Sample Category Title

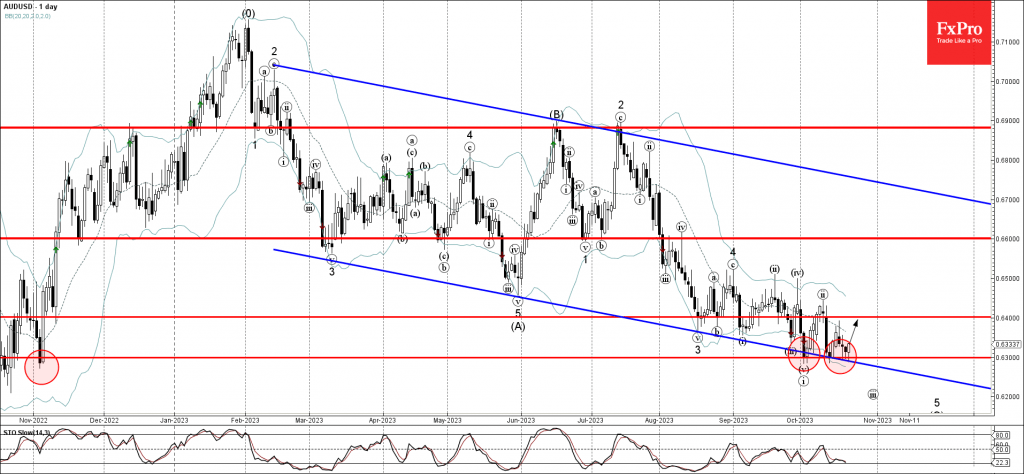

AUDUSD Wave Analysis

- AUDUSD reversed from key support level 0.6300

- Likely to rise to resistance level 0.6400

AUDUSD currency pair recently reversed up from the key support level 0.6300 (which has been reversing the pair from November).

The support level 0.6300 was strengthened by the lower daily Bollinger Band and by the support trendline of the weekly down channel from February.

Given the strength of the support level 0.6300, AUDUSD can be expected to rise further toward the next resistance level 0.6400.

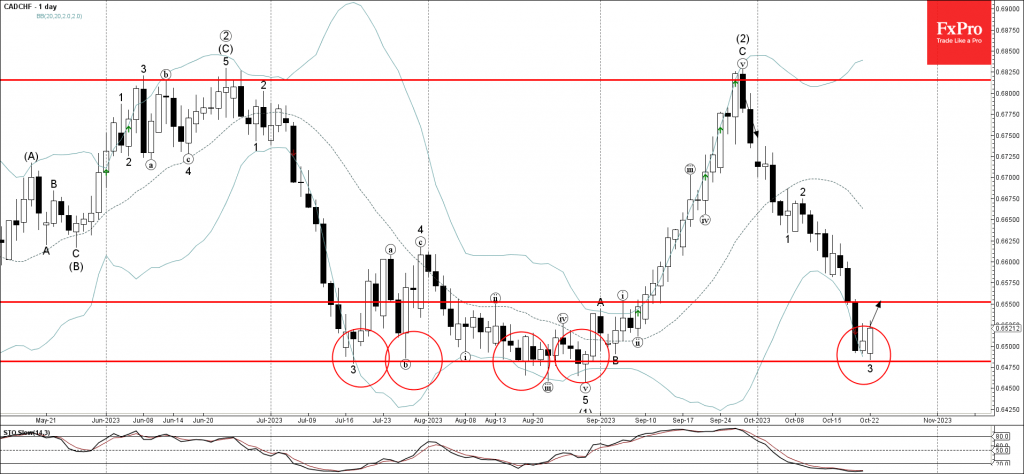

CADCHF Wave Analysis

- CADCHF reversed from support level 0.6480

- Likely to rise to resistance level 0.6550

CADCHF currency pair recently reversed up from the powerful support level 0.6480 (which has been reversing the pair from July) coinciding with the lower daily Bollinger Band.

The upward reversal from the support level 0.6480 stopped the previous sharp downward impulse wave 3.

Given the strength of the support level 0.6480 and the oversold daily Stochastic, CADCHF can be expected to rise further toward the next resistance level 0.6550.

NAS100 – Nerves Remain Ahead of PMIs on Tuesday as Stocks Start the Week Choppy

- US 10-year yield above 5% for first time since 2007

- Economic fears mounting

- NAS100 survives test of key support

It’s been a jittery start to the week, with the continued rise in US yields making investors very nervous about what challenges lie ahead for the economy.

