Sample Category Title

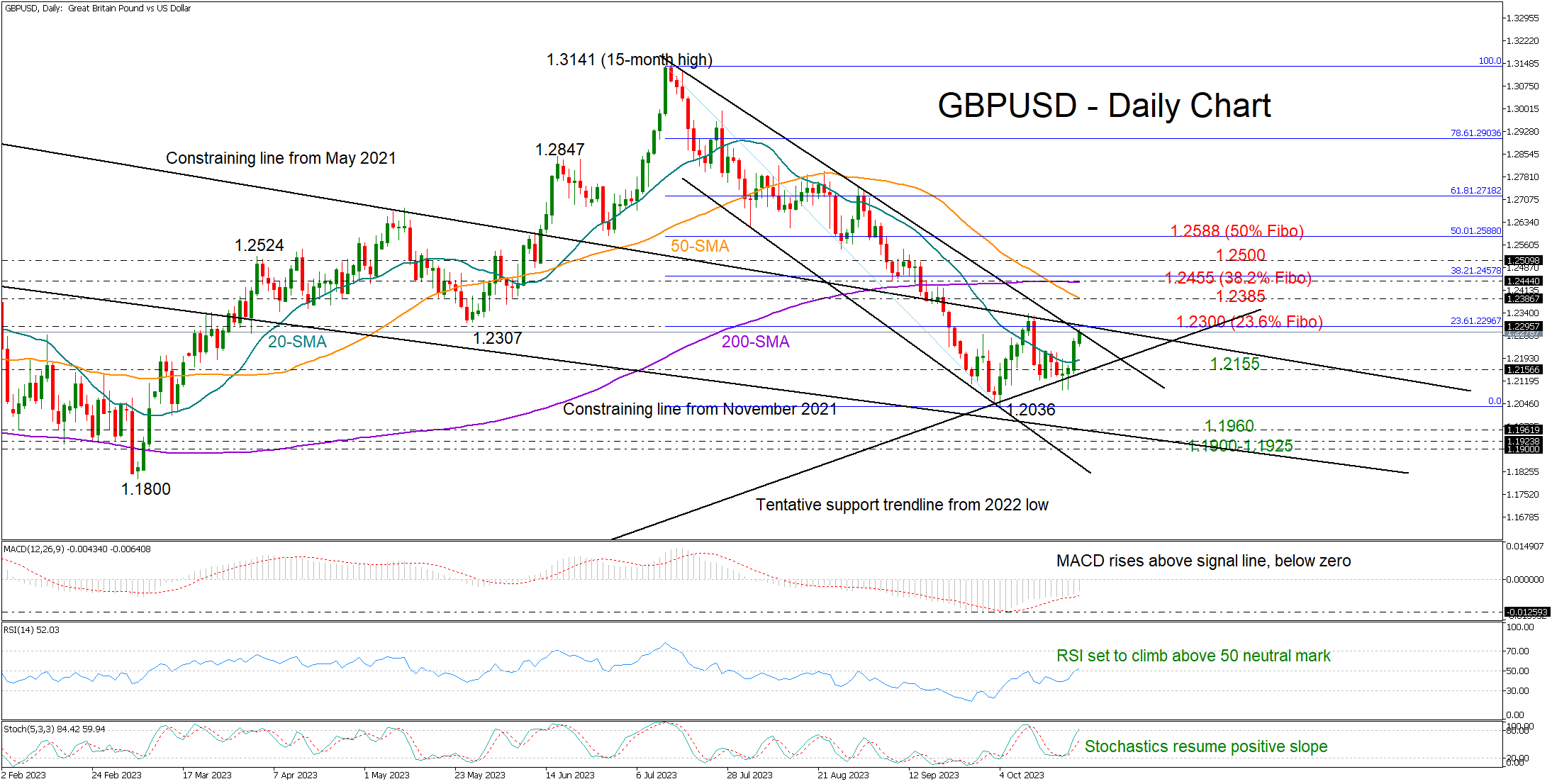

GBPUSD Receives Positive Vibes

- GBPUSD has its best day since July

- Bulls await a close above 1.2300

GBPUSD enjoyed a whopping start to the week, marking one of its strongest days since mid-July to rise as high as 1.2257 on Monday.

The technical outlook is looking promising at the moment. The pair confirmed a bullish doji candlestick pattern near last week’s low of 1.2089 and around the support trendline drawn from the 2022 low, suggesting more positive sessions ahead. The technical indicators align with this scenario too, with the RSI entering the bullish area above 50 and the MACD recovering above its red signal line. Likewise, the stochastic oscillator has resumed its positive slope.

The upper band of the bearish channel is being examined at 1.2278, while the 23.6% Fibonacci retracement is within a breathing distance at 1.2300. The long-term falling constraining line from May 2021 could also keep the bulls busy in the same neighborhood.

