Sample Category Title

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0601; (P) 1.0640; (R1) 1.0707; More...

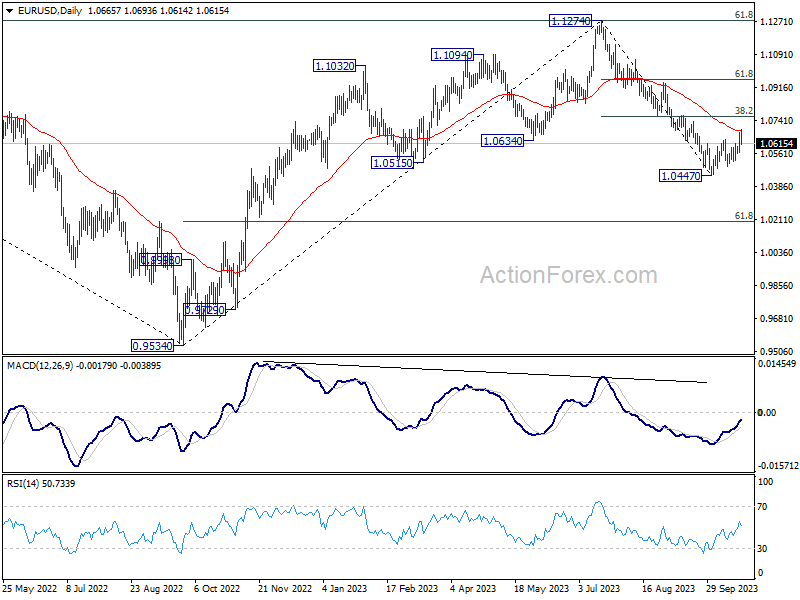

Intraday bias in EUR/USD is turned neutral again as it retreated notably today after hitting 55 D EMA (now at 1.0684). On the upside, above 1.0693 will resume the rebound to 1.0764 cluster resistance (38.2% retracement of 1.1274 to 1.0447 at 1.0763). On the downside, break of 1.0522 support will retain near term bearishness for resuming the whole decline from 1.1274 through 1.0447 next.

In the bigger picture, fall from 1.1274 medium term top could still be a correction to rise from 0.9534 (2022 low). But chance of a complete trend reversal is rising. In either case, current fall should target 61.8% retracement of 0.9534 to 1.1274 at 1.0199 next. For now, risk will stay on the downside as long as 55 D EMA (now at 1.0684) holds, in case of rebound.

Euro’s Rally Halted by Disheartening PMIs; Aussie Up on RBA’s Hawkish Tone ahead of CPI

Euro's forward drive this week faced a halt as subpar PMI readings painted a concerning picture for the Eurozone economy. The data fuels concerns that the Eurozone economy might be heading into deeper waters. At the same time, British Pound is weighed down by slowing wages growth and weak PMIs too. Swiss Franc is also on a similar downward slide following the European counterparts.

On the other hand, the Dollar is putting up a valiant effort to stabilize, though it's currently overshadowed by the Australian and New Zealand Dollars. Notably, Australian Dollar is drawing strength from comments by RBA Governor. The remarks underscored that potential rate hike remains on the table, depending largely on inflationary outlook. On the other hand, Japanese Yen and Canadian Dollar currently demonstrate a neutral stance without clear directional cues.

Shifting the spotlight to other markets, Gold witnesses a moderate dip, continuing its consolidation phase after last week's unsuccessful attempt on 2000 level. Concurrently, WTI crude oil displays a slight weakening sentiment as the market remains cautious, awaiting any escalations or de-escalations concerning Middle East tensions. Bitcoin, after a robust surge earlier, seems to be pausing for breath, steadying below the 35k mark. US 10-year yields exhibit a modest recovery, potentially laying the groundwork for another attempt to hit 5% level.

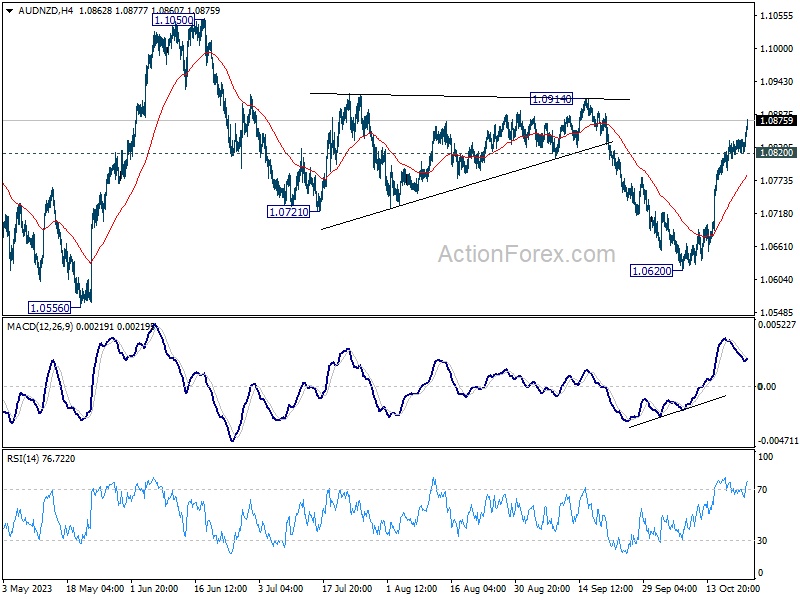

On a technical note, AUD/NZD is extending the rise from 1.0620, and further rally is expected as long as 1.0820 minor support holds. The corrective decline from 1.1050 should have completed with three waves down to 1.0620. Firm break of 1.0914 resistance would set the stage for stronger rise back to 1.1050 resistance. The next move will depend on tomorrow's Australia CPI and the implication for RBA meeting on November 7.

In Europe, at the time of writing, FTSE is down -0.09%. DAX is up 0.19%. CAC is up 0.51%. Germany 10-year yield is down -0.046 at 2.828. Earlier in Asia,Nikkei rose 0.20%. Hong Kong HSI dropped -1.05%. China Shanghai SSE rose 0.78%. Singapore Strait Times rose 1.00%. Japan 10-year JGB yield dropped -0.0201 to 0.854.