We’ve heard a lot about the resilience of the US economy and the evidence has been there for all to see. But that resilience has for a long time been paired with a belief that rates won’t stay at the peak for long, a view that has been gradually fading as rate cuts have been pushed back further and further into the future.

Ultimately, there’s only so much the economy can withstand and recent moves in yields suggest bond investors are coming around to the Fed’s way of thinking.

Whether that will remain the case, I’m less convinced, but as things stand there’s clearly a growing view that the economy will be pushed over the edge sooner or later, at which point the discussion around rate cuts can take hold.

Major support holds firm again

From a technical perspective, the NAS100 is looking vulnerable although once more it has survived the earlier scare.

Source – OANDA on Trading View

A descending triangle has formed over the last few months with the base falling around 14,500 where the index briefly dipped below earlier today.

A break below this level could be viewed as a very bearish move and a sign of further potential pain to come. While there are other past support levels that may stand out below, such as 14,250 as we saw back in June, the next major area may arguably be around 13,500-14,000.

This is where the 200/233-day simple moving average band falls which the index hasn’t traded significantly below since the start of the year.

BTC/USD: Is Bitcoin Back?

- Bitcoin hits $31,000, highest levels since July

- Michael Saylor’s MicroStrategy Bitcoin position turns positive (average $29,582 purchase price)

- Major bond market yield reversal keeps cryptos broadly supported (Eth up 3.4%, Solana up 2.4%, and Dogecoin up 4.9%)

Bitcoin is rallying alongside tech stocks as the bond market has a major reversal. Today’s rally that took prices to a three-month high is not about spot Bitcoin ETF optimism but about a significant reversal in the dollar and 10-year Treasury yield. Bitcoin could continue to rally if investors continue expect risk appetite prefers risky assets over Treasuries. The key for Bitcoin won’t just be positive ETF news but will require a peak in rates to be confidently priced in. There is still a risk that investors might prefer stocks versus cryptos. As long as the Fed is done with this hiking cycle and soft landing hopes remain, that should be a positive backdrop for Bitcoin.

If Bitcoin is able to rally above the $31,500 level, bullish momentum could support a rally towards the $35,700 region, which is the 38.2% Fibonacci retracement level of the collapse record highs ($68,772) to this cycle’s low ($15,278).

What would really get the crypto world going again is we start to new money become highly committed. Endorsements from Michael Saylor, Elon Musk, or even Cathy Wood will do little to attract new investors. It is unlikely that Bitcoin skeptics will be changing their tune anytime soon.

Some bitcoin supporters believe that the next halving in 162 days could potentially be the key catalysts to send Bitcoin back above the $40,000 level. A lot needs to go well for crypto, but at the very least it seems regulation won’t kill the space.

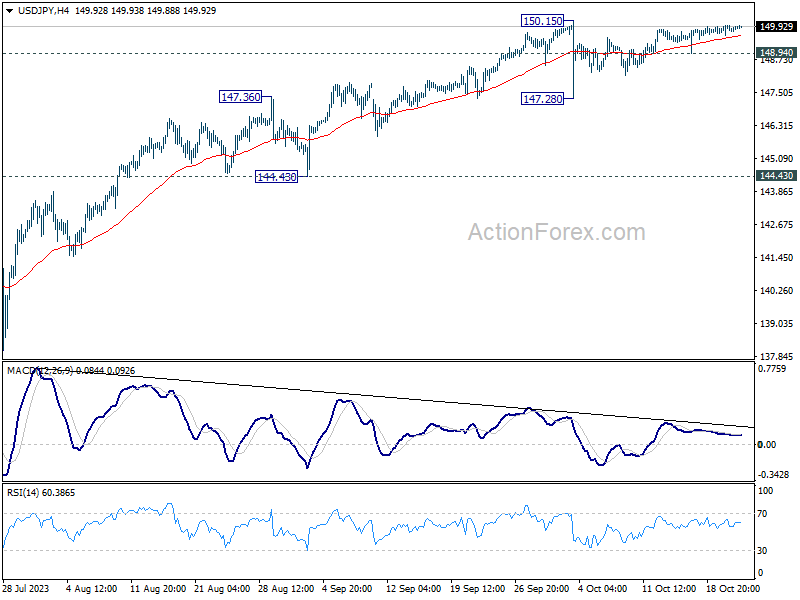

Japanese Yen Eyes Potential Intervention Amid Rising USD/JPY

The USD/JPY currency pair, after almost breaching the significant 150.00 threshold, retreated slightly. As of Monday morning, the pair stands close to this pivotal mark at 149.93.