Another extension higher could take a halt within the 1.2385-1.2455 area, where the 50- and 200-day simple moving averages (SMAs), and the 38.2% Fibonacci level are all located. A break above that border could brighten the short-term outlook, especially if the 1.2500 round level proves easy to pierce through. Then, the spotlight would immediately turn to the 61.8% Fibonacci of 1.2588.

In the event of a bearish correction, the 2022 ascending trendline could again come to the rescue at 1.2155. If not, the bears will attempt to reach October’s low of 1.2036, a break of which could direct the pair towards the descending line from November 2021 at 1.1960. The 1.1900-1.1925 region could be the next target.

All in all, there are encouraging signals in the GBPUSD market, with the focus turning now to the 1.2278-1.2300 zone. A step above that border could add extra fuel to the bullish wave.

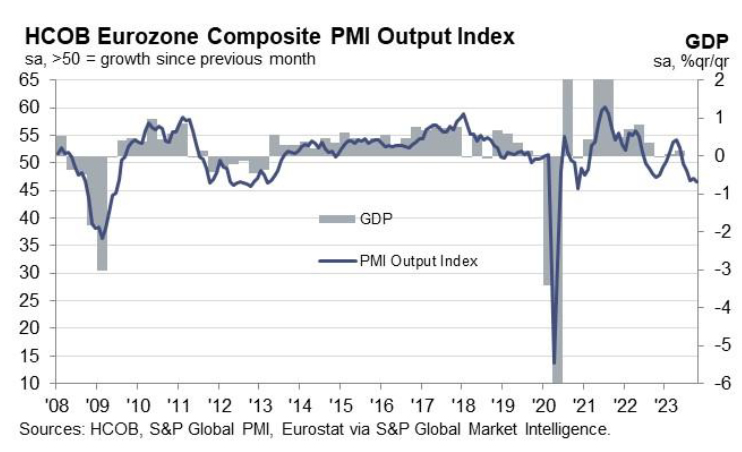

Eurozone PMI composite fell to 35-month low, moving from bad to worse

Eurozone economy appears to be on shaky ground, with the latest PMI figures showing continued deterioration. October saw Manufacturing PMI slide to 43.0 from 43.4, while Services PMI dropped to a concerning 32-month low of 47.8, down from 48.7. Composite PMI wasn't left behind, recording a 35-month low at 46.5, down from 47.2.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, stated, "In the Eurozone, things are moving from bad to worse." He highlighted that manufacturing has been grappling with a slump for over a year now. When examining the top Eurozone players, France and Germany, de la Rubia noted that their manufacturing downturns are almost on par.

However, it's not all gloom for France in the services sector. Despite a lower activity index compared to Germany, France showcases some resilience with new businesses not declining as rapidly. Moreover, companies in France are steadily adding jobs rather than eliminating them.

Another noteworthy aspect is the persistent price increases within the services sector. Comparing it to prior economic downturns, inflation for both input prices and prices charged has only marginally slowed down. This trend might be challenging for ECB. As de la Rubia points out, "these figures reinforce the case of a pause in the interest rate cycle instead of thinking aloud about loosening monetary policy."

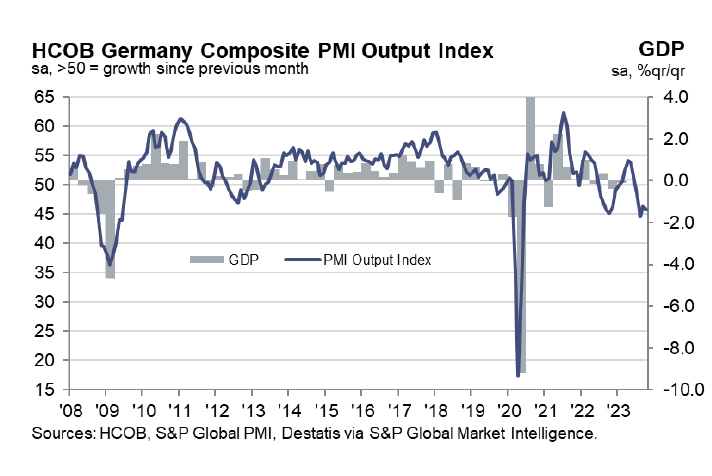

Germany’s PMI composite fell to 45.8, suggests -0.4% GDP contraction in Q4

Germany PMI Manufacturing rose from 39.6 to 40.7 in October, a 5-month high. PMI Services fell from 50.3 to 48.0. PMI Composite fell from 46.4 to 45.8.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, said:

"With the HCOB PMI indices baked into our GDP nowcast, we are calculating a -0.4 percent slip in GDP this quarter, after an estimated -0.8 percent slide the quarter before. If these nowcasts hit the mark, this would result in a -0.8 percent overall growth rate for 2023. This would make the German government's -0.4 percent shrinkage call seem pretty rosy.