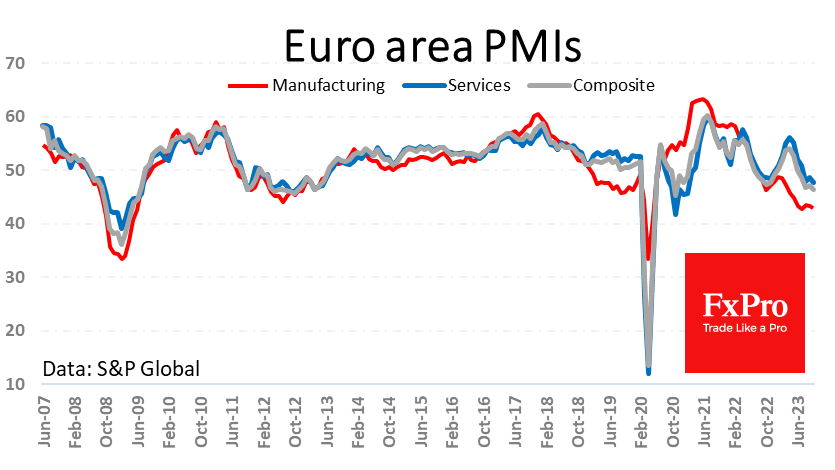

Eurozone PMI composite fell to 35-month low, moving from bad to worse

Eurozone economy appears to be on shaky ground, with the latest PMI figures showing continued deterioration. October saw Manufacturing PMI slide to 43.0 from 43.4, while Services PMI dropped to a concerning 32-month low of 47.8, down from 48.7. Composite PMI wasn't left behind, recording a 35-month low at 46.5, down from 47.2.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, stated, "In the Eurozone, things are moving from bad to worse." He highlighted that manufacturing has been grappling with a slump for over a year now. When examining the top Eurozone players, France and Germany, de la Rubia noted that their manufacturing downturns are almost on par.

However, it's not all gloom for France in the services sector. Despite a lower activity index compared to Germany, France showcases some resilience with new businesses not declining as rapidly. Moreover, companies in France are steadily adding jobs rather than eliminating them.

Another noteworthy aspect is the persistent price increases within the services sector. Comparing it to prior economic downturns, inflation for both input prices and prices charged has only marginally slowed down. This trend might be challenging for ECB. As de la Rubia points out, "these figures reinforce the case of a pause in the interest rate cycle instead of thinking aloud about loosening monetary policy."

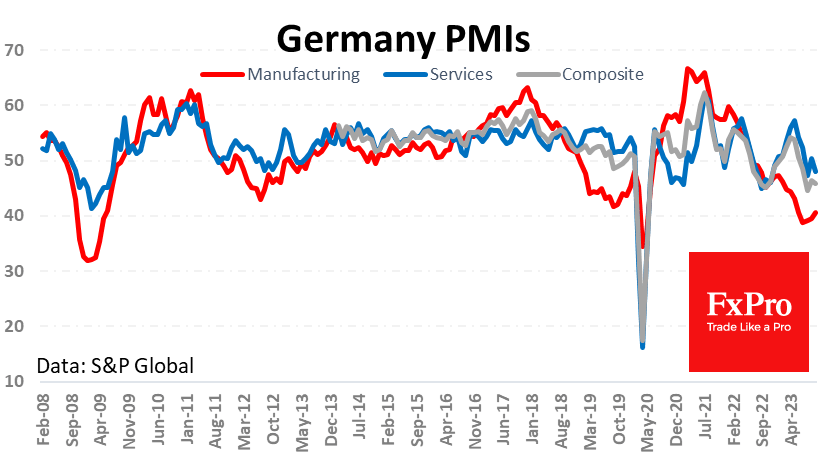

Germany PMI Manufacturing rose from 39.6 to 40.7 in October, a 5-month high. PMI Services fell from 50.3 to 48.0. PMI Composite fell from 46.4 to 45.8.

France PMI Manufacturing fell from 44.2 to 42.6 in October, hitting a 41-month low. PMI Services improved from 44.4 to 46.1, a 3-month high. PMI Composite rose from 44.1 to 45.3, a 2-month high.

Germany's Gfk consumer sentiment fell to -28.1, hope of recovery this year laid to rest

Germany's Gfk consumer sentiment for November fell from -26.7 to -28.1. In October, economic expectations improved slightly from -3.4 to -2.4. Income expectations fell form -11.3 to -15.3. Propensity to buy ticked up from -16.4 to -16.3. Propensity to save rose from 8.0 to 8.5.

"With the third decline in a row, hopes of a recovery in consumer sentiment this year must finally be laid to rest," explains Rolf Bürkl, consumer expert at NIM.

"Above all, high prices for food are weakening the purchasing power of private households in Germany, so private consumption will not be able to support the economy this year."

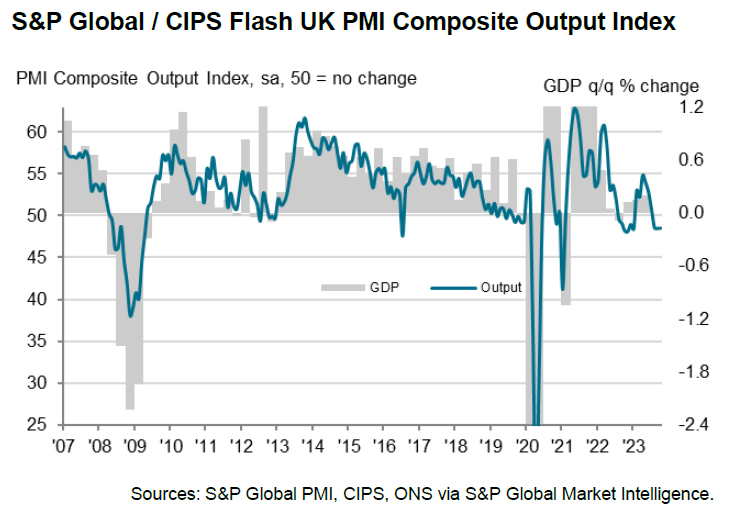

UK PMI composite ticks up to 48.6, recession cannot be ruled out

UK PMI Manufacturing saw a modest uptick, moving from 44.3 to 45.2 in October. In contrast, Services sector edged downwards, marking a 9-month low, albeit by a marginal decrement from 49.3 to 49.2. Composite PMI slightly climbed, positioning at 48.6 from a previous 48.5.

