against inflation is going well. German yields at a given point dropped almost 10 bps at the long end of the curve but quickly pared much of those losses. Net daily changes eventually amount to 0.1-3.8 bps. US Treasuries underperformed with yields adding to earlier gains after all US PMIs unexpectedly returned above 50, even if it is marginally. Changes vary between 1.7 (30-y) and 6.4 (2-y) bps adds 3.4 bps. The US dollar recoups some of the losses incurred in yesterday’s afternoon (European) trading. EUR/USD turned from close to but below 1.07 to just north of 1.06 currently. DXY bounced off 105.38 support to just shy of 106. UK PMIs were not at all convincing either (48.6 composite) but given their close-to-consensus outcome, sterling was temporarily able to take the upper hand against a euro in the defensive. EUR/GBP hit an intraday low of 0.8683 but isn’t planning to give up the 0.87 big figure that easily. The Hungarian forint is steady around EUR/HUF 381 and doesn’t underperform regional peers (CZK, PLN) after the central bank cut rates by a more than expected 75 bps to 12.25%. Front end yields drop up to 20 bps. Hungarian money markets expect the policy rate to further decline to around 10% by end 2023. Stocks in Europe rise 0.2%, erasing early losses. Wall Street opens with 0.4-0.8% gains.

News & Views

The October ECB Bank lending survey showed that credit standards (internal guidelines or loan approval criteria of banks) for credit to enterprises and to households tightened further in Q3. In both cases it exceeded the sector’s previous expectation. For Q4, Euro Area banks expect more tightening for loans to firms and for consumer credit, but they see broadly unchanged conditions for loans for housing purchases. At the same time banks reported a sharper than expected decline in loans of all categories (firms and households). The decline was mainly driven by higher interest rates as well as lower fixed investment and weaker consumer confidence. For Q4, banks see a further net decline in demand across all loan categories, albeit less pronounced than in Q3. Banks reported a deterioration in access to funding, especially retail funding due to increased competition for liquidity and other alternatives. The ECB reducing the asset portfolio contributed to the deterioration in market financing conditions and banks’ liquidity positions. This also applies to the phasing out of TLTRO operations. Banks project the positive impact of higher ECB interest rates on net interest rate margins to abate in de coming months. Further negative impact via higher provisions/impairments might be on the cards.

Spain’s Socialist Party and the Far-left Sumar group reached an agreement on a coalition. Amongst other plans, they intend to reduce the workweek to 37.5 hours. However, the coalition still needs to support of other parties, most probably of some parties advocating more independence for Catalunya. Acting PM Sanchez has until 27 November to find enough support in Parliament for a new term. If not, new elections will be called for January.

US PMI composite rose to 51.0, hopes of soft landing encouraged

US PMI Manufacturing ticked up from 49.8 to 50.0 in October. PMI Services rose from 50.1 to 50.9. PMI Composite rose from 50.2 to 51.0.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said:

"Hopes of a soft landing for the US economy will be encouraged by the improved situation seen in October. The S&P Global PMI survey has been among the most downbeat economic indicators in recent months, so the upturn in US output growth signalled at the start of the fourth quarter is good news. Future output expectations have also turned up despite rising geopolitical concerns and domestic political tensions, climbing to the joint-highest for nearly one-and-a-half years.

"Sentiment has improved in part due to hopes of interest rates having peaked, something which looks increasingly likely given the further cooling of inflationary pressures witnessed in October. In spite of higher oil prices, firms' input cost inflation fell sharply to the lowest since October 2020, and average selling prices for goods and services posted the smallest monthly rise since June 2020.

"The survey's selling price gauge is now close to its pre-pandemic long-run average and consistent with headline inflation dropping close to the Fed's 2% target in the coming months, something which looks likely to be achieved without output falling into contraction. That said, the tensions in the Middle East pose downside risks to growth and upside risks to inflation, adding fresh uncertainty to the outlook."