This temporary pullback is hinged on the anticipation that the US Federal Reserve might uphold the prevailing interest rates for an extended duration at its upcoming meeting.

However, the immediate circumstances are what truly grip the market's attention. A leap beyond the 150.00 mark in the USD/JPY might be interpreted as a cue for Japanese monetary authorities to step in with an intervention. Notably, on 3 October, the greenback soared to 150.16 but experienced a swift descent. The financial fraternity remains in the dark about whether this drop was an outcome of market jitters or a sequence of automated trading orders being triggered.

The decision to implement currency interventions rests upon the perspectives of the Central Bank and the Ministry of Finance.

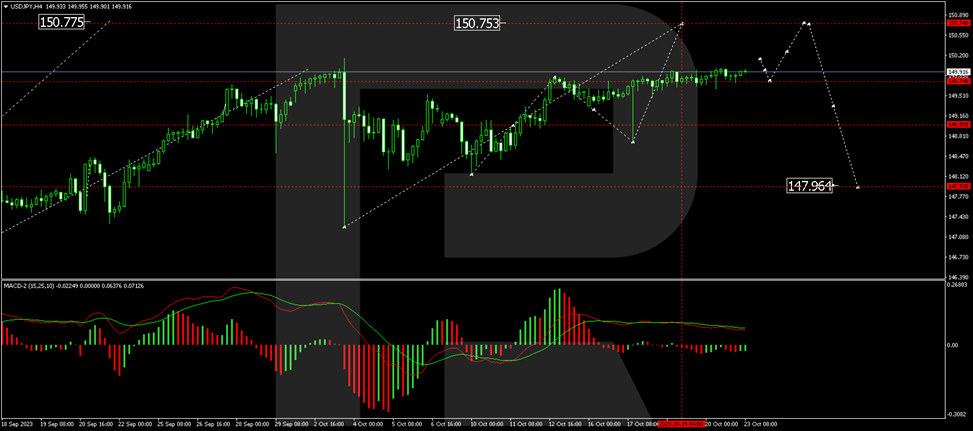

Technical Analysis: USD/JPY

On this timeframe, USD/JPY managed to hit the predicted peak of its bullish wave at 149.81 before initiating a mild correction to 148.72. Presently, the bullish structure is expanding, targeting 150.77. A recent bullish leg concluded at 149.92, with a consolidation pattern emerging underneath. A bearish adjustment to 149.33 seems plausible before a surge towards 150.15. From this juncture, the upward trajectory might continue to 150.77. The MACD lends technical validation to this forecast. Its signal line, positioned comfortably above the zero benchmark, points definitively northwards, suggesting further elevation.

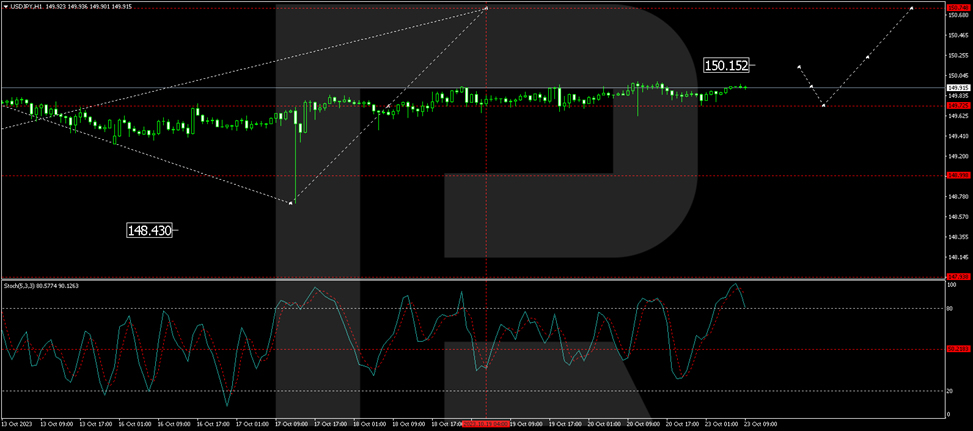

In the H1 outlook, a consolidation pattern is noticeable around the 149.73 region. The market currently depicts an upward movement towards 149.90. Subsequent movements might see a dip to 149.72 and then a rally to 150.15, potentially leading to 150.77. The Stochastic oscillator backs this analysis. Its signal line, presently above the 80 level, is oriented southwards, targeting the 50 benchmark. An anticipated rebound from this point, followed by an ascent to 80, seems likely.