According to Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, the UK is treading dangerously close to recessionary waters. Williamson highlighted the combined impacts of the rising cost of living, soaring interest rates, and dwindling exports as the chief culprits behind a third consecutive month of diminishing output.

While the rate of economic decline is currently moderate, with predictions hinting at just a -0.1% quarterly GDP drop, the darkening cloud of economic uncertainty suggests tougher times might be ahead. "A recession, albeit only mild at present, cannot be ruled out," he added.

On a brighter note, the cost pressures evident earlier have started to soften, partly attributed to diminishing wage inflation and decline in prices set by manufacturers. Nonetheless, service sector continues to grapple with inflation, which even saw a slight bump. This indicates that headline inflation might persistently hover around the 4% range as we transition into early next year.

This poses a dilemma for policymakers, especially when factoring in potential inflationary pressures from surging oil prices. "It would be unlikely for policymakers to rule out the possibility of rates rising again later in the year," he said.

UK payrolled employment fell -11k in Sep, pay growth slowed to 5.7% yoy

In September, UK payrolled employment fell -11k. Median monthly pay rose 5.7% yoy, slowed notably from August's 7.7% yoy. Annual growth in median pay was highest in the transportation and storage sector, with an increase of 13.5%, and lowest in the health and social work sector, with a decrease of -0.3%.

In the three months to August, unemployment rate fell from 4.3% to 4.2%, below expectation of 4.3%.

RBA Bullock signals readiness to hike again if inflation outlook revised up

RBA Governor Michelle Bullock emphasized the central bank's ongoing commitment to stabilizing inflation and promoting job growth in her speech today. While the Governor acknowledged the possibility of maintaining the current cash rate level to achieve these objectives, she did not shy away from highlighting potential challenges. "There are risks that could see inflation return to target more slowly than currently forecast," she noted.

In response to the potential of inflationary pressures, Bullock assured that the Board remains vigilant: "The Board will not hesitate to raise the cash rate further if there is a material upward revision to the outlook for inflation."

As the Board gears up for its subsequent gathering, Bullock emphasized the significance of upcoming data. She mentioned, "The Board will receive several pieces of information before its next meeting that will be important for this assessment."

She elaborated on the forthcoming procedures, revealing, "This includes a full update of the staff's forecasts. We will reconsider the outlook for the economy in light of incoming information and will have opportunities to explain our assessment in the media release and Statement on Monetary Policy that will follow the November meeting."

Australia's PMI composite dives to 47.3, slowdown amid sticky inflation

Australia's economic indicators from October paint a worrisome picture, as PMI Manufacturing dipped to a six-month low at 48.0, down from 48.7. More significantly, PMI Services plunged to a 10-month trough, dropping from 51.8 to 47.6. PMI Composite, which combines both manufacturing and services, dropped to a concerning 21-month low of 47.3 from 51.5.

Weighing in on these figures, Warren Hogan, Chief Economic Advisor at Judo Bank, mentioned PMI output index reverting to cyclical lows around 47 after a brief rise above the neutral 50 mark in September. These PMI indicators resonate with the ongoing narrative that Australia's economic momentum has decelerated in 2023, aligning with the anticipated gentle slowdown most economists had projected.

A silver lining, however, emerges from the employment index, which remains steadfastly above the 50-mark. Hogan interprets this as a sign that the deceleration in business activities hasn't notably dampened hiring trends.

However, a significant area of concern highlighted by Hogan is the enduring nature of inflation pressures, which he refers to as "stickiness". Both input and output price indexes remain elevated, not hinting at an imminent return of inflation to RBA's target.

As RBA prepares for its board meeting, set to coincide with Melbourne Cup day, the latest PMI readings, especially concerning inflation, are unlikely to drastically influence the interest rate decision. Hogan articulated, "A strong case exists for a further modest upward adjustment to the Australian cash rate target, to ensure the economy remains on the so-called 'narrow path'. If we are to avoid recession, Australia will need an extended period of below-trend growth to ensure inflation returns to target by 2025."

Japan's PMI manufacturing unchanged at 48.5, worst slump in eight months

October saw Japan's PMI Manufacturing remain unchanged at 48.5, missing expectations of 48.9 and marking the fifth consecutive month showing deteriorating operating conditions. Additionally, PMI Services and PMI Composite displayed downturns, with the former dropping from 53.8 to 51.1 and the latter declining from 52.1 to a sub-50 figure of 49.9.

Jingyi Pan, Economics Associate Director at S&P Global Market Intelligence, noted that this is the first instance of a decline in business activity for the private sector since December 2022. The drop, albeit marginal, was primarily due to a more pronounced decrease in manufacturing output – the fastest rate seen in eight months. On the other hand, services activity did continue its expansion, albeit at its slowest pace for the year.

The overall sentiment among firms was not particularly encouraging either. They expressed the least optimism since the beginning of the year concerning future output, suggesting a tempered outlook for the immediate future. However, a silver lining in the employment sector, which saw a resurgence, particularly in the service sector.

On the pricing front, both manufacturing and service sectors experienced diminished cost pressures. This deceleration resulted in output prices within the private sector rising at their most muted pace since February 2022.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0601; (P) 1.0640; (R1) 1.0707; More...

Intraday bias in EUR/USD is turned neutral again as it retreated notably today after hitting 55 D EMA (now at 1.0684). On the upside, above 1.0693 will resume the rebound to 1.0764 cluster resistance (38.2% retracement of 1.1274 to 1.0447 at 1.0763). On the downside, break of 1.0522 support will retain near term bearishness for resuming the whole decline from 1.1274 through 1.0447 next.