"The PMI results show that the downturn is broad based. Manufacturing output continues to fall at a steep rate and activity in the services sector, which grew last month, swung into the red again.

"Input prices in the German services sector are continuing to rise at an unusual high rate. Increased energy prices and high wage pressures are most likely at the core of this development. Firms are still managing to roll some of those inflated costs onto the customer's tab, and October did not see much change in that. Thus, there is no reason to pull the plug on inflation concerns."

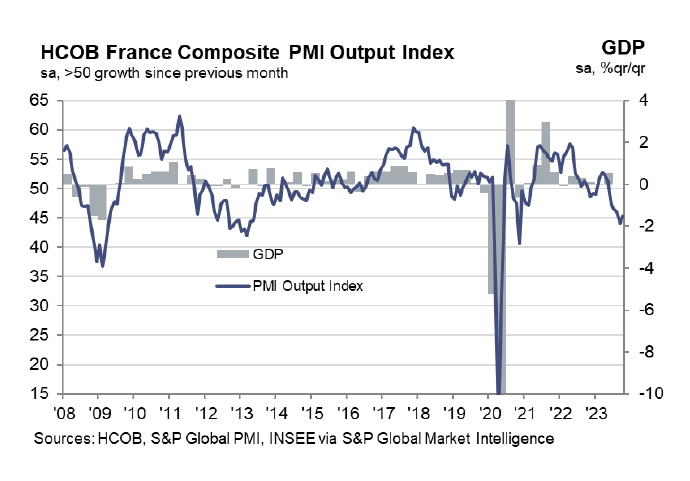

France PMI manufacturing fell to 41-mth low, services stay in contraction

France PMI Manufacturing fell from 44.2 to 42.6 in October, hitting a 41-month low. PMI Services improved from 44.4 to 46.1, a 3-month high. PMI Composite rose from 44.1 to 45.3, a 2-month high.

Norman Liebke, Economist at Hamburg Commercial Bank, said: "The French economy is still feeling the heat at the start of the fourth quarter... Our GDP nowcast model, with PMI figures in the mix along with a bunch of other indicators, is pointing to fractional growth in the fourth quarter.

"The services sector is hitting roadblocks... Things are going south in the manufacturing sector, and there is no relief in sight... Price indices are in perilous territory.... Higher inflation rates would put the European Central Bank into a difficult position as it more or less signalled at its last meeting that no further rate hikes will be carried out."

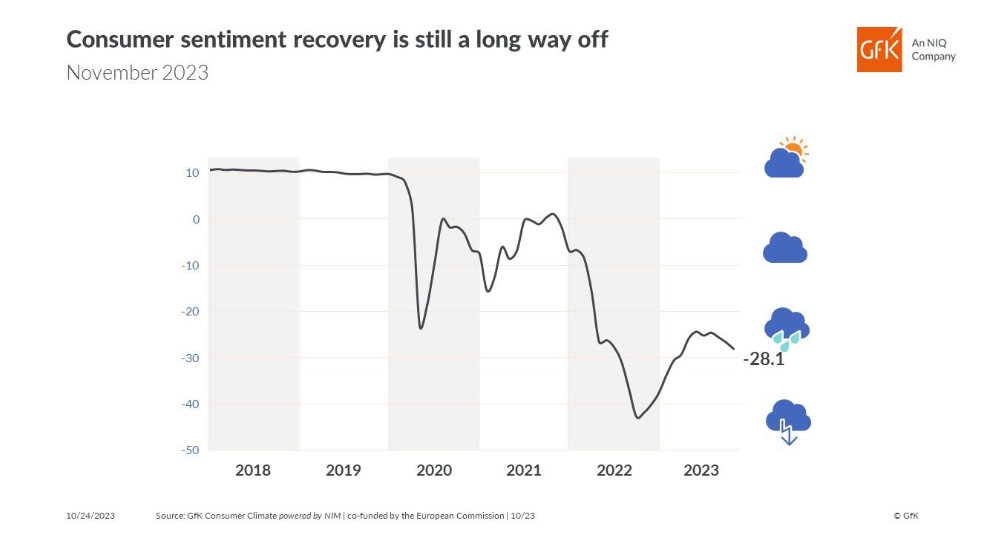

Germany’s Gfk consumer sentiment fell to -28.1, hope of recovery this year laid to rest

Germany's Gfk consumer sentiment for November fell from -26.7 to -28.1. In October, economic expectations improved slightly from -3.4 to -2.4. Income expectations fell form -11.3 to -15.3. Propensity to buy ticked up from -16.4 to -16.3. Propensity to save rose from 8.0 to 8.5.