Conclusion

The USD/JPY continues to flirt with the crucial 150.00 level, inciting speculation about potential intervention by Japanese financial authorities. While recent price movements suggest bullish momentum, traders should remain vigilant and consider both fundamental catalysts and technical signals before making trading decisions.

GBP/USD Drifting, UK Employment Report Next

- UK retail sales slide in September

- UK releases employment data on Tuesday

The British pound is showing very limited movement on Monday. In the North American session, GBP/USD is trading at 1.2154, down 0.07%

UK employment expected to slide

The UK delayed has delayed the release of employment and unemployment data until Tuesday, after releasing wage growth last week. Wages including bonuses dropped from 8.5% to 8.1%, which is still very high and is driving inflation. Job growth is expected to drop by 198,000 in the three months to September, after a massive decline of 207,000 previously. The unemployment level is expected to remain at 4.3%.

UK retail sales cool

UK retail sales disappointed in September, as warm weather and the cost-of-living crisis dampened purchases of autumn clothing. Retail sales slipped 0.9% m/m in September, versus a 0.4% gain in August and below the consensus estimate of -0.2%. On an annualized basis, retail sales declined by 1.0% in September, following a revised -1.3% in August and shy of the consensus estimate of -0.1%.

The soft retail sales report will likely reduce growth in the third quarter and that could mean a contraction in GDP in Q3. Consumers have been squeezed by cost of living pressures and are spending more and getting less in return. Inflation is galloping at 6.7%, the highest in the G-7. Against this grim backdrop, GfK consumer confidence fell to -30 in September, down from -21 a month earlier and well below the consensus estimate of -20. The GfK report noted that high fuel costs, elevated borrowing costs and the Middle East conflict were driving growing unease among consumers.

Federal Reserve Chair Powell spoke on Thursday, warning that inflation remained too high and bringing it down to the 2% target would require the economy and the labour market to cool. Powell was non-committal about further rate hikes, noting that the spike in long-term Treasuries could dampen inflation without the Fed having to act. Powell’s remarks were perceived as somewhat dovish by the markets, as the Fed rate odds of a hike in December, which were as high as 45% last week, fell to 20% on Friday, according to the CME FedWatch.

GBP/USD Technical

- GBP/USD tested support at 1.2158 earlier. Below, there is support at 1.2097

- There is resistance at 1.2227 and 1.2288

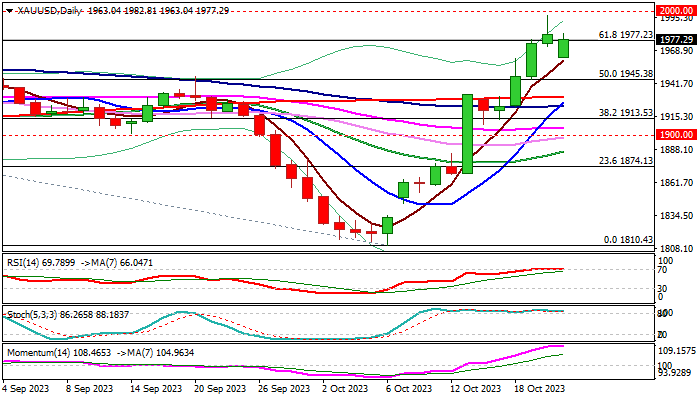

Gold Consolidating Under $2000, Bulls Hold Grip for Now

Gold is consolidating under new five-month high on Monday after larger steep uptrend stalled on approach to psychological $2000 barrier.

Strong upside rejection on Friday points to increased headwinds from $2000 zone which marks significant obstacle, prompting traders to collect some profits from over 7% rally in past two weeks.

Overstretched daily indicators also contribute to current pause, though the pullback was so far shallow and signaling that bulls hold grip for renewed probe above $2000.

Unrest in the Middle East prompted traders into safety, with threats that conflict may escalate, boosting demand for safe-haven bullion and continuing to inflate the price.

Pullback so far found a footstep above rising 5DMA ($1960), with extended dips expected to stay above $1945 (broken 50% retracement of $2080/$1810), to mark a healthy correction and keep larger bulls intact.