In the bigger picture, fall from 1.1274 medium term top could still be a correction to rise from 0.9534 (2022 low). But chance of a complete trend reversal is rising. In either case, current fall should target 61.8% retracement of 0.9534 to 1.1274 at 1.0199 next. For now, risk will stay on the downside as long as 55 D EMA (now at 1.0684) holds, in case of rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:00 | AUD | Manufacturing PMI Oct P | 48 | 48.7 | ||

| 22:00 | AUD | Services PMI Oct P | 47.6 | 51.8 | ||

| 00:30 | JPY | Manufacturing PMI Oct P | 48.5 | 48.9 | 48.5 | |

| 06:00 | EUR | Germany Gfk Consumer Confidence Nov | -28.1 | -27.3 | -26.5 | -26.7 |

| 06:00 | GBP | Claimant Count Change Sep | 20.4K | 2.3K | 0.9K | -9.0K |

| 06:00 | GBP | ILO Unemployment Rate 3M Aug | 4.20% | 4.30% | 4.30% | |

| 07:15 | EUR | France Manufacturing PMI Oct P | 42.6 | 44.8 | 44.2 | |

| 07:15 | EUR | France Services PMI Oct P | 46.1 | 44.6 | 44.4 | |

| 07:30 | EUR | Germany Manufacturing PMI Oct P | 40.7 | 40.1 | 39.6 | |

| 07:30 | EUR | Germany Services PMI Oct P | 48 | 50.1 | 50.3 | |

| 08:00 | EUR | Eurozone Manufacturing PMI Oct P | 43 | 43.7 | 43.4 | |

| 08:00 | EUR | Eurozone Services PMI Oct P | 47.8 | 48.7 | 48.7 | |

| 08:30 | GBP | Manufacturing PMI Oct P | 45.2 | 45.2 | 44.3 | |

| 08:30 | GBP | Services PMI Oct P | 49.2 | 49.5 | 49.3 | |

| 12:30 | CAD | New Housing Price Index M/M Sep | -0.20% | 0.10% | 0.10% | |

| 13:45 | USD | Manufacturing PMI Oct P | 49.5 | 49.8 | ||

| 13:45 | USD | Services PMI Oct P | 49.9 | 50.1 |

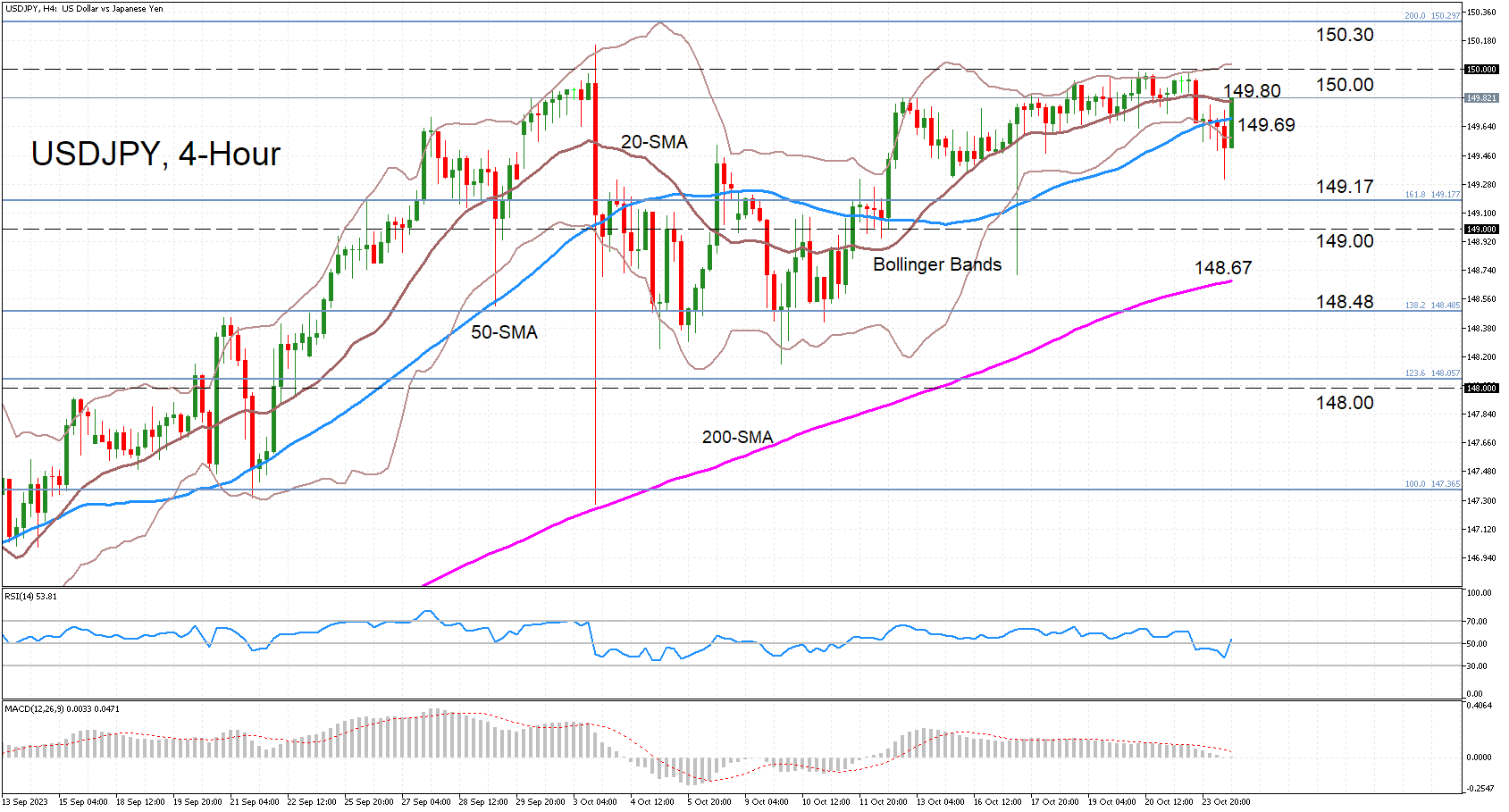

USDJPY Rebounds After Brief Bearish Episode

- USDJPY skids, slipping below moving averages in 4-hour chart

- But selloff is already fading and rebound underway

- Bigger picture remains neutral

USDJPY came under selling pressure during the past 24 hours, slipping to a one-week low of 149.31 earlier in today’s session. However, not only does the pair remain within its recent tight trading range, but also, the negative momentum appears to be receding.