"With the third decline in a row, hopes of a recovery in consumer sentiment this year must finally be laid to rest," explains Rolf Bürkl, consumer expert at NIM.

"Above all, high prices for food are weakening the purchasing power of private households in Germany, so private consumption will not be able to support the economy this year."

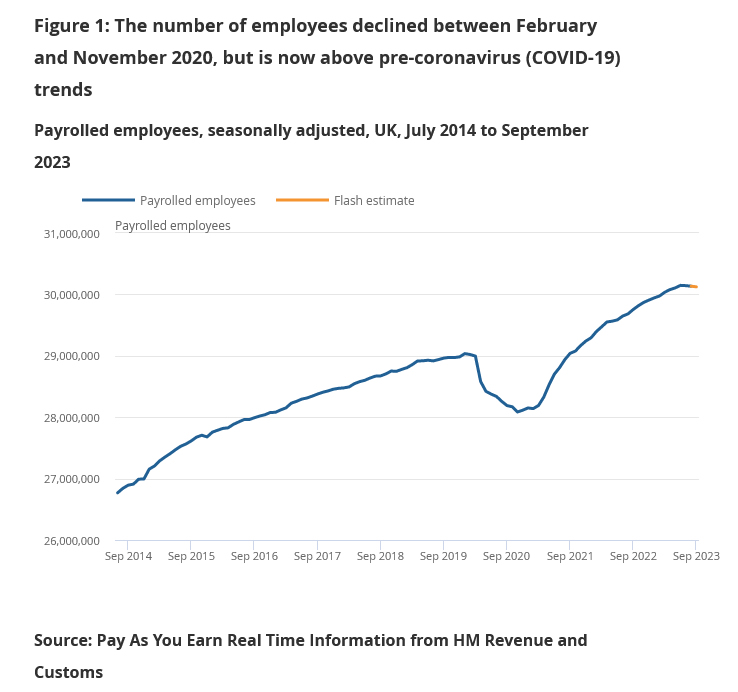

UK payrolled employment fell -11k in Sep, pay growth slowed to 5.7% yoy

In September, UK payrolled employment fell -11k. Median monthly pay rose 5.7% yoy, slowed notably from August's 7.7% yoy. Annual growth in median pay was highest in the transportation and storage sector, with an increase of 13.5%, and lowest in the health and social work sector, with a decrease of -0.3%.

In the three months to August, unemployment rate fell from 4.3% to 4.2%, below expectation of 4.3%.

Cryptocurrency Market Capitalization Sets Year’s High

Amid the frenzy over expectations that the SEC will approve applications for spot bitcoin ETFs, the cryptocurrency market capitalization reached USD 1.25 trillion this morning, for the first time in 2023. Expectations have increased following reports that the US Securities and Exchange Commission will not appeal a court ruling that the rejection of Grayscale Investments' ETF application was improper.

It is important to understand that an ETF is a financial instrument that will allow a wide range of people to easily officially invest in bitcoin without opening an account on a crypto exchange, which can be associated with difficulties and dangers.

Although there has been no official announcement yet, the news background is extremely positive:

→ Blackrock is rumoured to have informed the SEC that it will begin buying BTC for its BTC ETF;

→ Blackrock spot BTC ETF has appeared on the lists of clearing house DTCC with the ticker IBTC.

The growth leader, of course, is bitcoin. Its price reached USD 35k this morning — for the first time since May 2022. Following this, other assets also perked up – in particular, Ethereum, the second most important cryptocurrency, rose above USD 1,800.

The chart shows that ETH/USD:

→ the ETH price is near the upper limit of the downward channel that has been in effect since May of this year;

→ level 1,820 may provide resistance;

→ the price of ETH has exceeded the level of 1,740, which can now provide support.

It is worth noting that when (and if) the application for a bitcoin ETF is officially approved, the price of the coin may even weaken, since the market looks overbought and is already taking into account the effect of what will happen. However, BTC could be followed by a rush for Ethereum ETFs.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