Res: 1982; 1997; 2000; 2016

Sup: 1960; 1945; 1931; 1926

Sunset Market Commentary

Markets

The US 10-yr yield temporarily breached 5% for the first time since July 2007. The US 5-yr yield is now the only point on the curve not to have traded above that psychological number this month. Daily changes currently vary between +4.0 bps (2-yr) and +6.2 bps (10-yr). Friday’s US budget data put the onus on deteriorating public finances, reminding the investor community that the US government will run a 7%-plus deficit at a time when the US central bank is running down its balance sheet. Fears that the Israeli-Hamas tensions would escalate or turn into a broader Middle-East conflict didn’t materialize. The latter doesn’t prevent a stock sell-off with European indices currently down another 0.5%. US indices open up to 1.0% lower (Nasdaq) with stock market shell-shocked by the new bond sell-off. Finally, it’s worth nothing that US inflation expectations are testing the upper bound of this year’s sideways trading range between 2.1% and 2.5%. Since Fed talk shifted towards skipping the November rate hike (because of higher LT bond yields tightening financial conditions), we’ve seen US inflation expectations adding around 15 bps. That’s because US eco data continue to point to a (very) tight labour market in combination with a soft landing scenario. If the Fed holds rates while inflation remains to high and growth stronger than expected than it will translate into… higher inflation expectations at the long end of the curve. Once again highlighting the Catch-22 of the US central bank. It’s a materialization of the Fed’s own prophecy: “the risk/economic cost of stopping the tightening cycle too fast is way bigger than conducting a rate hike too much”. The trade-weighted dollar remains somewhat numbed by current market conditions (risk aversion, higher volatility and rising real rates vs credit risk and inflation expectations). DXY holds steady just above the 106-level while EUR/USD switches sides around 1.06 (currently 1.0610). USD/JPY briefly surpassed the 150-level this morning, with lives to fight another day (149.90). Last week’s technical break above EUR/GBP 0.87 stands for now (0.8715).

The Belgian debt agency today tapped OLO 86 (€0.52bn 1.25% Apr2033), OLO 97 (€1.23bn 3% Jun2033) and OLO 98 (€1.08bn 3.3% Jun2054). The combined amount sold (€2.83bn) was near the upper bound of the indicative €2.6-2.9bn target range. The total auction bid cover was rather low at 1.32. The richening of OLO’s following the debt agency’s bumper €22bn retail note earlier September is a probable cause. The debt agency now raised a total amount of €43.03bn in OLO funding this year (€16bn syndications), exceeding the official target of €42.1bn. News & Views

Not a day goes by lately or rumours about the Bank of Japan readying possible tweaks to its ultra-easy policy hit the news wires. Reuters today citing three sources familiar with the matter reported the possibility the BoJ could change its yield curve programme at the October 31 policy meeting. Much depends on how the market moves leading up to that date, they said. Japanese yields have risen sharply in lockstep with rates in other advanced economies including the US. The 10-y yield today rallies further north to a new 16-year high of 0.877%, closing in on the current de facto 1% yield cap. While there’s no consensus currently to raise this cap immediately (i.e. at the October meeting), doing so would take off pressure on the BoJ to ramp up bond buying in an already thin market. But some in the committee fear such action would be seen as the central bank plotting an exit strategy at a time when they consider ultra-easy policy still necessary. The BoJ’s steadfast approach has come with a great cost for the yen. USD/JPY briefly rose above the critical level of 150 in Asian dealings this morning.

Germany’s Bundesbank in its monthly report said that the economy probably contracted “somewhat” in the third quarter this year. The central bank referred to declining industrial production, a shrinking construction sector and weakening demand (including externally). The Bundesbank noted ongoing strong employment and wage increases serve as a buffer for the economy amid an extended period of flat or negative growth (four consecutive quarters if the Q3 projection materializes). That said, the jobless rate could tick up slowly towards the end of the year. It expects inflation to ease further in coming months though core inflation may remain above 4% amid sticky service sector price pressures.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.68; (P) 149.83; (R1) 150.01; More...

Intraday bias in USD/JPY remains neutral for the moment. Consolidation pattern from 150.15 could extend further. On the downside, below 148.94 minor support will turn bias to the downside for another down leg towards 147.28. On the upside, firm break of 150.15 will resume larger up trend to test 151.93 high.

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by sustained break of 145.06 resistance turned support will be the first sign that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.