After repeated failed knocks at the 150-door, USDJPY took a tumble, slipping below both the 20- and 50-period simple moving averages (SMA). The dive also took the price below the lower Bollinger band, signalling an imminent reversal, although the momentum oscillators did not turn overly bearish.

The RSI has now started to point upwards, reaching the 50 neutral threshold, while the MACD has flatlined at zero below its red signal line.

With the bulls attempting to push the price higher again, it will be essential to overcome the 20-period SMA, which is providing immediate resistance around 149.80, having already reclaimed the 50-period SMA. Clearing the 20-period SMA would set the stage for a re-challenge of the critical 150 level. However, even if there is a successful break above 150, the price would need to aim a little higher, such as the 200% Fibonacci extension of the August-September dip at 150.30 for a more convincing breakout.

Should the bearish forces manage to overpower again, the next stop south could be the 161.8% Fibonacci extension of 149.17 before touching base with the 200-period SMA at 148.67.

In brief, the latest slide seems to have been short lived and hasn’t made much of a dent, with the near- to-medium-term price action remaining comfortably within the recent sideways range defined by the 150 ceiling and the 138.2% Fibonacci floor. Only a major advance above 150 would mark the resumption of the longer-term uptrend.

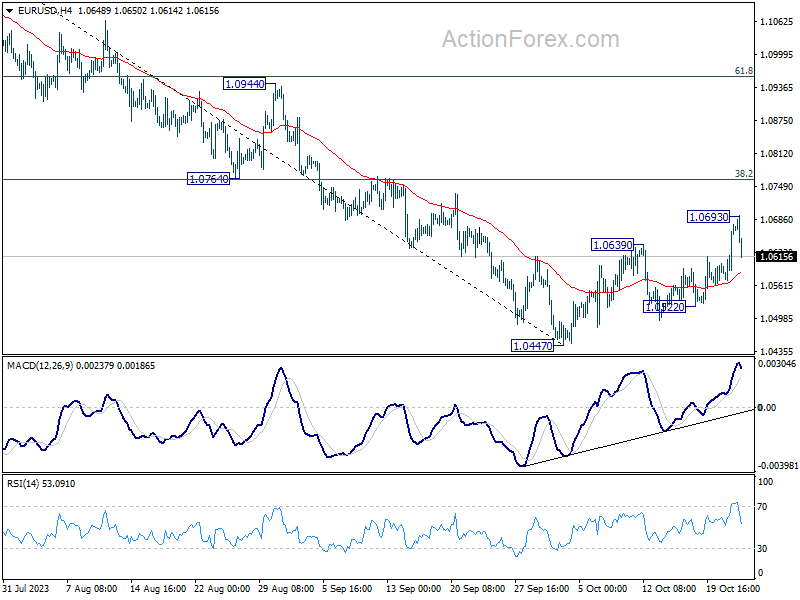

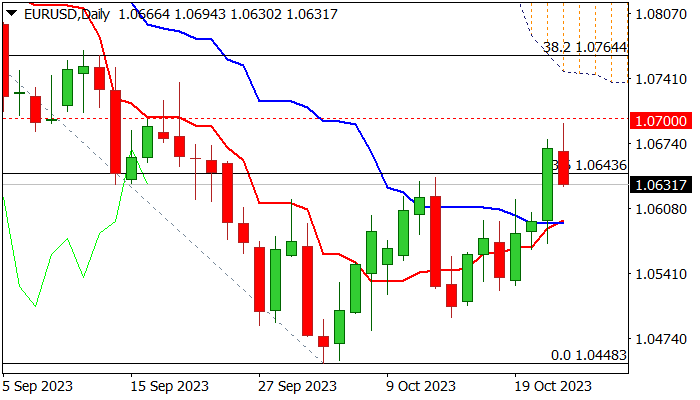

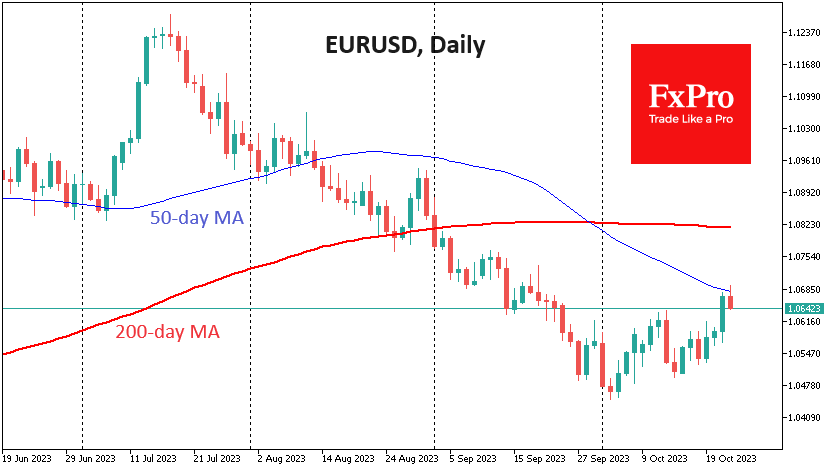

EUR/USD: Recovery Loses Traction after Weak PMI’s Hurt Fresh Bullish Sentiment

EURUSD edged lower on Tuesday after three-day recovery acceleration faced increased headwinds on approach to psychological 1.0700 barrier, reinforced by falling 55DMA.

Recently strength started to lose traction after weaker than expected EU/German PMI’s in October added to concerns about economic growth and started to deflate risk appetite.