USD/JPY Bullish Momentum Seems to be Fading

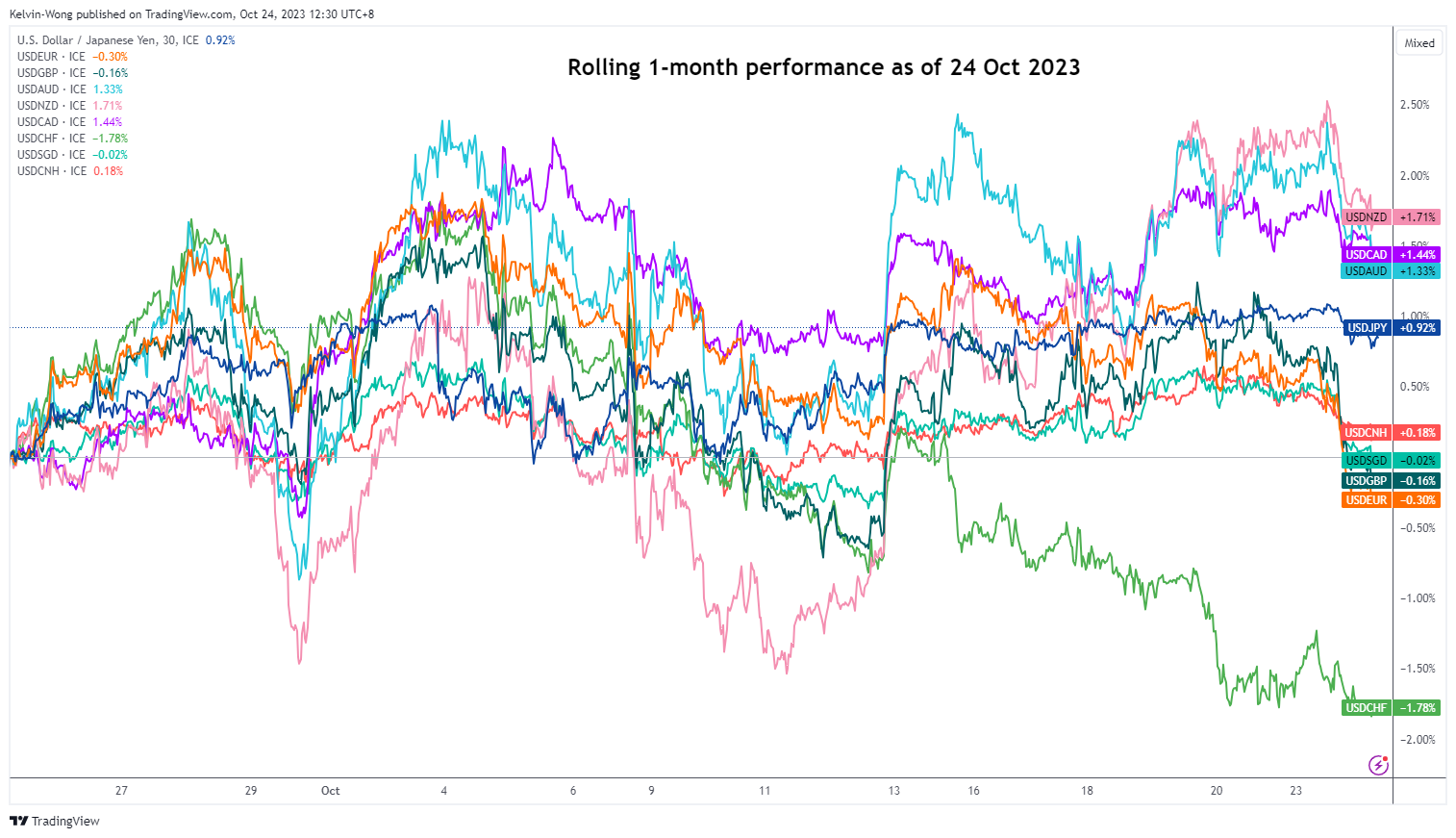

- USD/JPY’s current year-to-date outperformance has started to dissipate based on a shorter-term one-month rolling basis.

- A disappointing Japan Services PMI (flash) for October has failed to ignite an intraday bullish movement in USD/JPY.

- Three main factors that are likely to be the cause; intervention risk, inter-market expectations, and momentum.

- Watch the key 20-day moving average on the USD/JPY, now acting as support at 149.30.

The major uptrend phase of the USD/JPY in place since mid-January 2023 seems to be losing its bullish inertia even though it has recorded a year-to-date gain of +14.16% as of 24 October at this time of the writing, the best US dollar major pair ahead of the USD/CAD (+0.72%), USD/EUR (-0.15%), USDGBP (-1.78%), and USD/CHF (-3.78%).

On a shorter horizon based on the one-month rolling performances of the major US dollar pairs as of 24 October 2023, the bullish momentum of the USD/JPY has started to dissipate from a peak of +1.16% to a current gain of +0.90% (see figure 1).

Fig 1: US dollar major pairs rolling 1-month performances as of 24 Oct 2023 (Source: TradingView, click to enlarge chart)

A disappointing Services PMI has failed to ignite a rally in USD/JPY

Also, today’s weak Japan’s flash Services PMI print for October came in below expectations (51.1 versus 52.9 forecasted & 53.8 in September) where the growth in the services sector slowed to a ten-month low has failed to ignite a short-term intraday bullish movement in the USD/JPY.