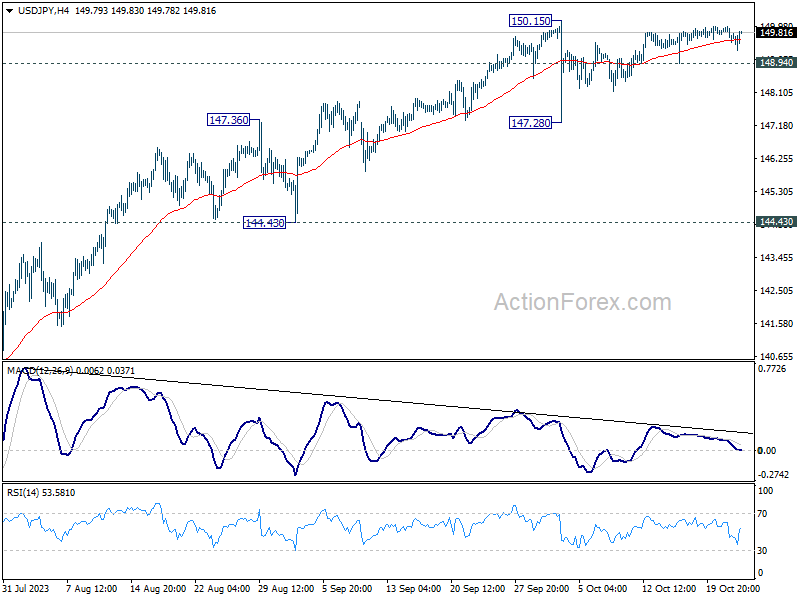

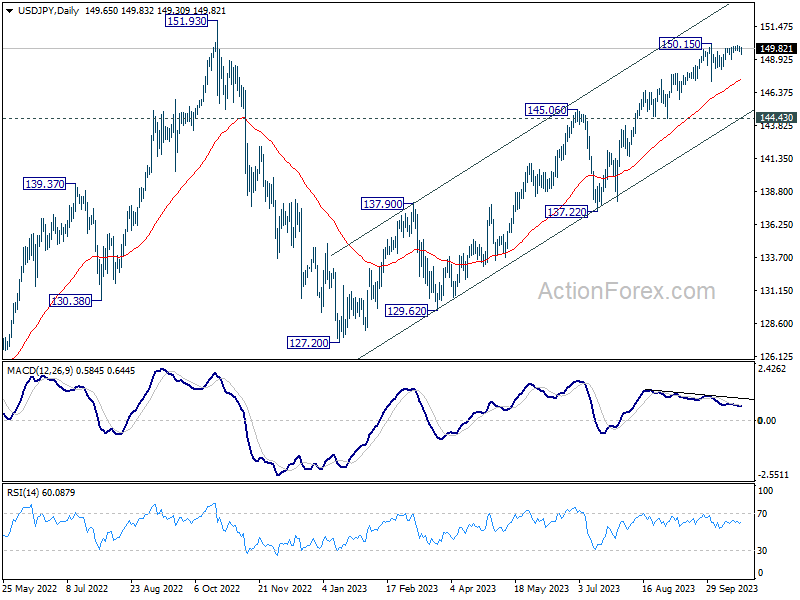

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.52; (P) 149.75; (R1) 149.95; More...

Intraday bias in USD/JPY remains neutral at this point. Consolidation pattern from 150.15 could extend further. On the downside, below 148.94 minor support will turn bias to the downside for another down leg towards 147.28. On the upside, firm break of 150.15 will resume larger up trend to test 151.93 high.

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by sustained break of 145.06 resistance turned support will be the first sign that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.