Current pullback is supported by fading bullish momentum and overbought stochastic on daily chart, but would mark a healthy correction of two-legged recovery from 1.0448 (2023 low) if dips find ground above 1.0600 zone, where daily Tenkan-sen and Kijun-sen are forming a bull-cross.

Reversal above 1.06 handle would keep bulls in play for renewed attack at 1.07 pivot, break of which to signal bullish continuation and expose next key barriers at 1.0746/64 (Fibo 38.2% of 1.1275/1.0448 downtrend/base of falling thick daily Ichimoku cloud.

Caution on loss of 1.0600 support zone, which would risk further weakness and shift near-term focus to the downside.

Res: 1.0643; 1.0694; 1.0746; 1.0764.

Sup: 1.0616; 1.0595; 1.0565; 1.0495.

Euro Dampened by Weak PMI Data

Economic activity in Europe is cooling, raising the spectre of an emerging recession in Germany and the whole eurozone.

The PMI indices have proven to be a reliable indicator of the economic cycle for currency and equity market investors. The latest preliminary estimates for October disappointed, showing a deepening of the recession rather than the expected improvement.

The main disappointment was the German services sector, where the index fell from 50.3 to 48.0, back into contraction territory, unable to stay in growth territory and much weaker than the expected 50.1.

In France, the services index came in at 46.1, better than the expected 44.9 but still very low.

As a result, the PMI for the entire euro area fell to 47.8, the lowest level since February 2021.

The euro area manufacturing sector accelerated its contraction, falling from 43.4 to 43.0 instead of the expected rebound to 43.6.

The composite index fell from 47.2 to 46.5, the sharpest decline since October 2020. The fact that markets had braced themselves for a rise to 47.4 fuelled the sell-off in the single currency.

The EURUSD lost nearly 0.5% shortly after the data was released, turning sharply lower on a move away from 1.07. Technically, sellers piled on the pressure after the pair touched its 50-day moving average, a medium-term trend indicator.

A close below 1.07 would be a reminder that the pair’s slow recovery from 1.05 levels this month was a correction of oversold and not a trend change.

Fundamentally, Europe again shows it is struggling to grow with rising interest rates and volatile energy prices. These conditions have led the ECB to stop raising rates earlier than the Fed. Perhaps, as in the previous cycle of rate hikes following the global financial crisis, the ECB will turn to easing earlier than the Fed. This is an important factor weighing on the euro against the dollar at a time when the carry trade has re-emerged as a market driver.

RBA Bullock signals readiness to hike again if inflation outlook revised up

RBA Governor Michelle Bullock emphasized the central bank's ongoing commitment to stabilizing inflation and promoting job growth in her speech today. While the Governor acknowledged the possibility of maintaining the current cash rate level to achieve these objectives, she did not shy away from highlighting potential challenges. "There are risks that could see inflation return to target more slowly than currently forecast," she noted.

In response to the potential of inflationary pressures, Bullock assured that the Board remains vigilant: "The Board will not hesitate to raise the cash rate further if there is a material upward revision to the outlook for inflation."

As the Board gears up for its subsequent gathering, Bullock emphasized the significance of upcoming data. She mentioned, "The Board will receive several pieces of information before its next meeting that will be important for this assessment."

She elaborated on the forthcoming procedures, revealing, "This includes a full update of the staff's forecasts. We will reconsider the outlook for the economy in light of incoming information and will have opportunities to explain our assessment in the media release and Statement on Monetary Policy that will follow the November meeting."