In the past, disappointing key economic data in Japan tended to lead to a bid in USD/JPY as market participants upped the expectations of the Bank of Japan (BoJ) to delay monetary policy normalization away from short-term negative interest rates which in turn maintained the policy divergence status quo between the BoJ and US Federal Reserve as well as the rest of the world’s central banks that have pivoted away from either zero or negative interest rates since 2022.

What is causing the lack of bullish enthusiasm in USD/JPY?

There are three possible factors; intervention risk from policymakers, inter-market expectations, and momentum.

Firstly, verbal interventions in the past two months by Japan’s Ministry of Finance (MoF) officials have been drummed up as the JPY weakened considerably against the US dollar due to robust key US economic data that increased the odds of the Fed’s current stance of keeping US interest rates at a higher level for a longer period.

Also, MoF’s verbal intervention is likely to have morphed into a recent real intervention in the foreign exchange market to halt the pace of JPY weakness on 3 October where the USD/JPY printed an intraday high of 150.16 during the start of the US session before it tumbled significantly by -282 pips to hit an intraday low of 147.34 within a short span of just five minutes even though there was no official intervention confirmation by MoF officials.

Therefore, in the minds of market participants, the USD/JPY’s psychological level of 150 has subconsciously become the “line in the sand” that increases the risk of FX intervention when the movement of the USD/JPY probed close to around 150.

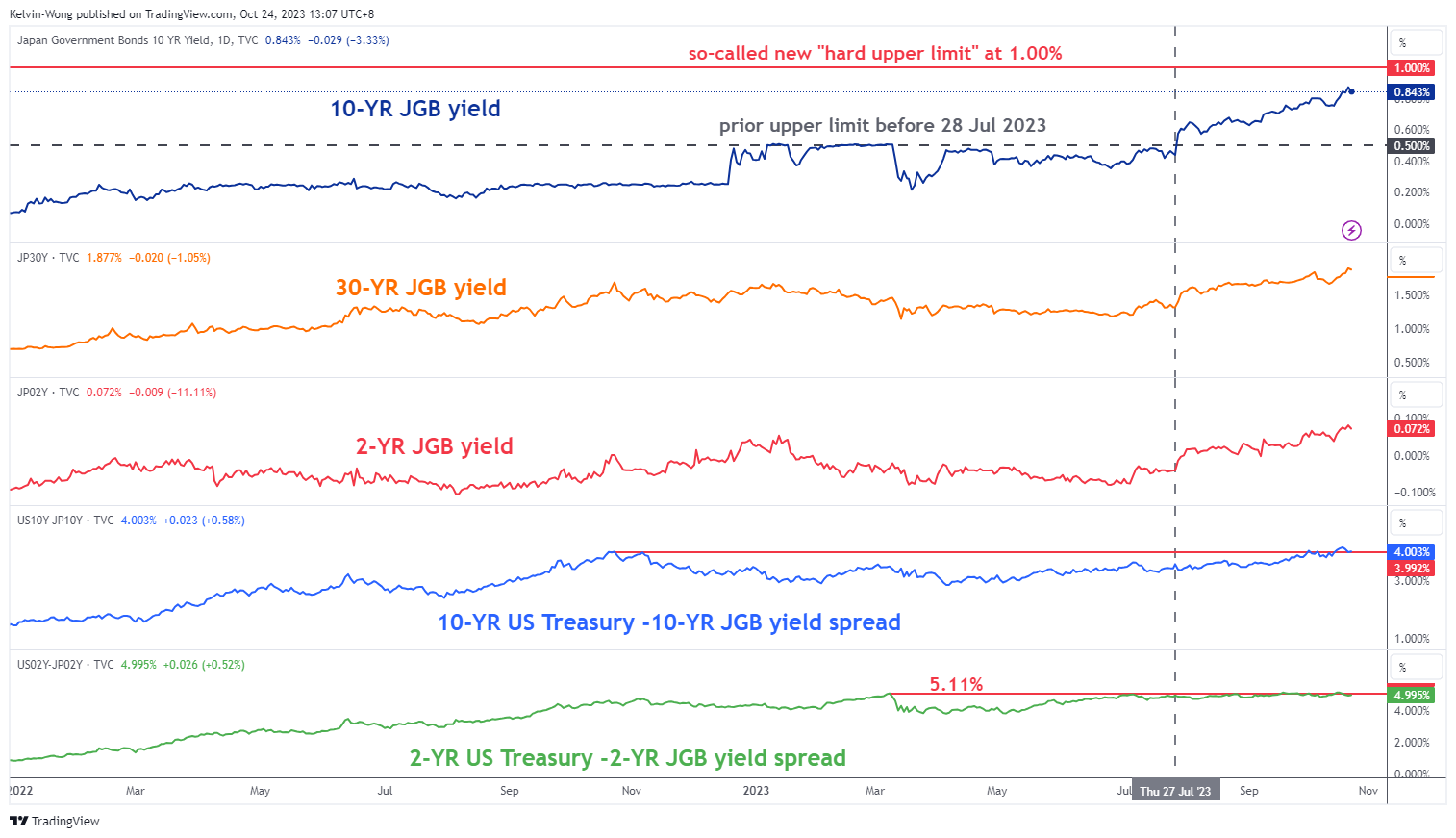

Fig 2: JGB yields & yield spread with US Treasuries as of 24 Oct 2023 (Source: TradingView, click to enlarge chart)