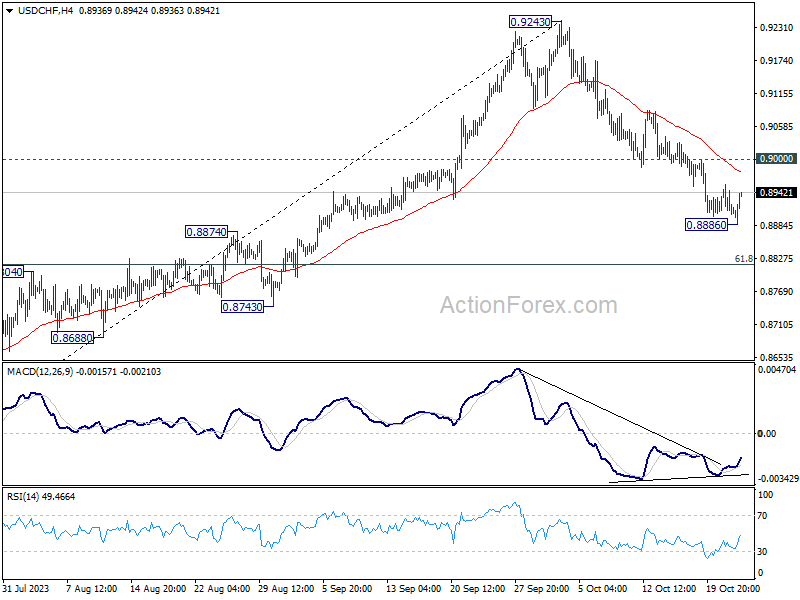

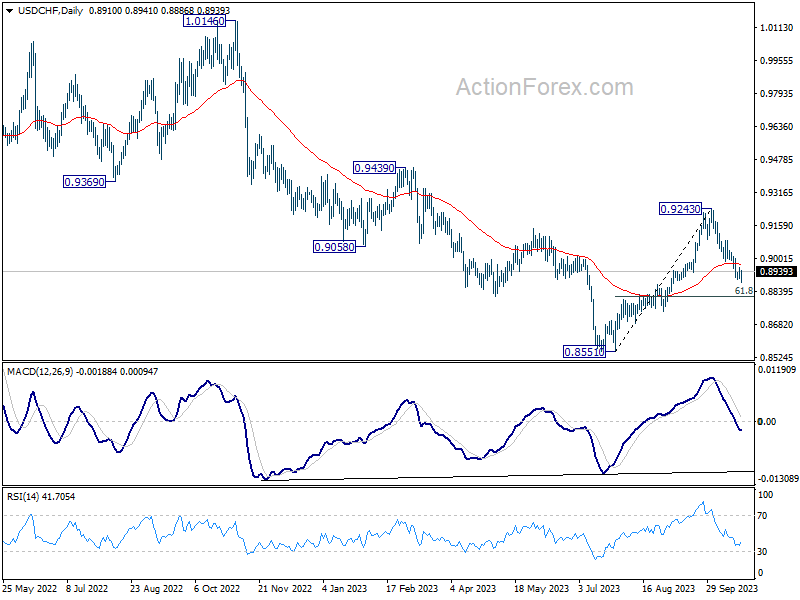

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8892; (P) 0.8925; (R1) 0.8945; More....

USD/CHF recovered quickly after a brief dip to 0.8886 and intraday bias remains neutral. Further decline is expected as long as 0.9000 resistance holds. Below 0.8886 will resume the fall from 0.9243 to 61.8% retracement of 0.8551 to 0.9243 at 0.8815 next. Sustained break there will pave the way to retest 0.8551 low. Nevertheless, break of 0.9000 will turn bias back to the upside for stronger rebound.

In the bigger picture, the firm break of 55 D EMA (now at 0.8974) argues that rebound from 0.8551 might be completed as a correction at 0.9243. In other words, larger fall from 1.0146 (2022 high) is possibly not over yet. Risk will now stay on the downside as long as 0.9243 resistance holds. Firm break of 0.8551 will confirm down trend resumption.