BTCUSD Skyrockets on ETF Speculation

- Bitcoin surges to an almost 18-month high

- Broader picture appears overly positive

- But overstretched rally increases the risk of a correction

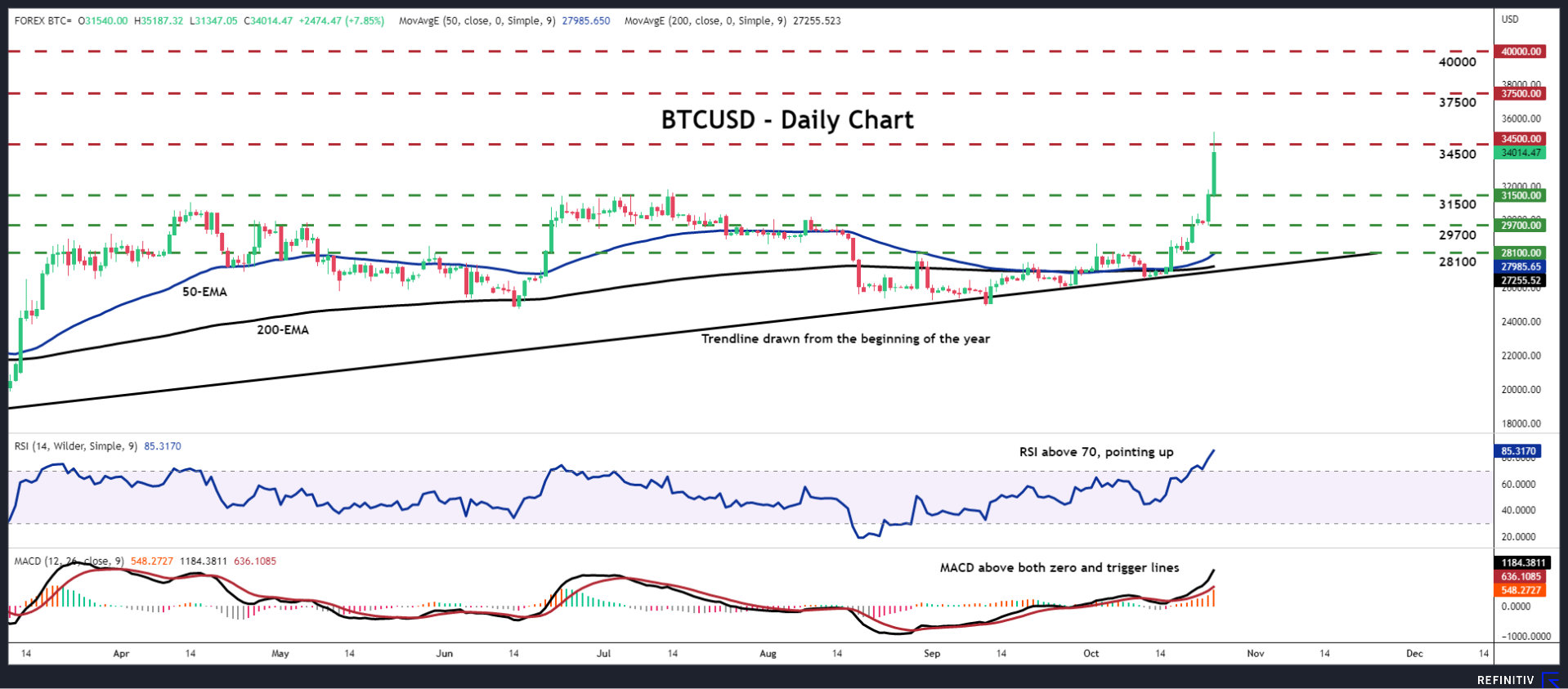

BTCUSD (Bitcoin) soared to an almost 18-month high on Tuesday, driven by speculation that an exchange-traded fund (ETF) that tracks the price of Bitcoin could soon be approved by the United States.

The crypto king rallied more than 10% to hit 35,187, before pulling back below the 34,500 zone, which is marked as resistance by the inside swing low of February 24, 2022. Overall, Bitcoin is trading well above the upward sloping trendline taken from the first day of the year, and thus, the picture appears to be overly positive.

Both the RSI and the MACD are detecting strong upside momentum, corroborating the latest surge, and suggesting that buyers are likely to stay interested in this cryptocurrency a while longer. The former is lying well above its 70 line and continues to point north, while the latter is running above both its zero and trigger lines, pointing up as well.

If another attempt to break above 34,500 proves successful, the bulls may then feel encouraged to climb towards the 37,500 zone, marked by the inside swing low of May 1, 2022. If that obstacle is not able to stop the rally either, then the next area to watch out for may be the round number of 40,000.

On the downside, if the bulls decide to lock profits due to the immediate and steep surge, they may allow a pullback towards the 31,500 barrier, which offered resistance in June and July, and if they are not willing to buy again around there, then the retreat may continue towards yesterday’s low of 29,700.

To sum up, BTCUSD has been in a rally mode since yesterday on bets of an ETF approval, with the broader uptrend looking promising. However, the steep rally increases the risk of a counter, corrective, move before the initiation of the next impulsive wave.

Crypto Market Explodes with Growth

Market picture

The crypto market cap has risen over 7.3% in the last 24 hours to $1.25 trillion. It is the highest valuation since April when fears over the safety of money in the regional banks drove the influx. The formal reason was further speculation around the launch of a spot ETF on Bitcoin. At the same time, the liquidation of short positions intensified the amplitude, as the wave of triggered orders came at a time of low market liquidity.

Bitcoin opened Tuesday with a jump to $35.2K, a level not seen since May 2022. The first cryptocurrency’s dominance index exceeded 52%, the highest since April 2021.

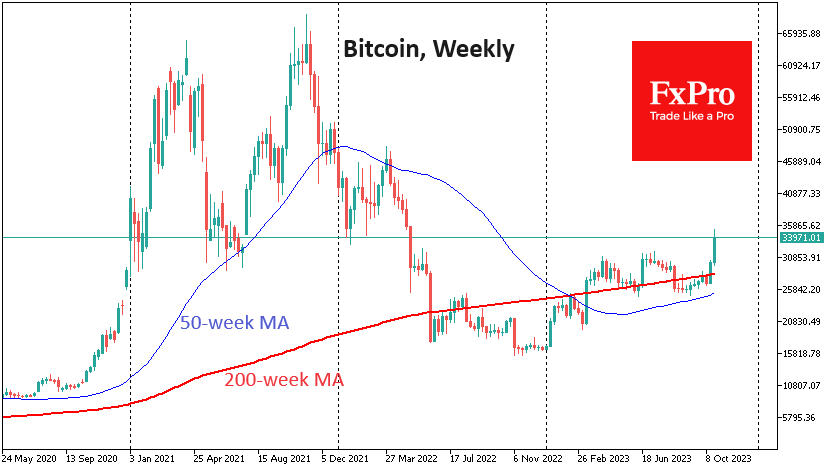

The technical picture points to a long-awaited exit from consolidation and a rapid start to growth. The first cryptocurrency found systematic support in early October at the 50-day moving average. It overcame this with a sharp move at the beginning of last week and then held above the 200-day. Now, it is gaining strength in the area above the 200-week, where long-term holders can join the buying.

The $31K to $46K range is an area of thin air, with not many obstacles. The market blew it down quickly last year, and it is worth being ready to mirror the move this time around.

News Background

According to CoinShares, investments in crypto funds rose by $66 million last week, the fourth consecutive week of inflows. Bitcoin investments increased by $55 million, while Ethereum investments decreased by $7.4 million. Investment in Solana increased by $15.5 million, significantly outperforming all altcoins.

Anticipating the approval of spot bitcoin ETFs stimulates further inflows into the first cryptocurrency. However, the investments are relatively small compared to June, when Blackrock filed its ETF application with the SEC, suggesting that investors are more cautious this time, CoinShares noted.

Bernstein said that the SEC’s approval of the Bitcoin ETF could act as a powerful catalyst for the start of a new bull cycle in the cryptocurrency market. For the first time in the history of cryptocurrencies, institutional investors have a chance to enter the market before the massive hype begins.

Accounting firm Ernst & Young points to the substantial institutional demand for Bitcoin-based financial instruments. Large organisations are ready to invest “trillions of dollars” in SEC-registered crypto products.

One of the developers of the Lightning Network discovered a vulnerability in the Bitcoin scaling solution that could have compromised the funds transfer. The vulnerability has now been fixed.

UK PMI composite ticks up to 48.6, recession cannot be ruled out

UK PMI Manufacturing saw a modest uptick, moving from 44.3 to 45.2 in October. In contrast, Services sector edged downwards, marking a 9-month low, albeit by a marginal decrement from 49.3 to 49.2. Composite PMI slightly climbed, positioning at 48.6 from a previous 48.5.