Secondly, the shorter-term 2-year yield spread premium of the US Treasury not over the Japanese government bonds (JGB) has started to narrow since 28 July after the implementation of “flexible yield curve control” on the 10-year JGB yield by BoJ. Also, it has failed to break above its current year-to-date peak of 5.11% printed in March 2023 (see figure 2).

The 2-year sovereign yield tends to be more sensitive to a central bank’s monetary policy and the 2-year JGB yield has jumped significantly from -0.04% to 0.07% at this time of the writing due to increasing expectations that BoJ is likely to scrap its short-term negative interest rates policy by the first half of 2024.

In addition, recent data from Japan’s overnight index swap curve has indicated a 20% chance that BoJ will end negative interest rates in December 2023, and the probability rises to 100% by April 2024.

Thirdly, the medium-term bullish momentum of the USD/JPY as indicated by the daily RSI indicator has flashed a bearish divergence condition just below a medium-term resistance of 150.30 (see figure 3).

Fig 3: US/JPY medium-term & major trends as of 24 Oct 2023 (Source: TradingView, click to enlarge chart)

This technical observation suggests an easing of bullish momentum. A clear break with a daily close below the key 20-day moving average (price actions have traded above it since 31 July 2023) now acting as support at 149.30 increases the odds of a potential multi-week bearish reversal towards the medium-term support at 144.80.

Short Term Consolidation Might be in the Cards

Markets

“We covered our bond short”. A tweet by the founder of Pershing Square Capital Management on X succeeded in doing what geopolitics, economic data, Fed speak and technical factors recently failed to do: trigger a correction higher in US Treasuries/core bond markets. It’s telling about markets in general that Bill Ackman squaring his position in 30-yr Bonds can trigger such an (algo-driven?) response. An empty eco calendar and thin trading made way for the (outsized) reaction. A late swoon in oil prices (Brent crude from $92/b to $89.5/b) added to the momentum. Still, it remains to be seen how lasting such market reactions are though. Daily yield changes on the US yield curve ranged between 2.5 bps (2-yr) and 8.5 bps (20-yr). German Bunds followed the move to a lesser extent with intraday differences between +1 bp and -2.6 bps (30-yr). Greek GGB’s and Italian BTP’s outperformed following weekend decisions by rating agency S&P. Greek bonds were granted back their first investment grade rating amongst big three rating agencies while Italy avoided a rating and even an outlook downgrade (BBB; stable outlook). 10-yr yield spreads vs Germany narrowed by 7 bps for the both of them.

US stock markets opened around 1% lower, erasing these losses within the first half hour as long term bond yields plunged. Weakness into the close suggest little potential in the equity rebound with only Nasdaq ending with small gains. From a technical point of view, the S&P 500 set a new sell-off low and closed below the 200d mavg. In FX space, the dollar fainted. EUR/USD had already regained the 1.06 big figure with the upleg accelerating after taking out first minor resistance (October high at 1.0640). The pair eventually closed at 1.0670, leaving the downward trend channel in place since mid-July and turning the technical picture more neutral short term. 38% retracement on the downmove since mid-July stands at 1.0766.

Today’s eco calendar contains global PMI’s. After yesterday’s correction, it will be interesting to see whether markets take weaker or close to consensus data as a reason to do some more short covering ahead of ECB (Thursday) and Fed (next week) policy meetings. We hold our view that short term consolidation might be in the cards, but that medium-to-long term underlying market sentiment remains bearish for bonds. For the US 10-yr yield, the October correction low around 4.5% in the reference.

News and views

Czech National Bank board member Prochazka said investors are overestimating the pace and amount of potential monetary easing to come. In the interview published yesterday, he added that the central bank would proceed cautiously when lowering rates because underlying price pressures are still strong. At the time of his comments Prochazka said markets were anticipating the CNB to cut twice this year and a policy rate of 3.5% by end next year compared to the 7% today. CNB governor Michl did say several times they have a strategy for monetary easing in place. KBC Economics expects the policy rate to be cut by 50 bps in total by end this year with a bias towards going in two 25 bps steps (November & December).