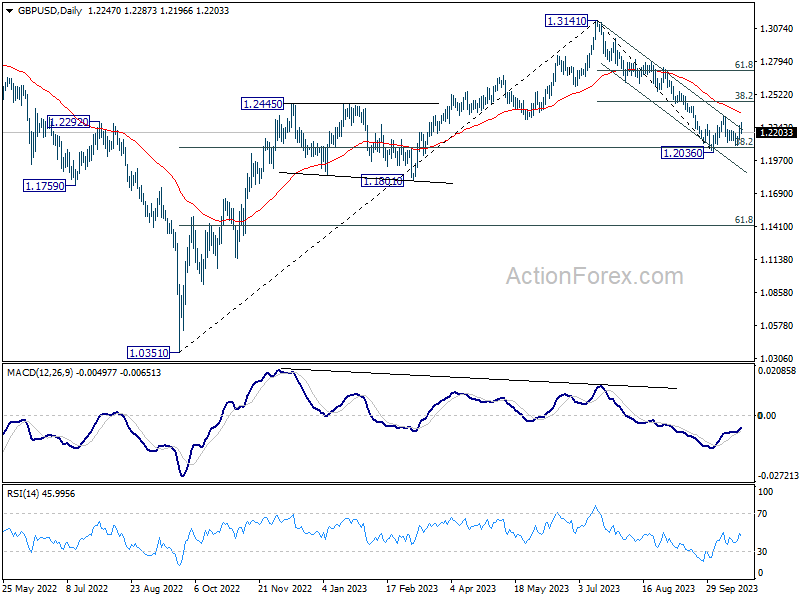

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2174; (P) 1.2216; (R1) 1.2290; More

Intraday bias in GBP/USD remains neutral as range trading continues between 1.2036/2336. Downside breakout is still mildly in favor. On the downside, decisive break of 1.2036 will resume whole decline from 1.3141 for 1.1801 support next. However, break of 1.2336 will turn bias back to the upside for 38.2% retracement of 1.3141 to 1.2036 at 1.2458.

In the bigger picture, fall from 1.3141 medium term top could still be a correction to up trend from 1.0351 (2022 low) only. But risk of complete trend reversal is rising. Sustained break of 38.2% retracement of 1.0351 to 1.3141 at 1.2075 will pave the way to 61.8% retracement at 1.1417. For now, risk will stay on the downside as long as 55 D EMA (now at 1.2384) holds, in case of rebound.

British Pound Edges Lower as Employment Market Cools

- UK labour market cools

- UK Manufacturing and Service PMIs decline

The British pound is slightly lower on Tuesday, after climbing 0.68% a day earlier. In the European session, GBP/USD is trading at 1.2218, down 0.23%.

UK job growth, unemployment rises

The UK has released “experimental” employment data on Tuesday, replacing the standard labour market survey due to falling response rates. The new reporting format didn’t change the fact that the UK labour market continues to lose steam. The unemployment rate held steady at 4.2%, unemployment rose by 74,000 and the number of employed people fell by 82,000. Last week’s wage growth report showed that wages including bonuses fell from 8.5% to 8.1% y/y for the three months to August, which is still very high and a significant driver of inflation.

Employment data is a key factor for the Bank of England, which will have to decide whether to raise rates or pause at the meeting on November 2nd. The BoE paused in September for the first time since the tightening cycle began in December 2021. Governor Bailey said at that meeting that positive inflation data had allowed the BoE to hold rates. There are no more tier-1 releases ahead of the November meeting, which means that investors will be listening carefully to any comments from Bailey & Co. ahead of the meeting.

The UK also released PMI reports today, which provided further evidence of a weak economy. The Manufacturing PMI improved slightly to 45.2 in October, up from 44.3 in September and above the market consensus of 44.7. Manufacturing has contracted for eight straight months, the longest downturn in 15 years. Services eased from 49.3 to 49.2 in October, missing the market consensus of 49.3. It marked the lowest level in nine months. The neutral 50 level separates contraction from expansion..

GBP/USD Technical

- GBP/USD is testing support at 1.2216. Below, there is support at 1.2174

- There is resistance at 1.2290 and 1.2332