According to Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, the UK is treading dangerously close to recessionary waters. Williamson highlighted the combined impacts of the rising cost of living, soaring interest rates, and dwindling exports as the chief culprits behind a third consecutive month of diminishing output.

While the rate of economic decline is currently moderate, with predictions hinting at just a -0.1% quarterly GDP drop, the darkening cloud of economic uncertainty suggests tougher times might be ahead. "A recession, albeit only mild at present, cannot be ruled out," he added.

On a brighter note, the cost pressures evident earlier have started to soften, partly attributed to diminishing wage inflation and decline in prices set by manufacturers. Nonetheless, service sector continues to grapple with inflation, which even saw a slight bump. This indicates that headline inflation might persistently hover around the 4% range as we transition into early next year.

This poses a dilemma for policymakers, especially when factoring in potential inflationary pressures from surging oil prices. "It would be unlikely for policymakers to rule out the possibility of rates rising again later in the year," he said.

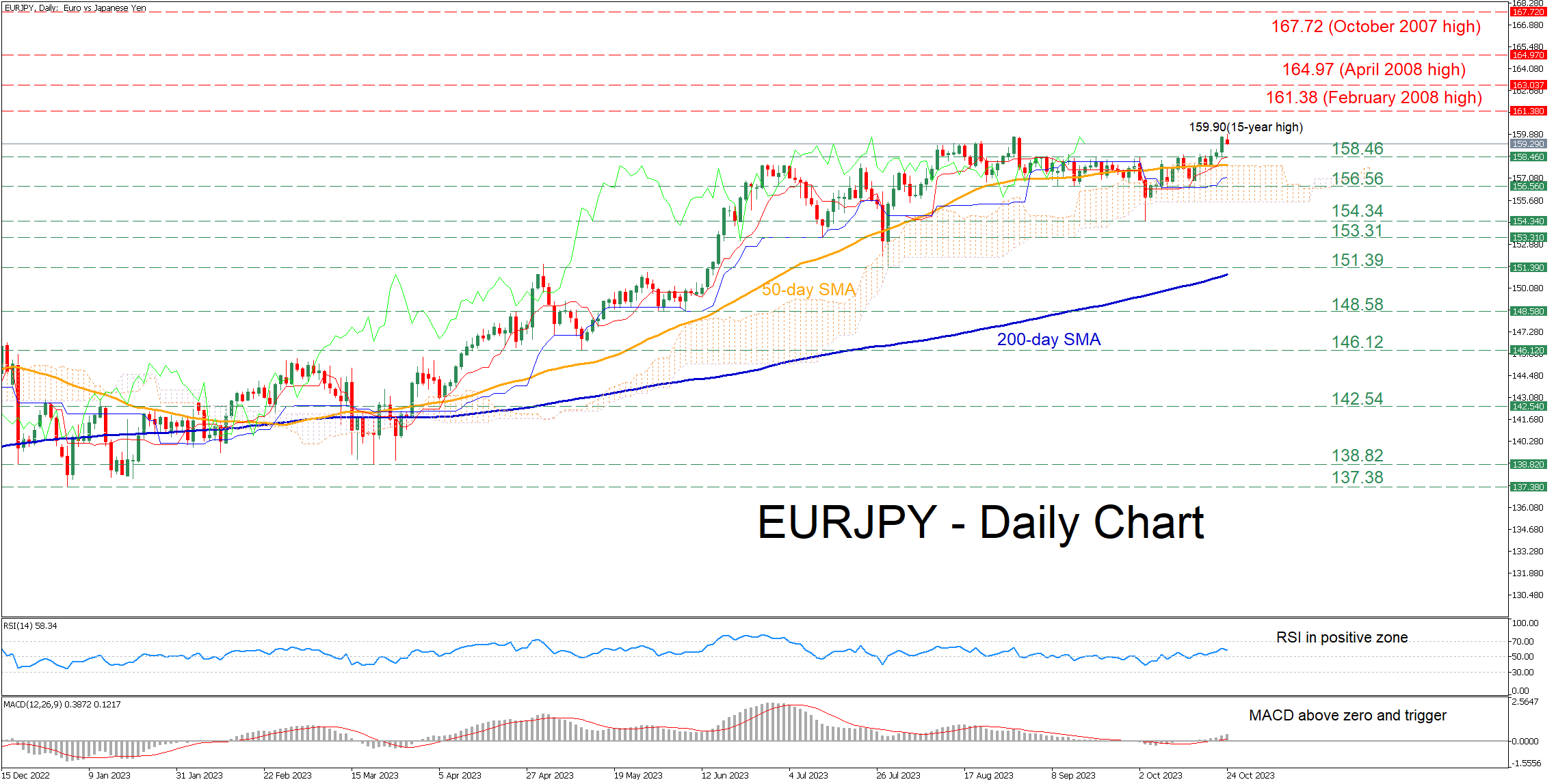

EURJPY Jumps to Fresh 15-year High

- EURJPY posts a new 2023 peak in today’s session

- Quickly erases gains, seems unable to extend its advance

- Momentum indicators suggest that bulls have lifted foot off the gas

EURJPY had been stuck in a rangebound pattern for the last couple of months, repeatedly failing to extend its bullish medium-term technical structure. Even though the price managed to record a fresh 15-year peak of 159.90 in today's session, it seems to be lacking the necessary momentum to push even higher.

Should buying pressures intensify, the price could storm towards fresh multi-year highs, where the February 2008 peak of 161.38 might curb the pair’s upside. Surpassing that zone, the price may ascend towards the April 2008 high of 164.97. Conquering this barricade, the bulls could then aim for 167.72, the highest level observed in October 2007.

If the price reverses lower, the previous resistance region of 158.46 could now serve as strong support. A break below that territory could trigger a retreat towards the September-October support of 156.56. Failing to halt there, the price could then test the October low of 154.34.

In brief, EURJPY posted a fresh 15-year high on Tuesday but still failed to stage a broader rally to the upside. Is the price heading back to its tight range?