Japanese PMIs declined further in October. The composite reading fell from 52.1 to 49.9, the first sub 50 reading since December last year. Manufacturing stabilized at 48.5 where a smaller decline in new orders compensated for a stronger drop in actual output while lower capacity pressures led to employment falling for the first time since February 2021. The drag on the composite figure thus came exclusively on the account of the services sector. Activity there is still growing but at the slowest pace YtD (51.1 from 53.8). New business rose at a weaker rate while foreign demand declined for the first time in 14 months. But optimism about the future as well as indications of staff shortages led to a solid increase in employment. The latter should be welcomed by the Bank of Japan, who is looking for sustained wage increases to support inflation durably. Price pressures in the sector remain elevated, the survey noted, but both input costs and charges rose at slower rates in October. The Japanese yen reacted stoic to the release. USD/JPY trades slightly lower at 149.69 though this follows general dollar weakness.

US Treasuries Rebound and Oil Retreats, But Underlying Risks Remain the Same

We continue to see high volatility in the US sovereign papers near important psychological levels where investors are invited to decide what to do next. In this respect, the US 10-year yield shortly crossed above the 5% psychological mark yesterday, then retreated sharply in a move that was qualified by a large short covering after two popular bond bears Bill Ackman and Bill Gross said that they covered their short bets on US Treasuries. Ackman said that ‘there is too much risk in the world to remain short bonds at current long-term rates’.

And boom. The US 10-year yield fell below the 4.85% level. Of course, the rising US debt, and the rising US interest rates which make the debt more expensive to finance, remain a big issue. The US debt rose more than $600 bn since it crossed the $33 trillion mark and the total US debt is up by more than $2 trillion since the end of the debt ceiling crisis, back in summer. The US has been adding around $22 billion debt each day since a month; that equals to almost a billion dollar per hour. And the most important thing is, the Fed is no longer a big buyer. Therefore, the upside pressure in the US long-term yields could ease near and above the 5% level. But the yield curve will likely stay high for long, and a further upside move in the US 10-year yield couldn’t be ruled out to end the inversion of the 2-10-year portion of the yield curve.

A higher yield curve is not necessarily good news for the broader economy and stock valuations– unless the economy resists to higher rates.

The S&P500 extended losses below the 200-DMA yesterday and the index now approaches an important technical support, the 4180 level, the major 38.2% Fibonacci retracement on last year’s rally, and which should distinguish between the actual positive trend and a medium-term bearish reversal. Nasdaq 100, on the other hand, eked out a 0.30% gain yesterday in the run up to Microsoft and Alphabet earnings due after the bell today. Amazon is due to report on Thursday.

Together, 5 big tech names in the S&P500 – Amazon, Alphabet, Apple, Microsoft and Nvidia - are expected to post a combined 34% rise in their earnings in the Q3 compared to the same time last year. Because they have a heavy weight in the major US indices, the Big Tech could offer investors yet another reason not to give up on the US stocks. But keep in mind that without the Big 5, earnings for the S&P500 companies would be down by around 5%.

Big Oil, big purchases

Chevron announced yesterday that it will buy Hess for $53 billion, or for $60bn including debt. Earlier this month, Exxon Mobil had announced to buy Pioneer Natural Resources for around $60bn to extend its Permian footprint. The Big Oil companies have such a big amount of cash in their hands that either they announce huge share buybacks and nice dividend payouts, or big mergers. Both are good for investors. Climate change doesn’t impact the good fortune of these companies, for now. On the contrary, the deals are proof that traditional energy companies are confident in the industry, and they find it useful to grow their core fossil business lines, rather than going into alternative energy sources. In this respect, Occidental Petroleum reportedly ditched the world’s biggest carbon capture plant – after spending more than a billion USD to buy a startup called Stratos.

In summary, the big oil companies are taking a big step back from their climate goals, they keep investing in what makes money: fossil fuel. And the recent rise in oil prices plays in their favour as well. The barrel of US crude retreat to $86pb this week, as tensions in Gaza didn’t escalate as much as feared, and as Hamas released two more hostages. But the risk of a sudden jump in oil prices prevails. If not, Saudi Arabia will likely come to the rescue of oil bulls near the $80pb.

On a side note, according to the US Department of Energy, there are about 17 days left in the US strategic petroleum reserves. The US produces enough oil to continue feeding America with enough energy, but the meagre 17 days of stockpile limits Joe Biden’s ability to contain any important price pressure in the future, which could be triggered by an escalation of tensions in the Middle East for example. Therefore, any selloff in oil could be an interesting entry opportunity for those betting for higher for longer oil prices, due to supply restrictions and geopolitical tensions. I expect the barrel of US crude to swing within the $80-100pb range.